Pension Protection Fundresearchbriefings.files.parliament.uk/documents/SN03917/SN03917.pdf ·...

24

www.parliament.uk/commons-library | intranet.parliament.uk/commons-library | [email protected] | @commonslibrary BRIEFING PAPER Number CBP-03917, 30 January 2018 Overview of the Pension Protection Fund By Djuna Thurley Inside: 1. Background 2. Schemes 3. PPF compensation 4. Funding 5. The Financial Assistance Scheme

Transcript of Pension Protection Fundresearchbriefings.files.parliament.uk/documents/SN03917/SN03917.pdf ·...

www.parliament.uk/commons-library | intranet.parliament.uk/commons-library | [email protected] | @commonslibrary

BRIEFING PAPER

Number CBP-03917, 30 January 2018

Overview of the Pension Protection Fund

By Djuna Thurley

Inside: 1. Background 2. Schemes 3. PPF compensation 4. Funding 5. The Financial Assistance

Scheme

Number CBP-03917, 30 January 2018 2

Contents Summary 3

1. Background 4 1.1 Pensions Act 2004 4 1.2 Framework for the PPF 4

2. Schemes 6 2.1 Eligibility 6

Trigger for entering an assessment period 6 Purpose of assessment period 7

2.2 Numbers 8

3. PPF compensation 9 3.1 Two levels of compensation 9 3.2 The compensation cap 10

Long-serving scheme members 11 3.3 Indexation 13 3.4 Early payment 14 3.5 Lump sum payment in cases of terminal illness 15

4. Funding 16 4.1 The pension protection levy 16

Structure 16 Process for setting the levy 16

4.2 The PPF’s funding status 21

5. The Financial Assistance Scheme 22

Contributing Author: Djuna Thurley

3 Pension Protection Fund

Summary The Pension Protection Fund (PPF) was one of the measures set up by the Pensions Act 2004 in response to a series of high-profile cases in which pension schemes had wound up with insufficient assets to meet their pension commitments. It was established to pay compensation to members of defined benefit and hybrid occupational pension schemes where an employer has become insolvent, and where there are insufficient assets in the pension scheme to cover PPF levels of compensation. It is funded from the assets of schemes transferred to the Fund, investment returns and by annual levy on eligible schemes. It commenced operations on 6 April 2005 and applies to schemes that started winding up after that date.

This note provides an overview how the PPF works. More background to its establishment of the PPF is contained in a Library Briefing Papers, SN 2779 Pension Protection Fund 1993-2003 and 04/18 on the Pensions Bill 2003/04.

Number CBP-03917, 30 January 2018 4

1. Background Defined Benefit (DB) schemes provide pension benefits based on fixed factors – typically salary and length of service. From the point of view of members, the critical point is that they know what pension they will eventually get.

In the early years of the 21st century, there were a number of high profile cases which wound up with insufficient assets to meet their pension commitments, leaving members facing dramatic shortfalls in their pension.1

1.1 Pensions Act 2004 In response, the Labour Government legislated in the Pensions Act 2004 to establish a Pension Protection Fund to pay compensation to members of DB schemes where an employer has become insolvent, and where there are insufficient assets in the pension scheme to cover PPF levels of compensation.2 In a statement to Parliament in June 2003, the then Secretary of State for Work and Pensions, Andrew Smith, set out the rationale for this as follows:

[…] if people expect their holiday provider or motor insurer to be covered if the firm goes bust, there is no cover for something as important as an occupational pension. We will therefore legislate to set up a pension protection fund. That fund will take over the schemes of insolvent companies to ensure not only that pensions in payment are protected, but that those still working can be sure of getting 90 per cent of what they were promised. It will be paid for by a fixed-rate levy and an additional risk-related premium, which, together with a salary cap, will minimise perverse incentives and moral hazard. The fund will be a non-Government body. It will meet its obligations through the power to set and vary the level of charge without recourse to public funds. Taken with the other measures, that is a big extension of pension security, for the first time guaranteeing protection if a company scheme goes bust.3

Other pension protection measures introduced in the same legislation, included:

• Replacing the Minimum Funding Requirement – which had been criticised for “distorting investment decisions without providing effective protection for members” - with new scheme-specific funding requirements – see Library Briefing Paper SN-04877 Pension scheme funding requirements (October 2017);

• Strengthening the regulatory framework through the introduction of a new Pensions Regulator, with the objective of protecting the benefits of members of work-based pension schemes and reducing the risk of situations arising that may lead to claims for compensation from the Pension Protection Fund.4 See Library Briefing Paper SN-04368 The Pensions Regulator – powers to protect pension benefits (January 2018).

• Changes to the ‘priority order’ for distributing remaining funds when a scheme winds up. For more detail, see SN-03399 Winding up a pension scheme (January 2006).

1.2 Framework for the PPF The Pension Protection Fund is a statutory fund run by the Board of the Pension Protection Fund, a statutory corporation.5 The first chair of the PPF was Lawrence Churchill.6 The current

1 For more detail, see Standard Note, SN 2779 Pension Protection Fund 1993-2003 and in Library Research Paper

04/18 on the Pensions Bill 2003/04. 2 Pension Protection Fund, Annual Report and Accounts 2008/09, HC 1084; For further information on the Fraud

Compensation Fund, see SN/BT/2691, ‘Pensions: Fraud Compensation Fund’ 3 HC Deb, 11 June 2003, cc683-684 4 Pensions Act 2004, s5; The Pensions Regulator – about us 5 Pensions Act 2004, Section 107 6 Lawrence Churchill is now chair of the National Employment Savings Trust (NEST)

5 Pension Protection Fund

chair is Lady Judge. Its Chief Executive, from 1 April 2009 to early 2018, was Alan Rubenstein, formerly a Managing Director of Lehman Brothers.7 Oliver Morley will be Chief Executive from March 2018.8

The rules applying to the PPF are in Part 2 of Pensions Act 2004 and the regulations made under it. The Pensions Act 2008 provided for PPF compensation to be shared on divorce.9 The Pensions Act 2011 made some changes in the light of experience.10

There is a framework document and a memorandum of understanding between the PPF, TPR and DWP.

7 PPF Press Release, 2 February 2009, ‘Alan Rubenstein appointed as next PPF Chief Executive’; PPF, 2014/15

Annual Report and Accounts HC 302, July 2015 8 Oliver Morely CBE appointed as next PPF Chief Executive, PPF press release, 20 December 2017 9 Part 3. The background to these changes is discussed in Library Research Paper 07/94 – Pensions Bill 10 Pensions Bill 2011 – Impacts – Annex D: Pension Protection Measures; Library Research Paper 11/52 Pensions Bill

Number CBP-03917, 30 January 2018 6

2. Schemes

2.1 Eligibility Section 126 of the 2004 Act provides that a scheme is “eligible” for the PPF if it is “not a money purchase scheme” (i.e; one where contributions are paid into a fund, which is invested and can then be drawn down or used to buy an income at retirement).

