PECAN ROUNDTABLE - nutfruitcongress.org · US Kernel Exports Summary (Crop Year Basis: October to...

32

PECAN ROUNDTABLE

Transcript of PECAN ROUNDTABLE - nutfruitcongress.org · US Kernel Exports Summary (Crop Year Basis: October to...

PECAN ROUNDTABLE

IBERIA FLIGHT CHICAGO - MADRID

2

Olives and Nuts served…where are thepecans?

Presentation Agenda

1. Panel Introductions2. Estimated World Pecan Production3. US Summary Export shipments and domestic

consumption4. Global Production & Consumption Summary

• Australia• South Africa• China

5. Panel Discussion - Current trends, challenges,opportunities

6. Closing Comments7. Questions & Answers

3

Antitrust Statement: The fundamental purpose ofthis session is for the participants to discussdifferent aspects of the nut and dried fruit industry. Itis the policy and practice of the INC Foundation toconduct all its meetings and activities in strictcompliance with antitrust and competition laws.There shall be no discussions of competitivelysensitive information, including but not limited toprices, rates, coverage, market practices, claimssettlement practices, customers or any othercompetitive aspect of an individual company’soperation. INC participants to this meeting commitnot to enter into any agreements betweenundertakings, decisions by associations orundertakings and concerted practices which mayaffect trade and which have as their object or effectthe prevention, restriction or distortion of competitionwithin the internal market. Each participant isobligated to prevent any discussion from fallingoutside these bounds.

Copyright Notice: All images used in this presentation are for educational purposes only. They are either in the public domain and notsubject to copyright, or have been purchased. All images used in this presentation are the property of their respective copyright owners.

