Population Ageing, Government Budgets and the … Ageing, Government Budgets and the Baby Boomers...

30

Population Ageing, Government Budgets and the Baby Boomers Ann Harding Presentation to the Institute of Actuaries of Australia Conference on ‘The New Super Landscape’, Sydney, 30 November 2006 NATSEM, University of Canberra The research presented in this presentation was partly funded by ARC Grant No LP562493

Transcript of Population Ageing, Government Budgets and the … Ageing, Government Budgets and the Baby Boomers...

Population Ageing, Government

Budgets and the Baby Boomers

Ann Harding Presentation to the

Institute of Actuaries of Australia Conference on ‘The

New Super Landscape’, Sydney, 30 November 2006

NATSEM, University of Canberra

The research presented in this presentation was partly funded by ARC Grant No LP562493

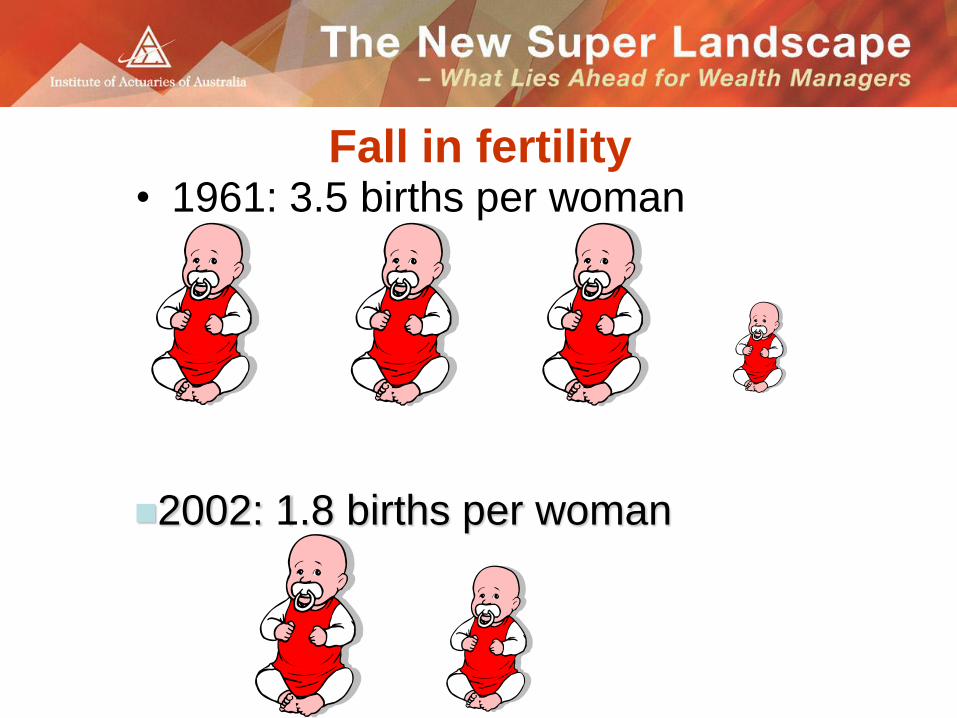

Fall in fertility • 1961: 3.5 births per woman

2002: 1.8 births per woman

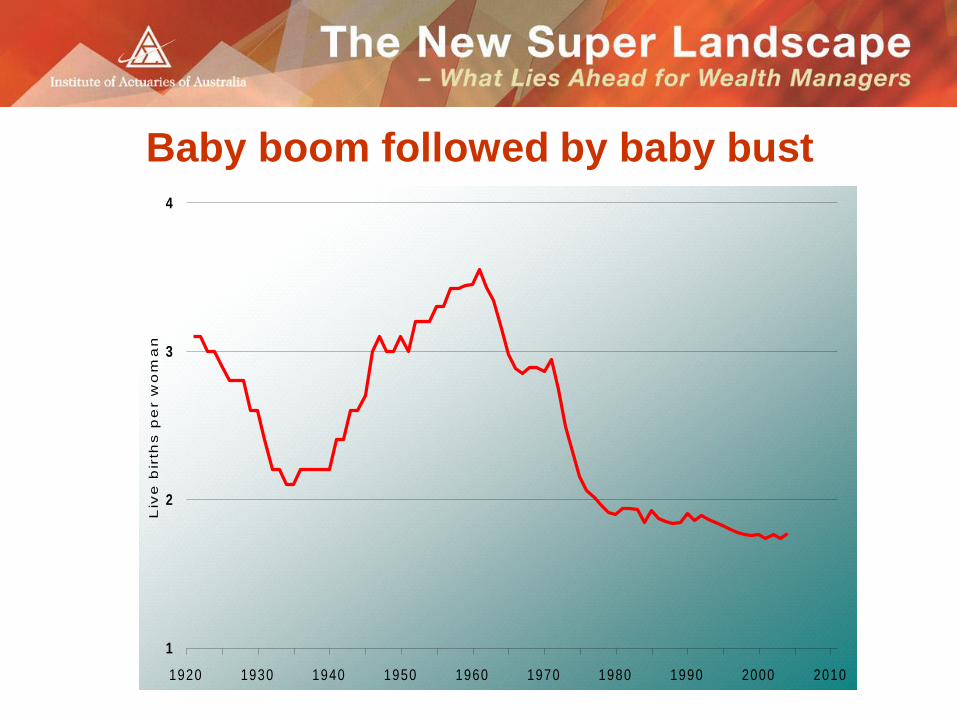

Baby boom followed by baby bust

1

2

3

4

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Liv

e b

irth

s p

er w

om

an

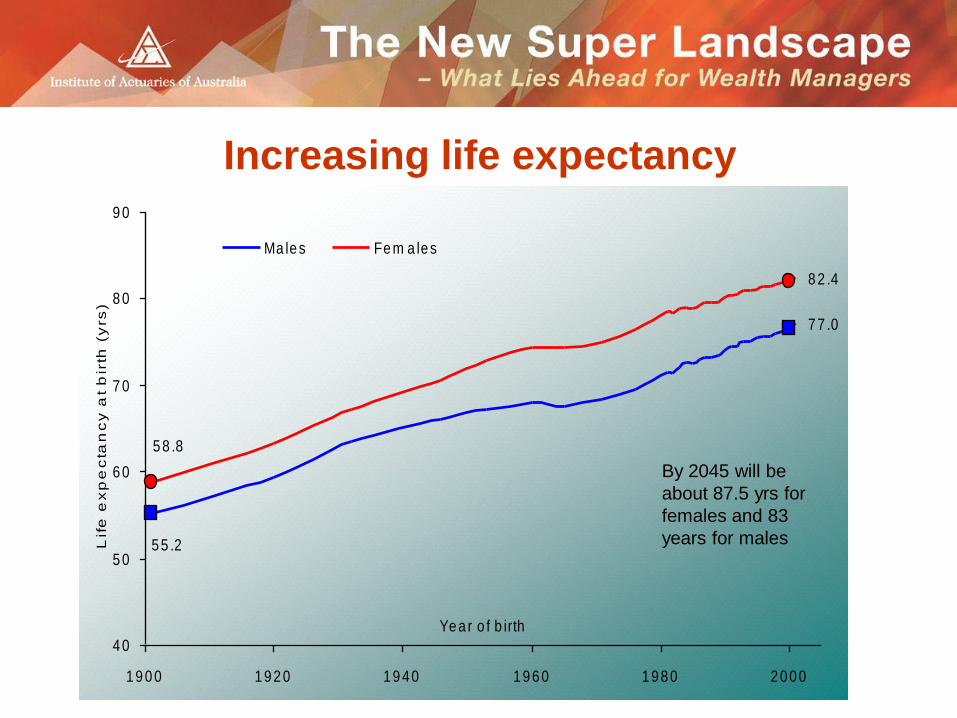

Increasing life expectancy

5 5 .2

7 7 .0

5 8 .8

8 2 .4

4 0

5 0

6 0

7 0

8 0

9 0

1 9 0 0 1 9 2 0 1 9 4 0 1 9 6 0 1 9 8 0 2 0 0 0

Ye a r o f b irth

Lif

e e

xp

ec

tan

cy

at

bir

th (

yrs

)

