Personal Finance 101 “The Big Picture”. Section 1 Big Picture Basics.

95

Personal Finance 101 “The Big Picture”

-

Upload

mabel-lawson -

Category

Documents

-

view

246 -

download

2

Transcript of Personal Finance 101 “The Big Picture”. Section 1 Big Picture Basics.

Personal Finance 101

“The Big Picture”

Section 1

Big Picture

Basics

Money

is NOT the most important thing in life

BUT…

Learn to live happily

The purpose of life is to

One of the essential elements of a happy and successful life is

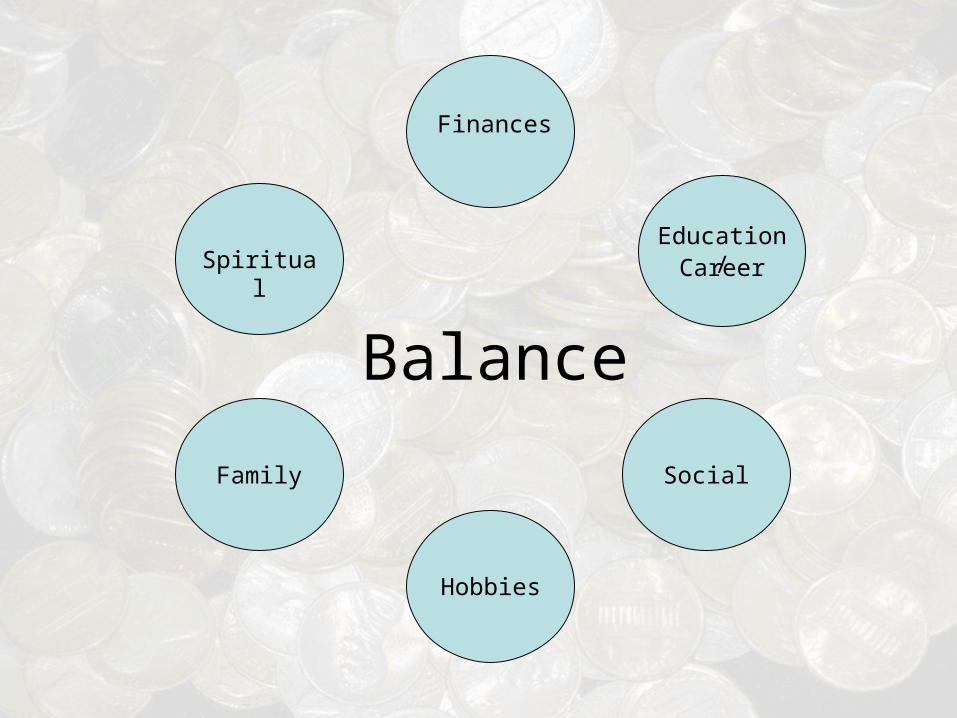

Balance

Spiritual

Finances

Education/Career

SocialFamily

Hobbies

Balance

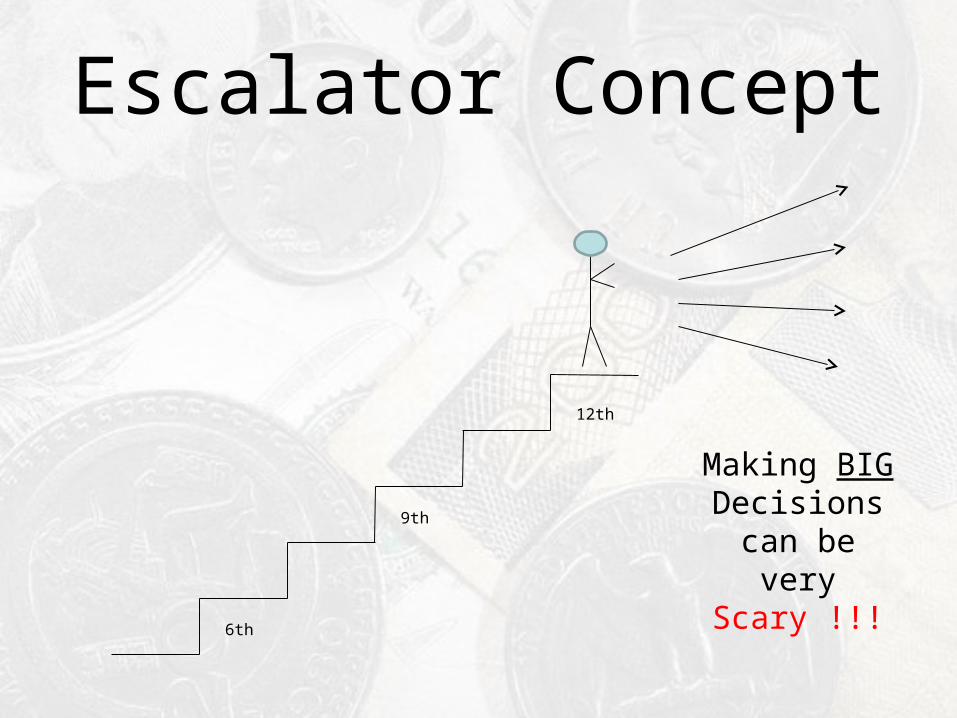

Escalator Concept

12th

9th

6th

Making BIG Decisions

can be veryScary !!!

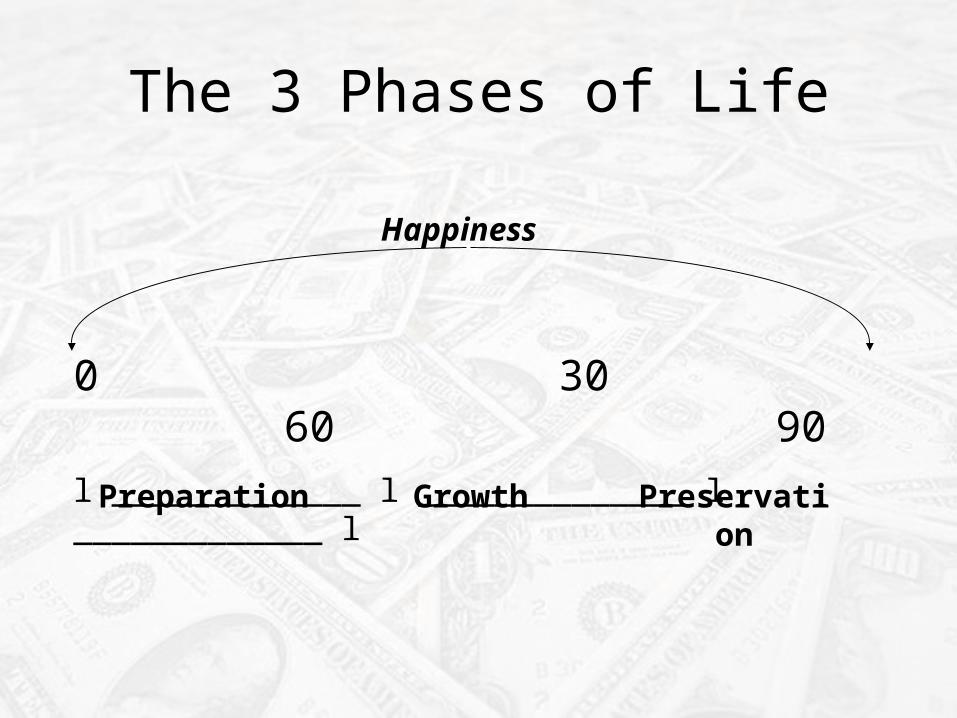

The 3 Phases of Life

Happiness

0 30 60

90

l _____________ l ______________ l _____________ lPreparation Growth Preservation

Phase 1: Preparation

0 30

l ______________________________ l

• Explore options

• Develop Skills (Earning Power)

• Practice Balance

Income & Expenses

The key is to maximize income (through earning power) and minimizing expenses

(using self-control).

Income is directly related to 3 things:

• Level of Skills developed

• Demand for those skills

• How easily you are replaced

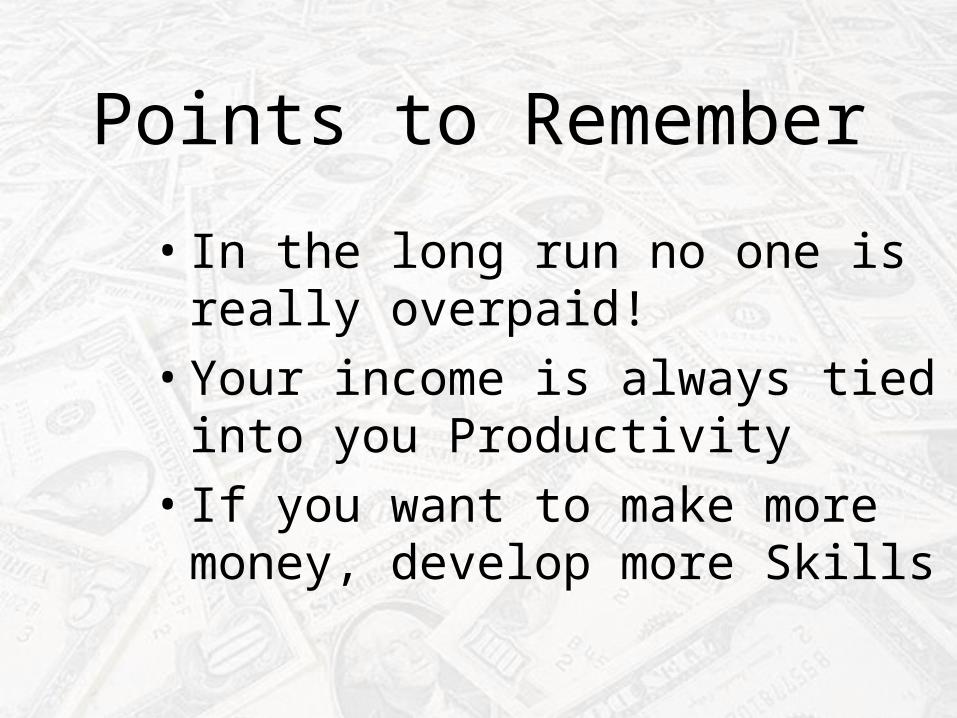

Points to Remember

• In the long run no one is really overpaid!

• Your income is always tied into you Productivity

• If you want to make more money, develop more Skills

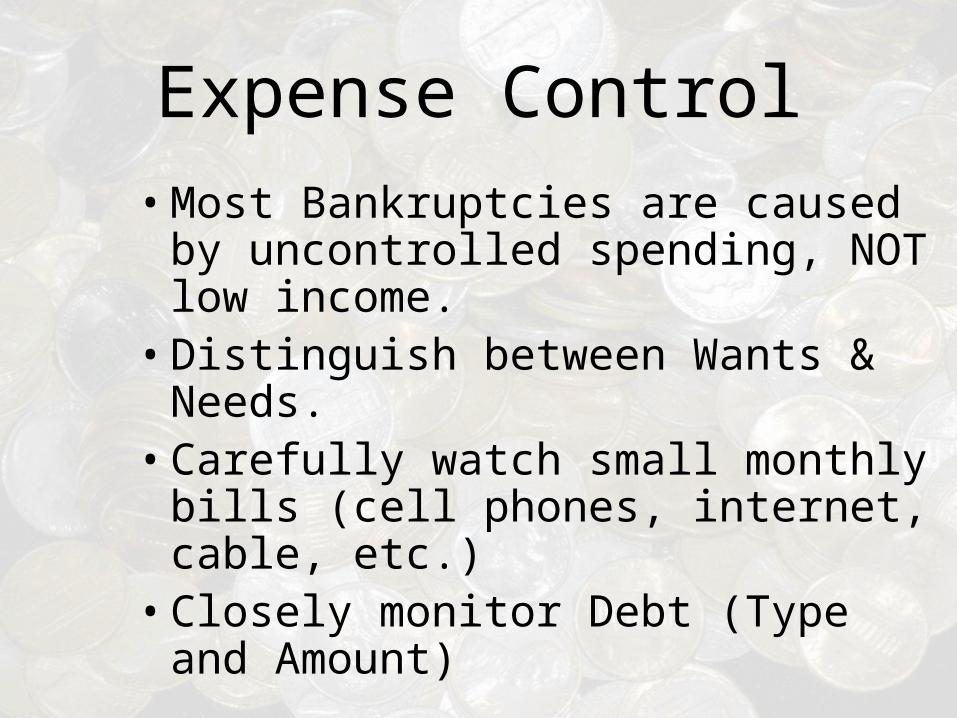

Expense Control

• Most Bankruptcies are caused by uncontrolled spending, NOT low income.

• Distinguish between Wants & Needs.

• Carefully watch small monthly bills (cell phones, internet, cable, etc.)

• Closely monitor Debt (Type and Amount)

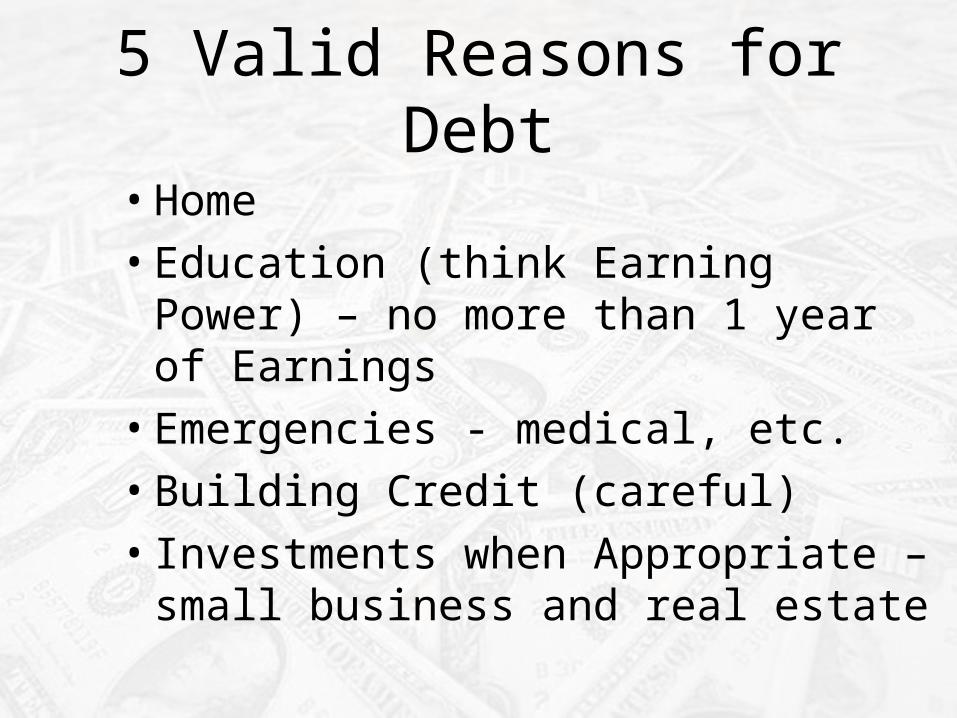

5 Valid Reasons for Debt

• Home

• Education (think Earning Power) – no more than 1 year of Earnings

• Emergencies - medical, etc.

• Building Credit (careful)

• Investments when Appropriate – small business and real estate

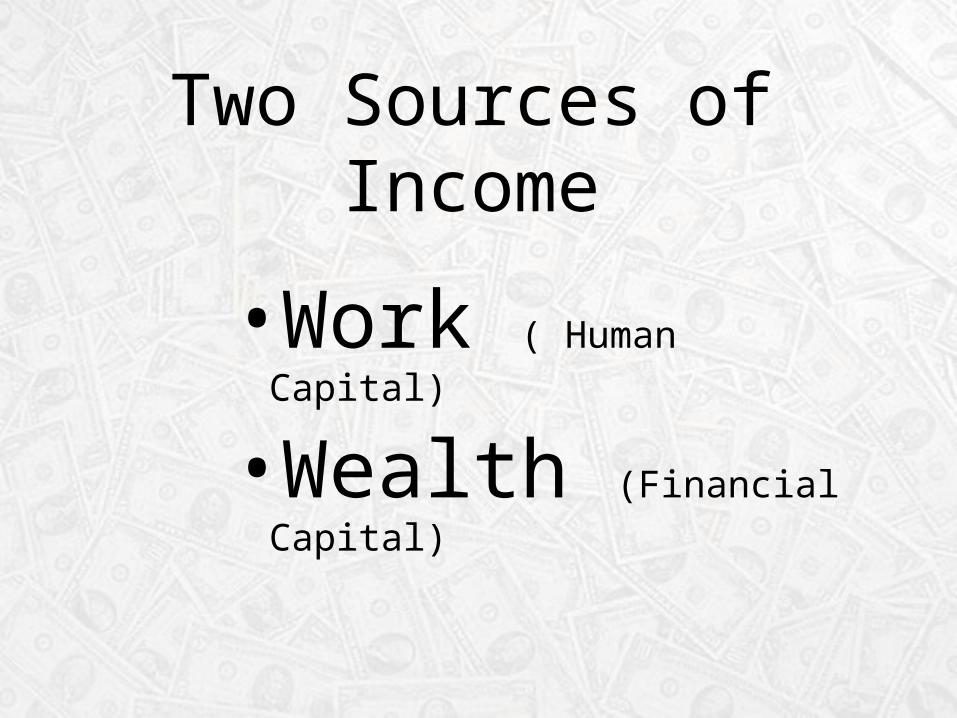

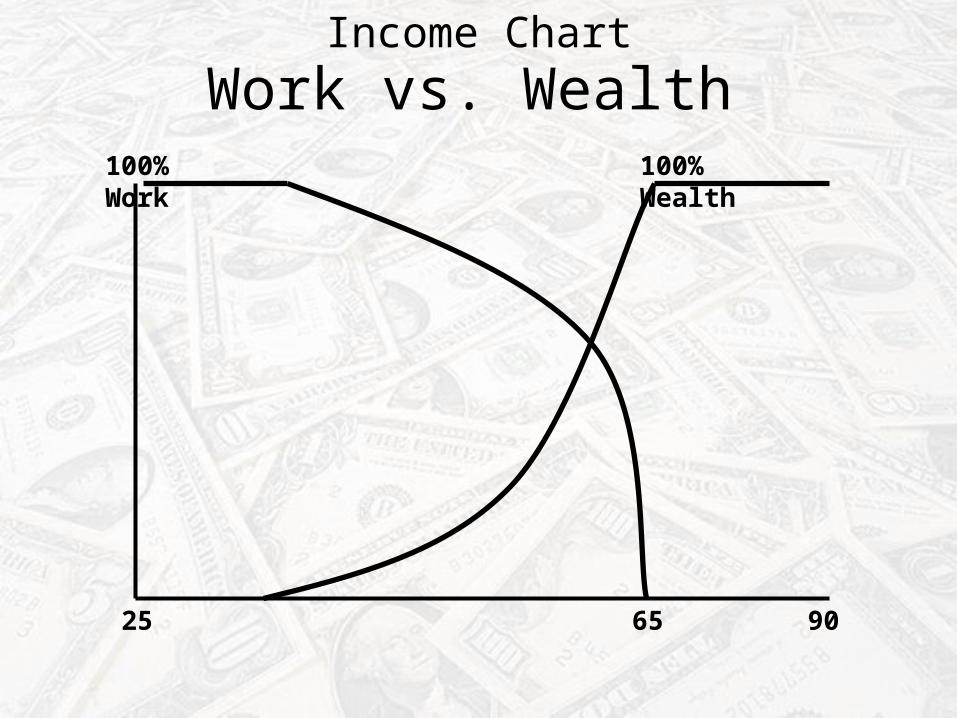

Two Sources of Income

•Work ( Human Capital)

•Wealth (Financial Capital)

Once your income and expense picture is stabilized you should start a program of moving from

income from Work to income from Wealth.

