Planning for Social Security€¦ · Social Security Retirement Benefits Social Security was...

9

Chlebina Capital Management, LLC Larry Chlebina President 843 N. Cleveland-Massillon Rd Suite DN12 Akron, OH 44333 330-668-9200 [email protected] www.chlebinacapital.com Planning for Social Security September 25, 2015 Page 1 of 9, see disclaimer on final page

Transcript of Planning for Social Security€¦ · Social Security Retirement Benefits Social Security was...

Chlebina Capital Management, LLCLarry ChlebinaPresident843 N. Cleveland-Massillon RdSuite DN12Akron, OH 44333330-668-9200lchlebina@ccapmanagement.comwww.chlebinacapital.com

Planning for Social Security

September 25, 2015Page 1 of 9, see disclaimer on final page

Social Security Retirement BenefitsSocial Security was originally intended toprovide older Americans with continuingincome after retirement. Today, though thescope of Social Security has been widened toinclude survivor's, disability, and otherbenefits, retirement benefits are still thecornerstone of the program.

How do you qualify forretirement benefits?

When you work and pay Social Security taxes(FICA on some pay stubs), you earn SocialSecurity credits. You can earn up to 4 creditseach year. If you were born after 1928, youneed 40 credits (10 years of work) to beeligible for retirement benefits.

How much will your retirementbenefit be?

Your retirement benefit is based on youraverage earnings over your working career.Higher lifetime earnings result in higherbenefits, so if you have some years of noearnings or low earnings, your benefit amountmay be lower than if you had worked steadily.Your age at the time you start receivingbenefits also affects your benefit amount.Although you can retire early at age 62, thelonger you wait to retire (up to age 70), thehigher your retirement benefit.

You can estimate your retirement benefitonline based on your actual earnings recordusing the Retirement Estimator calculator onthe Social Security website,www.socialsecurity.gov. You can createvarious scenarios based on current law thatwill illustrate how different earnings amountsand retirement ages will affect your benefits.

Retiring at full retirement age

Your full retirement age depends on the yearin which you were born.

If you were born in: Your full retirementage is:

1943-1954 66

1955 66 and 2 months

1956 66 and 4 months

1957 66 and 6 months

1958 66 and 8 months

1959 66 and 10 months

1960 and later 67

Note: If you were born on January 1 of anyyear, refer to the previous year to determineyour full retirement age.

If you retire at full retirement age, you'llreceive an unreduced retirement benefit.

Retiring early will reduce yourbenefit

You can begin receiving Social Securitybenefits before your full retirement age, asearly as age 62. However, if you retire early,your Social Security benefit will be less than ifyou wait until your full retirement age to beginreceiving benefits. Your retirement benefit willbe reduced by 5/9ths of 1 percent for everymonth between your retirement date and yourfull retirement age, up to 36 months, then by5/12ths of 1 percent thereafter. For example, ifyour full retirement age is 67, you'll receiveabout 30 percent less if you retire at age 62than if you wait until age 67 to retire. Thisreduction is permanent--you won't be eligiblefor a benefit increase once you reach fullretirement age.

Still, receiving early Social Security retirementbenefits makes sense for many people. Eventhough you'll receive less per month than ifyou wait until full retirement age to beginreceiving benefits, you'll receive benefitsseveral years earlier.

Delaying retirement willincrease your benefit

For each month that you delay receivingSocial Security retirement benefits past yourfull retirement age, your benefit will increaseby a certain percentage. This percentagevaries depending on your year of birth. Forexample, if you were born in 1943 or later,your benefit will increase 8 percent for eachyear that you delay receiving benefits. Inaddition, working past your full retirement agehas another benefit: It allows you to add yearsof earnings to your Social Security record. Asa result, you may receive a higher benefitwhen you do retire, especially if your earningsare higher than in previous years.

Working may affect yourretirement benefit

You can work and still receive Social Securityretirement benefits, but the income that youearn before you reach full retirement age mayaffect the amount of benefit that you receive.

Today, though the scope ofSocial Security has beenwidened to includesurvivor's, disability, andother benefits, retirementbenefits are still thecornerstone of the program.

