Pension solutions for multinational companies Robeco PPI · Framework for implementing change (DB...

28

Pension solutions for multinational companies Robeco PPI Confident – Asinta Conference Amsterdam, 24 May 2012 Jacqueline Lommen / Xander Smelter For institutional investors

Transcript of Pension solutions for multinational companies Robeco PPI · Framework for implementing change (DB...

Pension solutions for multinational companies

Robeco PPI

Confident – Asinta Conference

Amsterdam, 24 May 2012

Jacqueline Lommen / Xander SmelterFor institutional investors

2

1. International pension solutions via IORPs*

2. Dutch PPI pension institution

3. Robeco PPI

Pension solutions for multinational companies

IORP: Institution for Occupational Retirement Provisions

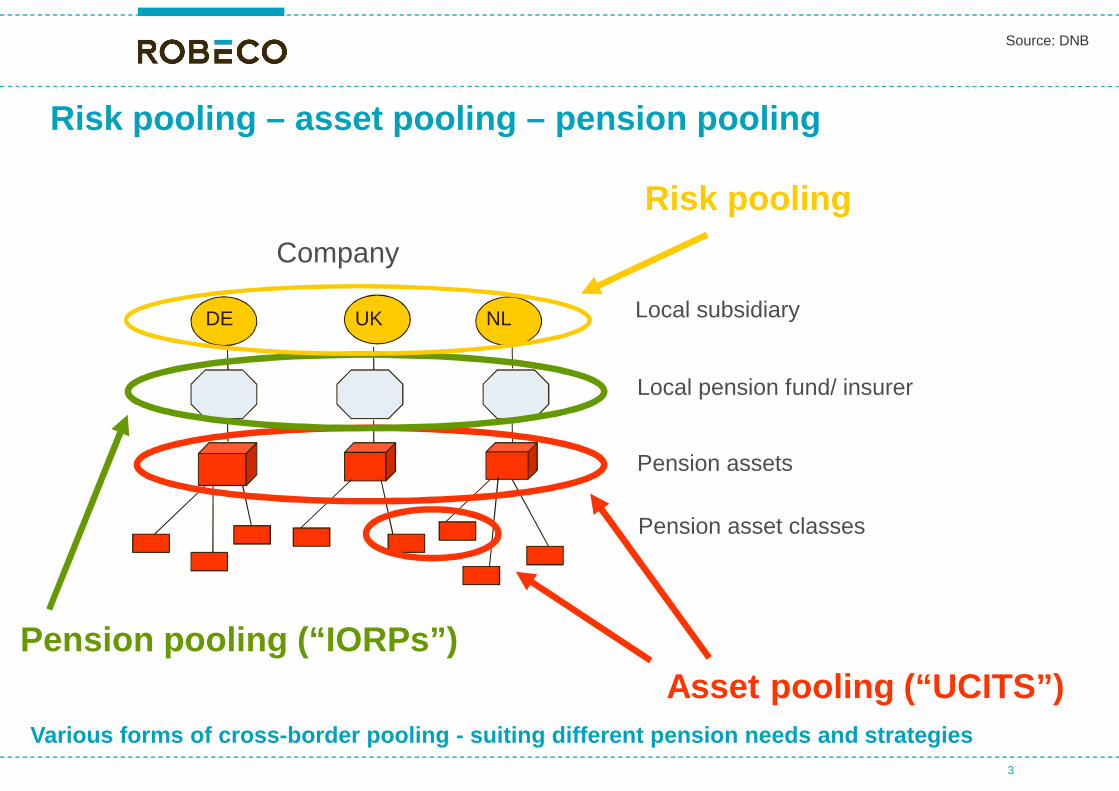

3

DE NLUK

Company

Pension pooling (“IORPs”)

Local subsidiary

Local pension fund/ insurer

Pension assets

Pension asset classes

Asset pooling (“UCITS”)

Risk pooling

Risk pooling – asset pooling – pension pooling

Source: DNB

Various forms of cross-border pooling - suiting different pension needs and strategies

Cross-Border IORPs: Strategic drivers formultinationalsMore grip and control /Reduced operational risks(IFRS, compliance, IORP2)

• More flexible and predictable funding• Improved operational oversight (compliance)• Integral risk management• Less management time

Cost savings(single European entity)

• Lower regulatory burden (single supervisor)• Biometric risk pooling• Tax advantages

Internal branding (common look/feel, equality)

Pension provisions for mobile employees and senior executives

Framework for implementing change (DB ->DC, gradual convergence)

Efficiency gains /Quality enhancement(economies of scale)

• Investment performance enhancement• Consistent administration hub(s)• Better access to top quality resources• Fewer providers and interfaces

Flexibility:maintainthe local schemespecifics e.g.format (DC/DB,indexation),financing(contributions),solidarity(ring-fencing), etc.

