Perspectives on China Economy and Markets Dr. HUANG Haizhou With input from CICC Macro and Strategy...

25

Perspectives on China Economy and Markets Dr. HUANG Haizhou With input from CICC Macro and Strategy Team January 2014 SFC CE Ref: AMU474 SAC License No. S0080613050003

-

Upload

vincent-boyd -

Category

Documents

-

view

214 -

download

0

Transcript of Perspectives on China Economy and Markets Dr. HUANG Haizhou With input from CICC Macro and Strategy...

Perspectives on China

Economy and Markets

Dr. HUANG HaizhouWith input from CICC Macro and Strategy Team

January 2014

SFC CE Ref: AMU474

SAC License No. S0080613050003

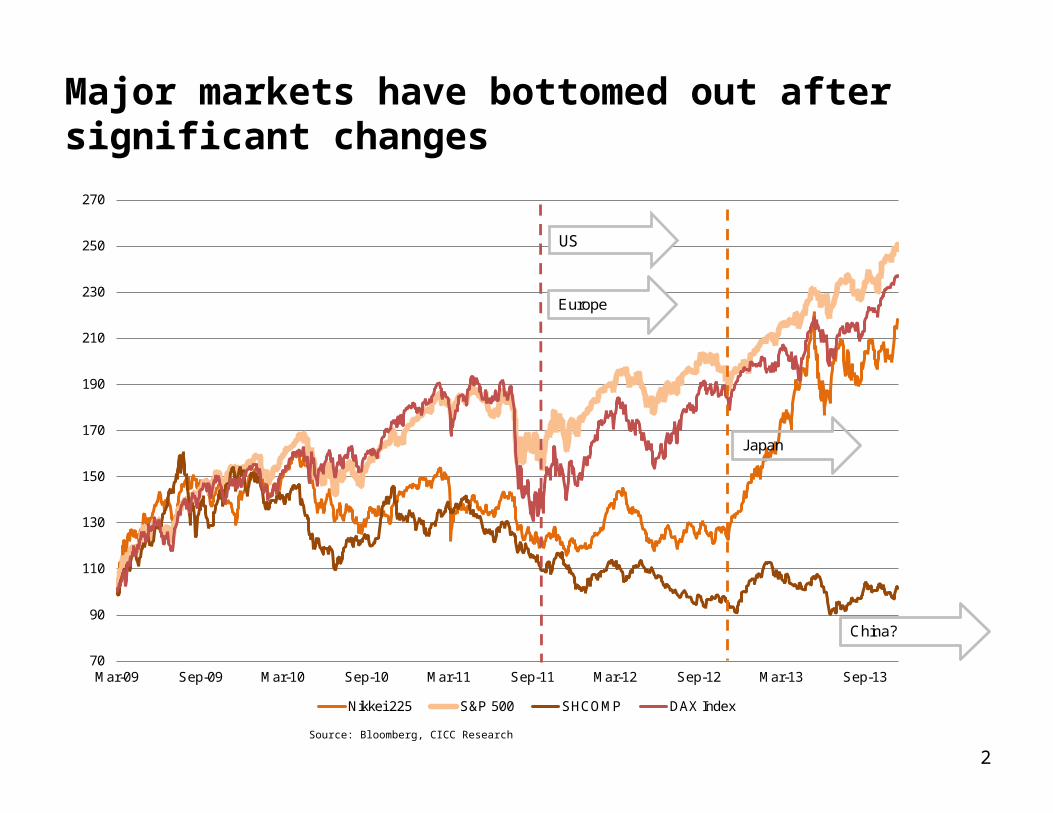

2Source: Bloomberg, CICC Research

70

90

110

130

150

170

190

210

230

250

270

Mar-09 Sep-09 Mar-10 Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13

Nikkei 225 S&P 500 SHCOMP DAX Index

Europe

Japan

China?

US

Major markets have bottomed out after significant changes

Global environment is becoming more supportive: global synchronized recovery in 2014?

3Source: Wind, CICC Research

600

800

1,000

1,200

1,400

1,600

1,800

950

1,950

2,950

3,950

4,950

5,950

Oct-01 Oct-02 Oct-03 Oct-04 Oct-05 Oct-06 Oct-07 Oct-08 Oct-09 Oct-10 Oct-11 Oct-12

SHCOMP Index S&P 500

?

