Performance of Financial Ratios and Hedging towards Firm ...

80

Performance of Financial Ratios and Hedging towards Firm Value of LQ45 companies in Indonesia By Irdian 014201400063 A Skripsi presented to the Faculty of Business President University in partial fulfillment of the requirements for Bachelor Degree in Management January 2018

Transcript of Performance of Financial Ratios and Hedging towards Firm ...

Performance of Financial Ratios and Hedging

towards Firm Value of LQ45 companies in

Indonesia

By

Irdian

014201400063

A Skripsi presented to the

Faculty of Business President University

in partial fulfillment of the requirements for

Bachelor Degree in Management

January 2018

i

PANEL EXAMINERS

APPROVAL SHEET

The Panel of Examiners declares that the skripsi entitled

“PERFORMANCE OF FINANCIAL RATIOS AND

HEDGING TOWARDS FIRM VALUE OF LQ45

COMPANIES IN INDONESIA” that was submitted by Irdian

majoring in Management from the Faculty of Business was

assessed and approved to have passed the Oral Examinations on

26th February 2018.

Panel of Examiners

Name and Signature of

Chair – Panel of Examiner

Name and Signature of

Examiner 2

Name and Signature of

Examiner 3

ii

SKRIPSI ADVISER

RECOMMENDATION LETTER

This skripsi entitled “PERFORMANCE OF FINANCIAL

RATIOS AND HEDGING TOWARDS FIRM VALUE OF

LQ45 COMPANIES IN INDONESIA” prepared and

submitted by Irdian in partial fulfilment of the requirements for

the degree of Bachelor in Management. The skripsi has been

reviewed and has been satisfied to accord with the requirement

for further examination. Therefore, I recommend this skripsi to

proceed for the Oral Defence

Cikarang, Indonesia, 24th January 2018

Acknowledged by, Recommended by,

Dr. Dra. Genoveva, M.M. Dr. Drs. Chandra Setiawan, M.M., Ph.D

Head of Management Study Program Advisor

iii

DECLARATION OF ORIGINALITY

I declare that this skripsi, entitled “PERFORMANCE

OF FINANCIAL RATIOS AND HEDGING

TOWARDS FIRM VALUE OF LQ45 COMPANIES

IN INDONESIA” is, to the best of my knowledge and

belief, an original piece of work that has not been

submitted, either in whole or in part, to another

university to obtain a degree.

Cikarang, January 26th, 2018

Irdian

iv

Abstract

This research aims to determine the factors that affect firm value proxy by

Tobin Q ratio. The determinants factors used are financial ratios such as

current ratio, debt to asset ratio and return on equity along with other

factors: tax rate, firm size and hedging dummy. Quantitative method is used

and 16 companies with specific criteria under LQ45 that listed in Indonesia

Stock Exchange are chosen as sample. The results revealed that current ratio

and return on equity have a positive significant affect toward firm value,

meanwhile debt to asset and firm size have a negative significant affect

toward firm value. Hedging and tax rate have no significant affect toward

the firm value. The most significant affect toward firm value from this

research is Return on Equity.

Keywords: firm value, financial ratios, tax rate, firm size, hedging

v

ACKNOWLEDGEMENT

In the name of God, the Most Gracious and the Most Merciful.

First of all, the researcher would like to deliver my highest gratitude to the

One and Only God, for His guidance and reinforcement in all time

especially during the completion of this study.

Researcher would like to convey immeasurable appreciation and deepest

thankfulness to these distinctive people who have given their full support in

making this study possible.

1. Researcher‟s best adviser, Dr. Drs. Chandra Setiawan, M.M., Ph.D., for

his indulgent guidance and constant support. The success of this research is

built within his constructive feedbacks during the research process.

2. Researcher‟s beloved parents, Syaiful Bunardi and Bong Siu Lan

together with the most outstanding brothers, Irwan Saputra, Hengki Setiadi,

Irvin for their support to encourage me until finished.

3. Tommy Saputra, Bayu Surya Dani, Ni Putu Kanilla Wati, Frengki

Wijaya, Aloysius Haryo Nugroho, Yasika Ayudaning Puspita, Laila

Sundari, Riska Ayu Saraswati, Jimmy Tan, Tubagus Achmad Rachmad

Saleh, Kaori Diana Putri, Marlinda and Sir Chandra’s fellow guidance and

all the Zombie squads, thanks for the moral support, sincere friendship and

unforgettable memories.

vi

To those who indirectly contribute in this research, your kindness matters a

lot for the researcher. Thank you very much.

Cikarang, January 26th, 2018

Irdian

vii

Table of Contents

PANEL EXAMINERS .............................................................................. i

SKRIPSI ADVISER ................................................................................. ii

RECOMMENDATION LETTER ............................................................ ii

DECLARATION OF ORIGINALITY .................................................... iii

Abstract .................................................................................................... iv

ACKNOWLEDGEMENT ........................................................................ v

List of Acronym ........................................................................................ x

Chapter I .................................................................................................... 1

INTRODUCTION .................................................................................... 1

1.1 Background of Study ....................................................................... 1

1.1.1 Need for study ............................................................................... 4

1.2 Problem Statement ........................................................................... 5

1.3 Research Questions .......................................................................... 6

1.4 Research Objectives ......................................................................... 6

1.5 Significant of Study ......................................................................... 7

1.6 Limitation ......................................................................................... 7

1.7 Thesis organization .......................................................................... 8

Chapter II .................................................................................................. 9

LITERATURE REVIEW ......................................................................... 9

2.1 Theoretical Review .......................................................................... 9

2.1.1 Firm Value ............................................................................. 9

2.1.2 Theory of Capital Asset Pricing Model ................................. 9

2.1.3 Corporate Risk Management ............................................... 10

2.1.5 Tobin Q Ratio as Measured ................................................. 11

2.2 Previous Research .......................................................................... 15

2.3 Research Gap ................................................................................. 18

viii

2.4 Theoretical Framework .................................................................. 19

2.5 Hypotheses ..................................................................................... 20

Chapter III ............................................................................................... 21

METHODOLOGY .................................................................................. 21

3.1 Research Method ........................................................................... 21

3.2 Research Framework ..................................................................... 22

3.3 Research Instrument ...................................................................... 23

3.4 Sampling Design ............................................................................ 23

3.4.1 Size of Population .................................................................... 23

3.4.2 Size of Sample ......................................................................... 24

3.5 Data Analysis ................................................................................. 26

3.5.1 Descriptive Statistic Analysis .............................................. 26

3.5.2 Panel Data Regression ......................................................... 27

3.5.3 Classical Assumption Test ................................................... 30

3.5.4 Multiple Regression Analysis .............................................. 34

3.6 Testing Hypotheses .................................................................... 36

3.6.1 Significant Level .................................................................. 36

3.6.2 T-test .................................................................................... 36

3.6.3 F-Test ................................................................................... 38

3.6.4 Coefficient of Determination ............................................... 40

Chapter IV ............................................................................................... 41

ANALYSIS OF DATA ........................................................................... 41

4.1 Company Profile ............................................................................ 41

4.2 Descriptive Analysis ...................................................................... 44

4.3 Data Analysis ................................................................................. 46

4.3.1 Classical Assumption Test ................................................... 46

4.3.2 Multiple Regression Analysis .............................................. 50

ix

4.4 T-Test, F-Test, and Coefficient of Determination ......................... 52

Chapter V ................................................................................................ 60

Conclusions and Recommendation ......................................................... 60

5.1 Conclusions .................................................................................... 60

5.2 Recommendations .......................................................................... 61

References ............................................................................................... 62

Journal .................................................................................................. 62

Book ..................................................................................................... 63

Thesis / Dissertation ............................................................................. 64

Website ................................................................................................ 65

Conference ........................................................................................... 65

Lists of Figures ........................................................................................ 66

x

List of Acronym

IFRS: International Financial Reporting Standards

CR: Current Ratio

TR: Tax Rate

DAR: Debt to Asset Ratio

ROE: Return on Equity

FS: Firm Size

Hg: Hedging

FV: Firm Value

LQ45: Top 45 Indonesia Companies

IDX: Indonesia Stock Exchange

BLUE: Best Linear Unbiased Estimator

1

CHAPTER I

INTRODUCTION

The scope of chapter I consist of Background of study, problem statement,

research questions, research objectives, limitations and thesis organization.

Background of study gives brief explanation about reason why the

researcher conducted this research. In the problem statement shows the

findings related to the hedging impact to the firm value. Research questions

contain the question about significant influence independent variables to

dependent variable. Research objectives contain the purpose of this

research. Significant of study explain about the research’s benefit.

Limitations explain several limitations that implemented in this research.

Thesis organization gives brief explanation for each chapter.

1.1 Background of Study

In financial world, growth of company has become consideration to the

people, stakeholder and shareholders. The growth and development of stock

companies overtime led an emergence the increased of stratum capital

owners which is they don’t directly involve to the company management

(Nabavand & Rezaei, 2015). Management is a representative of owner and

monitoring the activities of operations in the company. Company has

become larger overtime and makes people want to invest to the company to

get involved in the ownership. The one who invest in the company called

investor. Company performance is key indicator for the investor to do

investment. Investor judge the company based on their performance. Good

performance indicates that the company has generate more earnings by

utilize the asset that the company has. To determine whether the company

2

has a good or a bad performance, investor uses financial ratios to measure

the capability of the company.

Firm value is the easiest way for the investor to do valuation of the

company. Combination of the firm value and another financial ratio can

assess the financial areas. Based on Murtaqi (2017) firm value cover the

firm’s unique factors and affect the income. Financial ratios represent the

information that the investor need regarding to assess the company value.

Beside shareholder, creditor also has role to assess the firm’s asset because

creditor give loan to the firm. Debt is also a tool to maintain their capital

structure, besides using equity to gain their capital. Fail to pay the debt also

one of the reasons why many companies default. The larger debt of the

company the larger also risk to default. To minimize company become

default, hedging is a tool to reduce it.