Page 2 of 9, see disclaimer on final page

Here's how:

• If you're under full retirement age: $1 inbenefits will be deducted for every $2 inearnings you have above the annual limit

• In the year you reach full retirement age:$1 in benefits will be deducted for every $3you earn over the annual limit (a differentlimit applies here) until the month youreach full retirement age

Once you reach full retirement age, you canwork and earn as much income as you wantwithout reducing your Social Securityretirement benefit.

Retirement benefits for qualifiedfamily members

Even if your spouse has never worked outsideyour home or in a job covered by SocialSecurity, he or she may be eligible for spousalbenefits based on your Social Securityearnings record. Other members of yourfamily may also be eligible. Retirementbenefits are generally paid to family memberswho relied on your income for financialsupport. If you're receiving retirement benefits,the members of your family who may beeligible for family benefits include:

• Your spouse age 62 or older, if married atleast one year

• Your former spouse age 62 or older, if youwere married at least 10 years

• Your spouse or former spouse at any age,if caring for your child who is under age 16or disabled

• Your children under age 18, if unmarried• Your children under age 19, if full-time

students (through grade 12) or disabled• Your children older than 18, if severely

disabled

Your eligible family members will receive amonthly benefit that is as much as 50 percentof your benefit. However, the amount that canbe paid each month to a family is limited. Thetotal benefit that your family can receive basedon your earnings record is about 150 to 180percent of your full retirement benefit amount.If the total family benefit exceeds this limit,each family member's benefit will be reducedproportionately. Your benefit won't be affected.

How do you sign up for SocialSecurity?

You should apply for benefits at your localSocial Security office or on-line two or threemonths before your retirement date. However,the SSA suggests that you contact your localoffice a year before you plan on applying forbenefits to discuss how retiring at a certainage can affect your finances. Fill out anapplication on the SSA website, or call theSSA at (800) 772-1213 for more informationon the application process.

Planning for Earned Income in RetirementIf you're like a lot of people, retirement won'tbe the world of gardening, golfing, traveling,and tennis you once envisioned. Rather,retirement will mean relaxing and working.Maybe you've retired from your "regular" joband started a business, or perhaps you wantto work part-time just to stay busy. However, ifyou work after you start receiving SocialSecurity retirement benefits, your earningsmay affect the amount of your benefit check.

How your earnings affect yourbenefit

Your earnings in retirement may increaseyour retirement benefit

Your monthly Social Security retirementbenefit is based on your lifetime earnings.When you become entitled to retirementbenefits at age 62, the Social SecurityAdministration (SSA) calculates your primaryinsurance amount (PIA) upon which yourretirement benefit will be based. Later, your

PIA will be recalculated annually if you havehad any new earnings that might substantiallyincrease your benefit. So if you continue towork after you start receiving retirementbenefits, these earnings may eventuallyincrease your PIA and thus your retirementbenefit.

Your earnings in retirement may decreaseyour retirement benefit

If you earn income over a certain limit byworking after you begin receiving retirementbenefits, your benefit may be reducedproportionately. This limit, known as theretirement earnings test exempt amount,affects only beneficiaries under normalretirement age. The benefit reduction is basedon your annual earnings and is notpermanent; your monthly benefit is reducedstarting in January of the year following theyear you had excess earnings and will bereduced until the excess earnings are usedup.

If you expect you will havesubstantial earnings afteryou retire and you have notyet reached normalretirement age, you may beable to time yourpost-retirement earnings toprevent withholding of all orpart of your Social Securityretirement benefit.

Page 3 of 9, see disclaimer on final page

Example: Emily is entitled to a Social Securityretirement benefit of $800. When she was 64,her annual earnings exceeded the retirementearnings test exempt amount, so her benefitwas reduced by $600. Consequently, inJanuary of the following year, she receivedonly a $200 monthly benefit check ($800minus $600 equals $200). However, inFebruary, she again received an $800 monthlybenefit check.

Even if your monthly benefit is reduced in theshort term due to your earnings, you'll receivea higher monthly benefit later. That's becausethe SSA recalculates your benefit when youreach full retirement age, and omits themonths in which your benefit was reduced.

How much is the retirementearnings test exempt amount?