ROUNDTABLE PANELISTS

• Sally Arn – Carter Pecan, USA

• Cheng Hung Kay - CHK Trading, China-Hong Kong

• Richard Sampson Genest– Stahmann Farms, Australia

• Jill Whyte – Green and Gold Macadamias, South Africa

• Steve Zaffarano – Diamond Foods, USA

Moderator: Jeffrey Sanfilippo – John B. Sanfilippo & Son, Inc. USA

4

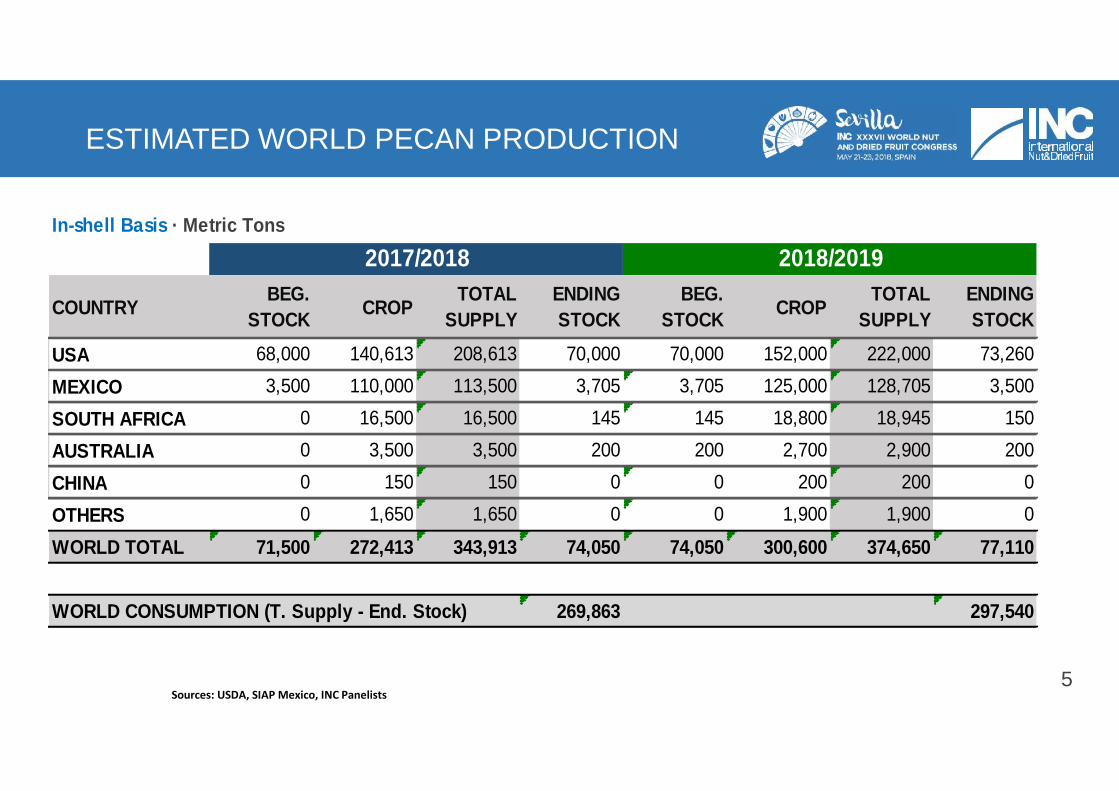

ESTIMATED WORLD PECAN PRODUCTION

5Sources: USDA, SIAP Mexico, INC Panelists

In-shell Basis · Metric Tons

COUNTRY BEG.STOCK CROP TOTAL

SUPPLYENDINGSTOCK

BEG.STOCK CROP TOTAL

SUPPLYENDINGSTOCK

USA 68,000 140,613 208,613 70,000 70,000 152,000 222,000 73,260

MEXICO 3,500 110,000 113,500 3,705 3,705 125,000 128,705 3,500

SOUTH AFRICA 0 16,500 16,500 145 145 18,800 18,945 150

AUSTRALIA 0 3,500 3,500 200 200 2,700 2,900 200

CHINA 0 150 150 0 0 200 200 0

OTHERS 0 1,650 1,650 0 0 1,900 1,900 0

WORLD TOTAL 71,500 272,413 343,913 74,050 74,050 300,600 374,650 77,110

WORLD CONSUMPTION (T. Supply - End. Stock) 269,863 297,540

2017/2018 2018/2019

ESTIMATED WORLD PECAN PRODUCTION

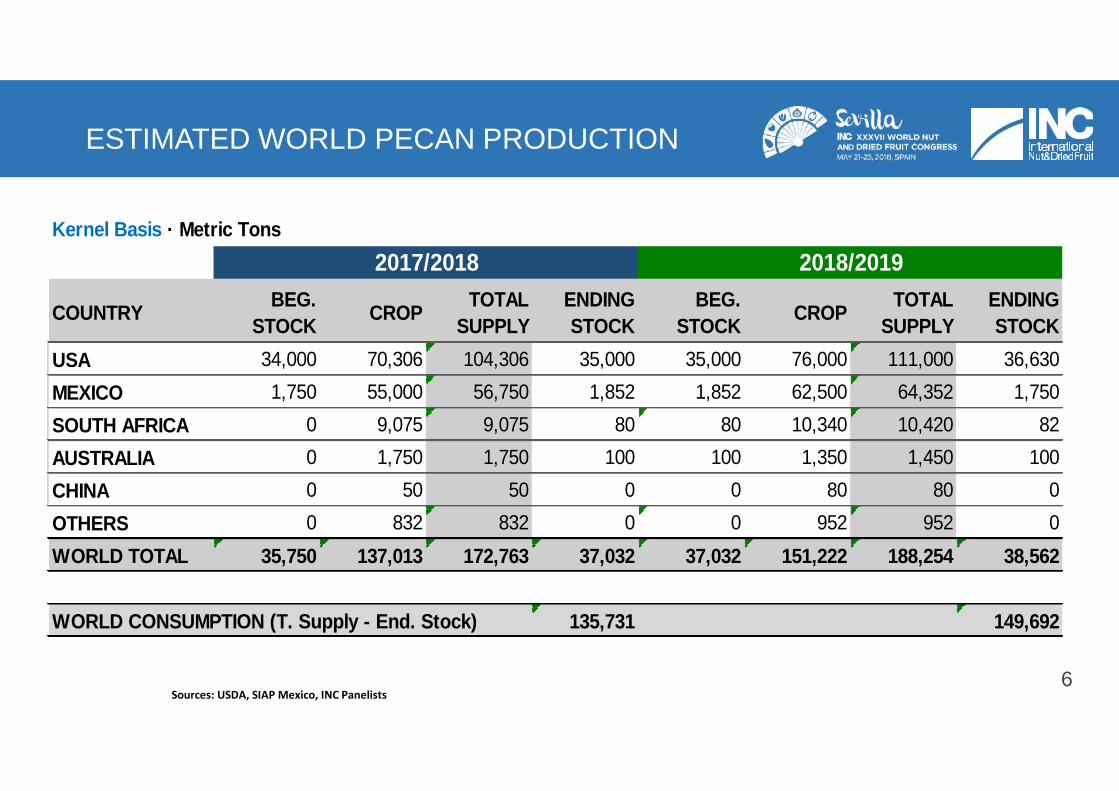

6Sources: USDA, SIAP Mexico, INC Panelists

Kernel Basis · Metric Tons

COUNTRY BEG.STOCK CROP TOTAL

SUPPLYENDINGSTOCK

BEG.STOCK CROP TOTAL

SUPPLYENDINGSTOCK

USA 34,000 70,306 104,306 35,000 35,000 76,000 111,000 36,630MEXICO 1,750 55,000 56,750 1,852 1,852 62,500 64,352 1,750SOUTH AFRICA 0 9,075 9,075 80 80 10,340 10,420 82AUSTRALIA 0 1,750 1,750 100 100 1,350 1,450 100CHINA 0 50 50 0 0 80 80 0OTHERS 0 832 832 0 0 952 952 0WORLD TOTAL 35,750 137,013 172,763 37,032 37,032 151,222 188,254 38,562

WORLD CONSUMPTION (T. Supply - End. Stock) 135,731 149,692

2017/2018 2018/2019

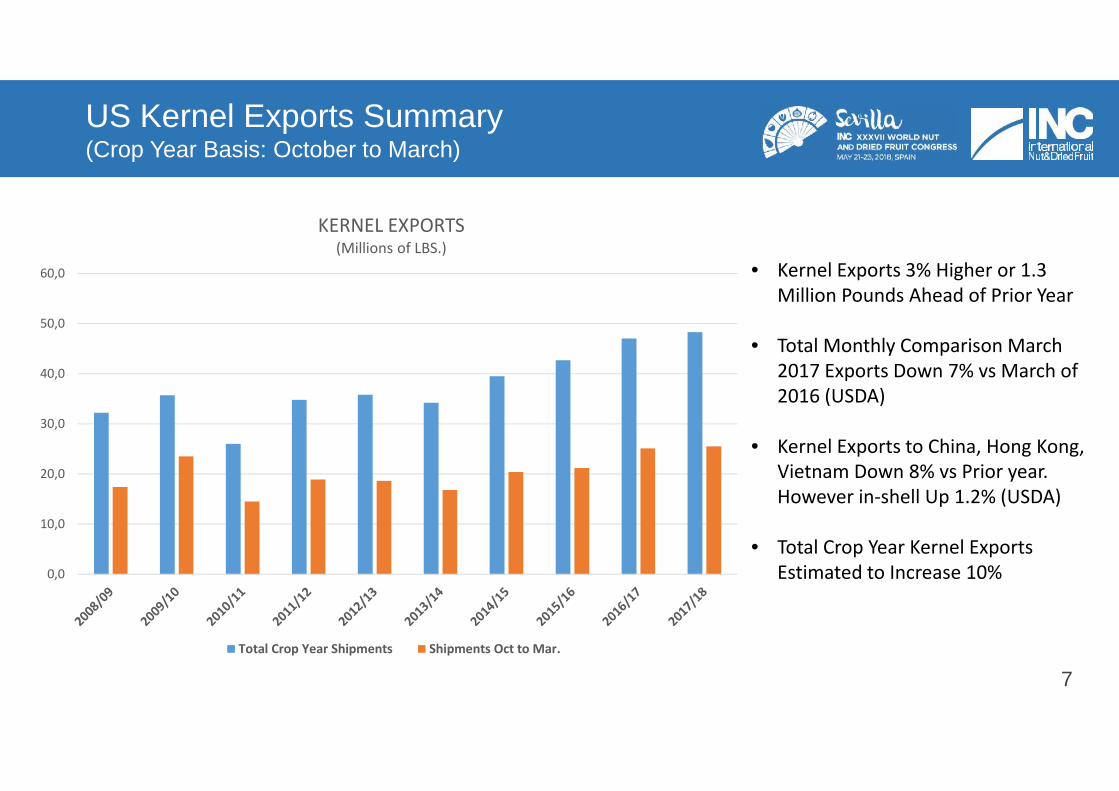

US Kernel Exports Summary(Crop Year Basis: October to March)

7

• Kernel Exports 3% Higher or 1.3Million Pounds Ahead of Prior Year

• Total Monthly Comparison March2017 Exports Down 7% vs March of2016 (USDA)

• Kernel Exports to China, Hong Kong,Vietnam Down 8% vs Prior year.However in-shell Up 1.2% (USDA)

• Total Crop Year Kernel ExportsEstimated to Increase 10%0,0

10,0

20,0

30,0

40,0

50,0

60,0

KERNEL EXPORTS(Millions of LBS.)

Total Crop Year Shipments Shipments Oct to Mar.

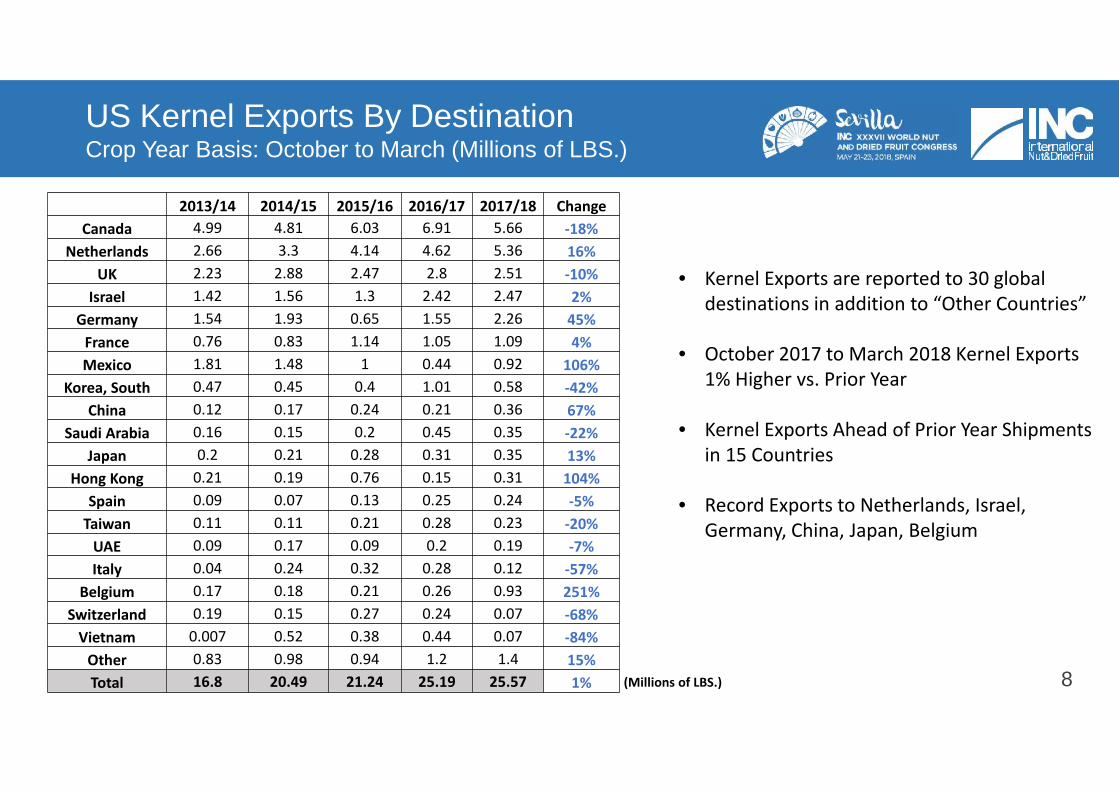

US Kernel Exports By DestinationCrop Year Basis: October to March (Millions of LBS.)

