Perspective on Canadian Gas Pipeline ROEs - Cepa.com€¦ · Perspective on Canadian Gas Pipeline...

25

Perspective on Canadian Gas Pipeline ROEs February 2008

Transcript of Perspective on Canadian Gas Pipeline ROEs - Cepa.com€¦ · Perspective on Canadian Gas Pipeline...

Perspective on Canadian Gas Pipeline ROEs

February 2008

Scope This document outlines key facts and views regarding return on equity (ROEs) on Transmission

Pipelines in Canada, with a specific focus on gas pipelines. It has been prepared by the

Canadian Energy Pipeline Association (CEPA) to support engagement and discussion of ROE

issues amongst CEPA members who are operating natural gas transmission systems and with

associated policy makers, regulators and stakeholders.

2

Summary Several Canadian regulatory jurisdictions have in existence similar formulas to determine

allowed rates of return on common equity (ROEs) for utility and pipeline assets. While there is

merit (eg. efficiency, link to debt markets) in using a formula approach to ROE, the ROEs that

result from the current formulas are too low, causing unfair returns. This paper, which is

focused on ROEs for natural gas transmission pipelines, provides the facts supporting this

position, and other background information to generate discussion on this topic.

The background information provided includes the legal obligation for regulators to provide fair

returns on invested capital, the methods that can be used to estimate an appropriate ROE, and

the ROE formulas currently in place.

The following facts are presented to support the position that gas pipeline ROEs are too low:

• U.S. and Canadian gas pipelines had similar ROEs at the time ROE formulas came into

use, but now U.S. gas pipelines have much higher ROEs, despite a relative increase in

the business risk of Canadian gas pipelines;

• U.S. local gas distribution companies (LDCs) had similar ROEs at the time ROE

formulas came into use, and now U.S. LDCs have much higher ROEs despite being less

risky;

• ROEs contractually negotiated for Canadian pipelines are consistently higher, and the

difference is likely greater than can be accounted for by additional risks inherent to

negotiated settlements;

• Analysis of Canadian stock market data shows that investors expect higher returns; and

• Since the ROE formulas were originally adopted, capital markets have changed in ways

that have led investors to require higher equity returns than those resulting from single-

variable ROE formulas.

To assist the discussion, this paper also addresses some common challenges to the assertion

that ROEs are too low.

CEPA intends this paper to be complementary to a paper issued by the Canadian Gas

Association (CGA) in May 2007. The CGA’s paper addresses ROEs from the perspective of

3

natural gas LDCs. CGA members also have formula-generated ROEs, and suffer from unfair

rates of return as a result.

Background

Who is the Canadian Energy Pipeline Association (CEPA)?

CEPA represents Canada's energy transmission pipeline companies. Its members transport

97% of Canada's daily crude oil and natural gas production from producing regions to markets

throughout Canada and the U.S. CEPA members operate over $20 billion in assets and project

$1 billion per year of capital investments over the next 2 decades. Collectively, total assets are

projected to double over the next 15 years in order to meet the needs of energy producers and

consumers. In order to ensure that the Canadian gas pipeline industry continues to be

maintained and expanded to meet these needs, sufficient returns are required on capital

invested.

The Fair Return Standard

Regulators allow the recovery of all prudently incurred and reasonable costs required to provide

service. These costs include the cost of capital employed, for which regulators are required to

provide a fair return. The “fair return standard” is based on court rulings on cost of capital

matters, and has three elements. A return is fair if 1) it enables the utility to attract capital on

reasonable terms, 2) maintains the financial integrity of the regulated entity, and 3) is

comparable to the returns available to enterprises of similar risk.

The fair return standard is not only a legal requirement but it is also based on sound economic

theory. It ensures that necessary regulated systems remain financially healthy and that its

investors are compensated appropriately and equitably.

The first two parts of the fair return standard, capital attraction and financial integrity, are related

but distinct tests. The capital attraction standard ensures the regulated entity can attract the

capital it requires to grow and maintain its system. The financial integrity standard requires that

the return allowed be sufficient to assure confidence in the financial soundness of the regulated

4

entity. In approving a cost of capital, regulators must consider the financial soundness of the

regulated entity and the risk that it could be unable to attract capital on reasonable terms. This

should have nothing to do with the ownership of the regulated entity. The company which owns

the regulated entity may be stronger or weaker financially, and may have more or less difficulty

raising capital than the regulated entity would. To address this, regulators follow the “stand-

alone principle” whereby cost of capital decisions are made for the regulated entity as if it were

a stand alone company. i In other words, the regulator asks how financially sound the regulated

entity is and whether it could raise capital on its own; the financial soundness and ability of the

parent company to raise capital are irrelevant.

The third part of the fair return standard, that the return be comparable to that of entities with

similar risk, has clearly not been met in recent decisions. Too often regulators have used

differences between comparators as reasons not to compare rather than as considerations in

how to compare. Regulators have rejected comparison to US pipelines,ii oil pipelines,iii or to

pipelines who have negotiated their rates through settlement agreements.iv There are few

sources for comparators, and it is circular to compare to other pipelines whose returns are also

based on an ROE generated the same way. Thus, where differences exist, the onus is on

regulators to exercise reasoned judgment and consider differences while making comparisons.