Work vs. Wealth

25 65 90

100% Work 100% Wealth

Income Chart

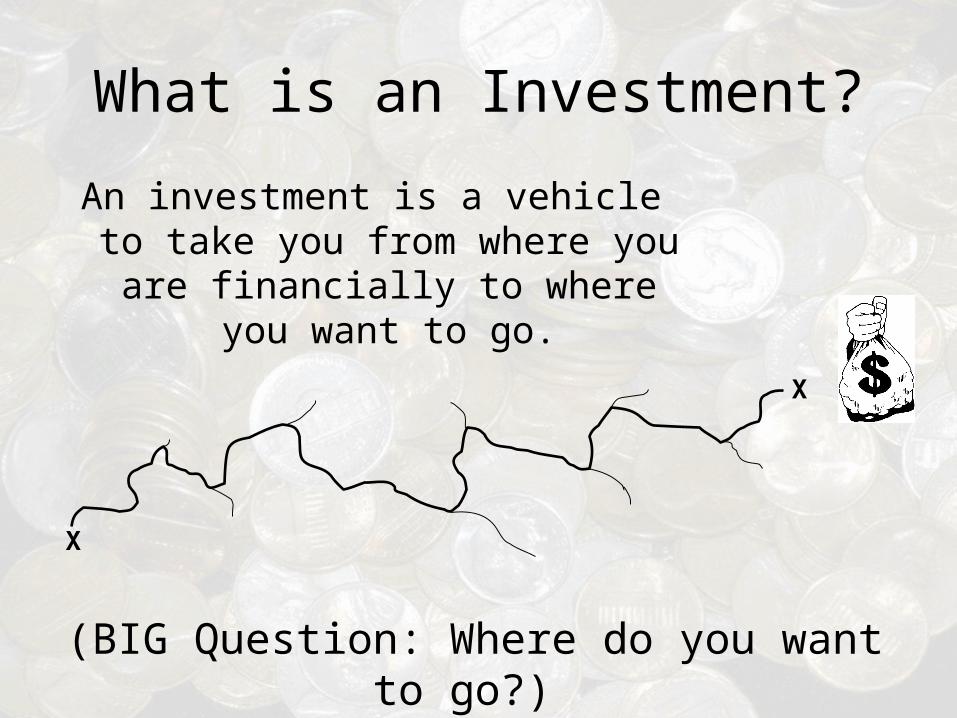

What is an Investment?

An investment is a vehicle to take you from where you are financially to

where you want to go.

(BIG Question: Where do you want to go?)

X

X

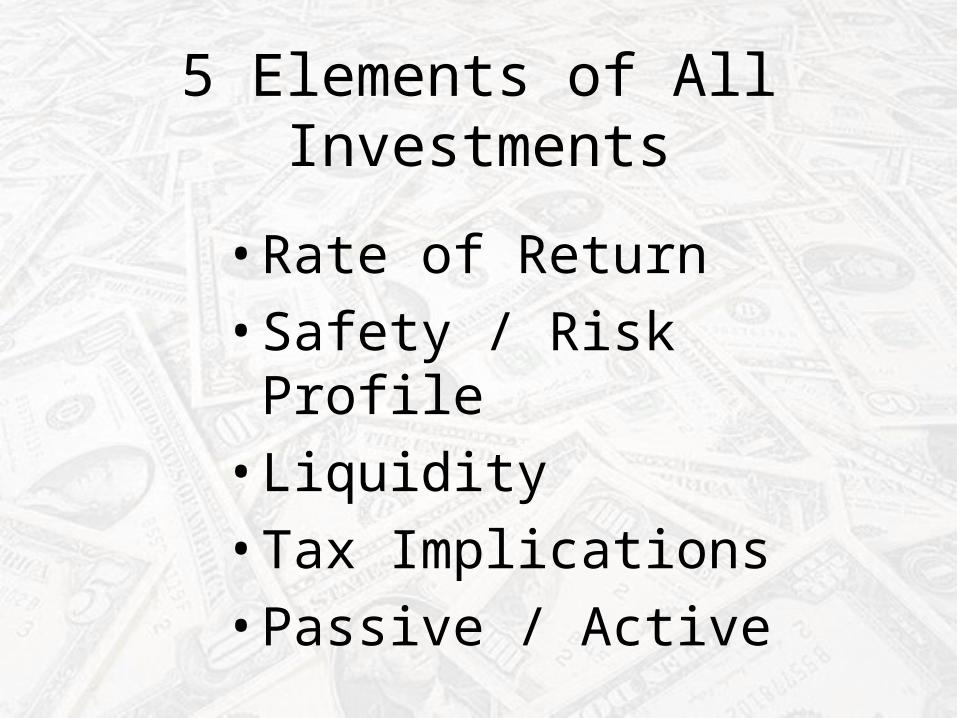

5 Elements of All Investments

• Rate of Return

• Safety / Risk Profile

• Liquidity

• Tax Implications

• Passive / Active

What is Interest?

Interest is the rental charge for using other peoples’ money.

Remember: It is better to receive than to give!

“The most powerful force in the universe is compound

interest”

- Albert Einstein

What makes compound interest so powerful?

Time

Compound interest is earning interest on previously earned interest.

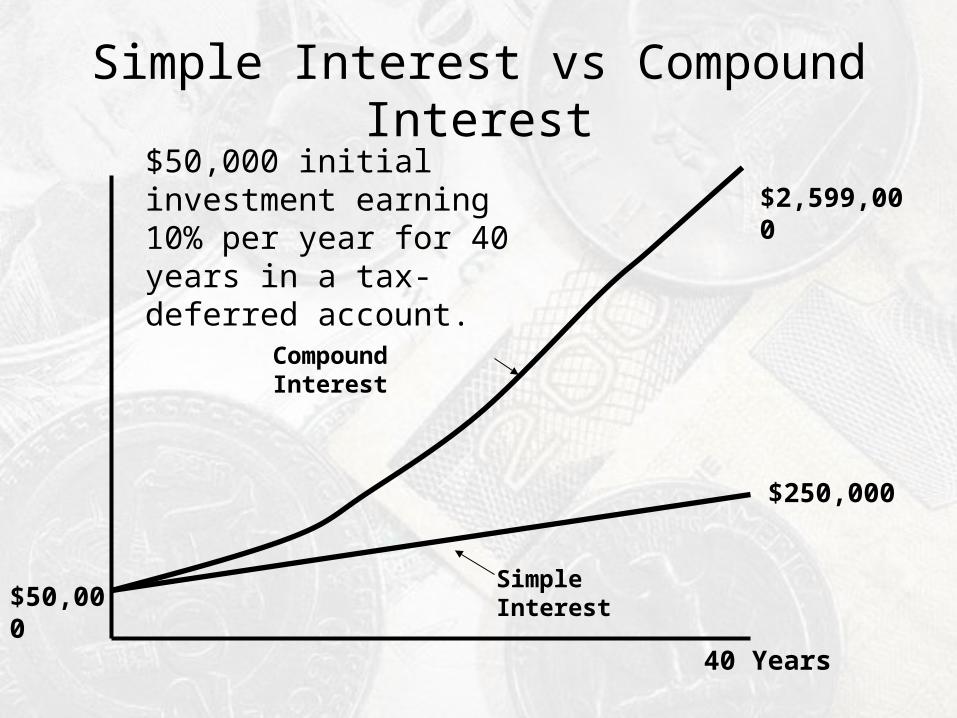

Simple Interest vs Compound Interest

40 Years

$50,000

$250,000

Simple Interest

$2,599,000

Compound Interest

$50,000 initial investment earning 10% per year for 40 years in a tax-deferred account.

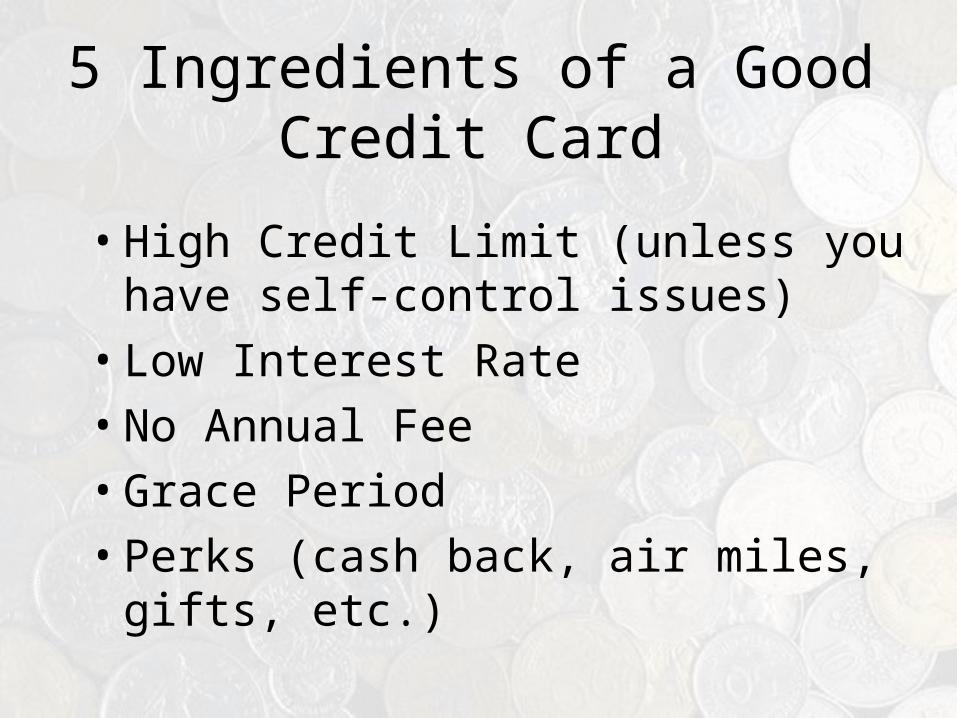

5 Ingredients of a Good Credit Card

• High Credit Limit (unless you have self-control issues)

• Low Interest Rate

• No Annual Fee

• Grace Period

• Perks (cash back, air miles, gifts, etc.)

Investment Categories

• Stocks

• Bonds

• Real Estate

• Small Business

• Collectibles • Specialty (Commodities, Metals, Notes, etc.)

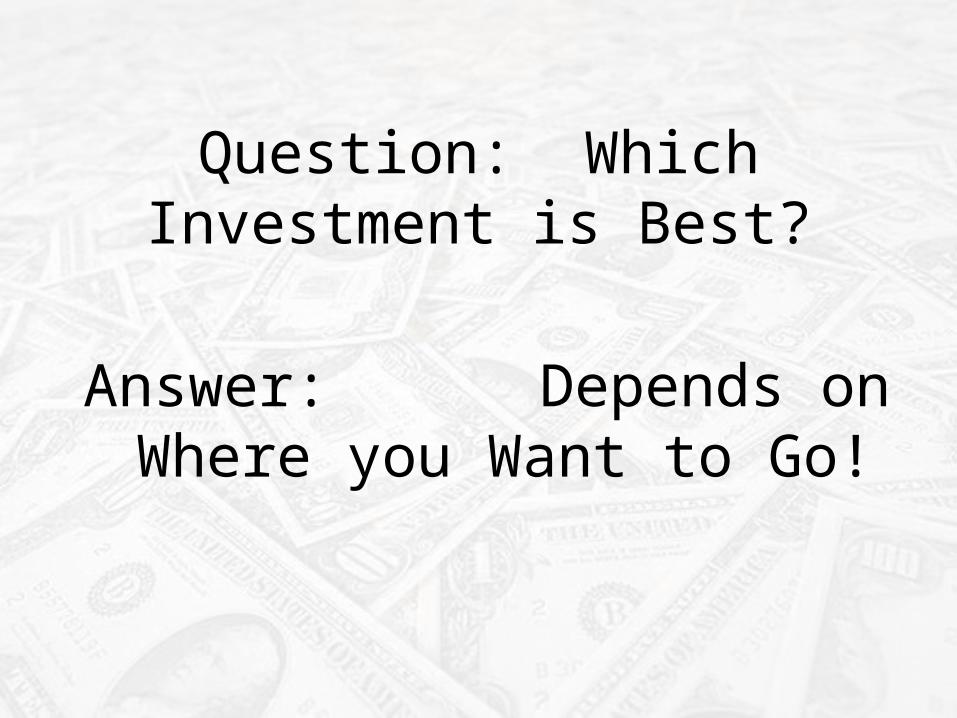

Question: Which Investment is Best?

Answer: Depends on Where you Want to Go!

Planning forRetirement

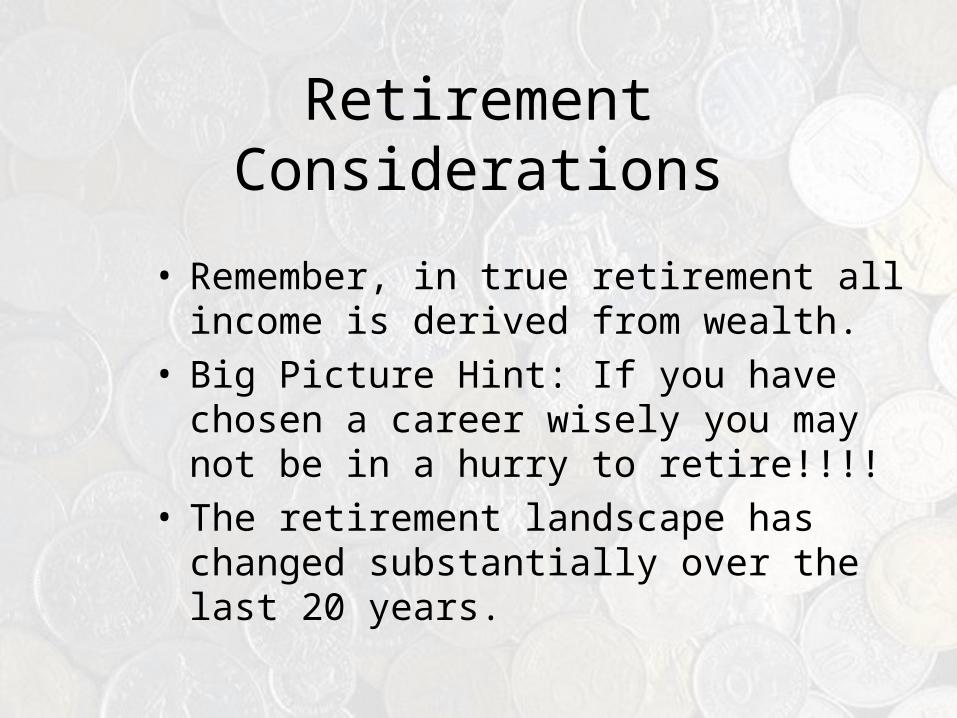

Retirement Considerations

• Remember, in true retirement all income is derived from wealth.

• Big Picture Hint: If you have chosen a career wisely you may not be in a hurry to retire!!!!

• The retirement landscape has changed substantially over the last 20 years.

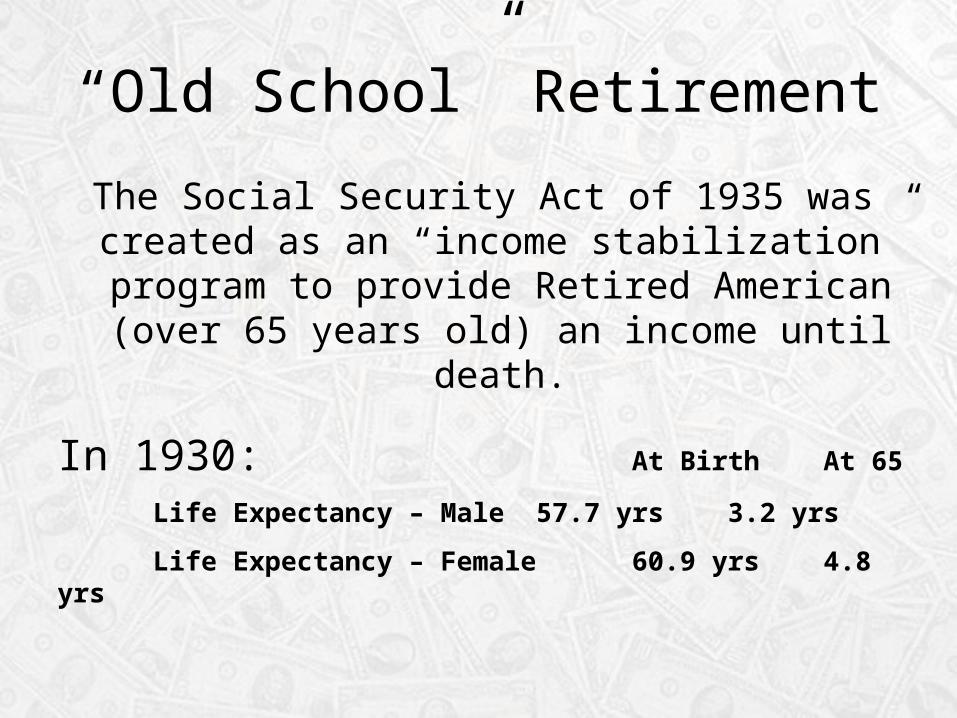

“Old School” Retirement

The Social Security Act of 1935 was created as an “income stabilization” program to provide Retired

American (over 65 years old) an income until death.

In 1930: At Birth At 65

Life Expectancy – Male 57.7 yrs 3.2 yrs

Life Expectancy – Female 60.9 yrs 4.8 yrs

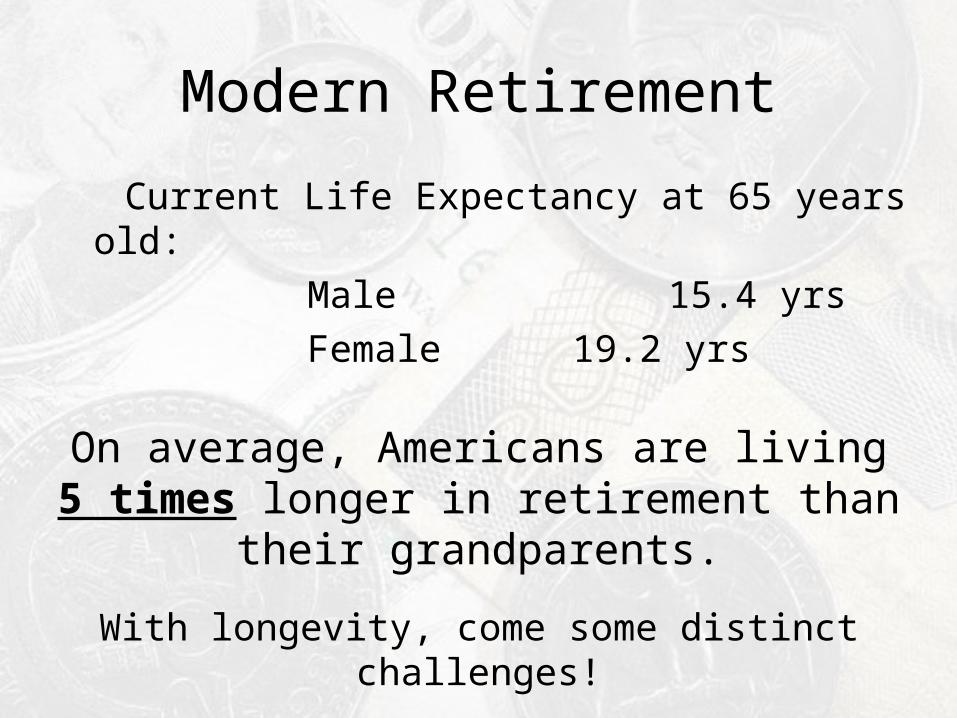

Modern Retirement

Current Life Expectancy at 65 years old:

Male 15.4 yrs

Female 19.2 yrs

On average, Americans are living 5 times longer in retirement than their grandparents.

With longevity, come some distinct challenges!

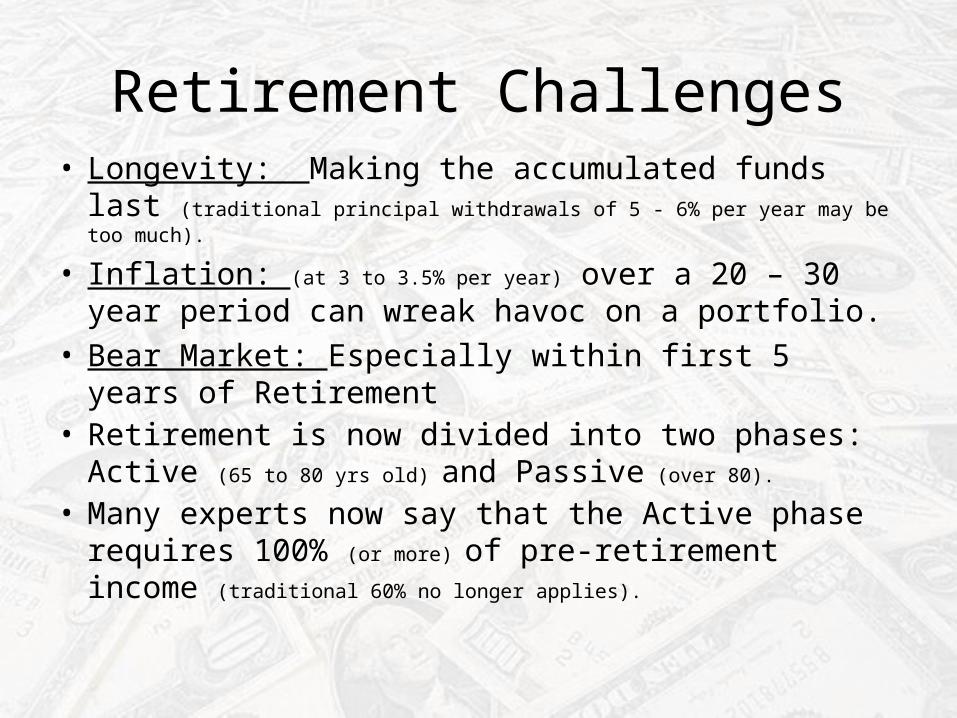

Retirement Challenges• Longevity: Making the accumulated funds last

(traditional principal withdrawals of 5 - 6% per year may be too much).