In 2015, the annual exempt amount is $15,720($15,480 in 2014) for beneficiaries undernormal retirement age. However, in the yearyou reach full retirement age, a different limitapplies. The limit in 2015 is $41,880 ($41,400in 2014), which applies to earnings up to, butnot including, the month you reach normalretirement age.

How much benefit is withheld ifyou exceed the annual earningslimit?

If you're under normal retirement age, $1 inbenefits is withheld for every $2 of earnings inexcess of the annual exempt amount.

Example: Ida was a self-employed potatofarmer. After she began receiving SocialSecurity retirement benefits at age 62, shecontinued to sell potatoes at her producestand outside of Boise. Since she exceededthe annual retirement earnings test exemptamount by $380, $190 was withheld from herbenefit check the following January.

In the year you reach normal retirement age,$1 in benefits is withheld for every $3 ofearnings in excess of the special exemptamount that applies that year, but onlycounting money earned before the month youreach normal retirement age.

Example: In the year that Ida reached normalretirement age, she earned $3,200 more thanthe special earnings limit that applies in thatyear. However, she earned $500 of that aftershe had reached normal retirement age, sothat amount wasn't counted in calculating howmuch benefit would be withheld. Instead, theremaining $2,700 was used in the calculation,

and $900 was withheld from Ida's benefit ($1for every $3 in excess of the earnings limit).

What kinds of earnings mayaffect your benefit?

Earnings that might reduce your benefit

• Wages you earned as an employee(counted for the taxable year they'reearned)

• Net earnings from self-employment (usuallycounted in the year earnings are received)

• Other types of work-related income, suchas bonuses, commissions, and fees

Earnings that won't reduce your benefit

• Pensions and retirement pay• Workers' compensation and unemployment

compensation benefits• Prize winnings from contests, unless part of

a salesperson's wage structure, or enteringcontests is your "business"

• Tips that are less than $20 a month• Payments from individual retirement

accounts (IRAs) and Keogh plans• Investment income• Income earned in or after the month you

reach normal retirement age

Other types of earnings may affect yourbenefit. If you have additional questions abouthow the Social Security Administration definesearnings, contact the SSA at (800) 772-1213.

Which of benefits may beaffected by excess earnings?

Your own retirement benefit

Your Social Security retirement benefit may bereduced if you earn income over theretirement earnings test exempt amount.

Benefits paid to your spouse or child

If you have retired and your spouse and/orchild receives benefits based on your SocialSecurity record, any excess earnings youhave may reduce their benefits. In addition,any excess earnings they have may reducetheir own benefits but not your benefit.

Example: Bill is 63 and receives a SocialSecurity retirement benefit. His wife Betty,who is also 63, receives a retirement benefitbased on Bill's earnings that is equal to 50percent of Bill's benefit. If Bill earns $200 overthe retirement earnings test exempt amount,

If you have retired and yourspouse and/or child receivesbenefits based on yourSocial Security record, anyexcess earnings you havemay reduce their benefits.

Page 4 of 9, see disclaimer on final page

his benefit is reduced by $100 ($200 dividedby 2) the following January. Betty's benefit isreduced by 50 percent of that amount, or $50.

However, assume that Betty also works andearns $200 over the retirement earnings testexempt amount. Her benefit will be reduced by$100 ($200 divided by 2). Her benefit isreduced an additional $50 by Bill's excessearnings. Bill's benefit, however, is reduced by$100 because of his own excess earnings butis not affected by Betty's excess earnings.

Benefits paid to your survivors

If you die and a member of your familyreceives a survivor's benefit, that benefit maybe reduced if the family member earns moneyin excess of the retirement test exemptamount.

Example: When Bill dies, Betty, his widow,begins receiving survivor's benefits based onBill's Social Security record. Since she earns$200 more than the exempt amount that year,Betty's survivor's benefit of $825 is reduced by$100 in January of the following year.

The earnings test is different inthe first year of retirement

Earnings from an employer

In the first year of retirement, the earnings testis applied differently than in later years.Normally, the earnings test is based on theamount of income you earned annually;however, in the first year of retirement, theearnings test can be based on the amount ofincome you earned monthly, if that wouldbenefit you. You can receive a full SocialSecurity benefit check for any whole month inwhich your earnings don't exceed 1/12th of theannual exempt amount.

