Polyethylene & PET Outlook - Blow Molding · PDF filePolyethylene & PET Outlook Howard...

46

Polyethylene & PET Outlook Howard Rappaport Senior Director, Chemicals IHS Global Insight – Price & Purchasing October, 2012 28th Annual Blow Molding Conference

Transcript of Polyethylene & PET Outlook - Blow Molding · PDF filePolyethylene & PET Outlook Howard...

Polyethylene & PETOutlook

Howard RappaportSenior Director, ChemicalsIHS Global Insight – Price & PurchasingOctober, 2012

28th Annual Blow Molding Conference

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

IHS – A leading information provider

We are over 5,600 people, in 40 countries, speaking 50 languages – all working each day to:

• Serve businesses and all levels of governments worldwide• Ranging from 80% of Global Fortune 500 to small businesses• Customers in 180 countries

• Provide comprehensive content, software and expert analysis and forecasts

Helping our customers drive critical processes and make high-impact decisions with speed and confidence

2

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

IHS Capabilities

3

• Bringing content and expertise in pivotal areas that shape today’s business landscape

Areas of Expertise & Content

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

IHS ChemicalIHS Chemical

CMAI + SRIC + HARRIMAN + CHEMICAL WEEK

IHS has brought together four strategic brands to create an unrivalled chemical industry offering...

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Transportation

Aerospace & Defense

Agriculture

Construction

Shipping

Electronics & Telecom

Government

Metals & Mining

Healthcare

Power & Utilities

Financial

Military & Security

EnergyOil & Gas

Consumer & Retail

IHS Chemical

Automotive

IHS Chemical

IHS Chemical Capabilities

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

The IHS Chemical Portfolio

News & Events

Chemical Week

Magazine

Chemicals Events

Daily News & Information

Services

Market Services

Aromatics & Fibers

Olefins & Derivatives

Chlor-Alkali & Vinyls

Plastics & Polymers

Methanol & Derivatives

Planning & Company Services

Chemical Economics Handbook

Specialty Chemicals

World Analysis

Directory of Chemical Producers

China Report

Special Studies

Technology Services

Process Economics Program

Carbon Footprint

Special Studies

Consulting Services

Strategy

Commercial Analysis

Transaction

Technology

Renewables

Legal Services

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Center of the industry has shifted to Asia

Economic Expansion: Basic demand to fast

growth emerging economies is evident

Investment Decisions:Two Options: Produce in

demand centers or leverage a clear cost

advantage

Tomorrow’s Market:Sustainability includes a systematic addition of performance products

0%10%20%30%40%50%60%70%80%90%

100%

1990 1995 2000 2005 2010 2015 2020

W. EuropeMiddle East

All Others

Other Asia

China

N. America

Basic Chemicals and PlasticsDistribution of Global Demand

Basic Chemicals & Plastics Demand Distribution is Shifting

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

NaturalGas

GasSeparation

Unit

RefineryCrudeOil

Reformer

Reformate BTXExtraction

SteamCracker

ButaneHydrogen

PropylenePygas

BTX

Raffinate

EthyleneEO/EG

POLYETHYLENE

ETHYLENE DICHLORIDE / PVC

EP RUBBER

ETHANOL

NaphthaGas Oil

EthanePropaneButane

TOLUENE

m-XYLENEp-XYLENE

BENZENE

o-XYLENE

XYLENES

PTA/DMT PET

PIA

PAN/DOP/Plasticizers

POLYPROPYLENE

Butadiene

MethanolSBR / PBR

ETHYLBENZENE/STYRENE

Crude Oil & Natural GasBuilding Blocks for the Industry

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0%

10%

20%

30%

40%

50%

60%

0

2

4

6

8

10

12

14

16

18

07 08 09 10 11 12 13 14 15 16 17 Crude (WTI) Natural Gas Gas as % of Crude

Dollars Per MMBtu Gas as a% of Crude, BTU Basis

North America Energy Price Trends

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0

2

4

6

8

10

0

40

80

120

160

200

07 08 09 10 11 12 13 14 15 16 17 Natural Gas Ethane Propane N-Butane

Gas Liquids, Cents Per Gallon Natural Gas, $/MMbtu

U.S. Natural Gas Liquids Price

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

U.S. AverageMDE Avg.

