Pertamina Energy Outlook 2015 -...

18

PT Pertamina (Persero) Jln. Medan Merdeka Timur No.1A Jakarta 10110 Telp (62-21) 381 5111 Fax (62-21) 384 6865 http://www.pertamina.com “Building world-class refining capacity for Indonesia’s energy needs” Pertamina Energy Outlook 2015 By : Iriawan Yulianto SVP Business Development PT Pertamina (Persero) Jakarta, 3-4 December 2014 CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of Pertamina is strictly prohibited

Transcript of Pertamina Energy Outlook 2015 -...

PT Pertamina (Persero)

Jln. Medan Merdeka Timur No.1A Jakarta 10110

Telp (62-21) 381 5111 Fax (62-21) 384 6865

http://www.pertamina.com

“Building world-class refining capacity

for Indonesia’s energy needs”

Pertamina Energy Outlook 2015

By :

Iriawan Yulianto

SVP Business Development

PT Pertamina (Persero)

Jakarta, 3-4 December 2014

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of Pertamina is strictly prohibited

| PERTAMINA 1

Contents

▪ Strategic Challenges

▪ Refinery Development Master Plan (RDMP)

▪ Grass Root Refinery (GRR)

| PERTAMINA 2

1 Based on UNEP, FACTS and McKinsey analysis 2 Not including new refineries and RDMP initiatives

Pertamina Refining face both external and internal challenges to achieve

its strategic aspiration

Internal challenges

External challenges

▪ SWOT analysis reveal various opportunities for GRM improvement

– There is a need to increase GRM across most RU

– Each RU has different key focus based on their SWOT

▪ Indonesia and ASEAN will be short in gasoline and diesel2, hence potentially requiring

Indonesia to import from sources outside ASEAN

– Indonesia will continue to have growing gasoline and diesel deficit

– ASEAN will also be in deficit for gasoline and diesel

▪ There is government support for increasing domestic production of gasoline and diesel

to limit dependency on imports

Security

of energy supply

▪ Indonesia’s demand for gasoline and diesel will continue to grow significantly

– Gasoline demand will grow by about 8% per year from 2012 to 2025

– Diesel demand will grow by about 5% per year from 2012 to 2025

▪ Product quality specifications will become more stringent in the next 5-10 years1

Refining market

▪ Domestic crude availability will decrease and only able to cover less than 50% of

Pertamina’s total refining capacity

– Domestic crude production is projected to decline by ~27% between 2012 and 2020

– In 2020 domestic crude’s total entitlement volume is only 449 MBD, which is less than 50%

of total refining capacity

▪ Pertamina will increasingly import crudes that are more sour, driving the need to release

sulfur constraints to maintain competitiveness

– In 2020 sour crudes will account for ~77% of the total production capacity for import crudes

– Sour crudes are cheaper than sweet crudes, therefore driving Pertamina’s need to release

sulfur constraints to maintain competitiveness

Feedstock

supply

Refinery

configuration

▪ Going forward refineries will have to increase its complexity and sulfur handling capacity

to become more competitive

STRATEGIC CHALLENGES

| PERTAMINA 3

▪ Indonesia’s domestic product coverage is substantially low compared to other

neighboring countries and can potentially pose a threat in security of fuel products

▪ Increasing the domestic production will increase the domestic fuel product coverage

Indonesia’s domestic fuel product coverage is low, posing risks in

security of energy supply

SOURCE: ICIS Supply & Demand Database; Pertamina M&T (only for Indonesia 2030); Team analysis

103 121 109181

262194

715848 44

Full

coverage

Domestic fuel product coverage1

Percent

1 Production [gasoline, diesel, gasoil] / Demand [gasoline, diesel, gasoil]

2 Assumed 400 KBD refinery at 95% utilization; 50% of the production will be gasoline, diesel and gasoil

3 Assumed 300 KBD refinery at 95% utilization, 67% of production for petroleum products, and 67% of this will be gasoline, diesel and gasoil