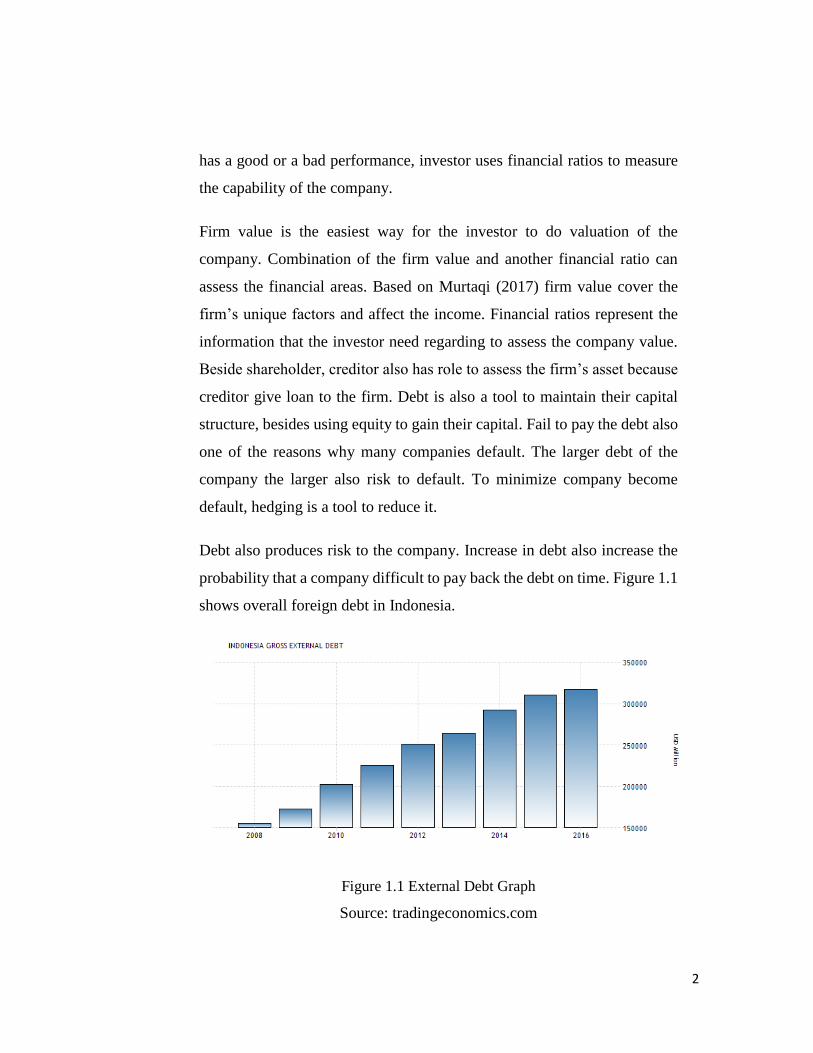

Debt also produces risk to the company. Increase in debt also increase the

probability that a company difficult to pay back the debt on time. Figure 1.1

shows overall foreign debt in Indonesia.

Figure 1.1 External Debt Graph

Source: tradingeconomics.com

3

To mitigate business that dealing with potential high risk, the enterprise risk

management is needed. To face uncertainty and reduce the risk while doing

businesses, using financial derivatives may be useful for the company. Most

likely, non-financial firms already using financial derivatives in their daily

business. Risk arise in many ways through global economy and financial

markets, risk become systematic with other units and interact with many

external parties (Sheng, 2010). On the other hand, George S. Oldfield

(1997) started wondering about which is better off transferring the risk to

the other parties or absorb the risk of the financial product and how they

manage the risk. Because of that many companies still used to transferring

their risk to the others rather than take the risk and managed it by

themselves.

Hedging has become a tool for the company to mitigate the risk but there

are still many companies are avoiding hedging itself. The factor that affects

a company hedging is a debt foreign currency. The companies think that

hedging is the same as insurance, when the accident doesn’t occur and they

still need to pay. Hedging is used to prevent any uncertainty in the financial

world and also prevent the financial crisis may occur in any time. There are

many components to prevent financial crisis may bring the companies to

bankruptcy. Another factor that company does hedge is fluctuated currency.

Because company cannot predict the fluctuated currency in financial world,

hedging is tool to anticipate the loss of income from trying to do business

using different currency. Hence, hedging might be a factor that impact to

the firm value. In figure 1.2 shows the fluctuation currency with the lowest

and the highest exchange rate of IDR 12,451 and IDR 14,739 to USD in

2015.

4

Figure 1.2 Fluctuation Currency History 2015

Source: usd.fx-exchange.com

Hedging is important to the firms when they do business using other

currency to fixing their currency rate in a length of time. Hedging is needed

for a business that related to export and import, also it needed for aviation

sector. Based on the IFRS accounting hedging rules, companies must

recognize the changes of fair value to the asset or liability or unrecognized

firm commitment or other components that could affect the profit or loss to

the firms.

1.1.1 Need for study

This researched has purpose to determine the relationship between firm

value and the control variables such as ROE, DAR, current ratio, firm size,

tax rate, and hedging dummy. This researched will focusing on the hedging;

therefore, the researcher aims to know “Performance of Financial Ratios

and Hedging towards Firm Value of LQ45 Companies in Indonesia”.

5

1.2 Problem Statement

According to F. Modigliani and Miller (1958) theory shows that risk

management using capital structure will not affect to the firm value;

therefore, hedging won’t affect the firm value. There are some research

theories and still argued that hedging has no impact to the firm value of the

company in Swedish firm (Nguyen, 2015). Meanwhile, Ayturk, et al.

(2016) found the result of the derivative uses doesn’t impact to the firm

value in Turkish market. The similarity on their research is they didn’t

diversify the industry that they chose. The opposite result can be found on

the research made by Dan, et al. (2005) stated hedging on gas with leverage,

profitability and reserves has significant impact to the firm value evidence

oil & gas Canadian companies but the result can be questionable also

because there is a research using oil & gas companies in U.S. Jin & Jorion

(2004) analyze that hedging doesn’t give impact to the market value of the

industry evidence U.S. oil & gas producers. The researches have different

result to other researches. Dan, et al. (2005) used oil & gas Canadian

companies as their sample different from the another researches. Jin and

Jorion (2004) found hedging doesn’t affect to the market value of the

industry although that they used same industry. Another research of Nguyen

(2015) and Ayturk, et al. (2016), they took sample based on derivative uses

of company based on their market. The differences of their results are

questionable whether the hedging does or doesn’t give impact to the firm

value. Investors might be still wondering if the hedging does or doesn’t give

them higher firm value. Firm that used hedging as their tool to mitigate the

risk can be speculated. Speculate the hedging might impact to their profit

loss. Those different results become matrix or references to me to do this

study.

6

1.3 Research Questions

The purpose of this study to know whether hedging does impact to the firm

value based on the Indonesia market or not. Because of the different results

to the previous researches, the study aims if hedging affect to the market

value positively.

1. Is there any significant influence on Current Ratio (CR) to Firm

Value?

2. Is there any significant influence on Tax Rate to Firm Value?

3. Is there any significant influence on Debt to Asset Ratio (DAR) to

Firm Value?

4. Is there any significant influence on Return on Equity (ROE) to Firm

Value?

5. Is there any significant influence on Firm Size to Firm Value?

6. Is there any significant influence on Hedging to Firm Value?

7. Is there a simultaneous significant influence on Current Ratio, Tax

Rate, Debt to Asset Ratio, Return on Equity, Firm Size and Hedging

to Firm Value?

1.4 Research Objectives

Based on the questions above, the purpose of this research are:

1. To determine the significant influence on Current Ratio (CR) to

Firm Value

2. To determine the significant influence on Tax Rate to Firm Value

3. To determine the significant influence on Debt to Asset Ratio

(DAR) to Firm Value

4. To determine the significant influence on Return on Equity (ROE)

to Firm Value

5. To determine the significant influence on Firm Size to Firm Value

7

6. To determine the significant influence on Hedging to Firm Value

7. To determine the simultaneous significant influence on Current

Ratio, Tax Rate, Debt to Asset Ratio, Return on Equity, Firm Size

and Hedging to Firm Value

1.5 Significant of Study

This study is given benefit to:

1. The investors

To give information for the investors about determinants to the

company firm value based on the key indicators to know whether

the company overvalue or undervalue and choose the best company

to invest in.

2. The researcher

This study can be as a foundation to create a new research using firm

value with the key indicators and enrich the knowledge deeper for

the researcher.

3. The students and university

To enrich the knowledge regarding firm value of company and apply

key indicators to measuring the performance of the company.

1.6 Limitation

1. This research is only focusing in the company that categorized as

LQ45 and listed in the Indonesia Stock Exchange (IDX).

2. In this research, researcher took seven year’s period of study started

from 2010 to 2016 that observed firms hedging activities. Therefore,

the researcher doesn’t know the requirement how long the hedging

firm’s activities affect firm value.

3. In this research, regression model can only be done using common

effect because of the variable hedging dummy value is 1 and 0.

8

1.7 Thesis organization

Thesis organization conducted as follows.

1. Chapter I – Introduction / Background

This chapter represent the research background of study, problem

statement, research questions, research objectives, significant of

study, limitations and organization paper. This chapter provide key

comprehension of this research.

2. Chapter II – Literature review

This chapter represent the theories of previous research. This

chapter consist of theoretical review, previous research, research

gap and hypothesis.

3. Chapter III – Research Methodology

This chapter represent the research data consist of research method,

research framework, research sample and data analysis method.

4. Chapter IV – Analysis and Interpretation

This chapter represent the finding analysis and interpretation of

result and consist of company profile, descriptive analysis, classical

assumption test, regression model analysis and interpretation of

results.

5. Chapter V – Conclusion and Recommendations

This chapter represent the conclusions and recommendations from

result of this paper.

9

CHAPTER II

LITERATURE REVIEW

2.1 Theoretical Review

2.1.1 Firm Value

Firm value is measure the asset of the company. It represents the future

business of the company. Fundamental of organization describe the value

of firm which is the manager who are being the representative to optimal

maximization of a firm (Ilaboya, Izevbekhai, & Ohiokha, 2016). The

prosperity of company and shareholder’s wealth can be seen when the firm

has high firm value. Firm value has become one of the indicator to investor

whether the firm has good prosperity in the future.

According to F. Modigliani and Miller (1963) stated that financing method

will not affect the firm value of a company since calculated by earning

power and risk of underlying assets. Therefore, financing method with debt

or equity will not affect the firm value because firm value increment based

on the earning power of the company.

According to Ilaboya, et al. (2016) stated that firm value has two

perspective measurement using profitability ratio such as return on asset

(ROA), return on equity (ROE) also profit margin and stock market

perspective using share price in the stock exchange market.

2.1.2 Theory of Capital Asset Pricing Model

Capital Asset Pricing model has become a famous model in financial

history. This model describes the relationship between expected return and

systematic risk that occurs in the financial world. Basic idea from this model

10

is the investor would like to choose efficient portfolio when the investor are

price takers and expect to have maximum return with the minimum variance

of risk (Nguyen, 2015). The formula to expected return as follows.

