PGBM01 - MBA Financial Management And Control (2015-16 Trm1 A)Lecture 9 long term decision making

28

PGBM01 Financial Management & Control Lecture 9 Long-term decision making By Andy Turton. [email protected] The University of Sunderland School of Business & Law

-

Upload

aquamarine-emerald -

Category

Business

-

view

531 -

download

1

Transcript of PGBM01 - MBA Financial Management And Control (2015-16 Trm1 A)Lecture 9 long term decision making

PGBM01

Financial Management & Control

Lecture 9 Long-term decision making

By

Andy Turton.

The University of Sunderland

School of Business & Law

Learning Objectives Characteristics of long-term decision making

Processes of decision making

Major techniques for decision making

Advantages and disadvantages of these methods

Other factors for decision making

2

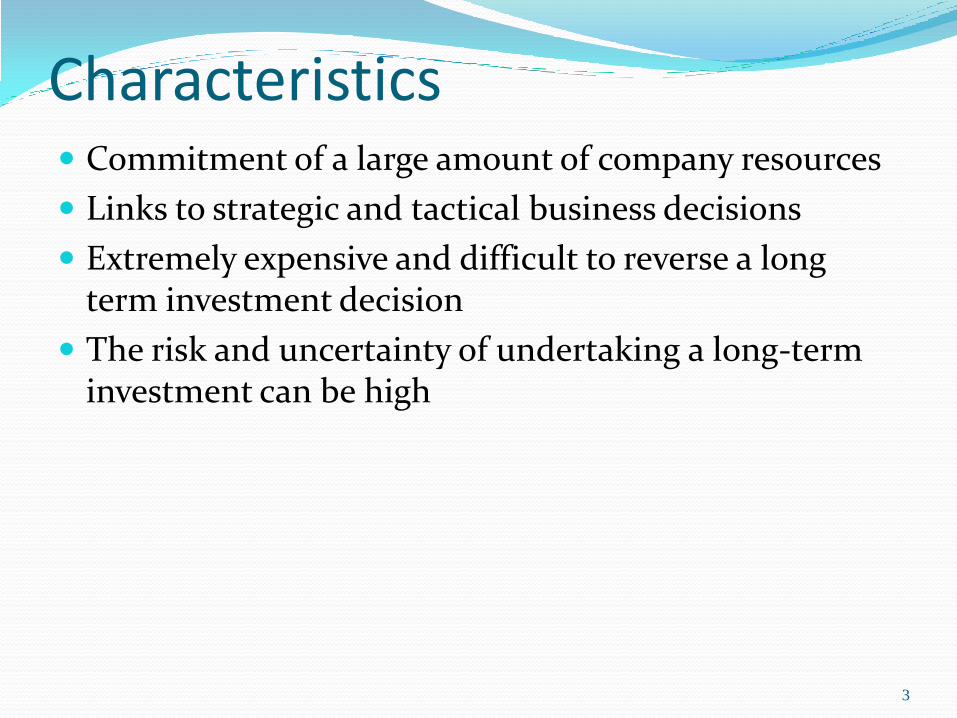

Characteristics Commitment of a large amount of company resources

Links to strategic and tactical business decisions

Extremely expensive and difficult to reverse a long term investment decision

The risk and uncertainty of undertaking a long-term investment can be high

3

Processes Initial investigation To determine if the investment proposal is a feasible

project (marketing; technical; legal and economic feasibility studies)

Factors to consider: resources required, technical and commercial feasibility, risks of the project, and how the project matches the firm’s strategic objectives

Detailed evaluation To forecast the expected cash flows from the project, by

using NPV, IRR or other relevant techniques Simulation and sensitivity analysis may be used to assess

the degree of risk involved in the project Sources of finance and non-financial factors need to be

detailed

4

Processes

Authorisation

Ranking of proposals in order of priority

The proposal meets the profitability criteria and is compatible with the overall strategy of the business

The decision should be made by senior management, or the board of directors if necessary

Project implementation

The appointment of a project manager or assignment of responsibility

The required resources are allocated and the specified targets are set to be achieved