Own identity:Maintain(part of)local governance,Information to members,language, etc.

Anticipating and digesting M&A transactions; divestitures

HRM / IEB manager

CFO / CRO Local Trustees /Members

4

Source: AonHewitt / Netspar

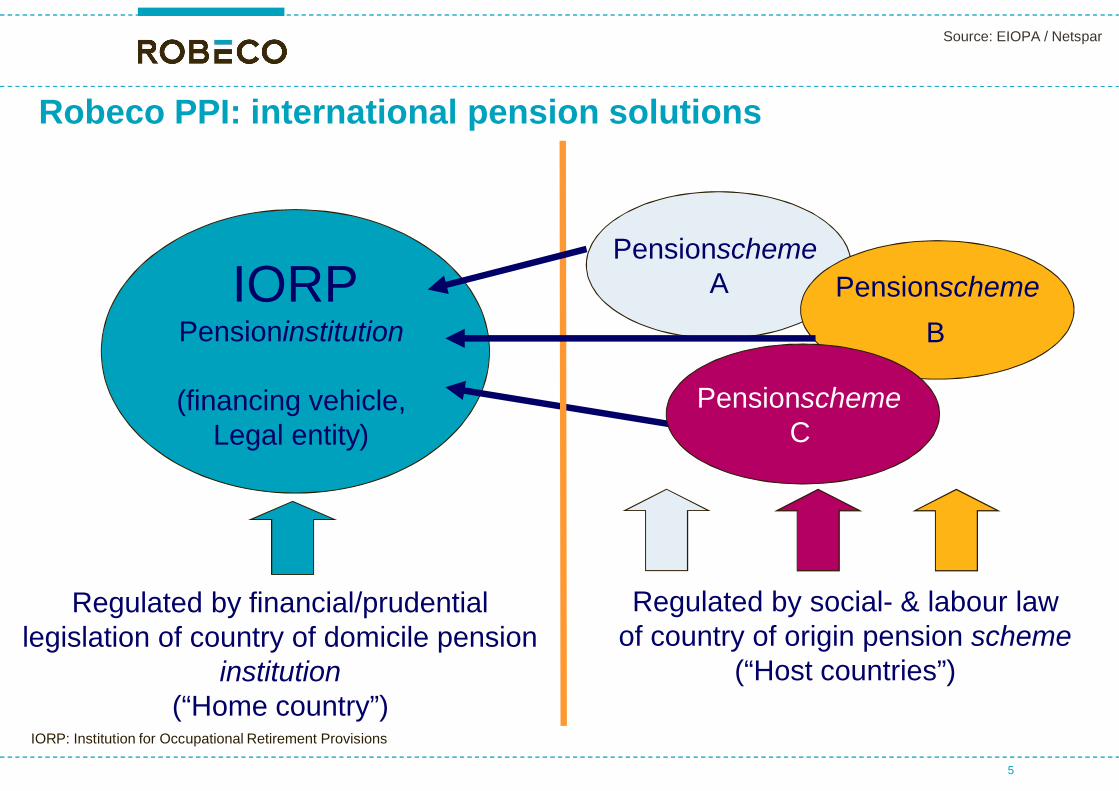

5

IORPPensioninstitution

(financing vehicle,Legal entity)

PensionschemeA Pensionscheme

B

Regulated by financial/prudentiallegislation of country of domicile pension

institution(“Home country”)

Regulated by social- & labour lawof country of origin pension scheme

(“Host countries”)

PensionschemeC

Robeco PPI: international pension solutions

Source: EIOPA / Netspar

IORP: Institution for Occupational Retirement Provisions

6

Two IORP models to choose from: “Closed-end” vs “Open-end”IORP

• IORP is created and owned by employer

• IORP capital is owned / paid up byemployer

• IORP manages schemes solely fromgroup/sector

• IORP is created and owned by financialprovider

• IORP capital is owned / paid up by provider

• IORP manages schemes from variouscompanies

Closed-end IORP Open-end IORP

IORP is a “pension trust”

Common business model in UK, Ireland,Benelux

IORP is a “financial institution”

Common business model in Germany,Switzerland, South-Europe, East-Europe

Both models can exist next to each other

7

Cross-border IORPs - Some market insights and lessonslearned1. Local Social- and labour law and tax no longer major obstacles for international pension solutions