• Inflation: (at 3 to 3.5% per year) over a 20 – 30 year period can wreak havoc on a portfolio.

• Bear Market: Especially within first 5 years of Retirement

• Retirement is now divided into two phases: Active (65 to 80 yrs old) and Passive (over 80).

• Many experts now say that the Active phase requires 100% (or more) of pre-retirement income (traditional 60% no longer applies).

• Longevity = Pensions or Annuities

• Inflation = Growth-oriented Investments

• Bear Market = Guaranteed Return• Investments ( Money-Market,

• Dividends and some Annuities)

Assessing Risks

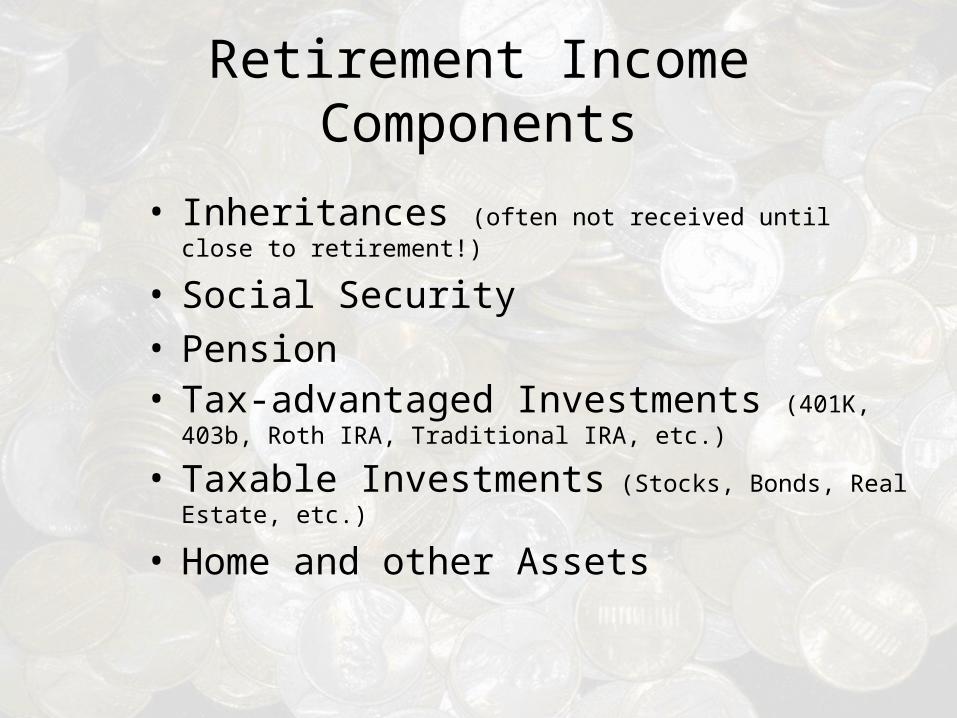

Retirement Income Components

• Inheritances (often not received until close to retirement!)

• Social Security• Pension• Tax-advantaged Investments (401K, 403b, Roth

IRA, Traditional IRA, etc.)

• Taxable Investments (Stocks, Bonds, Real Estate, etc.)

• Home and other Assets

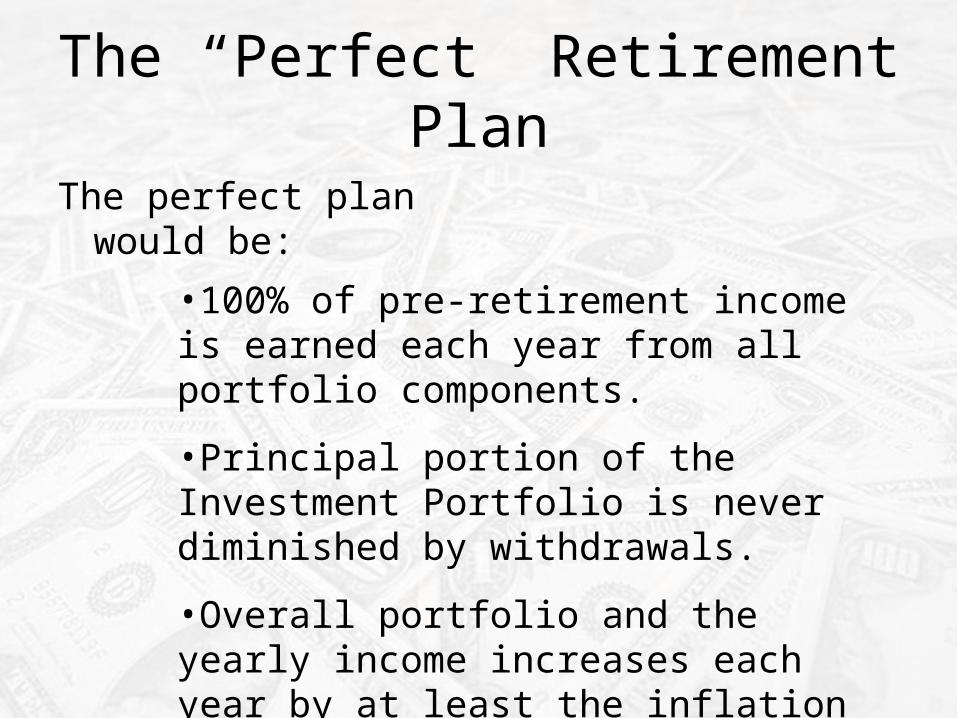

The “Perfect” Retirement Plan

The perfect plan would be:

•100% of pre-retirement income is earned each year from all portfolio components.

•Principal portion of the Investment Portfolio is never diminished by withdrawals.

•Overall portfolio and the yearly income increases each year by at least the inflation rate.

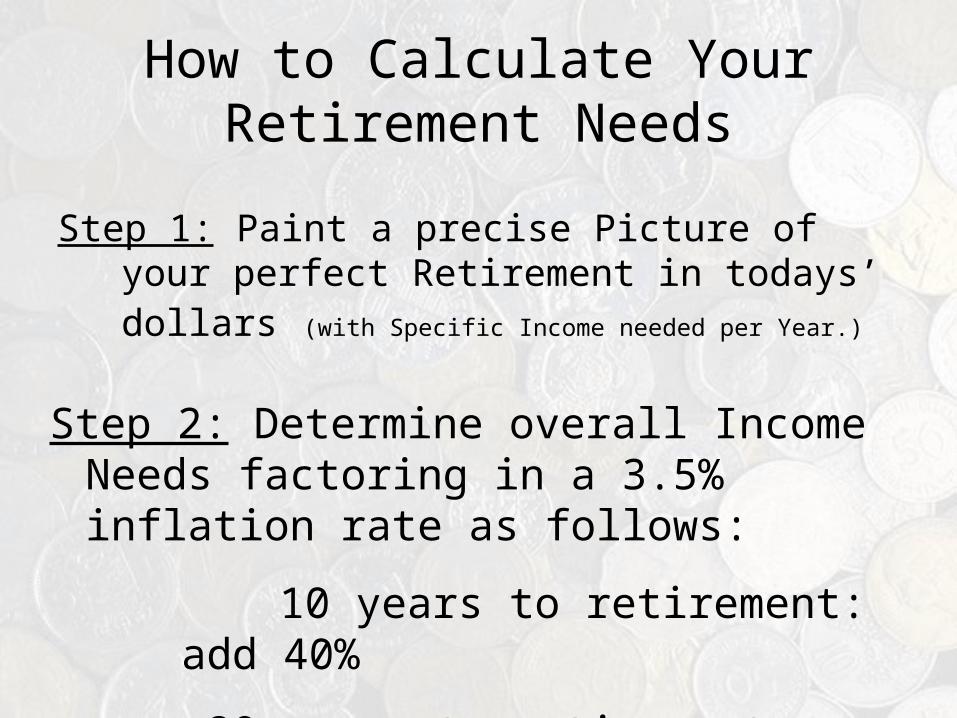

How to Calculate Your Retirement Needs

Step 1: Paint a precise Picture of your perfect Retirement in todays’ dollars (with Specific Income needed per Year.)

Step 2: Determine overall Income Needs factoring in a 3.5% inflation rate as follows:

10 years to retirement: add 40%

20 years to retirement: add 100%

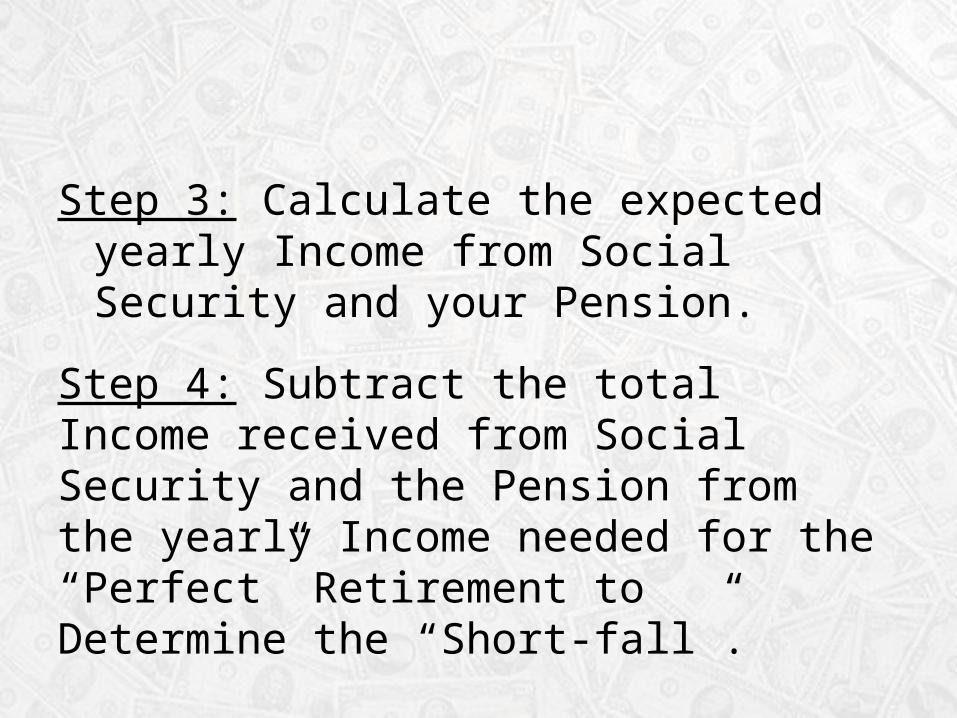

Step 3: Calculate the expected yearly Income from Social Security and your Pension.

Step 4: Subtract the total Income received from Social Security and the Pension from the yearly Income needed for the “Perfect” Retirement to Determine the “Short-fall”.

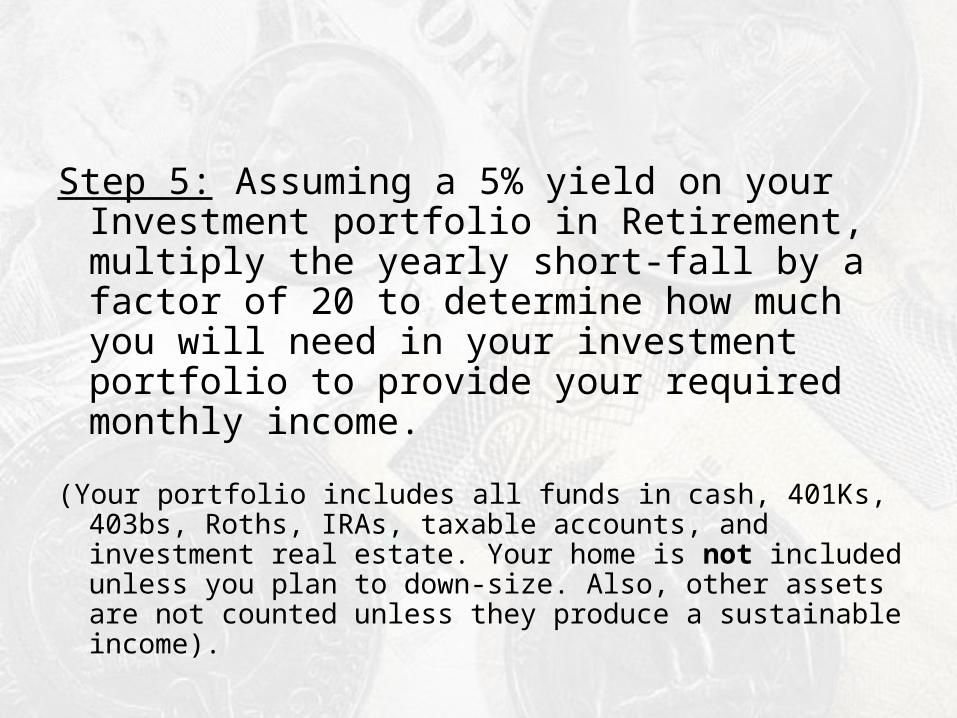

Step 5: Assuming a 5% yield on your Investment portfolio in Retirement, multiply the yearly short-fall by a factor of 20 to determine how much you will need in your investment portfolio to provide your required monthly income.

(Your portfolio includes all funds in cash, 401Ks, 403bs, Roths, IRAs, taxable accounts, and investment real estate. Your home is not included unless you plan to down-size. Also, other assets are not counted unless they produce a sustainable income).

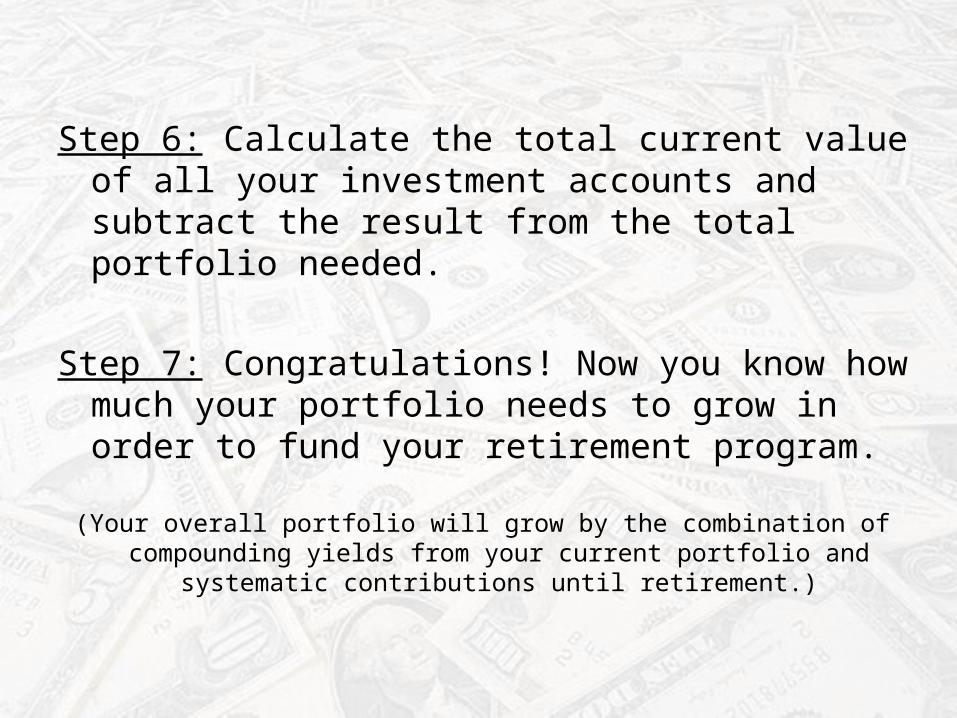

Step 6: Calculate the total current value of all your investment accounts and subtract the result from the total portfolio needed.

Step 7: Congratulations! Now you know how much your portfolio needs to grow in order to fund your retirement program.

(Your overall portfolio will grow by the combination of compounding yields from your current portfolio and systematic contributions until

retirement.)

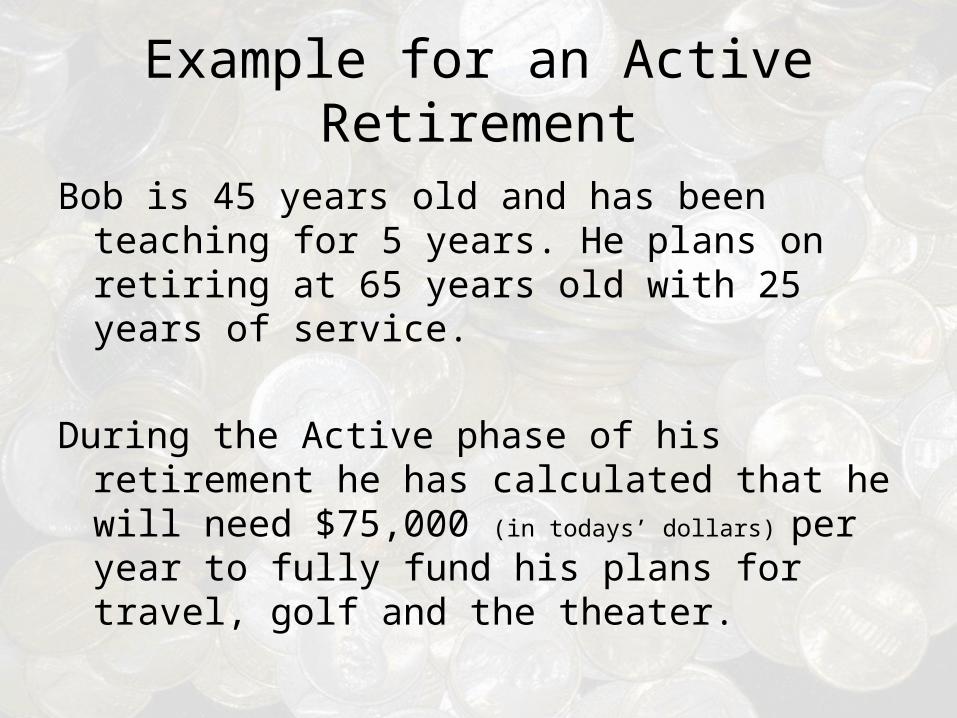

Example for an Active Retirement

Bob is 45 years old and has been teaching for 5 years. He plans on retiring at 65 years old with 25 years of service.

During the Active phase of his retirement he has calculated that he will need $75,000 (in todays’ dollars)

per year to fully fund his plans for travel, golf and the theater.