8

• Kernel Exports are reported to 30 globaldestinations in addition to “Other Countries”

• October 2017 to March 2018 Kernel Exports1% Higher vs. Prior Year

• Kernel Exports Ahead of Prior Year Shipmentsin 15 Countries

• Record Exports to Netherlands, Israel,Germany, China, Japan, Belgium

(Millions of LBS.)

2013/14 2014/15 2015/16 2016/17 2017/18 ChangeCanada 4.99 4.81 6.03 6.91 5.66 -18%

Netherlands 2.66 3.3 4.14 4.62 5.36 16%UK 2.23 2.88 2.47 2.8 2.51 -10%

Israel 1.42 1.56 1.3 2.42 2.47 2%Germany 1.54 1.93 0.65 1.55 2.26 45%

France 0.76 0.83 1.14 1.05 1.09 4%Mexico 1.81 1.48 1 0.44 0.92 106%

Korea, South 0.47 0.45 0.4 1.01 0.58 -42%China 0.12 0.17 0.24 0.21 0.36 67%

Saudi Arabia 0.16 0.15 0.2 0.45 0.35 -22%Japan 0.2 0.21 0.28 0.31 0.35 13%

Hong Kong 0.21 0.19 0.76 0.15 0.31 104%Spain 0.09 0.07 0.13 0.25 0.24 -5%

Taiwan 0.11 0.11 0.21 0.28 0.23 -20%UAE 0.09 0.17 0.09 0.2 0.19 -7%Italy 0.04 0.24 0.32 0.28 0.12 -57%

Belgium 0.17 0.18 0.21 0.26 0.93 251%Switzerland 0.19 0.15 0.27 0.24 0.07 -68%

Vietnam 0.007 0.52 0.38 0.44 0.07 -84%Other 0.83 0.98 0.94 1.2 1.4 15%Total 16.8 20.49 21.24 25.19 25.57 1%

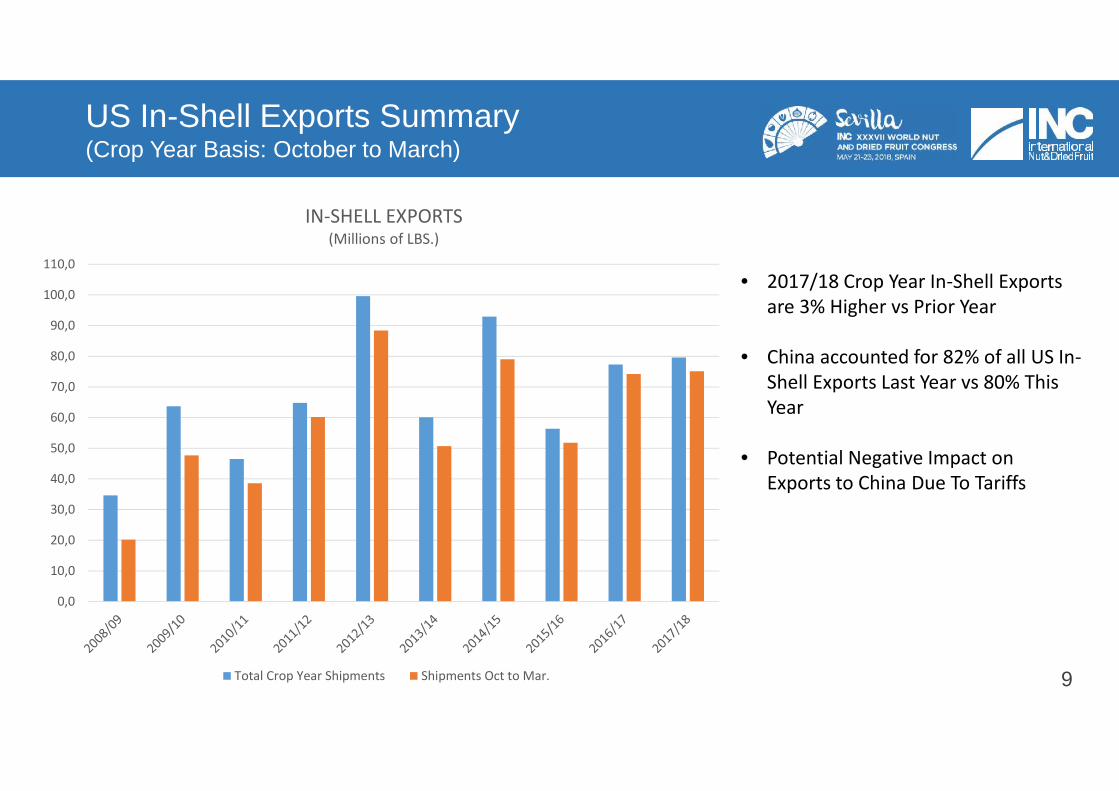

US In-Shell Exports Summary(Crop Year Basis: October to March)

9

• 2017/18 Crop Year In-Shell Exportsare 3% Higher vs Prior Year

• China accounted for 82% of all US In-Shell Exports Last Year vs 80% ThisYear

• Potential Negative Impact onExports to China Due To Tariffs

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

110,0

IN-SHELL EXPORTS(Millions of LBS.)

Total Crop Year Shipments Shipments Oct to Mar.

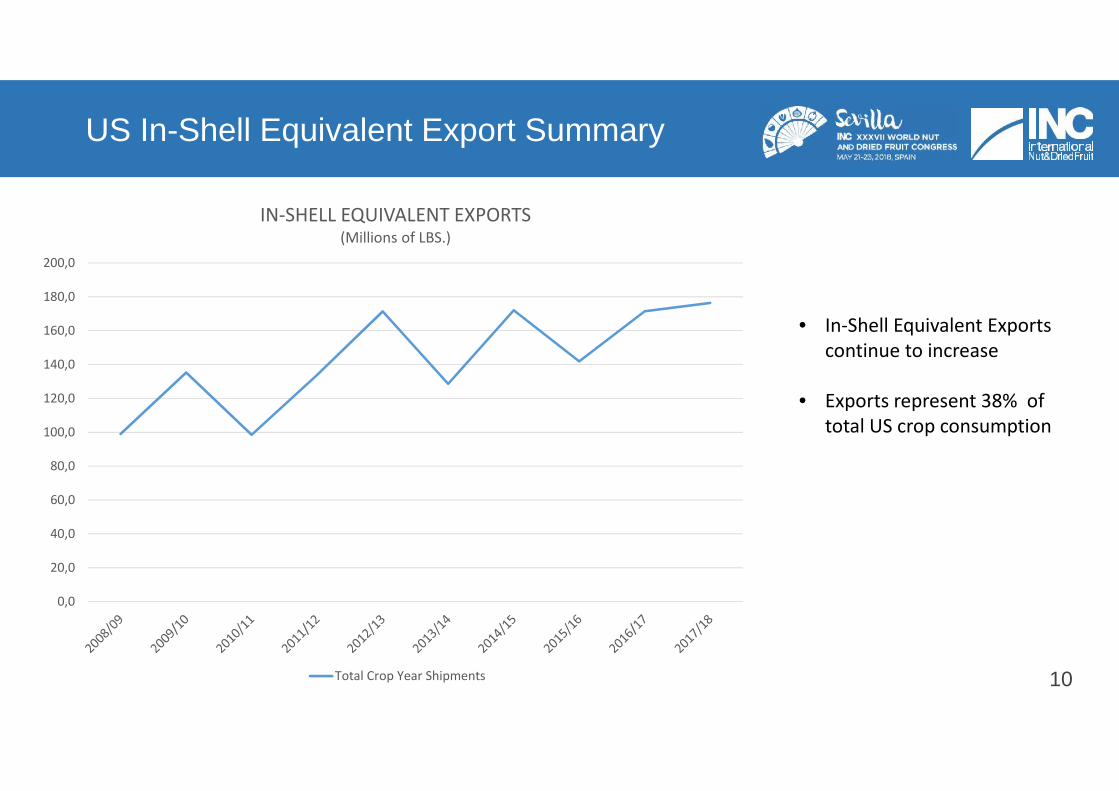

US In-Shell Equivalent Export Summary

10

• In-Shell Equivalent Exportscontinue to increase

• Exports represent 38% oftotal US crop consumption

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

200,0

IN-SHELL EQUIVALENT EXPORTS(Millions of LBS.)