2. European pension funds is about creating a single pension institution, not a single pensionscheme

3. Twothird is stakeholder management; onethird is technical issues

4. Stepwise approach; local triggers create momentum (eg: deficits, trustees, M&A, localrestrictions)

5. As well DB (first movers!) as DC schemes

6. Pilot cases to create cross-border pension platform – testing the waters

7. EU memberstates positioning themselves for the cross-border market and accommodatingprivate sector

8. …

Practical experience and momentum being gained

8

1. International pension solutions via IORPs*

2. Dutch PPI pension institution

3. Robeco PPI

Pension solutions for multinational companies

IORP: Institution for Occupational Retirement Provisions

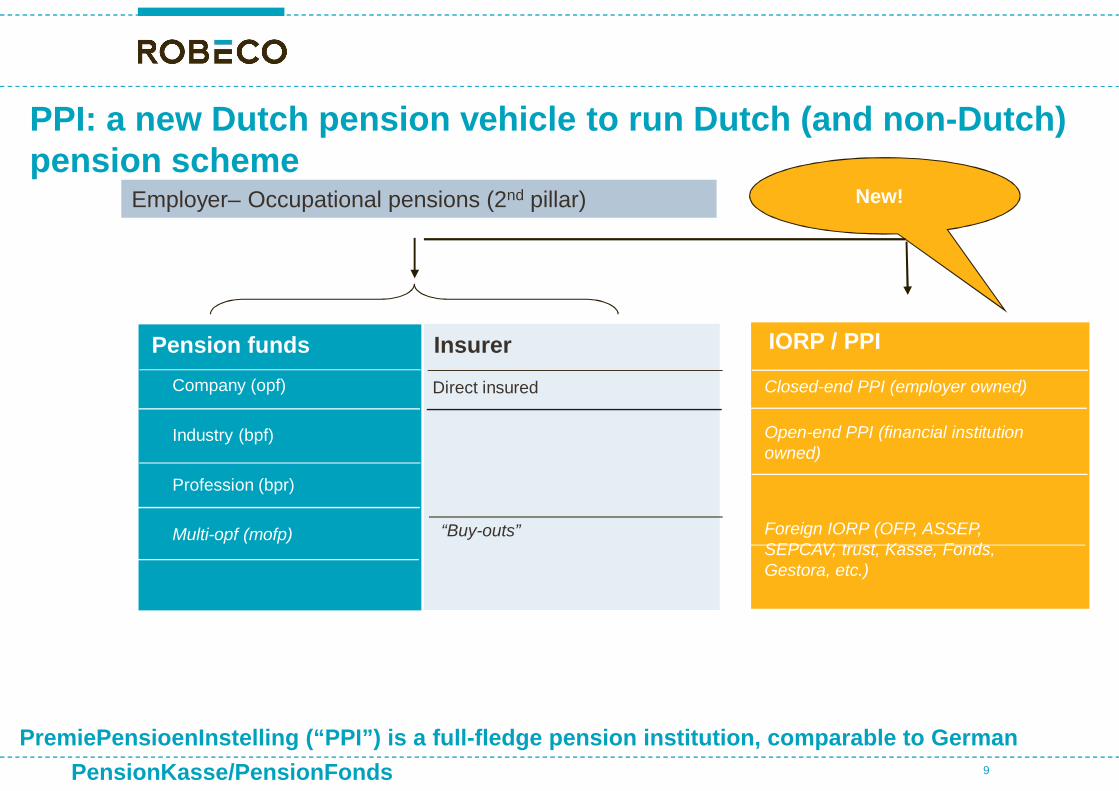

Employer– Occupational pensions (2nd pillar)

Pension funds InsurerClosed-end PPI (employer owned)

Open-end PPI (financial institutionowned)

Foreign IORP (OFP, ASSEP,SEPCAV, trust, Kasse, Fonds,Gestora, etc.)

New!

Direct insured

“Buy-outs”

IORP / PPI

Company (opf)

Industry (bpf)

Profession (bpr)

Multi-opf (mofp)

PPI: a new Dutch pension vehicle to run Dutch (and non-Dutch)pension scheme

9

PremiePensioenInstelling (“PPI”) is a full-fledge pension institution, comparable to GermanPensionKasse/PensionFonds

10

PPI – brief description

PPI:

1. “Premium Pension Institution” (“PremiePensioenInstelling”)

2. full-fledge pension institution equipped to run occupational pension schemes (“pensionplans”) on behalf of employers and employees

3. specially designed to act as a European-wide pension fund i.e. to run pension schemesfor employers and employees in various countries out of a single entity

4. has been introduced by law on 1/1/11

PPI introduction triggered by:

1. Positioning The Netherlands as a leading pension country and international pension hub

2. Facilitating employers in offering pensions to their employees (in local markets andinternational)

3. Triggering change in “troubled” local Dutch pension market

Cross-border pension institutions (“IORPs”): Acomparison

IR/ UK LU LI BE DE NLTrust ASSEP SEPCAV CAA PFonds OFP PFonds PKasse Pfonds PPI

Governance

Scope

Finance

“Nature” pensioninstitute

Pens inst invest fund insurer pensioninstitute

pensioninstitute

pensioninstitute

insurer pensioninstitute

investfund

Support

11

Source: Aon Hewitt

Fundamental differences between IORPs require a careful selection byemployers/employees see next slides

12

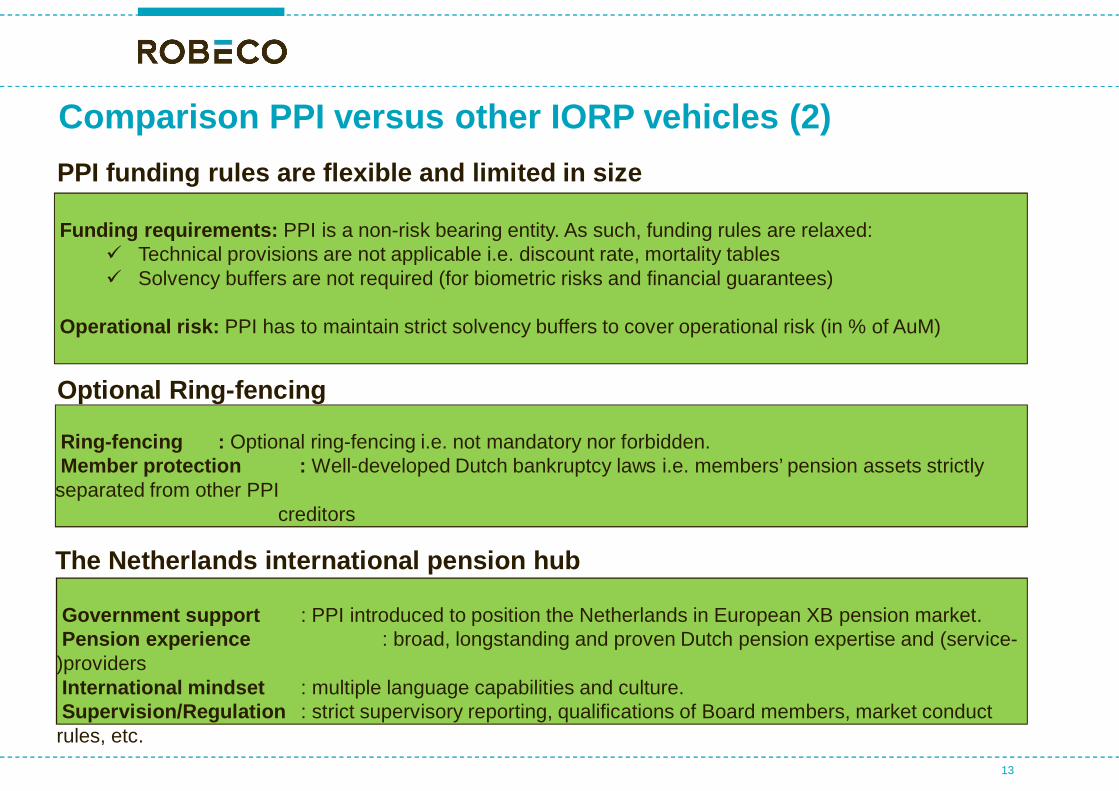

Comparison PPI and other IORP vehicles (1)

Ownership : Open-end and Closed-end PPILegal form : Free to choose (NV, BV, mutual)Governance : Flexible. Governance structure depends on legal form ánd on own preferenceBoard composition : No mandatory trustees or employee representatives in overall PPI Board

PPI Governance structure is very flexible

PPI is a non-risk bearing entity

The PPI itself is NOT allowed to absorb financial (minimum return) guarantees nor biometric risk (longevity,death, disability) on its own balance sheet.