Ma le s Fe m a le s

By 2045 will be

about 87.5 yrs for

females and 83

years for males

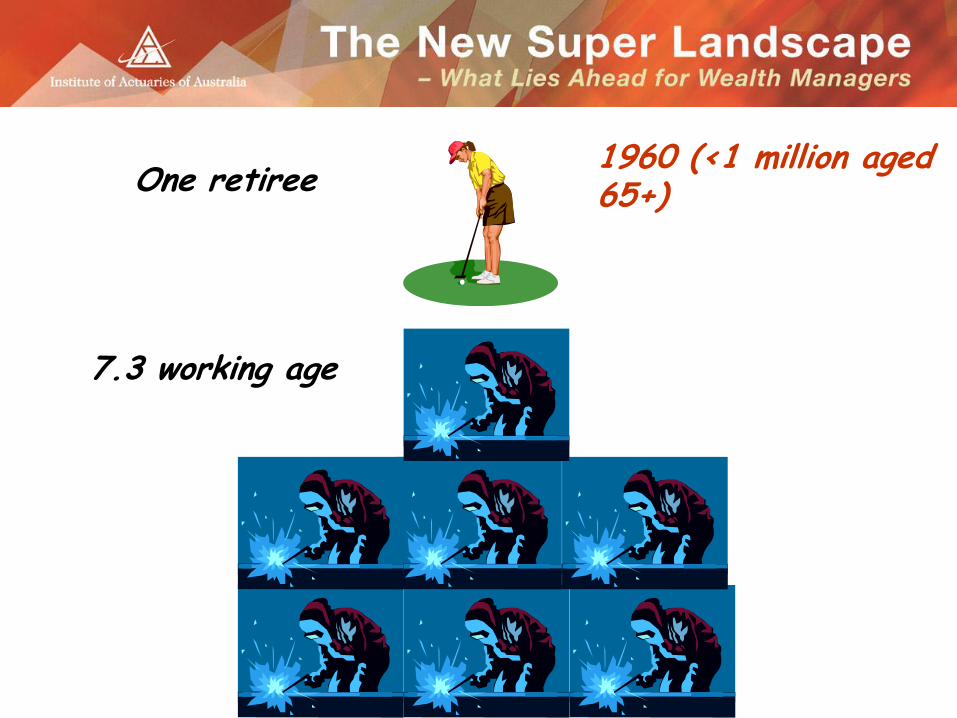

One retiree 1960 (<1 million aged 65+)

7.3 working age

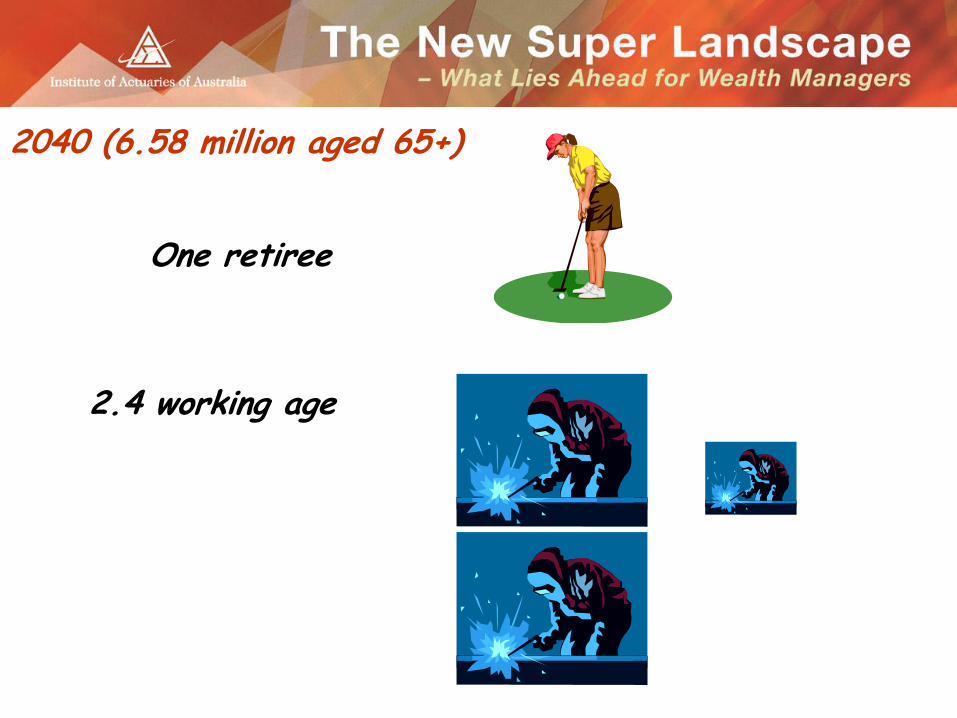

One retiree

2040 (6.58 million aged 65+)