This means that the PPF covers defined benefit schemes and the defined benefit elements of hybrid schemes, with some exceptions set out in regulations – such as public service pension schemes and schemes with a ‘Crown Guarantee.’11 DB schemes that started to wind up before April 2005 are eligible for the Financial Assistance Scheme (FAS).12

The PPF website explains that, for a scheme to enter the PPF the following criteria must be satisfied:

a) the scheme must be a scheme which is eligible for the Pension Protection Fund;

b) the scheme must not have commenced wind up before 6 April 2005;

c) an insolvency event must have occurred in relation to the scheme's employer which is a qualifying insolvency event;

d) there must be no chance that the scheme can be rescued; and

e) there must be insufficient assets in the scheme to secure benefits on wind up that are at least equal to the compensation that the Pension Protection Fund would pay if it assumed responsibility for the scheme.13

Trigger for entering an assessment period The trigger for a scheme entering a PPF assessment period is generally that an insolvency practitioner notifies the PPF that “qualifying insolvency event” has occurred in relation to the employer of an eligible scheme.14

The definition of insolvency event under section 121 of the 2004 Act is consistent with those in the Insolvency Act 1986. The insolvency events vary depending on whether an employer is an individual, a company or a partnership. Most formal insolvency proceedings are covered, with the exception of members’ voluntary liquidation (which is a solvent form of liquidation and therefore not appropriate for compensation).15 (There is provision for relevant schemes whose sponsoring employer cannot have an insolvency event to be able able to enter the Pension Protection Fund.16)

However, there are cases where an employer facing insolvency has a deficit and will propose a rescue or restructuring package which will allow the employer to continue trading with the PPF taking on the scheme. The PPF has explained the main principles that must apply for it to do this:

• Insolvency has to be inevitable – this means that we will have to take on the pension debt whatever happens.

11 Pensions Act 2004 (s126) Pension Protection Fund (Entry Rules) Regulations 2005 (SI 2005/590); Pension

Protection Fund website – About us - eligibility 12 Pensions Act 2004, s286; The Pensions Act 2008, s124 provided for some schemes caught between the PPF and

the FAS to enter the FAS - see HL Deb, 14 July 2008, c1070 and SI (2008/3068) 13 The rules are in the Pensions Act 2004 (chapter 3) and the Pension Protection Fund (Entry Rules) Regulations 2005

(SI 2005/590); PPF website – Eligibility 14 Pensions Act 2004, s120-1. For where an employer cannot technically become insolvent, see s128 15 PPF website – insolvency events 16 Pensions Act 2004, s128; SI 2016/294

7 Pension Protection Fund

• The employer’s pension scheme will receive money or assets which are significantly better than it would have received through the otherwise inevitable insolvency are considered by the PPF to be realistic compared to the pension buy-out deficit.

• What is offered to the pension scheme in the restructure or rescue is fair compared to what other creditors and shareholders will receive as part of the deal.

• The pension scheme will be given 10 per cent equity in the new company if the future shareholders are not currently involved with the company. It will receive at least 33% if the parties are currently involved;

• We need to make sure the pension scheme would not have been better off by the Pensions Regulator issuing a contribution notice or financial support direction.

• The fees charged by the banks are reasonable where the deal involves a refinancing. • The other party pays legal fees incurred as part of the deal for both ourselves and the

scheme trustees.17 The PPF explains that it “does not enter into such agreements lightly” and that most negotiations take place alongside the Pensions Regulator (TPR) which usually need to ‘clear the deal’ before any agreement can be made.18 As examples of where it has become involved in restructuring or rescue deals, it cites Kodak, Monarch and UK Coal. TPR can issue reports under section 89 of the Pensions Act 2004 to explain the approach taken in such cases. For example: • Report in relation to the Kodak Pension Plan (November 2014) • Report in relation to UK Coal Operations Ltd (November 2014).

Purpose of assessment period The purpose of an assessment period is to determine whether the PPF should accept responsibility for the scheme. The PPF explains:

During the assessment period, and in order to determine whether it should assume responsibility for an eligible pension scheme, the Pension Protection Fund will look to establish answers to two key questions:

• can the pension scheme be rescued?

• can the pension scheme afford to secure benefits which are at least equal to the Pension Protection Fund protected liabilities if it assumed responsibility for the pension scheme?

If the answer to either of these questions is ‘yes’, the Pension Protection Fund will cease to be involved with the pension scheme and the pension scheme will either continue or wind-up outside of the Pension Protection Fund.

However, if the answer to both is ‘no’, and the relevant processes and procedures have been completed, the Pension Protection Fund will assume responsibility for the pension scheme.19

During an assessment period, trustees remain responsible for paying pensions, which must be paid at PPF compensation levels.20

There is an overview of what happens in an assessment period on the PPF website and a more detailed account in PPF’s Trustee Good Practice Guide.

17 PPF, Restructuring and insolvency. The PPF approach 18 Ibid; The framework within which the Pensions Regulator works is discussed in more detail in Library Briefing

Paper SN-04638 19 PPF website – trustee guidance – overview of the assessment period 20 Pensions Act 2004, s138; Pension Protection Fund – Assessment period

Number CBP-03917, 30 January 2018 8

2.2 Numbers In its first full year of operation the PPF accepted 98 schemes, with 43,000 members, into its assessment period. 10,000 members were receiving payments from their pension schemes at PPF levels of compensation.21 In December 2006, the PPF announced that it had started making direct payments to members of the first three pension schemes to transfer to the PPF.22

By the end of March 2017, 894 schemes had transferred to the PPF was managing £38.7 billion of assets. The PPF had 234,882 members (128,358 pensioner members and 106,524 deferred members). The average annual compensation per member was £4,380. 23

Details of schemes in assessment and those that have transferred to the PPF are on the website.

21 PPF press release, “PPF provides security in retirement for 43,000 people in first year”, 7 November 2006 22 PPF Press Release, ‘Landmark payments signal new era in pension protection’, 1 December 2006 23 PPF Annual Report and Accounts 2016/17, p17; PPF Annual Report 2014/15, p10

9 Pension Protection Fund

3. PPF compensation

3.1 Two levels of compensation The PPF provides two levels of compensation – in broad terms -100% to people who have reached pension age or are in receipt of an ill-health or survivors’ pension at the time the scheme enters the PPF assessment period and, in other cases, 90% subject to a cap.24

Its website explains:

If You Have Retired

You will have been receiving a pension from your scheme before your former employer went bust.

If you were beyond the scheme’s normal retirement age when your employer went bust, the Pension Protection Fund will generally pay 100 per cent level of compensation, which means we will generally pay you the same amount in compensation when your scheme enters the PPF.

Your payments relating to pensionable service from 5 April 1997 will then rise in line with inflation each year, subject to a maximum of 2.5 per cent a year. Payments relating to service before that date will not increase.

This information may also apply if you retired through ill-health or if you are receiving a pension in relation to someone who has died.

If You Retired Early

If you retired early and had not reached your scheme’s normal pension age when your employer went bust, then you will generally receive 90 per cent level of compensation based on what your pension was worth at the time. The annual compensation you will receive is capped at a certain level.

