Pension Auto Enrolment - Employers guide

16

Workplace pensions reforms Preparing for Auto-enrolment Employee Benefits

Transcript of Pension Auto Enrolment - Employers guide

Workplace pensions reforms Preparing for Auto-enrolment

Employee Benefits

2 Preparing for Auto-enrolment

Will our business need to comply with the automatic enrolment requirements and, if so, when?

Yes, the new “employer duties” will apply to

all UK employers, irrespective of how few or

how many employees they have. However, the

effective date for compliance is being phased

in between 1st October 2012 and 1st February

2018, with the earlier dates applying to larger

employers. A sample of the “staging dates” is

given below:

You can choose to bring forward your staging

date, but you must inform The Pensions

Regulator of your intention to do so and be able

to demonstrate your ability to discharge the

new duties.

What is meant by “automatic enrolment”?

This means that an employee must be admitted

to membership of a “Qualifying Scheme”

automatically, without the need to complete

any forms or obtain anyone’s permission. This

must happen no later than three months after

becoming an “Eligible Jobholder”. Until now, the

majority of UK pension schemes have operated

on the basis of employees opting in to a pension

scheme, often after meeting some eligibility

criteria determined by the employer. In future,

the default position will be that employees must

be included in the pension scheme unless they

opt out.

Which of our employees will need to be

included?

The requirement to be automatically enrolled

into a Qualifying Scheme will apply to all

“Eligible Jobholders” in the UK, aged between 22

and State Pension Age, providing that they earn

above a minimum earnings trigger, expected to

be set in line with the income tax threshold each

year. Those outside these age limits or on lower

earnings will be able to opt in.

If an employee opts out, is that the end of our duties as an employer to him/her?

No, where an employee opts out of the

employer’s chosen pension scheme, he/she may

opt back in at any time and the employer must

then pay the appropriate level of contributions.

Furthermore, there is a duty on employers to

automatically re-enrol any employees that

have opted out previously, at each three year

anniversary of the original staging date (the

employee can opt out again each time).

What level of contributions must be paid?

Once the full provisions are in place, the

combined employer and employee contributions

must be equivalent to at least 8% of the

employee’s “Qualifying Earnings”. The employer’s

contribution, within the 8% total, must be at

least 3% of Qualifying Earnings and the employee

makes up the difference (with tax relief included).

For 2013/2014, qualifying earnings will be an

employee’s earnings between £5,668 and

£41,450. These figures are expected to be

reviewed annually.

Between October 2012 and September 2017, the

minimum required contribution rates will be just

1% each for the employer and employee. Then,

from October 2017 the employer must pay at

least 2% included in a total of 5%, before the

full contributions take effect in October 2018.

Employers who use a Defined Benefit (Final

Salary) scheme to meet the new requirements

can defer their automatic enrolment date until

the end of the staging period (October 2017),

although employees can opt in before then.

If the scheme is closed before October 2017,

contributions must be backdated to the original

staging date.

Can we offer our employees an alternative cash sum or other benefit

instead?

No. You must make arrangements for the

payment of pension contributions at the

prescribed rates and must not offer any

inducement or incentive which may be seen as

encouraging employees to opt out. Employers

operating flexible benefit schemes may need

to pay particular attention to their existing

arrangements, to ensure that the minimum

pension requirements are met.

I’ve heard of NEST in connection with the new pension regime, but what is NEST and will this be useful to our business?

NEST is the National Employment Savings Trust,

a centralised, defined contribution occupational

pension scheme, which may be used by

employers to meet their new duties in relation

Number of employees Staging date

10,000 - 19,999 1 March 2013

6,000 - 9,999 1 April 2013

4,000 - 5,999 May/June 2013

3,000 - 3,999 1 July 2013

1,250 - 2,999 Aug/Sept 2013

800 - 1,249 1 October 2013

500 - 799 1 November 2013

350 - 499 1 January 2014

250 - 349 1 February 2014

50 - 249 1 April 2014 - 1 April 2015

Less than 50 1 June 2015 - 1 April 2017

New employees Up to Feb 2018

You will have heard about Workplace Pensions Reform and the requirement to automatically enrol

employees into a workplace pension scheme. From 1 October 2012, this became a reality for the UK’s largest

employers. Below, we provide a brief update on the key features that will soon be part of the daily lives of

anyone involved in the administration of pension schemes for employees.