Note: PPI is fully allowed to run/offer pension schemes which include these risk covers, but risks have tobe outsourced to a 3rd party e.g. insurance company, captive

PPI has a broad scope

Pension schemes : All kind of pension schemes (“premieregelingen”)Geographical focus : Pension schemes for employees and employees from various countries i.e. >EU30Companies : No restrictions regarding origin of employer i.e. part of a specific group, industry, region

13

Funding requirements: PPI is a non-risk bearing entity. As such, funding rules are relaxed:Technical provisions are not applicable i.e. discount rate, mortality tablesSolvency buffers are not required (for biometric risks and financial guarantees)

Operational risk: PPI has to maintain strict solvency buffers to cover operational risk (in % of AuM)

PPI funding rules are flexible and limited in size

Ring-fencing : Optional ring-fencing i.e. not mandatory nor forbidden.Member protection : Well-developed Dutch bankruptcy laws i.e. members’ pension assets strictlyseparated from other PPI

creditors

Optional Ring-fencing

Comparison PPI versus other IORP vehicles (2)

The Netherlands international pension hub

Government support : PPI introduced to position the Netherlands in European XB pension market.Pension experience : broad, longstanding and proven Dutch pension expertise and (service-)providersInternational mindset : multiple language capabilities and culture.Supervision/Regulation : strict supervisory reporting, qualifications of Board members, market conductrules, etc.

14

1. International pension solutions via IORPs*

2. Dutch PPI pension institution

3. Robeco PPI

Pension solutions for multinational companies

IORP: Institution for Occupational Retirement Provisions

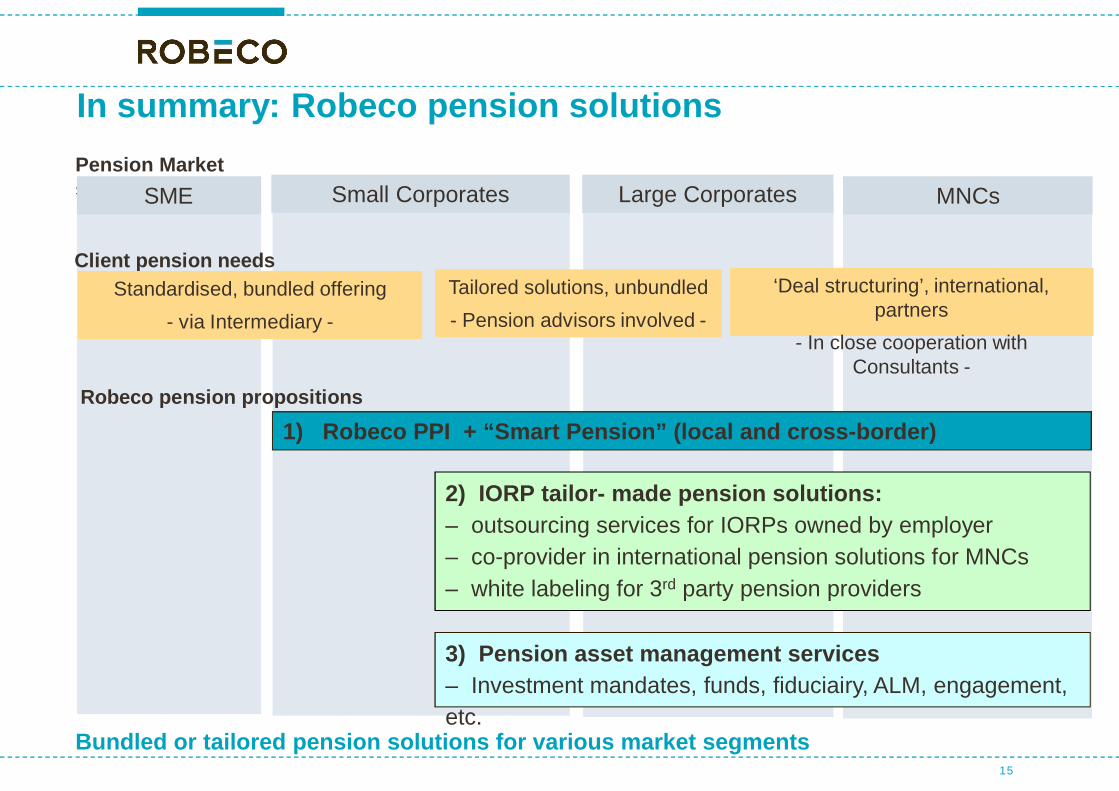

In summary: Robeco pension solutions

15

Small CorporatesPension Marketsegments Large Corporates MNCs

Client pension needsTailored solutions, unbundled- Pension advisors involved -

Standardised, bundled offering- via Intermediary -

‘Deal structuring’, international,partners

- In close cooperation withConsultants -

Robeco pension propositions

1) Robeco PPI + “Smart Pension” (local and cross-border)

2) IORP tailor- made pension solutions:– outsourcing services for IORPs owned by employer– co-provider in international pension solutions for MNCs– white labeling for 3rd party pension providers

Bundled or tailored pension solutions for various market segments

3) Pension asset management services– Investment mandates, funds, fiduciairy, ALM, engagement,etc.