Otherwise, the fair return standard, which legally requires comparisons, is not met.

The fair return standard applies to the overall cost of capital, comprised of the cost of debt and

the cost of equity. This paper focuses on ROE because debt rates are rarely contentious,

equity ratios have been deemed by Canadian regulators based on individual business risks, and

since ROEs are set by formulas which apply to many pipelines.

Methods of Estimating an Appropriate ROE

Setting an appropriate ROE is a challenge that requires regulators to not only understand and

measure risk, but to put a price on risk differences based on an understanding of how risk is

being priced in the capital market. Academics do not agree on a single method or test to

determine an appropriate ROE. They have a number of methods to estimate the cost of capital,

each with its own underlying theory and its own unique shortcomings. Estimating an

appropriate ROE with any of these methods involves the challenge of gathering an appropriate

sample. While the results of all methods have been considered by regulators in the past, the

5

most recent EUB and NEB decisions have relied primarily or solely on Equity Risk Premium

(ERP) based methods.v, vi

The methods of estimating cost of capital fall in three broad categories: the Comparable

Earnings (CE), Discounted Cash Flow (DCF), and Equity Risk Premium methods. The CE

method compares the actual ROEs earned by companies with comparable risk. While this

method relies on accounting data which can be affected by accounting concepts such as

accruals and gains and losses on sales, it is a straight-forward application of the comparable

return standard.

The DCF method is universally accepted in the U.S. and universally given little or no weight in

Canada recently. It is based on the constant dividend growth model and the theory that the

appropriate cost of equity is the risk-adjusted discount rate applied to dividends to obtain the

current value of a stock. The formula is;

This formula is then rearranged to back-out an estimate of the ROE from data on the current

stock price, expected dividends, and the projected growth rate. After selecting a sample, the

main challenge of this method is determining estimates of future growth rates. These estimates

normally rely on economic growth forecasts and dividend growth forecasts published by equity

analysts. One advantage of this method is that investors and investment analysts routinely use

the formula above in making valuations. The DCF method is also a forward-looking test, unlike

most other tests.

The ERP method determines an ROE as the sum of a risk-free rate of return plus a risk

premium. The theory is that the risk-free rate of return compensates investors for the time value

of money while the risk premium compensates for any additional amount of risk. The Capital

Asset Pricing Model (CAPM) is the traditional ERP model, and is represented by the following

formula:

Rate Growth - ROE per Expected sYear' NextPrice =

Dividends unit

6

MRPRF ROE += ×β

where RF is the risk-free rate of return, MRP is the market risk premium which is the market-

determined price for the average amount of risk, and β is the entity’s risk relative to the average

market risk. The unique challenge with this CAPM method is estimating β and the MRP through

statistical analysis of stock market data.

A relatively new ERP method is the Fama-French model. It is based on evidence that the

CAPM model underestimates the return on equity for low beta stocks and for high value stocks

(stock with a low market to book ratio).vii These biases of the CAPM model would cause an

underestimation of the appropriate ROE for a Canadian gas pipeline. To correct for these

biases in the CAPM model, the Fama-French model adds variables for company size and

company value to the traditional CAPM model. The formula for this method is;

βα += SMBRF-ROE 1 εβ ++ HML2

where

α is the abnormal returns of the company’s stock;

SMB is the size factor (small market capitalization returns minus big market

capitalization returns);

HML is the book-to-market factor (high B/M returns minus low B/M returns);

β1 and β2 are the respective sensitivities of stock to the SMB and HML risk factors;

and

ε is the diversifiable or firm specific risk.

Another approach to estimating cost of equity that can be combined with these methods is the

After-Tax Weighted Average Cost of Capital (ATWACC) method. It is based on the premise

that the overall after tax cost of capital is constant over a wide range of capital structures.

Based on this premise, either an ATWACC should be approved by the regulator or ROE and

capital structure should be considered together, not in isolation, to result in a fair return.

ATWACC’s are a real-world measure, since businesses consider whether the ATWACC of a

project is above or below a hurdle rate of return when considering whether or not to proceed

with that project.

7

There are many methods and variations of methods which can be used to estimate the cost of

capital. However, when parties prepare evidence for a cost of capital proceeding, they typically

present a method that has been accepted in the past. If new methods are disregarded because

they are new, regulators will end up with a very narrow, and possibly outdated view when

evaluating cost of capital evidence.

Current ROE Formulas

The British Columbia Public Utilities Commission (BCUC) was the first Canadian regulator to

establish a formula ROE and was followed by the NEB and three other provincial regulators.

These regulators use virtually identical ERP-based formulas to set approved ROEs each year

by adjusting the previous year’s ROE by a proportion of the change in the forecast long-term

Government of Canada bond yields (a measure of the risk-free rate of return). The table below

provides the results of these formulas in 2007 and 2008, which are very similar, and average

8.51% in 2007 and 8.78% in 2008.