Connect to rsmtenon.com 3

to some or all of their employees. Although it is

available to all companies, it is primarily aimed

at low to moderate earners and their employers.

In the build up to the automatic enrolment,

several new pensions schemes have been

launched in direct competition to NEST.

Is NEST just like any other defined contribution company pension scheme?

In many ways, yes, although it will have a limit

on contributions that can be paid and, at least

for the first five years of its operation, it is not

expected to allow transfers of funds in or out.

There are also some differences in relation

to benefit options for those who leave after a

short period of membership and, in the event

of a member’s death before retirement, the

benefits will not be exempt from Inheritance Tax

(although this is not expected to be a concern

for the target membership).

Will there be an upper limit on the contributions an employer must pay?

Yes, there will be a maximum contribution

an employer must pay on behalf of any one

employee, which will be determined by the

upper limit on Qualifying Earnings. That said,

an employer can pay significantly higher

contributions if it wishes to do so, and many

senior employees and directors will already

be enjoying significant, tax-efficient pension

rewards.

Note that there will be a maximum contribution

that can be paid to NEST by and on behalf of

each employee. For the 2013/14 tax year this is

£4,400 p.a.

4 Preparing for Auto-enrolment

Can we make use of our existing company pension scheme?

Yes, an existing scheme can be used for

automatic enrolment, providing it meets certain

standards. A combination of two or more

different schemes, including NEST, may be used

to meet the requirements.

Broadly, a Defined Benefit (Final Salary) scheme

will be qualifying if it is made available to all

Eligible Jobholders and if it is either contracted

out of the State Second Pension (S2P, formerly

SERPS) or offers a pension accrual rate of

at least 1/120th for each year of Pensionable

Service.

A Defined Contribution (Money Purchase)

scheme must meet the minimum contribution

requirements as explained above i.e. a minimum

total contribution of 8% of “Qualifying Earnings”

with at least 3% being paid by the employer.

What if we do not currently have a pension scheme for all employees?

In the circumstances where a suitable pension

scheme is not already in place, options will

include joining NEST; changing the eligibility

terms of any existing scheme or setting up a

new scheme for those employees who would

otherwise be excluded.

What happens if we do nothing?

The Pensions Regulator (TPR) will be responsible

for ensuring that employers meet their

obligations in relation to Workplace Pensions

Reform. Although TPR’s approach will be to

educate and encourage compliance, persistent

offenders could face substantial fines or even

imprisonment.

Apart from paying the contributions, is there anything else we need to do?

The Pensions Act 2008 places certain duties on

employers in respect of communications and

record keeping. A formal statement must be

issued to each Eligible Jobholder on or before

joining, including, amongst other things, full

details of the proposed scheme; the effective

date of joining and informing them of their right

to opt out. The employer must also maintain

records of any opt-outs and submit an annual

return to The Pensions Regulator.

Where can we get advice on exactly how all this affects our business?

There is generic information on the websites

of The Pensions Regulator, the Department for

Work and Pensions and NEST Corporation, but

many employers will need detailed advice on

what the new “employer duties” mean to their

business and, perhaps more importantly, how to

ensure that they meet these obligations in the

most appropriate and cost effective way.

Employers will have different duties depending on the type of worker. Employers will need to identify each type of worker and perform the relevant duties for each type.