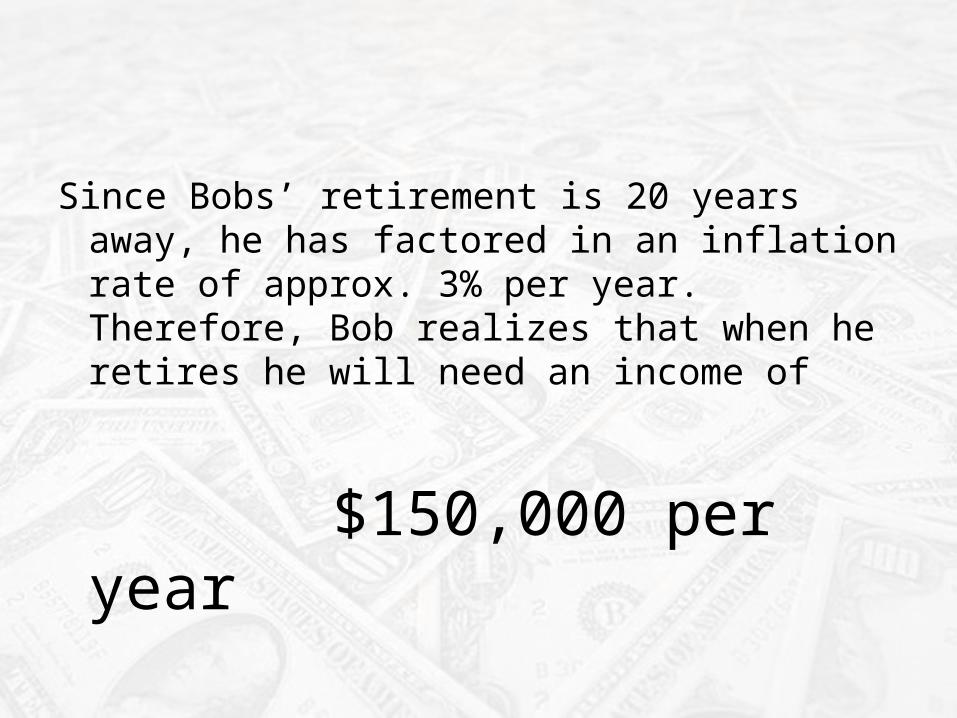

Since Bobs’ retirement is 20 years away, he has factored in an inflation rate of approx. 3% per year. Therefore, Bob realizes that when he retires he will need an income of

$150,000 per year

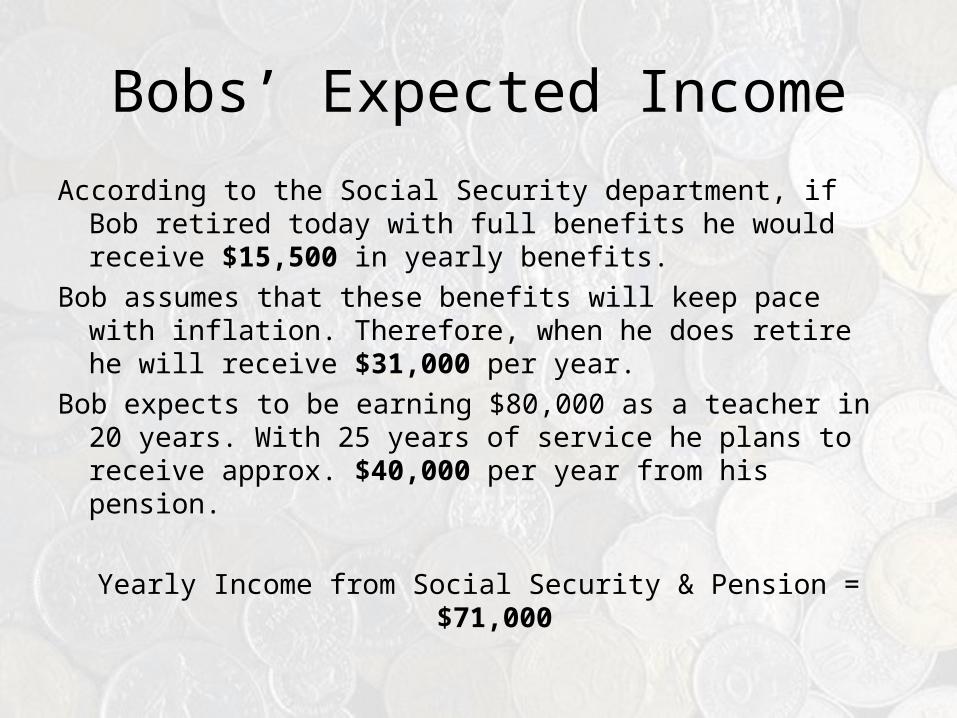

Bobs’ Expected Income

According to the Social Security department, if Bob retired today with full benefits he would receive $15,500 in yearly benefits.

Bob assumes that these benefits will keep pace with inflation. Therefore, when he does retire he will receive $31,000 per year.

Bob expects to be earning $80,000 as a teacher in 20 years. With 25 years of service he plans to receive approx. $40,000 per year from his pension.

Yearly Income from Social Security & Pension = $71,000

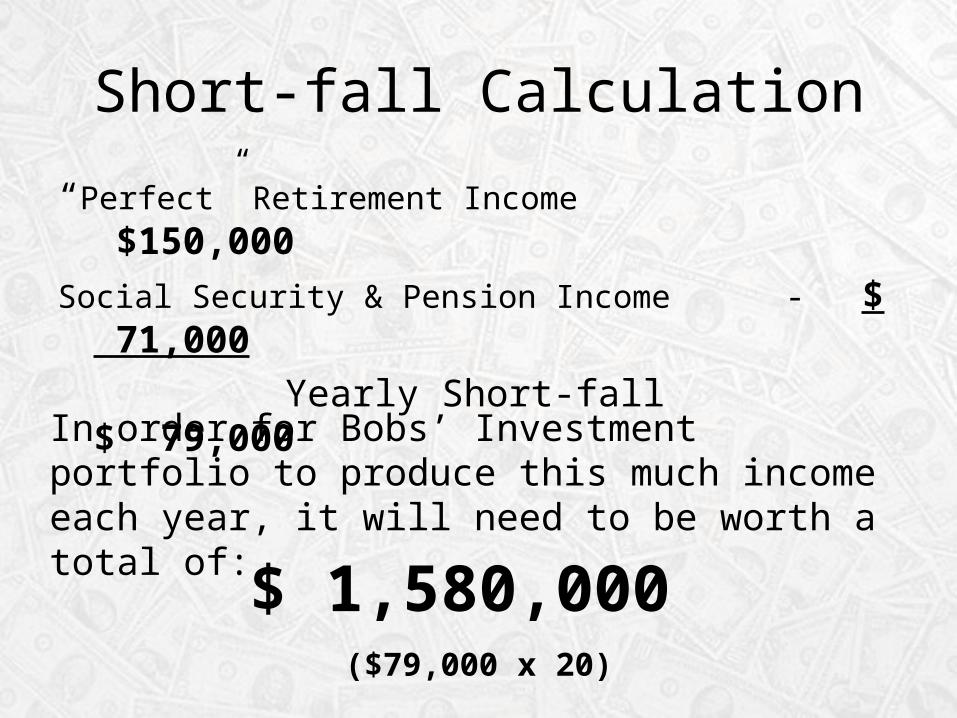

Short-fall Calculation

“Perfect” Retirement Income $150,000

Social Security & Pension Income - $ 71,000

Yearly Short-fall $ 79,000

In order for Bobs’ Investment portfolio to produce this much income each year, it will need to be worth a total of:

$ 1,580,000 ($79,000 x 20)

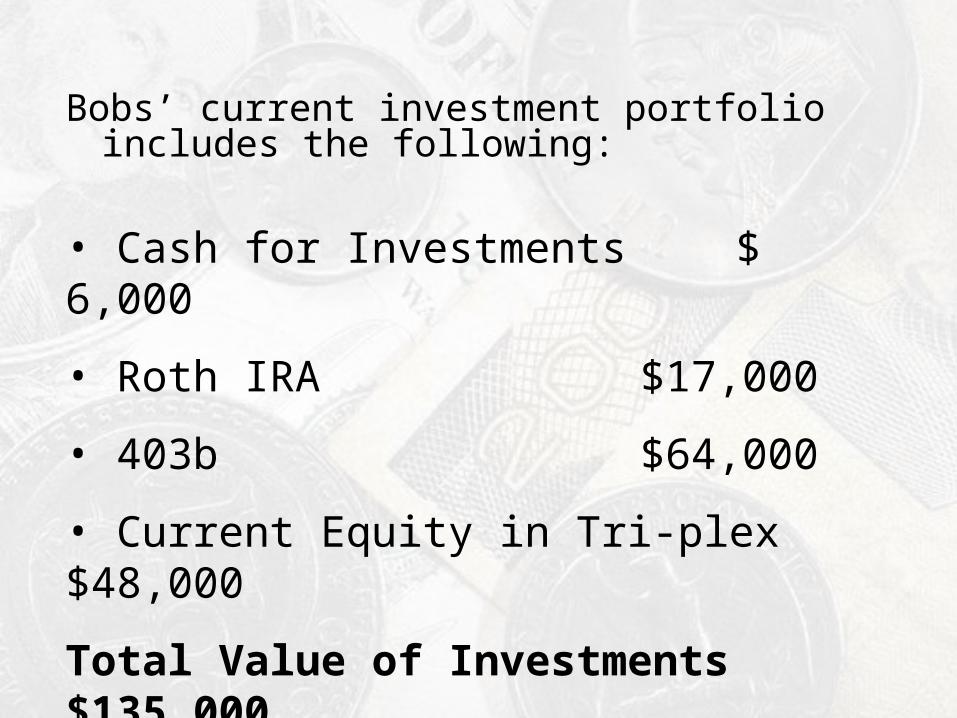

Bobs’ current investment portfolio includes the following:

• Cash for Investments $ 6,000

• Roth IRA $17,000

• 403b $64,000

• Current Equity in Tri-plex $48,000

Total Value of Investments $135,000

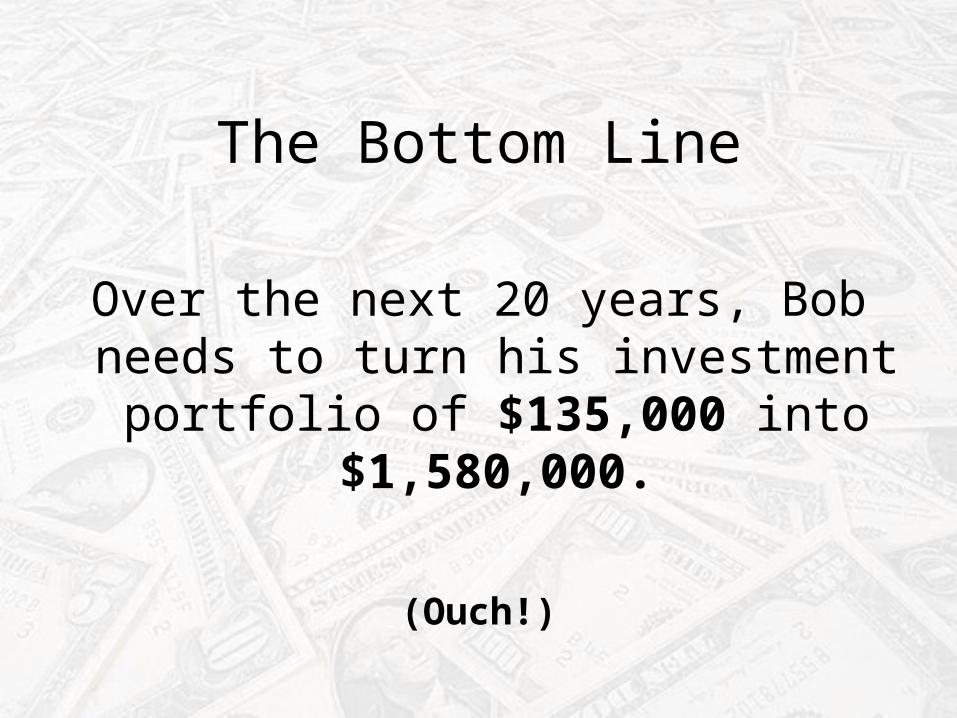

The Bottom Line

Over the next 20 years, Bob needs to turn his investment portfolio of

$135,000 into $1,580,000.

(Ouch!)

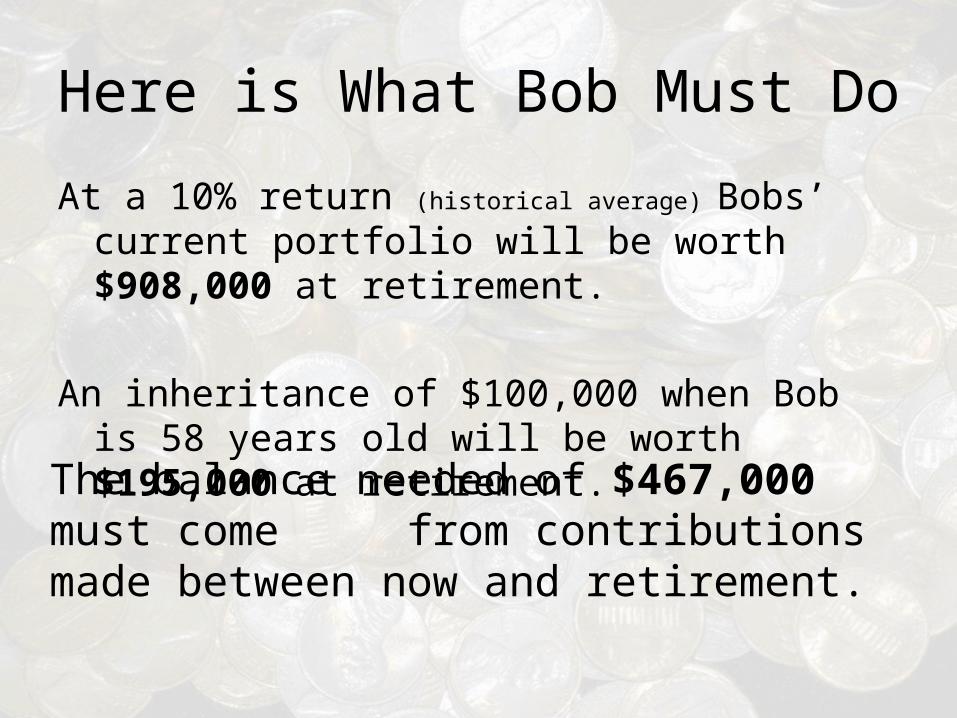

Here is What Bob Must Do

At a 10% return (historical average) Bobs’ current portfolio will be worth $908,000 at retirement.

An inheritance of $100,000 when Bob is 58 years old will be worth $195,000 at retirement.

The balance needed of $467,000 must come from contributions made between now and retirement.

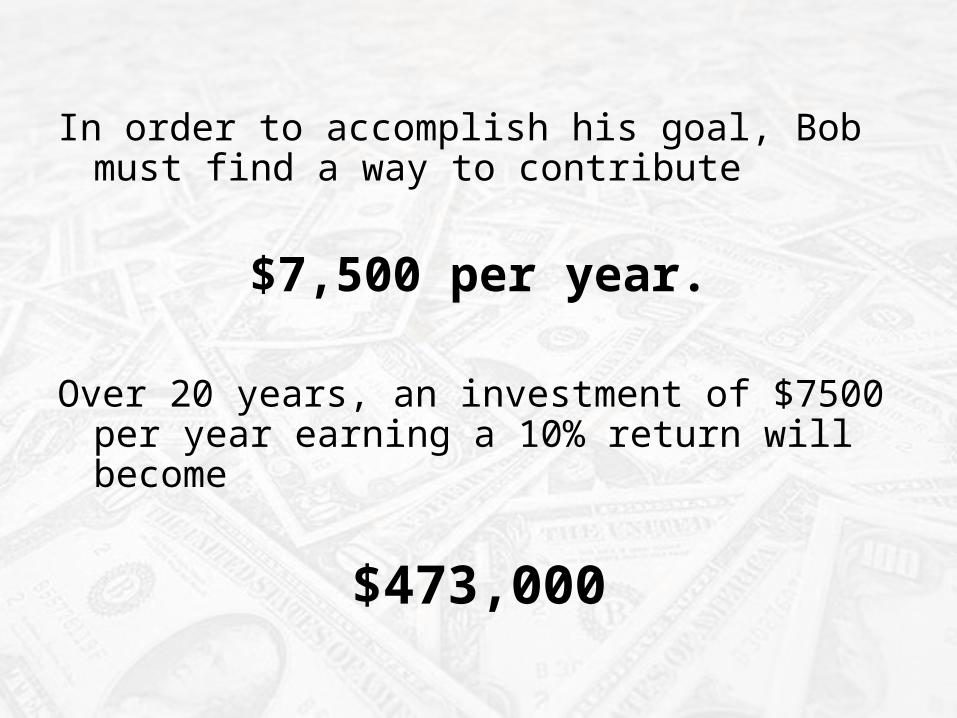

In order to accomplish his goal, Bob must find a way to contribute

$7,500 per year.

Over 20 years, an investment of $7500 per year earning a 10% return will become

$473,000

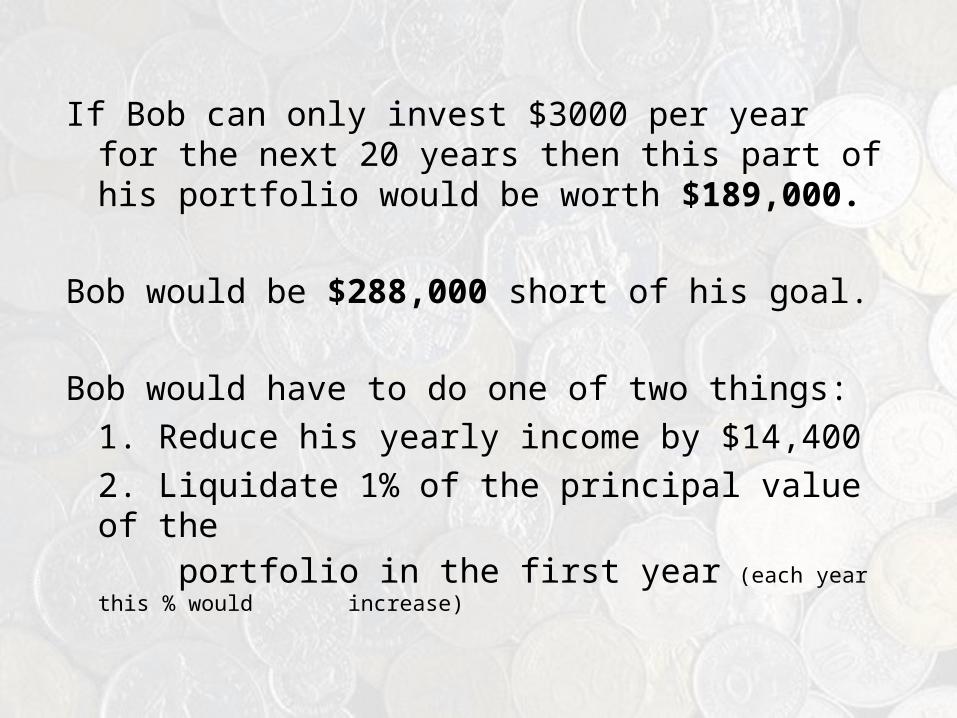

If Bob can only invest $3000 per year for the next 20 years then this part of his portfolio would be worth $189,000.

Bob would be $288,000 short of his goal.

Bob would have to do one of two things:

1. Reduce his yearly income by $14,400

2. Liquidate 1% of the principal value of the

portfolio in the first year (each year this % would increase)

Investing

For the

Long Haul

Section 2

Question : When should you Start Investing?

Answer:

the SOONER the BETTER!

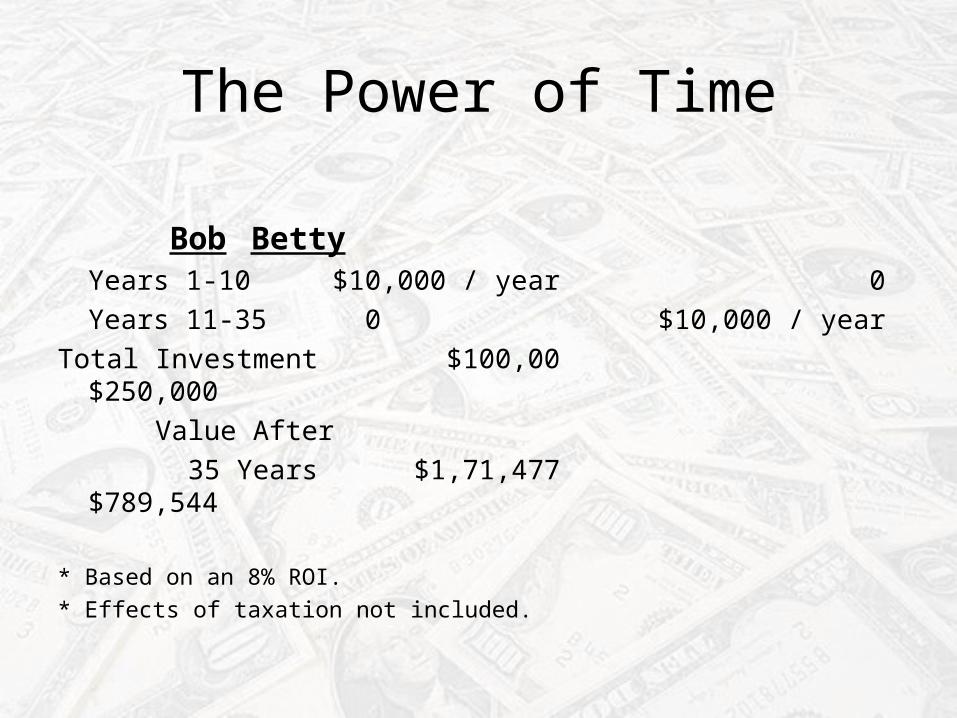

The Power of Time

Bob BettyYears 1-10 $10,000 / year 0

Years 11-35 0 $10,000 / year

Total Investment $100,00 $250,000

Value After

35 Years $1,71,477 $789,544

* Based on an 8% ROI.