(Eq.1)

Where:

rf = risk free rate

βi = beta from industry

rm = expected market return

Researcher include CAPM in the literature review to give understanding

contradictive theories regarding risk management could affect the firm

value. From shareholder’s perspective risk management should contribute

to the firm value. However, it is no entirely obvious why risk management

can increase firm value (Nguyen, 2015).

2.1.3 Corporate Risk Management

Risk is interwoven with the corporate business’s strategy and impact

considerably to the competitive position (Aleš S. Berk, 2009). The risk is a

combination of the likelihood of an occurrence of a hazardous event or

exposures to danger and the damaged might be caused by action or event.

There are several risks according to the type and impact of organization and

its environment. There are written as follows.

1. Strategic risk is risk occurs and affect the strategy of the firm.

11

2. Operation risk is affect the firm capability of producing the goods.

3. Supply risk is affect the flow of resources to enable the operations.

4. Fiscal risk is arising through the taxation.

5. Reputation risk is loss in confidence of the firm.

6. Asset impairment risk is risk due to reduce in capability to increase

net profit.

7. Regulatory risk is risk caused the change of regulatory and affect the

business.

One of the tools to minimize the corporate risk by doing hedging. Hedging

is an investment tool to reduce the risk adverse movement in an asset.

Hedging often used for the company which is the business operations using

foreign currency as their main currency to purchase goods. Shareholder

maximization state that firm do hedging to reduce the cost that involved

with highly volatile cash flows (Jin & Jorion, 2004). There are three type

explanation about hedging with literature. Mayer et al. (1982) stated that

hedging reduces the financial distress and hedging is a way to get tax

incentives. When firm hedging, it will help to reduce the taxes. Leland and

Hayne (1997) stated debt from firm capacity will also increase, therefore

realizing the great leverage with greater taxes advantages. In addition,

hedging might be a signal for the investor to observed the managerial ability

of the firm.

2.1.5 Tobin Q Ratio as Measured

Tobin q ratio popularized by James Tobin of Yale University. The q ratio

defined as the market value of firm divided by replacement cost of firm total

asset (Ilaboya et al. 2016). Most of study used Tobin q ratio as measurement

for firm market value. Tobin q ratio defined market value by number of

share multiple by share price in stock exchange market and divided to book

12

value total asset of firm. Tobin q ratio is one of the tool to assess

performance of company. Tobin q ratio formula can be determined below.

(Eq.2)

Where:

Total market value of firm = share price x number of shares

If the Tobin q ratio is 1 means that the market value has same value with

the replacement cost of the firm. Tobin q ratio with less than 1 means that

the company has lower market value compared to the book value total asset

of firm and categorized as “Undervalued”. Tobin q ratio with greater than 1

means that the company has higher market value compared to the book

value of total asset of firm and categorized as “Overvalued”. Hence, Tobin

q ratio give an information to the investor whether the company has

undervalued or overvalued and the performance of future growth for the

firm.

2.1.5.1 Current Ratio

Current ratio is liquidity ratio to measure the ability of the firm pay its debt

whether its short-term or long-term debt (Murtaqi, 2017). Murtaqi, (2017)

stated that current ratio has positive significant influence to the firm value

using Tobin q ratio even thought, current ratio doesn’t give the highest

significant to the firm value.

If the current ratio value is less than 1 means that the firm has more debt to

pay indicates that obligation of firm to pay would be unable to paid their

13

debt on time. It tells the investor that the firm has liquidity problem and

indicated the firm has financial health issues.

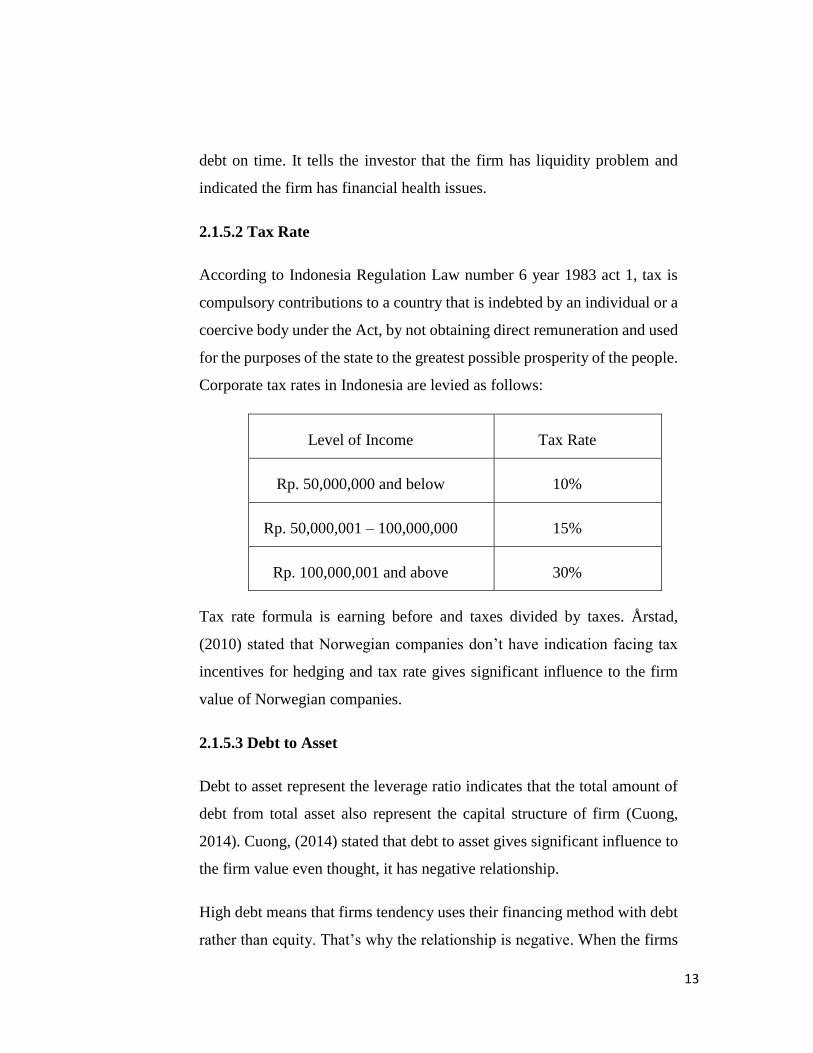

2.1.5.2 Tax Rate

According to Indonesia Regulation Law number 6 year 1983 act 1, tax is

compulsory contributions to a country that is indebted by an individual or a

coercive body under the Act, by not obtaining direct remuneration and used

for the purposes of the state to the greatest possible prosperity of the people.

Corporate tax rates in Indonesia are levied as follows:

Level of Income Tax Rate

Rp. 50,000,000 and below 10%

Rp. 50,000,001 – 100,000,000 15%

Rp. 100,000,001 and above 30%

Tax rate formula is earning before and taxes divided by taxes. Årstad,

(2010) stated that Norwegian companies don’t have indication facing tax

incentives for hedging and tax rate gives significant influence to the firm

value of Norwegian companies.

2.1.5.3 Debt to Asset

Debt to asset represent the leverage ratio indicates that the total amount of

debt from total asset also represent the capital structure of firm (Cuong,

2014). Cuong, (2014) stated that debt to asset gives significant influence to

the firm value even thought, it has negative relationship.

High debt means that firms tendency uses their financing method with debt

rather than equity. That’s why the relationship is negative. When the firms

14

have high debt means the firms have less equity. High debt also give high

probability of firm cannot pay their debt and become default.

2.1.5.4 Return on Equity

Return on equity represent the profitability ratio indicates that how much

the firm generate profit from their shares. Nabavand and Rezaei (2015)

stated that return on equity gives positive significant influence to the firm

value. Return on equity formula is net profit divided by total equity of firm.

High growth company expected to give higher return on equity means that

the company has good profitability. Therefore, investor can measure the

profitability of company using return on equity. Higher the ROE, higher

also the net profit that the company generate.

2.1.5.5 Firm Size

Firm size represent the size of the company indicates that bigger size of

company also has bigger value of asset. (Nguyen, 2015) stated that firm size

gives significant influence to the firm value even thought, it gives negative

relationship.

Based on the Grossman and Hart, (1983) theorem of principal and agency

problem stated that big firm has tendency to hired agent and pay the

incentives to them although the incentive might be expensive. It leads the

company become less efficiency. Big firm size also has tendency using debt

as their financing method. That’s why, it has negative relationship.

2.1.5.6 Hedging Dummy

Hedging dummy represent the company does or doesn’t hedging based on

the annual report and using dummy variable is appropriate for this

15

regression analysis due to it is hard to measure the size of hedging cost for

each company. Hedging doesn’t give significant influence to the firm value

based on the (Nguyen, 2015). It has contradictive result with Dan et al.

(2005) found that hedging has significant influence to the firm value. The

result might be bias because their research environment is different.

In this research, hedging dummy value is 1 if the company does hedge and

0 if the company doesn’t hedge. Hedging also related to the debt and tax.

When company does hedge means that the company has foreign debt. That

explains the tax shield of company. When company does hedge explain that

the company must pay higher interest rate and will impact to lower taxes.

2.2 Previous Research

Previous Research

No. Author, Title Variable Method Result

1. Nadya Marsha and

Isrochmani

Murtaqi (2017);

The Effect of

Financial Ratios

on Firm Value in

The Food and

Beverage Sector of

The IDX

DV: Firm

Value (Tobin

Q Ratio)

IV: ROA,

Current

Ratio, Acid

Test Ratio

Linear

Regress

ion

ROA, Current

Ratio has positive

significant

influence and

Acid Test Ratio

has negative

significant

influence and

simultaneous

significant

influence to the

Firm Value

(Tobin Q Ratio)

2. Yusuf Ayturk, Ali

Osman Gurbuz

and Serhat Yanik

(2016); Corporate

derivatives use and

firm value:

Evidence from

Turkey

DV: Firm

Value (Tobin

Q Ratio)

IV: Ln Total

Asset, ROA,

Dividend

Dummy,

Leverage,

Diversificati

Linear

Regress

ion

Ln Total Asset

has negative

significant

influence and

Dividend Dummy

have positive

significant

influence to the

Firm Value

16

on, Cap.