Connect to rsmtenon.com 5

Guidance notes

Since October 2012, any UK employer who employs at least one person will be legally obliged to:

nSet up and register a pension scheme

suitable for automatic enrolment

nAutomatically enrol certain workers (known

as eligible jobholders) into that pension

scheme

nArrange membership of a pension scheme

for certain other workers

nMake contributions for eligible jobholders

and certain other workers

nManage the automatic enrolment, joining

and opt out processes

nProvide specific information to workers,

pension scheme providers and The Pensions

Regulator (TPR)

nKeep records of how they have fulfilled and

continue to fulfil their duties

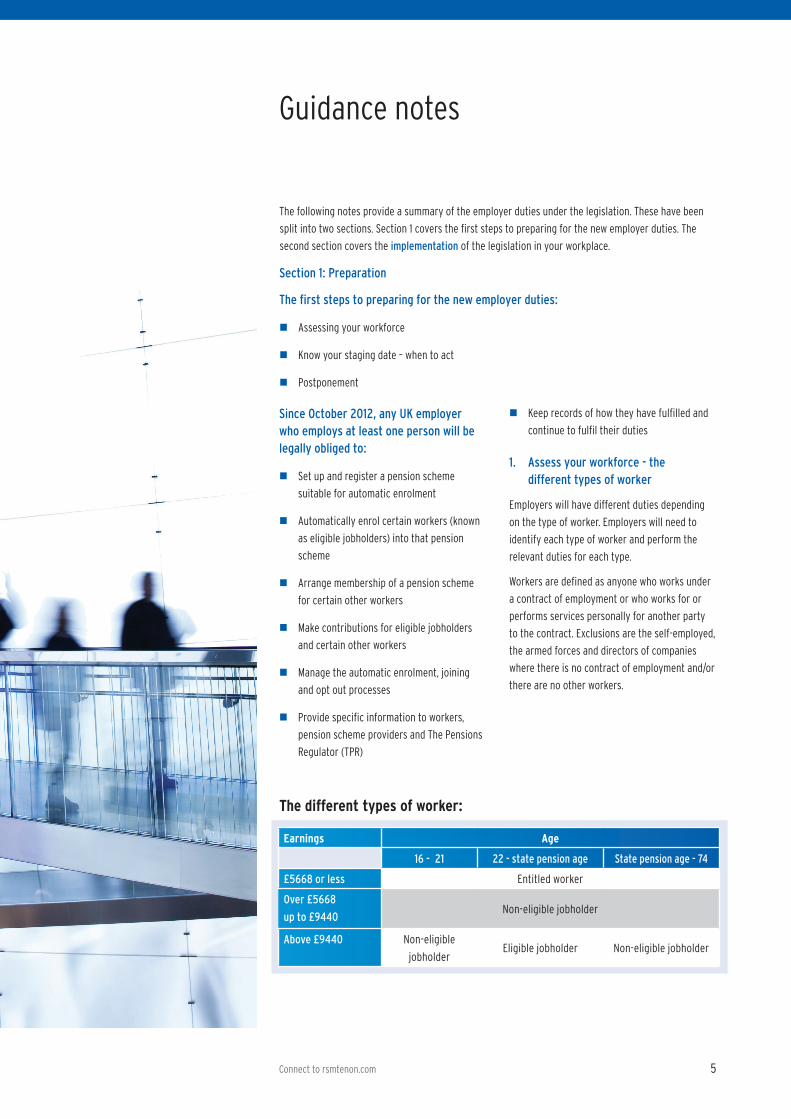

1. Assess your workforce - the different types of worker

Employers will have different duties depending

on the type of worker. Employers will need to

identify each type of worker and perform the

relevant duties for each type.

Workers are defined as anyone who works under

a contract of employment or who works for or

performs services personally for another party

to the contract. Exclusions are the self-employed,

the armed forces and directors of companies

where there is no contract of employment and/or

there are no other workers.

Earnings Age

16 - 21 22 - state pension age State pension age - 74

£5668 or less Entitled worker

Over £5668

up to £9440Non-eligible jobholder

Above £9440 Non-eligible

jobholderEligible jobholder Non-eligible jobholder

The following notes provide a summary of the employer duties under the legislation. These have been

split into two sections. Section 1 covers the first steps to preparing for the new employer duties. The

second section covers the implementation of the legislation in your workplace.

Section 1: Preparation

The first steps to preparing for the new employer duties:

n Assessing your workforce

n Know your staging date – when to act

n Postponement

The different types of worker:

6 Preparing for Auto-enrolment

Connect to rsmtenon.com 7

2. Know your staging date –

when to act?