SME

Insurance

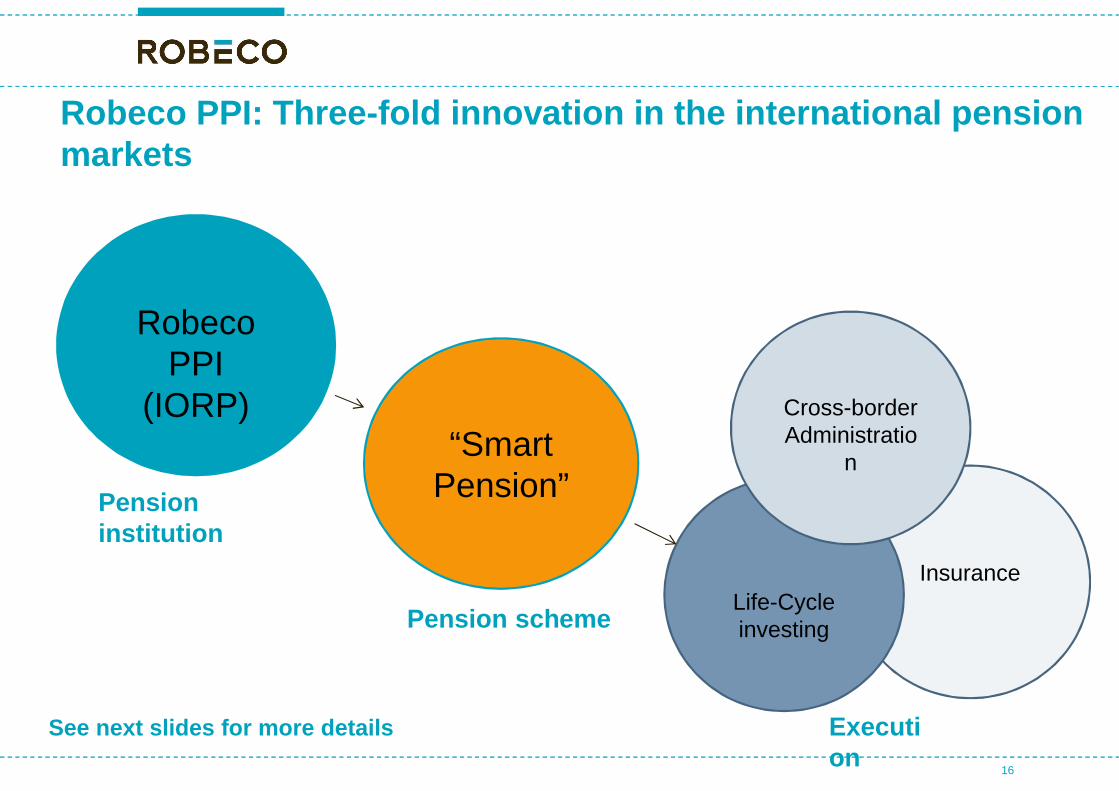

Robeco PPI: Three-fold innovation in the international pensionmarkets

16

RobecoPPI

(IORP)“Smart

Pension”

Life-Cycleinvesting

Pensioninstitution

Pension scheme

Cross-borderAdministratio

n

Execution

See next slides for more details

17

Robeco PPI: an international pension provider

Robeco PPI launched in 2011Fully licensed pension institution (open-end IORP), well-funded and backed up by Robeco

Operating out of new Dutch PPI vehicle

Leveraging on Robeco’s >25years DC pension experience

>50,000 scheme members, Aum circa 1bn

International focus

Partnering model; best-in-class providers

Insurance cover for biometric risksPreferred partnerTailor-made pension solutions(international)

Administration and membercommunicationInternational capabilities and mindset

Investing via innovative LifecyclingInternational pension assetmanager

Insu-rance

RobecoPPI

(IORP)

SmartPensio

n

Life-Cycle

investing

XBAdmini-stration

Insu-rance

18

Pension scheme “Smart Pension” (1)

RobecoPPI

(IORP)

SmartPensio

n

Life-Cycle

investing

XBAdmini-stration

Black versus White ??!! DBDC

Employers:“IFRS proof” & predictable impact on P&L

Low and transparant operational costs (advantages ofscale)

Integer pension promise

Employees:Controlled life-cycling investing (default option)

Transparency re. premium contribution, accrued valueand expected pension benefit

Collective biometric risk coverage (solidarity)Simplicity

Smart DC

19

St PPIRobeco

SmartPensionScheme

Easy

Advanced1.Life Cycling

3.Opting Out

2.Minimumreturn /Guarantee

Pension scheme “Smart Pension” (2) Insu-rance

RobecoPPI

(IORP)