* Effects of taxation not included.

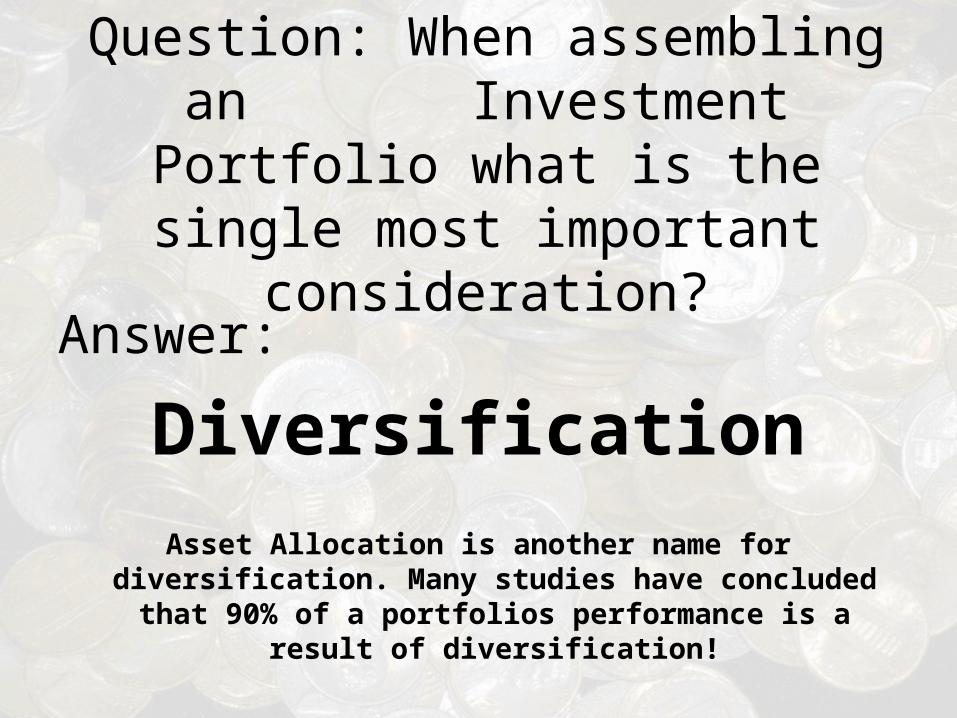

Question: When assembling an Investment Portfolio what is the

single most important consideration?

Answer:

DiversificationAsset Allocation is another name for diversification.

Many studies have concluded that 90% of a portfolios performance is a result of diversification!

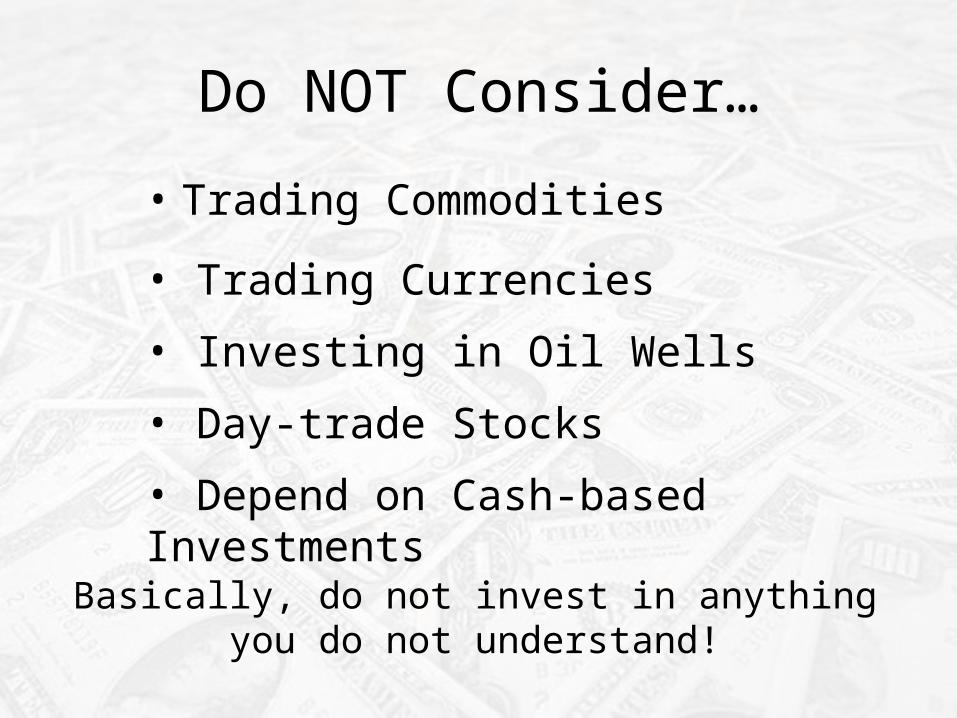

Do NOT Consider…

• Trading Commodities

• Trading Currencies

• Investing in Oil Wells

• Day-trade Stocks

• Depend on Cash-based Investments

Basically, do not invest in anything you do not understand!

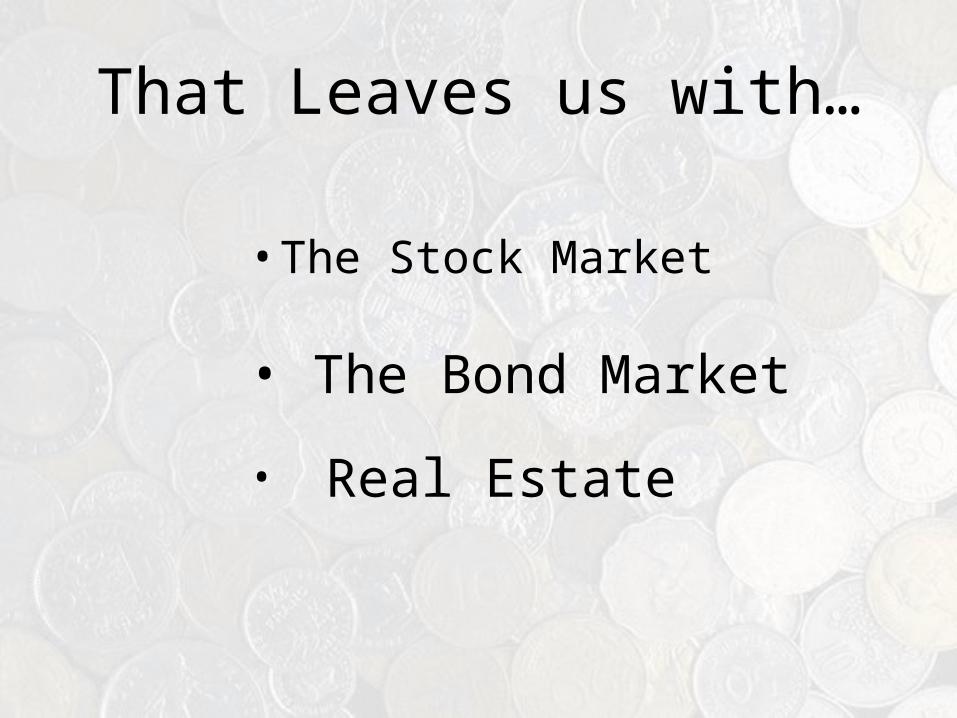

That Leaves us with…

• The Stock Market

• The Bond Market

• Real Estate

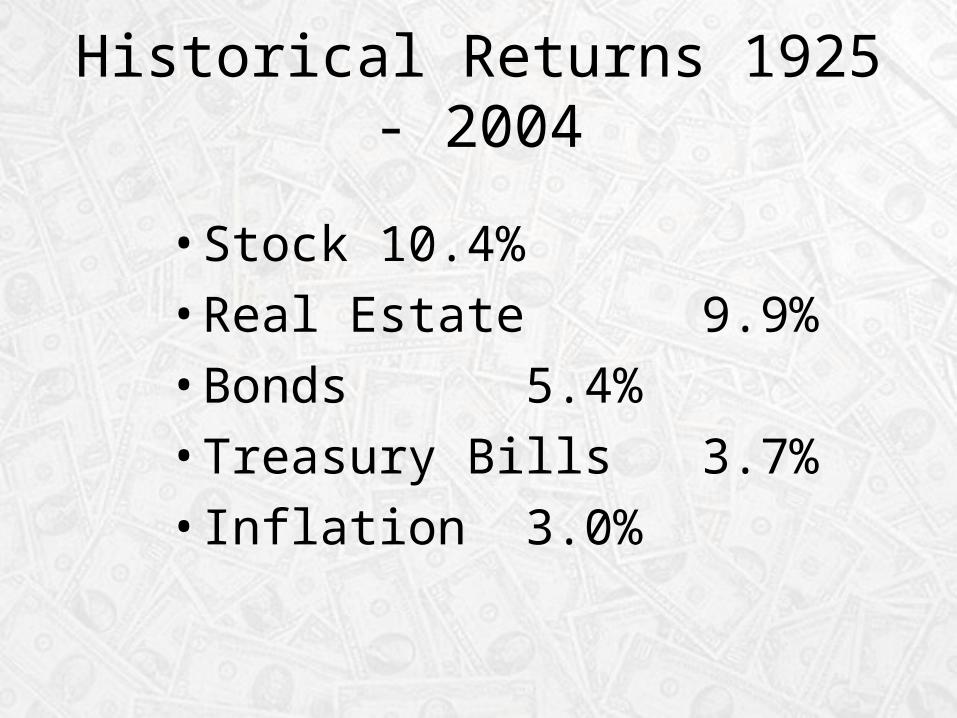

Historical Returns 1925 - 2004

• Stock 10.4%

• Real Estate 9.9%

• Bonds 5.4%

• Treasury Bills 3.7%

• Inflation 3.0%

Cash-Based Investments(Savings Accounts, CDs, Treasury Bills, Etc.)

These investments do not provide enough returns to truly outpace

Inflation over time.

Always have an Emergency Fund in Cash

(2-3 months of expenses)

Bonds

Bonds are conservative, income-producing investments suitable in or near retirement.

During the Growth phase they should represent a relatively small part (if any) of

an investment portfolio.

Real Estate

Investment Real Estate should be a part of every truly diversified investment portfolio.

It has a number of unique and powerful advantages over other types of

investments.

Some advantages include Preferential Tax treatment, Immunity from “Bear” markets and LEVERAGE.

Stock Market Investment Vehicles

• 401k / 403b

• Traditional IRA

• Roth IRA

• Taxable Accounts

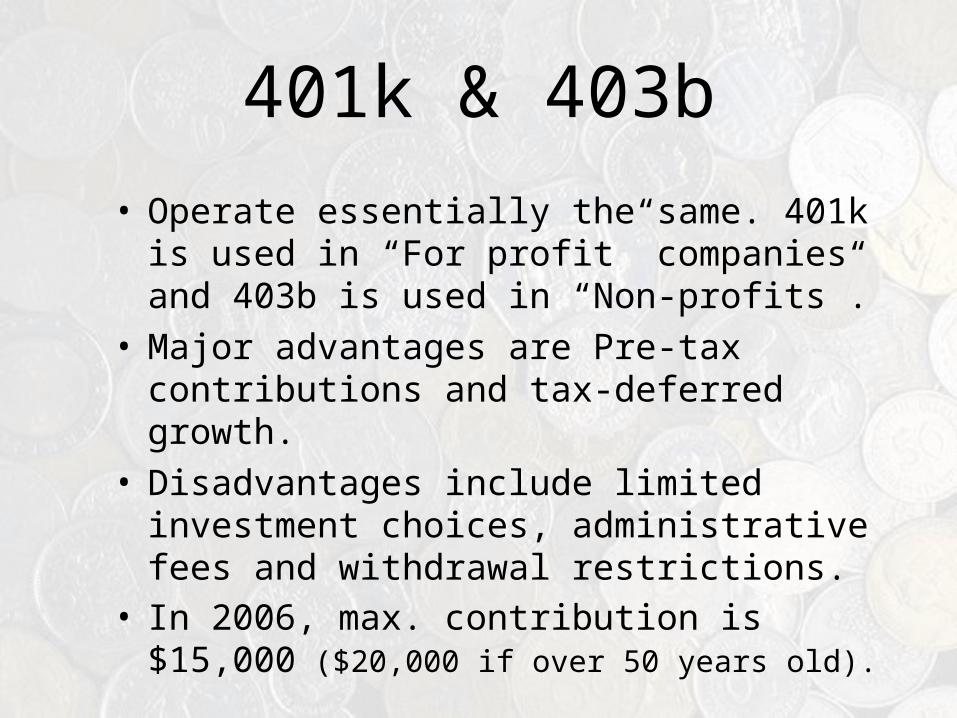

401k & 403b

• Operate essentially the same. 401k is used in “For profit” companies and 403b is used in “Non-profits”.

• Major advantages are Pre-tax contributions and tax-deferred growth.

• Disadvantages include limited investment choices, administrative fees and withdrawal restrictions.

• In 2006, max. contribution is $15,000 ($20,000 if over 50 years old).

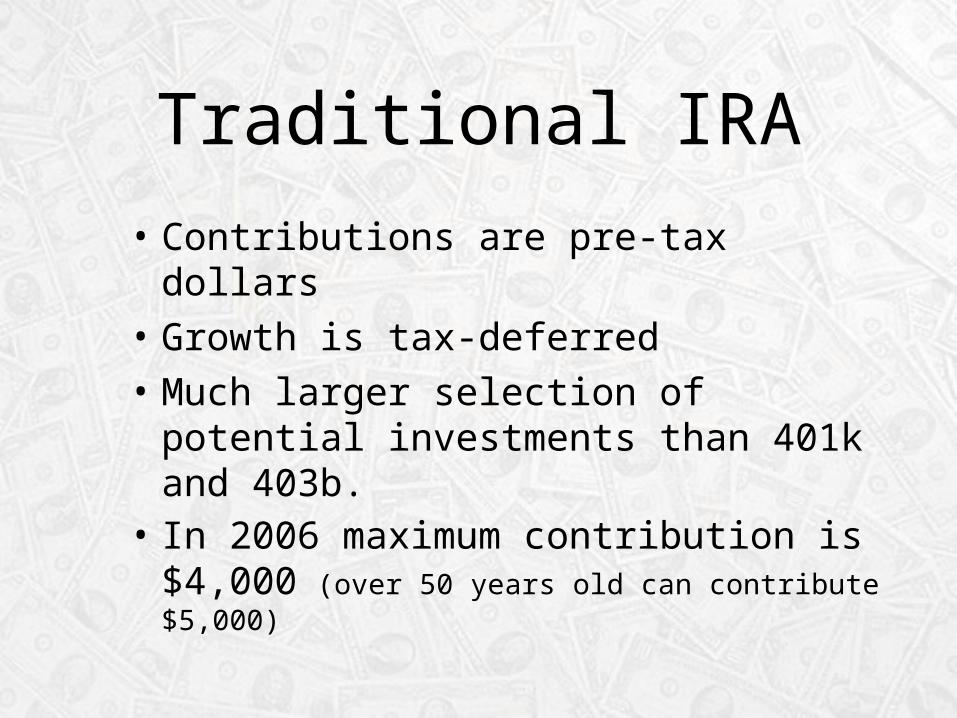

Traditional IRA

• Contributions are pre-tax dollars

• Growth is tax-deferred

• Much larger selection of potential investments than 401k and 403b.

• In 2006 maximum contribution is $4,000 (over 50 years old can contribute $5,000)

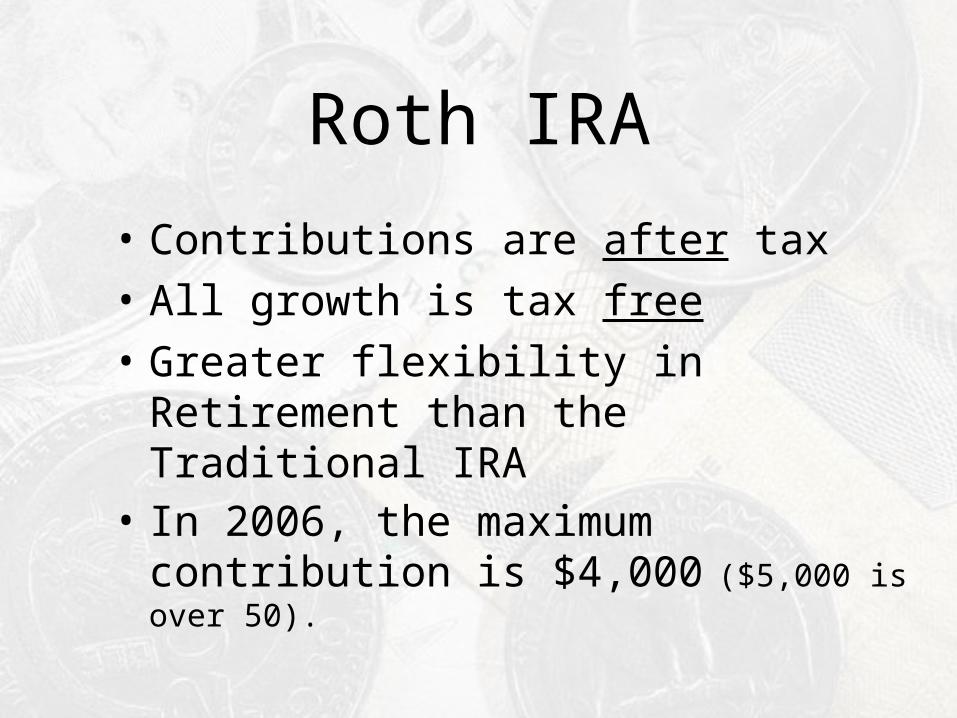

Roth IRA

• Contributions are after tax

• All growth is tax free

• Greater flexibility in Retirement than the Traditional IRA

• In 2006, the maximum contribution is $4,000 ($5,000 is over 50).

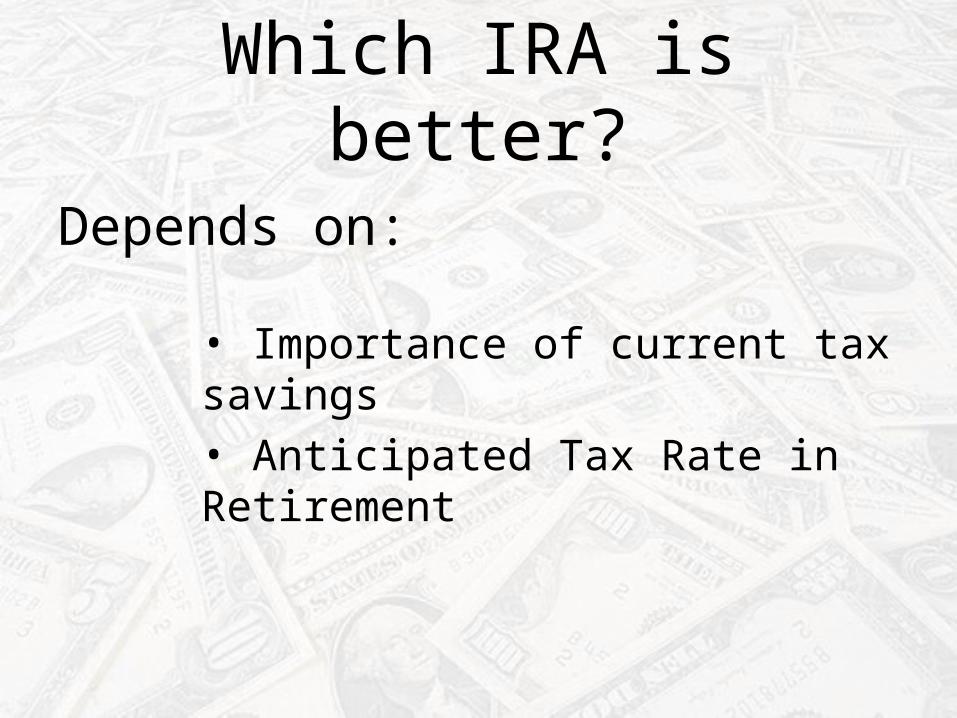

Which IRA is better?