2013

2025

93 112 125185

224 206

606338 37

Full

coverage 87

118

PTT/SA2

coverage

RAPID3

coverage

1

IDN AUS VNM MYS CHN THA JPN TWN SGP KOR

| PERTAMINA 4

By 2025, Indonesia faces a significant shortage in refining capacity,

equivalent to ~5-8 refineries

1 Includes gasoline, gas oil and diesel 2 Based on base case demand scenario per Pertamina M&T

3 Assumed each refinery produce 200 KBD of fuel products

Indonesia refinery product supply and demand1

KBD

SOURCE: Pertamina M&T, team analysis

12

2012-13

529

1,050 1,050 1,050

2025

541

529

12

1,681

1,948

2,250

2020

541

529

Existing supply

Low case

Additional supply from RU IV RFCC

Base case

High case

Equivalent

to ~4-8

world-

class

refineries3

6.0%2

0.1%

CAGR

4.9%

3.7%

2

Scenarios

Fuel

subsidy

reduction

GDP

growth

Substitution of

gas/bio-fuel

based vehicles

6% No

change

None High

5% 50%

reduction

B10 Base

4% 100%

reduction

B10 and NGV Low

▪ Estimated shortage by 2025

is between 4 and 8 refineries

– High case: ~1,700 KBD

– Base case: ~1,400 KBD

– Low case: ~1,100 KBD

| PERTAMINA 5

Refining Development Master Plan (RDMP) Grass Root Refinery (GRR)

Pertamina is implementing two programs:

RDMP and GRR to close the deficit

SOURCE: Team analysis

West2

KBD

East3

KBD

1,393

529

X2.5

Supply in 2025 Supply in 2013

1 Base case 2 Region I to IV 3 Region V to VIII 4 Nelson Complexity Index

5 Assumed utilization rate of 95% 6 May be pushed to second phase

5 9

Complexity

NCI4

Fuel product demand1

and supply after RDMP

Current After RDMP

1,136

946 190

1,136

1,273

637

447 190

637

675

38

Total

supply

Demand

in 20251

GRR5 After

RDMP

Supply Demand

Building 2 new refineries to meet west and

east Indonesia’s growing demand Des-

cription

Upgrading 5 existing refineries to increase

the capacity and competitiveness Description

2

KBD

BPP

% MOPS 104 94

| PERTAMINA 6

Contents

▪ Strategic Challenges

▪ Refinery Development Master Plan (RDMP)

▪ Grass Root Refinery (GRR)

| PERTAMINA 7

Pertamina’s Refining Development Master Plan (RDMP) will transform

its refining business by upgrading up to 5 major refineries

SOURCE: Pertamina

Crude flexibility

Sulfur handling limit from

0.4% to ~2% S

~2% S of crude flexibility

Crude quantity

From 820,000 BPD

to 1,610,000 BPD

x2 increased capacity

Product quality

EURO IV up from EURO II

Gasoline from 500 to <50 ppm S

Diesel from 3,500 to <50 ppm S

Complexity

8-9 NCI

Complexity improved

from 5 to 8-9

Dumai refinery

Balikpapan refinery

Plaju refinery

Balongan refinery

Cilacap refinery

PRELIMINARY

| PERTAMINA 8

RDMP strategic partner selection process in currently in progress;

Pertamina would like to sign MOU with strategic partner(s) on Dec 10

SOURCE: Pertamina

1 Request for information

6 companies 13 companies 30 companies 4 companies

Phase 1

(~2021):

MoU sign

on Dec 10

Phase 2

(by 2025):

~400

com-

panies

▪ Balikpapan

▪ Cilacap

▪ Balongan

▪ Dumai

▪ Plaju

Mar, 2014 Jun, 2014 Aug, 2014 Nov, 2014

Preliminary

screening

RFI1

acceptance

RFI response

and roadshow Due diligence Criteria

| PERTAMINA 9

The RDMP landscape across Indonesia would have

different regions in the accelerated scenario

Dumai

Plaju

Balongan Cilacap

Balikpapan

SOURCE: Team analysis

Tuban

XXX

XXX

RDMP

GRR

Sumatra Kalimantan and Sulawesi

West and

Central Java

East Java and

NTT and NTB

| PERTAMINA 10

Pertamina would like to sign an MOU with strategic partner(s) by our

anniversary (Dec 10)

SOURCE: Pertamina

2014

May Jun Jul Aug Sep Oct Nov Dec

Clarification stage

Market sounding

Site visits

Activity

Signed MOU Dec 10th

Partnership decision

Due diligence

Jul 25th: site visits finalized

Jul 25th: response to RFI required

Jun 13th: expression of interest required

Oct 30th: due

diligence finalized

Heads of

Agreement

(Q1 2015)

BFS and partner

selection

(2013-2014)

BED / FEED

(Q2 2015- Q4 2016)

JV Establishment

(Q2 2015- Q4 2016)

Final

Investment

Decision

(Q1 2017)

EPC

(2018-2021)

EPC Contractor

Selection

(Q2-Q4 2017)

| PERTAMINA 11

Contents

▪ Strategic Challenges

▪ Refinery Development Master Plan (RDMP)