Total Crop Year Shipments

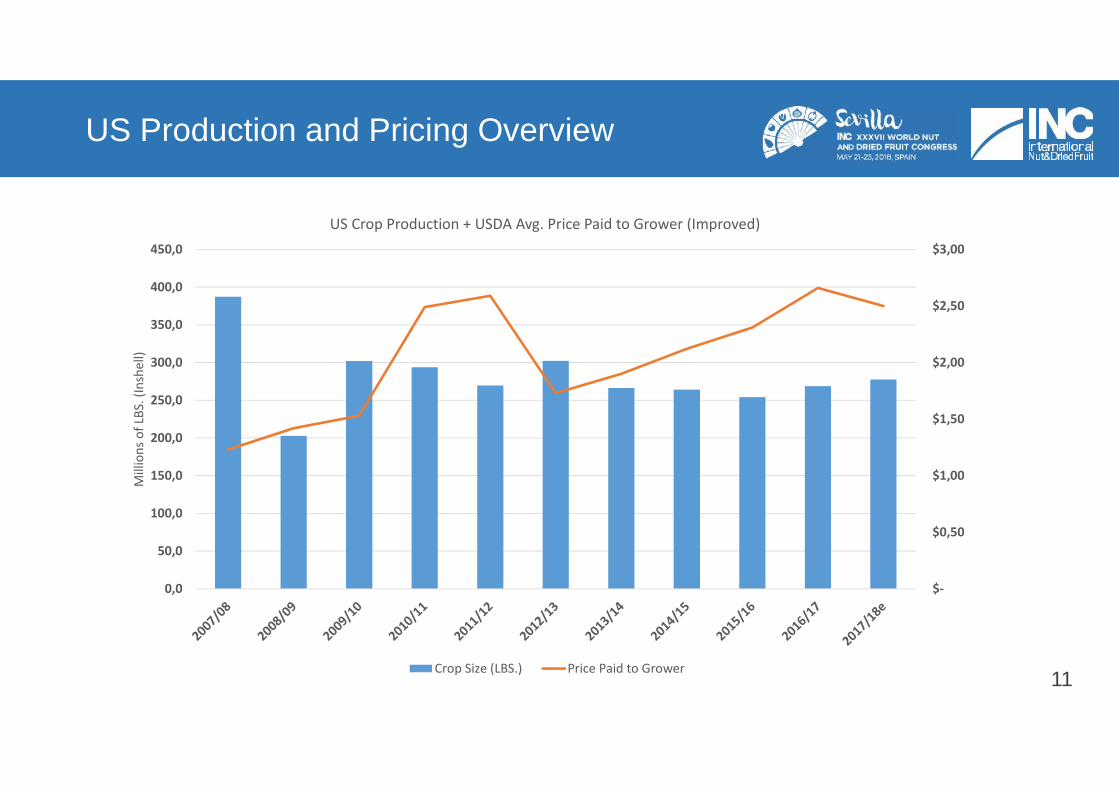

US Production and Pricing Overview

11

$-

$0,50

$1,00

$1,50

$2,00

$2,50

$3,00

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

450,0

Mill

ions

of L

BS. (

Insh

ell)

US Crop Production + USDA Avg. Price Paid to Grower (Improved)

Crop Size (LBS.) Price Paid to Grower

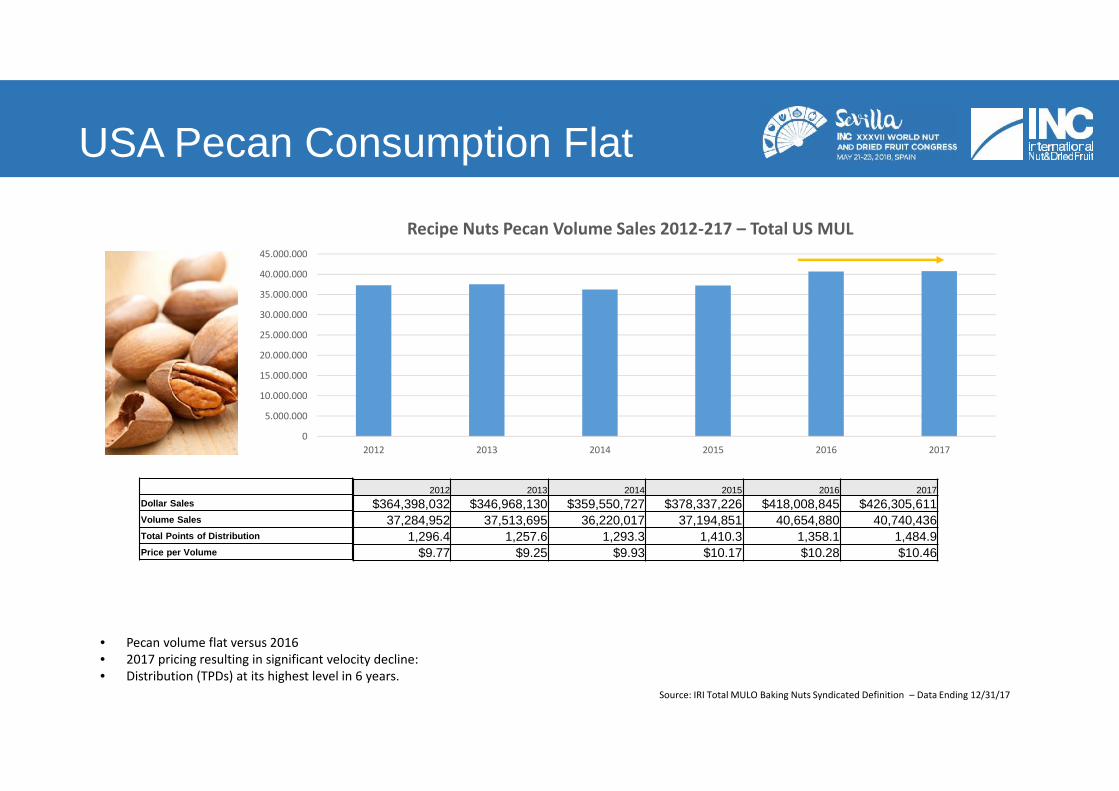

USA Pecan Consumption Flat

Source: IRI Total MULO Baking Nuts Syndicated Definition – Data Ending 12/31/17

• Pecan volume flat versus 2016• 2017 pricing resulting in significant velocity decline:• Distribution (TPDs) at its highest level in 6 years.

Dollar Sales

Volume Sales

Total Points of Distribution

Price per Volume

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

30.000.000

35.000.000

40.000.000

45.000.000

2012 2013 2014 2015 2016 2017

Recipe Nuts Pecan Volume Sales 2012-217 – Total US MUL

2012 2013 2014 2015 2016 2017$364,398,032 $346,968,130 $359,550,727 $378,337,226 $418,008,845 $426,305,611

37,284,952 37,513,695 36,220,017 37,194,851 40,654,880 40,740,4361,296.4 1,257.6 1,293.3 1,410.3 1,358.1 1,484.9