Depends on:

• Importance of current tax savings

• Anticipated Tax Rate in Retirement

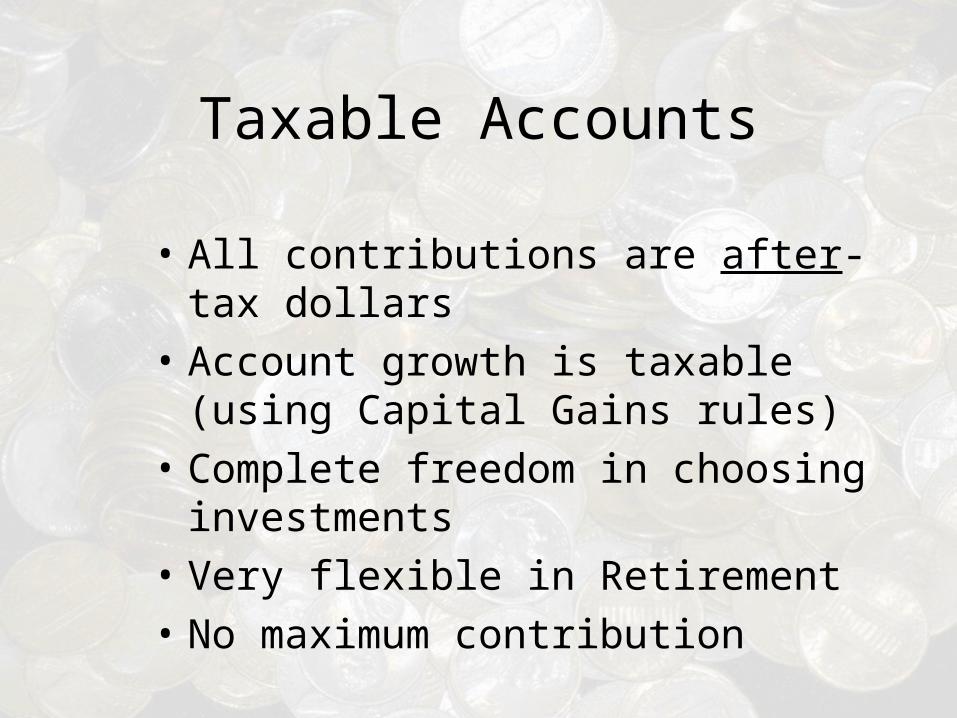

Taxable Accounts

• All contributions are after-tax dollars

• Account growth is taxable (using Capital Gains rules)

• Complete freedom in choosing investments

• Very flexible in Retirement

• No maximum contribution

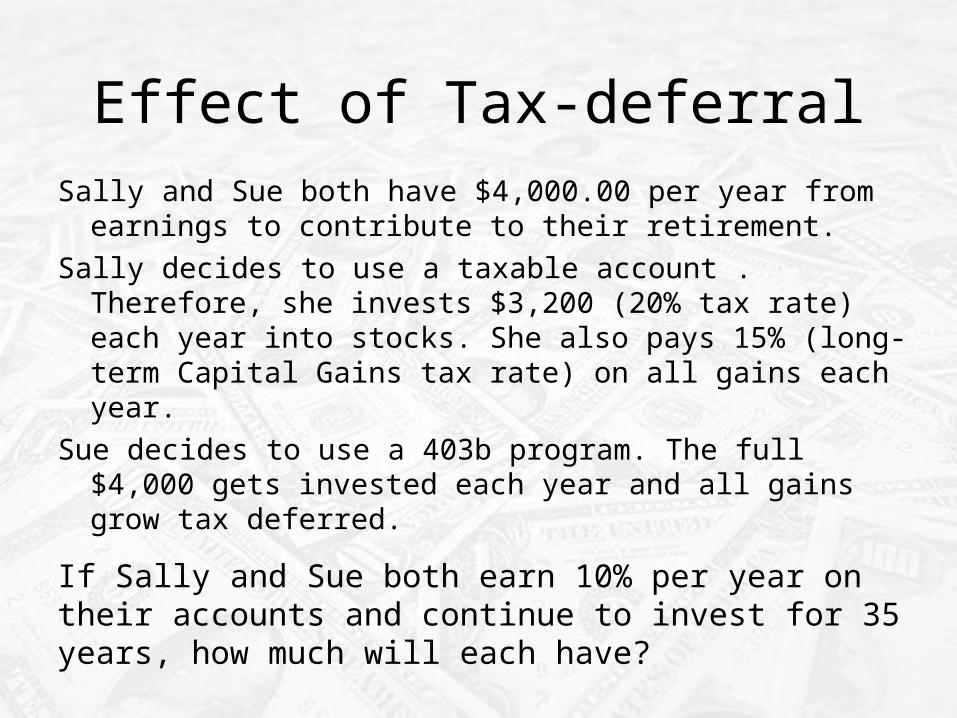

Effect of Tax-deferralSally and Sue both have $4,000.00 per year from earnings

to contribute to their retirement.

Sally decides to use a taxable account . Therefore, she invests $3,200 (20% tax rate) each year into stocks. She also pays 15% (long-term Capital Gains tax rate) on all gains each year.

Sue decides to use a 403b program. The full $4,000 gets invested each year and all gains grow tax deferred.

If Sally and Sue both earn 10% per year on their accounts and continue to invest for 35 years, how much will each have?

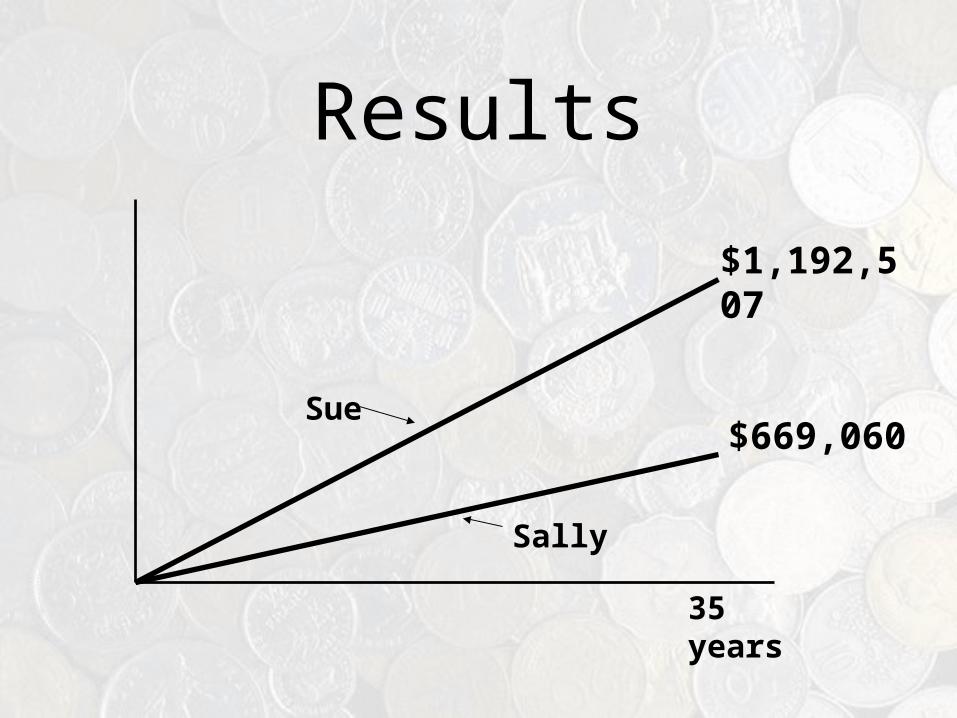

Results

Sue

Sally

$1,192,507

$669,060

35 years

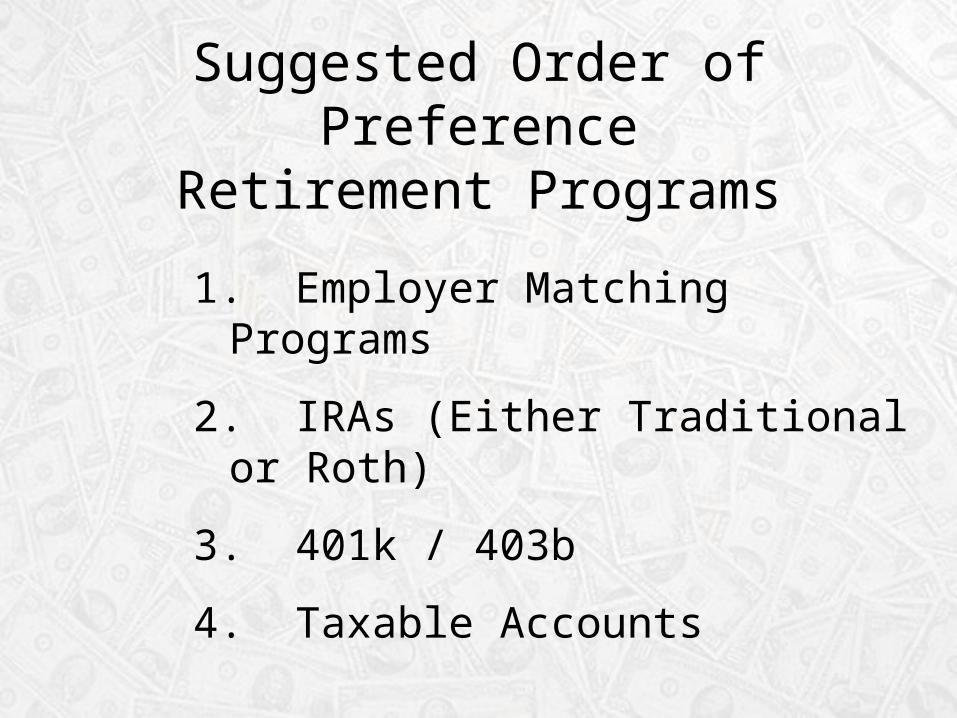

Suggested Order of PreferenceRetirement Programs

1. Employer Matching Programs

2. IRAs (Either Traditional or Roth)

3. 401k / 403b

4. Taxable Accounts

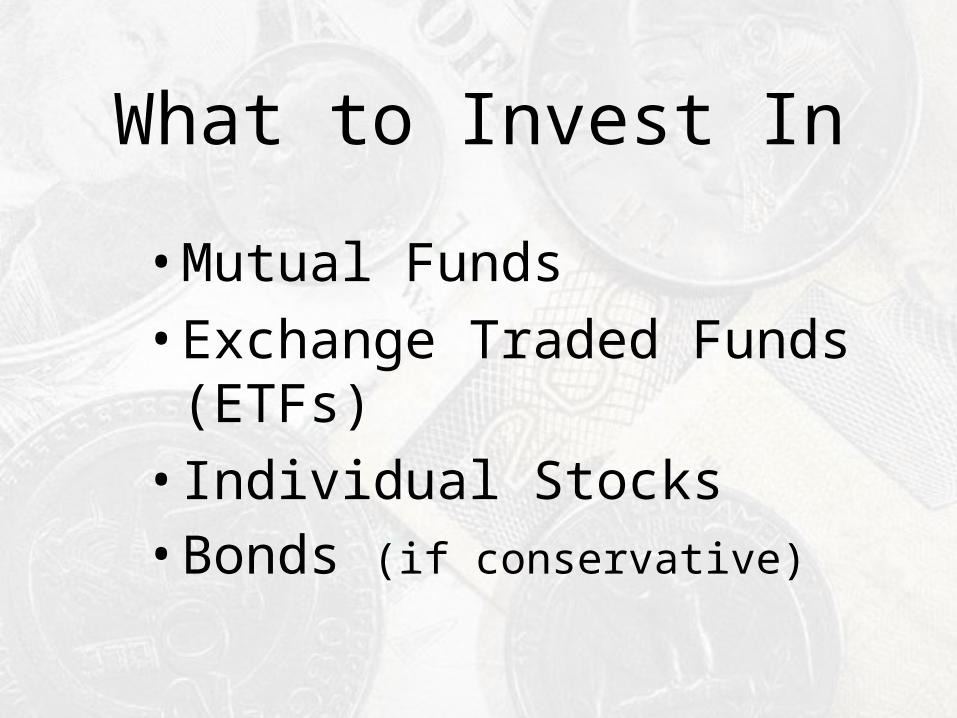

What to Invest In

• Mutual Funds

• Exchange Traded Funds (ETFs)

• Individual Stocks• Bonds (if conservative)

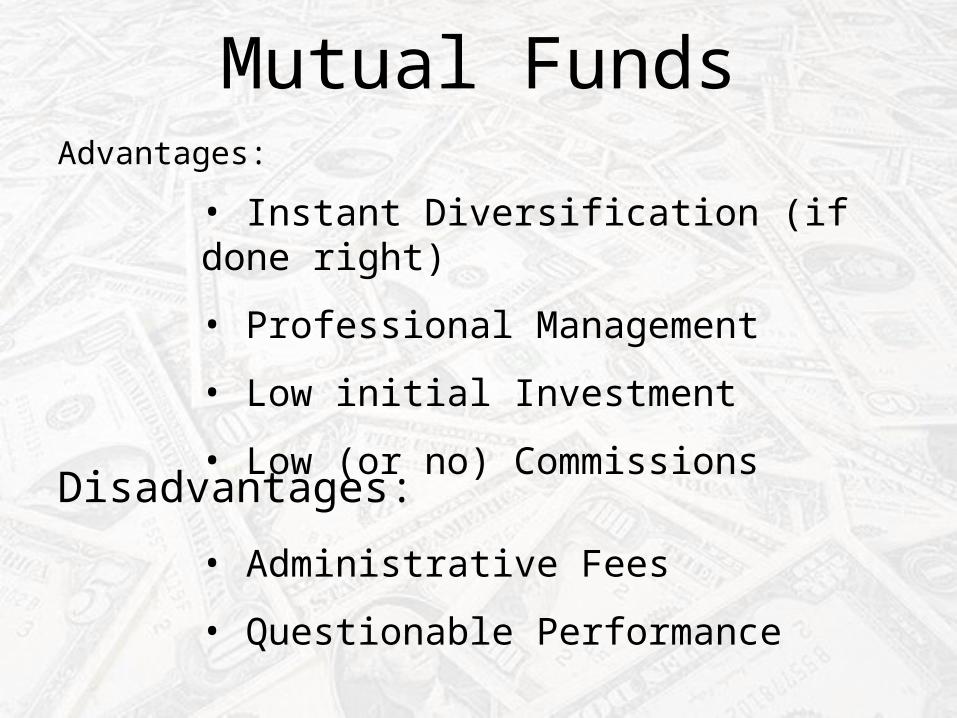

Mutual FundsAdvantages:

• Instant Diversification (if done right)

• Professional Management

• Low initial Investment

• Low (or no) Commissions

Disadvantages:

• Administrative Fees

• Questionable Performance

ETFsAdvantages:

• Same diversification as Mutual Funds

• Trade like stocks

• Low Administrative fees

• No “hidden” Capital Gains

Disadvantages:

• Purchase and Sale commissions

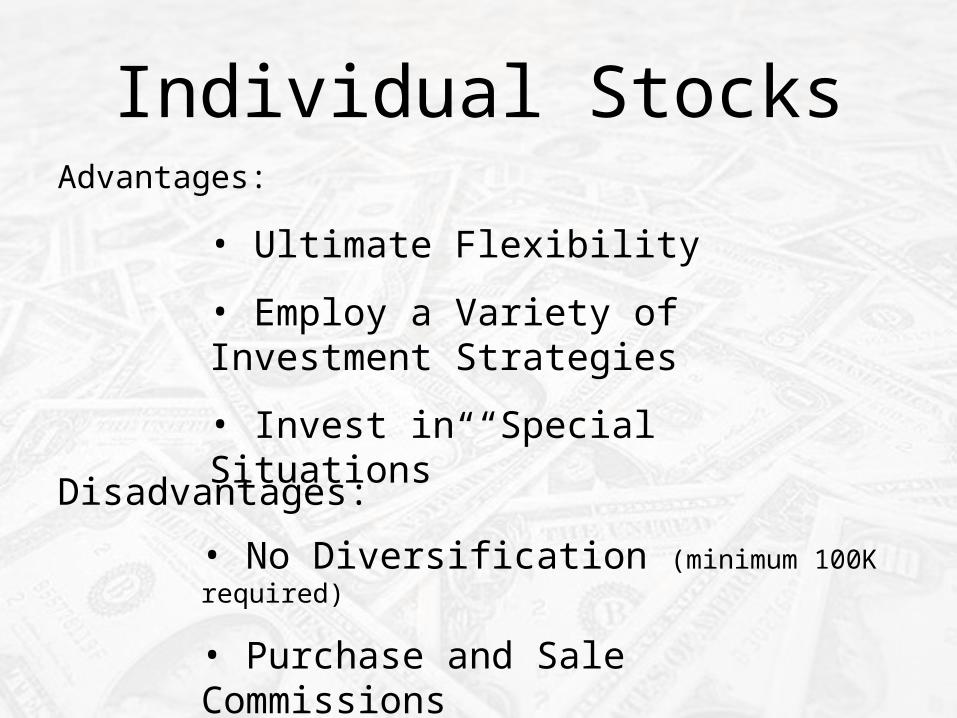

Individual StocksAdvantages:

• Ultimate Flexibility

• Employ a Variety of Investment Strategies

• Invest in “Special Situations”

Disadvantages:

• No Diversification (minimum 100K required)

• Purchase and Sale Commissions

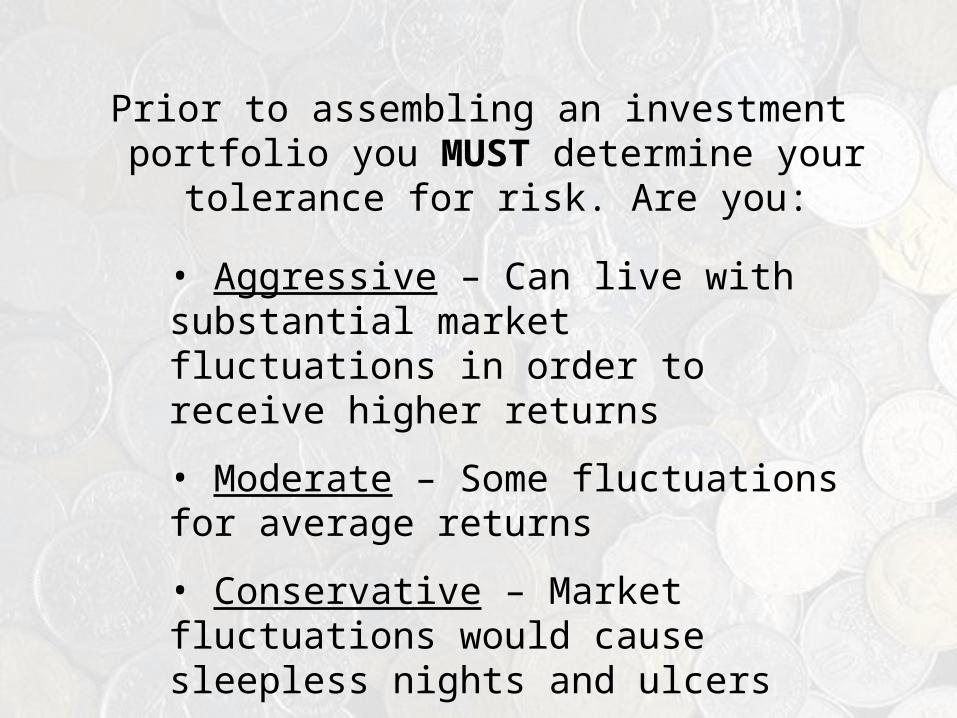

Prior to assembling an investment portfolio you MUST determine your tolerance for risk. Are

you:

• Aggressive – Can live with substantial market fluctuations in order to receive higher returns

• Moderate – Some fluctuations for average returns

• Conservative – Market fluctuations would cause sleepless nights and ulcers

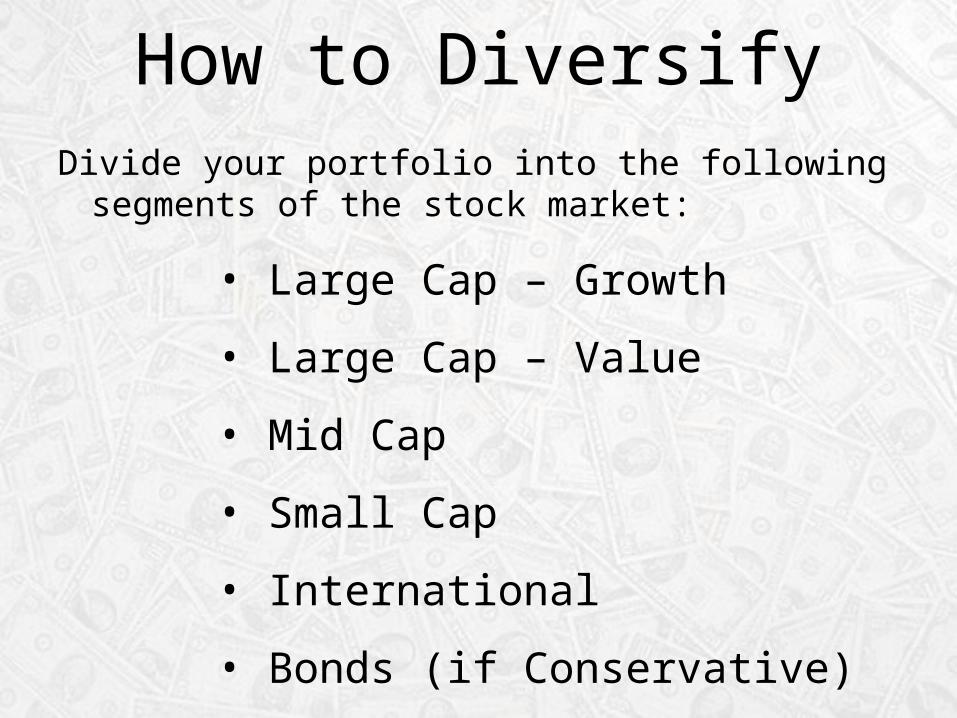

How to DiversifyDivide your portfolio into the following segments of

the stock market:

• Large Cap – Growth

• Large Cap – Value

• Mid Cap

• Small Cap

• International

• Bonds (if Conservative)

At various times each of these segments will “lead the market” while others will lag. By diversifying you will always achieve a blended return.