4

Investors have downgraded expectations for the Chinese economy

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

Oct

-07

Nov

-07

Dec

-07

Jan-

08F

eb-0

8M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-08

Jul-0

8A

ug-0

8S

ep-0

8O

ct-0

8N

ov-0

8D

ec-0

8Ja

n-09

Feb

-09

Mar

-09

Apr

-09

May

-09

Jun-

09Ju

l-09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10F

eb-1

0M

ar-1

0A

pr-1

0M

ay-1

0Ju

n-10

Jul-1

0A

ug-1

0S

ep-1

0O

ct-1

0N

ov-1

0D

ec-1

0Ja

n-11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12F

eb-1

2M

ar-1

2A

pr-1

2M

ay-1

2Ju

n-12

Jul-1

2A

ug-1

2S

ep-1

2O

ct-1

2N

ov-1

2D

ec-1

2Ja

n-13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep

-13

Oct

-13

SHCOMP Index and consensus GDP growth

2008 2009 2010 2011 2012 2013 2014 SHCOMP Index (RHS)

(Consensus GDP growth,%)

2008

2009

2010

2011

2012

2013

2014

Source: Wind, Bloomberg, CICC Research

5

We see upside risks to Chinese economy

5

6

7

8

9

10

11

12

13

1,500

1,700

1,900

2,100

2,300

2,500

2,700

2,900

3,100

3,300

3,500

SHCOMP Index and China's GDP growth

SHCOMP Index (LHS) GDP:QoQ

4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3 Q 4Q 1Q 2Q 3Q2008: -65.4% 2009: 80.0% 2010: -14.3% 2011: -21.7% 2012:3.17% YTD:-4.9%

Source: Wind, CICC Research

China: GDP growth

6Source: CEIC, CICC Research

© CICC Macro

6.7 6.9 7.8 9.4 6.7 6.3 8.9 8.0 7.7 7.5 7.0 7.0

8.1

7.6 7.47.8 7.7

7.57.8

7.47.8

8.0

7.57.3

5

6

7

8

9

10

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2012: 7.7% 2013E: 7.6% 2014E: 7.6%

%GDP QoQ GDP YoY

China economy: Supply is not the main bottleneck

777Source: CEIC, CICC Research

-10

-5

0

5

10

15

20

2005 2006 2007 2008 2009 2010 2011 2012 2013

%GDP YoY PPI YoY

888

YoY YoY

-6

-4

-2

0

2

4

6

8

10

Consumers Corporations Property investors

%Real interest rate Nominal interest rate Price growth

Real interest rates diverge for different sectors

Source: CEIC, CICC Research * as of Nov 2013

999

YoY YoY

-20

-10

0

10

20

30

40

2005 2006 2007 2008 2009 2010 2011 2012 2013

%

80

85

90

95

100

105

110

115

1202010=100Delivery Value for Export YoY (LHS)

REER (RHS)

RMB appreciation amplifies negative effects of structural problems on the economy

Source: CEIC, CICC Research

Stabilization in growth

Factors supporting aggregate demand

– Fiscal expansion

– Targeted credit policy

– Property market warms up

Economic growth to stabilize at around 7.5%

– 7.6% for 2013, 7.6% for 2014

– Upside risks

Inflation to remain mild

– CPI : 2.7% for 2013, 3.1% for 2014

1010

Priorities in structural reforms

Opening up: China (Shanghai) Free Trade Zone

Reduce monopoly and promote competition

Tax and fiscal reforms

Interest rate liberalization and opening of the capital account

New urbanization and land reform

Relax family planning policy

1111

12

A-share Strategy: key points

A-share market likely to deliver 20% annual return in 2014.

Macro: 2014 will be different from previous years as:

– Investors have downgraded expectations for the Chinese economy;

– A new round of reforms is likely to improve economic potential, balance and quality; and

– The synchronized recovery of major global economies is likely to last into 2014, boding well for the

Chinese economy.

Earnings: we expect A-share earnings to grow 15.2% 2014 ( top-down);

Valuation & Liquidity: CSI300 valuation at historical low in terms of PE/PB, Small-mid caps’ valuation

at historical high; growth recovery has supported some moderate valuation expansion in large cap index.