The cap at age 65 is, from 1 April 2017, £38,505.61 (this equates to £34,655.05 when the 90 per cent level is applied) per year. This is set by DWP.

From 6 April 2017, the Long Service Cap came into effect for members who have 21 or more years' service in their scheme. For these members the cap is increased by three per cent for each full year of pensionable service above 20 years, up to a maximum of double the standard cap.

The earlier you retired, the lower the annual cap is set, to compensate for the longer time you will be receiving payments.

You can view a full list of the compensation caps for 2017/18 at each age here.

Once compensation is being paid, then payments relating to pensionable service from 5 April 1997 will rise in line with inflation each year, subject to a maximum of 2.5 per cent. Payments relating to service before that date will not increase.

If You Have Yet to Retire

When you reach your scheme's normal retirement age, we will pay you compensation based on the 90 per cent level subject to a cap, as described above.

Until you reach normal retirement age and your compensation is put in payment, your compensation entitlement will rise in line with inflation each year, subject to a cap. See our FAQ about revaluation of compensation while you are a deferred member.

24 Pensions Act 2004, Sch 7

Number CBP-03917, 30 January 2018 10

From 30 April 2013, you may be able to take your compensation at a later age than your normal retirement age. If you defer taking your compensation, it will receive an actuarial adjustment to reflect the period it is postponed.

Once compensation is being paid, then payments relating to pensionable service from 5 April 1997 will rise in line with inflation each year, subject to a maximum of 2.5 per cent. Payments relating to service before that date will not increase.

If You Die

After your death, we will pay compensation to any children you may have who are under 18 years old, or under 23 if they are in full-time education or have a disability.

We will also generally pay compensation to any legal spouse, civil partner or other relevant partner. However, individual circumstances may differ depending on the rules of the former pension scheme.

Please read our leaflet on Compensation Payments for Survivors on our PPF members' site.

If You Are Divorced

A member’s compensation can be shared with their ex-spouse or former civil partner if the court makes a pension compensation sharing order. Please read our Divorce Booklet on the PPF members' site for more information. The charges for dealing with a Pension Sharing Order may be different, so you should contact the PPF for more details on these.25

As suggested above, compensation can be paid to survivors. In the case of unmarried partners, there must have been provision for this under the scheme rules. The pension scheme member must have made a valid nomination, or the surviving partner will need to show they were living together at the time of death and were financially dependent or interdependent.26

There is information for scheme members on the PPF website.

3.2 The compensation cap For the majority of those below normal pension age when the scheme enters a PPF assessment period, the PPF will pay a 90% level of compensation, subject to a cap. From April 2017, the cap at age 65 was £38,505.61 pa (which meant - when applying the 90 per cent provision at age 65 – a maximum level of compensation of £34,655.05).27 From April 2018, the cap will be £39,006.18 (£35,105.56 when the 90% was applied).28

The rationale behind the cap is to limit PPF expenditure and to provide an incentive for higher earners, who may have influence over the management of a defined benefit scheme, to ensure that a scheme remains out of the PPF if possible.29

When the legislation was before Parliament, the then Shadow Pensions Minister, Nigel Waterson, questioned the discrepancy in treatment of those under and over normal pension age: He noted that a number of organisations had suggested putting “pensioners” and “non-pensioners” on the same footing.30 In response, the then Pensions Minister, the late Malcolm Wicks, said:

25 PPF website/compensation 26 Pension Protection Fund (Compensation) Regulations 2005 (SI 2005 No. 670), regs 4-6; See also, PPF Factsheet,

Compensation for Survivors and Children, August 2007 27 PPF website - compensation 28 Explanatory Memorandum to SI 2018/39 29 Explanatory Memorandum to SI 2012/528, para 7.3; For more detail, see Library Briefing Paper SN-03917 Pension

Protection Fund (July 2012) 30 Pensions Bill Committee Deb, 30 March 2005, c477

11 Pension Protection Fund

The PPF is a unique institution [...] It is a compensation scheme to ensure people that their pension rights will be safeguarded. Exactly what their pension rights are, and whether they are high enough and so on, is something that we are discussing.[...]

Let me explain why we do not favour paying everyone 100 per cent. In an ideal world we would have liked to pay everybody exactly what they were expecting from their scheme, but sadly we cannot do that. In the real world, employers have to bear the cost of the PPF and there are moral hazard issues, which we would be foolish to ignore.[...].31

In response to further questioning, he added that a balance needed to be struck and that both pensioners and non-pensioners were likely to be better off than if no PPF were established:

In terms of the famous cliff edge, I can see the letters coming in now—and I understand why—from people close to retirement age and to the 100 per cent. I hope that when they write those letters to the then Minister with responsibility for pensions they will reflect that if we had not got the PPF the figure might have been 30 per cent. That is the alternative. I hope that we shall all keep reminding ourselves of that. We might think that 90 per cent. or 100 per cent. is right, but both of them are better than 30 per cent.32

Long-serving scheme members On1 July 2013, the then Pensions Minister, Steve Webb, announced that he intended to change the rules to enable those with service of more than 20 years with a firm to get an enhanced level of PPF compensation. This was because the cap – which was intended partly as a cost-control measure and partly to prevent moral hazard – had a disproportionate effect on scheme members with long service:

The original thinking behind that cap was partly as a cost-control measure and partly to prevent moral hazard. The argument there was that if the rules stated that anybody who was drawing a pension would get that in full, even after an insolvency event, and the people who had not started to draw a pension would have to make do with what was left in the fund, there might be an incentive for those in the know at the top of a firm close to insolvency to retire and draw their pension before scheme pension age [...] However, one of its consequences was a disproportionate effect on those with long service and, in a debate in Westminster Hall on the Visteon pension scheme for former Ford workers in December 2012, I announced that we were looking at the operation of the cap.33

The law would change to increase the cap by 3% for each full membership year above 20:

It brings in a new compensation cap, which essentially will be based on an enhanced level for people who have served for more than 20 years. There is a figure for the cap which can be actuarially reduced for people who take early retirement. That will be increased and we envisage this to be by 3% for each year of service beyond 20. It is very much focused on those who have relatively high pensions. We are not talking about people on very low pensions, but about people who have worked for a firm for a long period and who have expectations about their pensions. 34

The impact assessment explained that the change would increase PPF’s liabilities and thereby lead to an increase in the PPF levy:

[…] on the assumption that the costs of the higher cap will be passed on in full to levy payers, it is estimated that the present value of increased levy payments over the period to 2030 will be £139.3 million, although there are significant uncertainties around this.35

There was uncertainty about the extent of the increase because some of the costs would be otherwise absorbed:

31 Ibid, c486 32 Ibid, c487 33 PBC Deb 11 July 2013 c422-3 34 HC Deb 1 July 2013 c604; DEP 2013-1146, July 2013 ; Pensions Act 2014 - Impact Assessment,May 2014 35 Pensions Bill 2013-14 – summary of impacts (May 2014), page 35