Approved Formula ROEs

Jurisdiction Formula

Implemented 2007 ROE 2008 ROE

National Energy Board 1995 8.46% 8.71% Alberta Energy and Utilities Board 2004 8.51% 8.75% British Columbia Utilities Commission 1994 8.37% 8.62%

Enbridge 1997 8.41% not availableOntario Energy Board Union 1997 8.54% not available

Québec régie de l'énergie for Gaz Métro 1999 8.76% 9.05%

As bond yields have dropped, so have the formula generated ROEs. The ROE in the 1995

base year of the NEB Formula was 12.25%, and has fallen by 379 basis points relative to 2007.

The ROE awarded for the 2004 base year of the EUB formula was 9.60%, and has fallen by 109

basis points relative to 2007.

8

Growing Gap Relative to U.S. ROEs Formula ROEs have dropped in Canada, while gas pipeline ROEs approved by the U.S.

Federal Energy Regulatory Commission (FERC) have not, as shown below.

NEB Formula vs U.S. Gas PipelinesROE

8.71%

8.46%

8.88%

9.46%9.56%9.79%

9.53%

9.61%

9.90%

9.58%

10.21%

10.67%

11.25%

12.25%

8%

9%

10%

11%

12%

13%

14%

15%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

NEB Formula ROE US ROEs (FERC Approved Litigated Cases) US ROEs (FERC Approved Settlement Cases)

Source: FERC Decisions

Over this time period, Canadian pipelines have faced increasing risks as they have entered a

competitive age and faced increased supply risk, while U.S. gas pipelines have not faced such

structural changes. In any event, it would be difficult to argue that U.S. gas pipelines have

experienced an increase in relative risk since 1995.

U.S. gas pipeline ROEs are relevant for comparison. Markets continue to globalize, and

investors can now switch their investments between Canada and the U.S. as easily as switching

between sectors within the same country. There are also no material differences in fiscal or

monetary policy to affect comparability. In other words, higher ROEs are easily available to

Canadian investors who invest in U.S. gas pipelines instead of Canadian gas pipelines.

Comparison to U.S. regulated entities is logical since they a have similar regulatory model.

9

Whether subject to Canadian or U.S. FERC regulation, a gas pipeline faces the same long term

risk of failing to recover the capital invested.

As mentioned, the FERC uses the DCF methodology to set approved ROEs for gas pipelines.

Like all methods, the DCF method includes the challenge of finding an appropriate comparator

group. Recent merger and acquisition activity in the U.S. had limited the DCF sample, or “proxy

group.” As a result, the FERC began adding LDCs to its proxy group, and making ROE

adjustments to account for the greater risk of pipelines relative to LDCs. The FERC recently

issued a Policy Statement proposing that pipelines organized as Master Limited Partnerships

(“MLPs”) be included in the proxy group to increase its size.viii Based on research by the

Interstate Gas Association of America, including MLPs in the sample should tend to increase

the ROEs that result from the DCF test.ix

The NEB formula ROE has also dropped significantly in relation to the ROEs of U.S. gas and

electric LDCs. A recent Concentric Energy Advisors report prepared for the OEB concluded

that there are no significant differences that would lead to a difference in investor required

returns for Canadian and U.S. LDCs.x By extension it can be concluded that U.S. LDCs are

less risky than Canadian gas pipelines, since gas pipelines have no franchises and greater

supply, market and competitive risk. The figure below shows that the NEB formula return has

dropped significantly and is now below the ROEs awarded to U.S. gas and electric LDCs.

10

NEB Formula vs U.S. Gas & Electric LDCs ROE

8.71%

8.46%

8.88%9.46%9.56%

9.79%

9.53%9.61%

9.90%

9.58%

10.21%10.67%

11.25%

12.25%

8%

9%

10%

11%

12%

13%

14%

15%

16%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

NEB Formula ROE U.S. Gas & Electric LDCs

Source: Public Utilities Fortnightly

A gap has clearly grown between Canadian and U.S. ROEs, which cannot be explained by

changes in relative risk.

Gap Relative to Negotiated Canadian ROEs

Pipelines and their customers often negotiate an explicit ROE for a new or an existing pipeline.

These ROEs are invariably higher than the formula ROEs at the time. The ROE negotiated in a

single settlement reflects a negotiated trade-off between ROE and other risk factors. However,

the fact that all settled ROEs are significantly higher than the alternative formula ROE suggests

that pipelines and their customers are able to agree that formula ROEs do not appropriately

reflect the cost of equity capital. It is worth noting that for U.S. gas pipelines, the ROEs

determined in litigated cases and settlements are very similar, as shown above.

11

While Canadian pipelines may accept increases in short-term risk in some settlements, this

cannot explain a 200 to 400 basis point premium over the formula ROE. The following table

shows some negotiated ROEs. ROEs established as a premium to the NEB formula would be

reset upon a change in the NEB formula. Note that several of these examples are for oil

pipelines, where transportation costs have historically been small in relation to the value of the

commodity in comparison to gas pipelines, and where settlements have been more prevalent.

Pipeline/Pipeline Project ROE

Alliance (2000 to 2014) 11.25% M&NP (2007 settlement) 13% Trans Mountain (2006 to 2010 Settlement) 10.75%

Alberta Clipper NEB Formula ROE + 225 Basis Points Line 4 Extension NEB Formula ROE + 225 Basis Points Mackenzie Valley NEB Formula ROE + 221 Basis Points Southern Lights 12%

The evidence suggests that in Canada, formula returns are a floor for negotiations, and not a

level that parties consider a reasonable benchmark. As a result, they affect the returns that are

negotiated, as the fall-back to settlement.