Real reforms will arouse revaluation of China.

Sectors:

We suggested buying three types of sectors towards the end of 2013: 1) Real estate, building materials

and steel; 2) Mass consumer goods such as home appliances, foods and beverages; 3) Securities

firms and insurance companies;

Investors should also keep a close eye on the rail, shipping, airline, healthcare and media sectors.

Meanwhile, we remain bearish on base materials (e.g. coal and non-ferrous metals) and sectors with

stretched valuations and a gloomy outlook (e.g. electronic components).

13

2014E top-down earnings should grow by 15.2%

Source: Wind, CICC Research

Earnings forecast: 2012 1~3Q13 2013E 2014E

Top-down:

Non-financials

Revenue growth 7.9 9.6 10.7 12.8

Net margin 4.16 4.39 4.36 4.50

Earning growth -11.8 13.3 12.0 18.0

Financials 13.7 16.5 15.0 13.0

Overall 0.8 15.1 13.7 15.2

Bottom-up

for CSI300 Index 2013E 2014E 2013E 2014E

Non-financials 12.9 16.4 13.0 13.5

Financials 14.7 11.8 15.4 13.1

Overall 14.0 13.6 14.5 13.2

Consensus CICC

CSI300 valuation at historical low

14Source: Wind, CICC Research

0

5

10

15

20

25

30

35

40

45

50

Apr

-05

Jun-

05A

ug-0

5S

ep-0

5N

ov-

05

Jan-

06M

ar-0

6M

ay-0

6Ju

l-06

Sep

-06

No

v-0

6D

ec-

06

Feb

-07

Apr

-07

Jun-

07A

ug-0

7O

ct-0

7D

ec-

07

Jan-

08M

ar-0

8M

ay-0

8Ju

l-08

Sep

-08

No

v-0

8Ja

n-09

Mar

-09

May

-09

Jun-

09A

ug-0

9O

ct-0

9D

ec-

09

Feb

-10

Apr

-10

Jun-

10Ju

l-10

Sep

-10

No

v-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1A

ug-1

1N

ov-

11

De

c-1

1F

eb-1

2A

pr-1

2Ju

n-12

Aug

-12

Oct

-12

De

c-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3S

ep-1

3

CSI 300 CSI 500 SME GEM

Sector allocation: We suggested buying three types of sectors

15Source: Wind, CICC Research

Sub

Cycle

Liquidity

Fiscal policy

Global

economy

Sub

M-L termtrend

Short-termtrend

Policy

Sub

Grow

th

Revision

Stability

Cash flow

Sub

Historical

comparison

Horizontal

comparison

Global

comparison

Sub

Fund

position

Overbought/oversold

Real Estate OW 5 4 4 2 4 3 5 3 5 4 4 4 3 5 1 4 4 3 3 5 5 3

Securities OW 5 5 4 4 4 4 5 4 5 5 5 3 5 3 3 2 2 2 2 3 3 3

Insurance OW 4 3 3 3 4 3 3 3 3 3 5 4 5 4 2 3 5 2 1 3 3 3

Home Appliances OW 5 5 4 4 3 4 4 3 5 3 5 5 4 5 4 4 3 5 5 3 5 2