The employer duties will be introduced in stages

from October 2012 and also larger employers will

have their duties imposed first, smaller employers

last. TPR will generally determine the size of the

employer based on the Pay as You Earn (PAYE)

scheme information available to them on 1 April

2012. Any fluctuation in the number of people

in the PAYE scheme after that date will not

change the staging date, although if employers

merge after 1 April 2012 the staging date will be

determined by the largest PAYE scheme of the

merged employers.

It is possible to bring forward a staging date to

align it with other key dates in an operational

calendar but once a change has been notified

to the Pensions Regulator this will be officially

recognised as the date from which an Employer

must comply with the new duties. Note that it is

not possible to delay the staging date.

3. Postponement

Employers may postpone the assessment of

worker type for up to three months. There are four

possible types of notice that an Employer could

issue to advise workers of the postponement of

the auto enrolment process.

nGeneral notice A – contains the information

that must be provided to all the different

categories of worker. General notice A is

issued to any worker irrespective of worker

category and whether or not they are a

member of a qualifying scheme with that

employer

nGeneral notice B – the same as general

notice A but excluding the information

for jobholders who are active members of

a qualifying scheme with that employer.

General notice B is only issued to a worker

or workers who are not active members of a

qualifying scheme with that employer

Eligible jobholder Non eligible jobholder Entitled worker

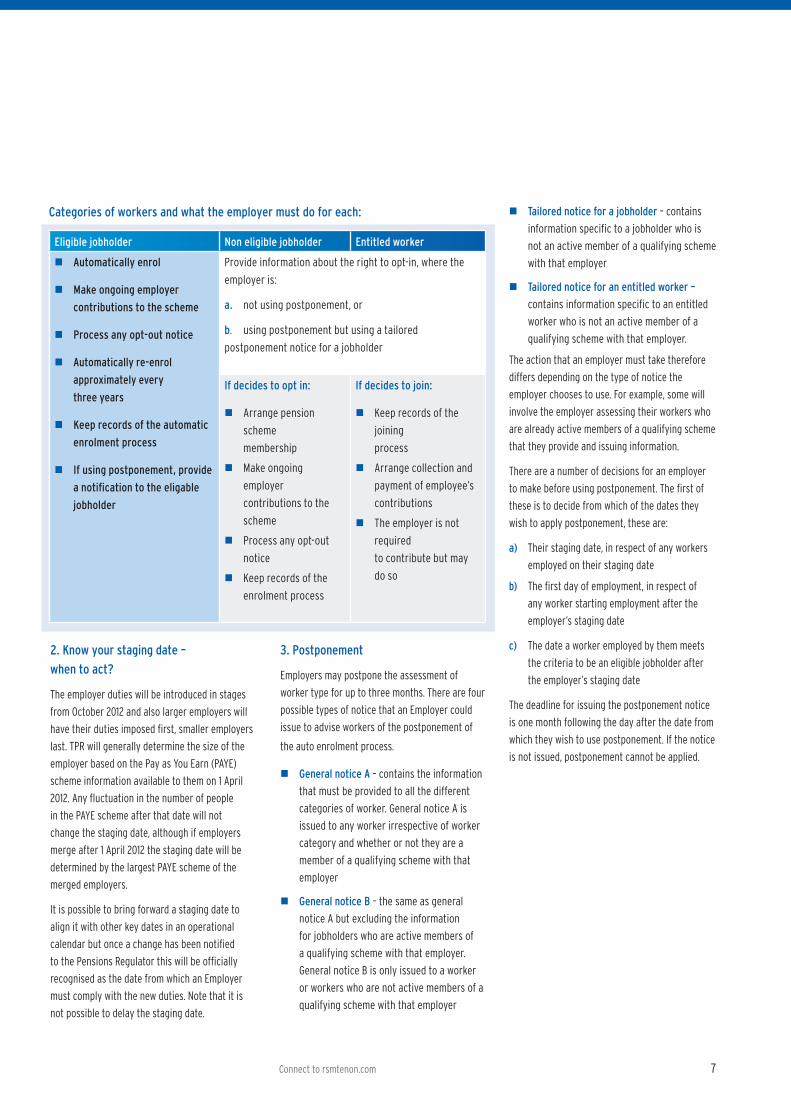

n Automatically enrol

n Make ongoing employer

contributions to the scheme

n Process any opt-out notice

n Automatically re-enrol

approximately every

three years

n Keep records of the automatic

enrolment process

n If using postponement, provide

a notification to the eligable

jobholder

Provide information about the right to opt-in, where the

employer is:

