Payroll2015

44

PAYROLL LAW WELCOME! Your Facilitator Today is Lisa Smith

-

Upload

smithpayroll -

Category

Business

-

view

80 -

download

0

Transcript of Payroll2015

PAYROLL LAW

WELCOME!

Your Facilitator Today is Lisa

Smith

F. O. G.

If you wanna catch the smart fish, you gotta use the Smart Bait!

- Joe Phillips

The Best Practices Policies and Procedures

Desk References

Professional Resources

Government Resources

Rule of 3s

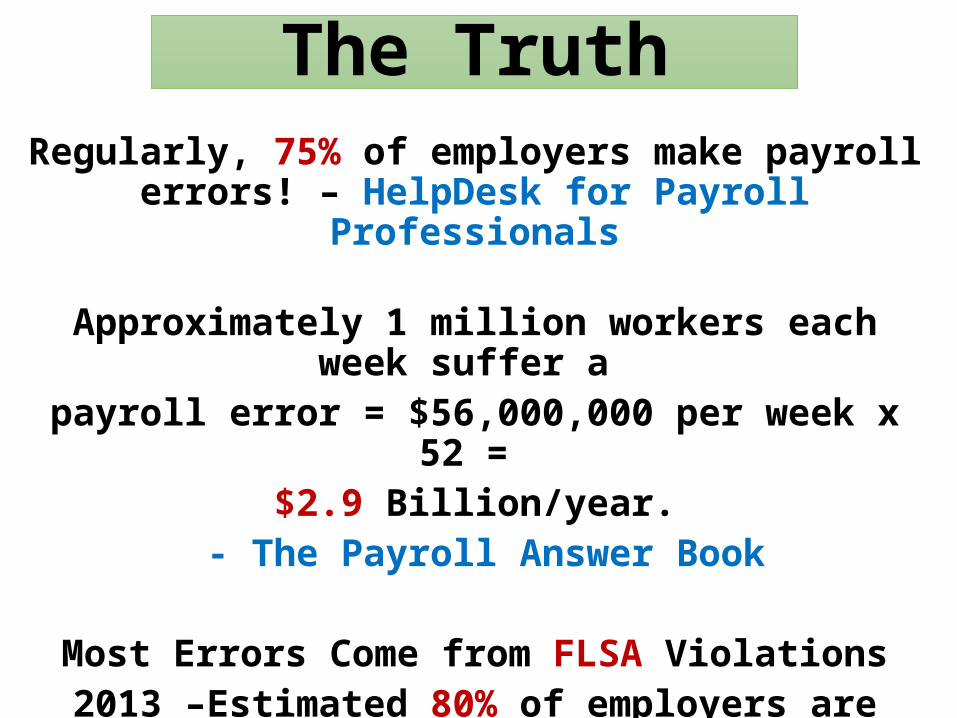

The TruthRegularly, 75% of employers make payroll errors! –

HelpDesk for Payroll Professionals

Approximately 1 million workers each week suffer a payroll error = $56,000,000 per week x 52 =

$2.9 Billion/year. - The Payroll Answer Book

Most Errors Come from FLSA Violations2013 –Estimated 80% of employers are getting it wrong.

- Department of Labor

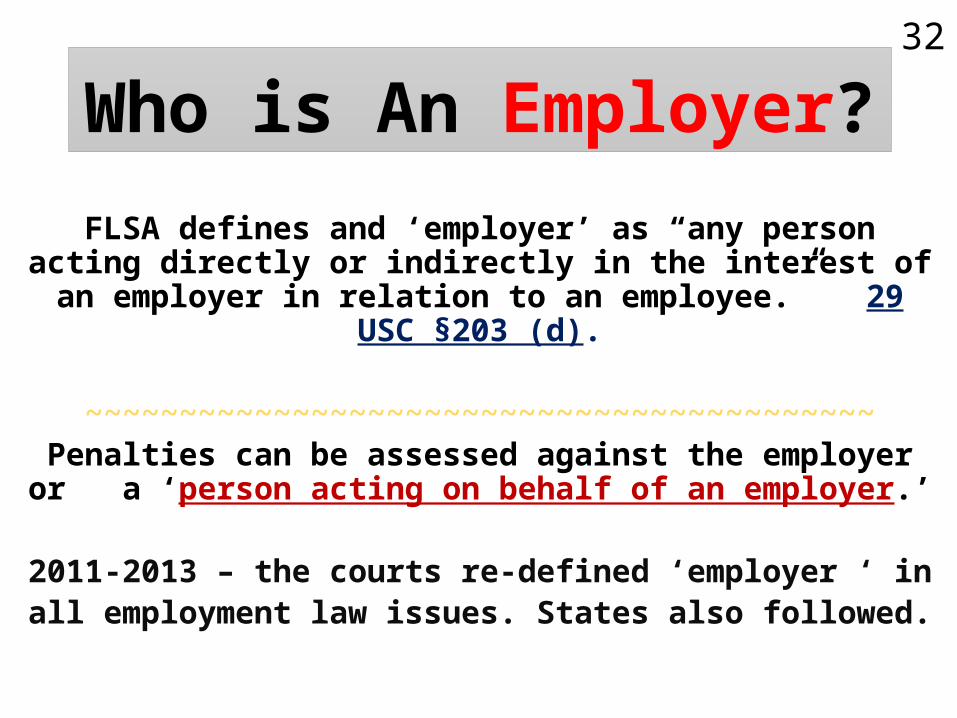

Who is An Employer?FLSA defines and ‘employer’ as “any person acting directly or

indirectly in the interest of an employer in relation to an employee.” 29 USC §203 (d).

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~Penalties can be assessed against the employer or a ‘person

acting on behalf of an employer.’

2011-2013 – the courts re-defined ‘employer ‘ in all employment law issues. States also followed.