Analysis of Canadian Stock Market Data

CEPA retained Dr. Stephen Gaske, a cost of capital expert, to conduct an ERP-based analysis

as a further indication of whether current formula-based ROEs are reasonable. His analysis,

appended to this paper, is a straightforward analysis of two samples of Canadian stocks. His

Energy Transportation Sample (consisting of Emera, Enbridge, Fortis, TransCanada, Canadian

Utilities, Westcoast and Terasen while still public) has an average equity risk premium over the

past 23 years of 7.6%, which results in an 11.88% ROE when added to current long term bond

yield. In his opinion, this result appears more reasonable than the ROEs currently produced by

Canadian ROE formulas. Dr. Gaske also evaluates equity risk premiums over time, and finds

that the moving averages for both samples have been increasing. These results support

12

CEPA’s position that the current formula-based ROEs are too low, and that it is time to open up

broader discussion on this topic.

Changes in Financial Markets

The ROE required to meet the fair return standard depends on the price investors put on

differences in risk and the accessibility of capital, which are determined in competitive capital

markets. Its determination is too complex to be captured by any single-variable formula.

Capital markets have changed significantly since ROE formulas were established, increasing

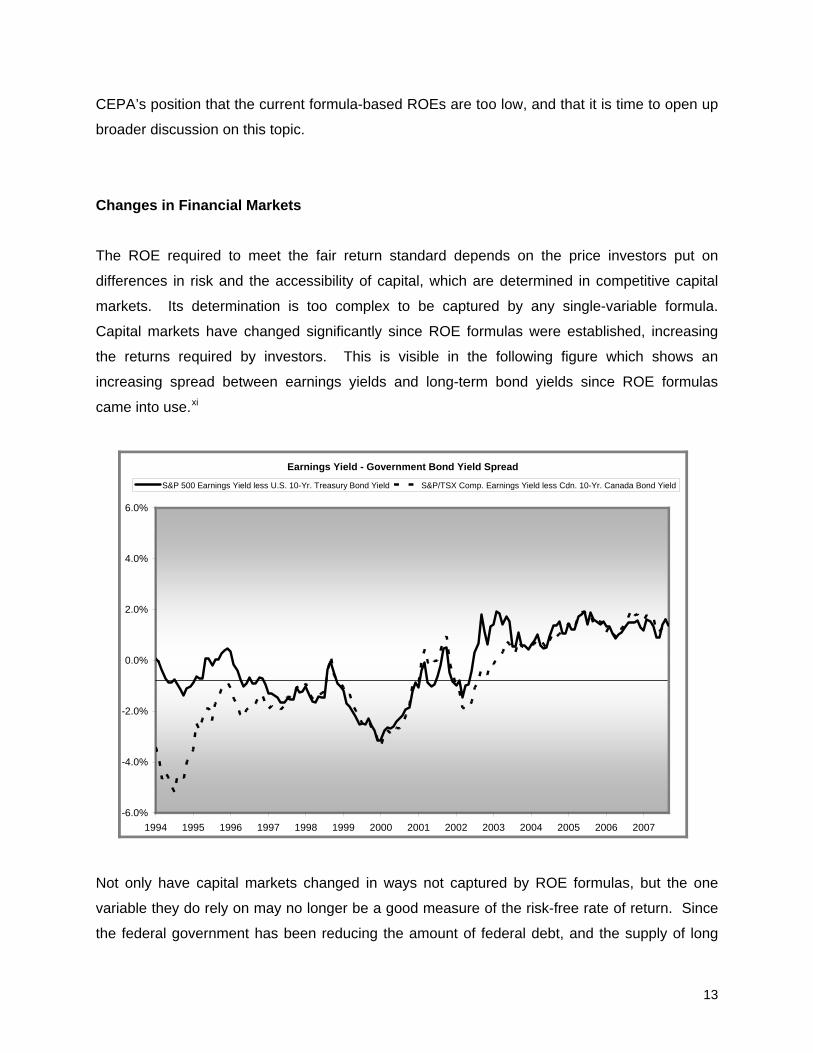

the returns required by investors. This is visible in the following figure which shows an

increasing spread between earnings yields and long-term bond yields since ROE formulas

came into use.xi

Earnings Yield - Government Bond Yield Spread

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

S&P 500 Earnings Yield less U.S. 10-Yr. Treasury Bond Yield S&P/TSX Comp. Earnings Yield less Cdn. 10-Yr. Canada Bond Yield

Not only have capital markets changed in ways not captured by ROE formulas, but the one

variable they do rely on may no longer be a good measure of the risk-free rate of return. Since

the federal government has been reducing the amount of federal debt, and the supply of long

13

term government bonds has decreased while the economy has been growing, the price of

bonds has increased and bond yields have been reduced. Thus, improved government

finances have artificially reduced pipeline ROEs.

The following figures show the decline in bond yields and the current low spread between 10

and 30 year bond yields.