5

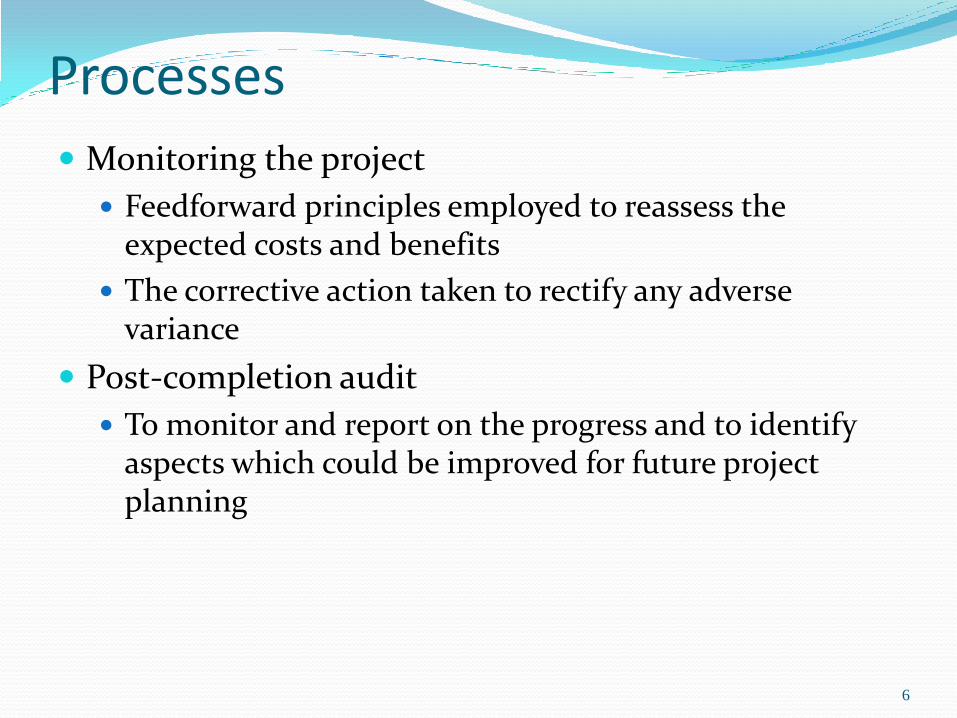

Processes

Monitoring the project

Feedforward principles employed to reassess the expected costs and benefits

The corrective action taken to rectify any adverse variance

Post-completion audit

To monitor and report on the progress and to identify aspects which could be improved for future project planning

6

Methods of Investment Appraisal Payback period (PP)

The length of time: cash proceeds recover the initial capital

expenditure

Accounting Rate of Return (ARR)

A return measurement by using average annual profits

Net Present Value (NPV)

The present value of the net cash inflows less the initial

investment

Internal Rate of Return (IRR)

A return measurement takes into account the time value of

money

7

Example There are two optional projects for your company to

choose. However, you can only choose one of them. The data for the initial investments are in the following table. You are required to calculate:

PP

ARR

NPV

IRR, and

Your recommendation

8

Data for the Projects

Project A Project B

Initial investment £100,000 £100,000

Net cash inflows

Year 1 £45,000 £30,000

Year 2 £40,000 £30,000

Year 3 £25,000 £44,000

Year 4 £30,000 £46,000

9

• The depreciation is £20,000 per year.

• The residual value for both projects is the same, £20,000.