$9.77 $9.25 $9.93 $10.17 $10.28 $10.46

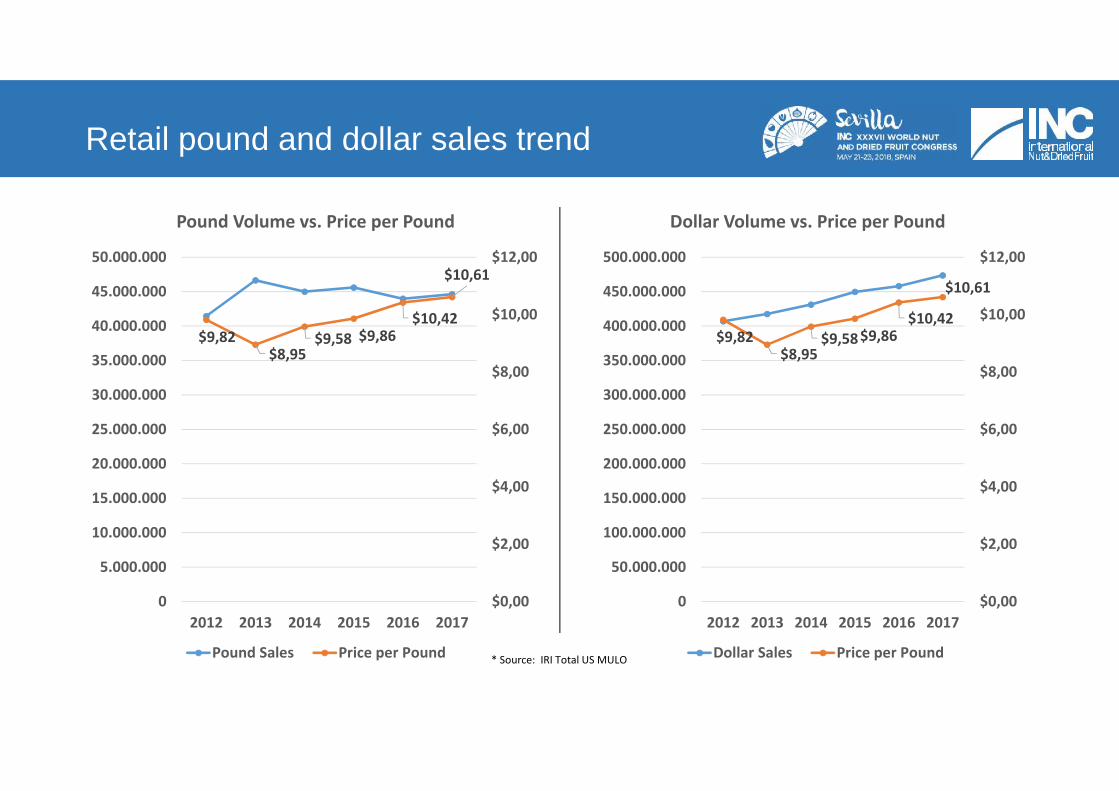

Retail pound and dollar sales trend

$9,82$8,95

$9,58 $9,86$10,42

$10,61

$0,00

$2,00

$4,00

$6,00

$8,00

$10,00

$12,00

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

30.000.000

35.000.000

40.000.000

45.000.000

50.000.000

2012 2013 2014 2015 2016 2017

Pound Volume vs. Price per Pound

Pound Sales Price per Pound * Source: IRI Total US MULO

$9,82$8,95

$9,58 $9,86$10,42

$10,61

$0,00

$2,00

$4,00

$6,00

$8,00

$10,00

$12,00

0

50.000.000

100.000.000

150.000.000

200.000.000

250.000.000

300.000.000

350.000.000

400.000.000

450.000.000

500.000.000

2012 2013 2014 2015 2016 2017

Dollar Volume vs. Price per Pound

Dollar Sales Price per Pound

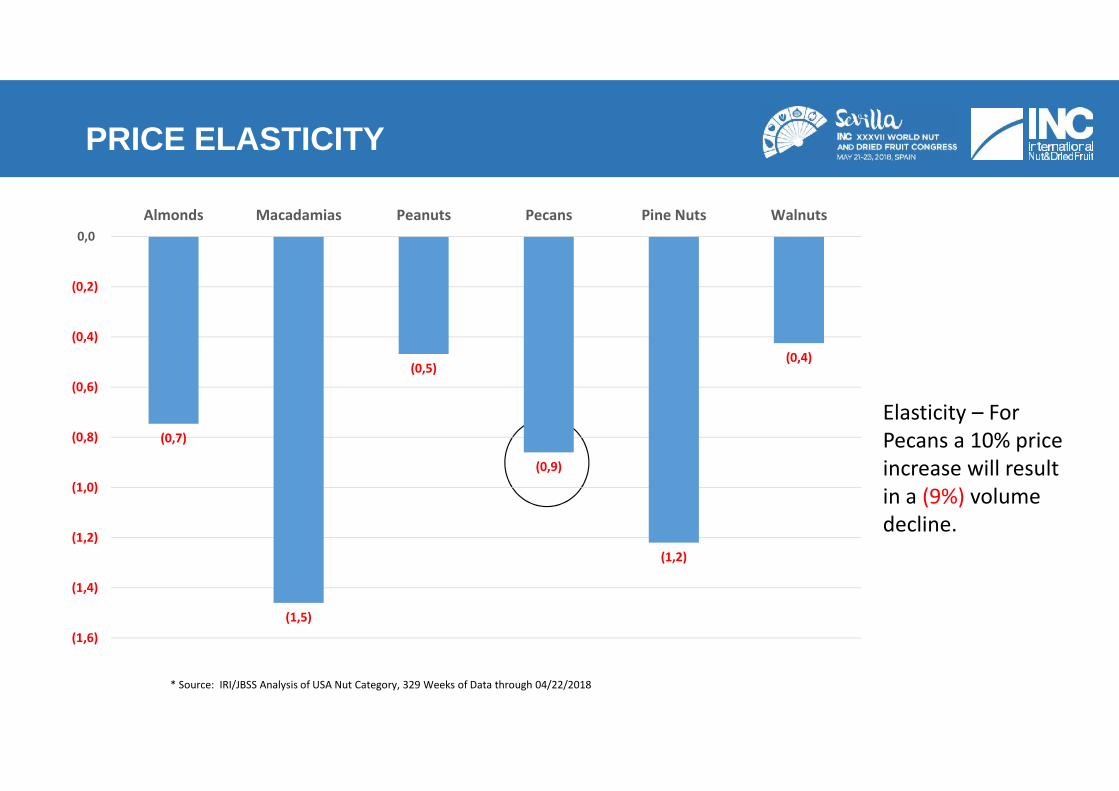

PRICE ELASTICITY

(0,7)

(1,5)

(0,5)

(0,9)

(1,2)

(0,4)

(1,6)

(1,4)

(1,2)

(1,0)

(0,8)

(0,6)

(0,4)

(0,2)

0,0Almonds Macadamias Peanuts Pecans Pine Nuts Walnuts

* Source: IRI/JBSS Analysis of USA Nut Category, 329 Weeks of Data through 04/22/2018

Elasticity – ForPecans a 10% priceincrease will resultin a (9%) volumedecline.

PROMOTION & RESEARCH

• NUTRIENTS.COM - The NPSA-fundedTufts University study, found thatincorporating pecans into a typicalAmerican diet significantly improvedinsulin sensitivity and had a significanteffect on markers of cardiometabolicdisease.

• Eating Pecans had Significant Effect onBiomarkers of Heart Disease and Type2 Diabetes