10 & 30 Year Canadian Bond Yield

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

10 Year 30 Year

14

10-30 Year Canadian Bond Yield Spread (Basis Points)

-30

-20

-10

0

10

20

30

40

50

60

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

It would be a coincidence if a single variable formula set as long as 13 years ago generated a

reasonable ROE today. It is equally unlikely that a reasonable return result could be set for the

year 2021 with a formula determined today.

Potential Questions

In order to advance discussion on this topic, this section addresses some questions that may be

raised in response to this paper.

Why have gas pipelines not applied for higher ROEs if they are too low?

Each company has its own motivations, but there are some common reasons. ROE litigation is

costly and contentious, and the evidentiary standard may be high given the subjective nature of

the matter. Settlements are typically preferred if they result in an increase in ROE relative to the

formula result. Settlements allow pipelines and their customers to collaborate on other matters

instead of opposing each other in lengthy, adversarial proceedings.

15

Why does investment continue if the ROE is too low?

As long as a gas pipeline operates, its owners will continually invest to maintain safe operations.

Investments are also made to serve new customers. These are long term investments, and are

made with the expectation that the returns will be fair over the life of the asset. Expansions and

extensions are also required in order to avoid bypass by a competing pipeline, which would

undermine the value of the initial investment.

Without an improvement in formula-based returns, Canadian pipeline infrastructure investment

is being put at risk, along with the development of Canada’s natural resources. If investors

begin to lose faith that a regulator will award reasonable returns, they will be less likely to invest

in that jurisdiction. It could take many years of corrected action by regulators before investors

regain confidence, during which economic development could be impeded.

Why are entities earning formula ROEs purchased for more than book value if ROEs are too

low?

Recent purchases above book value have suggested to some that formula-based returns are

higher than the cost of capital to investors. Apart from the fact that book values are an

accounting construct, there are a number of other reasons investors would pay more than book

value for an asset. A few examples are creative financing, expectations of higher returns (either

by regulatory change or settlement/incentives), and strategic value. There have also been

cases where, in hindsight, too much has been paid for a regulated asset.xii

Why are stock prices and credit ratings unharmed if ROEs are too low?

There is no gas pipeline in Canada which trades on the stock market as a “pure play” gas

pipeline. They are all held by parent companies with other assets or include other non-

regulated assets. Considering the stock prices and debt ratings of a parent company is not

consistent with the stand-alone principle described above. While some regulated entities may

be rated by credit ratings agencies, these ratings are affected by the credit quality of the parent

organization.

16

17

Further, there is evidence that the investment community is concerned about the ROEs

awarded to gas pipelines, as described in the NEB’s 2007 Hydrocarbon Transportation System

Assessment:

Many analysts expressed support for a formulaic approach to determining ROEs

because of the transparency, stability and predictability that this method

provides. However, a number expressed the view that the ROE resulting from the

formula was too low, and contend that they are much lower than regulated ROEs

in the U.S. and U.K. While views ranged widely on this issue, some felt that the

typically lower ROEs in Canada were not justified by the differences in risk for

Canadian companies compared to FERC-regulated pipelines. Some parties

suggested it was time for the Board to revisit the ROE Formula.xiii

Conclusion

Canadian gas pipelines are being awarded formula ROEs that result in unfairly low returns.

U.S. gas pipelines and LDCs, and Canadian pipelines who settle their returns, have ROEs 200

to 400 basis points higher than formula ROEs. Dr Gaske’s conclusion is within this range,

based on a simple ERP-based statistical analysis of utility index data. It is no surprise that

formulas are unable to track the dynamics of a capital market, which incorporates the

expectations of investors based upon all available information. The time has come for

stakeholders to engage in discussion on this matter, and to consider the potential

consequences of awarding low ROEs for energy infrastructure.