SmartPensio

n

Life-Cycle

investing

XBAdmini-stration

Examples of Robeco PPI clientcases:1. Supplementary DC schemes2. Transition from (closed) DB to

DC schemes3. Liquidations of pension funds4. International solutions

Insu-rance

20

Investments: DC Life cycling – Advanced (1)

RobecoPPI

(IORP)

SmartPensio

n

Life-Cycle

investing

XBAdmini-stration

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63

Risicovol Risico-arm

• Allocation between matching (green colour) and return fund (red colour)

• Allocation path is client-specific (”risk tolerance”) Per company, group of employees or evenindividual member

• Based on latest “Human capital Theory”

% ofAssets

Age of schememember

Smart pension Advanced offers a tailored solution taking into account different risk tolerance ofscheme members

Several criteria taken intoaccount in setting tailored

allocation path:DC scheme purpose, Age,

Salary level, Human capital,Premium contributions

Return

Risk

Insu-rance

RobecoPPI

(IORP)

SmartPensio

n

Life-Cycle

investing

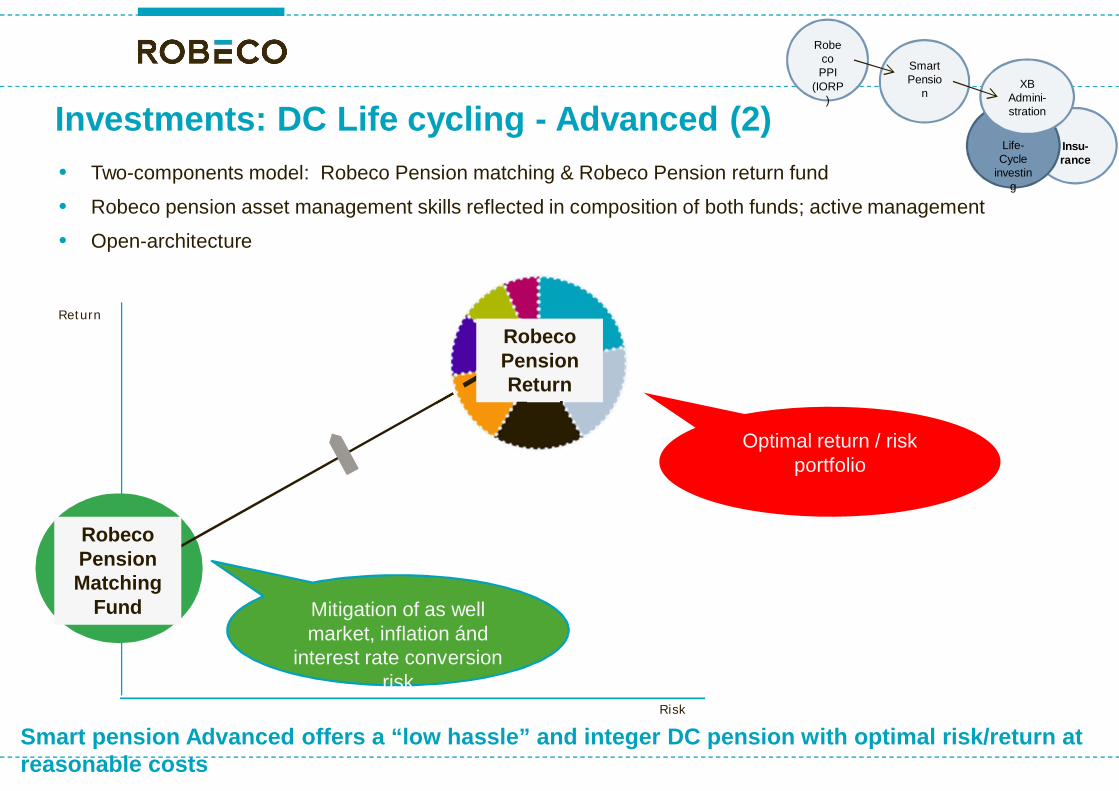

XBAdmini-strationInvestments: DC Life cycling - Advanced (2)

• Two-components model: Robeco Pension matching & Robeco Pension return fund

• Robeco pension asset management skills reflected in composition of both funds; active management

• Open-architecture

RobecoPensionReturnFund

RobecoPensionMatching

Fund Mitigation of as wellmarket, inflation ánd

interest rate conversionrisk

Smart pension Advanced offers a “low hassle” and integer DC pension with optimal risk/return atreasonable costs

Optimal return / riskportfolio

Insu-rance

Pension administration: web-enabled membercommunication

electronic binder

Insight and switches

Pension planner

Employer dashboard

22

Multi-country and multi-lingual

Up-to date information

RobecoPPI

(IORP)