32

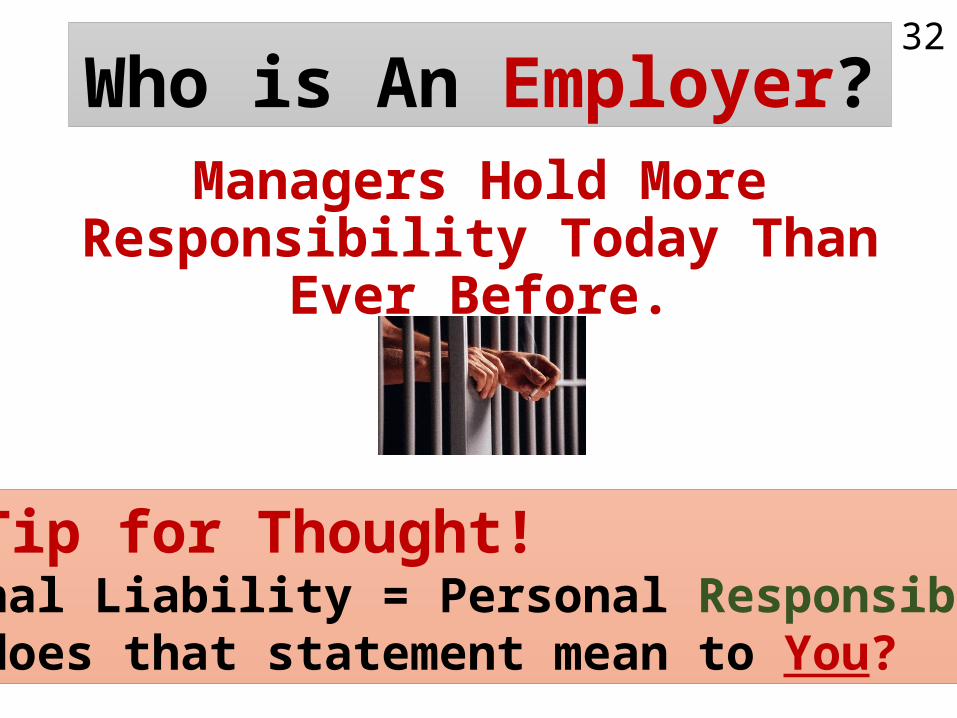

Who is An Employer?Managers Hold More Responsibility

Today Than Ever Before.

32

Hot Tip for Thought! Personal Liability = Personal Responsibility.What does that statement mean to You?

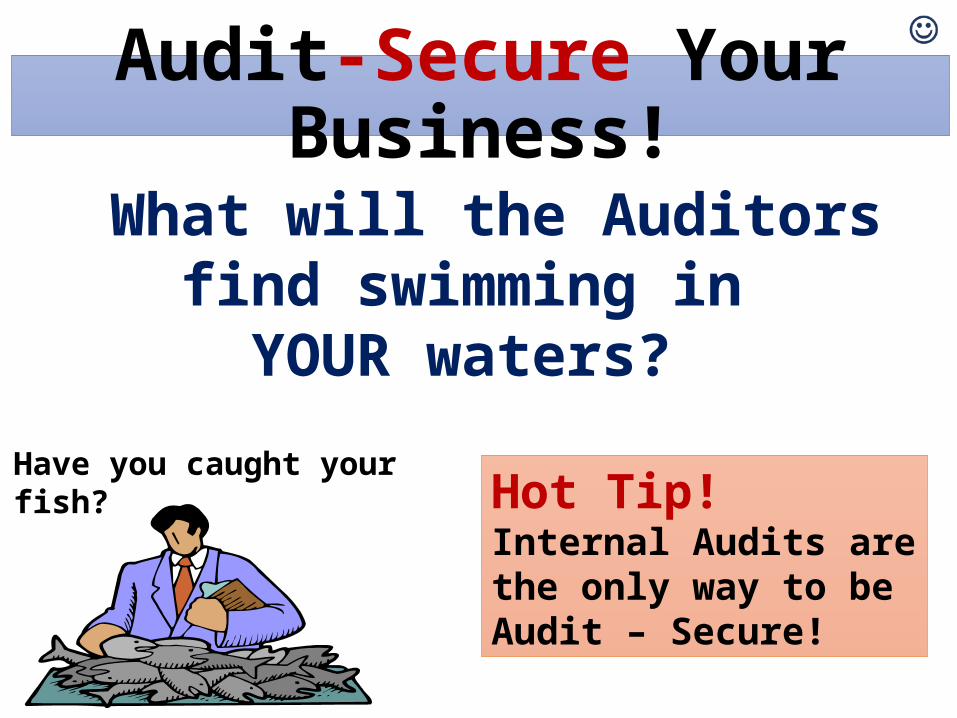

Audit-Secure Your Business!

What will the Auditors find swimming in

YOUR waters?

Have you caught your fish? Hot Tip!

Internal Audits are the only way to be Audit – Secure!

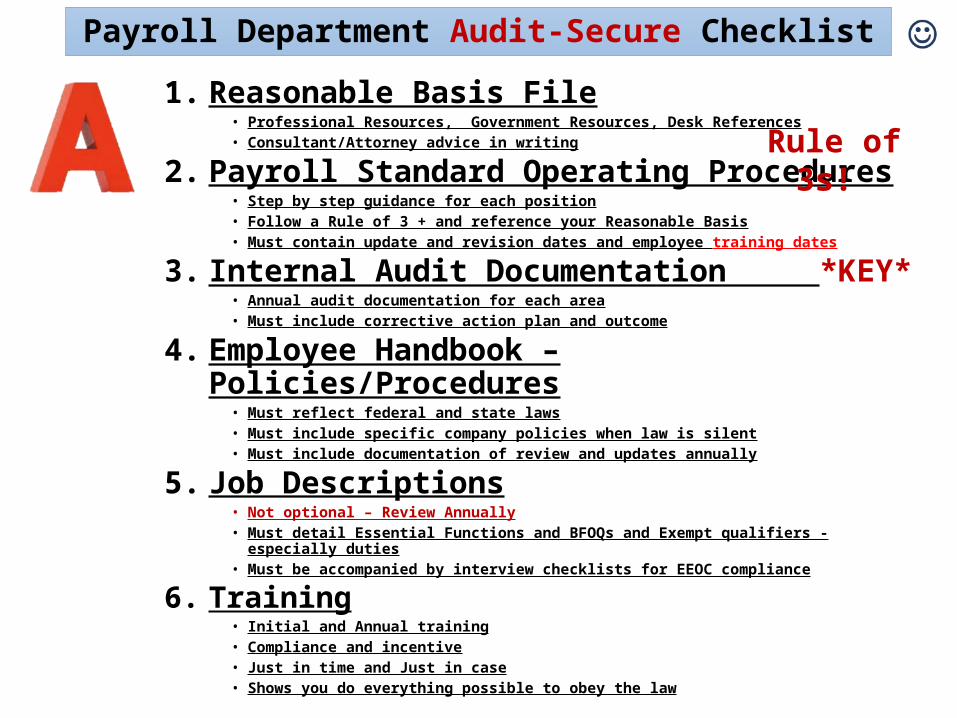

Payroll Department Audit-Secure Checklist

1. Reasonable Basis File• Professional Resources, Government Resources, Desk References• Consultant/Attorney advice in writing

2. Payroll Standard Operating Procedures• Step by step guidance for each position• Follow a Rule of 3 + and reference your Reasonable Basis• Must contain update and revision dates and employee training dates

3. Internal Audit Documentation *KEY*• Annual audit documentation for each area• Must include corrective action plan and outcome

4. Employee Handbook – Policies/Procedures• Must reflect federal and state laws• Must include specific company policies when law is silent• Must include documentation of review and updates annually

5. Job Descriptions• Not optional – Review Annually• Must detail Essential Functions and BFOQs and Exempt qualifiers - especially duties• Must be accompanied by interview checklists for EEOC compliance

6. Training• Initial and Annual training• Compliance and incentive• Just in time and Just in case• Shows you do everything possible to obey the law

Rule of 3s!