Ex/Sales,

Foreign

Sales,

Liquidity

and

Derivative

uses

(Tobin Q Ratio);

ROA, Leverage,

Diversification,

Cap. Ex/ Sales,

Foreign Sales,

Liquidity and

Derivatives uses

have no

significant

influence to the

Firm Value

(Tobin Q Ratio)

3. Eirik Haavaldsen

and Hans Fredrik

Ø. Årstad (2010);

Determinants and

Effects of

Corporate

Currency Hedging

DV: Firm

Value (Tobin

Q Ratio)

IV:

Derivatives,

Current

Ratio, Net

Debt, YoY

Revenue

Growth,

ROE% Mean

Tax Rate,

Hedging

Linear

Regress

ion

YoY Growth

Revenue, Tax

Rate, Hedging

have negative

significant

influence and

Current Ratio has

positive

significant

influence to the

Firm Value

(Tobin Q Ratio);

Derivatives, Net

Debt and ROE%

Mean has no

significant

influence to the

Firm Value

(Tobin Q Ratio)

4. Yanbo Jin and

Philippe Jorion

(2004); Firm

Value and

Hedging: Evidence

from U.S. Oil and

Gas Procedurs

DV: Firm

Value (Tobin

Q Ratio)

IV: Firm

Size,

Profitability,

Investment

Growth,

Leverage,

Dividend

Dummy,

Hedging

Linear

Regress

ion

Investment

Growth and

Dividend Dummy

have positive

significant

influence to the

Firm Value

(Tobin Q Ratio);

Firm Size,

Profitability,

Leverage,

Hedging Dummy

17

Dummy and

Production

Cost

and Production

Cost have no

significant

influence to the

Firm Value

(Tobin Q Ratio)

5. Behrooz Nabavand

and Javad Rezaei

(2015); Review

between Tobin's Q

with performance

Evaluation Scale

Based Accounting

and Marketing

Information in

Accepted

Companies in

Tehran Stock

Exchange

DV: Firm

Value (Tobin

Q Ratio)

IV: P/E

Ratio, EPS

Ratio, P/B

Ratio, ROE,

and ROA

Linear

Regress

ion

EPS Ratio, P/B

Ratio and ROE

have significant

influence to the

Firm Value

(Tobin Q Ratio);

P/E Ratio and

ROA have no

significant

influence to the

Firm Value

(Tobin Q Ratio)

6. Ngan Nguyen

(2015); Does

Hedging Increase

Firm Value?

DV: Firm

Value (Tobin

Q Ratio)

IV: Capex,

Diversified

Dummy,

Dividend

Dummy,

Hedging

Dummy,

Leverage,

Profitability,

Firm Size

Linear

Regress

ion

Dividend,

Profitability and

Firm Size have

positive

significant

influence and

Leverage has

negative

significant

influence to the

Firm Value

(Tobin Q Ratio);

Capex,

Diversified and

Hedging have no

significant

influence to the

Firm Value

(Tobin Q Ratio)

7. Chang Dan, Hong

Gu and Kuan Xu;

The Impact of

Hedging on Stock

Return and Firm

DV: Firm

Value (Tobin

Q Ratio)

IV: ROA,

Investment

Linear

Regress

ion

ROA and

Hedging Dgr

have positive

significant

influence to the

18

Value: New

Evidence from

Canadian Oil and

Gas Companies

Growth,

Access to

Financial

Market,

Leverage,

Hedging Dgr

(Delta Gas

Reserves)

and Hedging

Dgp (Delta

Gas

Production)

Firm Value and

Hedging Dgp and

Leverage have

negative

significant

influence to the

Firm Value

(Tobin Q Ratio);

Investment

Growth, Access

to Financial

Market have no

significant

influence to the

Firm Value

(Tobin Q Ratio

2.3 Research Gap

In the previous research, there are still many arguments that hedging doesn’t

affect firm value. However, there was a research showed that hedging

impact to the firm value (Dan et al. 2005). Those researches have many

different type of ways to see whether hedging affects the firm value and

those researches done in their country. Some countries may have different

economic condition. Hedging may impact to those countries that have

fluctuated economic or otherwise. The country may already become a

develop country and less volatility or fluctuated currency. That’s why,

hedging still be argued to many researchers that does hedging impact to firm

value. Uncertainty financial world has become a problem to the developing

country like Indonesia. When crisis impact to the develop country,

economic condition might also impact to the developing country. That’s

why, hedging has role to maintain their risk financial distress and future

cash flow so the investor will calmly invest their money to the company.

19

2.4 Theoretical Framework

Based on the theoretical review from previous research, the researcher had

developed model for theoretical framework of this research as in figure 2

According from this research, the researcher wants to know the relationship

between Current Ratio, Tax Rate, DAR, ROE, Firm Size and Hedging

towards the Firm Value of the company LQ45 and listed in Indonesia Stock

Exchange. In this research, researcher put current ratio as liquidity

measurement; tax rate taken from previous research, debt to asset ratio as

leverage measurement, ROE as profitability measurement, firm size taken

from previous research and hedging taken from previous research.

Figure 2 Research Theoretical Framework Firm Value

Source: Adjusted by Researcher 2017

FV

CR Hg FS ROE DAR TR

H1 H6 H5 H4 H3 H2

H7

20

2.5 Hypotheses

Based on the theoretical framework of this research, research conducted the

hypothesis as follows.

H1: There is a significance influence on Current Ratio towards Firm Value

in LQ45 Companies.

H2: There is a significance influence on Tax Rate towards Firm Value in

LQ45 Companies.

H3: There is a significance influence on Debt to Asset towards Firm Value

in LQ45 Companies.

H4: There is a significance influence on Return on Equity towards Firm

Value in LQ45 Companies.

H5: There is a significance influence on Firm Size towards Firm Value in

LQ45 Companies.

H6: There is a significance influence on Hedging towards Firm Value in

LQ45 Companies.

H7: There is significant simultaneous influence on Current Ratio, Tax Rate,

Debt to Asset, Return on Equity, Firm Size and Hedging towards Firm

Value in LQ45 Companies.

21

CHAPTER III

METHODOLOGY

3.1 Research Method

Quantitative Method

Quantitative research has purpose to explaining and determining the

predicted variable through numerical observation and presentation that

reflect from the independent variable. Quantitative method has two methods

to determine the data. In this research, researcher uses secondary data as

method to gathering the information that related to the research.

In this research, researcher collected the secondary data from audited annual

report of LQ45 companies from period of 2010 - 2016. The secondary data

are current ratio (X1), tax rate (X2), debt to asset ratio (X3), return on equity

(X4), firm size (X5), hedging dummy (X6) as the independent variable and

firm value (Y) as the dependent variable. Using quantitative method,

researcher can determine the result of this study using Eviews (Econometric

Views) 10 to generate the data analysis.

Researcher uses Eviews to produce the result of this study by processing the

raw data. By using Eviews 10, researcher can determine the mean,

minimum, maximum and standard deviation through descriptive statistic. In

order to fulfill the BLUE parameter, researcher uses Eviews to generate

normality test, heteroscedasticity, autocorrelation and multicollienarity.

After this research fulfill the BLUE parameter, researcher continues to

generate regression model using Eviews 10. Hypothesis can be determined

by using F-test and T-test also interpretation of each independent variable

that influenced the dependent variable.

22

3.2 Research Framework

Research framework is framework that has logical argument with the

previous research that has successful created (Suryana, 2010). In figure 3.1

shows the research framework of this research.

Figure 3.1 Research Framework of “Performance of Financial Ratios and

Hedging towards Firm Value of LQ45 Companies in Indonesia"

Figure 3.1 Research Framework

Source: Created by researcher for research purpose, based on Suryana (2010).

Observation

Problem Identification

Findings

Formulate Problem

Formulate Hypothesis

Collecting Data from Annual Report

Data Analysis

Processing Data

Interpretation of Results

Summary and Conclusion

23

3.3 Research Instrument

Research instrument is a tool that chosen by researcher in their research or

study to collect the data into a systematic (Arikunto, 2000). By using

random sampling of LQ45 companies, researcher took randomly 16

companies. These companies are Adaro, Indofood CBP, Indofood, Astra

International, Astra Agro Lestari, Indocement, Lippo Karawaci, Pakuwon

Jati, AKR Corporindo, Bumi Serpong Damai, Kalbe Farma, Adhi Karya,

Telkom, Wijaya Karya, Perusahaan Gas Negara, Gudang Garam.

Researcher collected the data through audited annual report from Indonesia

Stock Exchange period of 2010 until 2016.

To optimize the results of this study, researcher uses Eviews 10 as a tool to

produce the analysis and regression model of this study. Beside using

Eviews 10 as tool to produce the analysis, researcher uses Microsoft Excel

2016 to maintain the raw information from annual report. To make it easier

to calculated, researcher categorize the data annually using table.

3.4 Sampling Design

Sampling is process selecting part of object that taken by researcher to

become an object of observation (Nasution, 2003). If a sampling is correctly

observed, the statistical analysis can conclude the whole population.

3.4.1 Size of Population

Population is a whole of object to be observed (Nasution, 2003).

Population has very large of number to be observed which is not

really proper to be observed. Therefore, a proportion of population

is selected to be observed in this research. In this research,

population is focused on the companies under LQ45 and listed in

Indonesia Stock Exchange.

24

3.4.2 Size of Sample

Sample is a part of population that can be representative to estimate

the whole population (Nasution, 2003). There are two technic of

sampling design. First, probability sample or random sample.

Probability sample has purpose to minimalize the bias of the object

taken by researcher. Second, non-probability sample or non-random

sample. Non-probability sample has characteristic that deviations of

sample value towards population cannot be measure. In this

research, researcher uses non-probability sample using purposive

sample. Purposive sample is sample that taken by researcher with

purpose for this research.

Therefore, probability sample using purposive sampling is chosen

in this research. There are several criteria to choose specific sample

in this research which are:

1. Company that listed in Indonesia Stock Exchange.

2. Company must have positive asset, liabilities and equity.

3. Financial institution and non-financial institution are

excluded due to different nature of business.

4. Company that listed under LQ45 at least 3 years in row or

more.

5. Company that should not be suspended under LQ45 from

2010 – 2016.

Therefore, there are 16 companies chosen as sample in this research

using the several criteria that determined by researcher.

As of 2017, this research takes sixteen companies and categorizes

as LQ45 listed in Stock Exchange Indonesia

25

1. PT. Adaro

2. PT. Adhi Karya

3. PT. Astra International Indonesia

4. PT. Astra Agro Lestari Indonesia

5. PT. AKR Corporindo

6. PT. Bumi Serpong Damai

7. PT. Gudang Garam

8. PT. Indocement

9. PT. Indofood

10. PT. Indofood CBP

11. PT. Kalbe Farma

12. PT. Lippo Karawaci

13. PT. Pakuwon Jati

14. PT. Perusahaan Gas Negara

15. PT. Telkom Indonesia

16. PT. Wijaya Karya

Therefore, there are sixteen companies chosen as sample with

population of LQ45 listed in Indonesia Stock Exchange is 45

companies.