2.4 working age

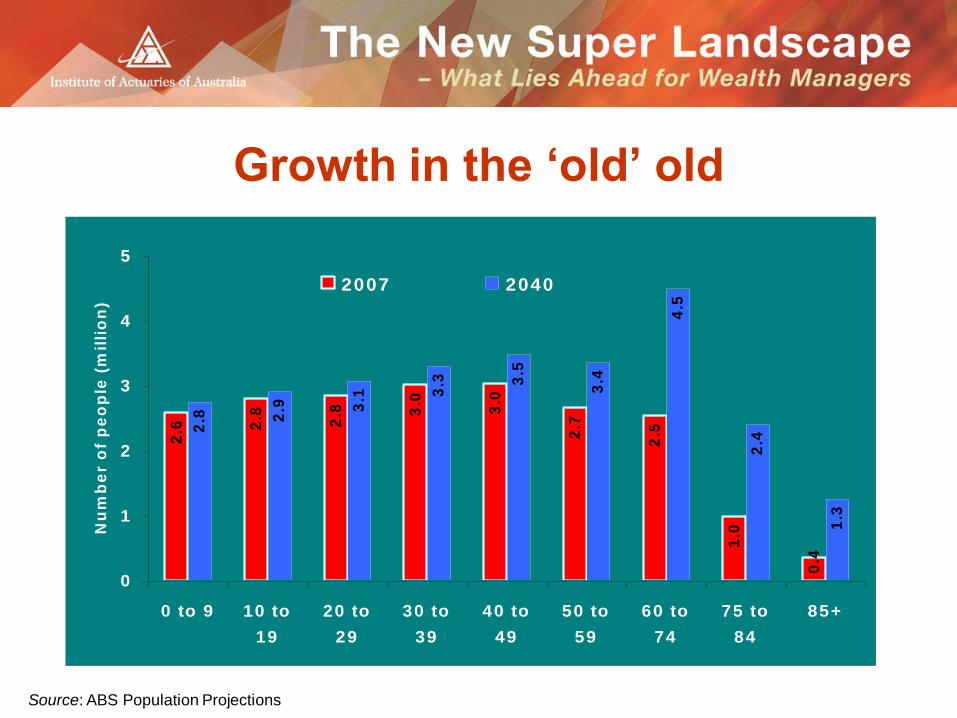

Growth in the ‘old’ old 2

.6 2.8 2.8 3

.0

3.0

2.7

2.5

1.0

0.4

2.8 2

.9 3.1 3

.3 3.5

3.4

4.5

2.4

1.3

0

1

2

3

4

5

0 to 9 10 to

19

20 to

29

30 to

39

40 to

49

50 to

59

60 to

74

75 to

84

85+

Nu

mb

er

of

pe

op

le (

mil

lio

n)

2007 2040

Source: ABS Population Projections

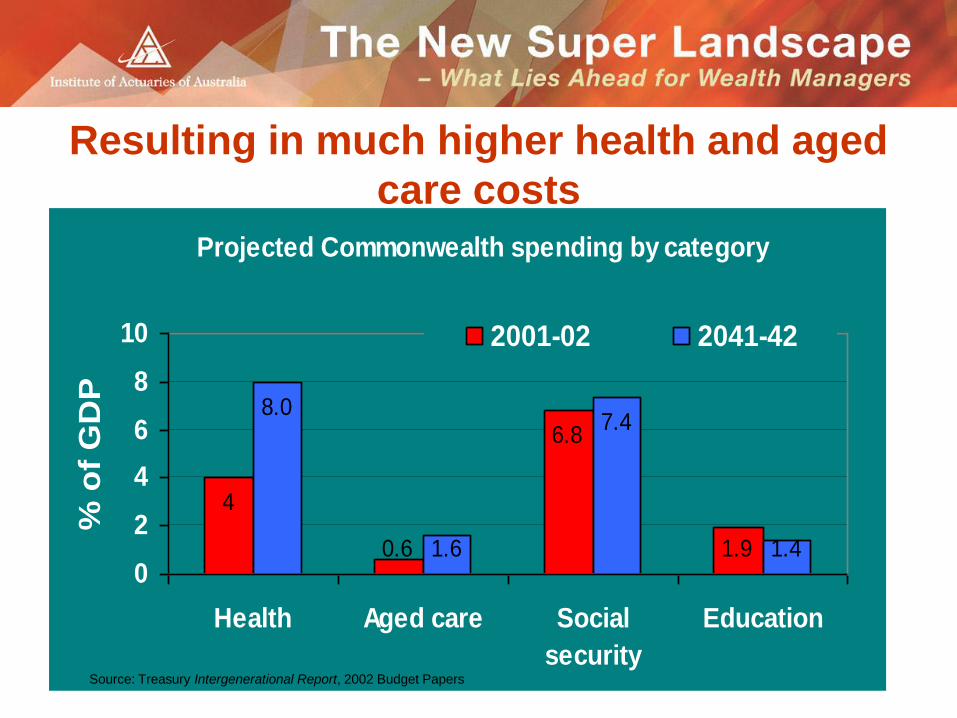

Resulting in much higher health and aged

care costs

Projected Commonwealth spending by category

4

0.6

6.8

1.9

8.0

1.6

7.4

1.40

2

4

6

8

10

Health Aged care Social

security

Education

% o

f G

DP

2001-02 2041-42

Source: Treasury Intergenerational Report, 2002 Budget Papers

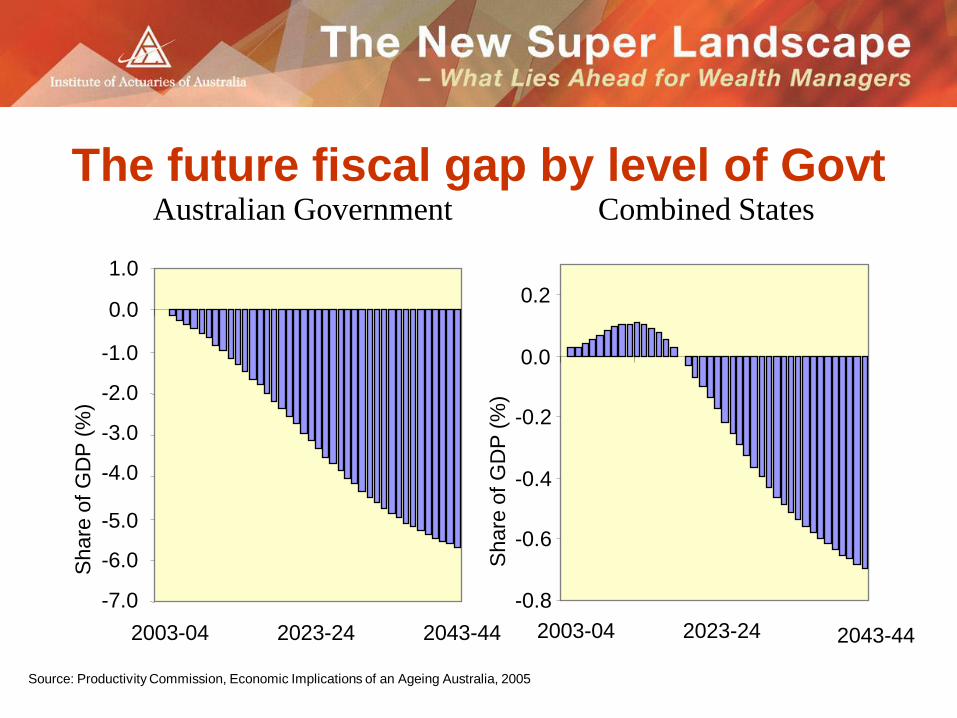

The future fiscal gap by level of Govt Australian Government Combined States

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2003-04 2023-24 2043-44

Share

of

GD

P (

%)

-0.8

-0.6

-0.4

-0.2

0.0

0.2

2003-04 2023-24 2043-44

Share

of

GD

P (

%)

Source: Productivity Commission, Economic Implications of an Ageing Australia, 2005