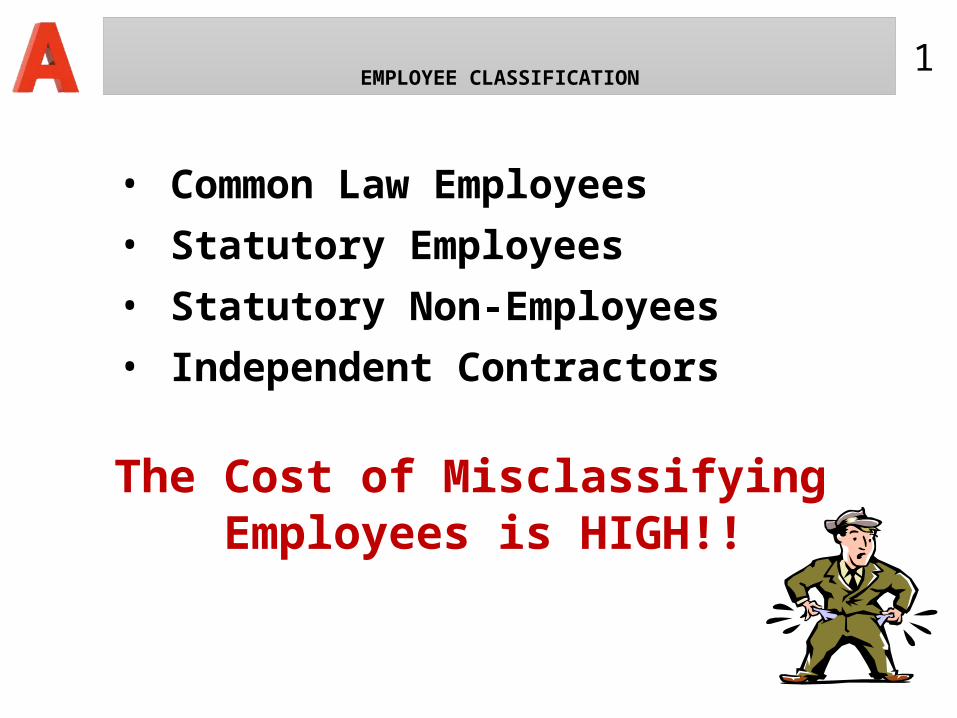

EMPLOYEE CLASSIFICATION

• Common Law Employees

• Statutory Employees

• Statutory Non-Employees

• Independent Contractors

The Cost of Misclassifying Employees is HIGH!!

1

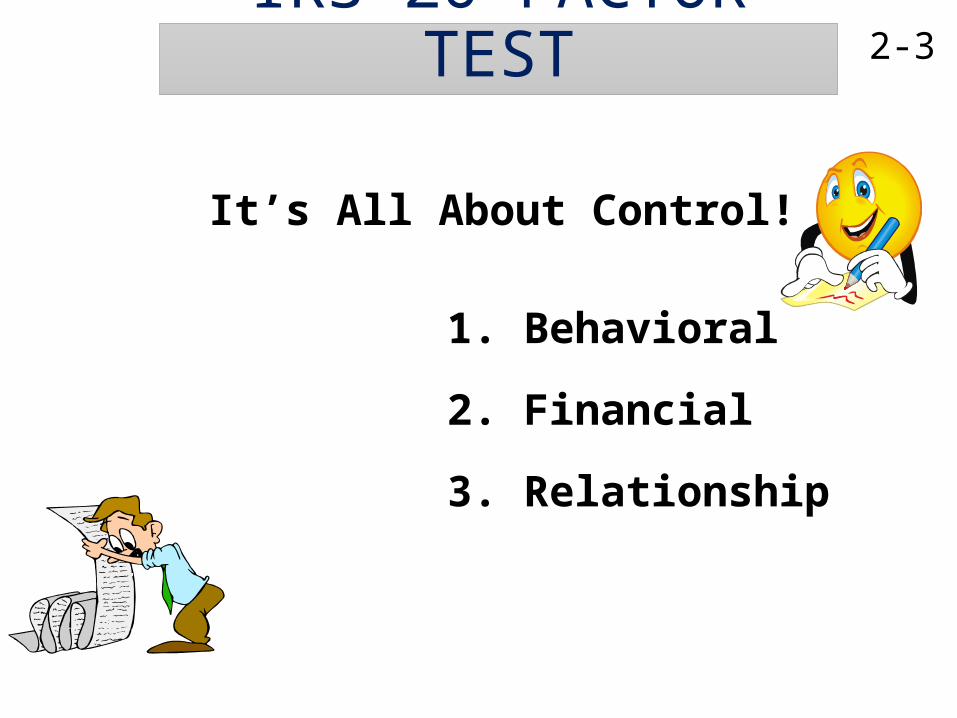

Employee vs.

Independent Contractor

#1 Most Audited Area!

IRS 20 FACTOR TEST

It’s All About Control!

1. Behavioral

2. Financial

3. Relationship

2-3

ABC TEST

A. Control or Direction of the WorkB. Outside Service

C. Independent Business or Trade

4-5

Audit-Secure Tips • Create your own checklist.• Conduct an internal audit.• Document self-corrections.• Create SOP• Train Payroll, HR and A/P