19

Endnotes

i The EUB describes the stand alone principle as follows: “The Board accepts that the underpinning of the stand-alone principle is that the regulated utility should not be subsidizing its non-utility operations or operations of members of its corporate family, neither should the non-regulated activities subsidize the utility operations” EUB Decision 2003-061, AltaLink Management Ltd. and TransAlta Utilities Corporation Transmission Tariff for May 1, 2002 – April 30, 2004 TransAlta Utilities Corporation Transmission Tariff for January 1, 2002 – April 30, 2002 August 3, 2003, p 83. ii See for instance, NEB Reasons for Decision RH-2-2004 Phase II. TransCanada Pipelines Cost of Capital pp. 70-71. April 2005; EUB Decision 2004-052 Generic Cost of Capital p.26. July 2, 2004. iii NEB Reasons for Decision RH-2-2004 Phase II. TransCanada Pipelines Cost of Capital pp. 68-69. April 2005. iv NEB Reasons for Decision RH-2-2004 Phase II. TransCanada Pipelines Cost of Capital pp. 68. April 2005 EUB Decision 2004-052 Generic Cost of Capital p.27. July 2, 2004 v The NEB used to consider the DCF and CE methods, but in the early 1990s shifted to giving most or all weight on the results of the ERP method. The NEB primarily considered a Comparable Earnings evaluation of Canadian industrials in RH-1-78 and RH-1-79. In RH-4-81, RH-3-82, and RH-2-83, the NEB made ROE determinations based “on its consideration of all of the evidence presented” which included multiple estimation methods. Decision RH-1-84 states “The Board is of the view that the determination of an appropriate rate of return on equity involves the use of methods that are subject to the exercise of judgment.” The Board made similar comments in RH-2-85, RH-3-86, and RH-1-88 Part II. In the RH-2-89 decision the Board found that the results of DCF test “should be given weight in assessing a fair rate of return on equity” despite “limitations of the approach.” In the early 1990’s the Board placed the primary weight on the ERP method and placed less weight on the CE and DCF methods (decisions RH-1-91 and RH-2-92). In RH-4-93 the Board put “little or no weight” on the results of the CE and DCF methods, stating that “these tests may prove useful under different economic conditions.” In the last NEB ROE decision, RH-2-94, the Board “decided to give primary weight to the results of the equity risk premium test.” vi The EUB once gave some weight to the results of the DCF test, but most recently placed no weight on the results of the DCF test. From 1990 to 1994, the EUB gave less weight to the results of the DCF method than the ERP method. For instance Decision E94060 states "The Board has in the past found that none of the methods advocated by the expert witnesses necessarily yields or provides a precise measurement of the fair rate of return on equity. However, the Board considers the results of each method helpful in its deliberations…The Board has taken note of the caution expressed by each of the expert witnesses respecting the use of the DCF method in today’s economic environment. The Board accepts that less weight should be placed on the absolute results of the DCF method under current economic conditions.” The EUB moved from “less weight” to “little weight” on DCF results in Decision U96001, also because of the effects economic conditions at the time may have had on the results of the DCF test. In the Board’s Generic Cost of Capital Decision (Decision 2004-052), the results of the DCF test were given no weight, as the Board was convinced by interveners that “the analysts’ earnings forecasts used in the development of the DCF estimates have been biased high.” vii Eugene F. Fama and Kenneth R. French, “The Capital Asset Pricing Model: Theory and Evidence” Journal of Economic Perspectives, Volume 18, Number 3, Summer 2004, Pages 43-44. viii FERC, Proposed Policy Statement on Composition of Proxy Groups for Determining Gas and Oil Pipeline Return on Equity, Issued July 19, 2007. ix Smead, Richard G of Navigant Consulting Inc. paper prepared for the Interstate Natural Gas Association of America, “Allowed Returns on Equity in the Interstate Gas Pipeline Industry: Issues and Options Regarding the FERC DCF Approach,” August 24, 2006. x Concentric Energy Advisors, A Comparative Analysis of Returns on Equity of Natural Gas Utilities, prepared for the Ontario Energy Board, pp. 3, 57, 58. xi The Earnings Yield is earnings in the stock market divided by the sum of stock prices. This measure can be compared to the yield on debt. xii On August 2, 2005 Kinder Morgan announced that it had agreed to acquire Terasen for US$5.6 billion or 2.6x estimated 2005 book value per share. Since then, Kinder Morgan has moved aggressively to divest non-core assets

20

acquired in the Terasen Inc. transaction. On February 26, 2007, it announced that it has agreed to sell Terasen Gas Inc. to Fortis Inc. for C$3.7 billion and on March 5, 2007, Kinder Morgan announced that it has agreed to sell the Corridor Pipeline and the $1.8 billion expansion of that pipeline to Inter Pipeline Fund for $760 million and $300 million of assumed debt relating to the expansion.. On April 30, 2007, Kinder Morgan Energy Partners completed the purchase of the Trans Mountain Pipeline system from Kinder Morgan for US$550 million plus US$450 million of assumed debt. In its Form 10-Q filing for the period ending March 31, 2007, Kinder Morgan Inc. announced that it has recorded a goodwill impairment charge of US$377.1 million relating to the Trans Mountain transaction. This charge is in addition to the US$650.5 million impairment charge recorded in its Form 10-K filing, resulting from the Terasen Inc. - Fortis Inc. transaction. xiii NEB, Canadian Hydrocarbon Transportation System: Transportation Assessment, July 2007, p. 40.

Appendix

Risk Premium Analysis Dr. Stephen Gaske

Canadian regulators currently set the rate of return on common equity for regulated pipelines by

using “equity risk premium” formula ROEs calculated each year by adding a percentage of the

change in yields on Bank of Canada bonds to the previous year’s ROE. The risk premium

approach explicitly recognizes that pipeline equity is riskier than long term Bank of Canada

bonds, and therefore that the expected return on equity should be higher in the pipeline industry

than the yield on Bank of Canada bonds. Although there is no doubt about the need for a risk

premium, the difficult problem for a regulator is to determine the size of the premium that is

required in order for a pipeline to attract capital on reasonable terms. However, just as bond

yields change from year to year, the required level of the premium also changes continually in

response to (i) changes in the financial market in general, and (ii) to changes in the risks of

pipelines in particular.

The formula currently used to estimate ROEs can generally be written:

ROE in Year 2 = ROE in Year 1 + 75% of the change in the forecast bond yield

This formula mechanically adjusts the allowed ROE in response to changes in interest rates.