Number CBP-03917, 30 January 2018 12

As described, the PPF is partly funded by way of a levy on schemes. We have assumed that an increase in the PPF liability will be fully reflected by an increase in the levy. However, caution should be exercised here, as when setting the levy, the Board of the PPF take into account a large range of different factors that exist at the time the levy is set (such as the risk of schemes entering the PPF, the level of funding if that event occurs, anticipated investment return) only one of which will be its liabilities. Thus, the estimated costs and benefits in this Impact Assessment are also highly sensitive to this assumption. Should investment return improve and/or the number of company insolvencies reduce, then some of these costs could be absorbed.36

There was some delay in issuing detailed proposals.37 However, on 15 September 2016, the Government launched a consultation on the draft regulations needed to insure the long service cap would operate as intended. The intention was for the PPF long service cap to be in place from April 2017. He would also consult on proposals for a similar long service cap in the FAS, to be in place from April 2018:

The FAS provides financial support for those who lost significant amounts of pension because their defined benefit occupational pension scheme collapsed underfunded. Generally the FAS helps those schemes which were affected before the introduction of the PPF and ensures a person gets at least 90 per cent of the pension due at the point the scheme collapsed. This calculation is subject to a maximum cap. It is our intention to amend this cap so that it will, like the PPF cap, increase by three per cent for each full year of pensionable service, over 20 years subject to a new maximum of twice the standard cap.

I will, in due course, be putting before Parliament regulations to implement this new cap. So that the FAS scheme manager has sufficient time to plan for these changes, it is our current intention that the FAS changes will apply from April 2018. Those already being paid assistance will get the uplift applied to their cap amount from the implementation date although, as in the PPF, this increase will not be backdated.38

The PPF “long service cap” came into force from 6 April 2017 under the Pension Protection Fund (Modification) (Amendment) Regulations 2017 (SI 2017/324).

Legal challenge

There is a legal challenge to the level of the PPF compensation cap in the European Court of Justice in the case of Grenville Hampshire (C-17/17).39 The key issue raised was:

whether Article 8 of Directive 80/987/EEC on the protection of employees in the event of the insolvency of their employer requires every employee, irrespective of the size or cost, to receive no less than 50 percent of their expected pension benefits. This is not accepted by the Board of the PPF or the Secretary of State for Work and Pensions who is an interested party in the case.40

In debate in the House of Lords, Baroness Buscombe explained the Government’s position:

[…] this legal challenge by Mr Hampshire contends that article 8 of the EU insolvency directive requires the UK to ensure that every pension scheme member gets at least 50% of their accrued benefits in the event of the insolvency of the sponsoring employer. It is possible for the capped amount of compensation or assistance to be less than 50% of the member’s accrued pension, for example where a member has a large pension due to a high salary and/or long service within the same pension scheme. However, we believe the numbers affected to be very low. Only around 400 PPF and 500 FAS members are currently affected by the cap, which represents around 0.3% of the total membership of both schemes as at April 2017. We estimate that a very small proportion of these capped

36 Pensions Bill 2013-14 – impact assessments - Annex J – The PPF compensation cap amendments (March 2013) 37 PQ 24981, 4 February 2016; See also HC Deb 7 September 2015 c19 38 HCWS163, 15 September 2016 39 Hampshire v The Board of the Pension Protection Fund [2016] EWCA Civ 786 40 Explanatory Memorandum to draft Financial Assistance Scheme (Increased Cap for Long Service) Regulations

2018, para 7.3

13 Pension Protection Fund

members are not receiving at least 50% of their accrued pension, and the increased FAS cap for long service will further reduce the number of members affected.

The Government’s concerns regarding the position for which Mr Hampshire argues relate to both the potential costs and the undermining of the principle of the cap. The impact on government, the PPF and pension schemes more generally in the event of an adverse decision would depend on the precise terms of the judgment, but the implications are likely to be significant. Even with relatively few scheme members affected, any requirement to ensure that every member of every scheme receives no less than 50% of their original scheme entitlement could, depending on the terms of the judgment and the nature of any legislative changes made in response, significantly increase the costs for both the FAS, which is funded by the taxpayer, and the PPF, which is funded via a levy on eligible pension schemes. We await judgment in the case in due course, and of course the Government will carefully consider it.41

3.3 Indexation PPF compensation payments are increased in line with prices capped at 2.5%, but only in respect of rights accrued from April 1997.42

This reflects the fact that before April 1997 there was no general obligation on occupational pension schemes to increase pensions in payment.43 The Pensions Act 1995 introduced a requirement to increase pensions in payment by the lower of the Retail Price Index (RPI) or 5%, on rights accrued since April 1997. Pensions Act 2004 reduced the cap from 5% to 2.5% for rights accrued in defined benefit schemes from 6 April 2005.44

When the Pensions Bill 2003/04 was before Parliament, the then Pensions Minister, the late Malcolm Wicks explained the Government’s view that, in principle, the PPF should not provide more generous benefits than pension schemes themselves:

The PPF is being set up to provide adequate protection for individuals who face losing some or all of their pension entitlements, not to provide a level of compensation that would attempt to match the level of scheme benefits, or even offer more. Providing indexation increases prior to 1997 could result in some members receiving a level of PPF compensation in excess of the level that would have been provided from their scheme. However, I stress that the PPF seeks to provide a consistent and meaningful level of compensation for all members eligible for fund assistance. Restricting the amount of indexation paid on PPF compensation would ensure that the PPF could do that, by being better able to predict its liabilities and plan ahead financially.45….

Providing more generous indexation arrangements would also have cost implications, of around £200 million.46 Switch to the CPI The Pensions Act 2004 originally provided for pension compensation to be increased in line with the Retail Prices Index (RPI).47 In July 2010, the Government announced its intention to switch from the RPI to the CPI for determining increases in occupational pensions and PPF and FAS compensation payments. The reason was that:

41 HL Deb 22 January 2018 c893-4 42 Pensions Act 2004, Sch 7, para 28 43 IDS Pension Service, Pension scheme design, March 2006, para 3.37 44 Section 278 and Commencement Order No 2, SI 2005/275 45 SC Deb, 30 March 2004, c512 46 Ibid, c513 47 Pensions Act 2004, s Sch 7, para 28

Number CBP-03917, 30 January 2018 14

The Government believe the CPI provides a more appropriate measure of pension recipients' inflation experiences and is also consistent with the measure of inflation used by the Bank of England.48

This was provided for in Pensions Act 2011 (s20).49 When this provision was before Parliament, the then Pensions Minister, Steve Webb, explained that the PPF was “essentially, a safety scheme”, not intended to provide exactly what the scheme would have provided. The impact would “vary hugely between individuals.”50

3.4 Early payment Individuals can chose to draw PPF compensation before normal pension age. However, they must be at least 55 and payment levels are actuarially reduced to take account of the fact that compensation will be in payment for longer.51 This is the case even where a person claims their pension early on ill-health grounds. In this respect, the PPF rules differ from those of many DB schemes, which often allow unreduced early payment of a pension on ill-health grounds. 52

