Pension Risk Management ALM Discussion

26

Financial Services, Regulatory, and Risk Consulting LLC Matthew Kruse, Partner in conjunction with Quiet Light Trading LLC January 2011

-

Upload

matthew-kruse-mba-ms-capital-markets-frm -

Category

Documents

-

view

215 -

download

3

Transcript of Pension Risk Management ALM Discussion

Financial Services, Regulatory, and Risk Consulting LLC Matthew Kruse, Partner

in conjunction with Quiet Light Trading LLC

January 2011

Section 1 Section 2 Section 3

De-Risking Glide Path Monitoring & Reporting

Asset Liability Management

Approach Funded Status* Attribution

Capital MarketsModeling

Tailor to each plan* Open / Closed / Frozen* Funded Status* Duration* Funding Policy

Risk Factors* Assets* Liabilities

Model Outputs

Implementation Metrics Analysis

FSR2Page 1 / 25

FSR2Page 2 / 25

FSR2Page 3 / 25

FSR2Page 4 / 25

FSR2Page 5 / 25

FSR2Page 6 / 25

FSR2Page 7 / 25

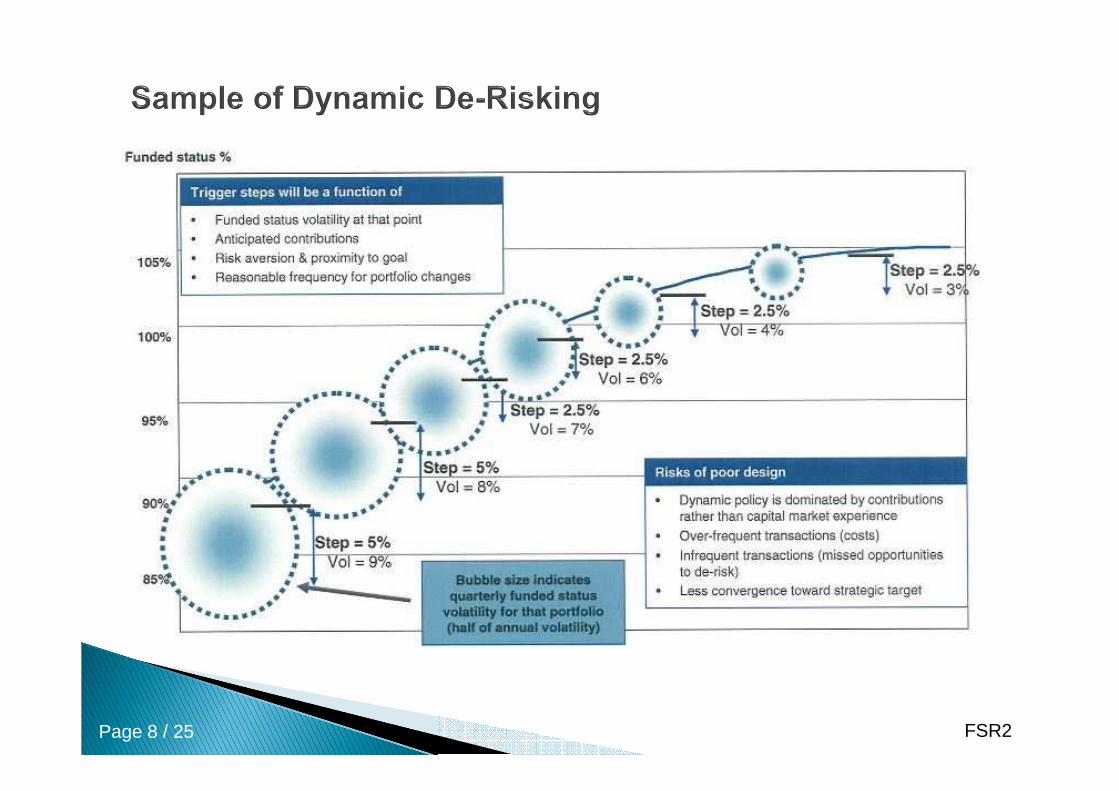

FSR2Page 8 / 25

FSR2

Commentsa) For a 100% funded plan, long term return on asset of approximately 7.6% should generate the necessary return to cover annual benefit accruals.

b) If the plan runs a surplus, a small allocation to growth assets would be sufficient to sustain the amount. This is based on the theory that liability matching to assets will generate a return equivalent to liability growth rates.

c) To mitigate volatility, such an allocation would improve the likelihood of sustaining the surplus.

Page 9 / 25

FSR2

Commentsa) Static asset allocation leads to more risk as funded status improves.

b) Steady level of surplus returns can be generated while taking less risk of losing funded status.