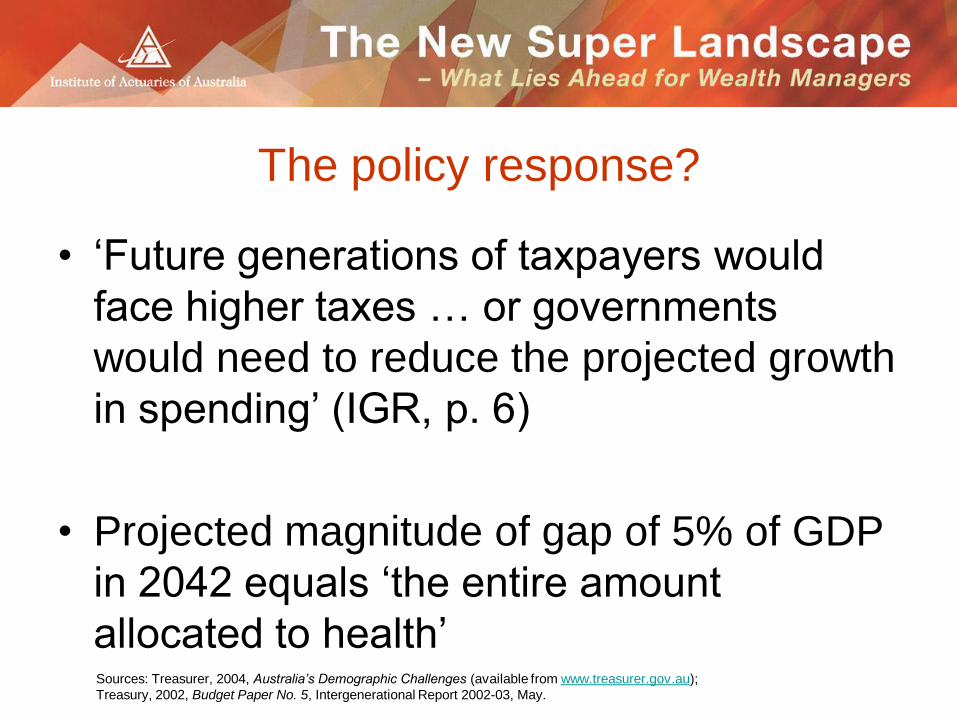

The policy response?

• ‘Future generations of taxpayers would

face higher taxes … or governments

would need to reduce the projected growth

in spending’ (IGR, p. 6)

• Projected magnitude of gap of 5% of GDP

in 2042 equals ‘the entire amount

allocated to health’ Sources: Treasurer, 2004, Australia’s Demographic Challenges (available from www.treasurer.gov.au);

Treasury, 2002, Budget Paper No. 5, Intergenerational Report 2002-03, May.