▪ Grass Root Refinery (GRR)

| PERTAMINA 12

5 key success factors for a world-class refinery in Indonesia

Suggested guideline Description

Scale and

complexity A

▪ Minimum 300 KBD

▪ Minimum complexity of 10

▪ Fully leverage economies

of scale to be competitive against

imports

Feedstock D

▪ ~60% through long-term

contract at international

market price and ~40% at

spot

▪ Balance between security of supply

and uncertainty on market price

▪ Flexibility to review the terms of

long-term contract

Location B ▪ West Indonesia: Tuban

▪ East Indonesia: TBD

▪ Close to demand center; minimal

exposure to earthquakes

Petchem E

▪ Integrated petrochemical

complex with GRR with

aromatic and olefin

▪ Petrochemical complex integrated

with GRR to boost economics

Land C

▪ Minimum 500 hectare

▪ Government land acquisition

and/or reclamation

▪ Minimum size of land to build an

integrated world-class refinery with

petchem complex

4

| PERTAMINA 13

RU VI Balongan

RU IV Cilacap

MoU with Saudi Aramco on Tuban refinery in West Indonesia

while location is being scouted for East Indonesia

SOURCE: Interim RDMP BFS result, Pertamina, team analysis

1 Includes gasoline and diesel 2 Assumed Region III supplied by Balongan 3 Assumed Region IV and V supplied by Cilacap

Highly attractive

Opportunity exist

Not attractive

RU II Dumai

RU III Plaju

RU V

Balikpapan

2682 -236

504

Region II: South

Sumatra

279 +79

200

Region I: North Sumatra

263

-53

316

Region VI : Kalimantan

Region VII: Sulawesi

312 +39

273 Region VIII: Papua

032-32

RU VII Kasim

Region III: West Java

Demand Supply

East: currently

scouting for

locations in East

Indonesia

4

Supply and base case demand of products1 at 2025 after RDMP, in KBD

1363 -116 252

Region IV: Central Java

West Indonesia East Indonesia

-235 1363 371

Region V: East Java, Bali, NTB & NTT

West: MoU with

Aramco on Tuban

refinery

| PERTAMINA

Grass Root Refinery (GRR) Building World-Class Refining Capacity for Indonesia’s Energy Needs….

SOURCE: Pertamina

Crude flexibility

Sulfur handling limit up to

~2% S

~2% S of crude flexibility

Crude quantity

Can be increased to

400,000 BPD

300,000 BPD

Product quality

EURO IV - V

Gasoline 10 - 50 ppm S

Diesel 10 - 50 ppm S

Complexity

10-12 NCI

World class Complexity

Bontang refinery

Tuban refinery

New Grass Root Refinery in Bontang

with PPP scheme (Government plan)

