Penetrating the US Wine Market - London Wine Fair

58

The Insider’s Guide to Penetrating the U.S. Market London Wine Fair 20 May 2015 Steve Raye John Beaudette Sid Patel

-

Upload

australia-trade-tasting -

Category

Food

-

view

599 -

download

0

Transcript of Penetrating the US Wine Market - London Wine Fair

The Insider’s Guide to Penetrating the U.S.

Market London Wine Fair

20 May 2015

Steve Raye John Beaudette Sid Patel

Speakers

Steve Raye, President Bevology Inc. [email protected]

John Beaudette, President MHW Ltd. [email protected]

Sid Patel, President Beverage Trade Network [email protected]

Overview Of The U.S. Beverage Alcohol Market & Brand Entry

Considerations

John Beaudette London Wine Fair

May 20, 2015

Agenda

• Overview Of Beverage Alcohol in the US

• Historical Perspective and the U.S. system works, the three tier system, brand economics

• Thoughts On Where the Industry is Heading, Changes in the Distribution System, and What May Impact the Future.

• Options To Market Entry

4

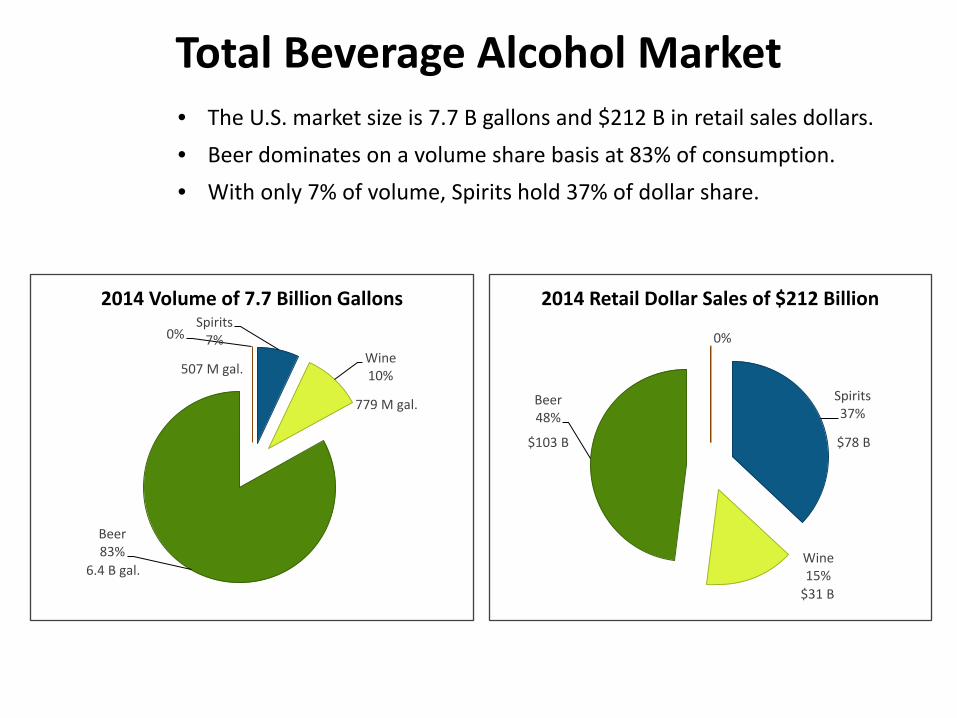

Total Beverage Alcohol Market • The U.S. market size is 7.7 B gallons and $212 B in retail sales dollars.

• Beer dominates on a volume share basis at 83% of consumption.

• With only 7% of volume, Spirits hold 37% of dollar share.

Spirits 7%

Wine 10%

Beer 83%

0%

2014 Volume of 7.7 Billion Gallons

507 M gal.

6.4 B gal.

779 M gal. Spirits 37%

Wine 15%

Beer 48%

0%

2014 Retail Dollar Sales of $212 Billion

$103 B

$31 B

$78 B

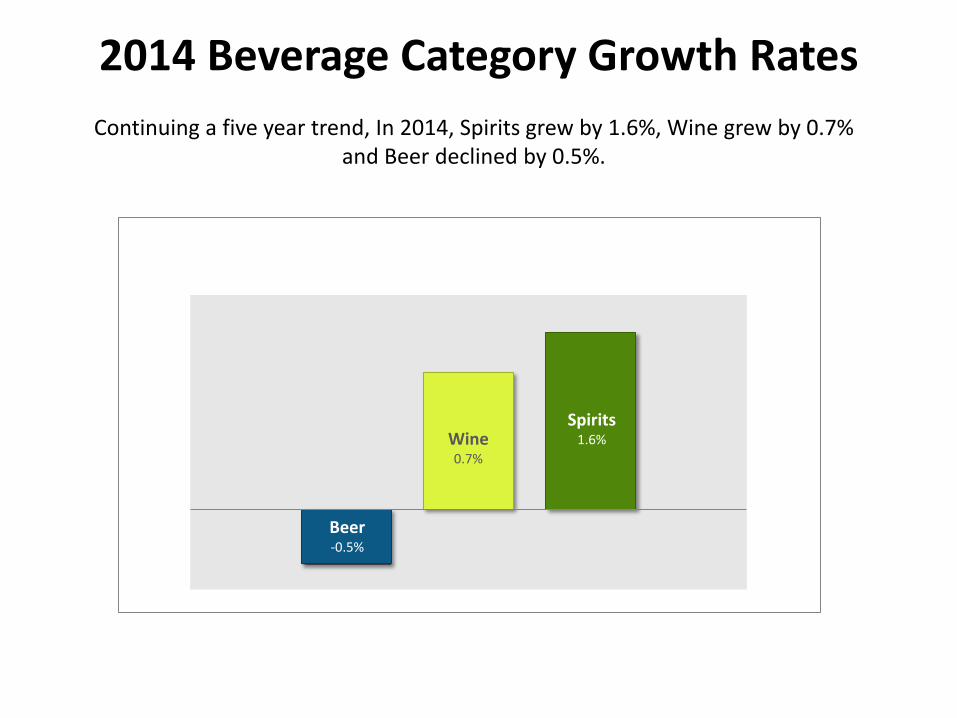

2014 Beverage Category Growth Rates

Beer -0.5%

Wine 0.7%

Spirits 1.6%

Continuing a five year trend, In 2014, Spirits grew by 1.6%, Wine grew by 0.7% and Beer declined by 0.5%.