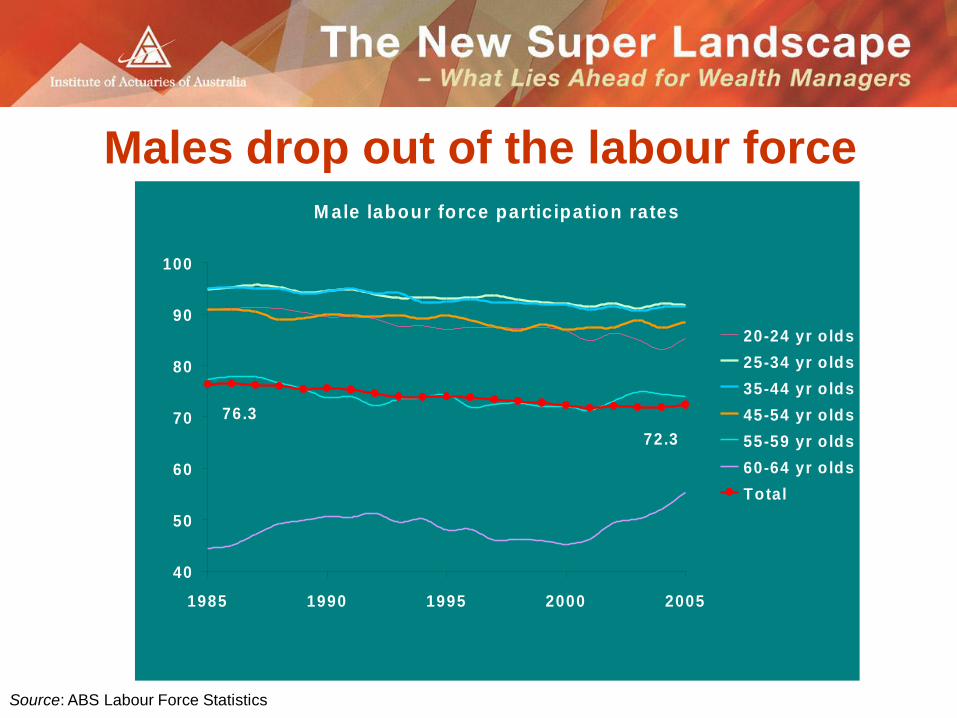

The ageing population and future

labour supply

Males drop out of the labour force

Source: ABS Labour Force Statistics

M ale labour force participation rates

40

50

60

70

80

90

100

1985 1990 1995 2000 2005

20-24 yr o lds

25-34 yr o lds

35-44 yr o lds

45-54 yr o lds

55-59 yr o lds

60-64 yr o lds

Total

72.3

76.3

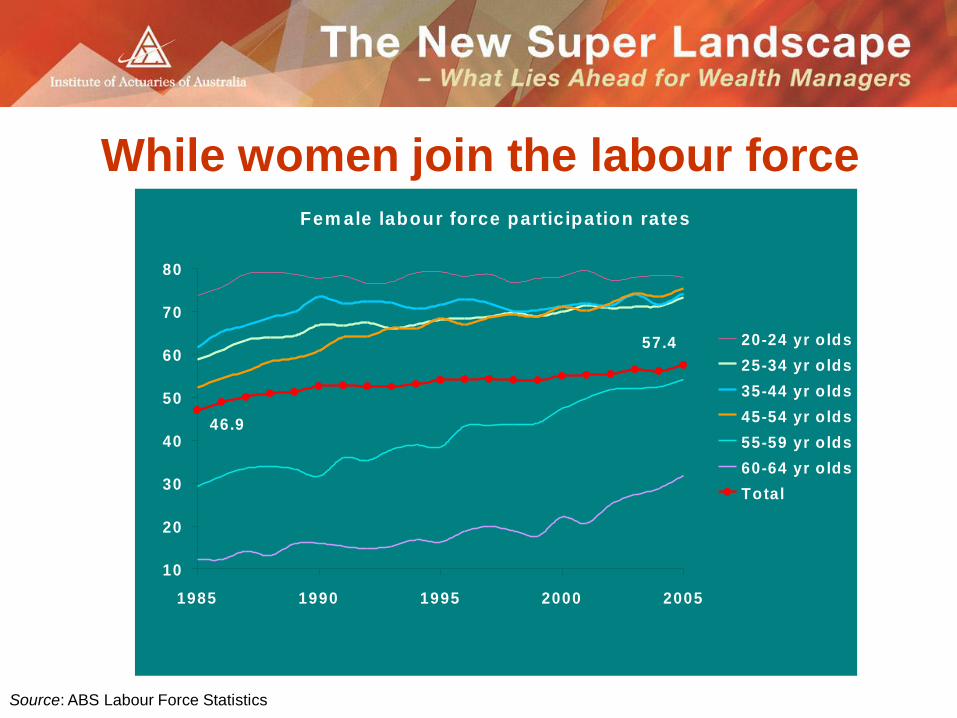

While women join the labour force

Source: ABS Labour Force Statistics

Fem ale labour force participation rates

10

20

30

40

50

60

70

80

1985 1990 1995 2000 2005

20-24 yr o lds

25-34 yr o lds

35-44 yr o lds

45-54 yr o lds

55-59 yr o lds

60-64 yr o lds

Total

46.9

57.4

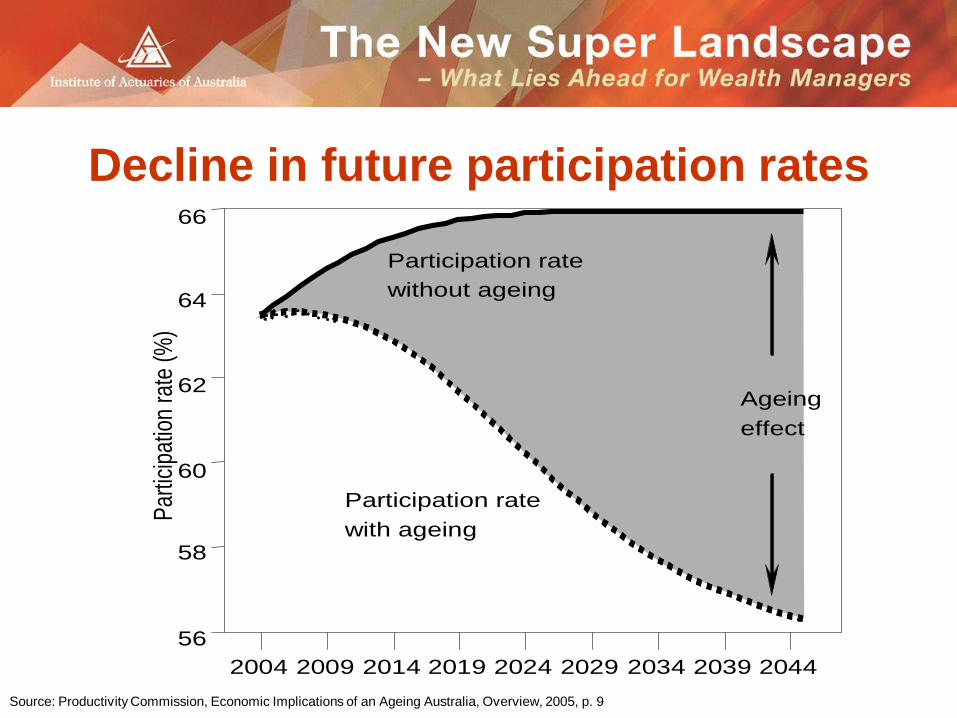

Decline in future participation rates P

artic

ipat

ion

rate

(%

)

2004 2009 2014 2019 2024 2029 2034 2039 2044

56

58

60

62

64

66

Participation rate

with ageing

Participation rate

without ageing

Ageing

effect

Source: Productivity Commission, Economic Implications of an Ageing Australia, Overview, 2005, p. 9

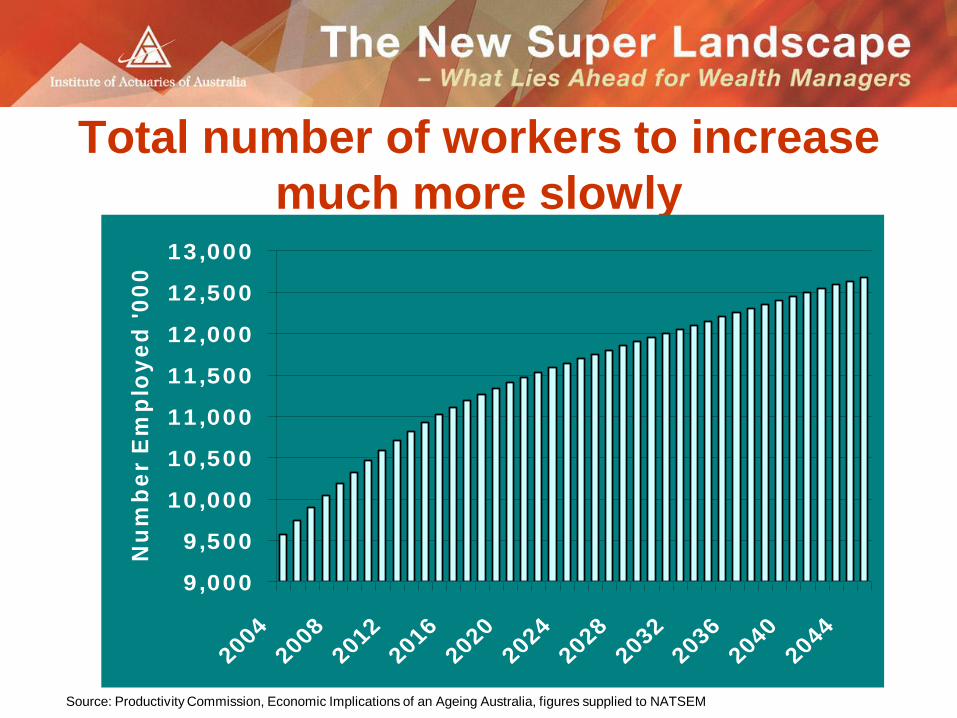

Total number of workers to increase

much more slowly

Source: Productivity Commission, Economic Implications of an Ageing Australia, figures supplied to NATSEM

9,000

9,500

10,000

10,500

11,000

11,500

12,000

12,500

13,000

2004

2008

2012

2016

2020

2024

2028

2032

2036

2040

2044

Nu

mb

er

Em

plo

ye

d '