The issue was also discussed when the Pensions Bill 2006-07 was before Parliament. Labour Peer, Lord Whitty tabled an amendment with the intention of allowing early payment of unreduced PPF or Financial Assistance Scheme (FAS) compensation on grounds of ill-health.53 Responding for the Labour Government, Lord McKenzie said he appreciated the difficult choices faced by people unable to work on grounds of ill-health and that many pension schemes offered different options for people retiring early due to ill-health. However, the fact that the PPF and FAS rules did not mirror those of individual pension schemes helped to ensure certainty about the level of payment and about the affordability of the schemes:

The Government deliberately created the PPF as a compensation scheme that would provide a better level of income overall than did schemes that were underfunded when they were wound up. Without the PPF, people who are taken ill or seriously disabled might have no pension at all to look forward to. We have taken care to ensure fairness and to avoid the trap of complexity that would result from creating a PPF that mirrored all the rules of every pension scheme. This means that we have made no special provision for people to receive compensation early specifically on the grounds of ill health. Instead, we have provided for people to apply for early compensation, subject to the adjustment, without having to explain why they wish to receive it. If we were to do as the amendment suggests, we would need to provide a mechanism for the PPF to determine when someone was suffering from severe ill health. Such matters are not always easy to determine.54

The Government amended the 2004 Act to allow members of the PPF who are terminally ill to claim a lump sum, bringing this into line with the practice of the FAS.55 Lord McKenzie explained that:

These amendments will allow those who have a progressive disease—which means that their death may reasonably be expected in six months—to apply for a lump sum. This lump sum will be equal to twice the annual rate of compensation that they would be entitled to had they reached normal pension age, in lieu of their future entitlement. Taken together, these amendments will ensure that a member with a terminal illness will be able to access a significant lump sum, averaging in the region of £10,000, using the same rules to define

48 HC Deb 8 July 2010 c15WS 49 Pensions Act 2011 (s20) 50 PBC Deb, 14 July 2011 (afternoon), c317-8 51 Pensions Act 2004, Schedule 7, para 25 and Pension Protection Fund (Compensation) Regulations, (SI 2005. No

670), reg 2 52 HC Deb, 21 November 2005, c1079W; IDS Pension Service, Pension Scheme Design 2007, page 46 53 HL Deb, 6 June 2007, c1218-20; The Financial Assistance Scheme was set up to provide some compensation to

schemes that started to wind up before the PPF came into force in April 2005 54 Ibid, c1220 55 Schedule 7, Pensions Act 2004 as amended by the Schedule 8, Pensions Act 2008; HL Deb, 3 June 2008, c83-4

15 Pension Protection Fund

“terminally ill” as those that are used in the financial assistance scheme and in DWP benefits.56

3.5 Lump sum payment in cases of terminal illness In 2008, the Labour Government amended the 2004 Act to allow members of the PPF who are terminally ill to claim a lump sum, bringing this into line with the practice of the FAS.57[1]

Work and Pensions Minister, Lord McKenzie explained that:

These amendments will allow those who have a progressive disease—which means that their death may reasonably be expected in six months—to apply for a lump sum. This lump sum will be equal to twice the annual rate of compensation that they would be entitled to had they reached normal pension age, in lieu of their future entitlement. Taken together, these amendments will ensure that a member with a terminal illness will be able to access a significant lump sum, averaging in the region of £10,000, using the same rules to define “terminally ill” as those that are used in the financial assistance scheme and in DWP benefits.58[2]

Information for scheme members is in PPF leaflet Terminal Ill-health pension benefits.

56 HL Deb, 14 July 2008, c1060; See Pensions Act 2008, Schedule 8 57 Pensions Act 2004, sch 7 as amended by Pensions Act 2008, sch 8; HL Deb, 3 June 2008, c83-4 58 HL Deb, 14 July 2008, c1060; [2] See Pensions Act 2008, Schedule 8

Number CBP-03917, 30 January 2018 16

4. Funding The PPF is funded by a combination of:

• The assets transferred from schemes for which it has assumed responsibility; • Recoveries of money, and other assets, from those schemes’ insolvent employers; • An annual levy raised from eligible pension schemes; and • Investment returns on assets held by the PPF.59

4.1 The pension protection levy Structure The pension protection levy is comprised of a risk-based levy (required by law to be at least 80 per cent of the total) and a scheme-based levy, making up the remainder.60 The PPF explains that:

The pension protection levy is one of the ways that the PPF funds the compensation payable to members of schemes that transfer to the Pension Protection Fund (PPF).

It is payable by all UK defined benefit (final salary) pension schemes whose members would be eligible for PPF compensation if the scheme employer(s) becomes insolvent and there are not enough assets remaining in the scheme to pay benefits at PPF levels of compensation. In some circumstances, though, some schemes may qualify for a levy waiver.

The pension protection levy is divided into two parts:

The scheme-based levy (SBL) is based on a scheme’s liabilities to members on a section 179 basis. This cannot make up more than 20 per cent of the total we aim to collect.

The risk-based levy takes account of the risk of a scheme’s sponsoring employer becoming insolvent (insolvency risk) and the amount of compensation that might then be payable by the PPF (underfunding risk).

It has to make up at least 80 per cent of the total we aim to collect, though some schemes with very low levels of risk may not have to pay the risk-based levy. Schemes can reduce the risk-based levy by certifying contingent assets and deficit reduction contributions. The risk-based levy also reflects asset-backed contributions (ABCs) certified by schemes.61

There is also a more technical explanation of how the levy works.

Process for setting the levy The Secretary of State is required to set a “levy ceiling” each year, preventing the Board from raising the levy above a set maximum. It is set at a level that “is sufficient to allow the Board of the PPF to raise a levy that ensures the safe funding of the compensation it provides, whilst providing reassurance to business that the levy will not be above a certain amount in any one year.”62 The ceiling is increased each year in line with earnings. It can be increase by more than this, but only if the Board makes a recommendation to that effect and the Treasury approves.63

59 PPF, ‘Consultation on the Future Development of the Pension Protection Levy’, November 2008, para 2.1.3;

Pensions Act 2004, s177-181 60 Pensions Act 2004, s175; Explanatory Memorandum to SI 2016/82, para 7.5 61 Pension Protection Fund Levy – About the Levy 62 Explanatory Memorandum to SI 2016/82, para 7.5 63 Pensions Act 2004, s178; Pensions Act 2004 – Explanatory Notes, para 651-653

17 Pension Protection Fund

The amount of the levy ceiling for the financial year beginning on 1 April 2018 is £1,024,372,330.64

Operating within the limits Parliament has set, the PPF sets the rules for calculating the levy and estimates how much it will try to collect. It explained how this worked in evidence to the Work and Pensions Select Committee in May 2016: 65

Each year the PPF must publish an estimate for next year’s collection – for 2016/17 this is £615m (compared to £635m in 2015/16 and £695m in 2014/15 reflecting changes in risk). Parliament has set an upper limit to the levy that the PPF could seek to collect; in 2016/17 this is £981.7m. The estimate is set on the basis of the amount we aim to collect given the risks we face and the individual position of the schemes we protect. The PPF annually publishes the rules by which the levy is calculated; the PPF aims for stability and predictability in levy bills and therefore the intention is that the rules remain broadly unchanged for three year periods (the latest runs from 2015/16 to 2017/18). Actual collection will vary from the estimate to an extent, as the data on which the levy is charged is not fully available at the point the estimate is made. Schemes can also take steps to reduce their risk which will reduce their levy bill. While the levy is not set in relation to any particular sets of claims, the below is illustrative of how the levy has remained broadly stable in a volatile claims environment.