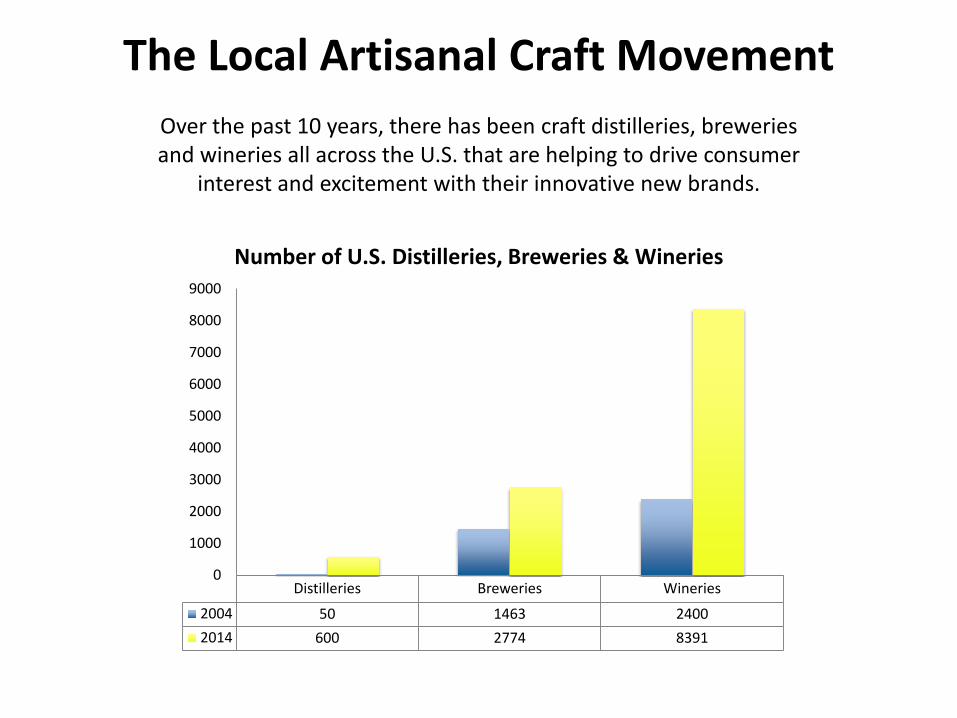

The Local Artisanal Craft Movement Over the past 10 years, there has been craft distilleries, breweries and wineries all across the U.S. that are helping to drive consumer

interest and excitement with their innovative new brands.

Distilleries Breweries Wineries 2004 50 1463 2400 2014 600 2774 8391

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Number of U.S. Distilleries, Breweries & Wineries

WINE TRENDS

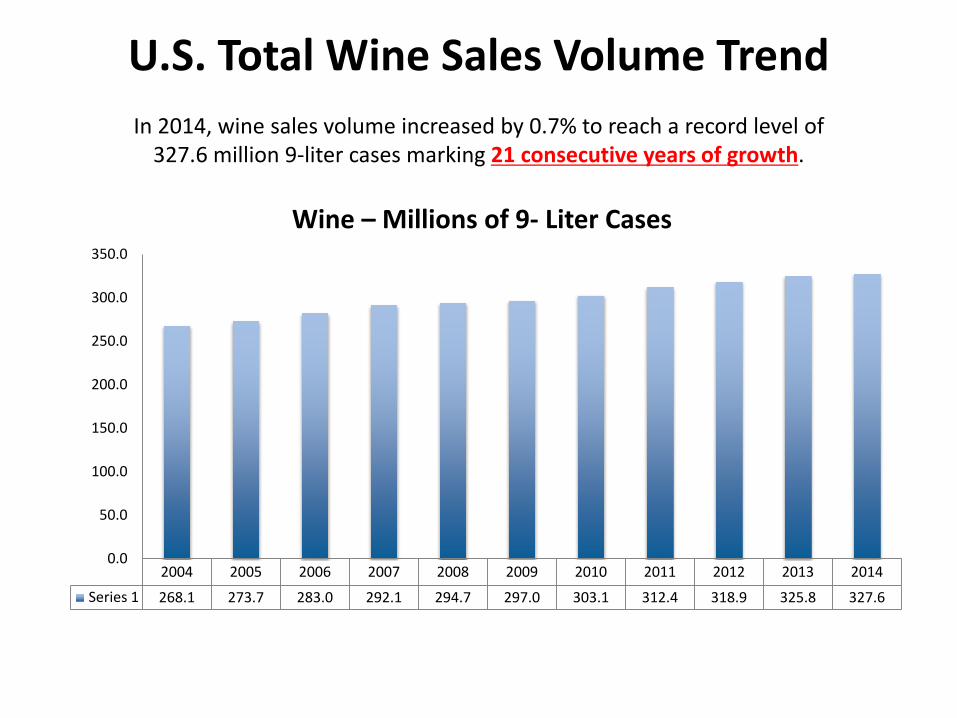

U.S. Total Wine Sales Volume Trend In 2014, wine sales volume increased by 0.7% to reach a record level of

327.6 million 9-liter cases marking 21 consecutive years of growth.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Series 1 268.1 273.7 283.0 292.1 294.7 297.0 303.1 312.4 318.9 325.8 327.6

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Wine – Millions of 9- Liter Cases