Food & Beverages OW 5 3 3 4 3 3 4 4 4 2 4 3 3 4 5 5 5 4 4 5 5 4

Construction materials OW 4 4 4 2 4 4 3 1 4 5 3 2 4 3 3 4 4 2 5 4 4 3

Steel OW 4 4 4 2 4 4 2 1 2 5 3 3 3 4 2 5 5 5 4 4 4 3

Environmental services Neutral 5 5 3 3 4 4 5 4 3 5 4 2 2 4 5 2 1 3 2 1 1 3

Auto & Parts Neutral 4 4 3 4 3 3 3 3 4 2 3 3 3 4 3 4 3 5 4 4 5 3

Apparel & Textiles Neutral 4 2 3 3 3 4 3 4 3 2 4 3 3 3 5 5 4 5 5 5 5 3

Railway & Toll roads Neutral 4 4 3 3 4 4 4 3 4 4 3 1 4 4 3 3 3 4 3 2 3 3

Ports & Shipping Neutral 4 4 4 3 3 4 4 2 4 5 3 5 5 1 1 3 3 3 3 2 3 3

Health Care Neutral 3 3 3 3 4 3 5 5 3 4 3 3 3 3 3 1 1 2 1 5 5 3

Airports & Airlines Neutral 3 4 4 3 3 4 3 2 5 2 2 1 5 1 4 4 4 4 3 3 3 3

Retail Neutral 3 3 4 3 3 3 3 3 1 4 3 2 4 5 1 3 2 4 2 5 5 4

Agriculture Neutral 3 3 3 4 3 3 4 3 5 3 2 4 1 3 4 3 2 3 2 5 5 3

Banks Neutral 3 3 3 4 3 3 1 1 1 4 5 2 5 5 2 5 5 5 3 3 3 3

Power Neutral 3 3 4 3 3 3 1 2 3 1 5 5 5 3 4 5 5 4 4 1 1 3

Media & Internet Neutral 3 3 3 3 4 3 4 5 2 2 5 5 4 2 5 1 1 1 1 1 1 4

Tech Equipments Neutral 2 5 3 3 4 4 5 3 4 4 1 2 2 3 3 1 1 3 1 1 1 3

Construction &Engineering

Neutral 2 1 3 2 3 3 2 2 3 3 4 3 3 5 2 5 5 5 5 3 3 3

Travel & Hotel &Restaurant

Neutral 2 2 3 3 3 3 3 3 2 3 2 2 2 2 5 3 2 2 5 5 5 3

Information Services Neutral 2 2 3 3 3 3 4 5 2 3 2 4 2 2 3 2 1 3 4 3 3 4

Oil & Gas Neutral 2 2 3 3 3 4 1 1 5 1 2 1 4 5 1 4 4 4 4 3 3 3

Electrical equipments Neutral 2 3 4 3 3 3 2 3 1 3 2 4 1 1 5 2 3 1 3 2 3 3

Machinery Neutral 2 2 4 2 3 4 3 3 3 3 1 1 1 2 1 2 2 1 3 3 3 3

Chemicals Neutral 1 1 3 2 3 3 2 2 4 1 1 4 1 1 1 1 3 1 1 3 3 3

Light Manufacturing UW 1 2 3 3 3 4 1 2 1 1 4 5 2 2 4 1 1 1 5 2 3 3

Electronic Components UW 1 3 3 3 4 3 2 4 1 2 1 5 1 1 4 2 3 2 2 1 1 3

Coal UW 1 2 3 3 3 4 1 1 1 1 1 1 2 2 2 3 4 3 2 3 3 3

Non-ferrous metals UW 1 2 3 3 3 4 1 1 2 1 1 1 1 1 2 1 2 1 1 4 3 3

Valuation Technical

SectorSector

Weighting

Macro Sector Earnings

Score

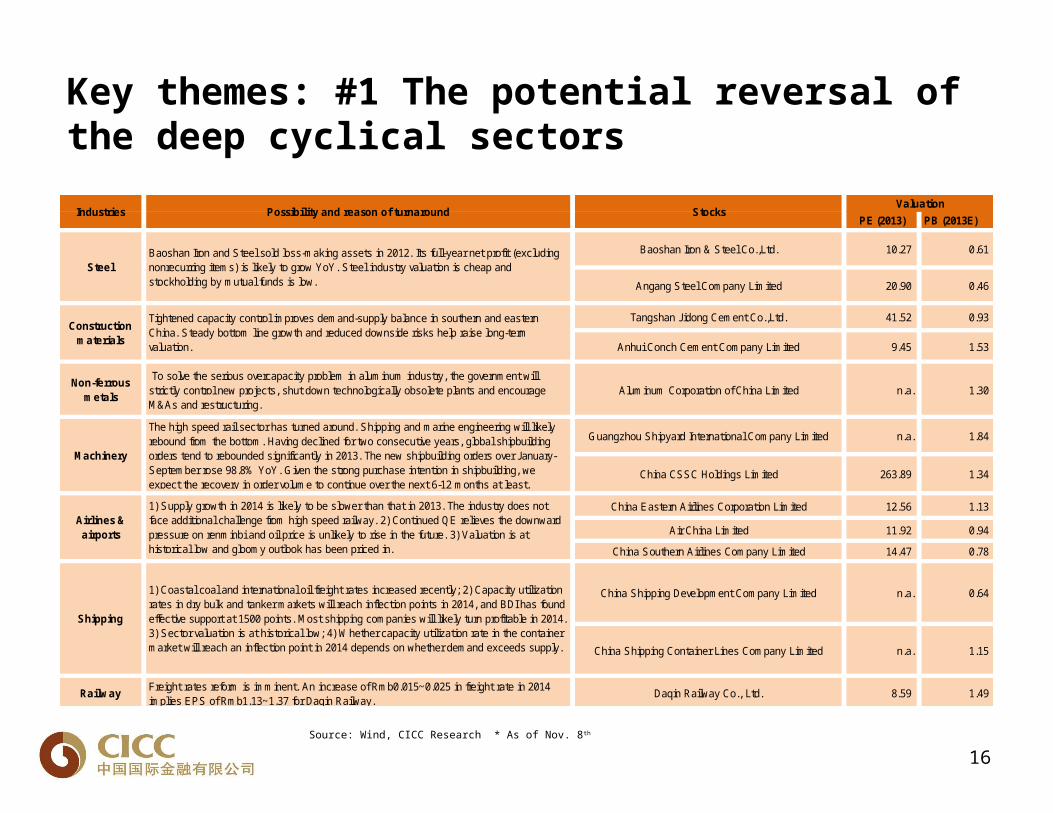

Key themes: #1 The potential reversal of the deep cyclical sectors

16Source: Wind, CICC Research * As of Nov. 8th

PE (2013) PB (2013E)

Baoshan Iron & Steel Co.,Ltd. 10.27 0.61

Angang Steel Company Limited 20.90 0.46

Tangshan Jidong Cement Co.,Ltd. 41.52 0.93

Anhui Conch Cement Company Limited 9.45 1.53

Non-ferrousmetals

To solve the serious overcapacity problem in aluminum industry, the government willstrictly control new projects, shut down technologically obsolete plants and encourageM&As and restructuring.

