IB History The Civil War (1861-1865) Through Maps, Charts, Graphs & Pictures.

Upload

anil-kumar-singhCategory

view

217download

0

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 1/28

India Semiconductor Association (ISA)

The India ESDM Story

November 2012

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 2/28

Contents

India Semiconductor Association (ISA)

ESDM Industry Overview

Role of Innovation in Development and Importance of Made

in India Products

Skill Development and its Availability

Government Policies and Initiatives

Opportunity Segments

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 3/28

India Story

• 560 million consumers in 20-49 age group expected by 2015

• 5th largest consumer market by 2025

• Increased disposable incomes & changing lifestyles

• Third largest pool of scientific & technicalmanpower

• Large English speaking population

• Over 550 universities (20,000 colleges)

• 1,500 research institutions and 9K PhDs

• Over 500K engineering graduates, andupto 3 million graduates and post

graduates

• Infrastructure spend to be the biggestthrust in coming years

• Investment in infrastructure in past fiveyears doubled from 4% to 8% of GDP

• US$ 1 trillion investment proposed for2012-17

Infrastructure initiatives

Large domestic market

Human capital

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 4/28

India Semiconductor Association (ISA)

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 5/28

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 6/28

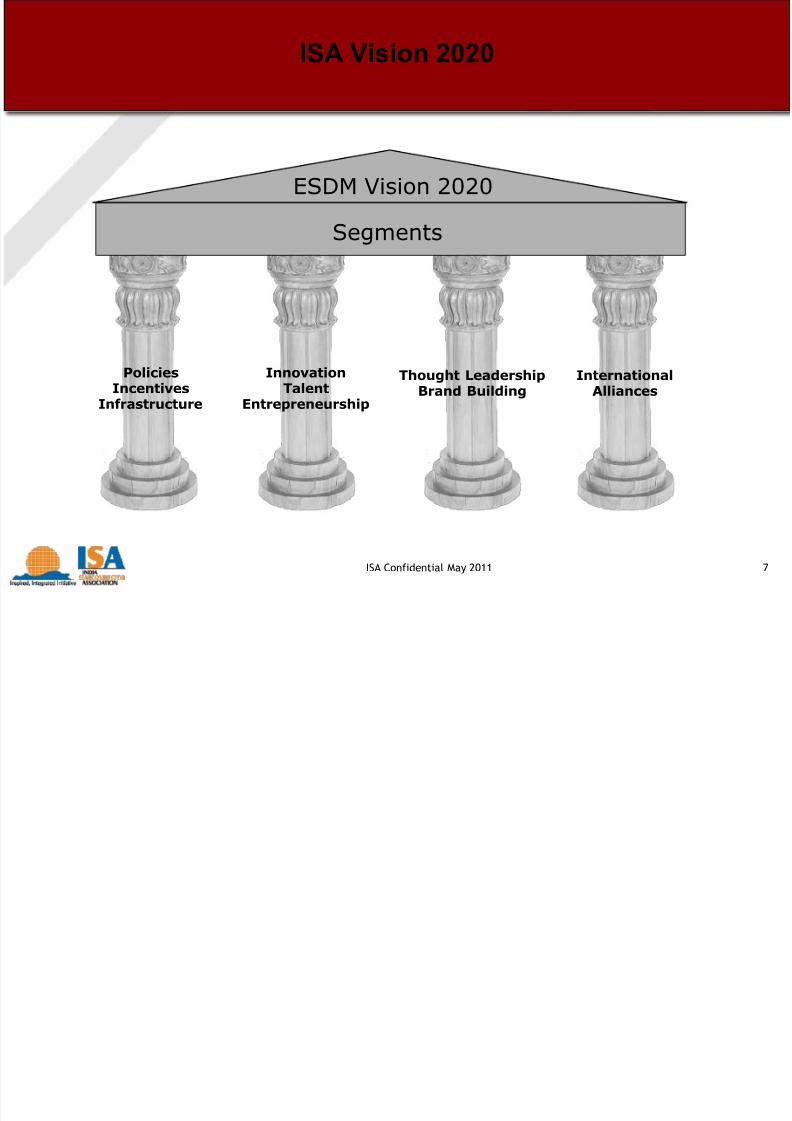

ISA Vision 2020

Vision

• Make India a powerhouse in Semiconductors and Electronics

Goal

• Facilitate ESDM industry to reach $400B target by 2020

Strategy• Knowledge Partnership with GoI: Stimulate growth of the ESDM

industry

• Grow and Mentor: Talent, Innovation, Entrepreneurship

• Build Brand India: Destination for ESDM

•

International Alliances: Bilateral business growth and sharing bestpractices

6

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 7/28

ISA Confidential May 2011 7

PoliciesIncentives

Infrastructure

ESDM Vision 2020

Segments

InnovationTalent

Entrepreneurship

Thought LeadershipBrand Building

InternationalAlliances

ISA Vision 2020

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 8/28

ESDM Industry Overview

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 9/28

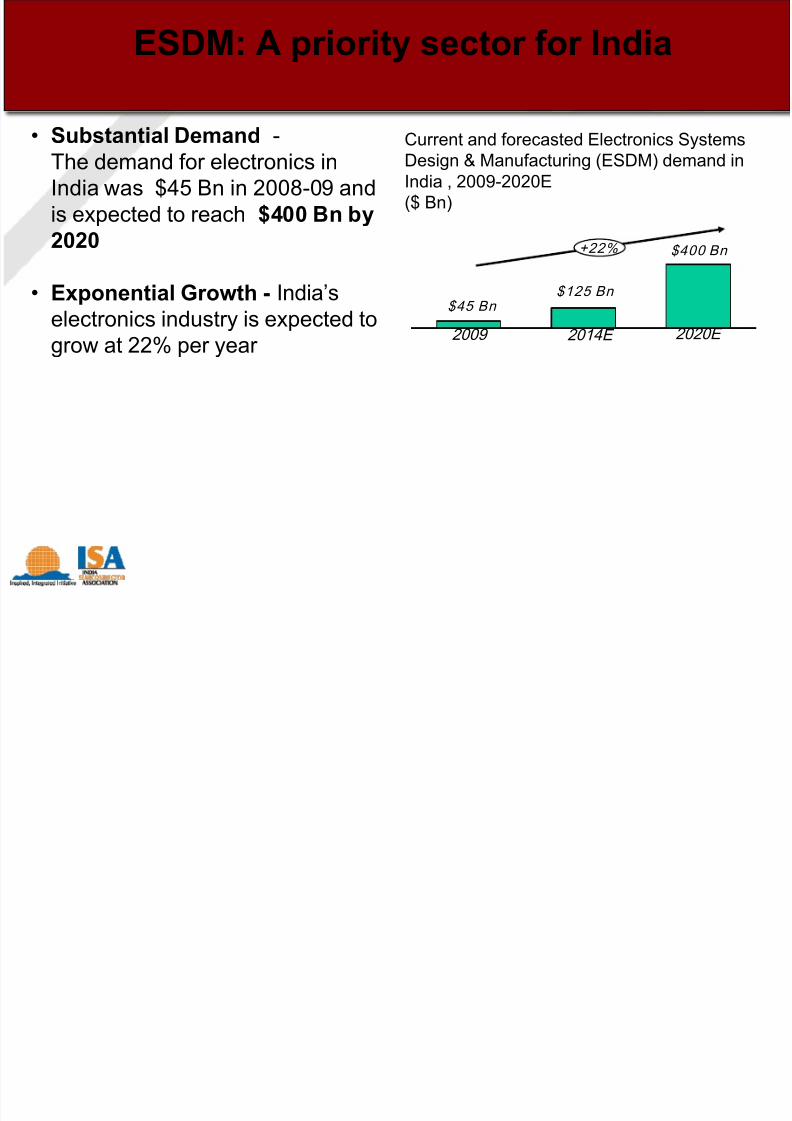

ESDM: A priority sector for India

• Substantial Demand -The demand for electronics inIndia was $45 Bn in 2008-09 andis expected to reach $400 Bn by2020

• Exponential Growth - India’s

electronics industry is expected togrow at 22% per year

Current and forecasted Electronics SystemsDesign & Manufacturing (ESDM) demand inIndia , 2009-2020E($ Bn)