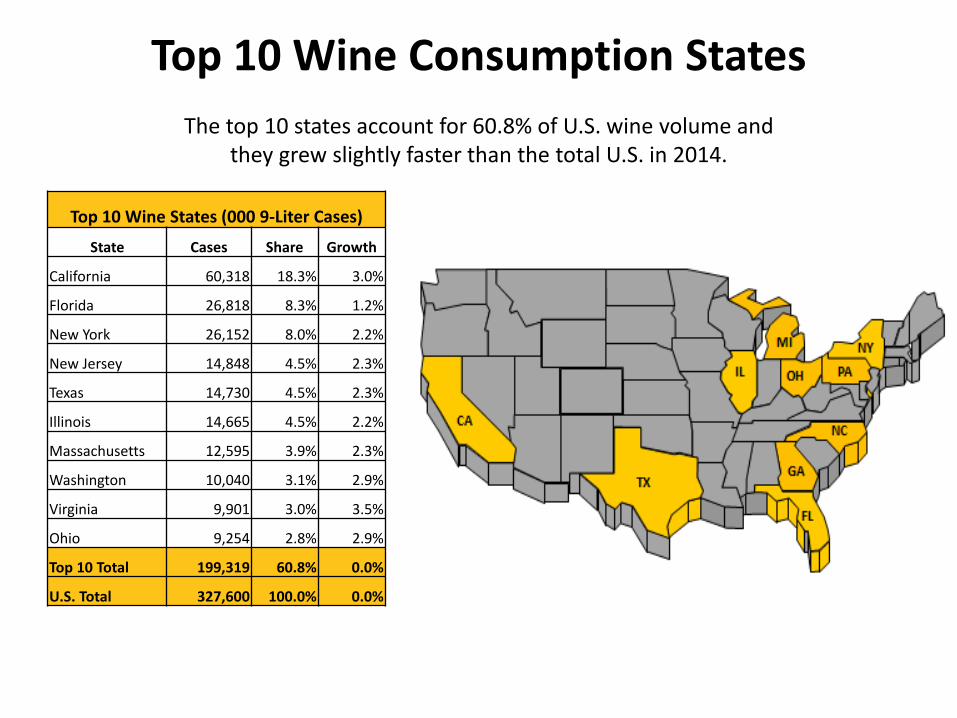

Top 10 Wine Consumption States The top 10 states account for 60.8% of U.S. wine volume and

they grew slightly faster than the total U.S. in 2014.

Top 10 Wine States (000 9-Liter Cases) State Cases Share Growth

California 60,318 18.3% 3.0%

Florida 26,818 8.3% 1.2%

New York 26,152 8.0% 2.2%

New Jersey 14,848 4.5% 2.3%

Texas 14,730 4.5% 2.3%

Illinois 14,665 4.5% 2.2%

Massachusetts 12,595 3.9% 2.3%

Washington 10,040 3.1% 2.9%

Virginia 9,901 3.0% 3.5%

Ohio 9,254 2.8% 2.9%

Top 10 Total 199,319 60.8% 0.0%

U.S. Total 327,600 100.0% 0.0%

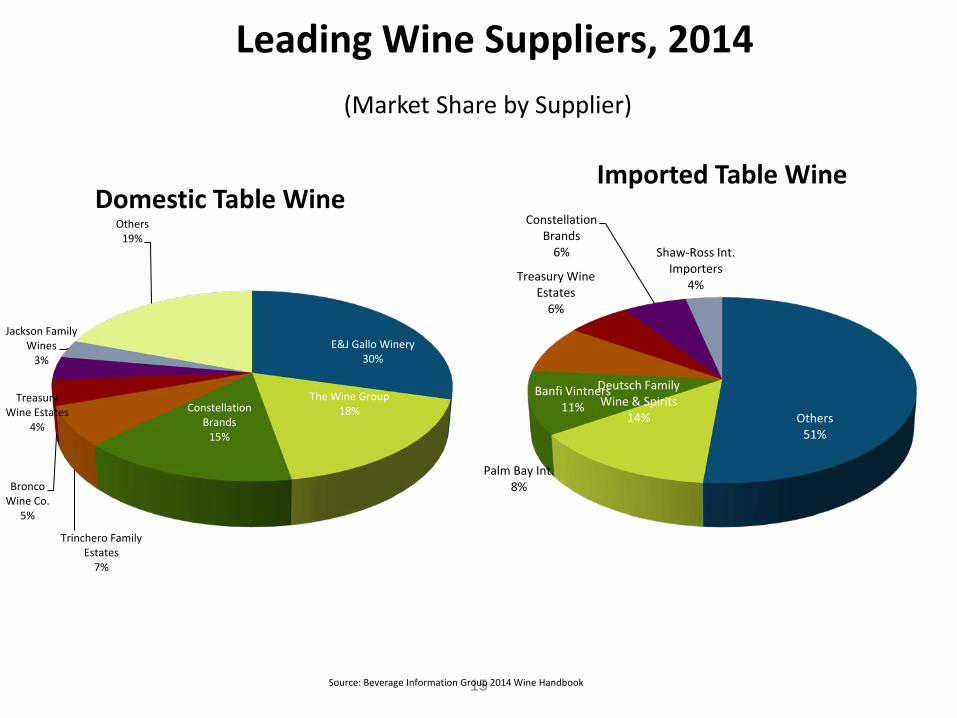

E&J Gallo Winery 30%

The Wine Group 18% Constellation

Brands 15%

Trinchero Family Estates

7%

Bronco Wine Co.

5%

Treasury Wine Estates

4%

Jackson Family Wines

3%

Others 19%

Domestic Table Wine

Leading Wine Suppliers, 2014

Others 51%

Deutsch Family Wine & Spirits

14%

Banfi Vintners 11%

Palm Bay Int. 8%

Treasury Wine Estates

6%

Constellation Brands

6% Shaw-Ross Int. Importers

4%

Imported Table Wine

15

(Market Share by Supplier)

Source: Beverage Information Group 2014 Wine Handbook

History of Beverage Alcohol in the US

17

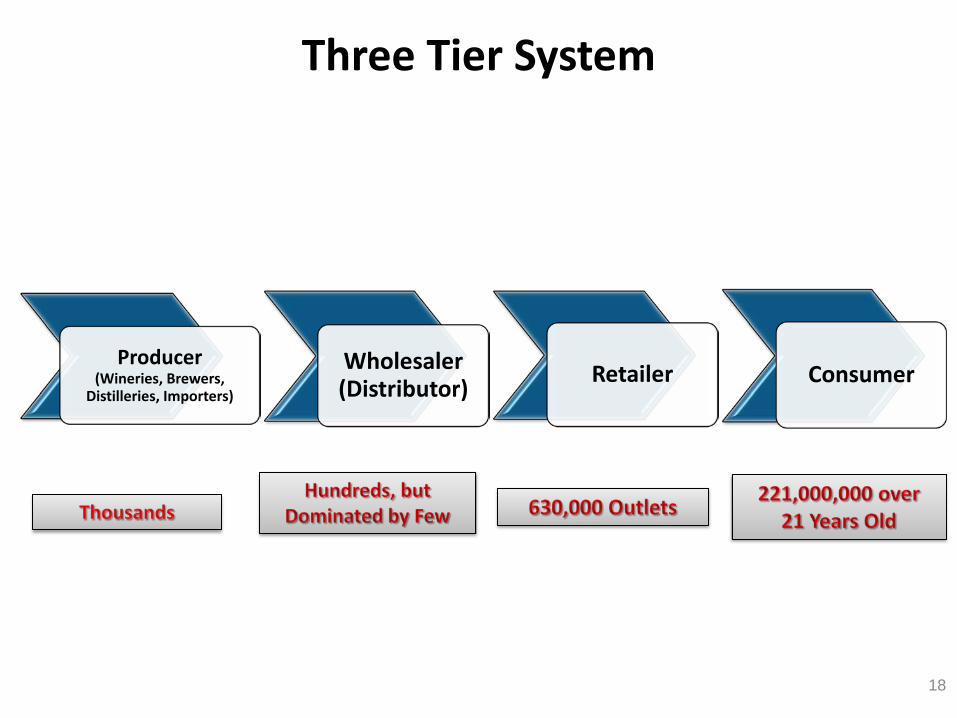

Three Tier System

18

Producer (Wineries, Brewers,

Distilleries, Importers)