15

Can pecans protect heart health?Published Tuesday 27 March 2018By Tim Newman

PROMOTION & RESEARCH

16

AMERICAN PECAN COUNCIL

3 PROJECTS

1. Launched their Brand onApril 25

2. Created assets to tell theirstory

3. Now funding research

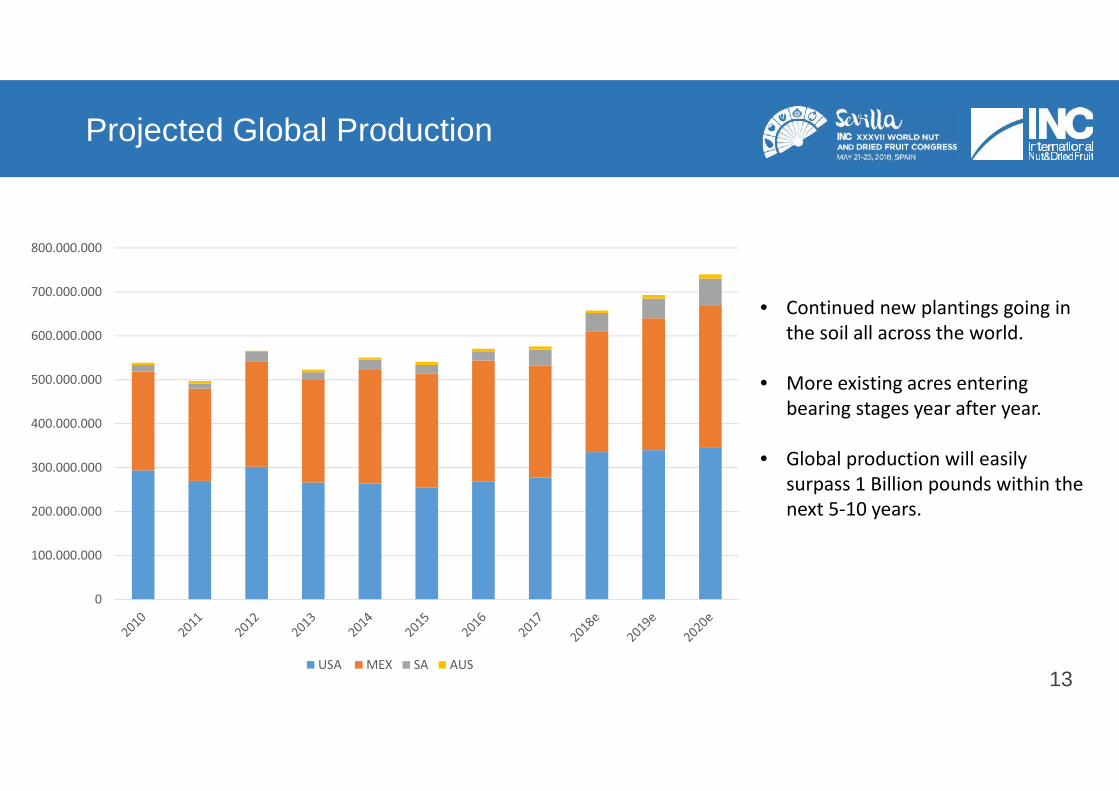

Projected Global Production

13

0

100.000.000

200.000.000

300.000.000

400.000.000

500.000.000

600.000.000

700.000.000

800.000.000

USA MEX SA AUS

• Continued new plantings going inthe soil all across the world.

• More existing acres enteringbearing stages year after year.

• Global production will easilysurpass 1 Billion pounds within thenext 5-10 years.

CHINA MARKET REVIEW

18Source: China Pecan Nut Association, CFNA

Chinese Pecan Farms in Jiangsu

Reason for Pecan Cultivation in China

19

• A typical relation between Chinese Hickory and Pecan.

• China is the origin of Hickory: ( Carya Cathayensis Sarg).

• Hickory has been lasting in China for more than 4,000 years.

• Pecan (Carya illinoensis K. Koch.) and Hickory are in the same item, family,the genus and species.

• Hickory needs at least 15-20 year to grow and have much thicker shell.

• Hickory demand outpaces supply. Every year there is a shortage.

• Pecan is considered a replacement for Hickory with a similar taste and muchshorter growing period and thin shell.

History of Pecan Cultivation in China

20

Big tree grown in 1970’sfrom seeding

Chinese Pecan Nursery

• Since the 1840’s, Pecan trees were brought by Americanmissionaries, merchants and diplomats to China as found nearchurches, residences, schools and ports alongside coastalareas.

• Between 1930’s-1970’s Pecan trees were developed asgreenery in some cities in the eastern coastal areas and YangziRiver Delta area.

• From 1980 to 2010, China established pecan farms in theEastern region with nurseries, hybrid research, trans-plants,variety cross-breading, gene bank.

• Since 2010, massive plantations set up in 13 provinces inEastern, Southwestern and Central parts of China.

Pecan Growing Areas and Size in China

21

Province Size (Hectare)

Yunnan 16,500Jiangsu 6,500Anhui 20,000Zhejiang 3,000Others*** 500Total 46,500

*** Includes Guangdong, Guangxi, Guizhou,Henan, Sichuan, Fujian,

Shandong, Jiangxi and Hunan

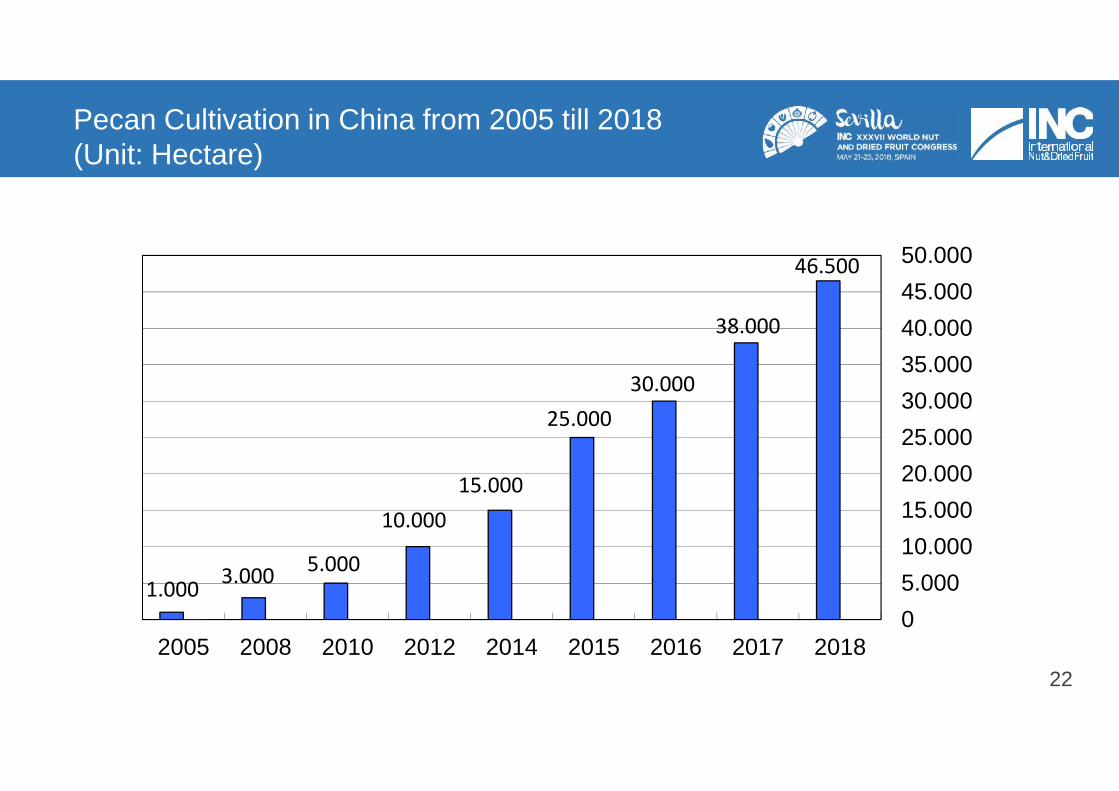

Pecan Cultivation in China from 2005 till 2018(Unit: Hectare)

22

1.000 3.000 5.000

10.00015.000

25.00030.000

38.000

46.500

05.00010.00015.00020.00025.00030.00035.00040.00045.00050.000

2005 2008 2010 2012 2014 2015 2016 2017 2018

Pecan Cultivars in China

23

Chinese Pecan Grafting

Big tree yield: 80 -100 kg/year

• Historically, over 100 U.S. cultivars were introduced to China,however, most of them were numbered and the exact namecouldn’t be known.

• More than 20 varieties are trans-planted from Australia, SouthAfrica and America such as Pawnee, Caddo, Wichita, WesternSchley, Barton, Mahan, Cheyenne, Kiowa, Cherokee, Desirable,Apache, Mohawk, Shoshoni Tejas and Shawnee in recent years.

• Mahan, Western, Tejas, Shoshoni, Wichita, Pawnee, Caddo,Shawnee could be separated and were the main cultivars cultivatedin China.