a. not using postponement, or

b. using postponement but using a tailored

postponement notice for a jobholder

If decides to opt in:

n Arrange pension

scheme

membership

n Make ongoing

employer

contributions to the

scheme

n Process any opt-out

notice

n Keep records of the

enrolment process

If decides to join:

n Keep records of the

joining

process

n Arrange collection and

payment of employee’s

contributions

n The employer is not

required

to contribute but may

do so

Categories of workers and what the employer must do for each: nTailored notice for a jobholder – contains

information specific to a jobholder who is

not an active member of a qualifying scheme

with that employer

nTailored notice for an entitled worker –

contains information specific to an entitled

worker who is not an active member of a

qualifying scheme with that employer.

The action that an employer must take therefore

differs depending on the type of notice the

employer chooses to use. For example, some will

involve the employer assessing their workers who

are already active members of a qualifying scheme

that they provide and issuing information.

There are a number of decisions for an employer

to make before using postponement. The first of

these is to decide from which of the dates they

wish to apply postponement, these are:

a) Their staging date, in respect of any workers

employed on their staging date

b) The first day of employment, in respect of

any worker starting employment after the

employer’s staging date

c) The date a worker employed by them meets

the criteria to be an eligible jobholder after

the employer’s staging date

The deadline for issuing the postponement notice

is one month following the day after the date from

which they wish to use postponement. If the notice

is not issued, postponement cannot be applied.

8 Preparing for Auto-enrolment

Choosing and using a qualifying pension scheme:

nMinimum requirements

nSelf certification

nPractical considerations

4. Pension Schemes under the new employer duties

Employers who already provide a pension scheme

(or schemes) for some or all of their workers, will

need to decide whether and how they want to

use this pension scheme to meet their duties for

existing members, as well as how they will fulfil

their new automatic enrolment responsibilities.

To make this decision, an employer will need to

understand both the qualifying scheme criteria

and the automatic enrolment scheme criteria and

satisfy themselves that their pension scheme

meets, or can be amended to meet, these criteria.

An employer without existing pension provision,

who is putting a pension scheme in place for

the first time to fulfil their enrolment duties, will

need to put an automatic enrolment scheme or

a qualifying scheme in place with effect from the

date the duties first apply.

There are three tiers of requirements that a

pension scheme must meet in order to be an

automatic enrolment scheme.

nAutomatic enrolment criteria

nQualifying criteria

nMinimum requirements

Automatic enrolment criteria

To be an automatic enrolment scheme, a scheme

must meet the qualifying criteria and it must not

contain any provisions that:

Prevent the employer from making the required

arrangements to automatically enrol, opt in or

re-enrol a jobholder

nRequire the jobholder to express a choice in

relation to any matter

nRequire the jobholder to provide any

information in order to remain an active

member of the pension scheme, for example

to choose an investment fund

Qualifying criteria

A qualifying scheme may be a UK scheme (one

with its main administration in the UK) or a non-UK

scheme (with its main administration outside the UK).

For a UK pension scheme to be qualifying in

relation to a jobholder, it must be:

nAn occupational or personal pension scheme

nTax registered, and

nSatisfy certain minimum requirements

Minimum requirements

Defined contribution (DC) occupational and

personal pension schemes (including Stakeholder

schemes).

The minimum requirements for these schemes are

based on the contribution rate. By October 2018,

this will require a total minimum contribution of

at least 8% of the jobholder’s qualifying earnings

in the relevant pay reference period, including a

minimum employer’s contribution of at least 3%.