Wholesaler (Distributor) Retailer Consumer

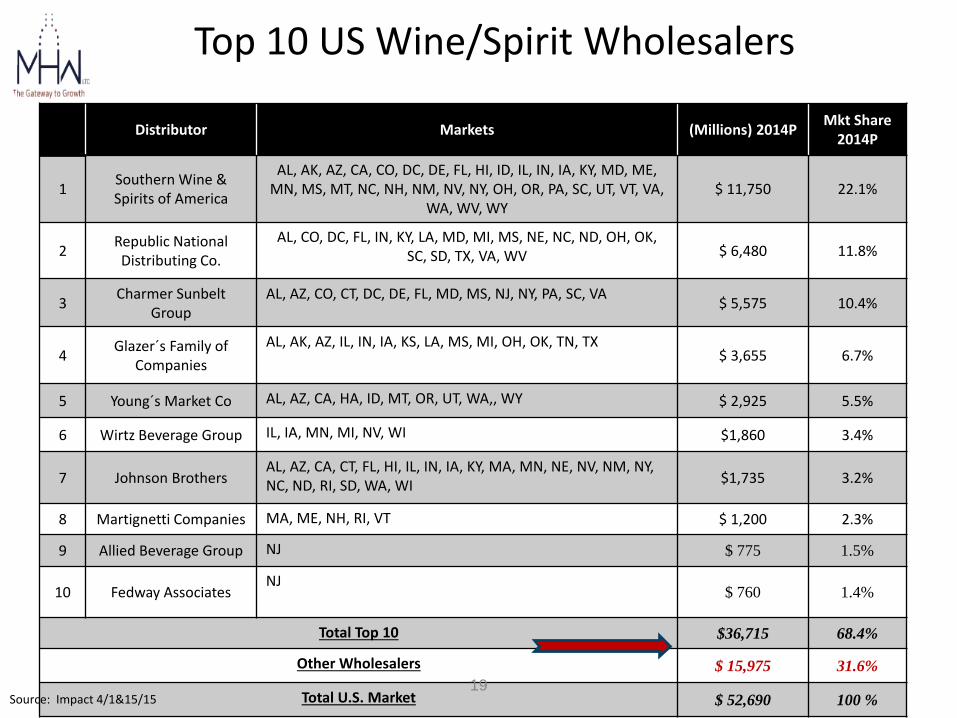

Distributor Markets (Millions) 2014P Mkt Share 2014P

1 Southern Wine & Spirits of America

AL, AK, AZ, CA, CO, DC, DE, FL, HI, ID, IL, IN, IA, KY, MD, ME, MN, MS, MT, NC, NH, NM, NV, NY, OH, OR, PA, SC, UT, VT, VA,