• 37 cultivars were selected by Chinese horticulturists and 2 specificvarieties are created & developed in China: Jinhua & Shaoxing

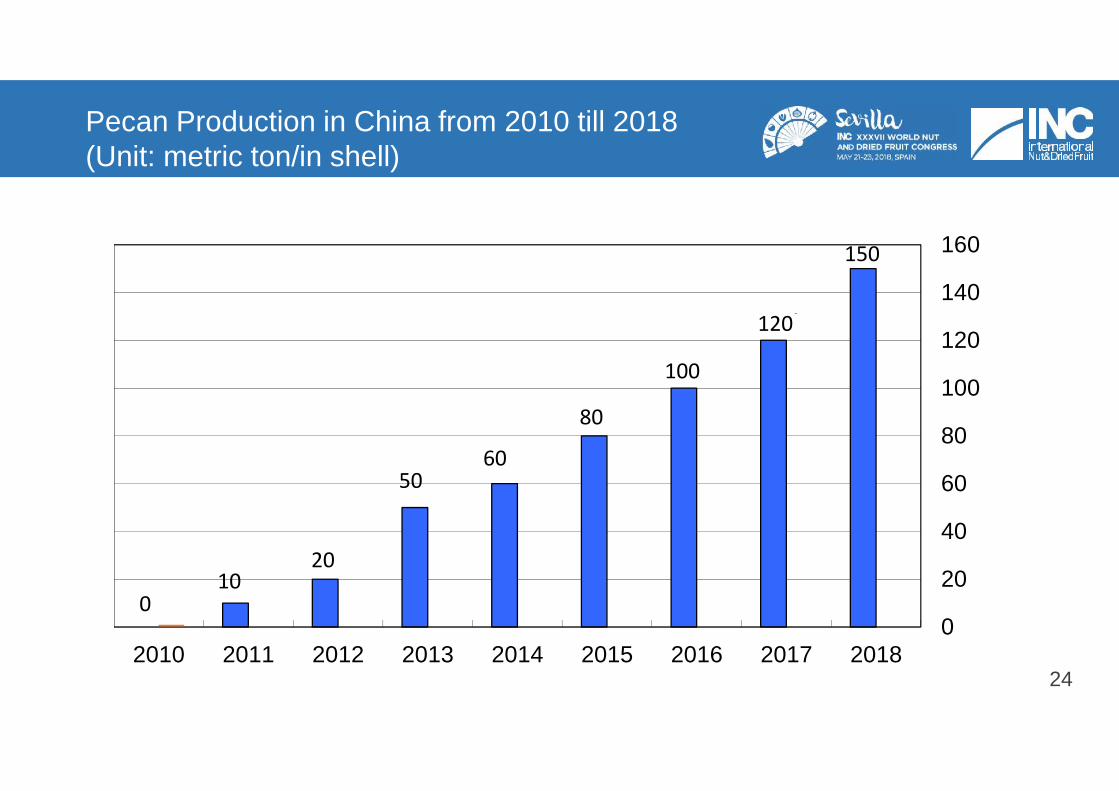

Pecan Production in China from 2010 till 2018(Unit: metric ton/in shell)

24

010

20

5060

80

100

120

150

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 2015 2016 2017 2018

.

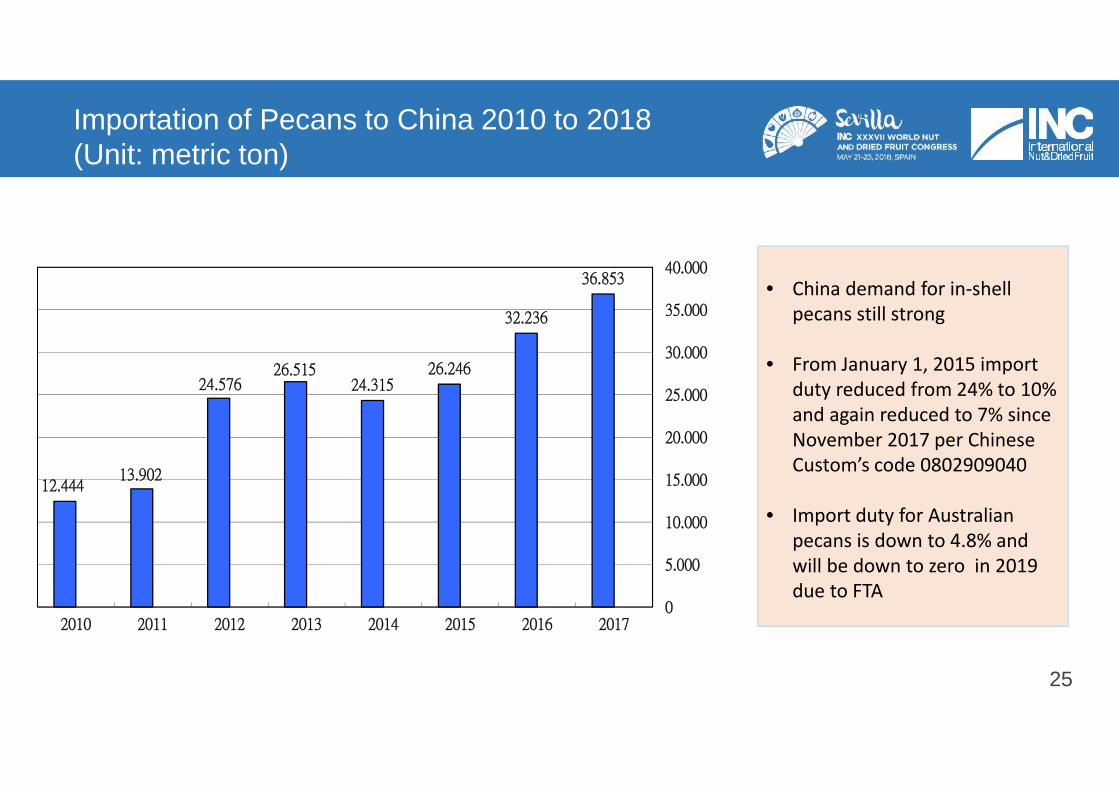

Importation of Pecans to China 2010 to 2018(Unit: metric ton)

25

12.44413.902

24.57626.515

24.31526.246

32.236

36.853

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

2010 2011 2012 2013 2014 2015 2016 2017

• China demand for in-shellpecans still strong

• From January 1, 2015 importduty reduced from 24% to 10%and again reduced to 7% sinceNovember 2017 per ChineseCustom’s code 0802909040

• Import duty for Australianpecans is down to 4.8% andwill be down to zero in 2019due to FTA

• China demand for in-shellpecans still strong

• From January 1, 2015 importduty reduced from 24% to 10%and again reduced to 7% sinceNovember 2017 per ChineseCustom’s code 0802909040

• Import duty for Australianpecans is down to 4.8% andwill be down to zero in 2019due to FTA

Closing Comments Key Highlights This Year

• Global production continues to grow

• Increase funding available and efforts have begun to invest in expandedpecan research, promotion and public awareness efforts

• Prices paid to US growers declined after four consecutive years ofincreases

• Potential trade tariffs could impact export markets

26

Panel Discussion Topics

14

• What are the crop sizes in Argentina and Peru and what new acreage is being planted?(Sally)

• What are the prospects for the South Africa crop in the coming years? (Jill)• What are the prospects for the Australia crop in the coming years? (Richard)• What are the prospects for the China crop and what do we know about the current

situation with tariffs on pecans and the potential impact? (Cheng)• How can the APC improve timing and accuracy of crop reporting? Is there a way to get

accurate crop information as it comes in, as opposed to all data coming in after the cropseason is already over? (Steve)

• The NPSA is currently working on a shelf life study to help improve industry standards.Are there any other studies you think would be beneficial to the industry? (All)

• What can be done to help promote the propagation of native pecan trees? As theproduction of this variety continues to decline, smaller pecan sizes and grades willbecome more limited. (All)