00

0

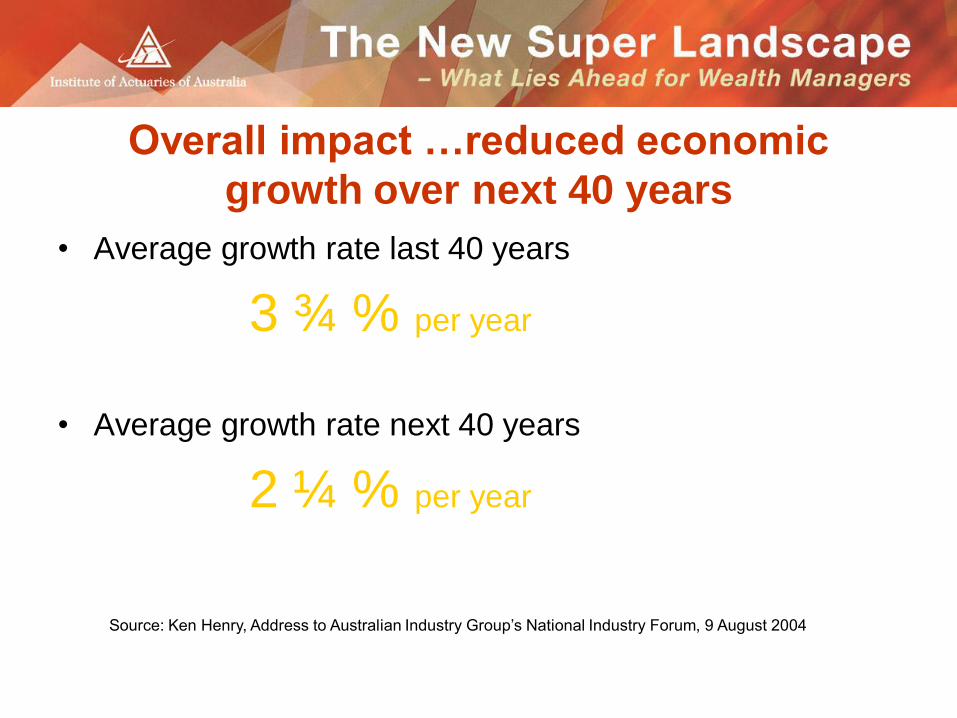

Overall impact …reduced economic

growth over next 40 years

• Average growth rate last 40 years

3 ¾ % per year

• Average growth rate next 40 years

2 ¼ % per year

Source: Ken Henry, Address to Australian Industry Group’s National Industry Forum, 9 August 2004

A comfortable retirement for the

boomers?

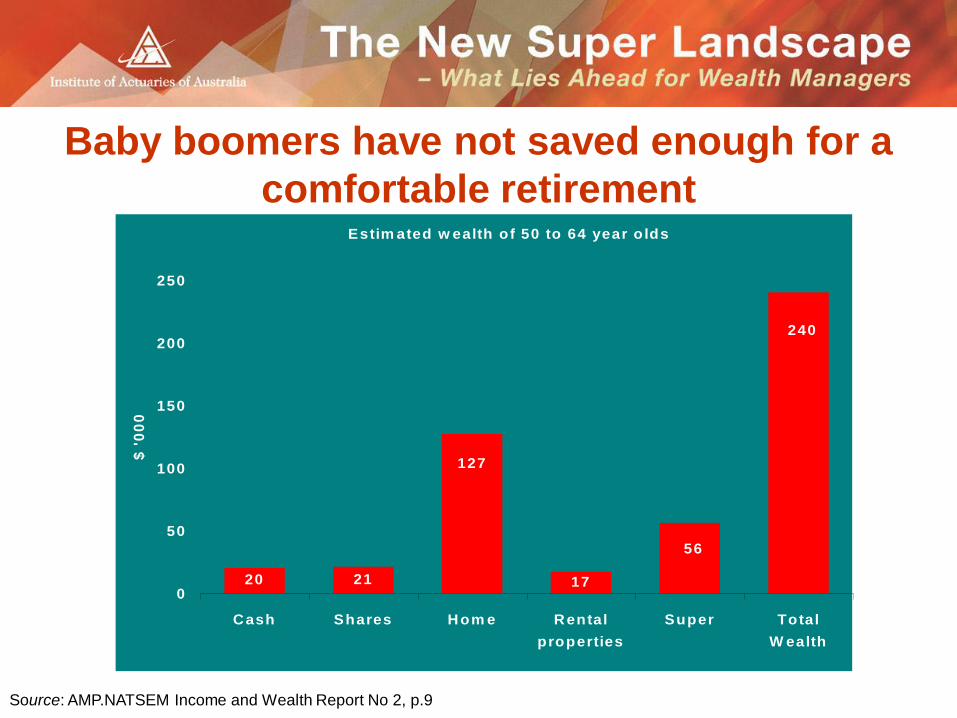

Baby boomers have not saved enough for a

comfortable retirement

Source: AMP.NATSEM Income and Wealth Report No 2, p.9

Estim ated w ealth of 50 to 64 year o lds

2120

240

127

56

170

50

100

150

200

250

Cash Shares Hom e Rental

properties

Super Total

W ealth

$ '

00

0

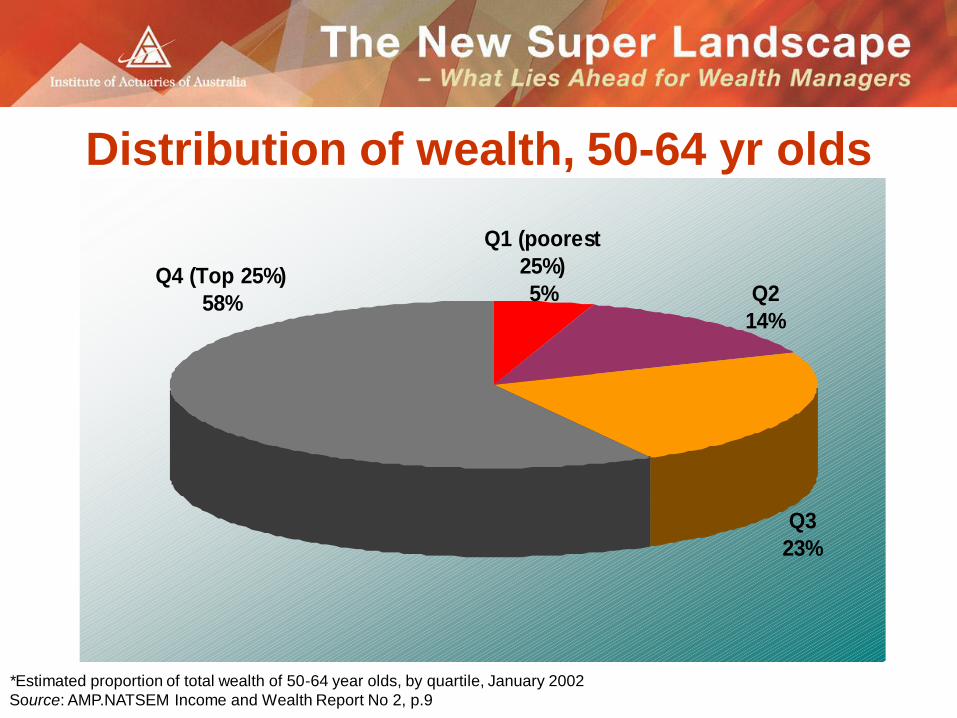

Distribution of wealth, 50-64 yr olds

Q2

14%

Q1 (poorest

25%)

5%

Q3

23%

Q4 (Top 25%)

58%

*Estimated proportion of total wealth of 50-64 year olds, by quartile, January 2002