WA, WV, WY $ 11,750 22.1%

2 Republic National Distributing Co.

AL, CO, DC, FL, IN, KY, LA, MD, MI, MS, NE, NC, ND, OH, OK, SC, SD, TX, VA, WV $ 6,480 11.8%

3 Charmer Sunbelt Group

AL, AZ, CO, CT, DC, DE, FL, MD, MS, NJ, NY, PA, SC, VA $ 5,575 10.4%

4 Glazer´s Family of Companies

AL, AK, AZ, IL, IN, IA, KS, LA, MS, MI, OH, OK, TN, TX $ 3,655 6.7%

5 Young´s Market Co AL, AZ, CA, HA, ID, MT, OR, UT, WA,, WY $ 2,925 5.5%

6 Wirtz Beverage Group IL, IA, MN, MI, NV, WI $1,860 3.4%

7 Johnson Brothers AL, AZ, CA, CT, FL, HI, IL, IN, IA, KY, MA, MN, NE, NV, NM, NY, NC, ND, RI, SD, WA, WI $1,735 3.2%

8 Martignetti Companies MA, ME, NH, RI, VT $ 1,200 2.3%

9 Allied Beverage Group NJ $ 775 1.5%

10 Fedway Associates NJ

$ 760 1.4%

Total Top 10 $36,715 68.4%

Other Wholesalers $ 15,975 31.6%

Total U.S. Market $ 52,690 100 %

Top 10 US Wine/Spirit Wholesalers

Source: Impact 4/1&15/15 19

Brand Approval / Launch Timeline

20

Federal Label (COLA) Approval

4 to 8 weeks depending on product and complexity

State Registration & Approval

1 to 8 weeks including price posting where

required

Product Ships To Wholesaler

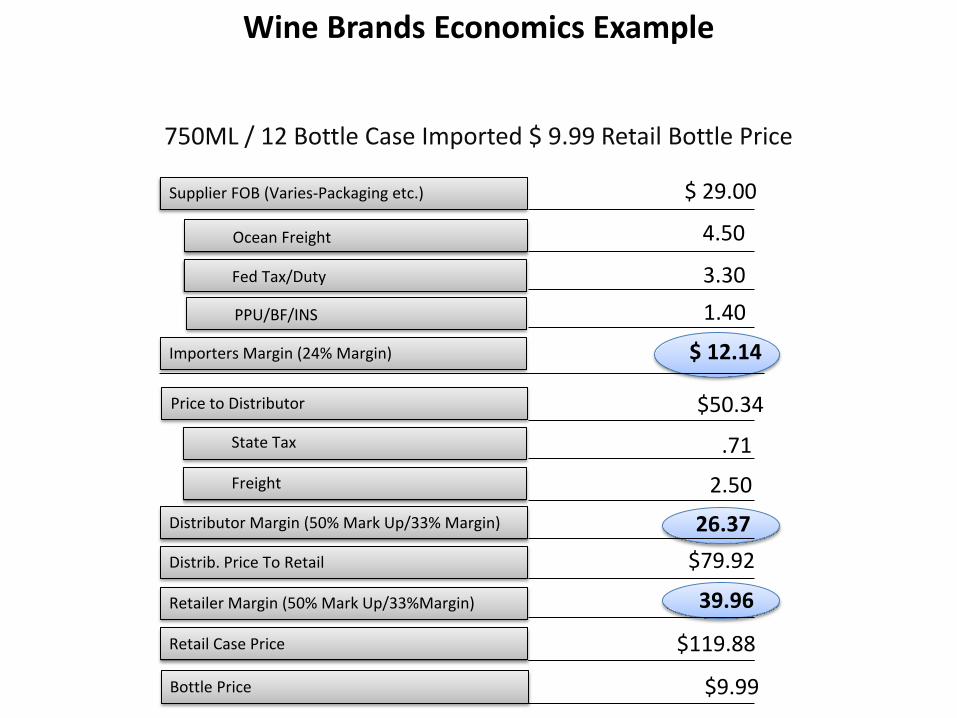

750ML / 12 Bottle Case Imported $ 9.99 Retail Bottle Price

Supplier FOB (Varies-Packaging etc.) $ 29.00

Ocean Freight 4.50

Fed Tax/Duty 3.30

PPU/BF/INS 1.40

Importers Margin (24% Margin) $ 12.14

Price to Distributor $50.34

State Tax .71

Freight 2.50

Distributor Margin (50% Mark Up/33% Margin) 26.37

Distrib. Price To Retail $79.92

Retailer Margin (50% Mark Up/33%Margin) 39.96

Retail Case Price $119.88

Bottle Price $9.99

Wine Brands Economics Example

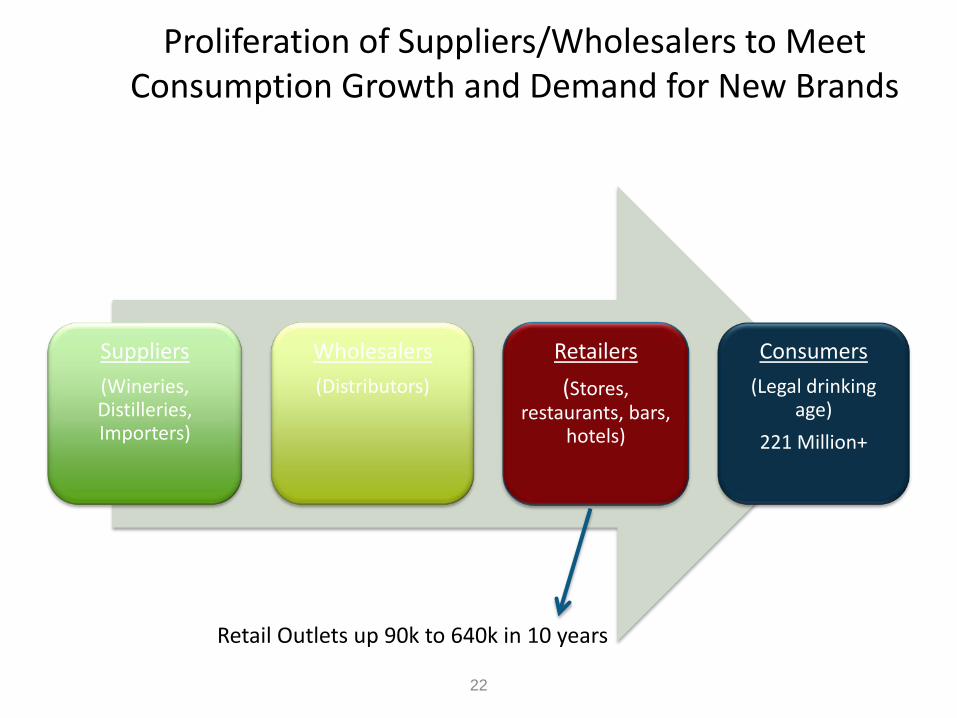

Suppliers (Wineries, Distilleries, Importers)

Wholesalers (Distributors)

Retailers (Stores,

restaurants, bars, hotels)

Consumers (Legal drinking

age) 221 Million+

Retail Outlets up 90k to 640k in 10 years

22

Proliferation of Suppliers/Wholesalers to Meet Consumption Growth and Demand for New Brands

Brand Sales & Valuation Trends

• Beverage Alcohol Brands Commanding Strong Prices • Valuation Ranges/Methods:

– Annual Case Multiples (ACM) $300 to $1,500 (spirits) – Revenue Multiples (1 to 5+Times) – EBITDA Multiple (6 to 14+ Times)

23

Potential Approaches to the U.S. Market

• Major National Importers/Suppliers (examples)

• Midsize / Small Importers and Distributors (many and growing). • Local / Regional Distributors (with importing capabilities). • Licensed Service Importers & National Distribution Companies. • Local Craft Brewers, Craft Distilleries, Wine Contract Production • Establish US Import & Distribution Company. • Other (Internet for wine), “Reverse Tier Marketing”/Private Labels.

24

Building Your Sales Process For the US Market.

By Sid Patel, CEO and Founder,

Beverage Trade Network.com

Fact. You are in the sales business.

Do you have a Sales Process?

• Preparation • Prospecting • Approach • Negotiation • Launch • Support

Wine like any other business needs to be sold.

A sales process should include

Preparation

Case Cards, Shelf Talkers, Brochures, Branded Cartons, Latest Vintage for Samples, Target Lists, Support Plan, Contract, Credit Application, Launch Plan, Sell Sheets.

Importers like to deal with prepared suppliers.

Are you ready with your Toolkit?