Aluminum Corporation of China Limited n.a. 1.30

Guangzhou Shipyard International Company Limited n.a. 1.84

China CSSC Holdings Limited 263.89 1.34

China Eastern Airlines Corporation Limited 12.56 1.13

Air China Limited 11.92 0.94

China Southern Airlines Company Limited 14.47 0.78

China Shipping Development Company Limited n.a. 0.64

China Shipping Container Lines Company Limited n.a. 1.15

RailwayFreight rates reform is imminent. An increase of Rmb0.015~0.025 in freight rate in 2014implies EPS of Rmb1.13~1.37 for Daqin Railway.

Daqin Railway Co., Ltd. 8.59 1.49

Shipping

1) Coastal coal and international oil freight rates increased recently; 2) Capacity utilizationrates in dry bulk and tanker markets will reach inflection points in 2014, and BDI has foundeffective support at 1500 points. Most shipping companies will likely turn profitable in 2014.3) Sector valuation is at historical low; 4) Whether capacity utilization rate in the containermarket will reach an inflection point in 2014 depends on whether demand exceeds supply.

Constructionmaterials

Tightened capacity control improves demand-supply balance in southern and easternChina. Steady bottom line growth and reduced downside risks help raise long-termvaluation.

Machinery

The high speed rail sector has turned around. Shipping and marine engineering will likelyrebound from the bottom. Having declined for two consecutive years, global shipbuildingorders tend to rebounded significantly in 2013. The new shipbuilding orders over January-September rose 98.8% YoY. Given the strong purchase intention in shipbuilding, weexpect the recovery in order volume to continue over the next 6-12 months at least.

Airlines &airports

1) Supply growth in 2014 is likely to be slower than that in 2013. The industry does notface additional challenge from high speed railway. 2) Continued QE relieves the downwardpressure on renminbi and oil price is unlikely to rise in the future. 3) Valuation is athistorical low and gloomy outlook has been priced in.

Industries Possibility and reason of turnaround StocksValuation

SteelBaoshan Iron and Steel sold loss-making assets in 2012. Its full-year net profit (excludingnonrecurring items) is likely to grow YoY. Steel industry valuation is cheap andstockholding by mutual funds is low.