In this research, researcher implement panel data which is consist of

cross-section and time series data. The cross-section data is sixteen

companies listed in Indonesia Stock Exchange as LQ45 and the time

series is seven years of period from 2010 to 2016. This research

decides to choose seven years as availability. Therefore, the number

of observation using panel data by sixteen companies with seven

years of period which are 112 data.

26

3.5 Data Analysis

3.5.1 Descriptive Statistic Analysis

Descriptive Statistic Analysis is analysis of activity that conduct an

assessment towards value, score or sizes of variables and as indicator of

independent variable that being reviewed (Agung, 2000). The information

generate in descriptive statistics are mean, minimum, maximum and

standard deviation.

Mean is average value of data by add up all the number and divide by how

many the numbers are (Nicholas, 2006). Min and Max are the smallest and

highest value of the observation. Mean can be measure as follows (Schwert,

2010).

(Eq.3)

Where:

N = Number of observations

Standard deviation is average of deviation from the mean (Nicholas, 2006).

The smaller standard deviation indicates that the narrower range between

highest and lowest value closely to average value. The formulation can be

measure as follows (Schwert, 2010).

27

(Eq.4)

Where:

N = Number of sample

y = Mean

3.5.2 Panel Data Regression

Panel data is formed between the time series and cross-section data (Endri,

2011). In time series model usually, the model just use many time periods

with one object of observation and cross-section model is the model with

more than one as object but with one-time period. Regression using data

panel usually called pooled data (Endri, 2011). There are two advantages

using pooled data (Endri, 2011). First, pooled data is combination of time

series and cross-section data able to create many degree of freedom with

high value. Second, combination of time series and cross-section able to

solve the issues when there is omitted-variable.

According to Endri (2011) there are three method of estimation parameter

model, which is:

1. Common Effect: Ordinary Least Square

This method is regression model by combination of the time series

and cross-section using OLS method or called common effect. In

common effect, the regression ignored the differences of individual

and time period. This model assumes that there are no differences

between object that observed such as a company has a same

behavior in various period time.

28

2. Fixed Effect.

Different with the common effect that has assumption there are no

differences between company and the period. Fixed effect has

assumption that there are variables that cannot fill the regression

model and allowing intercept inconsistent. This model has

advantages for the research with more time series than cross-section.

3. Random Effect.

In fixed effect, differences of individual and period through

intercept. Random effect shows the differences through the errors.

This model has advantages for the research that using more cross-

section than time series.

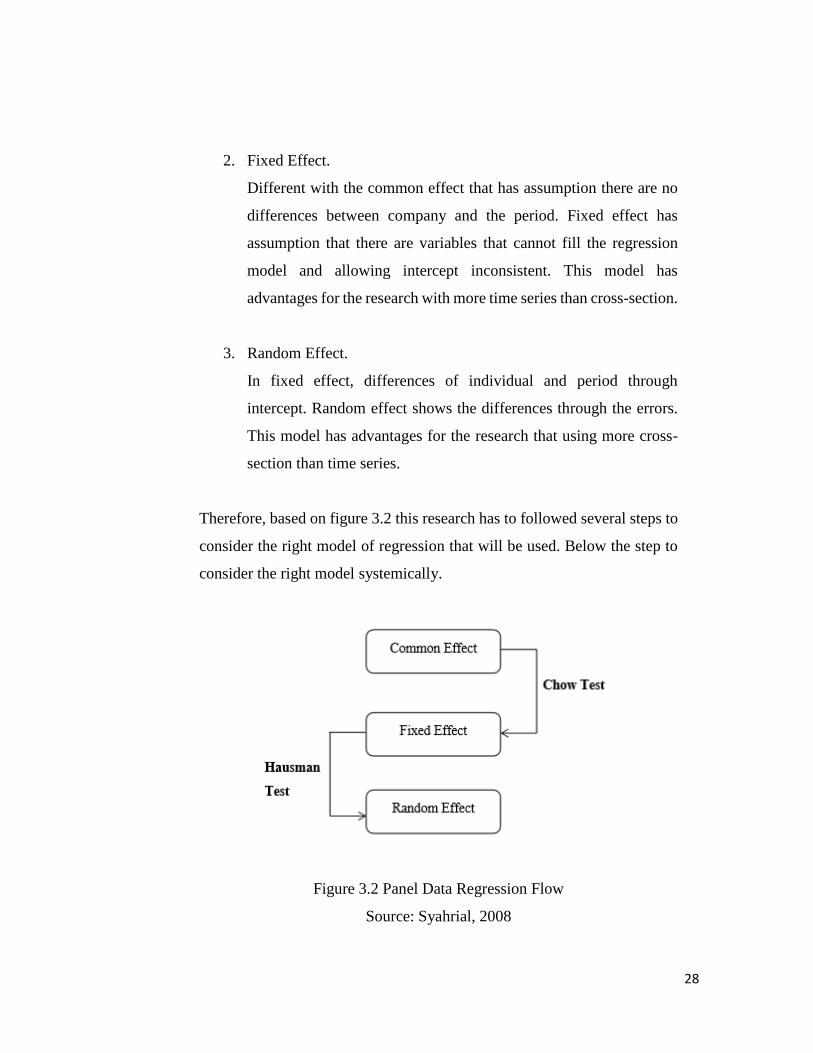

Therefore, based on figure 3.2 this research has to followed several steps to

consider the right model of regression that will be used. Below the step to

consider the right model systemically.

Figure 3.2 Panel Data Regression Flow

Source: Syahrial, 2008

29

1. Chow Test

Chow test is a test to determine the right model between fixed effect

and common effect. This model uses F-statistic to test by adding

dummy variable to know the differences intercept between fixed

effect and common effect (Endri, 2011). The formulate stated

below.

(Eq.5)

Where:

RSS = Residual sum of square

The null hypothesis is dummy variable is not significant towards

dependent variable so the research will choose common effect. The

alternate hypothesis is dummy variable is significant towards

dependent variable so the research will choose fixed effect. The

results of chow test can be determined as follows.

1. Ho is accepted and Ha is rejected if Probability value > 0.05,

which means common effect model is accepted.

2. Ho is rejected and Ha is accepted if Probability value < 0.05,

which means fixed effect model is accepted.

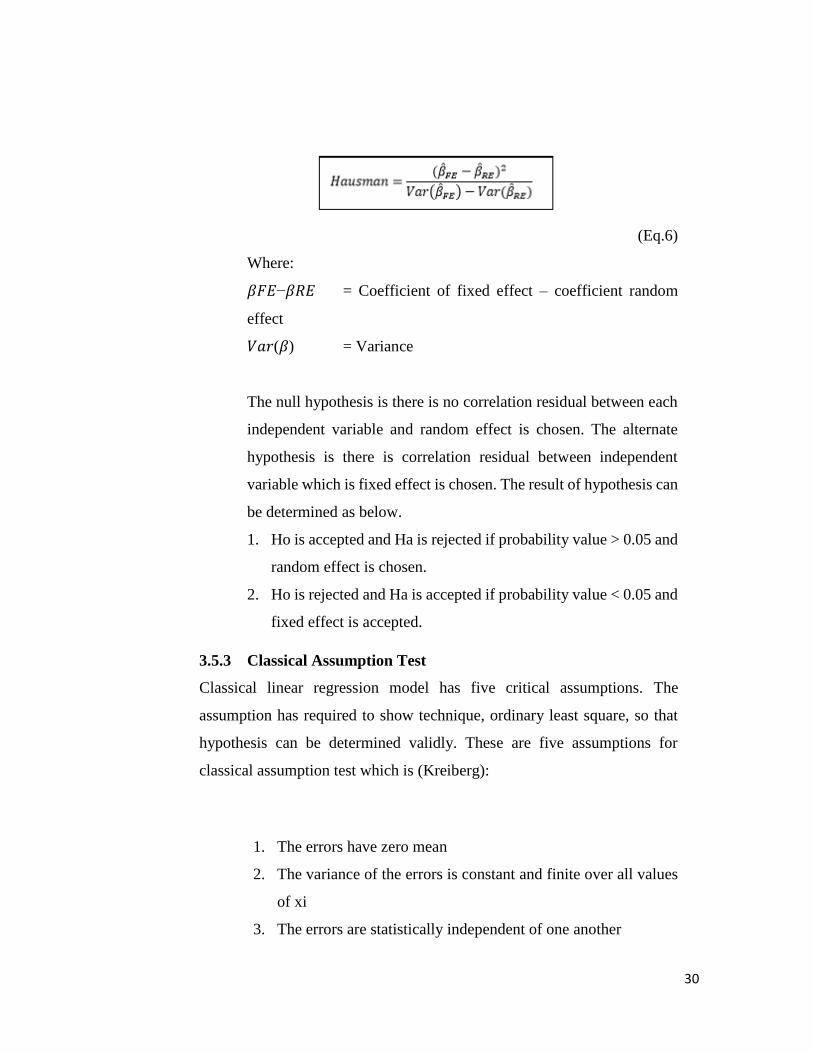

2. Hausman test

Hausman test is a test to determine the right model between random

effect and fixed effect. This test formed by hausman has asymptotic

χ2 distribution. The formula stated as follows.

30

(Eq.6)

Where:

𝛽𝐹𝐸−𝛽𝑅𝐸 = Coefficient of fixed effect – coefficient random

effect

𝑉𝑎𝑟(𝛽) = Variance

The null hypothesis is there is no correlation residual between each

independent variable and random effect is chosen. The alternate

hypothesis is there is correlation residual between independent

variable which is fixed effect is chosen. The result of hypothesis can

be determined as below.

1. Ho is accepted and Ha is rejected if probability value > 0.05 and

random effect is chosen.

2. Ho is rejected and Ha is accepted if probability value < 0.05 and

fixed effect is accepted.

3.5.3 Classical Assumption Test

Classical linear regression model has five critical assumptions. The

assumption has required to show technique, ordinary least square, so that

hypothesis can be determined validly. These are five assumptions for

classical assumption test which is (Kreiberg):

1. The errors have zero mean

2. The variance of the errors is constant and finite over all values

of xi

3. The errors are statistically independent of one another

31

4. There is no relationship between the error and the

corresponding x

5. εi is normally distributed

Therefore, the research can be called fulfilled the classical assumption test

if five assumptions above are implemented. To test whether the classical

assumption test fulfilled or not. Researcher uses these steps as follows.