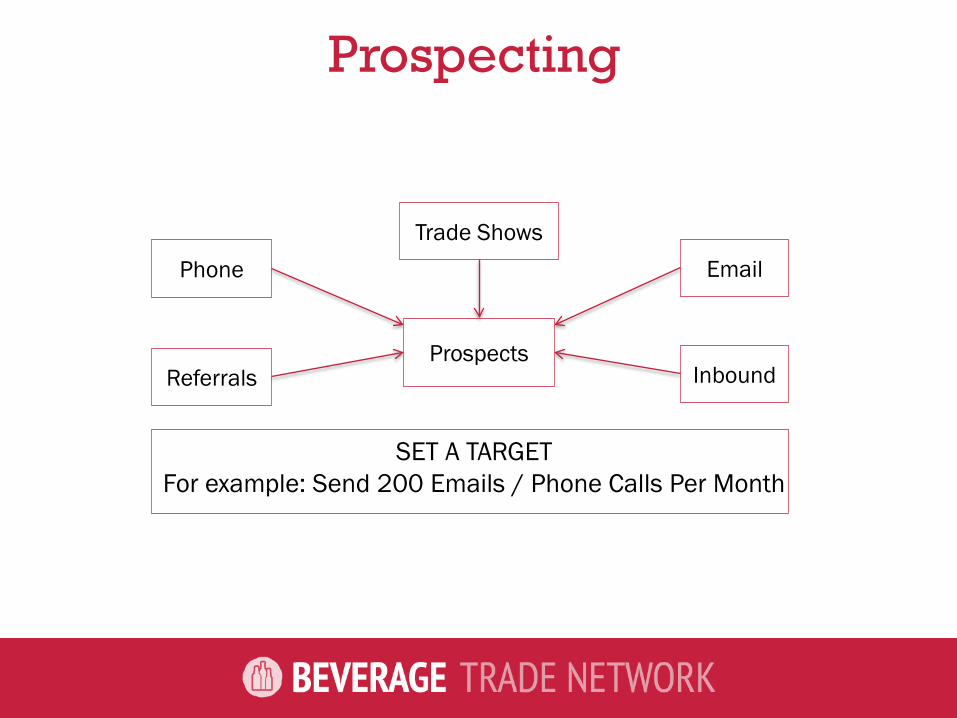

Prospecting

SET A TARGET For example: Send 200 Emails / Phone Calls Per Month

Email Trade Shows

Phone

Referrals Inbound Prospects

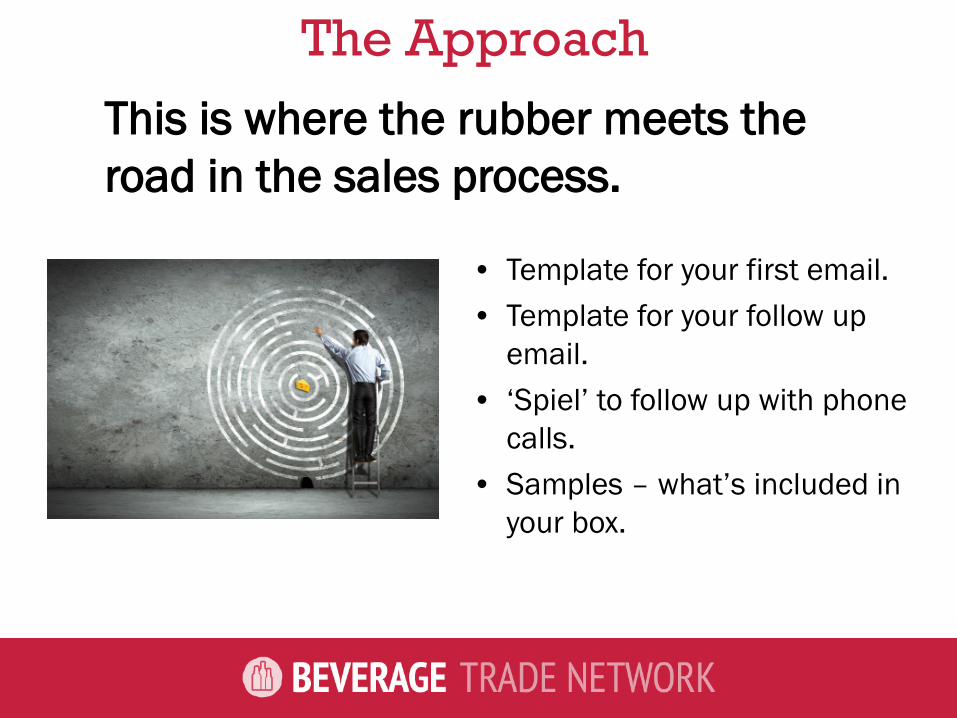

The Approach

• Template for your first email. • Template for your follow up

email. • ‘Spiel’ to follow up with phone

calls. • Samples – what’s included in

your box.

This is where the rubber meets the road in the sales process.

Negotiation.

Includes discussing • Good margins • Motivations of your

importer • Programming • Protect yourself

Plan beyond 1000 cases.

Coming to an agreement

Launch.

• Sales kick-off meeting • Market work in multiple

states with your importer’s distributors.

• In-store tastings and building key retail relations.

The goal is to deplete 50% of your brand’s stock at your importer before you return.

The most important time for your brand in the target market.

Support

• Market work • In-store tastings • Sales incentives • Retailers QD discounts

Invest ALL marketing dollars in trade only

Plan beyond 1,000 cases

Winning Sales Process

• Preparation • Prospecting • Negotiation • Launch • Support and second PO • Sell new SKUs to your current accounts with

same process.

Focus on depletion. Everyone wins.

Contact Info Sid Patel (CEO and Founder, Beverage Trade Network) E-mail [email protected] Phone +1 901 BTN LIVE

/BeverageTrade @BeverageTrade

U.S. WINE MARKET: DISRUPTING THE SYSTEM Non-traditional marketing strategies to gain a competitive edge.