Alberta Ethane

U.S. EthaneMDE

Ethane

West Europe Avg.

NE Asia Avg.SE Asia Avg.

50

250

450

650

850

1050

1250

1450

1650

0 20 40 60 80 100 120 140 160

(Dollars per Ton)

CUMULATIVE ETHYLENE CAPACITY (million tons)

2012 Ethylene Cost Curve

WTI Crude $94/Barrel Nat Gas $3.16/MMBtuEthane 35.3 cpg

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

What Does Shale Gas Development Do?Increasing NGL supplies within North America

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2005 2010 2015 2020 2025 2030

Ethane

Propane

n-Butane

i-ButaneNatural Gasoline

Barrels Per Day

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

North American Feedslate Becoming Lighter

• Given its high selectivity to ethylene & relative cost position to other feeds, ethane is consistently the most favored feed

• Once oil & gas began to diverge, producers have been shifting feedslates lighter to capitalize on the advantage

13

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Monthly Ethylene ProductionBy Feedstock

Ethane Propane Butane Naphtha Gas Oil

Wt% ProducedFrom Feedstock

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 14

2012 U.S. Ethylene Production Losses (With Forecast)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecUnconfirmed Unplanned**'11 Cumulative Production Loss Forecast '13 Cumulative Production LossSeries4

* Includes both confirmed and unconfirmed outages **Forecast period assumes a forecast of unplanned outages

Million Pounds, Monthly Million Pounds, Cumulative

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

15•Dow, Shell, NOVA, and Oxy capacity additions shown are CMAI estimates

Announced (-000- MT) 2012 2013 2014 FutureBASF/Fina (Port Arthur) 180Chevron Phillips (Cedar Bayou) 1500Dow (Taft / Freeport) 386 1500*Equistar (All locations) 121 310 90Exxon (Baytown) 1500Formosa (Point Comfort) 800Ineos (Chocolate Bayou) 50 57Oxy (Ingleside) 550*Sasol (Lake Charles) 1400Shell (Northeast) 1000*Westlake (Lake Charles) 30 110 80Williams (Geismar) 20 70 210Nova (Sarnia) 250*Braskem/Idesa (Mexico) 1000Unidentified 145 110

Total 100 1069 600 9500Cumulative Total 100 1169 1769 11,269

* Dow, Shell, NOVA, and Oxy capacity additions shown are IHS estimates

Ethylene Market ViewNorth American Capacity Additions Leverage Ethane

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 16

Global Annual Feedstock Cash Margins

-200

0

200

400

600

800

1,000

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17U.S. Ethane U.S. Integrated Lt. NaphthaWEP Naphtha Discounted Price SEA NaphthaU.S. Weighted Average

Dollars Per Metric Ton

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Ethylene Market View Global Net Ethylene Capacity

Million Tons, Ethylene Capacity Growth (Bars) or Demand Growth (Line)

17

-8-6-4-202468

1012

2000 2002 2004 2006 2008 2010 2012 2014 2016Americas Europes/CIS/BalticsMiddle East/Africa AsiaChange in World Demand

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• Shale development has enabled the North American producer to become one of the lowest cost producers in the world

• Combined with the Middle East, over 40% of the global ethylene capacity is now cost advantaged

• Other cracking capacity likely to trend towards increased LPG consumption in order to try and remain competitive

• Higher cost countries may respond with protectionist measures

Ethylene Market ViewDevelopment of two low production cost regions

*

*

Polyethylene

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

%: 12-17 Average Annual Growth Rate

Domestic Demand by Region

0.0 10.0 20.0 30.0 40.0

ISC

SAM

SEA

AFR/MDE

NAM

EUR

NEA

20122017

Demand by Region, Million Metric Tons

2.7%

8.5%

5.0%

4.9%

6.2%

2.4%

6.0% 2012-2017 Average Annual

Growth Rate, Total Demand: 4.7%

20122017

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Capacity, Million Metric Tons0 5 10 15 20 25 30 35 40 45 50 55 60 65