Over time this approach will always produce better returns than a concentrated portfolio.

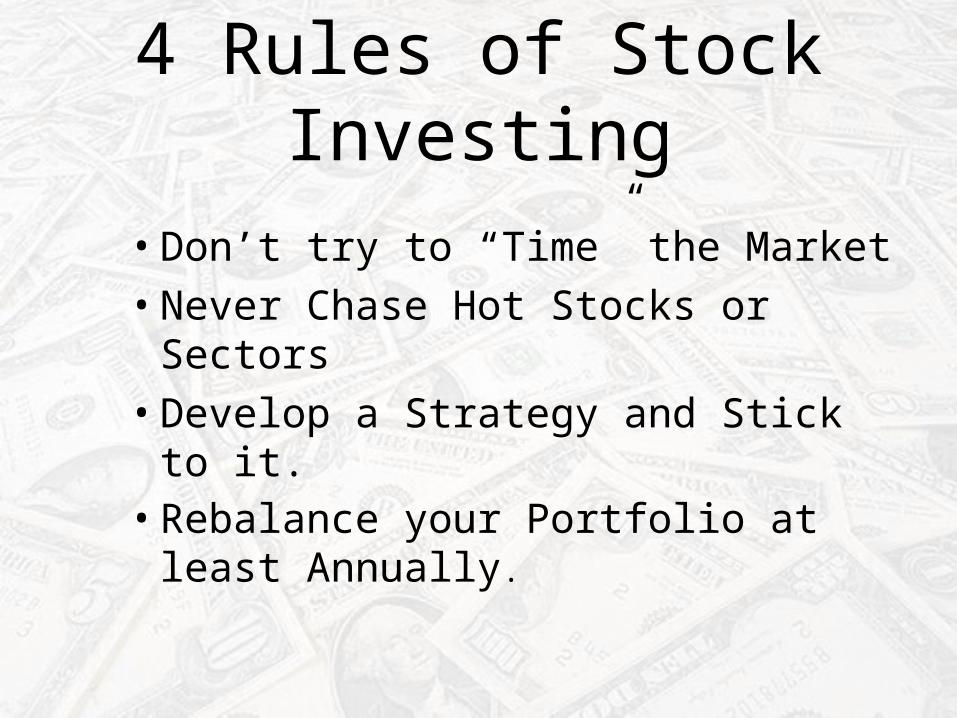

4 Rules of Stock Investing

• Don’t try to “Time” the Market

• Never Chase Hot Stocks or Sectors

• Develop a Strategy and Stick to it.• Rebalance your Portfolio at least

Annually.

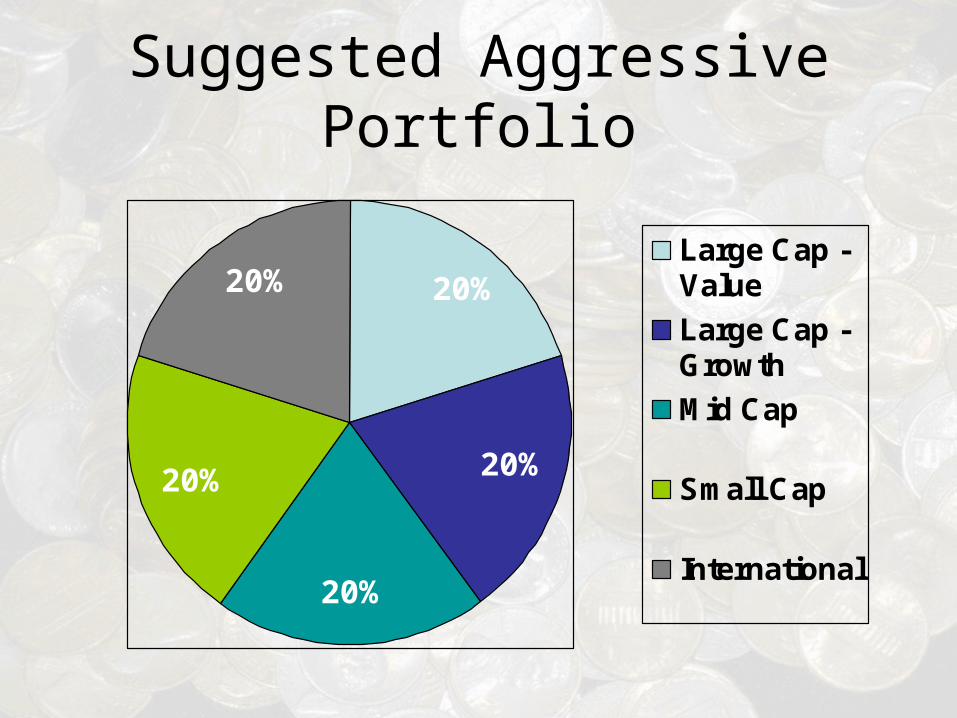

Suggested Aggressive Portfolio

Large Cap -Value

Large Cap -Growth

Mid Cap

Small Cap

International

20%

20%

20%

20%

20%

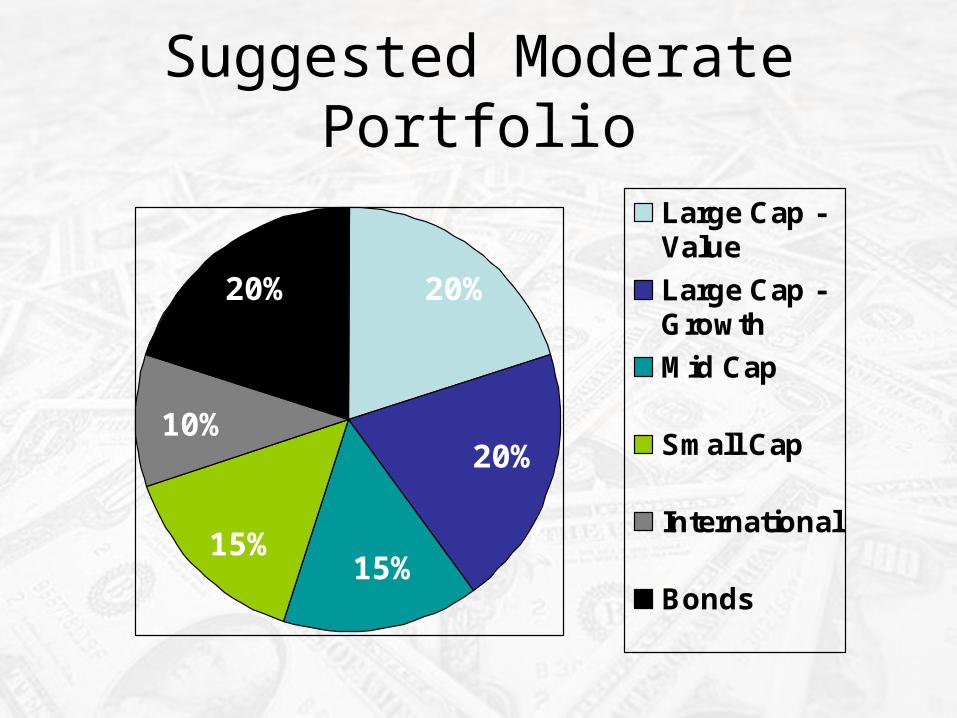

Suggested Moderate Portfolio

Large Cap -Value

Large Cap -Growth

Mid Cap

Small Cap

International

Bonds

20%

20%

20%

10%

15%15%

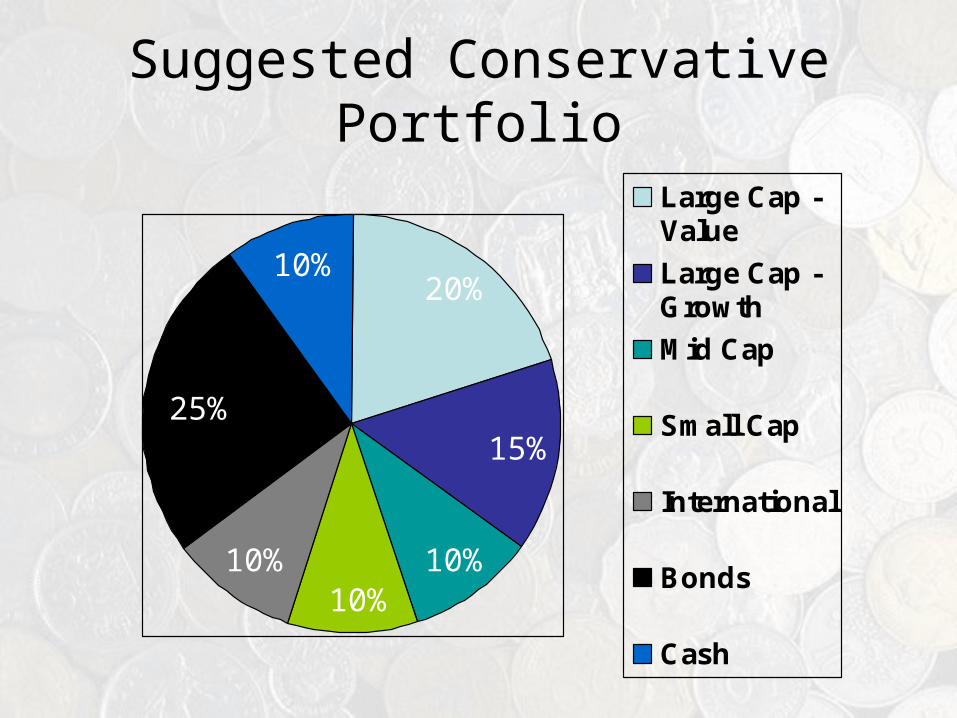

Suggested Conservative Portfolio

Large Cap -Value

Large Cap -Growth

Mid Cap

Small Cap

International

Bonds

Cash

20%

10%10%

10%

25%

10%

15%

The End

Real EstateInvesting

Section 3

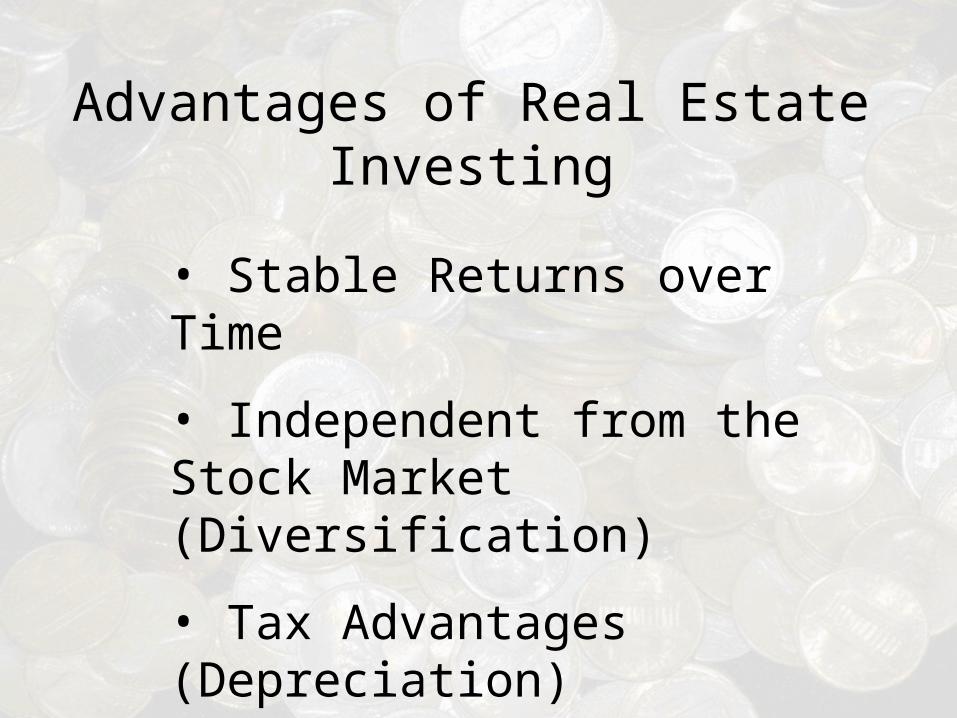

Advantages of Real Estate Investing

• Stable Returns over Time

• Independent from the Stock Market (Diversification)

• Tax Advantages (Depreciation)

• LEVERAGE

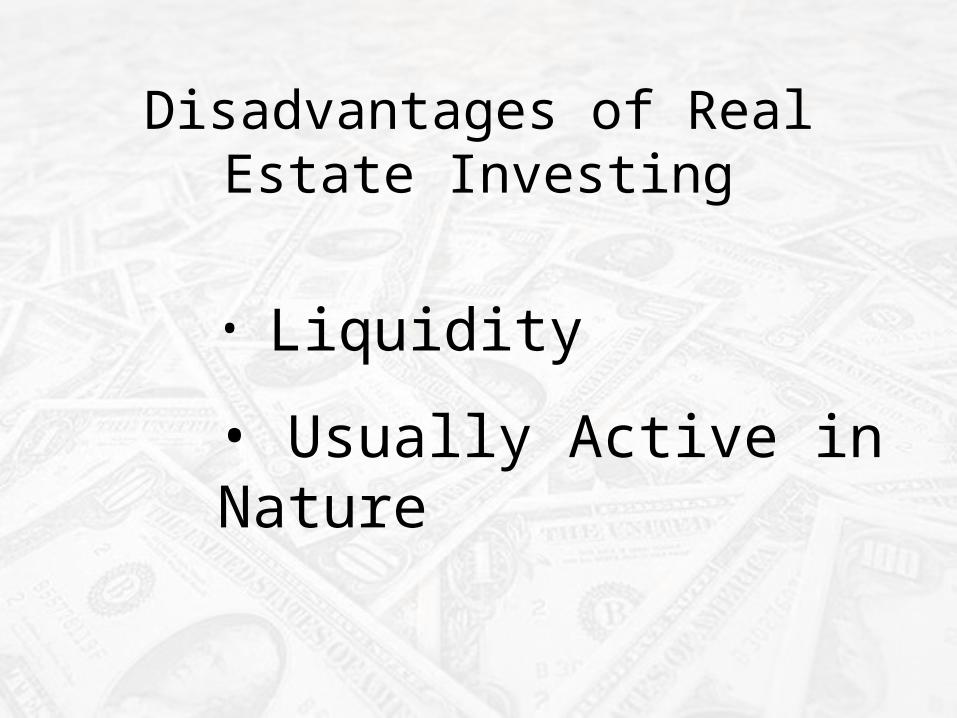

Disadvantages of Real Estate Investing

• Liquidity

• Usually Active in Nature

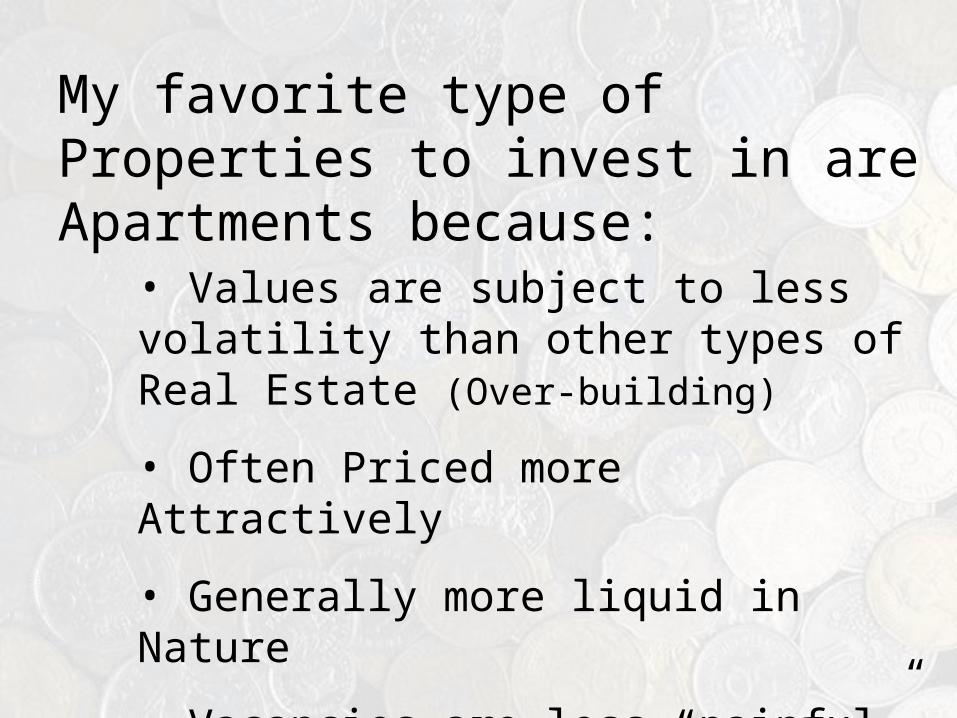

My favorite type of Properties to invest in are Apartments because:

• Values are subject to less volatility than other types of Real Estate (Over-building)

• Often Priced more Attractively

• Generally more liquid in Nature

• Vacancies are less “painful” and turnover much faster

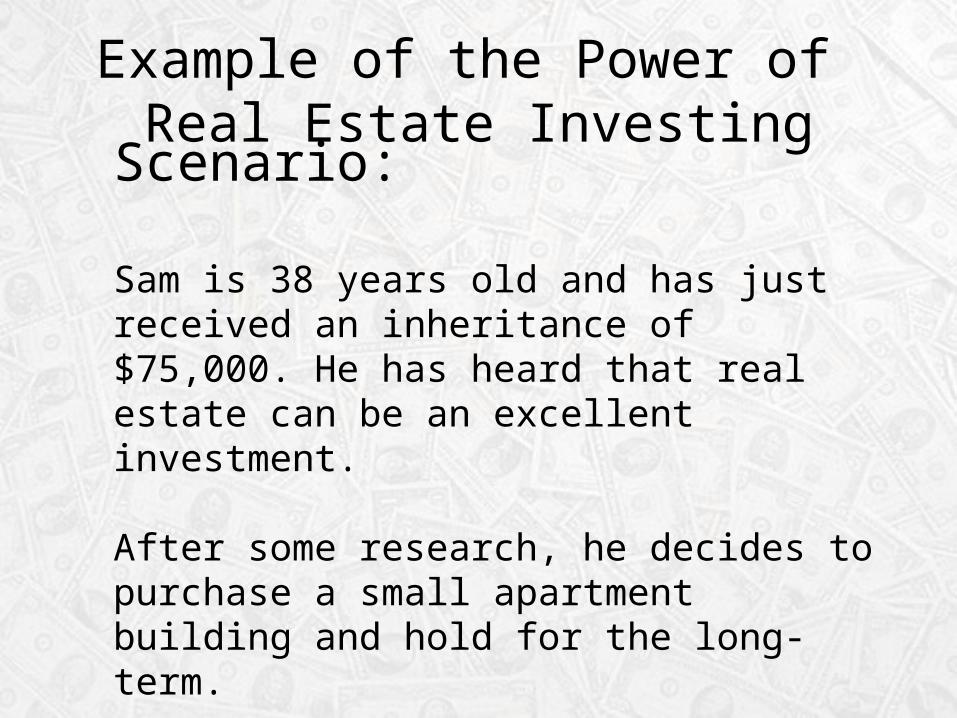

Example of the Power of Real Estate Investing

Scenario:

Sam is 38 years old and has just received an inheritance of $75,000. He has heard that real estate can be an excellent investment.

After some research, he decides to purchase a small apartment building and hold for the long-term.