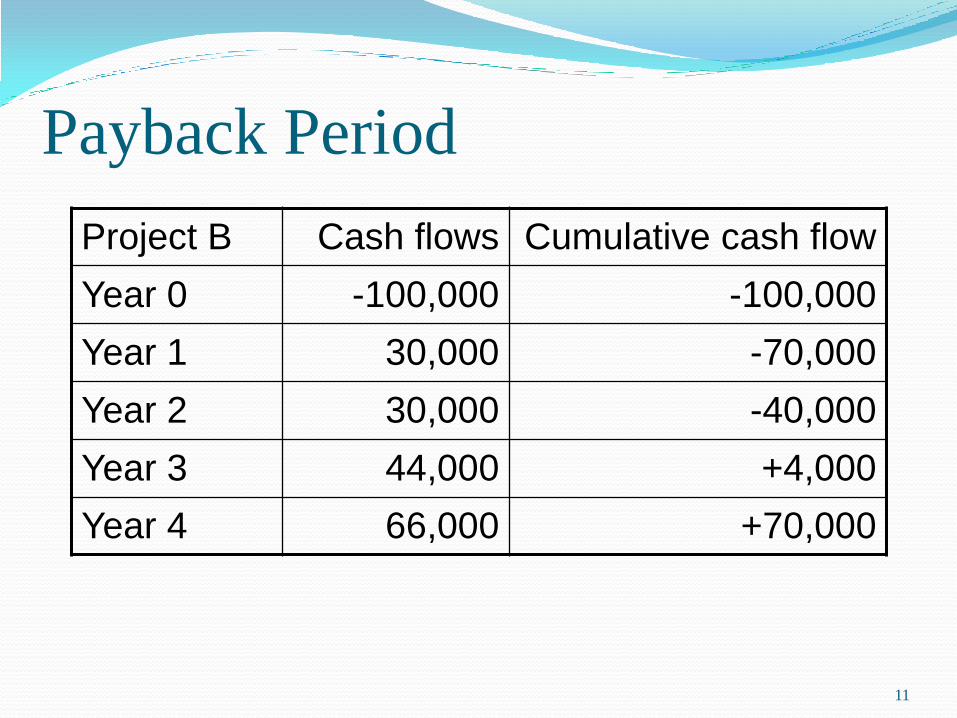

Payback Period The Payback period = the point in time at which

cash flows turn from negative to positive

Project A Cash flows Cumulative cash flow

Year 0 -100,000 -100,000

Year 1 45,000 -55,000

Year 2 40,000 -15,000

Year 3 25,000 +10,000

Year 4 50,000 +60,000

10

Payback Period

Project B Cash flows Cumulative cash flow

Year 0 -100,000 -100,000

Year 1 30,000 -70,000

Year 2 30,000 -40,000

Year 3 44,000 +4,000

Year 4 66,000 +70,000

11

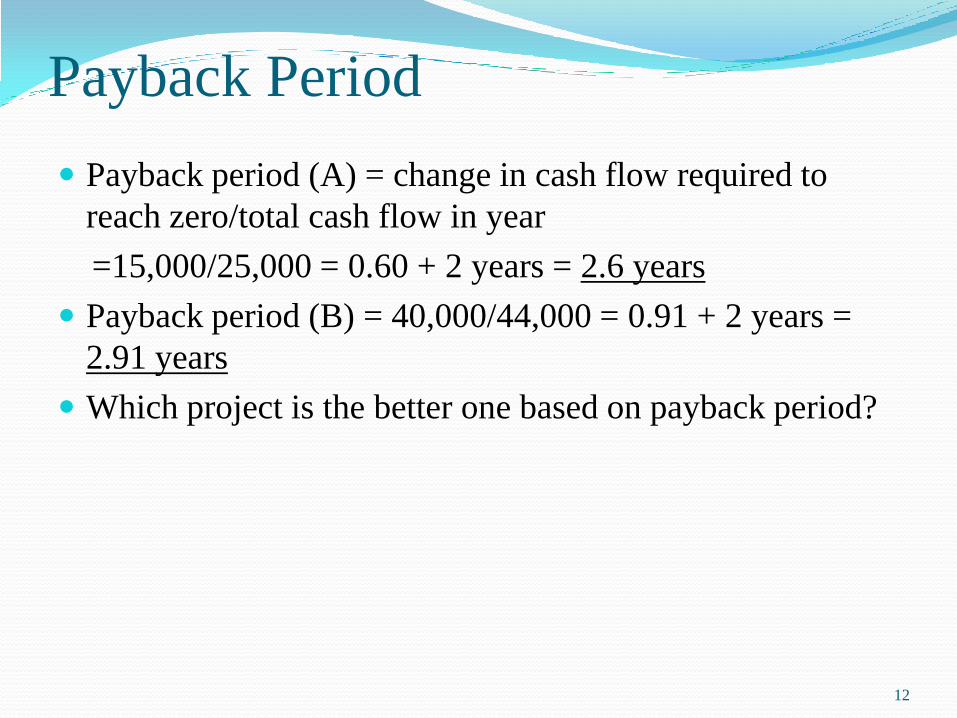

Payback Period

Payback period (A) = change in cash flow required to

reach zero/total cash flow in year

=15,000/25,000 = 0.60 + 2 years = 2.6 years

Payback period (B) = 40,000/44,000 = 0.91 + 2 years =

2.91 years

Which project is the better one based on payback period?

12

ARR Step 1: calculate annual profit

Annual profit = net cash inflow - depreciation

Step 2: calculate average profit

Average profit = total profits / number of years

Step 3: calculate average capital invested