2017

2012

2007

LDPE LLDPE HDPE

Global Production Capacity Growth

Total:77.8

Total:94.3

Total:120

AAGR 12-17LDPE = +17.8%

LLDPE = +34.2%HDPE = +27.4%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

%: 12-17 Average Annual Growth Rate

World Consumption by End Use

0.0 10.0 20.0 30.0 40.0 50.0 60.0

Film & Sheet

Injection Molding

Pipe & Profile

Extrusion Coating

Blow Molding

Wire & Cable

Rotomolding

Fiber

Raffia

Other20122017

5.0%

5.0%

5.7%

3.0%

4.6%

3.4%

5.0%

6.0%

4.5%

2.6%

2012-2017 Average Annual

Growth Rate, Total Demand: 4.7%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 23

North America New PE ProjectsCompany Location Country LDPE LLDPE HDPE Startup Type

2014-2015Equistar LaPorte, TX United States 300 Q1 2014 Hypo (1)Equistar Morris, IL United States 50 Q1 2014 Hypo (1)Nova Sarnia Canada 100 Q1 2015 Hypo

2016Braskem Idesa Coatzacoalcos Mexico 300 750 Q1 2016 (1)Nova Joffre Canada 250 Q1 2016 Hypo (1)Formosa Point Comfort, TX United States 300 Q4 2016 (1)ExxonMobil Mont Belvieu, TX United States 650 650 Q3 2016 (1)

2017Dow Gulf Coast United States 550 650 Q3 2017 HypoCPChem Sweeny, TX United States 500 500 Q3 2017 (1)

2018-2019Nova Sarnia Canada 350 Q3 2018 Hypo (1)Sasol Gulf Coast United States 500 500 Q3 2018 HypoShell Marcellus, United States 500 500 Q3 2019 HypoTotals, 000's MT 1050 3300 3550 7900Notes: (1): Announced projects included in our capacity database; (2): Announced expansions with IHS estimate of product and size, also not included in database; Hypo (1): reported projects not fully verifiedor approved and not included in the database; Hypo: IHS estimates of product and size for announced ethylene crackers - PE not in database.