Key themes: #2 SOE Reforms

17Source: Wind, CICC Research

Six major issues mentioned in Xi’s Wuhan speech in July

The four key aspects of SOE reforms

• Administrative monopoly to be reduced, and SOEs to face more competition from private businesses

•Make full use of domestic and international markets to utilize excessive capacity and to build world-class brands

• Change targets, enhance efficiency, dispose of non-core assets, establish incentive schemes & diversify ownership structure

•Refocus resources to key areas and refrain from others

Business focus

Incentive and

discipline

More competition

Global vision

Comprehensive reforms require in-depth

investigation of six issues

1) Accelerate the formation of a unified, open,

competitive and orderly market

system

2) Enhance the public sector's

economic development:

encourage, support and guide the private

sector's economic development

3) Improve macroeconomic

regulation; improve the efficiency and effectiveness of

government

4) Enhance social development; promote social

harmony and stability

5) Achieve social fairness and justice; safeguard people's

rights

6) Improve the party's leadership and governance capabilities; play

overview coordinating role

Key themes: #3 M&As

18Source: Wind, CICC Research

0

20

40

60

80

100

120

140

160

180

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Traditional industries Emerging industries FinancialsUSDbn

0%

2%

4%

6%

8%

10%

12%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

China USADeal value/GDP

Key themes: #4 Wireless Internet Applications

19Source: Wind, CICC Research

0

100

200

300

400

500

600

700

China Internet Users

Mobile Internet Users

Million

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200

400

600

800

1,000

1,200

1,400

Market size: Online shopping

Network utilization rate:online shopping (RHS)Rmb bn

20

~20% H-share upside in 2014The H-share market has lost 2% YTD, lagging behind global peers. We expect the HSCEI to rise ~20% to 12,500 by end-2014, with a ~13% contribution from earnings revisions and a ~7% boost from valuation expanding to 9.5x 12-month forward P/E

Macro: Reforms to improve growth qualityWe believe domestic growth will stabilize and downside risk is relatively limited. Our economists expect GDP growth is 7.6% in 2014, with a higher contribution from consumption . The expediting of reforms would enhance growth quality and raise medium- to longer-term growth potential

Earnings: Growth recovery to extendWe forecast H-share earnings to grow 14% in 2013 and accelerate to 15% in 2014. Non-financial earnings could grow 16% in 2014 thanks to higher top-line and a small expansion in profit margin; and financials are to deliver ~13% growth.

Valuation: ERP normalization to re-rate marketCurrent valuations of appear subdued relative to the historical range and global peers. We expect stabilizing domestic growth, mounting reform dividends and potential global tailwinds to help reduce H-share equity risk premium and prompt a moderate valuation expansion.

Implementation: Sector preference and top-picksFocus on growth visibility and reform beneficiaries, and overweight select financials (real estate and brokers), select infrastructure (construction and city utilities), and select consumption (internet/software, healthcare, auto and home appliance); underweight telecom, coal, retail, apparel/textile and power. Continue to recommend our thematic baskets of new urbanization and environmental protection.

RisksFor China, we watch financial system risks, cyclical growth momentum, reform execution etc.; from overseas, key issues include US fiscal impasse and Fed’s policy.

H-share Strategy: key points

2014 earnings to grow 15% on higher sales and profit margin

2121

Non-financial and financials earnings would growth 16% and 13% in 2014 respectively Non-financial top-line sales growth to expand thanks to higher 2014 nominal GDP growth estimated by our

economists Two drivers to potentially nudge-up non-financials profit margins in 2014: 1) subdued domestic commodity

prices and a more valuable Rmb; and 2) better operating efficiencyWe are looking for 15% earnings growth in 2014, thanks to ~16% growth in non-financials and ~13% growth for financial

companies

Sales Growth

Net Margin

Net Income Growth

Net Income

Consensus

Revision from Now

2011A Non-finan. 27% 7.2% 8%Financials 28%H-share 16%

2012A Non-finan. 11% 5.9% -9%Financials 15%H-share 1%

2013E Non-finan. 10% 6.1% 13% 15% -1%Financials 15% 16% -1%H-share 14% 14% -0%

2014E Non-finan. 11% 6.4% 16% 15% 1%Financials 13% 9% 4%H-share 15% 11% 3%

CICC Top-down Forecast vs. Consensus

Source: Bloomberg, FactSet, MSCI, CICC Strategy Research

ERP reduction to unlock value and induce valuation normalization

2222

Improving cyclical momentum and mounting reform dividends, as well as a potential global ERP reduction, to somewhat alleviate concerns about medium-/long-term growth