© 2015 Steve Raye

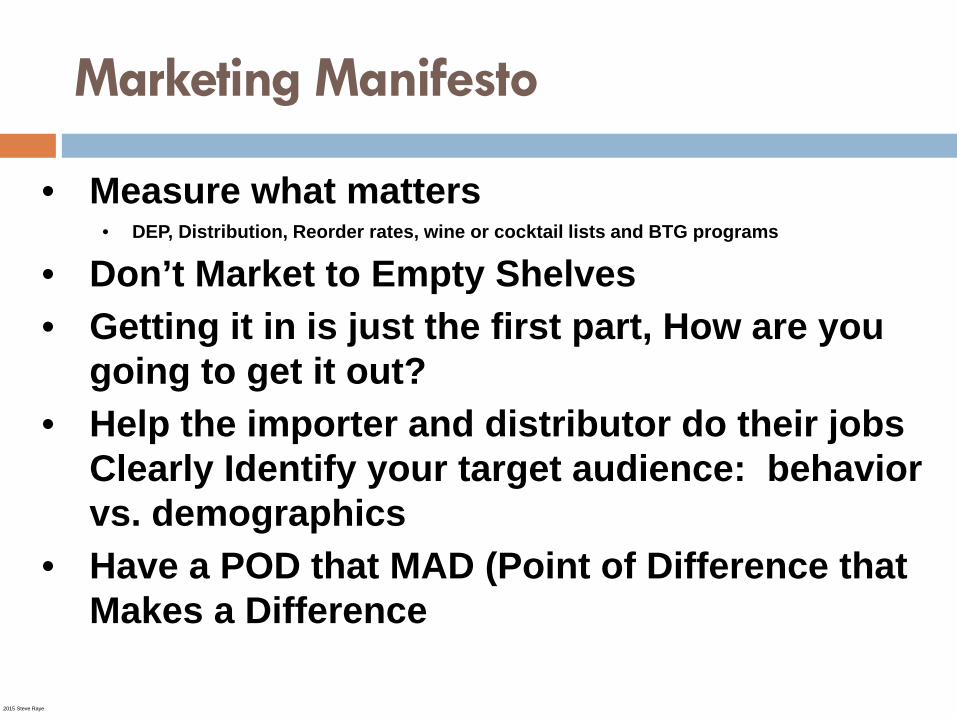

Marketing Manifesto

• Measure what matters • DEP, Distribution, Reorder rates, wine or cocktail lists and BTG programs

• Don’t Market to Empty Shelves • Getting it in is just the first part, How are you

going to get it out? • Help the importer and distributor do their jobs

Clearly Identify your target audience: behavior vs. demographics

• Have a POD that MAD (Point of Difference that Makes a Difference

© 2015 Steve Raye

You Can Change the Equation!

1 + 1 = 11

© 2015 Steve Raye

You Can Change the Equation!

1 + 1 = 11

© 2015 Steve Raye

How? Think and Act Differently

Zig

5

© 2015 Steve Raye

How? Think and Act Differently

Zig Zag

© 2015 Steve Raye

Guiding Principle

Align programs with account needs…help them build their business: WIIFM

“What’s in it for ME?”

•Increase sales (volume and profitability) •Increase customer frequency •Increase new traffic

© 2015 Steve Raye

U.S. Market Trends: Millennials Reshaping the Market

Millennials represent the largest wine consuming age-cohort—77 million.

All will reach LDA in 2015 They like to explore new and different things and are a

primary force driving wine growth – particularly imports. Peer vs. pundit recommendations, and research closer to

the actual point of purchase or consumption (label ID apps)

More likely to purchase imported wine

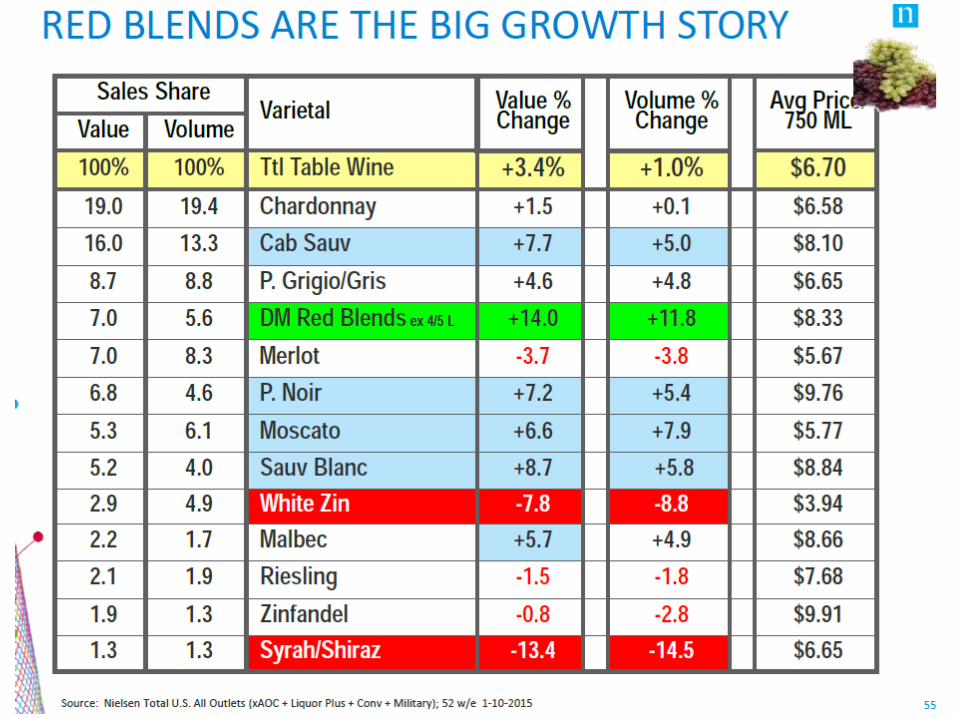

Red Blends continue to be hot Confusion in definition will result in shakeout in

reference to sweet vs. dry red blends Fragmentation in varietal preference is

changing the business Where once Cabs and Chards ruled, Red Blends,

Moscato, Prosecco, Pinot Noir, Pinot Grigio now compete. What’s next?

46

U.S. Market Trends: Varietals

U.S. Market Trends: Distribution Innovation

E-commerce and new/non-traditional distribution channels are rapidly growing, represent opportunity

Explosion in delivery-within-an-hour services: Drizly, Minibar Delivery, et al.