$45 Bn

+22% $400 Bn

$125 Bn

2009 2014E 2020E

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 10/28

Projected demand-supply gap inelectronics industry (USD billion)

400

10445

125

85

320

20 420

250

500

FY09 FY14 FY20

Total demandDomestic production (target)Domestic production (at current CAGR)

Production levelelectronics industrymay reach withfavorable policyenvironment

Producti on level electroni cs

industry will reach with currentpolicy environment

Gap between

current andexpecteddomestic production,offering significantopportunities forimprovement

Source: Report of sub-committee of task force set up by DIT, Government of India, stimulating ESDM industry in India (Dec 2009)

The impetus behind the ESDM initiative

10

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 11/28

11

Telecom Mobile

Industrial Electronics

Consumer Electronics

IT / OA

(Computers

peripherals)

ElectronicComponents

& other items

Medical Electronics

Automotive Electronics

Solar Photovoltaic

Atomic Energy

Space

Defence & Strategic

Needs

Avionics

Electronics: Integral part of our lives

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 12/28

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 13/28

13

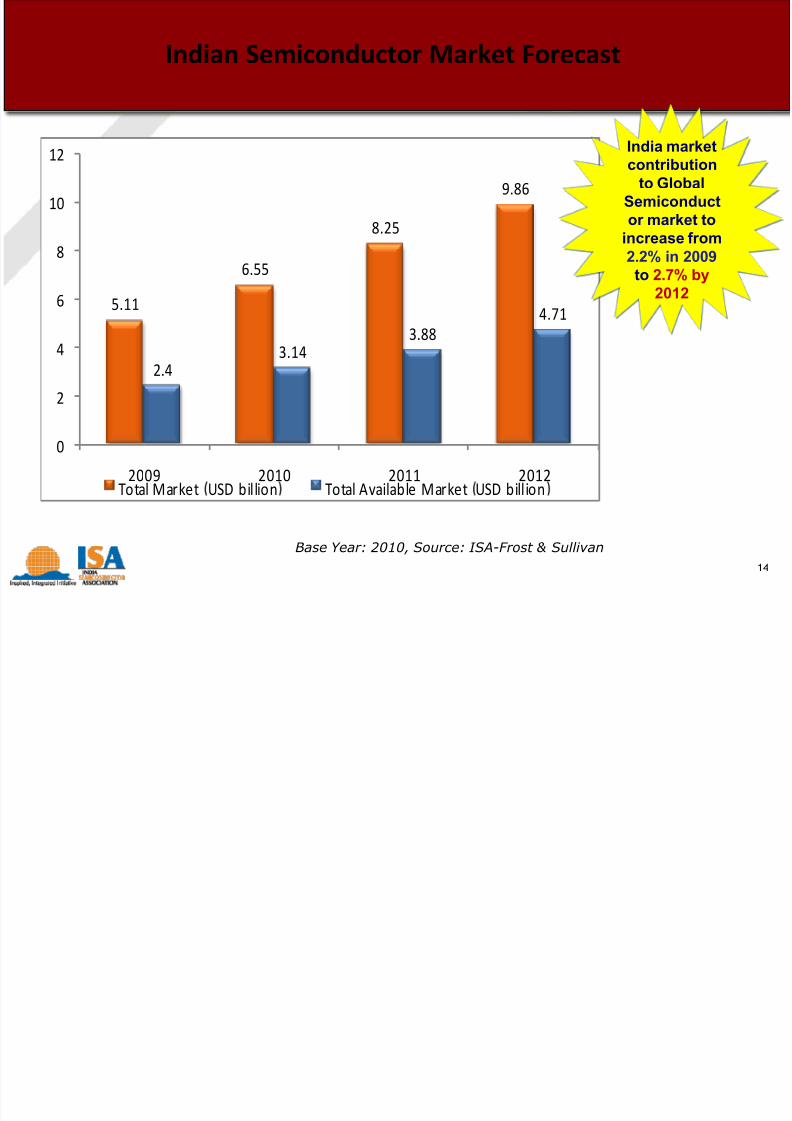

Indian Electronics Market Forecast

Base Year: 2010, Source: ISA- Frost & Sullivan

51.1

65.1

81.1

96.5

29.436

43.8

53.4

0

20

40

60

80

100

120

2009 2010 2011 2012Total Market (USD billion) Total Available Market (USD billion)

CAGR

TM: 21.8%

TAM: 21.7%

5.116.55

8.259.86

2.4 3.14 3.88 4.71

0

10

20

2009 2010 2011 2012

Indian Semiconductor Market Forecasts

Enormous potential to

grow domesticmanufacturing.