Source: AMP.NATSEM Income and Wealth Report No 2, p.9

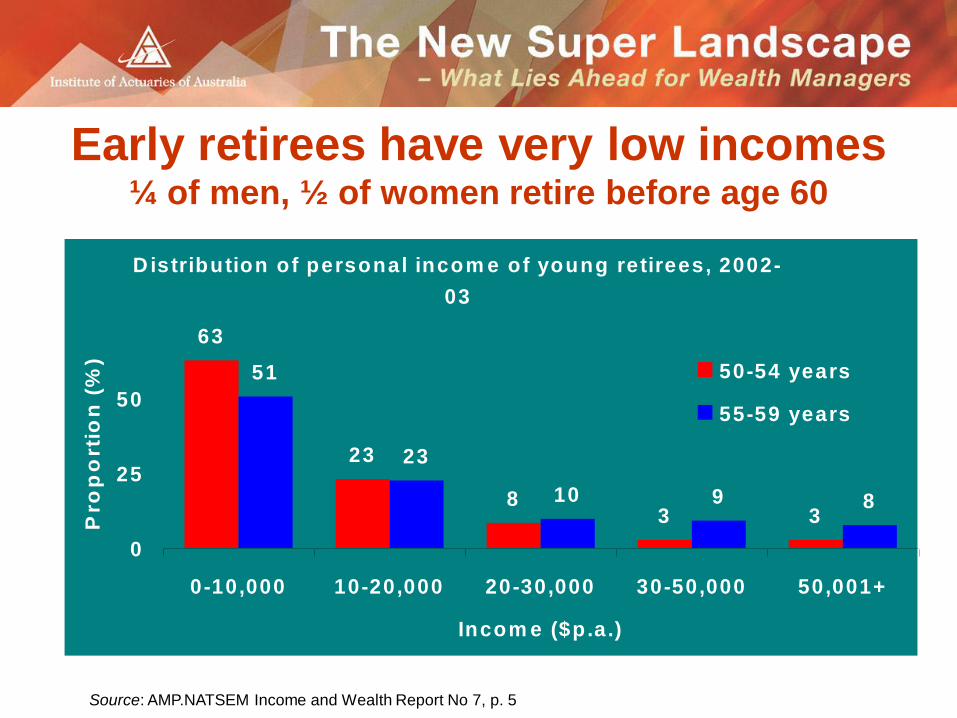

Early retirees have very low incomes ¼ of men, ½ of women retire before age 60

Source: AMP.NATSEM Income and Wealth Report No 7, p. 5

Distribution of personal incom e of young retirees, 2002-

03

63

23

83 3

51

23

10 9 8

0

25

50

0-10,000 10-20,000 20-30,000 30-50,000 50,001+

Incom e ($p.a.)

Pro

po

rtio

n (

%)

50-54 years

55-59 years

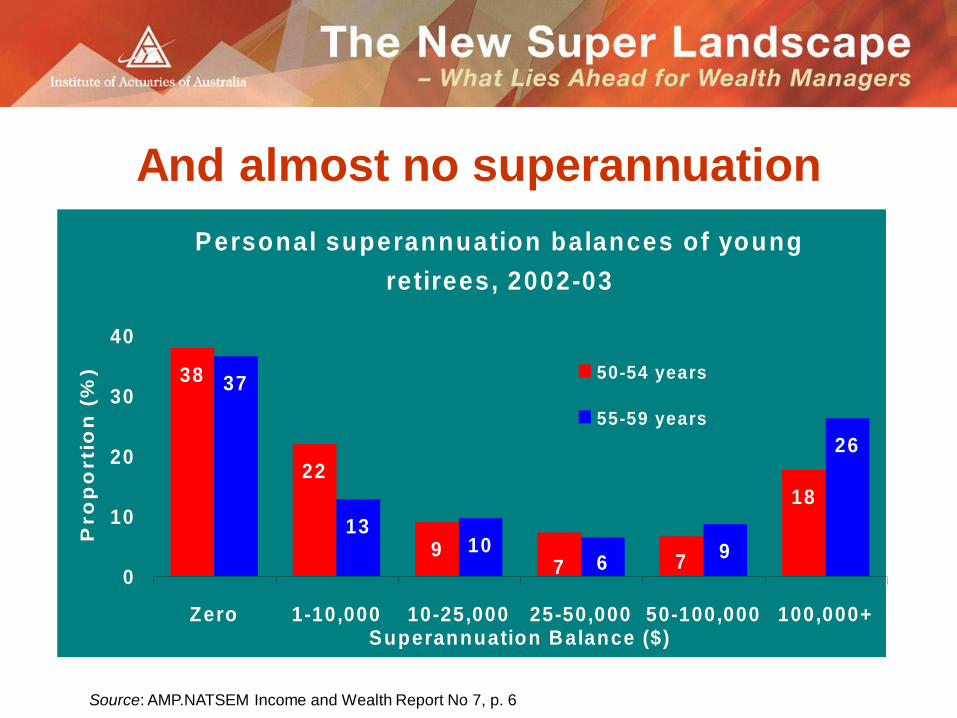

And almost no superannuation

Source: AMP.NATSEM Income and Wealth Report No 7, p. 6

Personal superannuation balances of young

retirees, 2002-03

38

22

9

18

37

1310 9

26

77 60

10

20

30

40

Zero 1-10,000 10-25,000 25-50,000 50-100,000 100,000+Superannuation Balance ($)

Pro

po

rti

on

(%

) 50-54 years

55-59 years

Treasurer’s view

“As our retirement income system matures, is

it fair to allow those with superannuation

assets to retire early, run down their assets and

then rely on taxpayers to fund the major part

of their retirement? This is an important issue

that we will need to consider very carefully.”

Costello, 2004

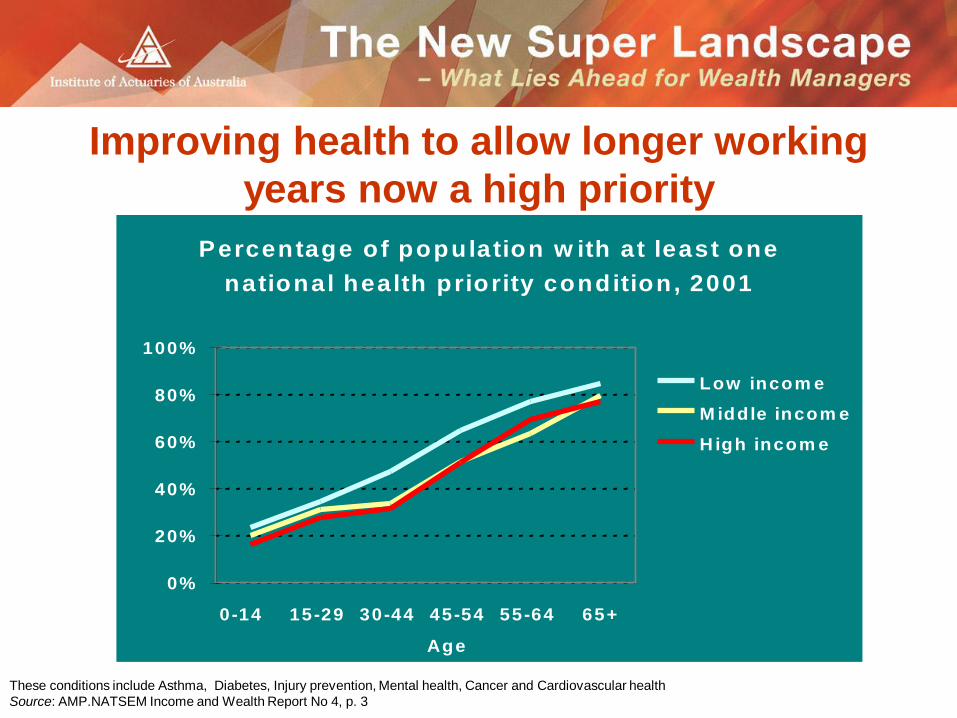

Improving health to allow longer working

years now a high priority

Percentage of population w ith at least one

national health priority condition, 2001

0%

20%

40%

60%

80%

100%

0-14 15-29 30-44 45-54 55-64 65+

Age

Low incom e

M iddle incom e

H igh incom e

These conditions include Asthma, Diabetes, Injury prevention, Mental health, Cancer and Cardiovascular health