Connect to rsmtenon.com 9

Salary Wages Bonuses

Overtime Commission Statutory sick pay

Statutory maternity pay Ordinary paternity pay Additional statutory paternity pay

Period Employer Minimum

contribution

Total minimum contribution

Staging date to 30 September

20171% 2%

1 October 2017 to 30

September 20182% 5%

1 October 2018 onwards 3% 8%

‘Qualifying earnings’ is a reference to earnings of between £5,668 and £41,450 made up of:

These contributions are due to be phased in and the table below details the minimum requirements:

Defined Benefit (DB) pension schemes

Most DB pension schemes will satisfy the minimum

requirement if the employer has been issued

with a contracting-out certificate by the National

Insurance Services to the Pensions Industry

(NISPI), part of HMRC (Her Majesty’s Revenue and

Customs). Otherwise, the minimum accrual rate is

1/120th of average qualifying earnings in the three

tax years before the end of pensionable service.

Hybrid pension schemes

A hybrid pension scheme is a scheme which has

elements of both DB and DC. Depending on the

type of pension scheme, it will have to meet the

same minimum requirements as for DB pension

schemes or a modified version,

or the same minimum requirements as a DC

pension scheme or a modified version, including

the option to use the certification process (see

overleaf), or a combination of the above.

10 Preparing for Auto-enrolment

Certification

Existing DC pension schemes, whether

occupational or personal pension schemes,

will base contributions on percentage rates of

pensionable pay. The definition of pensionable

pay in the scheme rules is likely to be different to

qualifying earnings.

In recognition of this, employers with schemes of

this type are able to self-certify that their scheme

meets the minimum qualifying criteria if the

scheme requires contributions in accordance with

one of the following tiers:

nTier 1 - A total minimum contribution of at

least 9% of pensionable pay (at least 4% of

which must be the employer’s contribution)

nTier 2 - A total minimum contribution of

at least 8% of pensionable pay (at least

3% of which must be the employer’s

contribution), provided that pensionable pay

constitutes at least 85% of earnings (the

ratio of pensionable pay to earnings can be

calculated as an average at scheme level)

nTier 3 - A total minimum contribution of at

least 7% of all earnings (at least 3% of which

must be the employer’s contribution)

For tiers one and two, pensionable pay must be at

least equivalent to basic pay.

5. Automatic enrolment process

Having identified an automatic enrolment duty in

respect of an eligible jobholder, the process for

automatically enrolling eligible jobholders into an

automatic enrolment scheme consists of a number

of steps set out in law.

The law also sets out the time limit for completing

automatic enrolment. Before the end of what is

known as the ‘joining window’ (the one-month

period from the eligible jobholder’s automatic

enrolment date), the employer must:

nGive information to the pension scheme

about the eligible jobholder

Give enrolment information to the eligible

jobholder

nMake arrangements to achieve active

membership for the eligible jobholder,

effective from their automatic enrolment

date

nThe employer is also required to keep certain

records of this process.

The information must be provided in writing. This

can include information sent by email, but does

not include merely signposting to an internet

or intranet site or displaying a poster in the

workplace.

Someone acting on the employer’s behalf, such

as an independent financial adviser or benefit

consultant can send the information, but it

remains the employer’s responsibility to make sure

it is provided, on time, and is correct and complete.

Once automatic enrolment has been completed, an

employer will have ongoing responsibilities either:

Period Employer Minimum Employee Minimum Total Minimum

T1 T2 T3 T1 T2 T3 T1 T2 T3

Staging date to 30 September 2017

2% 1% 1% 1% 1% 1% 3% 2% 2%

1 October 2017 to 30 September 2018

3% 2% 2% 3% 3% 3% 6% 5% 5%

1 October 2018 onwards

4% 3% 3% 5% 5% 4% 9% 8% 7%

These contributions are also due to be phased in and the table below details the minimum requirements:

nWith the pension scheme, as the jobholder

remains a member of the scheme, such as

paying contributions

nTo manage the opt-out process, if the

jobholder chooses to opt out of the pension

scheme

nTo keep records

The employer will need to calculate and pay their

own contributions as well as calculating, deducting

and paying the jobholder’s contributions to the

automatic enrolment scheme.

Connect to rsmtenon.com 11

“The employer will need to calculate and pay their own contributions as well as calculating, deducting and paying the jobholder’s contributions to theautomatic enrolment scheme.”