We expect ERP to narrow 0.5ppt from the current 7% to 6.5% by end-2014 Based on our 3-stage DDM and assuming China’s 10-year government bond yield is 4.3% at end-2014, the

corresponding end-2014 target 12-month forward P/E is ~9.5x, implying a 7% expansion

MSCI China has returned 20.5% since June 25, with a forward P/E expansion of 16.8% and forward EPS upgrade of 3.3%

We estimate 9~12x as the fair range for H-shares based on our 3-stage DDM

Source: Bloomberg, FactSet, MSCI, CICC Strategy ResearchSource: Bloomberg, FactSet, MSCI, CICC Strategy Research

6.0

6.3

6.6

6.9

7.2

7.5

90

100

110

120

130

140

Apr-12 Jun-12 Aug-12 Sep-12 Nov-12 Jan-13 Feb-13 Apr-13 Jun-13 Jul-13 Sep-13 Nov-13

(HK$)(Rebased) 12m forward EPS (RHS) 12m forward P/E MSCI China

MSCI China

12m fwd P/E

12m fwd EPS (HK$)

2013/11/6 61.8 8.9x 6.952013/6/25 51.3 7.6x 6.73

Change 20.5% 16.8% 3.3%

MSCI China

12m fwd P/E

12m fwd EPS (HK$)

2013/6/25 51.3 7.6x 6.732013/1/4 65.4 10.4x 6.28Change -21.6% -26.8% 7.2%

MSCI China

12m fwd P/E

12m fwd EPS (HK$)

2013/1/4 65.4 10.4x 6.282012/9/5 51.6 8.5x 6.10Change 26.8% 23.2% 3.0%

6

8

10

12

14

16

18

8.0% 8.5% 9.0% 9.5% 10.0% 10.5% 11.0% 11.5% 12.0% 12.5% 13.0%

Cost of equity

12

-mo

nth

fo

rwa

rd P

/E (

X)

9~12x the fair forward P/E range

Cost of equity sensitivity based on our MSCI China 3-stage DDM

Focus growth visibility & reform beneficiaries

2323

We continue to focus on growth visibility and reform beneficiaries in our sector picks. We suggest overweighting real estate and brokers, construction and city utilities and internet/software, healthcare, autos, home appliances, and underweighting telecoms, coal, retail, apparel/textiles, chemicals and power