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

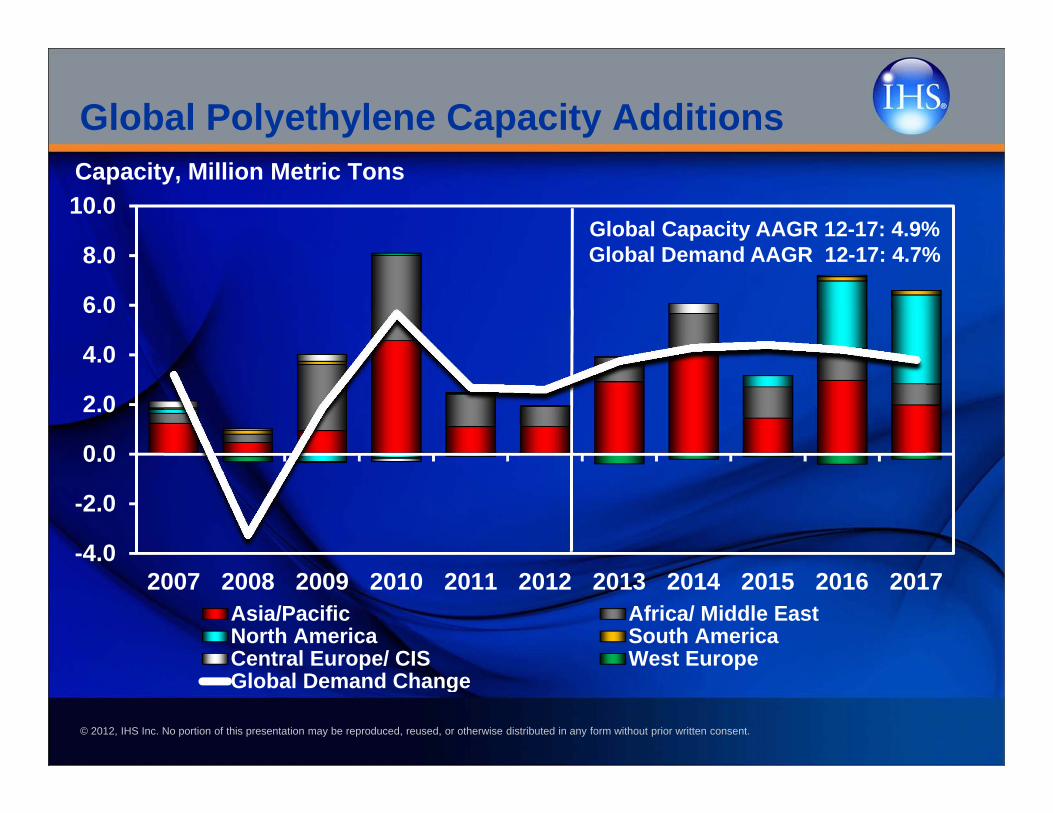

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Asia/Pacific Africa/ Middle EastNorth America South AmericaCentral Europe/ CIS West EuropeGlobal Demand Change

Capacity, Million Metric Tons

Global Polyethylene Capacity Additions

Global Capacity AAGR 12-17: 4.9%Global Demand AAGR 12-17: 4.7%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

PE: North America Current Situation

• Domestic demand is positive by 2.6% through August• Export volumes are negative by 3.5% YTD. • Total demand is higher versus 2011 YTD by 1.2%• Domestic / total demand has been trending higher since April

low point due to increased production capacity, lower prices, and restocking.

• Export volumes averaging about 700 million pounds per month = 22% of total through August. Exports as a % of production about 5% below 2011 level, and avg monthly shipments are about 25 million pounds lower than 2011 YTD.

• We expect demand to continue on the recent track and forecast total 2012 demand to approximate 2011 levels. 2013 growth slightly below GDP levels

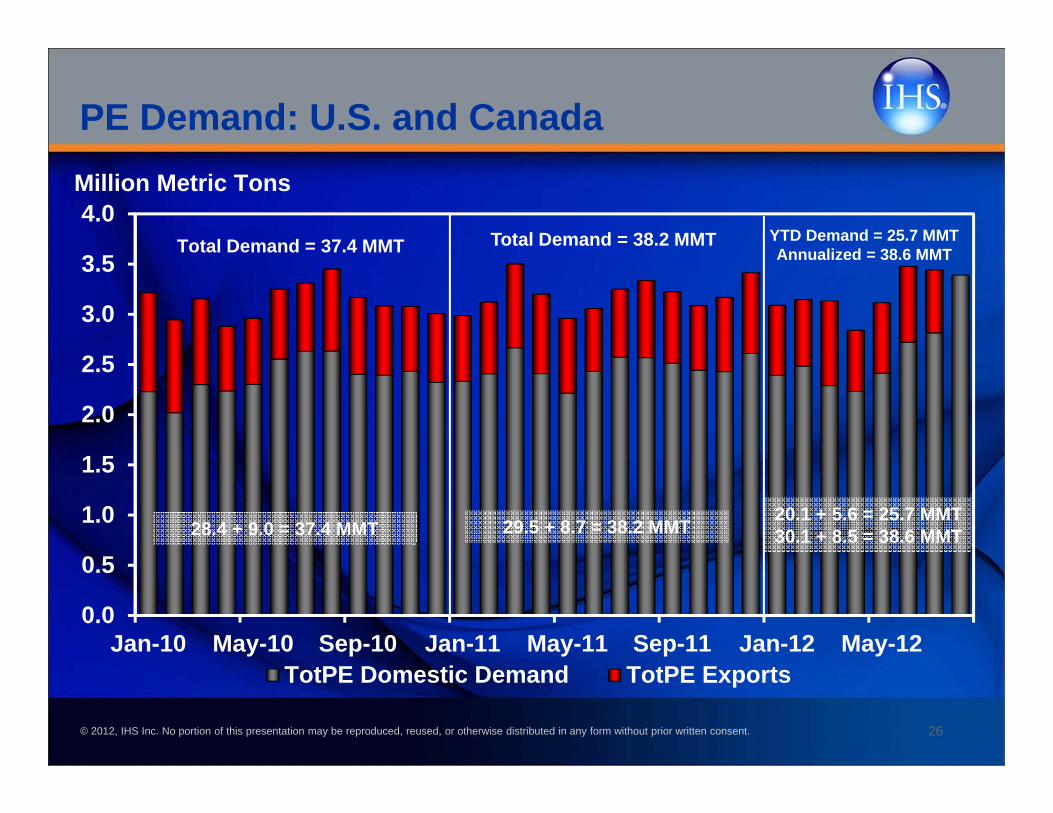

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 26

PE Demand: U.S. and Canada

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12TotPE Domestic Demand TotPE Exports