The allowed ROE moves up and down at 75% of the change in the forecast bond yield. As a

result, the size of the risk premium is adjusted each year by an amount equal to -25% of the

change in the bond yield. The mechanical adjustment in the size of the risk premium is

designed to make a rough adjustment for changes in the financial market in general by

assuming that the risk premium is greater when interest rates are relatively low and that a

smaller risk premium is required when interest rates are relatively high. While this might be a

reasonable representation of how the required risk premium is likely to react in the short run to

changes in financial market conditions (for which changes in the interest rate is intended to be a

rough proxy), there is nothing in this formula that allows the risk premium to adjust in the long

run if the relative risks of pipelines change over time. Consequently, it may be necessary to re-

calibrate the formula periodically.

To test whether the current formula is reasonably accurate, and to determine whether the

required risk premium may have changed significantly through the years, this analysis reviews

bond yields and market returns on utility common equity for various time periods during the 51

year period 1956-2006. Market returns on common equity were evaluated with two indices:

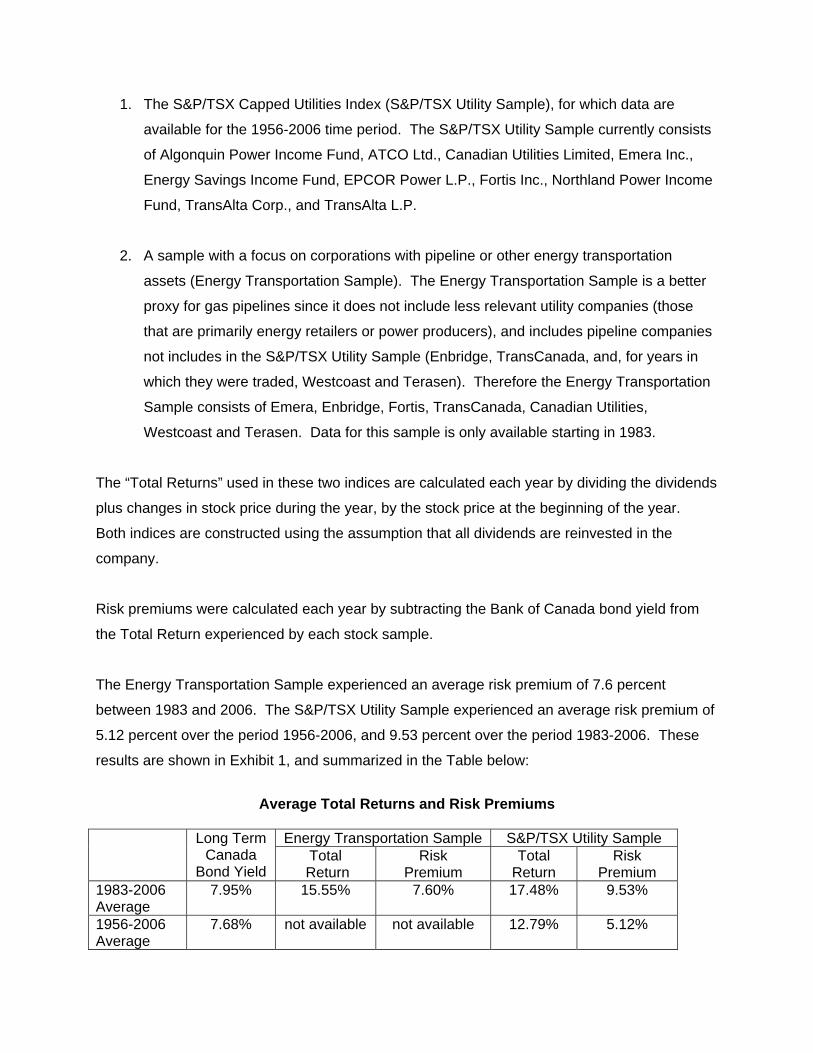

1. The S&P/TSX Capped Utilities Index (S&P/TSX Utility Sample), for which data are

available for the 1956-2006 time period. The S&P/TSX Utility Sample currently consists

of Algonquin Power Income Fund, ATCO Ltd., Canadian Utilities Limited, Emera Inc.,

Energy Savings Income Fund, EPCOR Power L.P., Fortis Inc., Northland Power Income

Fund, TransAlta Corp., and TransAlta L.P.

2. A sample with a focus on corporations with pipeline or other energy transportation

assets (Energy Transportation Sample). The Energy Transportation Sample is a better

proxy for gas pipelines since it does not include less relevant utility companies (those

that are primarily energy retailers or power producers), and includes pipeline companies

not includes in the S&P/TSX Utility Sample (Enbridge, TransCanada, and, for years in

which they were traded, Westcoast and Terasen). Therefore the Energy Transportation

Sample consists of Emera, Enbridge, Fortis, TransCanada, Canadian Utilities,

Westcoast and Terasen. Data for this sample is only available starting in 1983.

The “Total Returns” used in these two indices are calculated each year by dividing the dividends

plus changes in stock price during the year, by the stock price at the beginning of the year.

Both indices are constructed using the assumption that all dividends are reinvested in the

company.

Risk premiums were calculated each year by subtracting the Bank of Canada bond yield from

the Total Return experienced by each stock sample.