12 Preparing for Auto-enrolment

Section 2: Implementation

The second stage in this process will be

implementing your employer duties:

nOpting in, joining and contractual

enrolment

nOpting out

nSafeguarding individuals

nRecord keeping duties

6. Opting in, joining and contractual enrolment

There are three employer duties that cover

establishing active membership of a pension

scheme (‘the enrolment duties’):

nAutomatic enrolment: The employer must

make arrangements by which an eligible

jobholder becomes an active member of an

automatic enrolment scheme or qualifying

scheme with effect from the automatic

enrolment date

nOpting in: A jobholder can require the

employer to arrange for them to become an

active member of an automatic enrolment

scheme, with effect from the enrolment

date. They do this by giving the employer an

‘opt-in notice’

nJoining: An entitled worker can require the

employer to arrange for them to become an

active member of a pension scheme. They

do this by giving the employer a ‘joining

notice’

Opting in / Joining

If a jobholder chooses to exercise their right to

opt in, they do so by giving the employer an ‘opt-

in notice’. Upon receipt, the employer is required

to make arrangements for the jobholder to

become an active member of an automatic

enrolment scheme or qualifying scheme

from the enrolment date. The employer must

follow the same process as for the automatic

enrolment of eligible jobholders to enrol the

jobholder.

If an entitled worker chooses to exercise their

right to join, they do so by giving the employer

a ‘joining notice’. Upon receipt, the employer is

required to make arrangements for that worker

to become an active member of a pension

scheme. The scheme the employer uses for these

purposes does not have to be an automatic

enrolment scheme, or even a qualifying scheme.

Since an employer may receive an opt-in or

joining notice many months or even years after

issuing the information to the worker about their

appropriate right, a key task for the employer on

receiving the notice is to assess the category of

the worker submitting it.

This is to identify whether the worker is a

non-eligible jobholder with a right to opt in to

an automatic enrolment scheme, or an entitled

worker with a right to join a pension scheme, at

the time the worker gives the notice.

This is important because it determines which

process the employer must follow in arranging

for active membership, and may determine the

choice of pension scheme the employer uses.

For an employer who has chosen to use a

contractual agreement (for example, the

contract of employment) to enrol their workers

into a pension scheme, it is important to

understand the interaction with the employer

duties and the action they may still need to

take. As a minimum, they will still be required to

provide some information to their workers under

the new duties and they will still be required to

register with The Pensions Regulator to tell them

how they have complied with their duties.

7. Opting out

It is compulsory for an employer to

automatically enrol their eligible jobholders

into an automatic enrolment scheme. It is also

compulsory for an employer to arrange active

membership of an automatic enrolment scheme

if a jobholder opts in (or another scheme if an

entitled worker wishes to join).

However, ongoing membership of the scheme

is not compulsory for the jobholder. Where a

jobholder has been automatically enrolled, or

enrolled as a result of an opt-in request, they

can choose to ‘opt out’ of a pension scheme.

Eligible jobholders may choose to opt out after

they have been automatically enrolled and may

then opt back in at any time.

Non-eligible jobholders who have opted in may

choose to opt out, after they have been enrolled.

Workers who have already been enrolled under

contractual enrolment (eg under their contract

of employment) and entitled workers who have

asked to join a scheme do not have the right to

choose to opt out in order to receive a refund.

Instead, if they want to leave the scheme, they

must cease membership in accordance with the

scheme rules.

A jobholder who becomes an active member of a

pension scheme under the automatic enrolment

provisions has a period of time during which

they can opt out. This also applies to those

who become active members under the opt-in

provisions. This is known as the ‘opt-out period’.

For occupational pension schemes, the opt-out

period starts from the later of the date the

jobholder becomes an active member with effect

from the automatic enrolment date (ie the date

that the administrative steps for achieving active

membership are completed), or is provided with

written enrolment information.

For personal pension schemes (including

stakeholders), the opt-out period starts from the

later of when the jobholder is sent the terms and

conditions of the agreement to become an active

member or is provided with written enrolment

information.