Example: Caleb retired on July 31 at age 62.From January through July of that year, heearned $40,000. After he retired, he beganworking part-time and earned only $300 amonth from August to December (each month,less than the monthly earnings exemptamount). Thus, even though his annualearnings during the year he retired greatlyexceeded the annual earnings exemptamount, Caleb's benefit check was notreduced the following year.

Earnings from self-employment

If you're self-employed, the SSA alsoconsiders whether you perform substantialservices in your business. You will receive full

benefits for any month you're not substantiallyself-employed. In general, you're consideredto be substantially self-employed if youworked as a self-employed person more than45 hours in one month. If you work less than15 hours in one month, you will not beconsidered substantially self-employed, andyou probably will receive your full retirementbenefit for that month. If you work between 15hours and 45 hours a month, you may or maynot be considered substantially self-employedby the SSA, and your retirement benefit maybe affected.

How you can keep yourpost-retirement earnings fromexceeding the earnings exemptamount

Time your post-retirement earnings

If you expect you will have substantialearnings after you retire and you have not yetreached normal retirement age, you may beable to time your post-retirement earnings toprevent withholding of all or part of your SocialSecurity retirement benefit.

Create a self-employment loss

If you're self-employed, you may be able togenerate a self-employment loss to offsetexcess self-employment income.

Incorporate a sole proprietorship

If you incorporate a sole proprietorship as anS corporation, you may be able to reduce yourself-employment earnings by receiving profitdistributions that will not be consideredself-employment income for the purposes ofthe retirement earnings test.

Shift earnings to others

You may be able to reduce your netself-employment earnings if you shift earningsto others by forming a partnership with yourspouse or employing minor children.

Caution: The SSA may scrutinizequestionable retirement arrangements. Underthe law, you are entitled to work and combineyour Social Security benefits and earnings insuch a way as to get the most income youcan. However, you should not understate yourearnings or establish fictitious businessarrangements.

Page 5 of 9, see disclaimer on final page

Questions & Answers

Q: If you earn more than the retirementearnings exempt amount, when will all orpart of your benefit be withheld due toexcess earnings?

A: Your excess earnings will be withheldstarting in January of the year following theyear you had excess earnings.

Q: If you receive Social Securityretirement benefits based on yourex-spouse's Social Security earningsrecord, will your benefit be reduced ifyour ex-spouse works after retirement andearns more than the exempt amount?

A: No. If you've been divorced for more thantwo years, your benefits will not be reduced if

Q: How does the SSA know how muchyou earn after you retire?

A: The SSA knows how much you earnbecause you are required to estimate yourearnings when you apply for Social Securitybenefits. Later, the SSA will get informationabout your earnings from your IRS W-2 form(submitted annually by your employer) or, ifyou are self-employed, from your annualincome tax return. They also may ask you tosend them an earnings estimate annually. Inaddition, if you think the earnings used tocalculate your benefit may be incorrect,contact the SSA at (800) 772-1213 so thatyour benefit can be accurately calculated.

your ex-husband has excess earnings. Theonly way your benefit will be reduced is if youhave excess earnings.

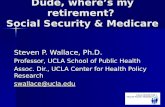

How Earnings Affect Social SecurityIf you begin to receive Social Security retirement (or survivor's) benefits before you reach fullretirement age, money you earn over a certain limit will reduce the amount of your Social Securitybenefit. In 2015, your benefit will be reduced by $1 for every $2 of earnings in excess of $15,720*

The chart below shows the effect of annual earnings of $10,000, $20,000, and $30,000 on a$12,000 annual Social Security benefit ($1,000 monthly) for someone who hasn't yet reached fullretirement age.

Source: Social Security Administration, 2014

*Special rules apply in both the year you reach full retirement age and the year you retire if youhave not reached full retirement age.

Page 6 of 9, see disclaimer on final page

Four Common Questions about Social SecurityAs you near retirement, it's likely you'll havemany questions about Social Security. Hereare a few of the most common questions andanswers about Social Security benefits.

Will Social Security be around when youneed it?