The chart below shows how our modelling anticipates that, while there is clearly uncertainty, our levy is likely to fall over time as a percentage of pension scheme liabilities.

64 Pension Protection Fund and Occupational Pension Schemes (Levy Ceiling and Compensation Cap) Order 2018 (SI

2018/39) 65 Explanatory Memorandum to SI 2018/39 para 7.7

Number CBP-03917, 30 January 2018 18

Once it has set its levy estimate, the PPF uses a “levy scaling factor” to distribute the levy proportionately among eligible schemes.66 Its evidence to the Work and Pensions Committee explained:

The funding position of each scheme is assessed using a standard valuation that schemes have to produce every three years. This is then rolled forward to a common date of the start of each levy year (the same data is used to produce our regular review of pension scheme funding). The funding position of the scheme is then ‘stressed’ to reflect that a claim on the PPF might arise when investments have performed poorly; different types of asset are stressed in different ways. The levy billed in 2015/16 used a new model to assess insolvency risk. The new model has been developed by the PPF with Experian and with input from the pensions industry and those with a wider interest. It is a statistical model based on company financial data and experience of insolvency amongst sponsors of eligible pension schemes. It is substantially more predictive than similar commercial models. It takes financial information for each of the employers which sponsor a pension scheme, uses a formula applied across different types of employer and provides a one year probability of how likely that company is to become insolvent. These probabilities are tracked on a monthly basis, and the average of the twelve probabilities used to place the employer in a band. This band is then used in the levy calculation. The individual levy bill of a particular scheme may therefore vary substantially year on year if their funding level or employer strength varies significantly. Employers, and related companies, can provide guarantees and pledges on assets to a scheme, which in turn reduce their risk of making claims, and is therefore reflected in a reduced levy bill. The individual levy bill payable by any scheme is capped at 0.75 per cent of the scheme’s PPF liabilities. The costs of this cross subsidy reflected by this cap is met through the scheme based levy payable by all schemes.67

There is a process for challenging decisions - see Reviews and Appeals.

Levy estimate for 2018

In its 2017 Report on Defined Benefit pension schemes, the Work and Pensions Select Committee said it supported the risk-based levy but that it was important that it did not increase insolvency by imposing disproportionate costs on schemes:

We are particularly concerned that some groups of employers without access to expensive professional advice, or with atypical business models, may be disadvantaged by the current levy calculations. A risk-based levy is only fair if it accurately reflects risk. We recommend that, as part of its forthcoming review of its levy rules, for the three years to 2018-19, the PPF examines the effect of the levy framework on particular types of employer, including mutual societies and SMEs. It should rectify or otherwise adjust for any anomalies which adversely affect such groups.68

It raised a particular issue affecting employers in the mutual sector. This was that ‘mortgage age data’ used in the calculation of insolvency risk, and collected from Companies House, is not available for mutuals. Such companies are instead given a “neutral” mortgage age risk score by the PPF, effectively increasing their levy.69

66 PPF, The Pension Protection Levy. Policy 2008-09 to 2010-11 67 Ibid 68 Work and Pensions Select Committee, Defined Benefit pension schemes, December 2016, para 80 69 Ibid, para 78

19 Pension Protection Fund

In response, the PPF said it was consulting on proposals to improve “predictiveness” and to ensure scorecards were better tailored to company size “resulting for example, in SMEs and not-for-profits paying levies that better reflect their risks.70 The Committee welcomed this:

The removal of mortgage age from the PPF’s new formula is good news for those mutuals who have been disadvantaged by levy calculations. We are pleased that the PPF has responded to the Committee’s recommendations and, more importantly, the evidence we heard from the sector71

In its 2018/18 Levy Policy Statement, the PPF set the framework for the levy for 2019/20 and 2020/21:

We take a long-term view of risk and set the levy rules accordingly, aiming to keep the rules stable for three years. Even in these uncertain times, our funding strategy remains robust and able to withstand the claims we face. Accordingly, we can confirm that the Levy Scaling Factor for 2018/19 will be 0.48 and the Levy Estimate £550 million, over 10 per cent lower than the 2017/18 figure.72

It had developed its approach to assessing the risk of employer insolvency by better assessing the risk of rated entities and SMEs.73 Its changes overall were expected to result in:

• Around three-fifths of schemes having a lower bill than if existing rules had been used; • Small and medium sized employers seeing a significant reduction in levy, in aggregate

paying one-third less in levy; • Not-for-profit entities and companies with published credit ratings paying less; and • Schemes with employers on scorecard 1 (the non-subsidiaries and large subsidiaries

scorecard) being the most likely to see an increase in levy, with around one in three seeing an increase in levy and average increases across the scorecard of 45%.74

Actions schemes can take to reduce their levy

Pension schemes and employers can reduce the amount of levy they pay:

Schemes can reduce the amount of levy they pay by putting in place contingent assets, such as parent or bank guarantees, or security over property. The PPF also considers deficit reduction contributions – special contributions to bolster the scheme – as reducing the risk of the scheme, which also reduces the amount of the levy bill.75

A leaflet produced jointly by the Pension Protection Fund and the CBI – How to reduce your pension protection levy – lists ten actions they can take. There is a levy waiver for schemes that pose very little risk to the PPF.76

Consultation on whether the levy framework could incentivise good governance

The Work and Pensions Committee also recommended that the levy framework should be re-examined to see how it could incentivise schemes to improve governance. The PPF agreed governance was “of critical importance to delivering positive outcomes for pension scheme members”. It had concluded in 2010 that there were “significant barriers” to trying to use the levy to incentivise improvements. However, it was keen to hear if stakeholders thought there

70 Letter from PPF to Work and Pensions Select Committee, 29 March 2017 71 PPF response to defined pensions report welcomed by Committee, March 2017 72 PPF, The 2018/19 Levy Policy Statement, December 2017 73 Ibid 74 ‘PPF cuts total levy target for 2018/19 and consults on plans to amend detailed scorecards’, Occupational

Pensions, Issue 366, November 2017 75 PPF and CBI, How to reduce your pension protection levy 76 PPF website/FAQ/what is a levy waiver?; Pension Protection Fund (Waiver of Pension Protection Levy and

Consequential Amendments) Regulations 2007 (SI 771/2007)

Number CBP-03917, 30 January 2018 20

was now a case for incorporating a discount for good governance in the levy calculation.77 It asked for views on how it could measure good governance in a way that is linked to reduction in risk:

11.2.19 The risk-based levy seeks to assess the risks posed by schemes to the PPF and we are constrained by legislation in terms of what can be taken into account. Good governance itself is not currently one of the factors set out in legislation on which the PPF is able to base the rules for the risk based levy. As a result, in order to provide any recognition for good governance in the levy we would need to have clear evidence that it contributes to one of the risk factors already set out in legislation. Specifically we would need to be able to show that good governance led to:

1. a demonstrable reduction in scheme sponsors’ insolvency risk,

2. a reduction in the size of the funding shortfall in the event of an employer insolvency event; or

3. a reduction in the risks associated with the nature of a scheme’s investments when compared with the nature of its liabilities.