Average capital invested = (initial cost + residual value) /2

Step 4: calculate ARR

ARR = (average profit/average capital invested)x 100%

13

ARR Project A

Average profit = (25,000 + 20,000 + 5,000 + 30,000)/4 =

80,000/4 = 20,000

Average capital invested = (100,000+20,000) /2 = 60,000

ARR = (20,000/60,000)x 100 = 33%

Project B

Average profit = (10,000 + 10,000 + 24,000 + 46,000)/4 =

22,500

Average capital invested = (100,000 + 20,000)/2 = 60,000

ARR = (22,500/60,000) x 100 = 38%

Which project is the better one?

14

The Time Value of Money What is the difference between £1 now and £1 in a year’s

time?

Factors change the value of money

Interest lost (an opportunity cost)

Inflation (loss of purchasing power)

Other risks to materialise the money (the level of demand

for a given project)

15

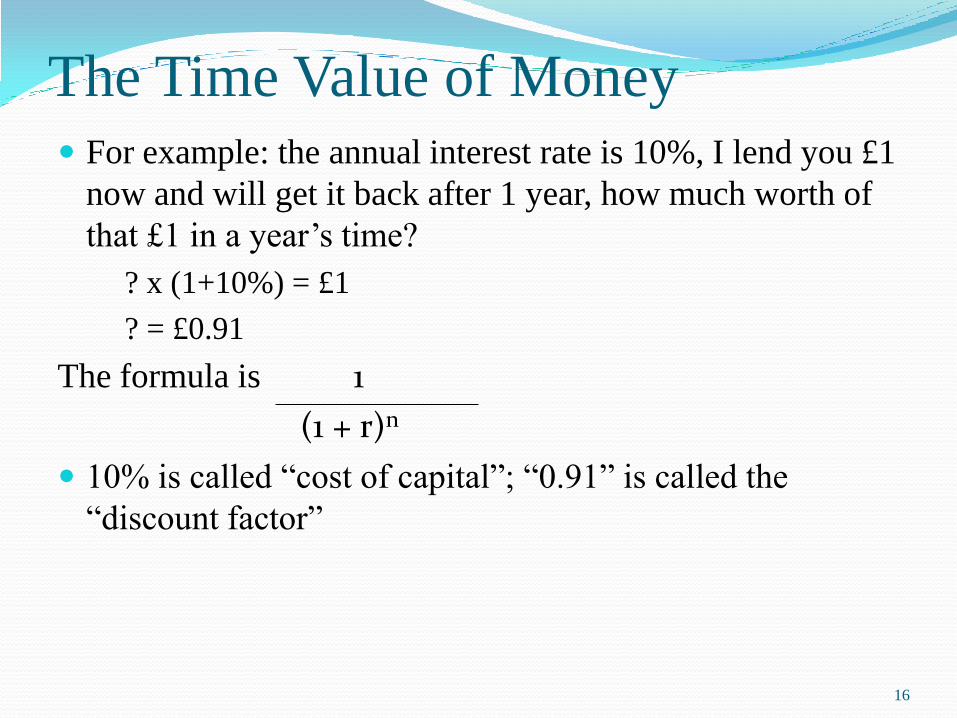

The Time Value of Money For example: the annual interest rate is 10%, I lend you £1

now and will get it back after 1 year, how much worth of

that £1 in a year’s time?