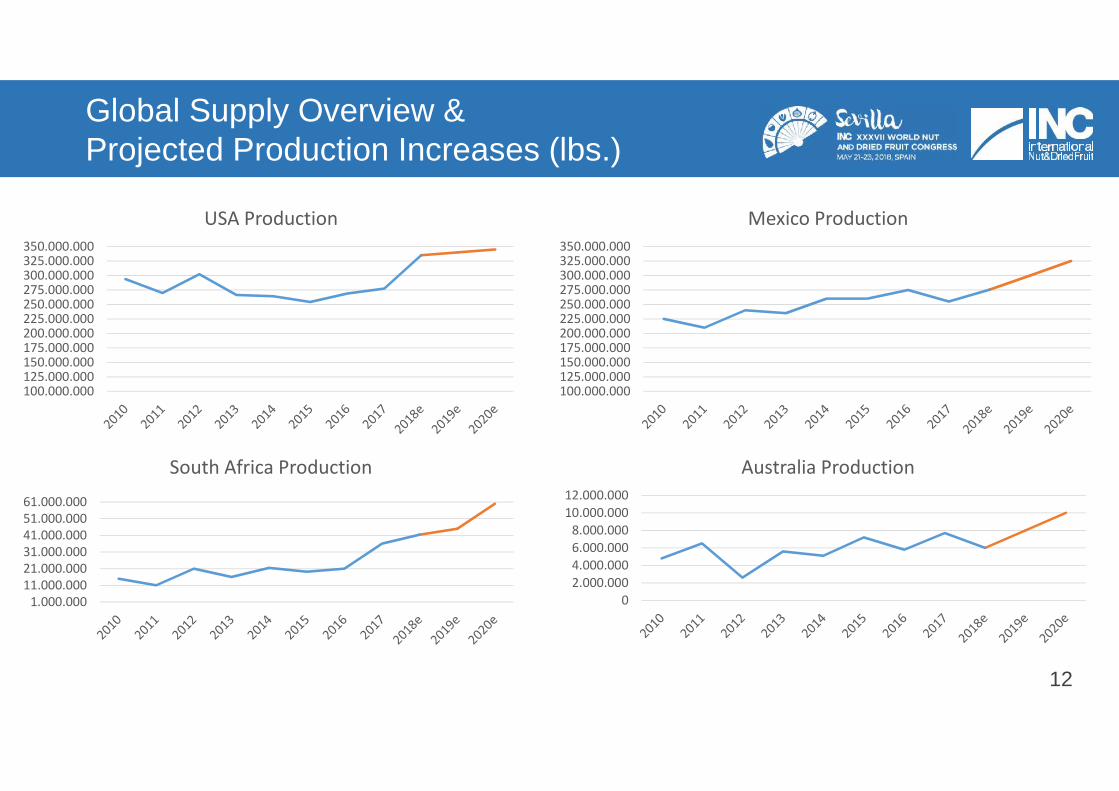

Global Supply Overview &Projected Production Increases (lbs.)

12

100.000.000125.000.000150.000.000175.000.000200.000.000225.000.000250.000.000275.000.000300.000.000325.000.000350.000.000

USA Production

100.000.000125.000.000150.000.000175.000.000200.000.000225.000.000250.000.000275.000.000300.000.000325.000.000350.000.000

Mexico Production

1.000.00011.000.00021.000.00031.000.00041.000.00051.000.00061.000.000

South Africa Production

02.000.0004.000.0006.000.0008.000.000

10.000.00012.000.000

Australia Production

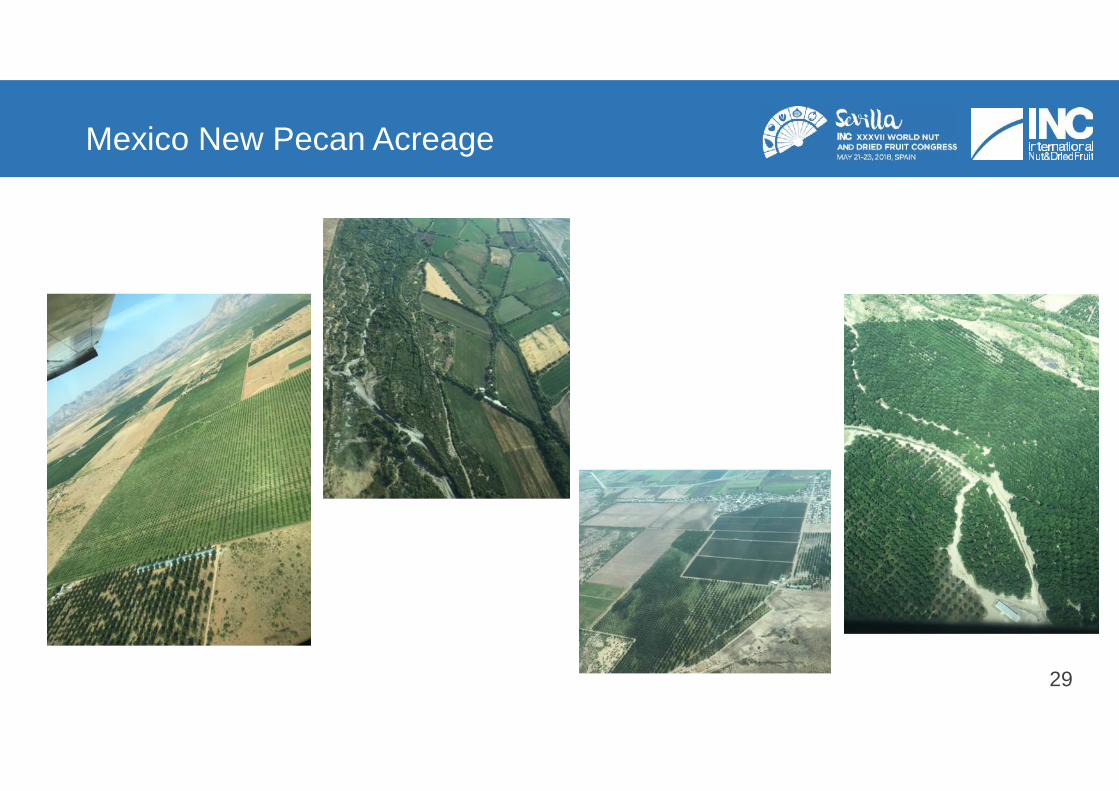

Mexico New Pecan Acreage

29

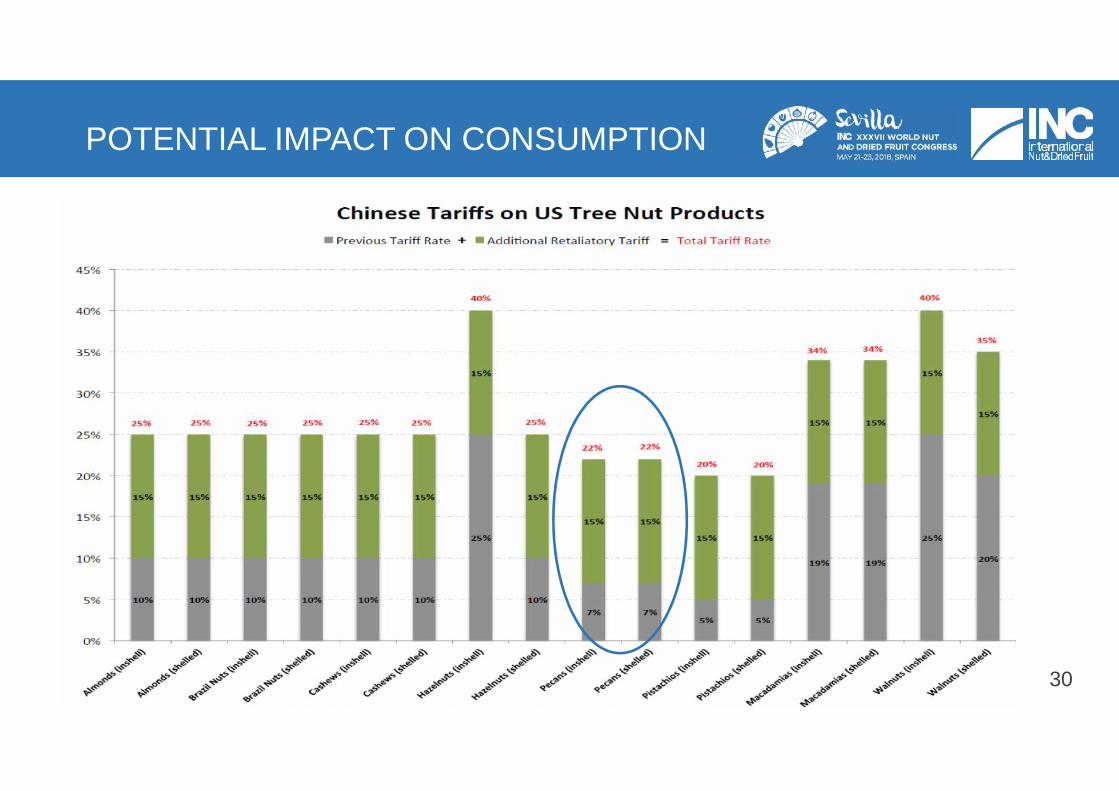

POTENTIAL IMPACT ON CONSUMPTION

30

QUESTIONS AND CLOSING COMMENTS

INC Discussion Questions From the Audience

31

PECAN ROUNDTABLE

32

Thank YouGraciasDankie谢谢