New Grass Root Refinery in Tuban B to B scheme with

Aramco

| PERTAMINA 15

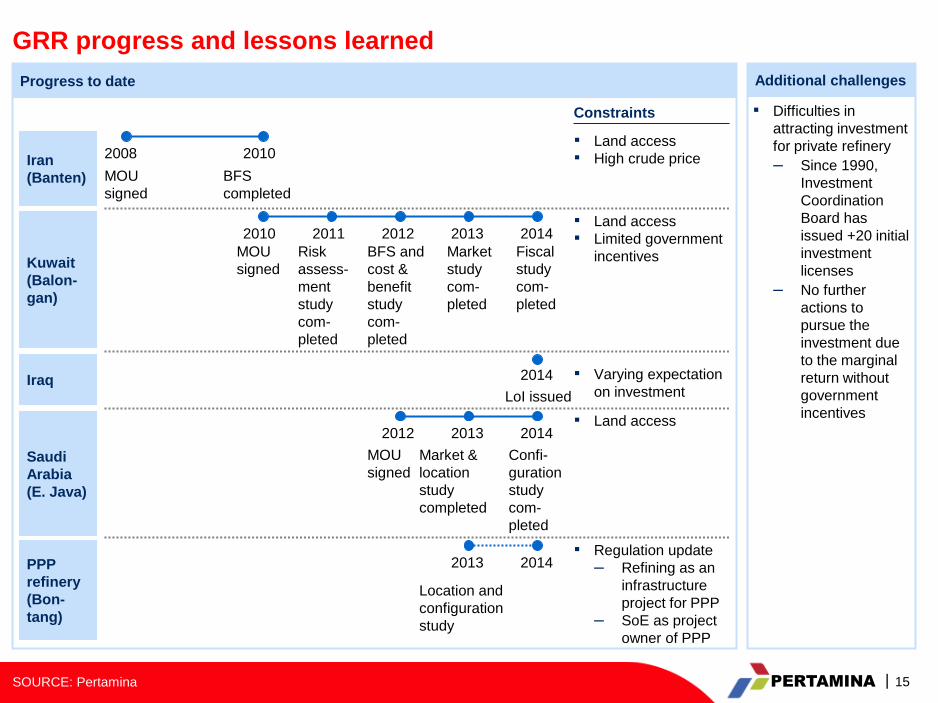

GRR progress and lessons learned

SOURCE: Pertamina

Progress to date Additional challenges

▪ Difficulties in

attracting investment

for private refinery

– Since 1990,

Investment

Coordination

Board has

issued +20 initial

investment

licenses

– No further

actions to

pursue the

investment due

to the marginal

return without

government

incentives

Iran

(Banten)

Constraints

MOU

signed

BFS

completed

2008 2010

Iraq 2014

LoI issued

Kuwait

(Balon-

gan)

MOU

signed

BFS and

cost &

benefit

study

com-

pleted

Market

study

com-

pleted

Fiscal

study

com-

pleted

2010

Risk

assess-

ment

study

com-

pleted

2011 2012 2013 2014

Saudi

Arabia

(E. Java)

MOU

signed

Market &

location

study

completed

Confi-

guration

study

com-

pleted

2012 2013 2014

PPP

refinery

(Bon-

tang)

2014 2013

Location and

configuration

study

▪ Land access

▪ High crude price

▪ Land access

▪ Limited government

incentives

▪ Land access

▪ Regulation update

– Refining as an

infrastructure

project for PPP

– SoE as project

owner of PPP

▪ Varying expectation

on investment

| PERTAMINA 16

Conclusion

▪ RDMP: Upgrading up to 5 existing refineries, equivalent to 2 new refineries

▪ GRR: Building 2 new refineries in Indonesia

▪ World-class strategic partners selected based on rigorous roadshow and due

diligence, signing of MoUs with Aramco, JX, PTT and Sinopec on Dec 10

▪ 2 new refineries pursued in parallel: in West Indonesia, Tuban Refinery with

Aramco; East Indonesian refinery location scouting in progress

▪ Phase 1 commissioning in 2020-2021 for Balongan, Cilacap, and Balikpapan;

Phase 2 commissioning by 2025 for Dumai and Plaju

▪ 5 key success factors for world-class GRR: Scale & complexity, location, land,

feedstock, and integration with petchem complex

2 RDMP

3 GRR

By 2030, Indonesia will need 3-6 new refinery equivalents and Pertamina is

implementing 2 programs to close the gap

1

| PERTAMINA 17

Thank You

These materials have been prepared by PT Pertamina (Persero) together with its subsidiaries, (the “Company”) and have not been independently verified. No representation or warranty, express or implied, is made and no reliance should be placed on the accuracy, fairness or completeness of the information presented, contained or referred to in these materials. Neither the Company nor any of its affiliates, advisers or representatives accepts any liability whatsoever for any loss howsoever arising from any information presented, contained or referred to in these materials. The information presented, contained and referred to in these materials is subject to change without notice and its accuracy is not guaranteed.

These materials contain statements that constitute forward-looking statements. These statements include descriptions regarding the intent, belief or current expectations of the Company or its officers with respect to, among other things, the operations, business, strategy, consolidated results of operations and financial condition of the Company. These statements can be recognized by the use of words such as “expects,” “plan,” “will,” “estimates,” “projects,” “intends,” or words of similar meaning. Such forward-looking statements are not guarantees of future performance and involve risks, uncertainties, and assumptions and actual results may differ from those in the forward-looking statements as a result of various factors. Forward-looking statements contained herein that reference past trends or activities should not be taken as a representation that such trends or activities will necessarily continue in the future. The Company has no obligation and does not undertake to update or revise forward-looking statements to reflect future events or circumstances.

These materials are highly confidential, are being given solely for your information and for your use and may not be copied, reproduced or redistributed to any other person in any manner. Unauthorized copying, reproduction or redistribution of these materials into the U.S. or to any U.S. persons as defined in Regulations under the U.S. Securities Act of 1933, as amended or other third parties (including journalists) could result in a substantial delay to, or otherwise prejudice, the success of the offering. You agree to keep the contents of this presentation and these materials confidential and such presentation and materials form a part of confidential information.

Disclaimer