Million Metric Tons

Total Demand = 37.4 MMT Total Demand = 38.2 MMT YTD Demand = 25.7 MMTAnnualized = 38.6 MMT

28.4 + 9.0 = 37.4 MMT 29.5 + 8.7 = 38.2 MMT 20.1 + 5.6 = 25.7 MMT30.1 + 8.5 = 38.6 MMT

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 27

0

10

20

30

40

50

60

70

0

20

40

60

80

100

120

140

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12Daily Demand Days Inventory

Million Pounds Days Inventory

U.S. & Canada PE Resin Producer Inventory

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 28

0102030405060708090

100

Jan-07 Nov-07 Sep-08 Jul-09 May-10 Mar-11 Jan-12 Nov-12 Sep-13NAM Cash Cost, Integrated NAM LLDPEWEP LLDPE CHINA LLDPE (Spot)

Cents Per Pound

Regional LLDPE Butene Prices

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 29

Polyethylene Chain Margins

-220

0

220

440

660

880

-10

0

10

20

30

40

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

PE Margin - Contract HDPE Blow Molding Non-Int. Including DiscountsEthylene Margin - Average Acquisition Ethylene Price Minus Ethane Cracking Costs

Cents Per Pound, Polyethylene Dollars Per Metric Ton

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• Global demand growth exceeds GDP growth with particular strength in Asia and Latin America

• Domestic demand growth in developed economies continues to lag GDP

• Significant capacity additions forthcoming in North America as producers leverage shale based economics

• Primary threats to margin growth are continued weakness in the global economy and longer term the start up of new capacity in U.S. and MDE

• Environmental issues curtail growth for HDPE HMW applications but “green” PE demand growth remains attractive.

• M LLDPE resins represent superior demand and margin growth opportunities

30

PE Summary

Polyester Chain Market Review

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Global Polyester Demand

China Non-China Asia Southeast Asia Indian Sub Cont.MDE/AFR Europe South America North America

55.6 Million Metric Tons

PET17.4 Million Metric Tons

32

Global Demand By Region

Fiber34.5 Million Metric Tons

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 33

World Polyester Demand Growth By Product

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Filament Staple Fiber PET Packaging

Thousand Metric Tons

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 34

World Polyester Demand Growth By Region

-3

-2

-1

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017China ISC Rest of World

Million Metric Tons

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 35

Polyester Raw Materials

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 36

Refineries Are Built to Make Fuel! PET Must Buy Away Its Feedstocks

NaturalGas

GasSeparation

Unit

RefineryCrude

OilReformer

Reformate BTXExtraction

SteamCracker

ButaneHydrogen

Propylene/PP

BTX

Ethylene

ETHYLENE GLYCOL

POLYETHYLENES

ETHYLBENZENE/STYRENE

ETHYLENE DICHLORIDE/PVC

NaphthaGas OilEthanePropaneButane

TOLUENE

m-XYLENE

p-XYLENE

BENZENE

o-XYLENE

XYLENES

PTA/DMT PET

PIA

Methane

Gasoline

Heating Fuel

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 37

Raw Material Utilization Per Unit of PET

+Ethylene Glycol

(MEG or EG)0.36

Ethylene0.22

O2+ +H2OEthylene

Oxide(EO)

Paraxylene (PX)

0.58O2

Terephthalic Acid (PTA)

+0.86Acetic Acid

Polyethylene Terephthalate

(PET)+H2O

Isophthalic Acid

0.01-0.03Naphtha

Crude Oil

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 38

Global PX Capacity Growth

60

65

70

75

80

85

90

95

-4-202468

10121416

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Asia Europe, Middle East, AfricaAmericas Global Demand GrowthExcess Capacity Operating Rate

Million Metric Tons Operating Rate, Percent

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 39

Global MEG Capacity Growth

40

50

60

70

80

90

100

-2

0

2

4

6

8

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Asia Europe, Middle East, AfricaAmericas Global Demand GrowthExcess Capacity Operating Rate