1. Normality Test

Normality test is test to measure whether the data for the research is

normally distributed or not in parametric statistics (Widhiarso).

Normality test can be done through statistical analysis or histogram.

The statistical analysis will show the estimated of distribution for

the regression. Histogram can describe the normality of distribution

data. If the curve of histogram focused on the middle and going

down for the both side or called the bell-shape, histogram can

conclude that the regression model is normally distributed.

However, just looking at the histogram with the bell-shaped. It

doesn’t rule out the possibility of the data is normally distributed.

The best way to check it whether it has normally distributed using

statistical analysis. Jacque-Bera is a method to test whether it is

normal distributed (Dian Christiani Kabasaranga, 2013).

(Eq.7)

Where:

S = Skewness

N = Number of Observation

K = Kurtosis

32

Dian (2013) stated that Jacque-Bera has distribution of chi-square

with X2. Compared to table with two degree of freedom with

significant value of 0.05 (α=5%).

1) Jacque-Bera value > X2, the residual is not normally

distributed.

2) Jacque-Bera value < X2, the residual is normally distributed.

Winarno (2011) stated that distribution of data can be tested by

Jacque-Bera probability. If the probability of Jacque-Bera is greater

than significant value of 0.05 then the data is normally distributed

and vice versa.

1) Jacque-Bera Probability > 0.05, the data is normally

distributed.

2) Jacque-Bera Probability < 0.05, the data is not normally

distributed.

2. Heteroscedasticity

Heteroscedasticity is distribution of same probability in the same

observation of x, and variance each residual is same (BASUKI,

2017). Heteroscedasticity can be detected by the scatterplot. If the

scatterplot created a same form or spread, then it can be concluded

there is a heteroscedasticity in the research. The regression model

called a good regression if there is no heteroscedasticity which

means that there is a singular metric of dependent variable that has

related to the two or more singulars metric of independent variable.

For testing the heteroscedasticity using white test based on the

BASUKI (2017), if the probability of Chi-Square value is greater

than 0.05 then the regression has fulfilled homoscedasticity or there

is no heteroscedasticity in the research vice versa.

33

1) If Prob. Chi-Square > 0.05, there is no heteroscedasticity.

2) If Prob. Chi-Square < 0.05, there is heteroscedasticity.

3. Autocorrelation

Autocorrelation is the correlation between each variances are same

or the variables are related to each other (BASUKI, 2017). If the

autocorrelation occurs the estimation of regression model will bias

or inefficiency. Classical assumption can be fulfilled if there is no

autocorrelation occurs in the research. To determine there is a

correlation in this research, researcher uses Durbin-Watson test. If

the range value of Durbin-Watson 1.5 between 2.5 based on the rule

of thumb still, consider as no autocorrelation. Durbin-Watson

formula as follows.

(Eq.8)

Therefore, the null hypothesis is there is no autocorrelation if the

Durbin-Watson value between range of 2. The alternate hypothesis

is there is a correlation if the Durbin-Watson value less or greater

than 2. The hypothesis can be determined as follows (Stephanie,

2017).

1. There is no autocorrelation if Durbin-Watson value equal to

2. Positive correlation if Durbin-Watson value less than 2.

3. Negative correlation if Durbin-Watson value greater than 2.

34

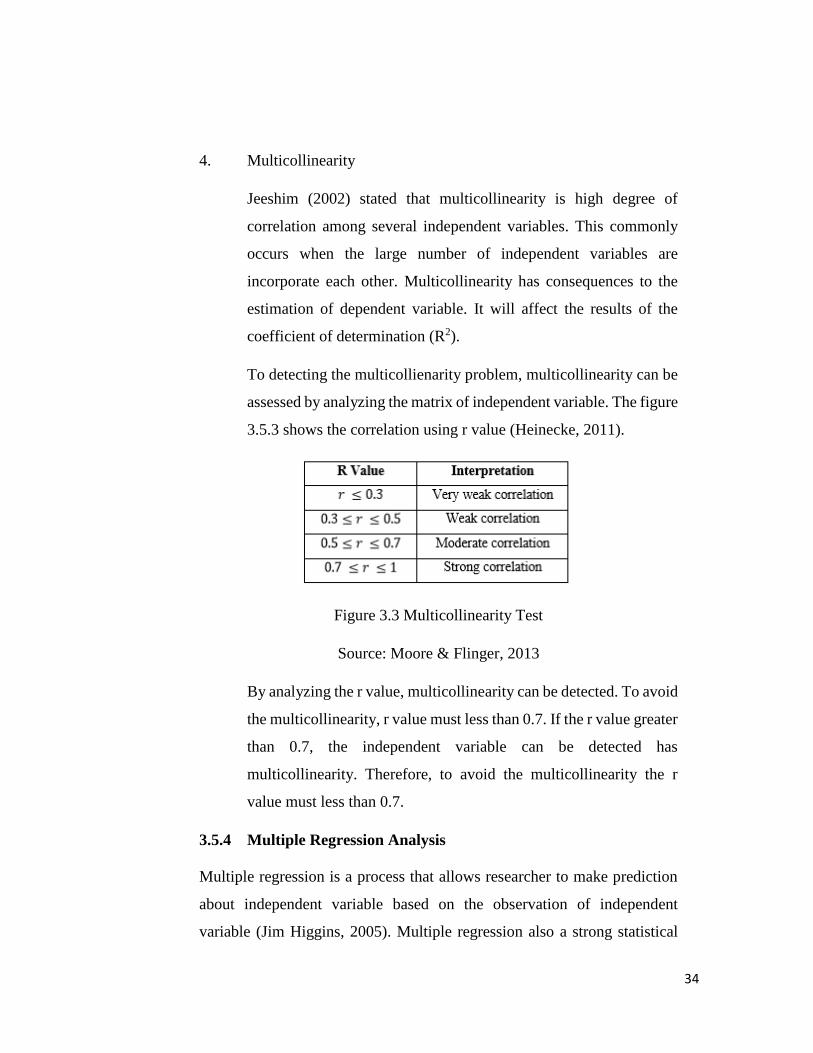

4. Multicollinearity

Jeeshim (2002) stated that multicollinearity is high degree of

correlation among several independent variables. This commonly

occurs when the large number of independent variables are

incorporate each other. Multicollinearity has consequences to the

estimation of dependent variable. It will affect the results of the

coefficient of determination (R2).

To detecting the multicollienarity problem, multicollinearity can be

assessed by analyzing the matrix of independent variable. The figure

3.5.3 shows the correlation using r value (Heinecke, 2011).

Figure 3.3 Multicollinearity Test

Source: Moore & Flinger, 2013

By analyzing the r value, multicollinearity can be detected. To avoid

the multicollinearity, r value must less than 0.7. If the r value greater

than 0.7, the independent variable can be detected has

multicollinearity. Therefore, to avoid the multicollinearity the r

value must less than 0.7.

3.5.4 Multiple Regression Analysis

Multiple regression is a process that allows researcher to make prediction

about independent variable based on the observation of independent

variable (Jim Higgins, 2005). Multiple regression also a strong statistical

35

and extremely powerful when the researcher develops “model” of the wide

various observation. Multiple regression provides the analysis of

relationship between two variables.

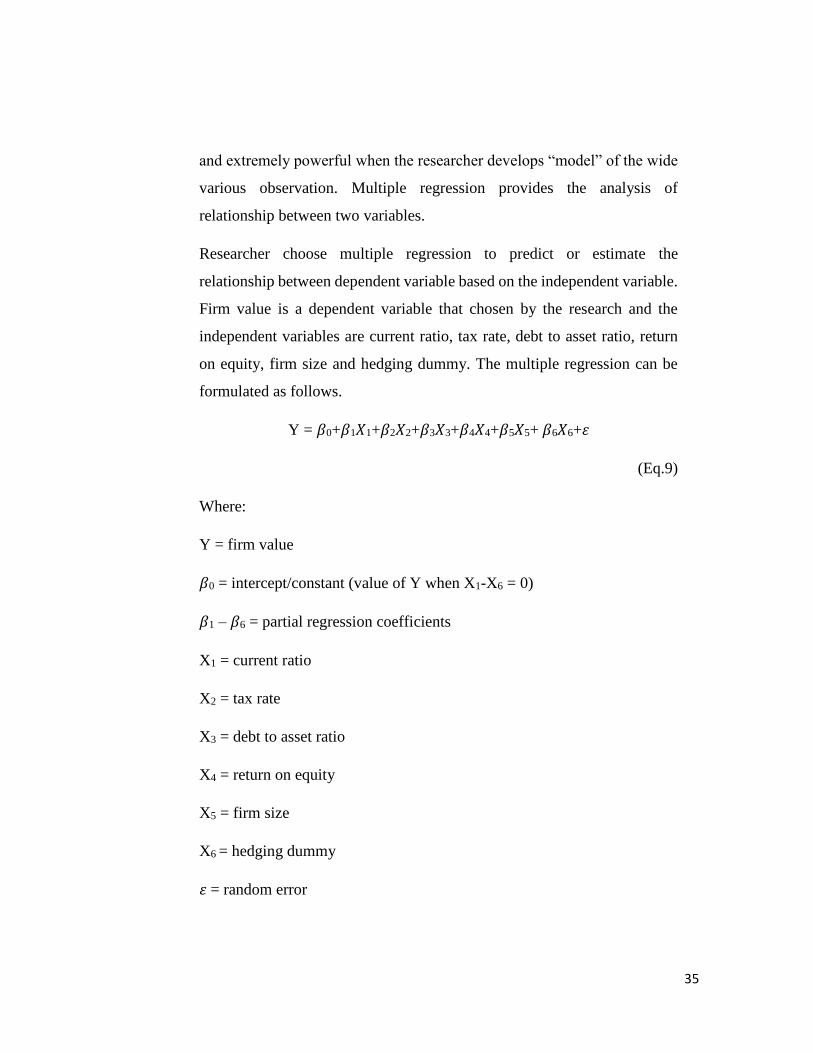

Researcher choose multiple regression to predict or estimate the

relationship between dependent variable based on the independent variable.

Firm value is a dependent variable that chosen by the research and the

independent variables are current ratio, tax rate, debt to asset ratio, return

on equity, firm size and hedging dummy. The multiple regression can be

formulated as follows.