Represents huge

opportunity to partner

with Indian companies

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 14/28

14

Indian Semiconductor Market Forecast

Base Year: 2010, Source: ISA-Frost & Sullivan

5.11

6.55

8.25

9.86

2.43.14

3.88

4.71

0

2

4

6

8

10

12

2009 2010 2011 2012Total Market USD billion Total Available Market USD billion

India marketcontribution

to GlobalSemiconductor market to

increase from2.2% in 2009

to 2.7% by2012

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 15/28

15

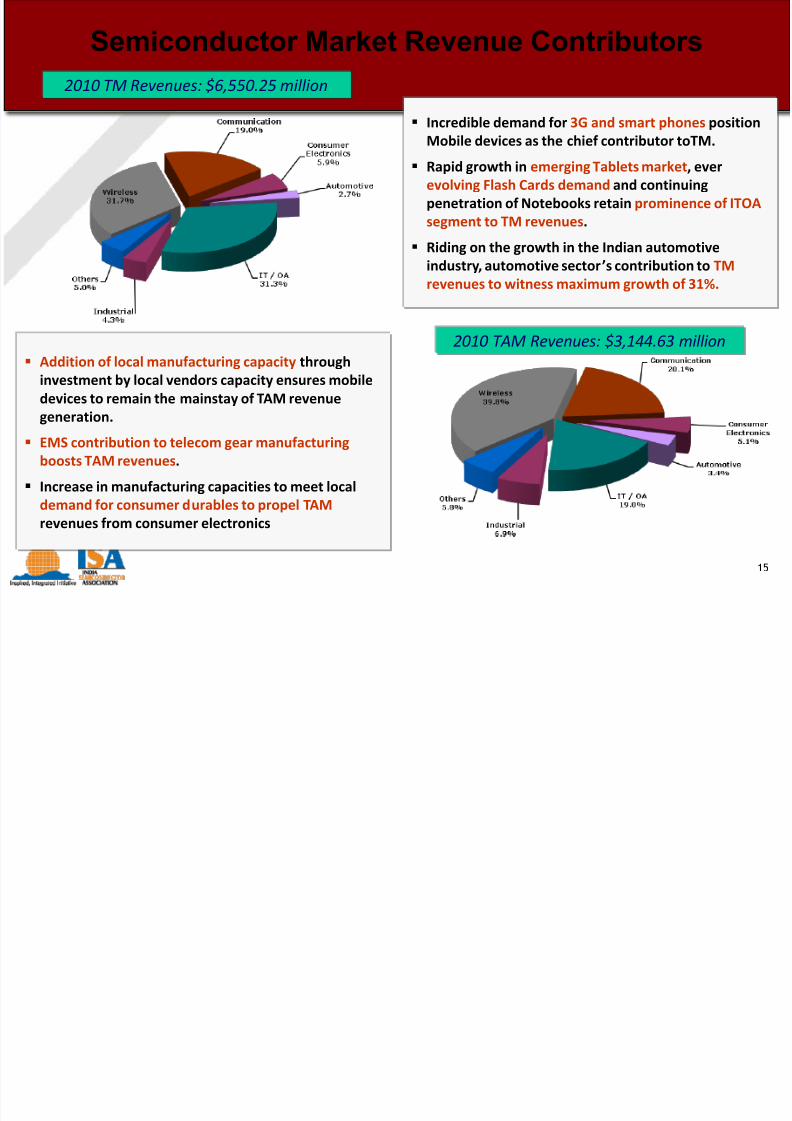

2010 TAM Revenues: $3,144.63 million

2010 TM Revenues: $6,550.25 million

Incredible demand for 3G and smart phones position

Mobile devices as the chief contributor toTM.

