Portfolio Management & CAPM - CA Sri Lanka

15

Portfolio Management & CAPM CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS & FINANCE SEMESTER 3: Financial Strategy M B G Wimalarathna (ACA, ACMA, ACIM, SAT, ACPM)(MBA–USJ/PIM)

Transcript of Portfolio Management & CAPM - CA Sri Lanka

Portfolio Management & CAPM

CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS & FINANCE SEMESTER 3: Financial Strategy

M B G Wimalarathna

(ACA, ACMA, ACIM, SAT, ACPM)(MBA–USJ/PIM)

Introduction

Portfolio Management refers managing a pool of investments for the given period of time. Pool of investments refers collection of different types of investments which ultimately represents the holding/ownership of the investor.

Factors such as globalization and liberalization of capital market activities creates many investment opportunities (sources of investments) locally and globally. Investors can be categorized as individuals/group of people and institutions.

Factors affecting choice of investments; Security Liquidity Return Risks (spreading risks) Growth prospects Attitude of the investor

Portfolio Risk and Return

In general, risk can be identified as a variability (of expectations)due to uncertainty. Hence, portfolio risk is also a variation of expected return on investment (portfolio) as opposed to actual return. Actual return will not same as expected due to many reasons. But, rational investor attempts to minimise such gap of variations. Gap represents the risk.

Return on portfolio is the weighted average return received from respective investments in the portfolio. This usually will be calculated by weighting the different returns as opposed total investment in each category. Even though, it is quite qualitative in nature, portfolio risk and return will be calculated based on mathematical approach. Return will be average of total returns while risk will be denoted/measured through standard deviation.

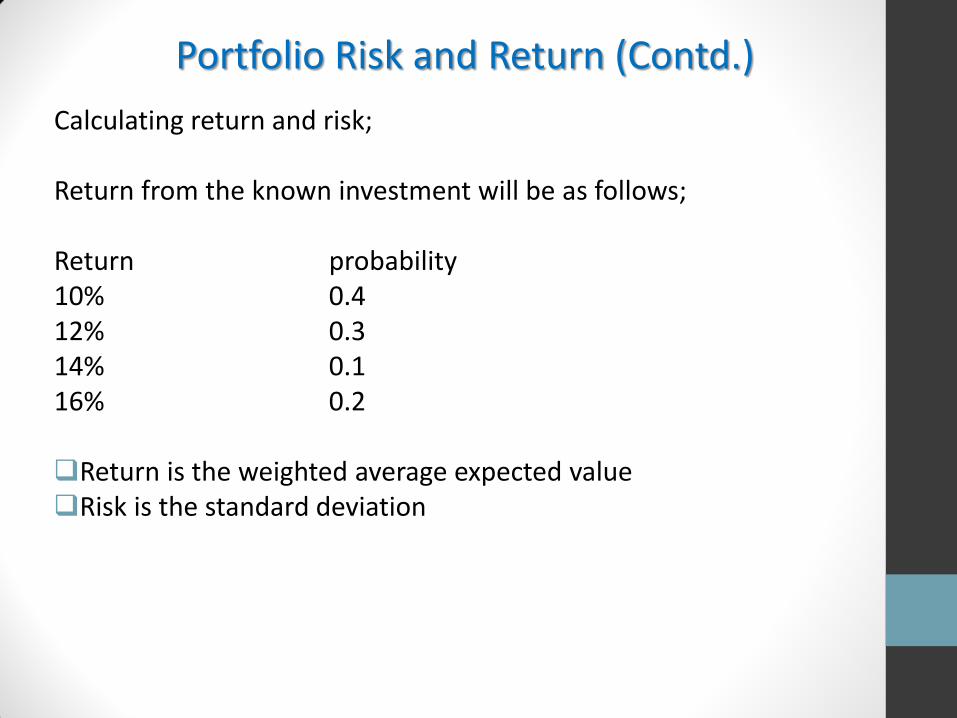

Portfolio Risk and Return (Contd.)

Calculating return and risk; Return from the known investment will be as follows; Return probability 10% 0.4 12% 0.3 14% 0.1 16% 0.2 Return is the weighted average expected value Risk is the standard deviation

Portfolio Risk and Return (Contd.)

Based on portfolio theory, a rational investor might attempt to reduce overall risk of investment by spreading the risks between each other. This usually called: diversification.