To deal quickly and efficiently with opt outs, the

employer should put processes in place that will

enable them to:

nCheck the validity of opt-out notices

nNotify the scheme of the opt out

nStop the deduction and payment of

contributions

nRefund contributions to the jobholder

Connect to rsmtenon.com 13

8. Safeguarding individuals

With effect from July 2012 the workplace pension

reform introduced new duties and safeguards that

employers must adhere to. The safeguards are

intended to protect individuals, meaning there are

certain things the employer must not do, both before

a person starts working for them and once that

person is a member of a pension scheme with that

employer.

The safeguards have been put in place to protect

entitled workers and jobholders, but the prohibited

recruitment safeguard extends this protection to job

applicants as well.

Unless the jobholder asks to leave, or is already an

active member of another qualifying pension scheme

with that employer, the employer must not take, or

fail to take, any action that results in either:

nThe jobholder ceasing to be an active member of

a qualifying scheme

nThe scheme of which they are an active member

ceasing to be a qualifying scheme

The employer must not treat a worker unfairly

or dismiss the worker on grounds related to the

employer duties.

Inducements

The law relating to inducements is an important

safeguard for entitled workers and jobholders. An

inducement is any action taken by the employer, the

sole or main purpose of which is to attempt to induce:

nA jobholder to opt out without becoming an

active member of a qualifying scheme with

effect from the date on which they originally

became an active member (ie their automatic

enrolment date or enrolment date)

nA jobholder or an entitled worker to cease

active membership of a pension scheme without

becoming an active member of another scheme

with effect from the day after the original

membership ceased.

Any entitled worker’s or jobholder’s decision to opt

out of, or leave, their current pension scheme should

be taken freely and without being influenced by the

employer.

14 Preparing for Auto-enrolment

The intention of the legislation is to encourage pension saving at a minimum level, not to restrict flexible

benefits packages that employers wish to offer their workers and the individual retains the right to choose

the make-up of their flexible benefits. However, employers must be confident that, in offering such a

package, their sole or main purpose is not to induce individuals to opt out of a qualifying scheme.

Prohibited recruitment conduct

The aim of this measure is to deter employers from trying to screen out job applicants on grounds relating

to potential pension scheme membership.

9. Keeping records

With the introduction of the employer duties from 2012, there is now a new legal requirement on employers,

trustees, managers and providers to keep certain records.

The records an employer must keep will enable them to prove that they have complied with their duties.

Keeping accurate records also makes good business sense because it can help an employer to:

nAvoid or resolve potential disputes with employees

nHelp check or reconcile contributions made to the pension scheme.

The employer must also keep records relating to the pension scheme and the pension scheme must keep

records relating to the active members and opt outs.

Who the record relates to What record must be kept How long it must be

kept

Jobholders and workers who become members

Name, national insurance number, date of birth, gross earnings in each relevant pay reference period, the contributions payable in each relevant pay reference period by an employer to the scheme, and the amount payable. This includes contributions due on the employer’s behalf and deductions made from earnings.The date contributions were paid to the scheme 6 years

Additional informationfor jobholders only

Automatic enrolment date, opt-in notice (original format), and the contributions to which the jobholder is entitled under the scheme rules (this demonstrates that the scheme used is a qualifying scheme)

Opt-out notice (original format) 4 years

Additional informationfor workers only

Date with effect from which the worker became an active memberJoining notice (original format)

6 yearsAll workers for whom the employer has used postponement

Name, national Insurance number (where one exists) and date the notice was sent to the worker

Connect to rsmtenon.com 15

www.rsmtenon.com/autoenrolment RSM Tenon Financial Management Limited is authorised and regulated by the Financial Conduct Authority, FCA register number 192618. A subsidiary of RSM Tenon Group PLC. RSM Tenon Group PLC is an independent member of the RSM International network. The RSM International network is a network of independent accounting and consulting firms each of which practices in its own right. RSM International is the brand used by the network which is not itself a separate legal entity in any jurisdiction. RSM Tenon Financial Management Limited (No 03953153) is registered in England and Wales. Registered Office 66 Chiltern Street, London W1U 4GB. England

BWF07470413 KD/7484/7513 exp: 06/04/2014

ding you d