11.2.20 If good governance cannot be said to fit into one of the above categories, a new factor for setting the levy would require legislation before we could incorporate it into our levy framework.

11.2.21 We are therefore seeking stakeholder suggestions as to how we could measure good governance that is linked to a reduction in risk in such a way and

• does not create unintended incentives, i.e. avoids encouraging a tick box approach but focusses on behaviours that make a substantive difference;

• does not create administrative burdens for schemes to prove they are meeting required standards and is easy to administer/verify, or

• is not so widely available that it does not differentiate between schemes with different governance standards (ie, if the majority of schemes qualify for a discount it would be counteracted by an increased levy scaling factor to ensure the required levy estimate is raised).78

In September 2017, it said it would not take forward proposals for a levy discount to reward good governance. Two thirds of respondents to its consultation had expressed doubts about either the principle or the practical difficulty of doing so:

7.1.4 A number of responses noted that good governance was likely to have positive effects on the risk that schemes pose – for example, through the positive impact that governance can have on investment decision making. However, it was argued that it was not practical to disentangle the influence of governance from other factors that influence the funding risk of schemes or insolvency risk of their sponsors. As a result, stakeholders argued, it wasn’t possible to demonstrate the individual contribution of governance.

7.1.5 A second concern was that, in principle, the positive effects of governance might already be being captured. Again, the example of the positive impact that governance can have on investment decision making was cited and that, over time, this could be expected to be reflected in improved scheme funding or decreased risk; each of which could be expected to reduce the levy directly. In these stakeholders’ views, there would be a sense of “double counting” in reflecting good governance.

7.1.6 A third challenge was to suggest, to the extent that a robust justification in risk terms was not available; allowance in the levy reflected an encouragement to good behaviour, and that regulatory activity – of the kind seen in recent years - was more appropriate than a pricing mechanism, such as the levy, which was likely to be a blunt instrument. […]

77 Letter from PPF to Work and Pensions Select Committee, 29 March 2017 78 PPF, Third Triennium Consultation Document, 23 March 2017

21 Pension Protection Fund

7.1.8 Finally, there was a concern that a good governance discount would predominantly benefit larger schemes as it might positively view those schemes with more sophisticated investment strategies, within more regulated sectors or with the required resources to evidence adherence to good/practice. In doing so it would run counter the desire to ensure that SMEs were not disadvantaged by the Levy Rules.79

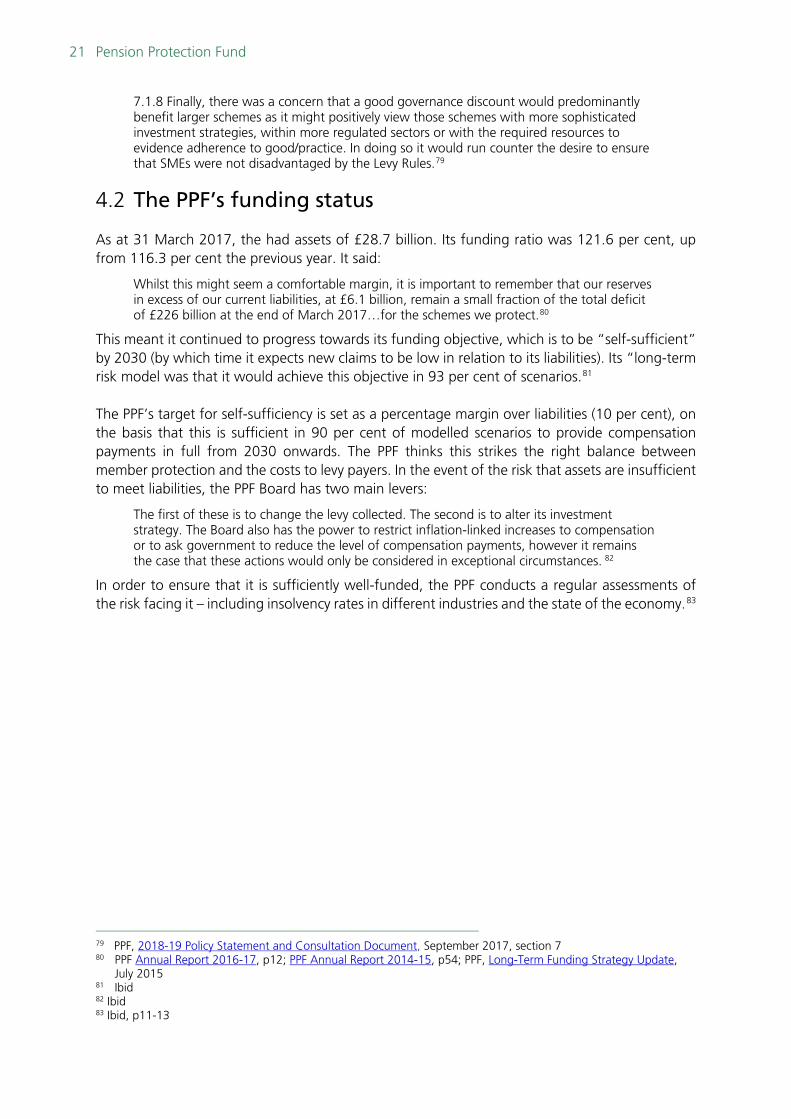

4.2 The PPF’s funding status As at 31 March 2017, the had assets of £28.7 billion. Its funding ratio was 121.6 per cent, up from 116.3 per cent the previous year. It said:

Whilst this might seem a comfortable margin, it is important to remember that our reserves in excess of our current liabilities, at £6.1 billion, remain a small fraction of the total deficit of £226 billion at the end of March 2017…for the schemes we protect.80

This meant it continued to progress towards its funding objective, which is to be “self-sufficient” by 2030 (by which time it expects new claims to be low in relation to its liabilities). Its “long-term risk model was that it would achieve this objective in 93 per cent of scenarios.81 The PPF’s target for self-sufficiency is set as a percentage margin over liabilities (10 per cent), on the basis that this is sufficient in 90 per cent of modelled scenarios to provide compensation payments in full from 2030 onwards. The PPF thinks this strikes the right balance between member protection and the costs to levy payers. In the event of the risk that assets are insufficient to meet liabilities, the PPF Board has two main levers:

The first of these is to change the levy collected. The second is to alter its investment strategy. The Board also has the power to restrict inflation-linked increases to compensation or to ask government to reduce the level of compensation payments, however it remains the case that these actions would only be considered in exceptional circumstances. 82

In order to ensure that it is sufficiently well-funded, the PPF conducts a regular assessments of the risk facing it – including insolvency rates in different industries and the state of the economy.83