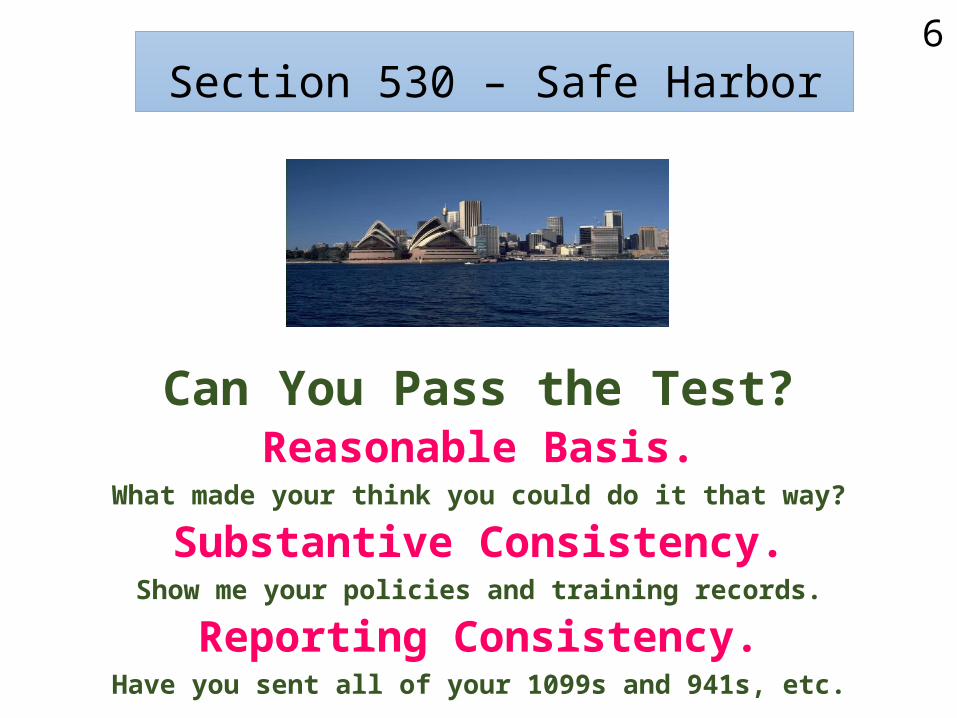

Section 530 – Safe Harbor

Can You Pass the Test?Reasonable Basis.

What made your think you could do it that way?

Substantive Consistency.Show me your policies and training records.

Reporting Consistency.Have you sent all of your 1099s and 941s, etc.

6

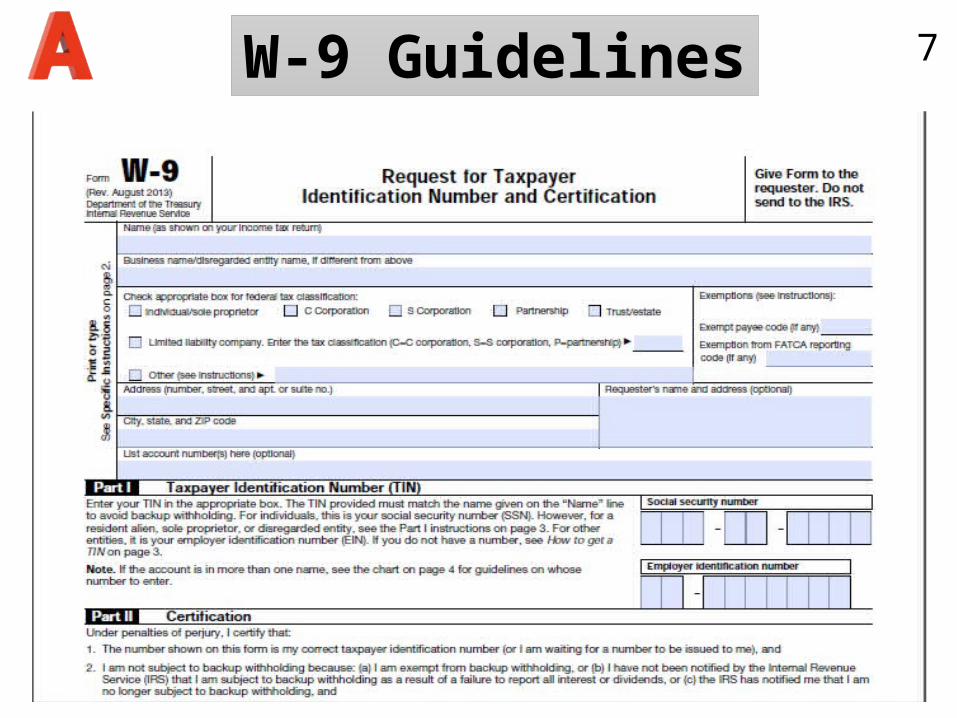

W-9 Guidelines 7

W-9 Guidelines 7

Audit-Secure Tips• Have a No Pay Policy!

• Create a Contractor Information Sheet

• Create a Standard Operating Procedure

• Train all applicable employees

1099 – MISC Reporting< $600 or more

< Used for Non-incorporated Businesses

< Always Report Attorney Fees – > $600 and Inc.

< Payments Made to Healthcare providers > $600 and Inc.

NOT 3rd Party Payers!

< Payments made for the purchase of fish to anyone engaged in the fish catching industry.

BOTTOM LINEIt is better to send too many 1099s than too few!

Sending ZERO 1099’s = $10,000 Fine!

9

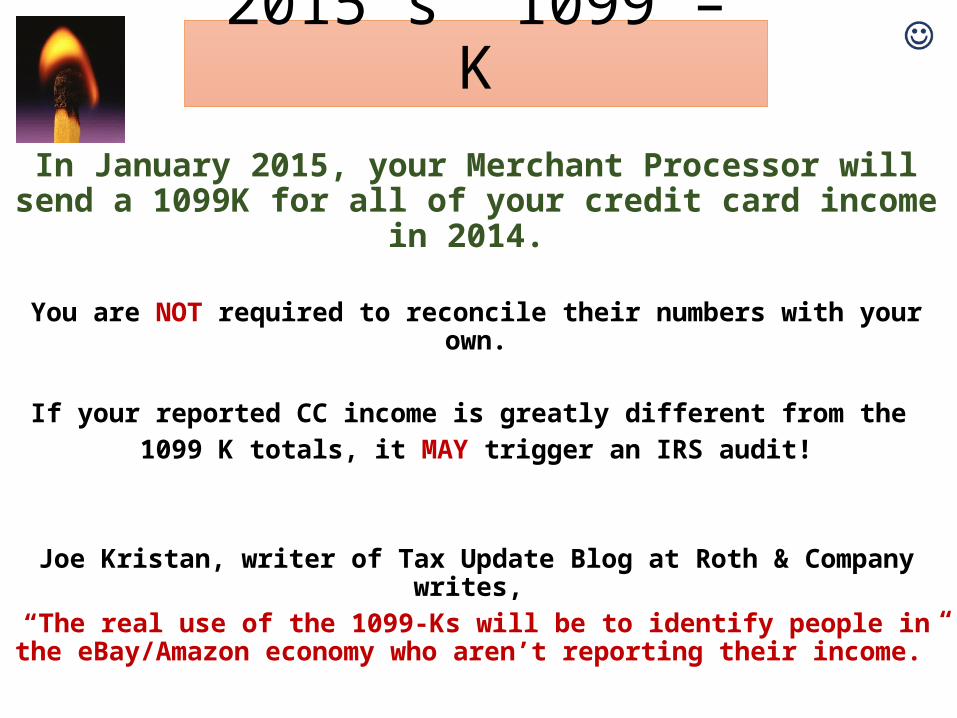

2015’s 1099 – K

In January 2015, your Merchant Processor will send a 1099K for all of your credit card income in 2014.