Delivery-Within-An-Hour

Drizly, Minibar Delivery Laser-Targeted to Millennials: immediate, no

shipping upcharge Geographically targetable down to metro

market Tool to drive retail distribution, support

wholesaler/importer E-commerce solution

© 2015 Steve Raye

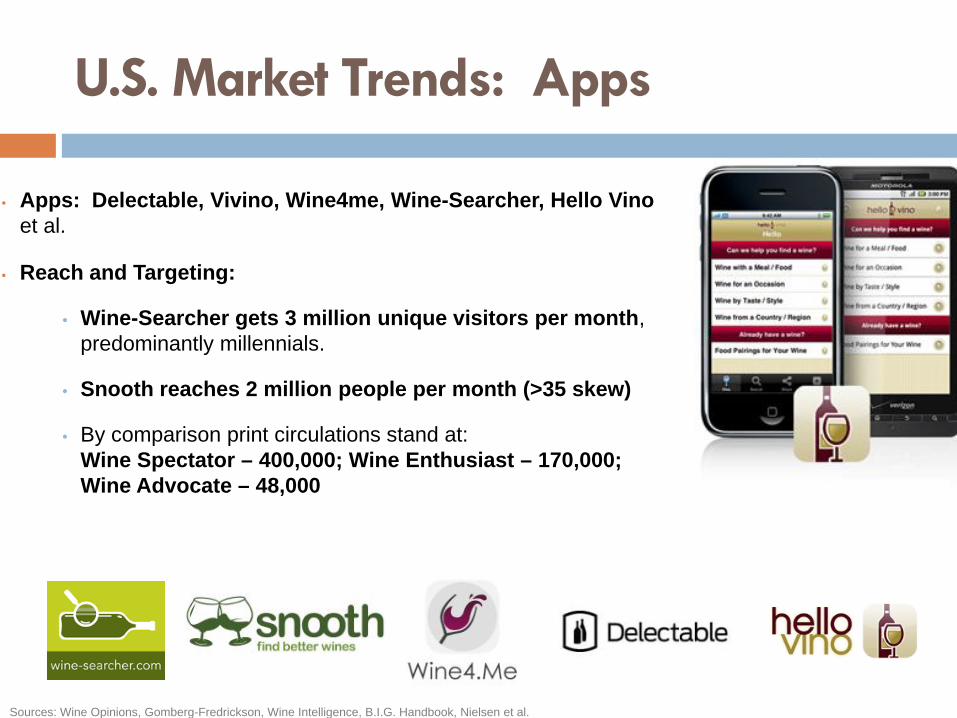

• Apps: Delectable, Vivino, Wine4me, Wine-Searcher, Hello Vino et al.

• Reach and Targeting:

• Wine-Searcher gets 3 million unique visitors per month, predominantly millennials.

• Snooth reaches 2 million people per month (>35 skew)

• By comparison print circulations stand at: Wine Spectator – 400,000; Wine Enthusiast – 170,000; Wine Advocate – 48,000

Sources: Wine Opinions, Gomberg-Fredrickson, Wine Intelligence, B.I.G. Handbook, Nielsen et al.

U.S. Market Trends: Apps

So What?

“I know half my advertising doesn’t work…I just don’t know which half”

Pure E-marketing/

Ecommerce

ROI

E-Commerce

Allows you to sell in multiple states, nearly nationally, when you may only have distribution in one.

Strong penetration with Baby Boomers, average purchase is 3X typical physical store purchase

Has established awareness that it represents a better selection of hard-to-find wines

Tools like Wine-Searcher drive intent to purchase

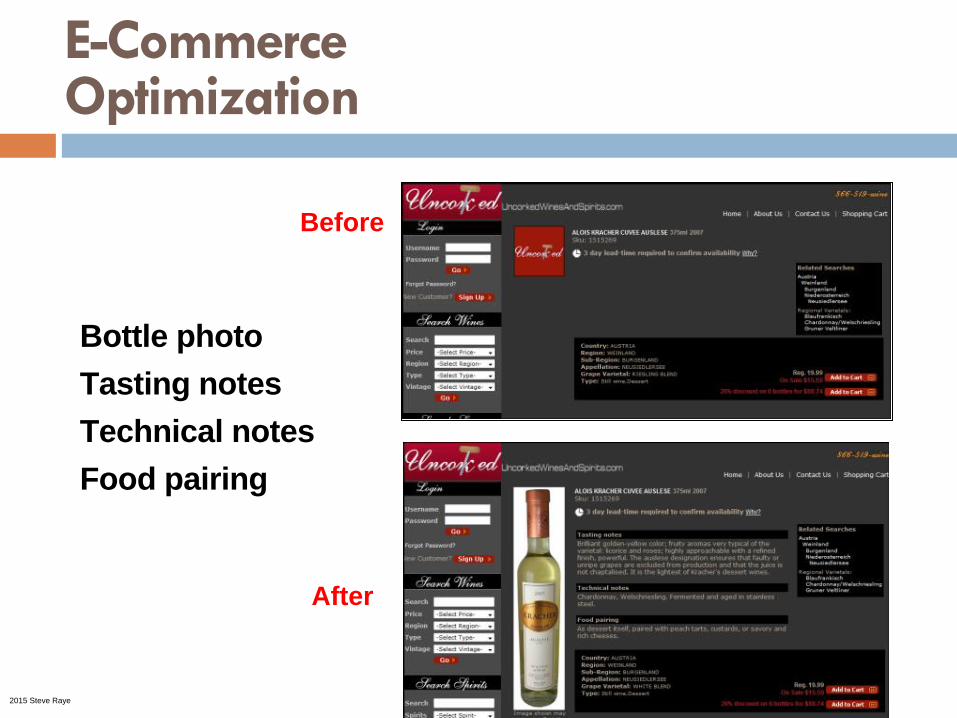

E-Commerce Optimization

Bottle photo Tasting notes Technical notes Food pairing

After

Before

© 2015 Steve Raye

Analysis and Performance Metrics: Free Market Research

Based on behavior…what they actually do vs. what they say they are going to do. Google Analytics Facebook Insights

Social Media Activation: Platform Recommendations

Facebook: Engage with your broadest audience of wine consumers.

Instagram: Every picture tells a story

Twitter: Trade focus

© 2015 Steve Raye

U.S. competitions accepting non-imported wines Ultimate Wine Challenge Accepts brands not currently imported to the US http://www.ultimate-beverage.com/ultimate-wine-challenge-UWC/2015-wine-entry-forms/

BTI (Beverage Testing Institute) Accepts brands not currently registered in the U.S. Check site for deadlines http://us6.campaign-archive2.com/?u=da8603c0af6040dcc7e4d9ed2&id=8fdf91dae4&e=

San Francisco Wine Competition Deadline May 22, 2015 http://www.sfwinecomp.com/

New York International Wine Competition May 17-18, 2015 (Deadline for entries May 12) https://www.nyiwinecompetition.com/

© 2015 Steve Raye

Strategies

Focus, focus focus… and triage your initiatives into “must”, “should”, “could”. Make sure you do the “musts” before you do “should do” or “could do.”

Must Do Should Do

Could Do Target audience:

Be specific…demographics are important, but behavior is critical. Only spend money that gets your content in front of prospects:

Who are most likely to be interested

Can act: buy your product, tell others

Takeaways

You can compete with the existing, major players by doing a few things really, really well Wine Apps: Delectable, Vivino, Hello Vino, Wine

Searcher, wine4.me E-commerce Delivery-within-an-hour Metrics matter: Behavior tracking, performance against

goals

© 2015 Steve Raye

Contact

Steve Raye, President Bevology Inc. [email protected] +1 860-833-6272

John Beaudette, President MHW Ltd. [email protected] +1 51-869-5970

Sid Patel, President Beverage Trade Network [email protected] +1 410-300-6597