Page 10 / 25

FSR2Page 11 / 25

FSR2Page 12 / 25

FSR2Page 13 / 25

FSR2Page 14 / 25

FSR2Page 15 / 25

FSR2Page 16 / 25

FSR2Page 17 / 25

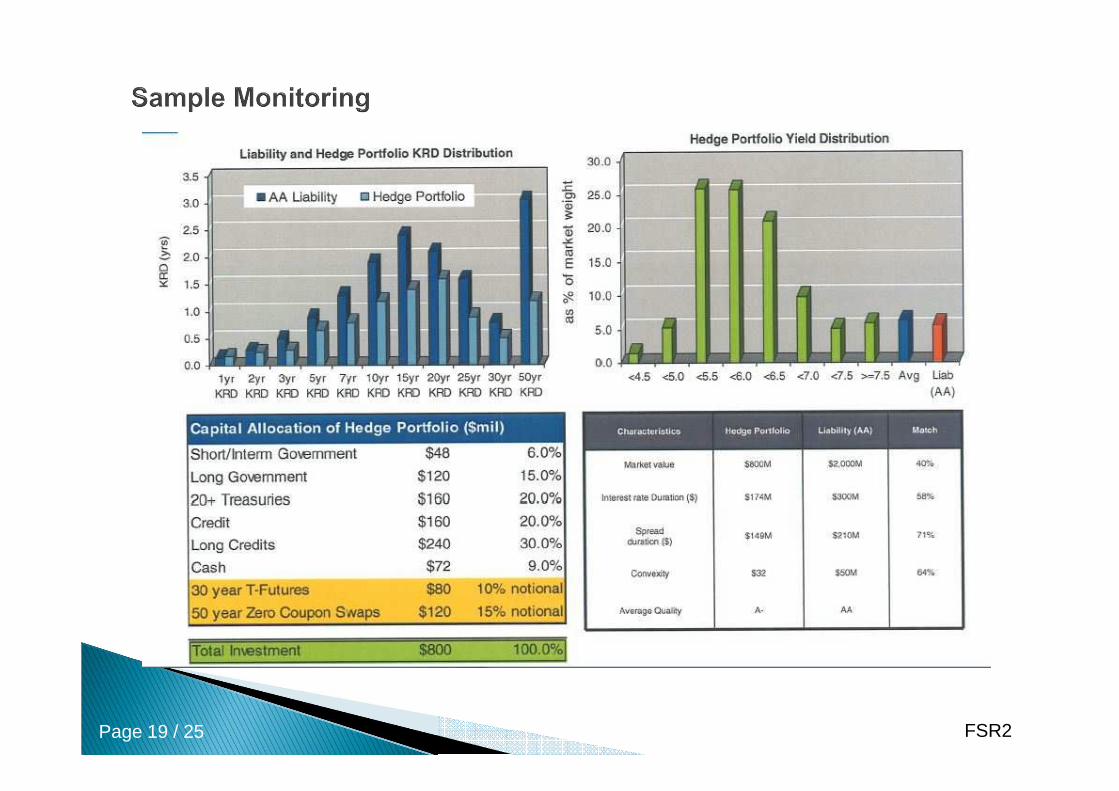

FSR2

It is important to monitor periodic changes in liabilities, assets, and funded status to attribute the sources of change for comparison to risk buckets and hedging targets.

The goal is to understand drivers of performance and have information to support adjustments to investment strategies.

Page 18 / 25

FSR2Page 19 / 25

FSR2Page 20 / 25

FSR2Page 21 / 25

FSR2Page 22 / 25

FSR2

Step 1: Generate* Inflation* Economic Growth

Step 2: Generate

* Nominal Yield Curve* Real Yield Curve* Equity Yields* Dividend Yields* Corporate Bond Spreads

Step 3: Determine Change in Exchange Rates

Step 4: Compute* Bond Returns* Equity Returns

Step 5: Determine International Returns

Page 23 / 25

FSR2

a) Within the model, the fundamental factors of growth (GDP), inflation, and interest rates should be contemplated, including correlations between the three.

b) A multi-factor Monte Carlo model is recommended.

c) Major economic impairments should be considered.

d) Results should be discussed with the team, to make informed strategy decisions.

Page 24 / 25

FSR2

Financial Services, Regulatory, and Risk Consulting appreciates the opportunity to offer ALM advisory services, in partnership with Quiet Light Trading LLC.

Feel free to contact Matthew Kruse to discuss engaging FSR2’s services.

Matthew KruseFSR2 [email protected]

Page 25 / 25