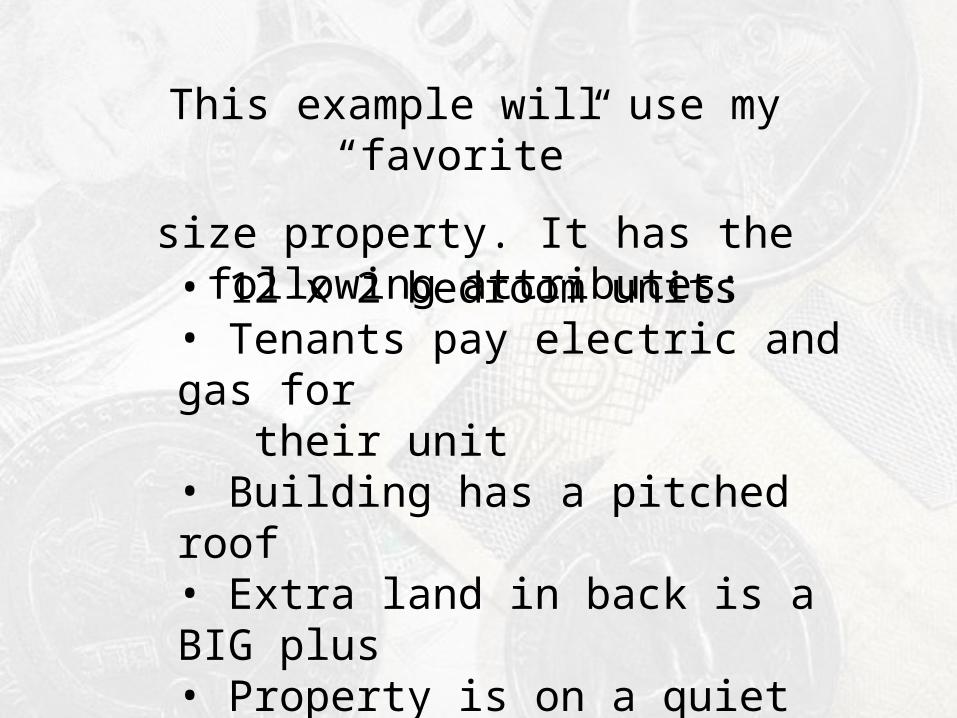

This example will use my “favorite”

size property. It has the following attributes:

• 12 x 2 bedroom units• Tenants pay electric and gas for their unit• Building has a pitched roof• Extra land in back is a BIG plus• Property is on a quiet street in an excellent area of the city

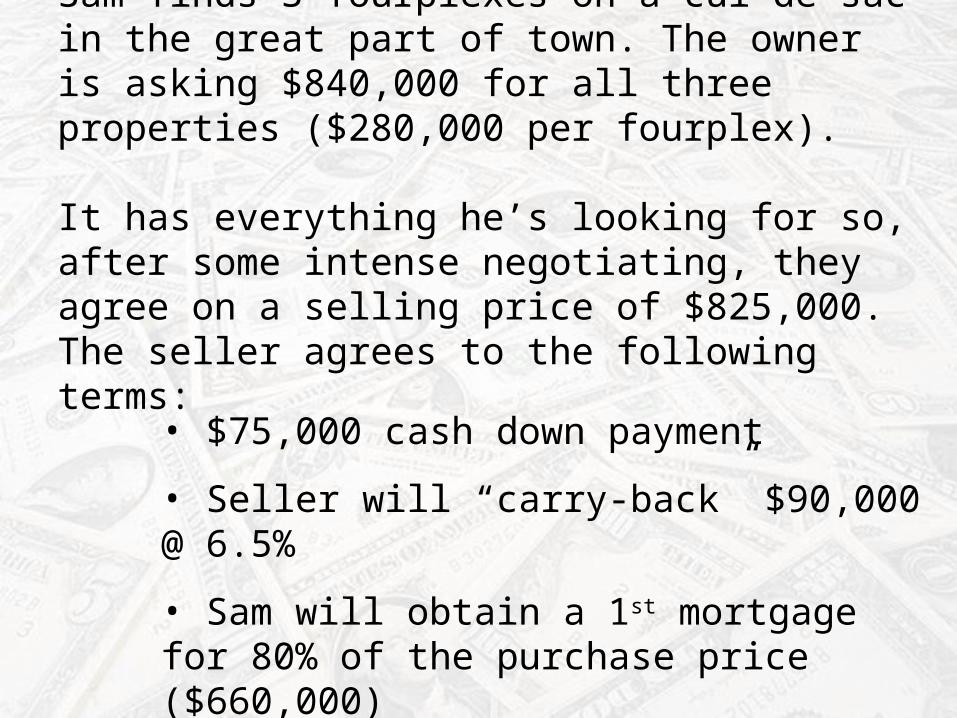

Sam finds 3 fourplexes on a cul-de-sac in the great part of town. The owner is asking $840,000 for all three properties ($280,000 per fourplex).

It has everything he’s looking for so, after some intense negotiating, they agree on a selling price of $825,000. The seller agrees to the following terms:

• $75,000 cash down payment

• Seller will “carry-back” $90,000 @ 6.5%

• Sam will obtain a 1st mortgage for 80% of the purchase price ($660,000)

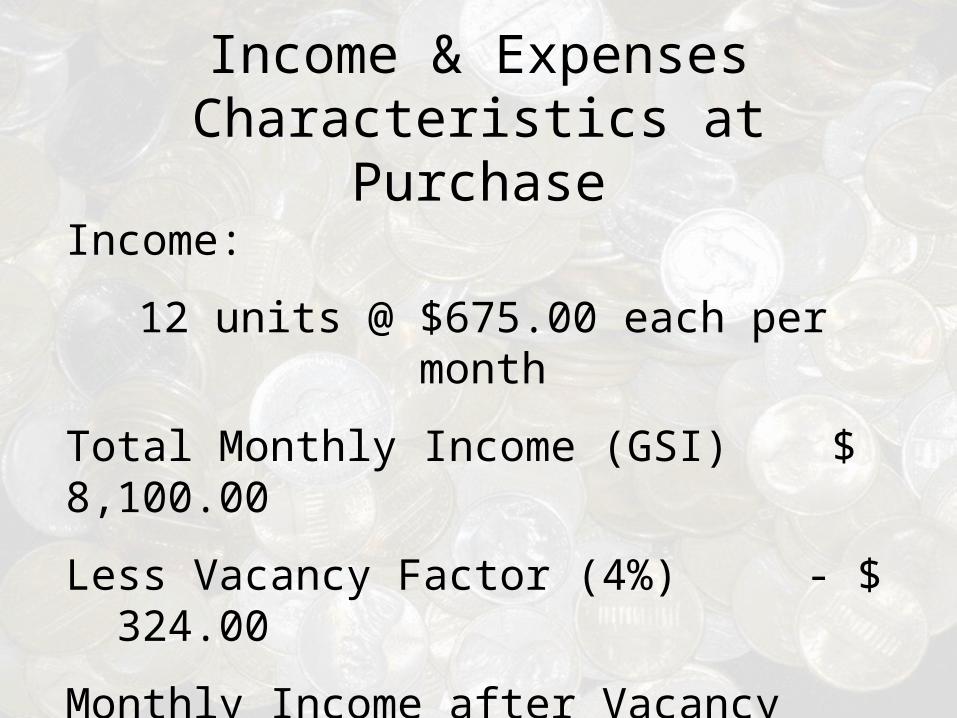

Income & Expenses Characteristics at Purchase

Income:

12 units @ $675.00 each per month

Total Monthly Income (GSI) $ 8,100.00

Less Vacancy Factor (4%) - $ 324.00

Monthly Income after Vacancy $7,786.00

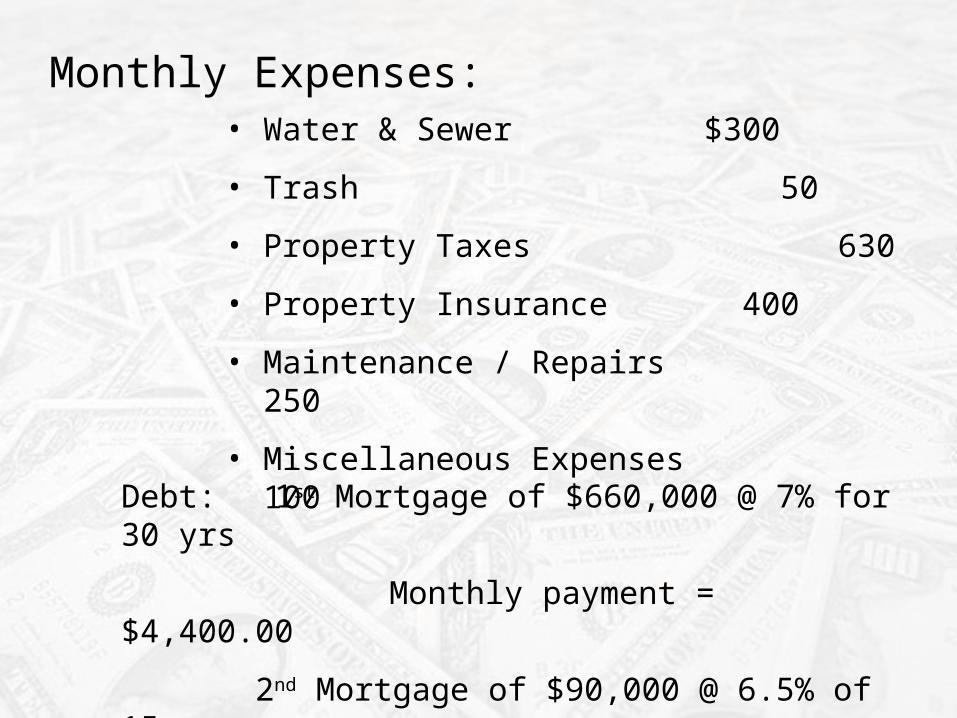

Monthly Expenses:• Water & Sewer $300

• Trash 50

• Property Taxes 630

• Property Insurance 400

• Maintenance / Repairs 250

• Miscellaneous Expenses 100

Debt: 1st Mortgage of $660,000 @ 7% for 30 yrs

Monthly payment = $4,400.00

2nd Mortgage of $90,000 @ 6.5% of 15 yrs

Monthly payment = $ 785.00

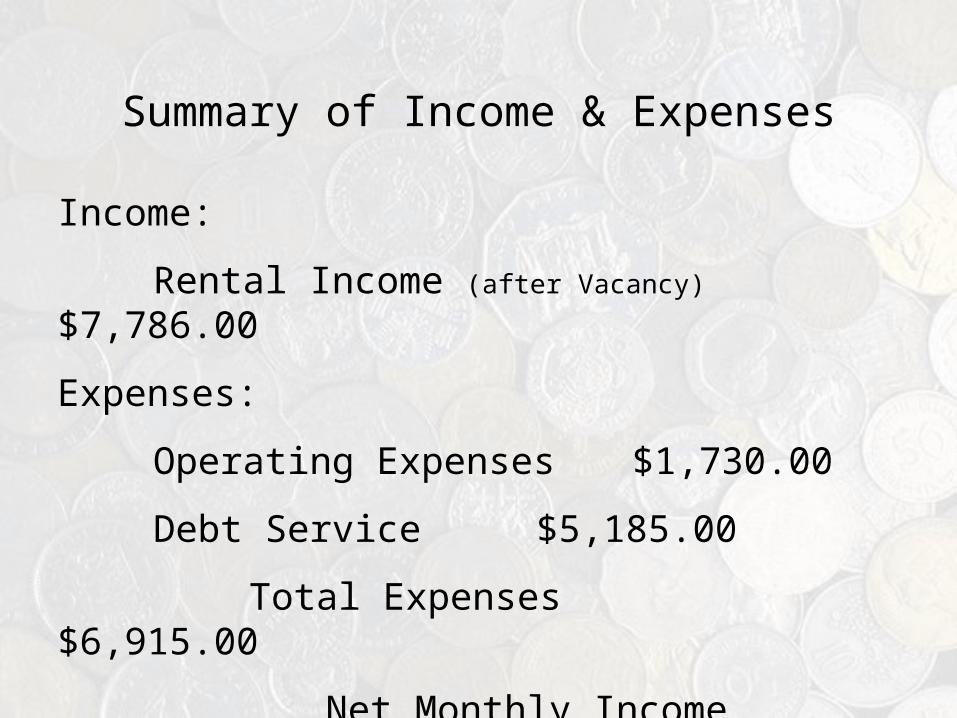

Summary of Income & Expenses

Income:

Rental Income (after Vacancy) $7,786.00

Expenses:

Operating Expenses $1,730.00

Debt Service $5,185.00

Total Expenses $6,915.00

Net Monthly Income $ 871.00

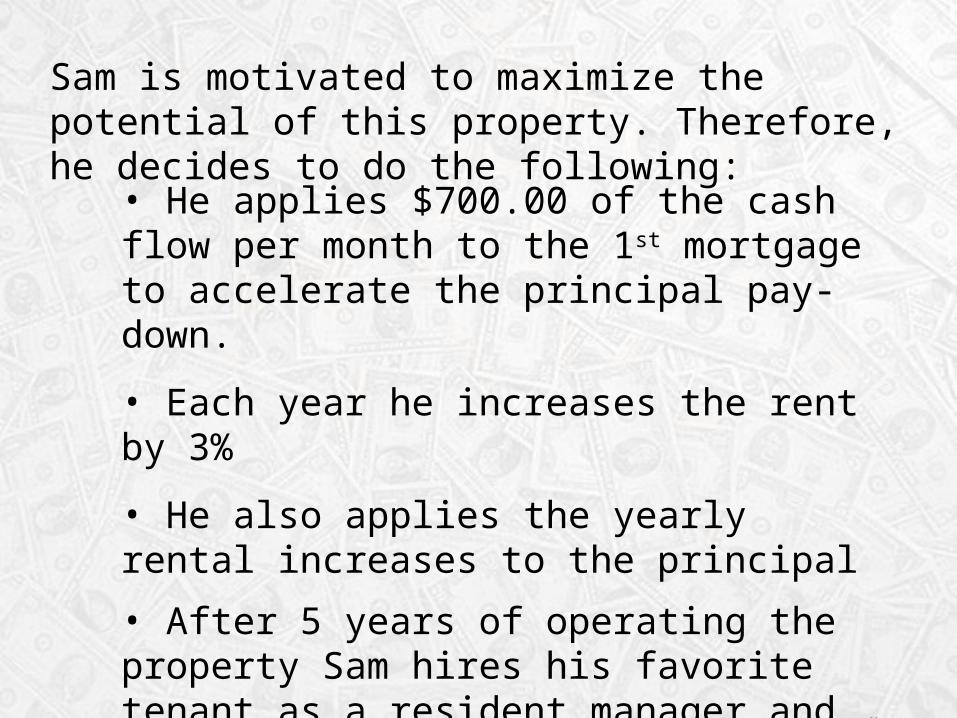

Sam is motivated to maximize the potential of this property. Therefore, he decides to do the following:

• He applies $700.00 of the cash flow per month to the 1st mortgage to accelerate the principal pay-down.

• Each year he increases the rent by 3%

• He also applies the yearly rental increases to the principal

• After 5 years of operating the property Sam hires his favorite tenant as a resident manager and pays him half rent (Prevents “Burn-out”)

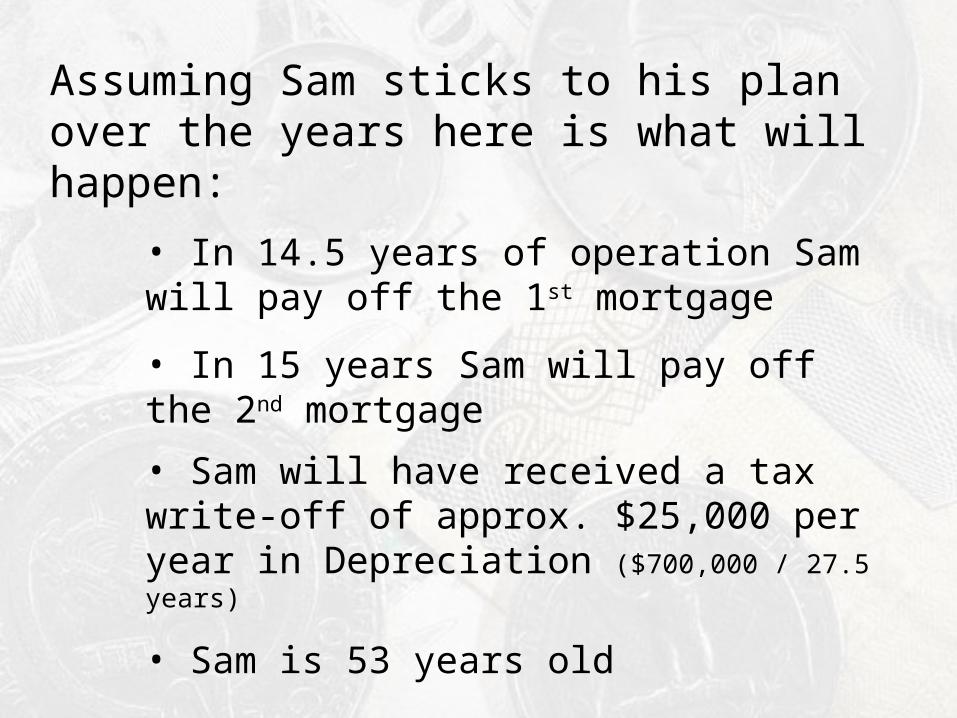

Assuming Sam sticks to his plan over the years here is what will happen:

• In 14.5 years of operation Sam will pay off the 1st mortgage

• In 15 years Sam will pay off the 2nd mortgage

• Sam will have received a tax write-off of approx. $25,000 per year in Depreciation ($700,000 / 27.5 years)

• Sam is 53 years old

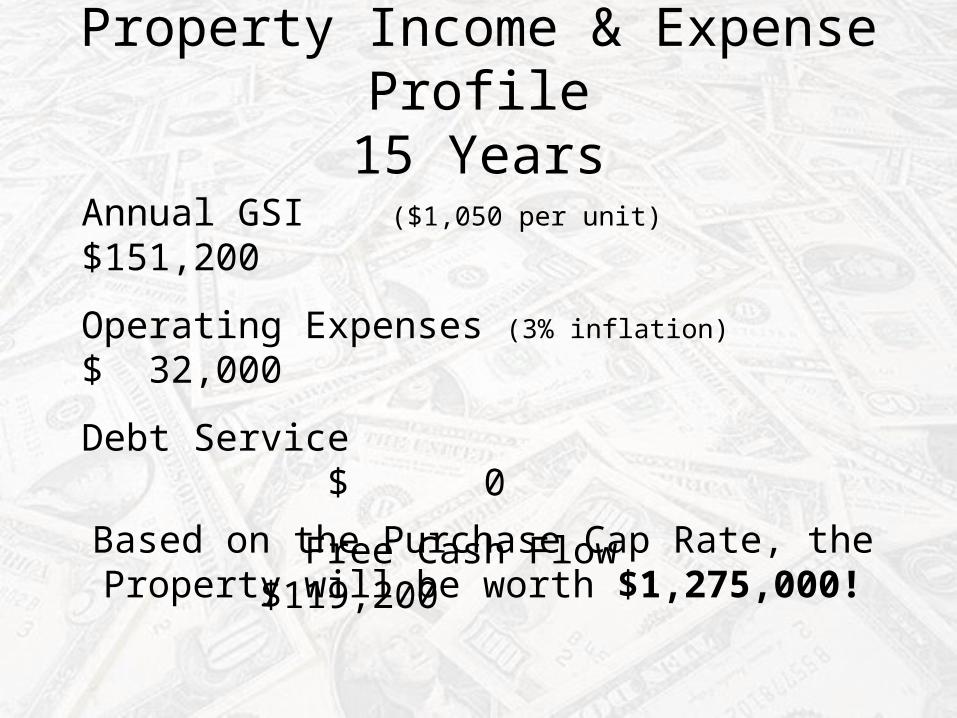

Property Income & Expense Profile15 Years

Annual GSI ($1,050 per unit) $151,200

Operating Expenses (3% inflation) $ 32,000

Debt Service $ 0

Free Cash Flow $119,200

Based on the Purchase Cap Rate, the Property will be worth $1,275,000!

The Bottom LineIn 15 years Sam will have turned $75,000 into $1,275,000 and the property will be

generating cash flow of approx. $120,000 per year.

Sam has harnessed the Power of LEVERAGE by letting his tenants pay off his

mortgages!

This represents a ROI of 1,600%!!! (over 20% yield per year)

The End