Y = 𝛽0+𝛽1𝑋1+𝛽2𝑋2+𝛽3𝑋3+𝛽4𝑋4+𝛽5𝑋5+ 𝛽6𝑋6+𝜀

(Eq.9)

Where:

Y = firm value

𝛽0 = intercept/constant (value of Y when X1-X6 = 0)

𝛽1 – 𝛽6 = partial regression coefficients

X1 = current ratio

X2 = tax rate

X3 = debt to asset ratio

X4 = return on equity

X5 = firm size

X6 = hedging dummy

𝜀 = random error

36

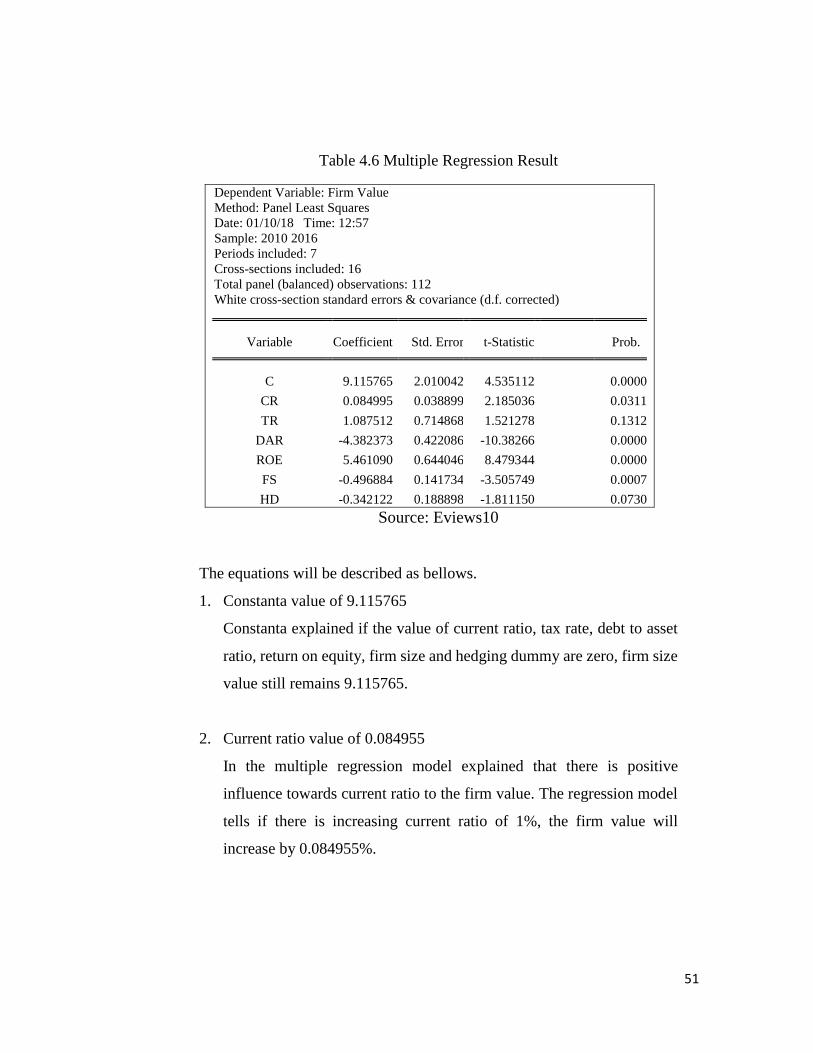

The partial regression coefficient is really important to predict the

contribution of independent variable to dependent variable. If the partial

regression coefficient has positive value means that the behavior of

dependent variable will follow the independent. An increment of

independent variable value also raising the value of dependent variable, vice

versa. If the partial regression coefficient has negative value means that

dependent and independent has opposite behavior. An increment of

independent variable will impact to the decreasing value of dependent

variable.

3.6 Testing Hypotheses

Testing hypothesis is test that conducted to know whether there is an

influence between independent variable to dependent variable in the

research. There are two type of hypothesis testing. First, null hypothesis (βn

= 0) that represent as H0. Second, alternative hypothesis (βn ≠ 0) that

represent as Ha. Null hypothesis means there is no significant influence

between independent variable to dependent variable meanwhile alternative

hypothesis mean there is significant influence between independent variable

to dependent variable.

3.6.1 Significant Level

This research apply test at significant value of 0.05 or α=5%. If probability

value or P-value greater than significant value, null hypothesis will be

applied which is mean that there is no significant influence.

3.6.2 T-test

T-test in multiple regression is to test whether the parameter estimation of

multiple regression is already right parameter or not. Right parameter means

that the parameter able to explain the dependent variable through

independent variable (Iqbal, 2015).

37

(Eq.10)

Where:

𝛽𝑖 = parameters of the model; the intercept and slope coefficients

𝛽 ̂ = estimator of 𝛽𝑖

se = standard error

The result of hypothesis can conclude to accept or reject hypothesis using

probability value of t-statistic each independent variable with significant

value of 0.05. The hypothesis of t-test conclude as follows.

1) Probability of t-statistics > 0.05 means that there is no significant

influence of independent variable to dependent variable and H0 is

accepted and Ha is rejected.

2) Probability of t-statistics < 0.05 means that there is a significant

influence of independent variable to dependent variable and H0 is

rejected and Ha is accepted.

To help the researcher determine the hypothesis for each independent

variable whether there is significant influence or not. Below is the t-test

hypothesis of this research.

1. 𝐻01: 𝛽1 = 0 or if probability t-statistics > α then there is no significant

partial influence of current ratio towards firm value in LQ45.

𝐻a1: 𝛽1 ≠ 0 or if probability t-statistics < α then there is significant

partial influence of current ratio towards firm value in LQ45.

38

2. 𝐻02: 𝛽2 = 0 or if probability t-statistics > α then there is no significant

partial influence of tax rate towards firm value in LQ45.

𝐻a2: 𝛽2 ≠ 0 or if probability t-statistics > α then there is significant

partial influence of tax rate towards firm value in LQ45.

3. 𝐻03: 𝛽3 = 0 or if probability t-statistics > α then there is no significant

partial influence of debt to asset towards price to firm value in LQ45.

𝐻a3: 𝛽3 ≠ 0 or if probability t-statistics > α then there is significant

partial influence of debt to asset towards price to firm value in LQ45.

4. 𝐻04: 𝛽4 = 0 or if probability t-statistics > α then there is no significant

partial influence of return on equity towards firm value in LQ45.

𝐻a4: 𝛽4 ≠ 0 or if probability t-statistics > α then there is significant

partial influence of return on equity towards firm value in LQ45.

5. 𝐻05: 𝛽5 = 0 or if probability t-statistics > α then there is no significant

partial influence of firm size towards firm value in LQ45.

𝐻a5: 𝛽5 ≠ 0 or if probability t-statistics > α then there is significant

partial influence of firm size towards firm value in LQ45.

6. 𝐻06: 𝛽6 = 0 or if probability t-statistics > α then there is no significant

partial influence of hedging dummy towards firm value in LQ45.

𝐻a6: 𝛽6 ≠ 0 or if probability t-statistics > α then there is significant

partial influence of hedging dummy towards firm value in LQ45.

3.6.3 F-Test

F-test or called test simultaneous model is step to identify the regression

model is feasible to use. Feasible means that the model estimation can

39

explain the dependent variable through independent variable (Iqbal, 2015).

The formula for t-test as follows.

(Eq.11)

Where:

𝑅2 = coefficient of determination

N = samples

k = number of independent variables

The result of hypothesis can conclude to accept or reject hypothesis using

probability value of f-statistic each independent variable with significant

value of 0.05. The hypothesis of t-test conclude as follows.

a) Probability of f-statistics > 0.05 means that there is no significant

influence of independent variable to dependent variable and H0 is

accepted and Ha is rejected.

b) Probability of f-statistics < 0.05 means that there is a significant

influence of independent variable to dependent variable and H0 is

rejected and Ha is accepted.

In this research, f-test will help the researcher to determine the simultaneous

influence of independent variable to dependent variable. The hypothesis for

f-test as follows.

1. H07: β1 = β2 = β3 = β4 = β5 = β6 0 or if probability f-statistics > α then

there is no significant simultaneous influence of current ratio, tax

rate, debt to asset, return on equity, firm size and hedging dummy

towards price to firm value in LQ45.

40

Ha7: at least there is one βi ≠ 0 or if probability f-statistics < α then

there is significant simultaneous influence of current ratio, tax rate,

debt to asset, return on equity, firm size and hedging dummy

towards price to firm value in LQ45.

3.6.4 Coefficient of Determination

Coefficient of Determination explained about variance of independent

variable to dependent variable (Iqbal, 2015). Coefficient determination

value can be measure as R-Square (R2) or Adjusted R-Square. R-Square

normally used when the independent variable just one and Adjuster R-

Square used when the independent more than 1. Normally all the researcher

use R-Square rather than Adjusted R-Square.

Value of R-Square can range from 0 to 1

a) Independent variables have weak capability to explain dependent

variable when R-Square is close to 0.

b) Independent variables have strong capability to explain dependent

variable when R-Square is close to 1.

Value of R-Square also can explain the multicollinearity. When value of R-

Square close to 0, the research might also expose to multicollinearity

Therefore, the research must have strong capability to explain the dependent

variable through independent variable.

41

CHAPTER IV

ANALYSIS OF DATA

4.1 Company Profile

1. Adaro

Adaro was established in 1982. PT. Adaro Energy Tbk. is an energy group

from Indonesia with coal mining through subsidiaries as main business.

Headquarters of Adaro Energy in Tabalong, South Kalimantan and the CEO

is Garibaldi Thohir.

2. Adhi Karya

PT. Adhi Karya (Persero) Tbk. is a company that has construction as main

business and located in Jakarta, Indonesia. PT. Adhi Karya Tbk has founded

on 1960 and the President director is Kiswodarmawan and the main

commissioner is Fadjroel Rachman.

3. Astra International

Astra International is a multinational company that has automotive as main

business. The founders of Astra International are Tjia Kien Tie, William

Soerjadjaja and Liem Peng Hong. Astra International was founded on 1957

and located in Jakarta.

4. Astra Agro Lestari Indonesia

Astra Agro Lestari is a company that located in Jakarta and has main

business on plantation. Astra Agro Lestari was founded on 1997 and

subsidiaries from Astra International. Crude Palm Oil and Kernels is a main

product of Astra Agro Lestari.