Source: AMP.NATSEM Income and Wealth Report No 4, p. 3

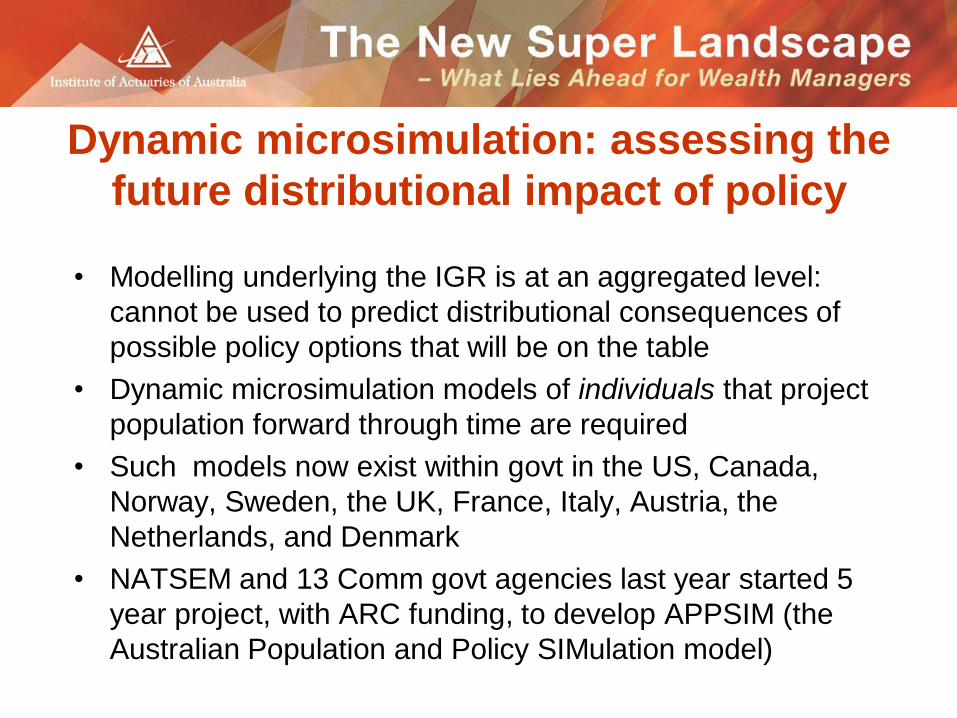

Projecting the future

Dynamic microsimulation: assessing the

future distributional impact of policy

• Modelling underlying the IGR is at an aggregated level:

cannot be used to predict distributional consequences of

possible policy options that will be on the table

• Dynamic microsimulation models of individuals that project

population forward through time are required

• Such models now exist within govt in the US, Canada,

Norway, Sweden, the UK, France, Italy, Austria, the

Netherlands, and Denmark

• NATSEM and 13 Comm govt agencies last year started 5

year project, with ARC funding, to develop APPSIM (the

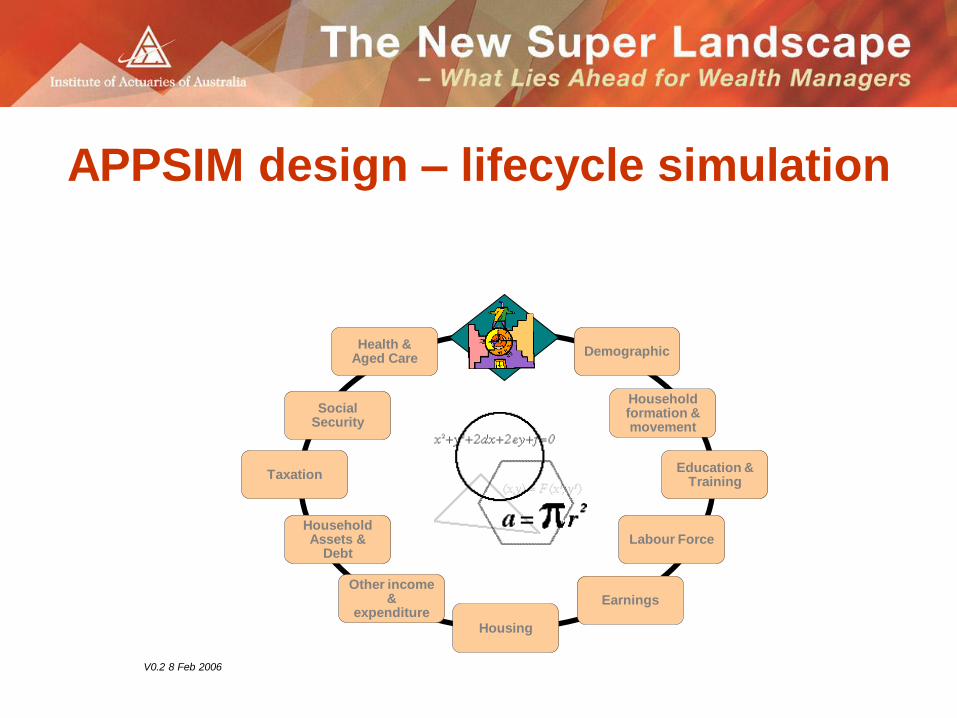

Australian Population and Policy SIMulation model)

Labour Force Household Assets &

Debt

Earnings

Taxation

Social Security

Education & Training

Household formation & movement

Demographic Health &

Aged Care

Other income &

expenditure Housing

New Year

?

V0.2 8 Feb 2006

APPSIM design – lifecycle simulation

Developing modelling infrastructure to

look at equity issues associated with

population ageing

• Who will pay the increased taxes predicted in the IGR?

• Who will pay more for their pharmaceuticals, medical services, education, child care, or aged care?

• What will be the impact between the different generations?

• Modelling to help ensure that we cope with the impacts of population ageing in the fairest and most efficient way

Policy responses to population ageing

• Treasury’s 3P’s - population, participation, and

productivity

– Govt focussing on welfare, workplace and labour

market reform

– Reforming super’n; encouraging business to look at

older/disdavantaged employees; chronic diseases

and LFP

– Immigration very partial solution

• Age pension reforms

– Impose an upper limit on exemption of home from the

pension means test

– Raise age at which get pension beyond 65 yrs

Conclusions • Effective labour supply growth to slow sharply in less

than 10 years time

– Lower labour force participation rates

– Reduced average hours

– Slower growth in worker numbers

• But about 1/4 of men and 1/2 of women retire before age 60

• Most 50-64 year olds have not saved enough for a financially comfortable retirement

• Many baby boomers will need to work longer and save harder if they want a comfortable retirement

• Economic growth to slow and fiscal pressures on govt to increase

Stay in touch with new research

NATSEM research freely available from

www.natsem.canberra.edu.au

To stay in touch via automatic email notification of new

research:

AMP:NATSEM reports freely available from

www.amp.com.au/ampnatsemreports