You are NOT required to reconcile their numbers with your own.

If your reported CC income is greatly different from the 1099 K totals, it MAY trigger an IRS audit!

Joe Kristan, writer of Tax Update Blog at Roth & Company writes, “The real use of the 1099-Ks will be to identify people in the eBay/Amazon economy who aren’t reporting their income.”

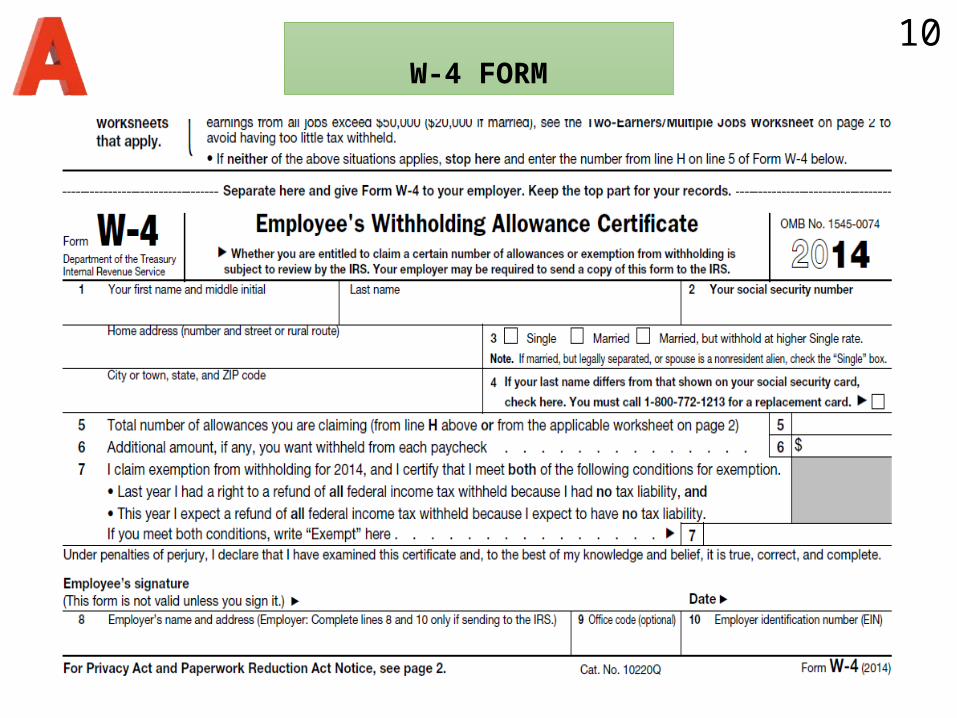

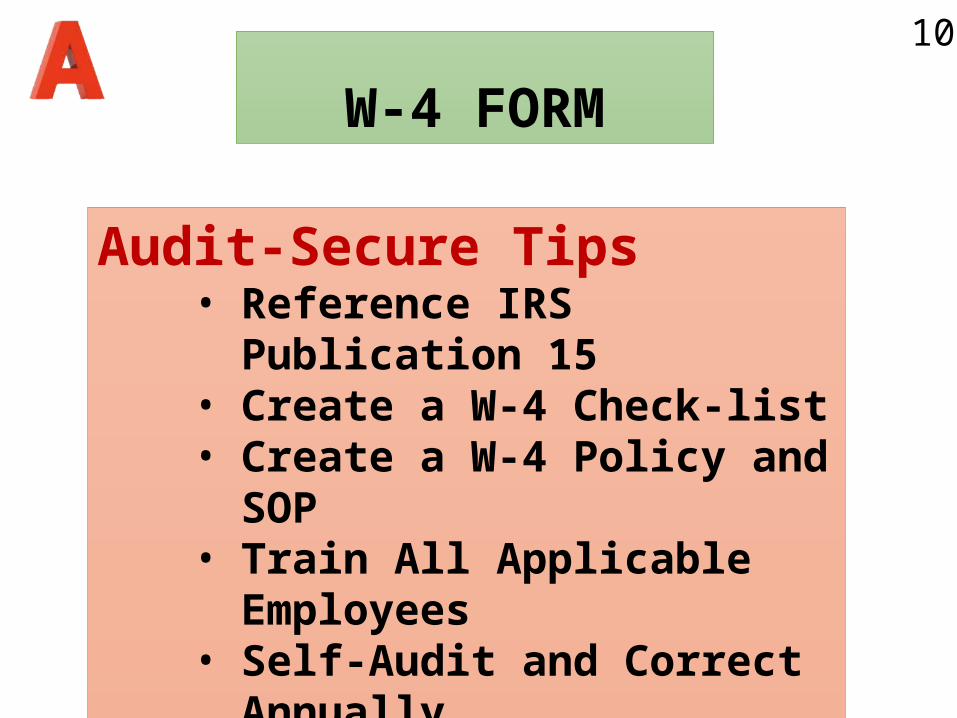

W-4 FORM10

W-4 FORM10

Audit-Secure Tips• Reference IRS Publication 15• Create a W-4 Check-list• Create a W-4 Policy and SOP• Train All Applicable Employees• Self-Audit and Correct Annually

THE NON-EXEMPT EMPLOYEE

“You ain’t gotta go home – But, You can’t stay HERE!!”