79 PPF, 2018-19 Policy Statement and Consultation Document, September 2017, section 7 80 PPF Annual Report 2016-17, p12; PPF Annual Report 2014-15, p54; PPF, Long-Term Funding Strategy Update,

July 2015 81 Ibid 82 Ibid 83 Ibid, p11-13

Number CBP-03917, 30 January 2018 22

5. The Financial Assistance Scheme The Financial Assistance Scheme (FAS) was set up under the Pensions Act 2004 to provide compensation to members of occupational pension schemes that wound up on the insolvency of the employer between 1 January 1997 and 6 April 2005 – ie. people not eligible for the Pension Protection Fund (PPF) which was set up for schemes that wound up underfunded from 6 April 20015.84

The PPF took over responsibility for administering the FAS from 2009. The FAS closed to new applications in September 2016.154,000 members of 1,000 schemes are now covered by it. The deadline for applications was 10 years later than originally intended. The deadline was “extensively communicated and no further potentially FAS-eligible schemes have contacted [the PPF] since.” 85 Unlike the PPF, which is funded by a levy on occupational pension schemes, the FAS is funded by the tax payer and the asset of schemes it has taken over.86

The FAS does not generally provide a complete replacement of an individual’s lost pension. People generally receive 90 per cent of the expected pension (the pension accrued at the point the scheme began to wind up) subject to a cap. For the year 2017-18, the cap is £34,229.87

The purpose of the cap was to limit costs and prevent moral hazard (i.e. deter excessive risk taking and malpractice by scheme administrators and trustees whereby decisions can be taken that result in insolvency of the company, in the knowledge that their pension benefits would in effect be insurance by the FAS.)88 However, the Government recognised that it had a disproportionate effect on individuals with long service in an individual pension scheme. To address this, it decided to modify the cap for people with long service.

In September 2016, the Government said it would consult on a long service cap for the FAS, to be in place from April 2018:

The FAS provides financial support for those who lost significant amounts of pension because their defined benefit occupational pension scheme collapsed underfunded. Generally the FAS helps those schemes which were affected before the introduction of the PPF and ensures a person gets at least 90 per cent of the pension due at the point the scheme collapsed. This calculation is subject to a maximum cap. It is our intention to amend this cap so that it will, like the PPF cap, increase by three per cent for each full year of pensionable service, over 20 years subject to a new maximum of twice the standard cap.

I will, in due course, be putting before Parliament regulations to implement this new cap. So that the FAS scheme manager has sufficient time to plan for these changes, it is our current intention that the FAS changes will apply from April 2018. Those already being paid assistance will get the uplift applied to their cap amount from the implementation date although, as in the PPF, this increase will not be backdated.89

It consulted on Applying the Financial Assistance Scheme increased cap for long service in September 2017 and responded to that consultation in December.

Draft regulations were then introduced to Parliament and debated in the House of Lords on 22 January 2018. Work and Pensions Minister Baroness Buscombe explained that the cap on FAS compensation helped to “limit the costs of the Financial Assistance Scheme, which is funded by

84 For more on the background, see Library Briefing Paper CBP 3085 Financial Assistance Scheme – 2008 (2010) 85 Pension Protection Fund Annual Report 2017, p12 86 HL Deb 22 January 2018 c884 and 889 87 Explanatory Memorandum to draft Financial Assistance Scheme (Increased Cap for Long Service) Regulations

2018, para 7.3 88 Ibid para 7.4 89 HCWS163, 15 September 2016

23 Pension Protection Fund

general taxation.” However, it had an impact on people who had “worked for a significant proportion of their working life to build up a pension with their employer and, consequently, may have little or no other private pension savings to offset against the shortfall between the capped assistance and what they had expected from the scheme.” The change in the draft regulations would help that group:

The provisions increase the cap by 3% for each full year of pensionable service over 20 years, subject to a new maximum of double the standard Financial Assistance Scheme cap. The new provisions will ensure that Financial Assistance Scheme members with long service will receive assistance which reflects a higher proportion of their accrued pension benefits.

It is estimated that 290 FAS members will benefit from the introduction of the regulations over the lifetime of the Financial Assistance Scheme. Although that is not many people, it is a significant proportion of the 500 people estimated to be affected by the cap. The change is expected to be widely welcomed by Financial Assistance Scheme members with long service, and their families.90

The Minister said the change would increase the overall cost of FAS payments by approximately £1.2 million per year in the first eight years, before starting to slowly decrease in following years. Unlike the PPF, which was funded by a levy on schemes, the FAS is funded by general taxation. There would also be administrative costs of some £400,000 (lower than the estimated figure in the Explanatory Memorandum):

While the costs may seem high for the benefit of relatively few scheme members, there is a great deal of work to do to go back through records and identify the relevant members and their data. We believe the cost is justified because the long service cap is the right thing to do.91

Shadow Work and Pensions Minister Lord McKenzie welcomed the change and described the FAS as a “worthy example of the state stepping in to support failures of private pension provision.”92 He asked about:

• why the cap increased by 3% for each year of service after 20; and

• the legal challenge in the European Court.93

• He also asked about the impact of the collapse of Carillion on the PPF:

It is to be welcomed that the PPF is in robust health, with, I think, £4.1 billion in reserve, but there is obviously a limit to the strain it can take.94

• The Minister responded that:

• The increase in compensation would take effect from the first payday on or after the regulations coming into force (currently 6 April 2018);

• Three per cent was chosen as the ‘escalation amount’ on basis that it was “sufficient to lift a substantial number of the target group out of the compensation cap entirely, while still being affordable for taxpayer. Lower percentages did not achieve this outcome.”

• Regarding the legal challenge, a date had been set for a hearing in the European Court of Justice on 8 March 2018. She explained:

90 HL Deb 22 January 2018 c884; Financial Assistance Scheme (Increased Cap for Long Service) Regulations 2018 91 Ibid 92 HL Deb 22 January 2018 c887 93 Ibid 94 Ibid

BRIEFING PAPER Number CBP-03917, 30 January 2018

About the Library The House of Commons Library research service provides MPs and their staff with the impartial briefing and evidence base they need to do their work in scrutinising Government, proposing legislation, and supporting constituents.

As well as providing MPs with a confidential service we publish open briefing papers, which are available on the Parliament website.

Every effort is made to ensure that the information contained in these publically available research briefings is correct at the time of publication. Readers should be aware however that briefings are not necessarily updated or otherwise amended to reflect subsequent changes.

If you have any comments on our briefings please email [email protected]. Authors are available to discuss the content of this briefing only with Members and their staff.

If you have any general questions about the work of the House of Commons you can email [email protected].

Disclaimer This information is provided to Members of Parliament in support of their parliamentary duties. It is a general briefing only and should not be relied on as a substitute for specific advice. The House of Commons or the author(s) shall not be liable for any errors or omissions, or for any loss or damage of any kind arising from its use, and may remove, vary or amend any information at any time without prior notice.

The House of Commons accepts no responsibility for any references or links to, or the content of, information maintained by third parties. This information is provided subject to the conditions of the Open Parliament Licence.