You've probably heard media reports aboutthe worrisome financial condition of SocialSecurity, but how heavily should you weighthis information when deciding when to beginreceiving benefits? While it's very likely thatsome changes will be made to Social Security(e.g., payroll taxes may increase or benefitsmay be reduced by a certain percentage),there's no need to base your decision aboutwhen to apply for benefits on this informationalone. Although no one knows for certain whatwill happen, if you're within a few years ofretirement, it's probable that you'll receive thebenefits you've been expecting all along. Ifyou're still a long way from retirement, it maybe wise to consider various scenarios whenplanning for Social Security income, but keepin mind that there's been no proposal toeliminate Social Security.

If you're divorced, can you receive SocialSecurity retirement benefits based onyour former spouse's earnings record?

You may be able to receive benefits based onan ex-spouse's earnings record if you weremarried at least 10 years, you're currentlyunmarried, and you're not entitled to a higherbenefit based on your own earnings record.You can apply for a reduced spousal benefitas early as age 62 or wait until your fullretirement age to receive an unreducedspousal benefit. If you've been divorced formore than two years, you can apply as soonas your ex-spouse becomes eligible forbenefits, even if he or she hasn't startedreceiving them (assuming you're at least 62).However, if you've been divorced for less thantwo years, you must wait to apply for benefitsbased on your ex-spouse's earnings recorduntil he or she starts receiving benefits.

If you delay receiving Social Securitybenefits, should you still sign up forMedicare at age 65?

Even if you plan on waiting until full retirementage or later to take your Social Securityretirement benefits, make sure to sign up for

you first become eligible during yourseven-month Initial Enrollment Period. Thisperiod begins three months before the monthyou turn 65, includes the month you turn 65,and ends three months after the month youturn 65.

The Social Security Administrationrecommends contacting them to sign up threemonths before you reach age 65, becausesigning up early helps you avoid a delay incoverage. For your Medicare coverage tobegin during the month you turn 65, you mustsign up during the first three months beforethe month you turn 65 (the day your coveragewill start depends on your birthday). If youenroll later, the start date of your coverage willbe delayed. If you don't enroll during yourInitial Enrollment Period, you may pay ahigher premium for Part B coverage later. Visitthe Medicare website, www.medicare.gov tolearn more, or call the Social SecurityAdministration at 800-772-1213.

Will a retirement pension affect yourSocial Security benefit?

If your pension is from a job where you paidSocial Security taxes, then it won't affect yourSocial Security benefit. However, if yourpension is from a job where you did not paySocial Security taxes (such as certaingovernment jobs) two special provisions mayapply.

The first provision, called the governmentpension offset (GPO), may apply if you'reentitled to receive a government pension aswell as Social Security spousal retirement orsurvivor's benefits based on your spouse's (orformer spouse's) earnings. Under thisprovision, your spousal or survivor's benefitmay be reduced by two-thirds of yourgovernment pension (some exceptions apply).

The windfall elimination provision (WEP)affects how your Social Security retirement ordisability benefit is figured if you receive apension from work not covered by SocialSecurity. The formula used to figure yourbenefit is modified, resulting in a lower SocialSecurity benefit.

Medicare. If you're 65 or older and aren't yetreceiving Social Security benefits, you won'tbe automatically enrolled in Medicare Parts Aand B. You can sign up for Medicare when

Page 7 of 9, see disclaimer on final page

Sources of Retirement Income: Filling the SocialSecurity GapAccording to the Social Security Administration, more than nine out of ten individuals age 65 andolder receive Social Security benefits. But most retirees also rely on other sources of retirementincome, as shown on this chart:

Source: Fast Facts & Figures About Social Security, 2014, Social Security Administration

Page 8 of 9, see disclaimer on final page

Chlebina Capital Management,LLC

Larry ChlebinaPresident

843 N. Cleveland-Massillon RdSuite DN12

Akron, OH 44333330-668-9200

September 25, 2015Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2015

IMPORTANT DISCLOSURES

Securities offered through Securities Service Network, Inc., Member FINRA/SIPC. Fee-based advisoryservices are offered through Chlebina Capital Management, LLC., a registered investment advisor.

Page 9 of 9