Rapid growth in emerging Tablets market, ever

evolving Flash Cards demand and continuing

penetration of Notebooks retain prominence of ITOA

segment to TM revenues.

Riding on the growth in the Indian automotive

industry, automotive sector’s contribution to TM

revenues to witness maximum growth of 31%.

Addition of local manufacturing capacity through

investment by local vendors capacity ensures mobile

devices to remain the mainstay of TAM revenue

generation.

EMS contribution to telecom gear manufacturing

boosts TAM revenues.

Increase in manufacturing capacities to meet local

demand for consumer durables to propel TAM

revenues from consumer electronics

Semiconductor Market Revenue Contributors

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 16/28

Skill Development and its Availability

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 17/28

Importance of skill development for ESDM industry

The industry is presently characterized by high level of imports and lowdomestic content, which is beginning to change with the Government’spro-active policy initiatives to encourage higher domestic value additionin Electronic Systems Design & Manufacturing (ESDM).

These initiatives will create significant opportunities and requirements for

skilled personnel. As the electronics industry is technology intensive, theworkforce would need to be continuously trained.

Availability of large pool of skilled workforce is necessary to attract FDI.

Hence, skill development finds a very important place in growth of thedomestic ESDM industry and progress of the country.

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 18/28

Employment Opportunity in ESDM

Employment Opportunity in ESDM

It is estimated that around 16.1 millionpeople will be directly employed in theindustry by 2014 and 27.8 million by 2020,as compared to the current 4.4 million.

Installed talent pool in Semiconductor

Industry, 2009-2012 (in ‘000s)

India has an abundance of skilledmanpower. Each year, aroundthree million science and

engineering graduates are addedto the workforce, much higherthan in China and other developedcountries. The quality of Indiangraduates is also ranked betterthan in China, Vietnam as well asJapan and the US on certainparameters.

Fresh graduate supply in India

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 19/28

Role of Electronics Sector Skills Council (ESSC)

ESSC will undertake pilot projects in the initial period of 1 year or so in thefunctions/occupations like Production, Service Support, Semiconductor design /R&D

Around 5000-6000 workforce will be imparted skills and certified during the pilotphase

Steady growth planned in the number of persons to be imparted skills to reacharound 6.5 lakh persons yearly by 2020

On a cumulative basis, 2 million workforce proposed to be trained and certifiedby 2020

28 trades proposed to be covered in the skill development plan

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 20/28

Government Policies and Initiatives

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 21/28

Govt. Procurement Projects

ISA Confidential May 2011 21

National Optical Fiber NetworkProvide broadband connectivity to panchayats so thatbanking and health services can be accessed online

US$ 4 Bn

US$ 1.2 Bn

US$ 4 Bn

National Knowledge NetworkInfrastructure project to connect educational and researchinstitutes

National e-Governance PlanCountrywide infrastructure reaching down to the remotest ofvillages; bringing public services closer to home

US$ 1.2 BnSet Top BoxDigital Addressable System (DAS) mandatory throughoutcountry by December’14

US$ 0.2 BnLED productsDistribution of free LED lights to all BPL families ; Excise duty

reduction on LED lamps and LEDs

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 22/28

Preferential Market Access

Electronic Development Fund

• Electronics Sector Skillcouncil

• Study to identify major jobroles

• Semiconductor Wafer Fab• Modified SIPS• Electronic Manufacturing

ClustersCreatingEcosyste

m

Building

Demand

R & Dinitiative

s

HR

aspects

Government Initiatives

ISA Confidential May 2011 22

Department of Electronics & Information Technology (DeitY)

Ministry of Communication & Information Technology, Government of India

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 23/28

Major Initiatives To Promote ESDM Sector

ISA Confidential May 2011 23

1. Setting up two Semiconductor Wafer Fabs for manufacture of Chips

2. Introducing Modified Special Incentive Package Scheme to encouragemanufacture of high priority electronic products in India by providingcapital grant

3. Provide incentives for setting up of Electronics Manufacturing Clusters.

4. Providing Preferential Market Access to domestically manufacturedelectronics products for government procurement and procurement bygovernment licensees.

5. Setting up of “Electronic Development Fund” for promotion of innovation,R&D, Indian IPR and development of Indian Microprocessor.