Non-Exempt = Minimum Wage and Overtime

26-31

ConsiderDOL v. Amish Cabinet Making Factory

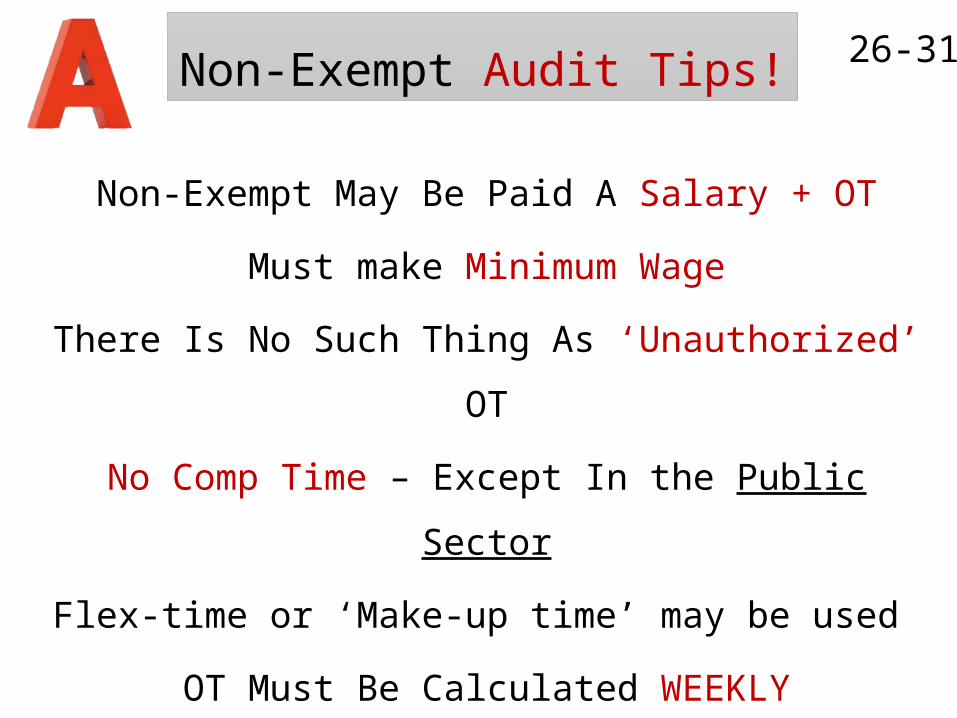

Non-Exempt Audit Tips!

Non-Exempt May Be Paid A Salary + OT

Must make Minimum Wage

There Is No Such Thing As ‘Unauthorized’ OT

No Comp Time – Except In the Public Sector

Flex-time or ‘Make-up time’ may be used

OT Must Be Calculated WEEKLY

26-31

WHAT IS WORK?

Rounding, Adjustments, and Long Punching5/6 or 7/8 Minute Rule

Lectures / Meetings / TrainingSome Are / Some Aren’t

Unauthorized Work? Does It Exist?

On Call PayEngaged to Wait OR Waiting to Engage?

29-32

E-Verify and New Hire Reporting HOT TIPS

Verify All SS#s @ www.ssa.gov to mismatch letters

Mandatory for Government Contractorswww.USCIS.gov for E-Verify Program

States Dictate How New Hires Are ReportedSee Page 54 Appendix By State

11

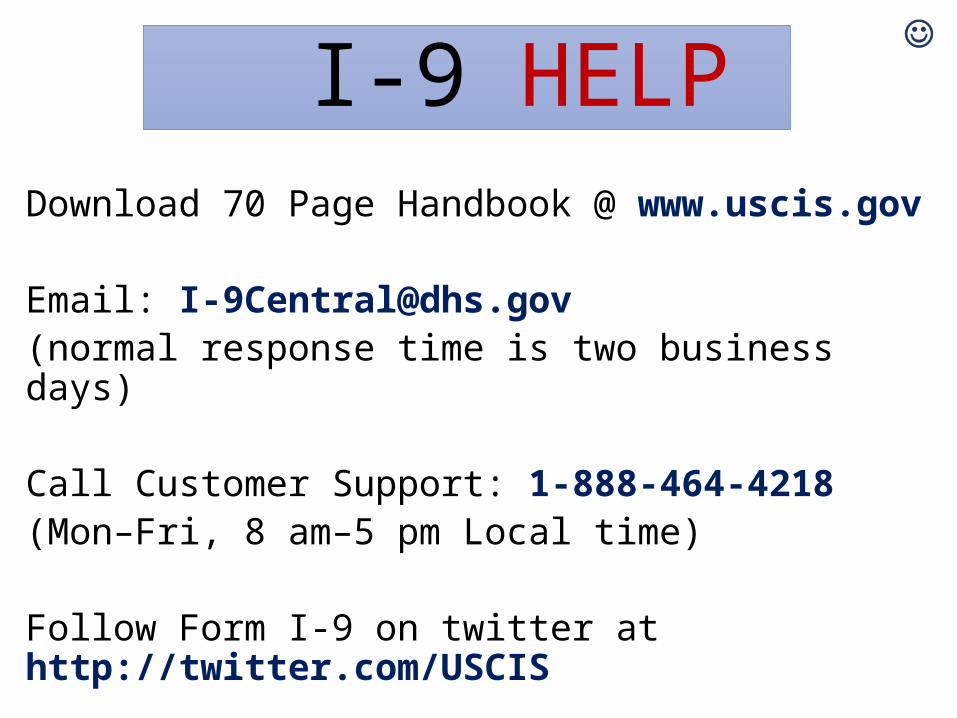

I-9 HELPDownload 70 Page Handbook @ www.uscis.gov

Email: [email protected] (normal response time is two business days) Call Customer Support: 1-888-464-4218 (Mon–Fri, 8 am–5 pm Local time) Follow Form I-9 on twitter at http://twitter.com/USCIS

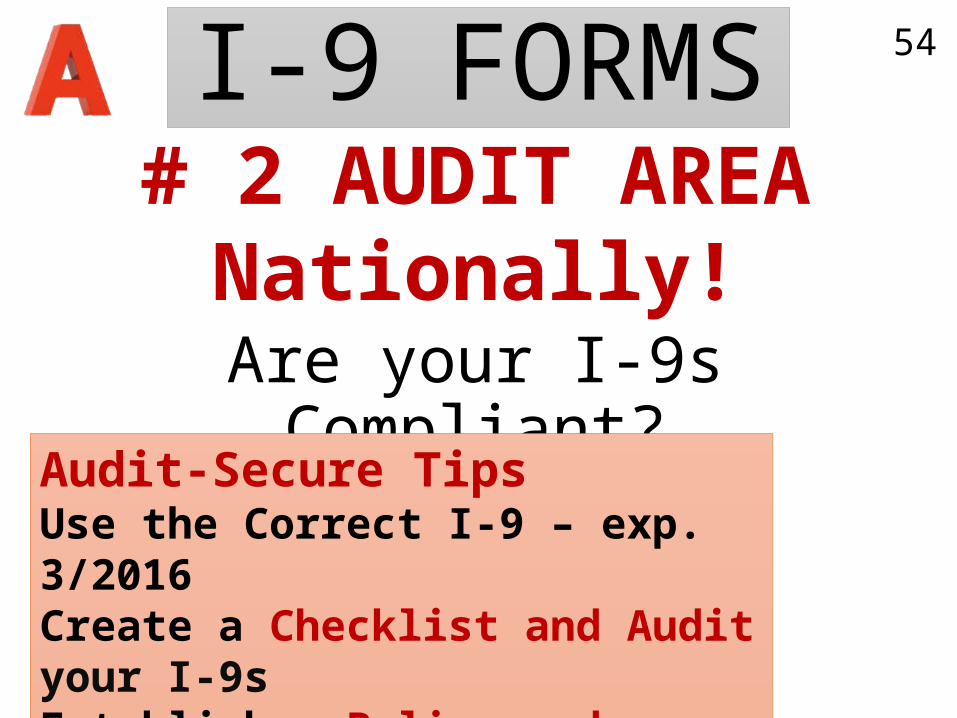

I-9 FORMS# 2 AUDIT AREA

Nationally!Are your I-9s Compliant?