? x (1+10%) = £1

? = £0.91

The formula is 1

(1 + r)n

10% is called “cost of capital”; “0.91” is called the

“discount factor”

16

NPV

Assume that your company’s cost of capital is 10%

Discount factors at 10% are:

Year 1 0.909

Year 2 0.826

Year 3 0.751

Year 4 0.683

Present value table distributed (page 559 in core textbook)

17

NPV

Project A Cash flow Disc. Factor (10%) Dis.d cash flow

Year 0 -100,000 1.00 (100,000)

Year 1 45,000 0.909 40,905

Year 2 40,000 0.826 33,040

Year 3 25,000 0.751 18,775

Year 4 50,000 0.683 34,150

NPV £26,870

18

NPV Project B Cash flow Dis. Factor (10%) Dis.d cash flow

Year 0 -100,000 1.00 (100,000)

Year 1 30,000 0.909 27,270

Year 2 30,000 0.826 24,780

Year 3 44,000 0.751 33,044

Year 4 66,000 0.683 45,078

NPV £30,172

19

• Which project is the better one based on NPV?

IRR IRR: the discount rate that yields net present value of zero

Project A

NPV = £26,870 when the discount rate is 10%

NPV = ? When the discount rate is 25%

Project A Cash flow Dis. factor (25%) Dis.d cash flow

Year 0 -100,000 1.00 (100,000)

Year 1 45,000 0.800 36,000

Year 2 40,000 0.640 25,600

Year 3 25,000 0.512 12,800

Year 4 50,000 0.410 20,500

NPV -5,100

20

IRR Project B

NPV = £30,172 when the discount rate is 10%

NPV = ? When the discount rate is 25%

Project B Cash flow Disc. factor (25%) Dis.d cash flow

Year 0 -100,000 1.00 (100,000)

Year 1 30,000 0.800 24,000

Year 2 30,000 0.640 19,200

Year 3 44,000 0.512 22,258

Year 4 66,000 0.410 27,060

NPV -7,482

21

IRR Project A

Total change in NPV = 26,870 – (-5,100)

= 31,970

Total change in discount rate = 25% -

10% = 15%

IRR = 10% + {(26,870/31,970) x15%} =

23%

22

IRR Project B

Total change in NPV = 30,172 – (-7,482)

= 37,654

Total change in discount rate = 25% -

10% = 15%

IRR = 10% + {(30,172/37,654) x15%} =

22%

23

Project Selection

Methods Single project Choice of projects A or B?

Payback Less than the target

period

Shortest payback

period

A

ARR Above the target

rate

With the highest

ARR

B

NPV A positive NPV With the highest

NPV

B

IRR Higher than the

target rate (cost of

capital)

With the highest IRR A

24

Advantages & Disadvantages

Method Advantages Disadvantages

Payback • Simple and easy to understand and

use

• Objective – using cash flows

• Liquidity – commercially realistic

• Cautious & risk averse – ignores

later cash flows

• Ignores the time value

of money

• Ignores cash flows

after the payback

period

ARR • Simple and easy to understand and

use

• Aids internal and external

comparisons

• Looks at the whole life of the project

•A useful tool to measure divisional

managerial performance

• Subjective – profit,

not cash flows

• Ignores the time value

of money

• Difficulty in use when

with same ARR and

various project sizes

25

Advantages & Disadvantages

Method Advantages Disadvantages

NPV • Takes account of the time value

of money

• Concerns of shareholder wealth

• Takes account of risk

• Looks at the whole life of the

project

• Difficult to be understood

by managers

• Adverse effects on

accounting profits in the

short run

• How to choose discount

rate?

IRR • Takes account of the time value

of money

• Easy to be understood by

managers

• Difficult to use in choosing

projects of varying sizes

• Difficult to choose when

have the same IRR

26

Conclusion Why NPV is more commonly used than ARR and PP?

What are disadvantages of NPV and IRR?

How to overcome disadvantages of NPV and IRR?

What are other factors needed to consider for a long-term investment?

27