6. Setting up of the National Electronics Mission (NEM)

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 24/28

Opportunity Segments

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 25/28

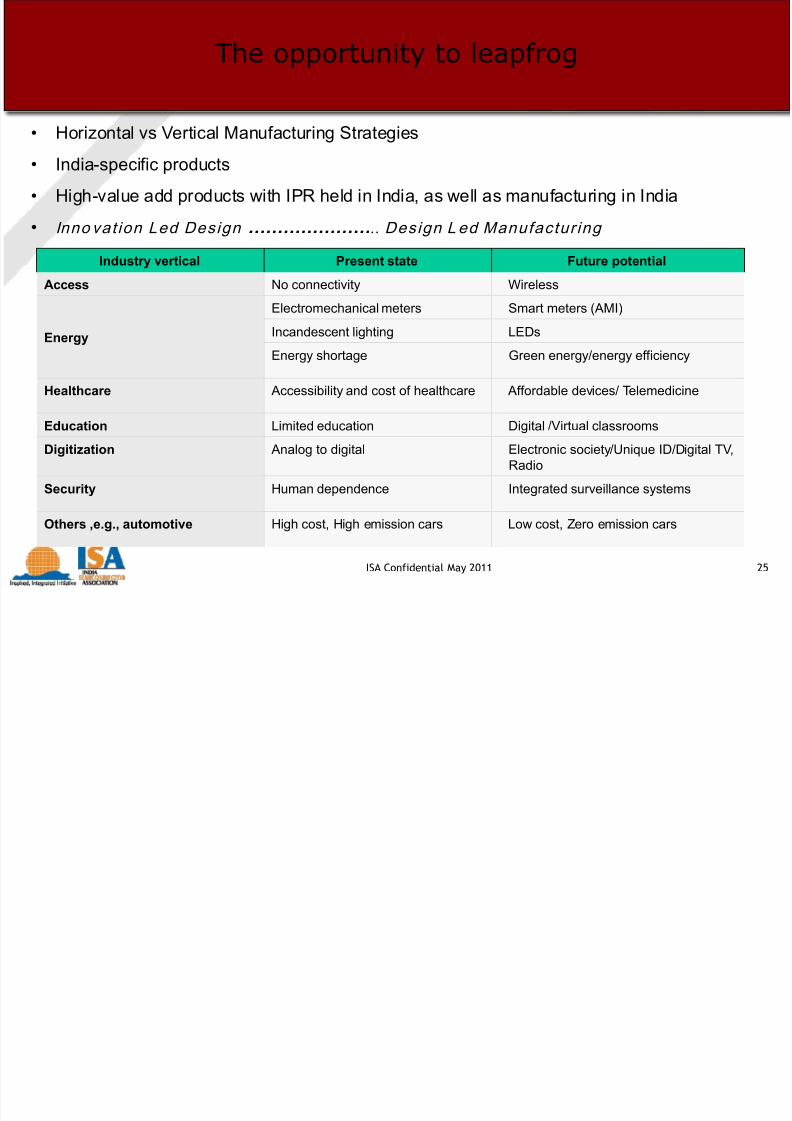

The opportunity to leapfrog

ISA Confidential May 2011 25

Industry vertical Present state Future potential

Access No connectivity Wireless

Energy

Electromechanical meters Smart meters (AMI)

Incandescent lighting LEDs

Energy shortage Green energy/energy efficiency

Healthcare Accessibility and cost of healthcare Affordable devices/ Telemedicine

Education Limited education Digital /Virtual classrooms

Digitization Analog to digital Electronic society/Unique ID/Digital TV,Radio

Security Human dependence Integrated surveillance systems

Others ,e.g., automotive High cost, High emission cars Low cost, Zero emission cars

• Horizontal vs Vertical Manufacturing Strategies• India-specific products

• High-value add products with IPR held in India, as well as manufacturing in India

• In n o v a t i o n L e d D e s i g n ………………….. D e s i g n L e d M a n u f a c t u r i n g