54

Audit-Secure TipsUse the Correct I-9 – exp. 3/2016Create a Checklist and Audit your I-9sEstablish a Policy and ProcedureTrain and Keep Records

2382

Platinum Package

Build your own pack if you like!4+ items = Special Pricing.

3 Payments

Trainer Bonus Gifts with any order placed today

SOP Development GuideWith samples of W-4 SOP and others

Affordable Care Act UpdatesTwo documents – Total 17 pages of updates/checklists

Internal Audit ChecklistsW-4 and ABC Checklists

PTO Policy Front loading

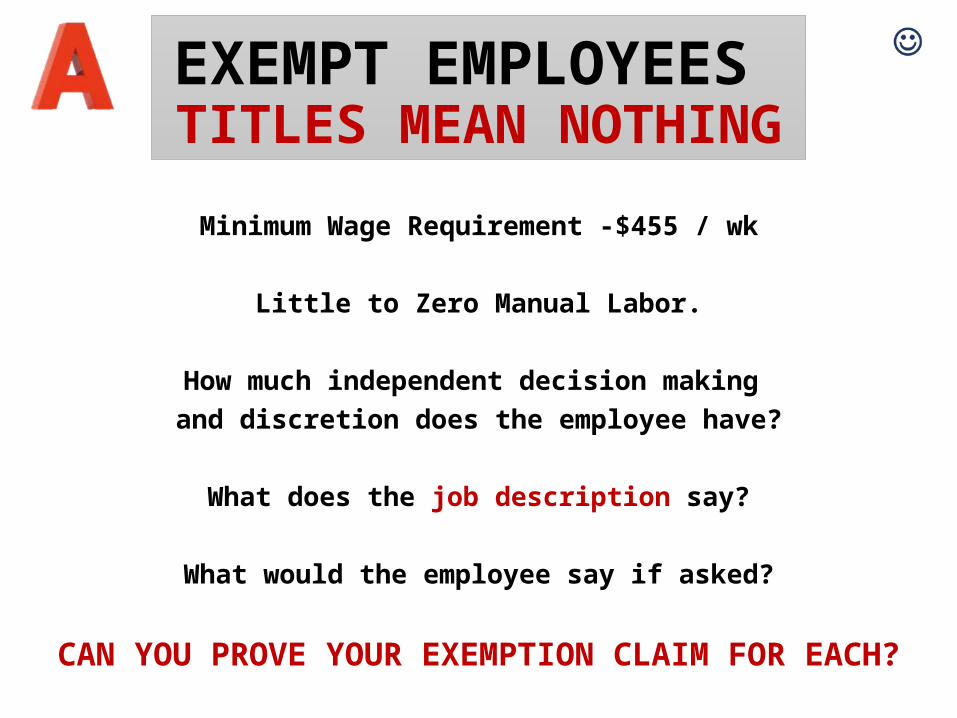

EXEMPT EMPLOYEES TITLES MEAN NOTHING

Minimum Wage Requirement -$455 / wk

Little to Zero Manual Labor.

How much independent decision making

and discretion does the employee have?

What does the job description say?

What would the employee say if asked?

CAN YOU PROVE YOUR EXEMPTION CLAIM FOR EACH?

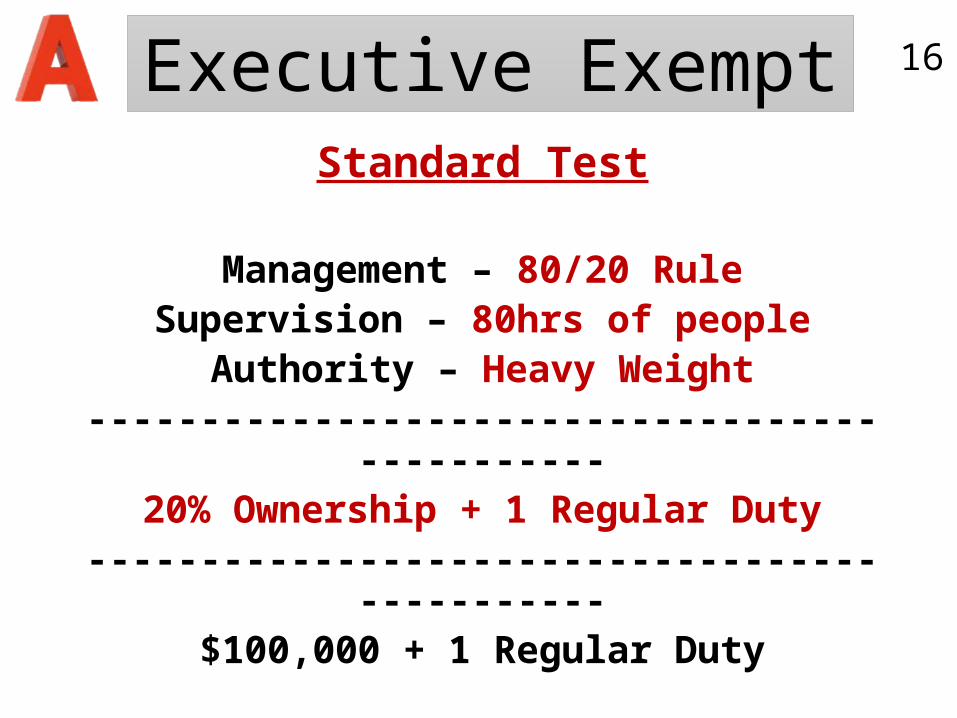

Executive ExemptStandard Test

Management – 80/20 RuleSupervision – 80hrs of people

Authority – Heavy Weight----------------------------------------------20% Ownership + 1 Regular Duty----------------------------------------------