The Energy Transportation Sample experienced an average risk premium of 7.6 percent

between 1983 and 2006. The S&P/TSX Utility Sample experienced an average risk premium of

5.12 percent over the period 1956-2006, and 9.53 percent over the period 1983-2006. These

results are shown in Exhibit 1, and summarized in the Table below:

Average Total Returns and Risk Premiums

Energy Transportation Sample S&P/TSX Utility Sample Long Term

Canada Bond Yield

Total Return

Risk Premium

Total Return

Risk Premium

1983-2006 Average

7.95% 15.55% 7.60% 17.48% 9.53%

1956-2006 Average

7.68% not available not available 12.79% 5.12%

When evaluating pipelines, the Energy Transportation Sample should be a better indicator of

required returns than a broader sample. Consequently, the 7.6 percent average risk premium

for pipelines should be a better estimate of the required risk premium than risk premiums

calculated for the S&P/TSX Utility Sample. Adding the 4.28 percent bond yield from 2006 to the

7.6 percent risk premium would produce an allowed rate of return of 11.88 percent. This is

hardly an excessive rate of return, and appears to be far more reasonable than the ROEs

currently resulting from Canadian ROE formulas.

Analysis of both indices suggests the required risk premium has increased significantly since

the 1990’s. The chart below shows the moving averages of the risk premiums for both indices,

which have increased while the yield on long term bonds has decreased.

Changes in Average Risk Premium and Interest Rate

1990-2006

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Yield on Long-Term Canada BondEnergy Transportation Sample Premium, 10-year moving average S&P/TSX Utility Sample Premium, 35-year moving average

Exhibit 1 Total Returns and Risk Premiums

Energy Transportation Sample S&P/TSX Utility Sample

Year

Yield on Long-Term Canada

Bond Annual Return

Risk Premium

10-Yr. Moving Average Premium

Annual Return

Risk Premium

35-Yr. Moving Average Premium

1956 3.63% 0.17% -3.46% 1957 4.11% -3.43% -7.54% 1958 4.15% 9.81% 5.66% 1959 5.08% 0.21% -4.87% 1960 5.19% 26.81% 21.62% 1961 5.05% 19.17% 14.12% 1962 5.11% -0.72% -5.83% 1963 5.09% 6.19% 1.10% 1964 5.18% 21.59% 16.41% 1965 5.21% 4.23% -0.98% 1966 5.69% -13.17% -18.86% 1967 5.94% 5.07% -0.87% 1968 6.75% 7.41% 0.66% 1969 7.58% -8.62% -16.20% 1970 7.91% 23.34% 15.43% 1971 6.95% 4.29% -2.66% 1972 7.23% -0.44% -7.67% 1973 7.56% -4.14% -11.70% 1974 8.90% 14.38% 5.48% 1975 9.04% 5.75% -3.29% 1976 9.18% 15.02% 5.84% 1977 8.70% 19.00% 10.30% 1978 9.27% 27.28% 18.01% 1979 10.21% 12.61% 2.40% 1980 12.48% 5.74% -6.74% 1981 15.22% -0.55% -15.77% 1982 14.26% 35.90% 21.64% 1983 11.79% 25.63% 13.84% 40.97% 29.18% 1984 12.75% 5.46% -7.29% 24.31% 11.56% 1985 11.04% 18.95% 7.91% 10.04% -1.00% 1986 9.52% -3.48% -13.00% 11.48% 1.96% 1987 9.95% 9.97% 0.02% 1.07% -8.88% 1988 10.22% 7.87% -2.35% 5.63% -4.59% 1989 9.92% 18.44% 8.52% 22.07% 12.15% 1990 10.85% 6.35% -4.50% 0.58% -10.27% 1.78% 1991 9.76% 3.90% -5.86% 27.02% 17.26% 2.37% 1992 8.77% -0.52% -9.29% -1.20% -2.24% -11.01% 2.27% 1993 7.85% 31.45% 23.60% -0.23% 23.52% 15.67% 2.56% 1994 8.63% -2.65% -11.28% -0.62% -6.04% -14.67% 2.28% 1995 8.28% 14.77% 6.49% -0.77% 18.44% 10.16% 1.95% 1996 7.50% 30.69% 23.19% 2.85% 32.68% 25.18% 2.27% 1997 6.42% 48.56% 42.14% 7.07% 37.33% 30.91% 3.32% 1998 5.47% 4.07% -1.40% 7.16% 36.55% 31.08% 4.17% 1999 5.69% -24.02% -29.71% 3.34% 72.34% 66.65% 5.61% 2000 5.89% 57.96% 52.07% 8.99% 18.70% 12.81% 6.00% 2001 5.78% 14.68% 8.90% 10.47% -25.19% -30.97% 5.66% 2002 5.66% 13.79% 8.13% 12.21% -3.86% -9.52% 5.41% 2003 5.28% 27.71% 22.43% 12.10% 22.92% 17.64% 5.90% 2004 5.08% 14.99% 9.91% 14.21% 18.01% 12.93% 6.73% 2005 4.39% 32.08% 27.69% 16.33% 25.78% 21.39% 6.90% 2006 4.28% 16.64% 12.36% 15.25% 7.36% 3.08% 7.06%

AVERAGE: 1983-2006 7.95% 15.55% 7.60% 17.48% 9.53% 1956-2006 7.68% 12.79% 5.12%