Diversification theory leads following three types of relationships between investments;

Positive Correlation : positive correlation effects when invest in shares of the companies having similar pattern of business. Both investments take similar direction. Umbrella and Raincoats business.

Negative Correlation : invest in shares of the companies having complete different pattern of business leads to negative correlation. Two types of investments take opposite direction. Umbrella and Ice-cream business.

No Correlation : when different investments do not denote pattern of relationship, it can be treated as no correlation situation. Telecommunication and Plantation.

Portfolio Theory and Financial Management

In most aspects of financial management, main focus is to enhance the shareholders’ wealth. Portfolio theory attempts to minimize the risks of investments through diversifications. Remember, minimizing risks does not count maximize the return. Hence, reasonable question arise whether company should more work towards diversification or refrain from diversification. Why company should refrain from diversification strategy; Company can get maximum from its employees when deployed

them with the work for which they have enormous level of skills and experience rather than deployed with the work new to them. You still can argue that staff can get training and/or recruit new staff with skills. But, all those claim costs and take time.

Portfolio Theory and Financial Management (Contd.)

Company can post growth momentum of revenue in the business that they are in for many years rather than in new business. With minimum effort, company can seek avenues for increase revenue and profit since it clearly demarcate the dimensions of business activities.

Since shareholders themselves can minimize risk being invest in

different sources, it is not expected from company to diversify the business and minimize the risks accordingly. Shareholders might willing to see company undertake (even) high risk projects which gives high level of return.

There is a high tendency of being takeover the individual businesses

due to the fact that when businesses are valued independently, those carry low level of EPS/PER.

Above factors do not necessarily alarm companies refrain from diversifications. But care is must when company planning to diversify into completely different types businesses.

Capital Asset Pricing Model (CAPM)

Capital Asset Pricing Model (CAPM)is an alternative to the dividend valuation model to determined the cost of equity capital. In CAPM, cost of company’s equity will be determined by considering both business and financial risk.

CAPM theory usually includes following propositions;

Investors who make an investment in shares require return in excess of risk free rate of return in order to compensate the systematic risk involved with the shares.

Investors do not expect premium for unsystematic risk since they can manage such risk by investing in portfolios.

Systematic risk varies depend on the nature of the company (shares) and as such investors expect high return when high systematic risk exist.

These will apply same for the companies invest in projects.

CAPM – Systematic & Unsystematic Risk

Systematic risk is the risk inherited with nature of the source of investment (shares) which is unavoidable. Hence, systematic risk must be accepted by any investor unless make an investment in risk-free source.

Risk which could manage through diversification is treated as unsystematic risk. Hence, unsystematic risk is not inherited which is avoidable.

When an investor wants to avoid risk in full, he/she should invest in risk-free sources of investments.

When investor having pool of investments in few companies shares, he/she experiences systematic risk as well as certain level of unsystematic risk.

When investor having well balanced pool of investments in companies shares, he/she experiences systematic risk and might avoid unsystematic risk.

Systematic Risk & CAPM

Taking all the shares in a stock market together, the total expected return from the market will vary due to systematic risk. CAPM developed with the aim of evaluating investment made in shares (stock market) rather than in projects.

Hence, it can clearly build the argument: CAPM is only considers systematic risk and such systematic risk

affects required return and share prices all the time. Systematic risk measured through beta factor.

A major assumption in CAPM is that there is linear relationship between the return recognize from individual shares and the average return recognize from all shares in the market.

CAPM – Beta Factor

In finance, the Beta (β) of a stock or portfolio is a number which describes the correlated volatility of an asset in relation to the volatility of the benchmark that asset being attached and compared to. This benchmark is generally the overall financial market and is often estimated via the use of representative indices such as ASPI. Hence, β essentially measures the changes in return between overall market (shares) as opposed to individual selected shares/pool of shares. For example; assume that return on shares of ABC Ltd tend to vary twice as much as returns from the market as a whole. Hence, when market returns increase by 4%, return of ABC shares expected to be increase by 8% and vice versa. Accordingly, the beta factor of ABC Ltd shares will be 2 (times).

CAPM – Beta Factor (Contd.)

Beta measures the part of the asset's statistical variance that cannot

be removed by the diversification provided by the portfolio of many

risky assets which cannot be net off the risk involved in one share

with another share. Beta can be estimated for individual companies

using regression analysis against a stock market index.