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 26/28

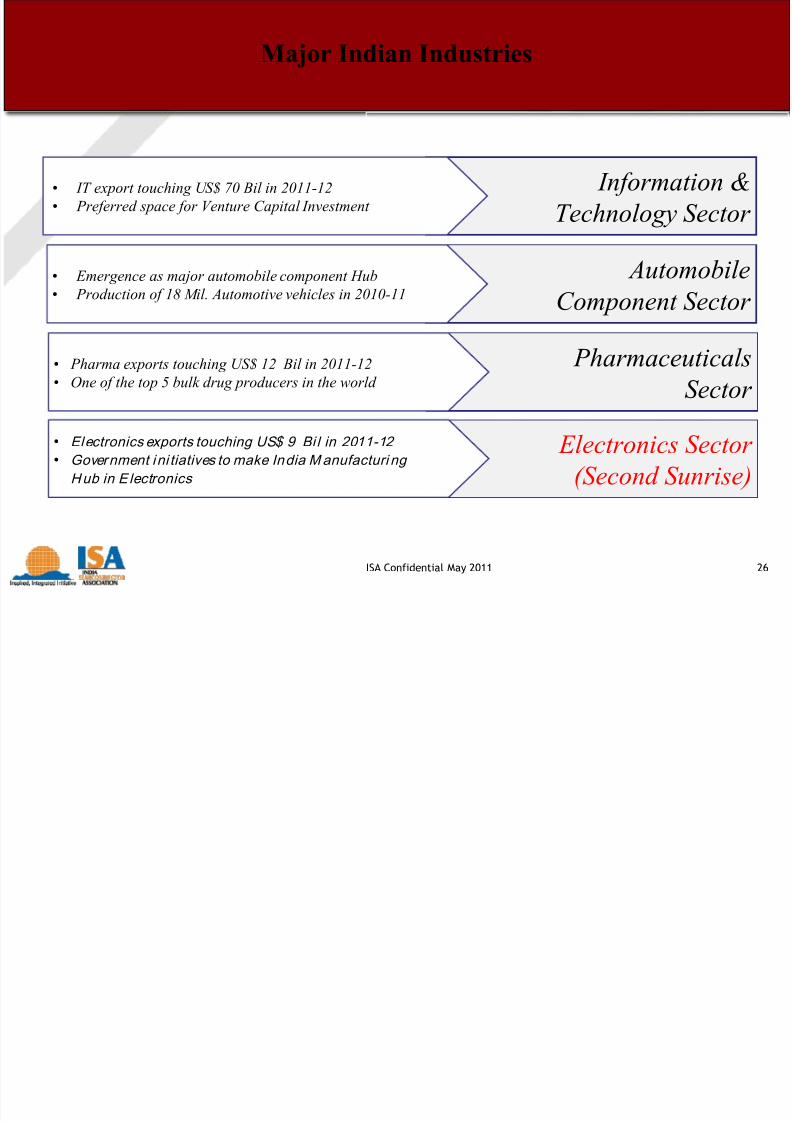

Major Indian Industries

ISA Confidential May 2011 26

Information &

Technology Sector • IT export touching US$ 70 Bil in 2011-12

• Preferred space for Venture Capital Investment

AutomobileComponent Sector •

Emergence as major automobile component Hub• Production of 18 Mil. Automotive vehicles in 2010-11

Pharmaceuticals

Sector • Pharma exports touching US$ 12 Bil in 2011-12

• One of the top 5 bulk drug producers in the world

Electronics Sector

(Second Sunrise)

• Electronics exports touching US$ 9 Bi l in 2011-12

• Government ini tiatives to make India Manufacturi ng

Hub in E lectronics

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 27/28

Opportunity in Strategic Electronics

ISA Confidential May 2011 27

Defense electronics production likely to reach Rs.15,000 crores this year.Value of electronics set to rise faster than the total value of strategicequipment.

Defence budget for 2012-13 set at Rs. 1.93 lakh crore.

Expected to provide mfg and biz opportunities of Rs.40,000 crores over the

next 5 yearsThe Offset opportunity estimated at USD 10-15 Billion over the next 4-7 years.

India is currently among the top 10 spenders worldwide with its defenceexpenditure growth at about 9.3%.

7/21/2019 Pictures & Graphs

http://slidepdf.com/reader/full/pictures-graphs 28/28

For More information

www.isaonline.org

[email protected]@isaonline.org