5 year rolling

Growth visibility Reform impactValuation Z-Score

Software & Services OW OW 7.5 29.6 13.0 ↑ ↑ 0.9

Real Estate OW OW 6.3 5.4 1.3 ↑ -0.7

Capital Goods OW OW 3.9 10.1 1.2 ↑ (construction) -0.1

Auto & Parts OW OW 3.2 11.3 2.5 ↑ (mid-/low tier) ↓ (luxury) 0.4

City Utilities OW Neutral 1.6 16.1 3.0 ↑ ↑ 0.5

Health Care OW Neutral 1.3 16.6 2.4 ↑ -0.4

Diversified Financials OW OW 0.9 13.3 1.2 ↑ -0.4

Home Appliance OW OW 0.2 14.2 5.4 ↑ ↑ 1.2

Banks Neutral Neutral 24.6 5.2 1.1 ↓ -1.2

Oil & Gas Neutral Neutral 12.4 8.6 2.0 ↑ (clean energy) ↓ (oil majors) -0.4

Insurance Neutral Neutral 7.5 12.8 2.0 ↑ -1.0

Consumer Staples Neutral Neutral 6.0 24.2 4.0 ↑ ↑ 0.6

Transportation Neutral Neutral 2.1 15.9 1.2 0.1

Hardware Neutral Neutral 1.8 14.7 2.1 ↑ -0.0

Cement Neutral Neutral 1.4 7.6 1.3 -0.7

Metals & Mining Neutral UW 1.2 18.2 0.9 ↓ -0.0

Paper Neutral Neutral 0.4 11.5 1.3 ↓ 0.1

Telecoms UW UW 10.9 11.0 1.5 ↓ ↓ -0.5

Coal UW UW 2.3 8.9 1.1 ↓ -0.6

Power UW Neutral 1.8 9.6 1.5 ↓ (coal-fired) -1.0

Retail UW UW 1.7 13.7 2.1 ↓ -0.8

Apparel & Textile UW UW 0.6 12.8 2.4 ↓ 1.2

Chemicals UW UW 0.4 10.8 1.4 ↓ -0.2

Why we OW/UW

Sector

CICC strategy

2014 preference

Previous preference

Sector weights

(%)

12m forward P/E (X)

12m trailing P/B (X)

Source: Bloomberg, Datastream, I/B/E/S, MSCI, CICC Strategy Research. Note: Based on MSCI China index constituents and GICS sector classifications; valuations are consensus estimates.

24 24

Source: CEIC, CICC Research

The long-term potential output will be driven by reform and opening-up

© CICC Macro

Disclosures

This document has been produced by China International Capital Corporation Limited, which is regulated by China Securities Regulatory Commission. This document is based on information available to the public that we consider reliable, but China International Capital Corporation Limited and its associated company(ies)(collectively, hereinafter “CICC”) do not represent that it is accurate or complete. The information and opinions contained herein are for investors’ reference only and do not take into account the particular investment objectives, financial situation or needs of any client, and are not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned. Under no circumstances shall the information contained herein or the opinions expressed herein constitute a personal recommendation to anyone. Investors are advised to make their own independent evaluation of the information contained in this document, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this document. Neither CICC nor its related persons shall be liable in any manner whatsoever for any consequences of any reliance thereon or usage thereof.The performance information (including any expression of opinion or forecast) herein reflect the most up-to-date opinions, speculations and forecasts at the time of the document’s production and publication. Such opinions, speculations and forecasts are subject to change and may be amended without any notification. Past performance is not a reliable indicator of future performance. At different periods, CICC may release reports which are inconsistent with the opinions, speculations and forecasts contained herein.CICC’s salespeople, traders, and other professionals may provide oral or written market commentary or trading ideas that may be inconsistent with, and reach different conclusions from, the recommendations and opinions presented in this document. Such ideas or recommendations reflect the different assumptions, views and analytical methods of the persons who prepared them, and CICC is under no obligation to ensure that such other trading ideas or recommendations are brought to the attention of any recipient of this document. CICC’s asset management area, proprietary trading desks and other investing businesses may make investment decisions that are inconsistent with the recommendations or opinions expressed in this document.This document may is distributed in Hong Kong by China International Capital Corporation Hong Kong Securities Limited (“CICCHKS”), which is regulated by the Securities and Futures Commission. This document may is distributed in Singapore only to accredited investors and/or institutional investors, as defined in the Securities and Futures Act and Financial Adviser Act of Singapore, by China International Capital Corporation (Singapore) Pte. Limited (“CICCSG”), which is regulated by the Monetary Authority of Singapore. By virtue of distribution by CICCSG to these categories of investors in Singapore, disclosure under Section 36 of the Financial Adviser Act (which relates to disclosure of a financial adviser’s interest and/or its representative’s interest in securities) is not required. Recipients of this document in Singapore should contact CICCSG in respect of any matter arising from or in connection with this document.This document may is distributed in the United Kingdom by China International Capital Corporation (UK) Limited (“CICCUK”), which is authorised and regulated by the Financial Conduct Authority. The investments and services to which this report relates are only available to persons of a kind described in Article 19 (5), 38, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005. This report is not intended for retail clients. In other EEA countries, the report is issued to persons regarded as professional investors (or equivalent) in their home jurisdiction.. This document may also be made available in other jurisdictions pursuant to the applicable laws and regulations in those particular jurisdications. Special DisclosuresCICC may have positions in, and may effect transactions in securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies. Investors should be aware that CICC and/or its associated person may have a conflict of interest that could affect the objectivity of this document. Investors are not advised to solely rely on the opinions contained in this document before making any investment decision or other decision.Copyright of this document belongs to CICC. Any form of unauthorized distribution, reproduction, publication, release or quotation is prohibited without CICC’s written permission.

25