Million Metric Tons Percent Operating

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 40

Global PTA Capacity Growth

50556065707580859095100

-5

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Americas Europe, Middle East, AfricaAsia Global Demand GrowthExcess Capacity Operating Rate

Million Metric Tons Operating Rate, Percent

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 41

Global PET Capacity Growth

60

65

70

75

80

85

90

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Americas Europe, Middle East, AfricaAsia Global Demand GrowthExcess Capacity Total Operating Rate

Million Metric Tons Percent Operating Rate

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

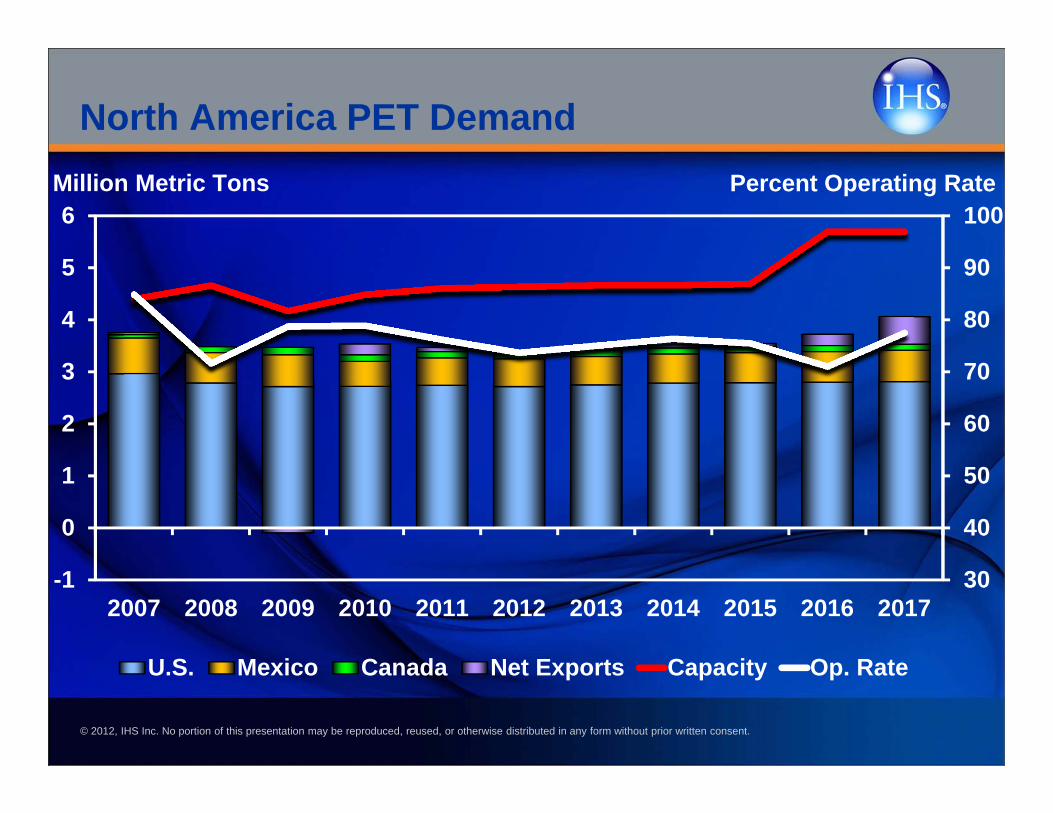

30

40

50

60

70

80

90

100

-1

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

U.S. Mexico Canada Net Exports Capacity Op. Rate

Million Metric Tons Percent Operating Rate

North America PET Demand

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

14%

14%

19%9% 3%

9%

17%

15%

2010/2011Pre-Consolidation

DAK Indorama M&G Nan Ya Selenis Wellman Invista Eastman

Total Capacity = 4635 Million Metric Tons

North American PET Consolidation

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

32%26%

33%7% 2%

DAK Indorama M&G Nan Ya Selenis

2014 North American PET Capacity

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0102030405060708090

100

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Crude PX Comp PTA Comp MEG Comp PET Spread R/C Frt

Cents Per Pound

PET – U.S. Component CostsNet Costs – Total Equals PET Price

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.