It is an basic principle in CAPM that unsystematic risk can be

cancelled out by diversification. Hence, risks of individual shares will

be cancelled within each other. But beta indicates specific

unsystematic risk which unable to cancelled automatically.

CAPM formula; Re = Rf + [Rm – Rf] β Re – expected return of share/cost of equity Rf – risk free rate of return Rm – return from the market as a whole β – beta factor

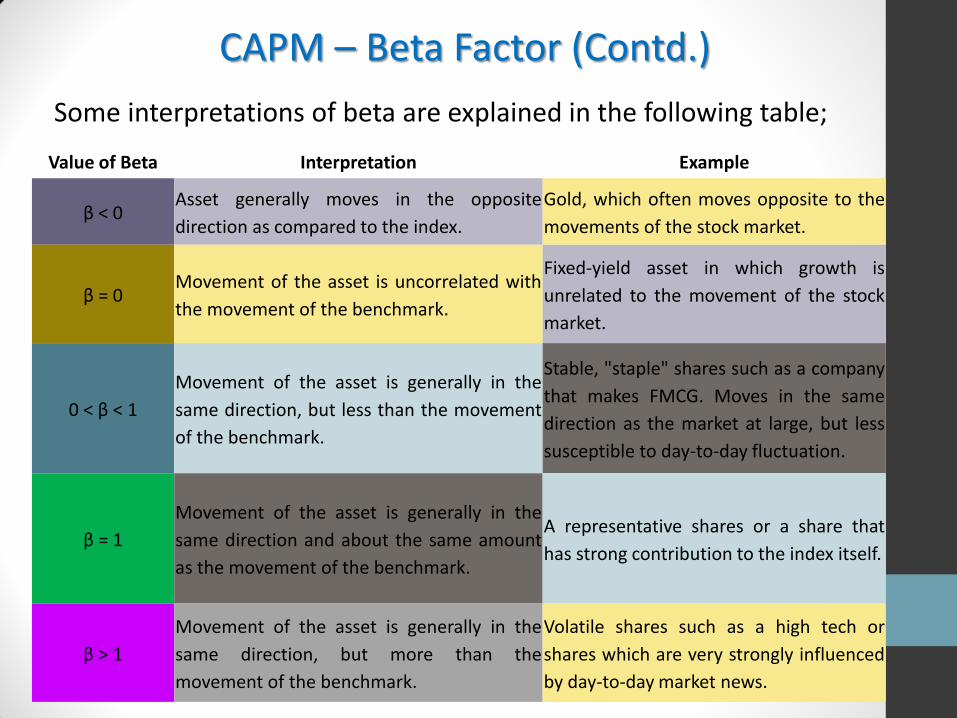

CAPM – Beta Factor (Contd.)

Some interpretations of beta are explained in the following table;

Value of Beta Interpretation Example

β < 0 Asset generally moves in the opposite

direction as compared to the index.

Gold, which often moves opposite to the

movements of the stock market.

β = 0 Movement of the asset is uncorrelated with

the movement of the benchmark.

Fixed-yield asset in which growth is

unrelated to the movement of the stock

market.

0 < β < 1

Movement of the asset is generally in the

same direction, but less than the movement

of the benchmark.

Stable, "staple" shares such as a company

that makes FMCG. Moves in the same

direction as the market at large, but less

susceptible to day-to-day fluctuation.

β = 1

Movement of the asset is generally in the

same direction and about the same amount

as the movement of the benchmark.

A representative shares or a share that

has strong contribution to the index itself.

β > 1

Movement of the asset is generally in the

same direction, but more than the

movement of the benchmark.

Volatile shares such as a high tech or

shares which are very strongly influenced

by day-to-day market news.

Portfolio Management and CAPM It is well established that; Each share carries beta factor Pool of shares (portfolio) carries beta factor Market as a whole carries beta factor Hence, A portfolio which represents almost all the shares (except risk free

securities) in the overall market has same return as expected from the market and as such beta factor will be 1.

A portfolio which comprised all risk free securities will have beta

factor of 0.

Portfolio Management and CAPM (Contd.) Why CAPM cannot practice successfully; In CAPM, we used historical data to determine excess return

between return from market and risk free return where actually decision will be made in the future.

Even though we assumed that government securities carries no

risk, in practice there will be risk involvement based on the nature of the security to some extent which ultimately results vary in the return.

Calculating most suitable beta factor will be a tuff task in real word

circumstance.