SmartPensio

n

Life-Cycle

investing

XBAdmini-stration

Employer Look&Feel

24/7 access

Call center

Interface with salary system

Insu-rance

23

Insurance: biometric risks & life-long annuities

RobecoPPI

(IORP)

SmartPensio

n

Life-Cycle

investing

XBAdmini-stration

Insurance coverAccrual phase: Survivors benefits and Disability benefits covered

Payout phase: life-long annuities

Insurance carrierGenerali is preferred insurance partner

Other insurers optional, depending on client’s preference

24

Brief Robeco Profile

* As of end Q1 2012: AuM euro 177bn

Retail 54.1%Institutional 45.9%

Client type breakdown Institutional business by client type

Netherlands 46.4%Rest of the world 53.6%

Clients by location

Pension funds 55.3%Insurance 19.4%Public/government 5.9%Corporate 5.1%Bank 4.5%Other 9.8%

25

Robeco: a longstanding international pension assetmanagement company

26

Robeco – international network

ChicagoHarbor Capital AdvisorsAsset management, sales

BostonRobeco Investment Management

Asset management, salesHarbor Capital Advisors

Sales

New YorkRobeco Investment ManagementAsset management, salesSAMAsset management, sales

ParisRobeco France

Asset management, sales

MadridRobeco Spain

Sales

Zurich; ZugRobeco Switzerland

SalesSAM

Asset management, salesCorestone

Asset management

RotterdamIntl. HQ; Alt & Sust. Inv.; Inv. Mgmt; Retail; TranstrendAsset management, sales, research

LuxembourgRobeco LuxembourgSales

FrankfurtRobeco GermanySales

BahrainRobeco Middle EastSales

MumbaiCanara RobecoAsset management, sales

Hong KongRobeco Greater Chinaand South East AsiaAsset management, sales

TokyoRobeco JapanSales

= investment management and sales= sales only= representative office

SydneySAMSales

ShanghaiRobeco Mainland ChinaRepresentative office

Greenbrae; Los AngelesRobeco Investment ManagementAsset management, sales

SeoulRobeco KoreaRepresentative office

TaiwanRobeco Greater Chinaand South East AsiaSales

Institutional Sales / Client Relationship Management

Bert EijkelenboomSalesmanager

Oskar PoieszManager Robeco Pension Providers

Frits BruiningsSenior Accountmanager

Ed VermeulenAccountmanager

Wendy WiglevenClient Service Officer

Client Services / Operational Support

Andrea van HaaftenSenior Client Service Officer

Selma TasgilClient Service Officer

Arjan van DongenAccountmanager /Proces Specialist

Premie PensioenInstelling

Jacqueline LommenBoard member Robeco PPIEuropean Pensions

Tel: +31.10.224.1283Mob: +31.6.1131.7279Email: [email protected]

27

Robeco PPI – Client contact persons

Maureen SchlejenDirector Pension Sales

Xander SmelterInstitutional Sales Benelux

Tel: +31.10.224.7230Mob: +31.6.1278.64.97Email: X.Smelter @robeco.nl

Important Information

• This document has been carefully prepared by ‘Stichting Robeco PremiePensioenInstelling’ (Robeco PPI). It isintended to provide the reader with information on Robeco PPIs specific capabilities, but does not constitute arecommendation to buy or sell certain securities or investment products.

• The information contained in this document is solely intended for professional parties under the Dutch Act on theFinancial Supervision (Wet financieel toezicht) or persons who are authorized to receive such information under anyother applicable laws.

• The content of this document is based upon sources of information believed to be reliable, but no warranty ordeclaration, either explicit or implicit, is given as to their accuracy or completeness. This document is not intended fordistribution to or use by any person or entity in any jurisdiction or country where such distribution or use would becontrary to local law or regulation.

• Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco PPIs expectations forthe future. Past performances may not be representative for future results and actual returns may differ significantlyfrom expectations expressed in this document. The value of your investments may fluctuate. Results obtained in thepast are no guarantee for the future.

• All copyrights, patents and other property in the information contained in this document are held by Robeco PPI. Norights whatsoever are licensed or assigned or shall otherwise pass to persons accessing this information.

• The information contained in this publication is not intended for users from other countries, such as US citizens andresidents, where the offering of foreign financial services is not permitted, or where Robeco's services are not available.

• Stichting Robeco PremiePensioenInstelling’ in Rotterdam (Trade Register no. 51867680) is licensed by the Dutchregulator ‘De Nederlandsche Bank’.

28

Disclaimer