42

5. AKR Corporindo

PT. AKR Corporindo is a multinational company that located in Jakarta and

has main business on fuels and natural gas. AKR Corporindo was founded

on 28 November 1977 and the founder is Soegiarto Adikoesoemo

6. Bumi Serpong Damai

PT. Bumi Serpong Damai is an Indonesia real-estate developer company

located in Tangerang. Its business segments are land, industrial building,

house, shop house, hotel, industrial building, office space and educational

centre. The company was founded on 1984 and the founder is Muktar

Widjaja.

7. Gudang Garam

PT. Gudang Garam Tbk. is an Indonesia company that has main business

on cigarettes located in Kediri, East Java. The founder is Surya

Wonowidjojo and founded on 1958.

8. Indocement

PT. Indocement Tunggal Prakarsa Tbk. is an Indonesia company that has

main business on cement. Indocement was founded on 1985 and the

president director is Christian Kartawijaya.

9. Indofood Sukses Makmur

PT. Indofood Sukses Makmur Tbk. is producer of food and beverages and

located in Jakarta. Indofood was founded on 14 August 1990 and the

founder is Sudono Salim.

43

10. Indofood CBP

PT. Indofood CBP Sukses Makmur Tbk. is a subsidiaries company from

Indofood and the company involved in the food industry. The headquarters

located in Jakarta.

11. Kalbe Farma

PT. Kable Farma Tbk. is an international company that produces pharmacy,

supplement, nutrition and health services that located in Jakarta. Kalbe

Farma was founded on 10 September 1966 and the founder are Khouw Lip

Tjoen,Khouw Lip Hiang, Khouw Lip Swan, Boenjamin Setiawan, Maria

Karmila, F. Bing Aryanto.

12.Lippo Karawaci

PT. Lippo Karawaci is a real-estate and developer company in Indonesia

and subsidiaries from Lippo Group. Lippo Karawaci was founded on

October 1990 and the CEO is Gouw Vi Ven.

13. Pakuwon Jati

PT. Pakuwon Jati Tbk. is a real-estate company and located in Surabaya.

PT. Pakuwon Jati Tbk. was founded on 1982. The founder is Alexander

Tedja.

14. Perusahaan Gas Negara

PT. Perusahaan Gas Negara (Persero) Tbk. is state-owned enterprises from

Indonesia and has main business on transmission and distributor of natural

gas. The company was founded on 1859 as I.J.N Eindhoven & Co. On 13

May 1965 change into PGN. The president director is Jobi Triananda

Hasjim.

44

15. Telkom Indonesia

PT. Telekomunikasi Indonesia Tbk. is a state-owned enterprises company

that provide information and communication. Telkom was founded on 23

October 1856 and the founder is Cacuk Sudarijanto.

16. Wijaya Karya

PT. Wijaya Karya Tbk. is an Indonesia company that operates in

construction. The company was founded on 11 Maret 1960. The main

commissioner is Dr. Ir. M. Basuki Hadimuljono, M.Sc and president

director is Bintang Perbowo, SE, MM.

4.2 Descriptive Analysis

Descriptive analysis describes the information for each variable that are

being observed. Using EViews 10, descriptive analysis mostly explained

about mean, median, maximum, minimum, standard deviation, skewness,

kurtosis, Jacque-Bera, probability and sum of observations. In this study,

there are 112 observations using cross-section data with seven years (2010-

2016) and sixteen companies. Summary of descriptive statistic will be

shown on table 4.1 interpret using EViews 10.

Table 4.1 Descriptive Statistic Result

FV_Y CR_X1 TR_X2 DAR_X3 ROE_X4 FS_X5 HD_X6

Mean 1.795 2.326 0.248 0.451 0.187 13.443 0.437

Maximum 5.126 6.985 0.530 0.850 0.475 14.418 1.000

Minimum 0.152 0.450 0.043 0.133 0.045 12.693 0.000

STD 1.224 1.528 0.100 0.176 0.087 0.412 0.498

∑Observ. 112 112 112 112 112 112 112

Source: Eviews10

According to the descriptive statistic result, we can conclude the

explanations as below:

45

1. Firm Value (FV) explained the dependent variable. It shows mean value

of 1.795 along with standard deviation of 1.224 indicates that the data

mostly spread around 1.795 ± 1.224. Standard deviation value has small

gap to the mean due to volatility between firm value of each company.

The maximum value of 5.126 happens to Kalbe Farma in 2012 and

minimum value of 0.152 happens to Adhi Karya in 2011.

2. Current Ratio (CR) explained the independent variable. It shows mean

value of 2.326 along with standard deviation of 1.528 indicates that the

data mostly spread around 2.326 ± 1.528. Standard deviation value still

under to the mean because of value of each company has different

fluctuatuion. The maximum value of 6.985 occurs to Indocement in

2011 and the minimum value of 0.450 occurs to Astra Agro Lestari in

2013.

3. Tax Rate (TR) explained the independent variable. It shows mean value

of 0.248 along with the standard deviation of 0.100 indicates that the

data mostly spread around 0.248 ± 0.100. Smaller standard deviation

indicates that the data has narrow between the lowest value to the

highest value. The maximum value of 0.530 occurs to Adaro in 2010

and the minimum value of 0.043 occurs to Astra Agro Lestari in 2016.

4. Debt to Asset Ratio (DAR) explained the independent variable. It shows

mean value of 0.451 along with the standard deviation of 0.176

explained that the data mostly spread around 0.451 ± 0.176. Standard

deviation has smaller value and narrower spread between the lowest

value to the highest value. The maximum value of 0.850 occurs to Adhi

Karya in 2012 and the minimum value of 0.133 occurs to Indocement

in 2016.

5. Return on Equity (ROE) explained the independent variable. It shows

mean value of 0.187 along with standard deviation of 0.087 explained

that the data mostly spread around 0.187 ± 0.087. Standard deviation

46

still smaller to the mean due to each company has small volatility. The

maximum value of 0.475 occurs to Telkom in 2016 and the minimum

value of 0.045 occurs to Adaro in 2015.

6. Firm Size (FS) explained the independent variable. It shows mean value

of 13.443 along with the standard deviation of 0.412 explained that the

data mostly spread around the 13.433 ± 0.412. Standard deviation has

small value indicates that the steady value of firm size for each

company. The maximum value of 14.418 occurs to Astra in 2016 and

the minimum value of 12.693 occurs to Pakuwon Jati in 2010.

7. Hedging Dummy explained the independent variable. It shows the mean

value of 0.437 along with the standard deviation of 0.498 indicates that

the data mostly spread around 0.437 ± 0.498. Standard deviation has

greater value to the mean value due to the data of hedging just 0 and 1.

When 0 is the company doesn’t do hedging and when 1 is the company

does hedging that explained the minimum and maximum of the value.

4.3 Data Analysis

4.3.1 Classical Assumption Test

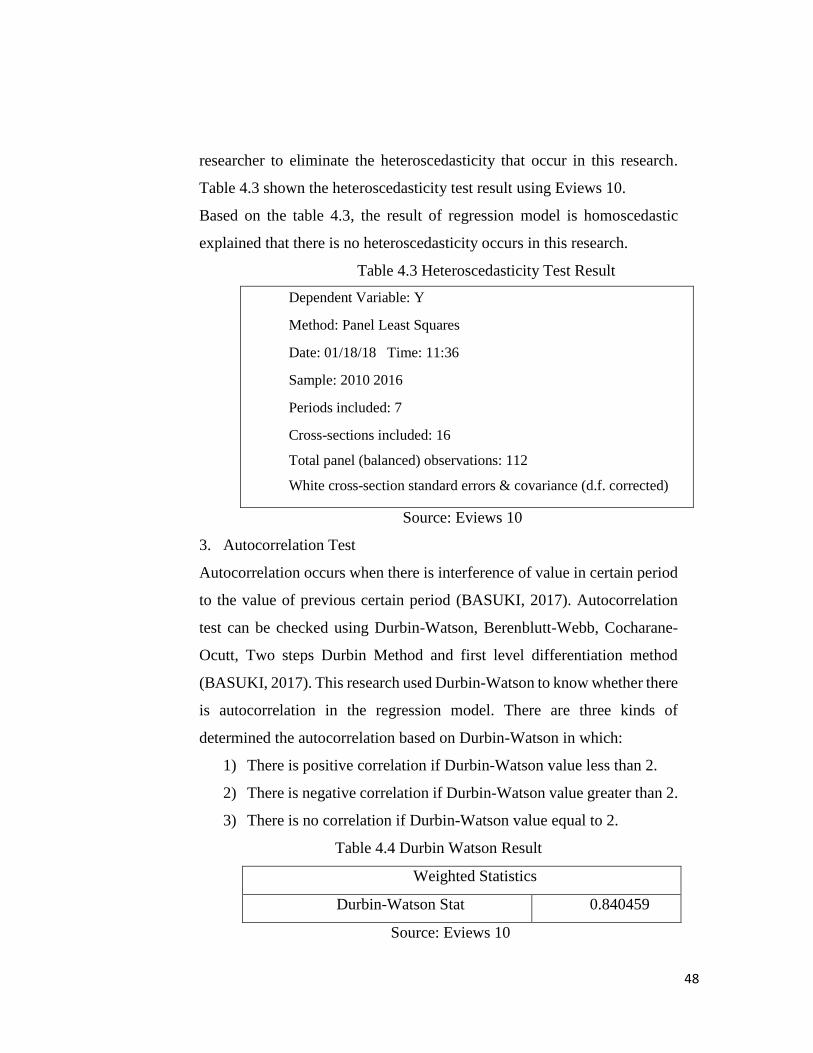

Classical assumption test needed to test whether the model has passed the

requirement. The model has to fulfilled the normality test,

heteroscedasticity, multicollinearity, and autocorrelation in order to reach

the valid result using multiple regression.

1. Normality Test

One of the statistical test used to know whether the data normally distributed

or not using normality test (Fallo, Setiawa, & Susanto, 2013). Normality

test generate the statistical and graphic information about distribution each

variable. By looking at the histogram, researcher knows the data normally

distributed or not. This research will show the analysis of the normality test

47

that conducted by the researcher using Jarque-Bera and probability that

shown by table.

Table 4.2 Normality Test Result

0

2

4

6

8

10

12

14

-1.0 -0.5 0.0 0.5 1.0 1.5

Series: Standardized Residuals

Sample 2010 2016

Observations 112

Mean -1.05e-16

Median -0.102699

Maximum 1.553917

Minimum -1.236007

Std. Dev. 0.603921

Skewness 0.354543

Kurtosis 2.715587

Jarque-Bera 2.723907

Probability 0.256160

Source: Eviews 10