$100,000 + 1 Regular Duty

16

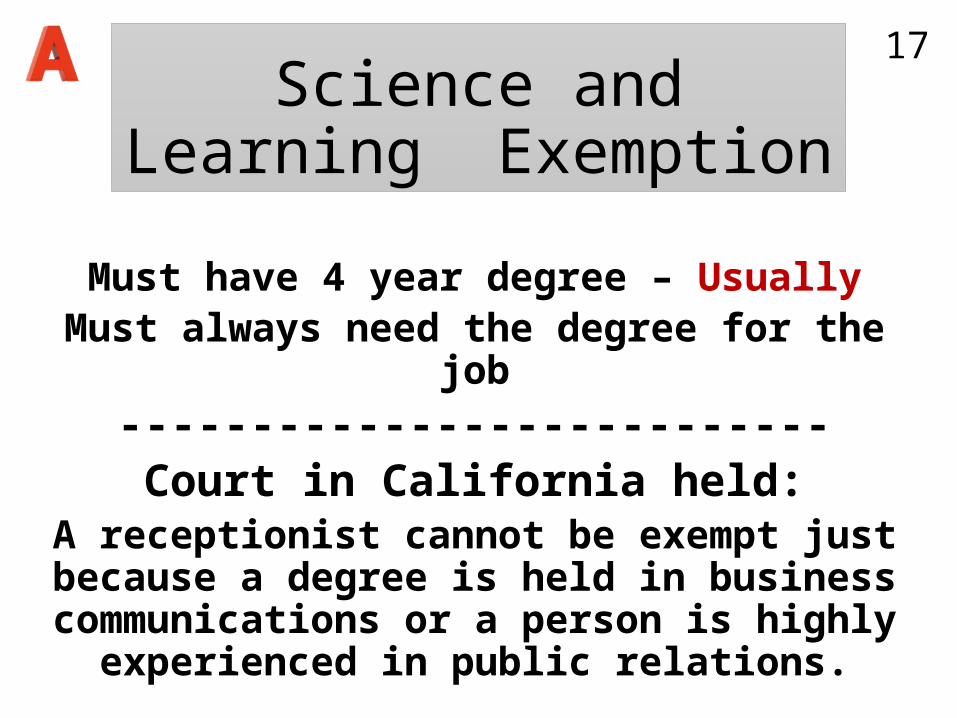

Science and Learning Exemption

Must have 4 year degree – UsuallyMust always need the degree for the job

---------------------------Court in California held:

A receptionist cannot be exempt just because a degree is held in business communications or a person is highly

experienced in public relations.

17

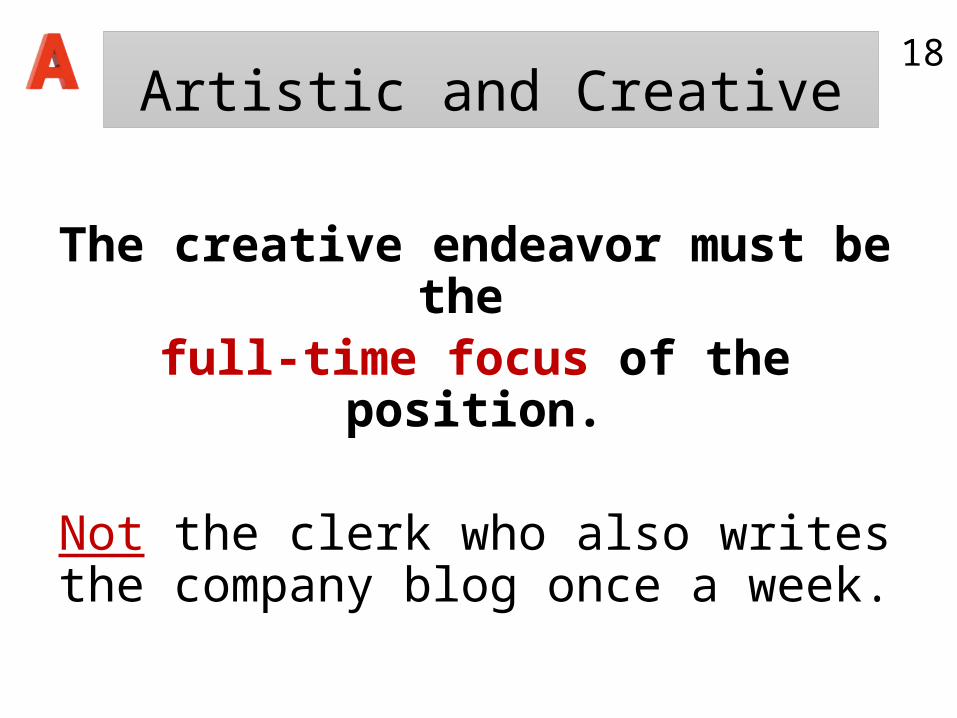

Artistic and Creative

The creative endeavor must be the full-time focus of the position.

Not the clerk who also writes the company blog once a week.

18

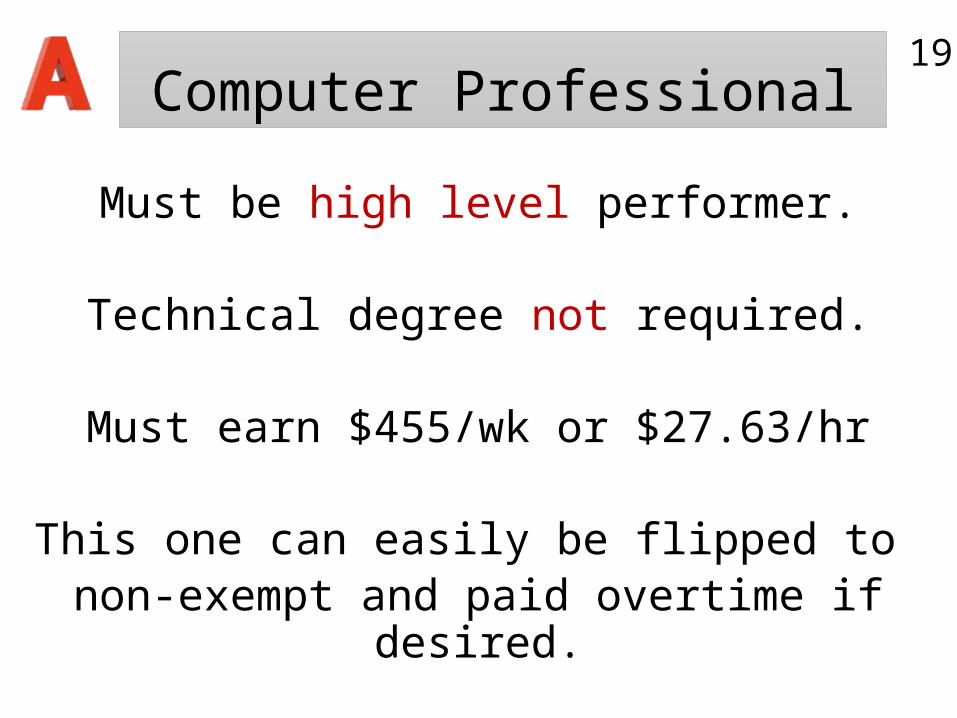

Computer Professional

Must be high level performer.

Technical degree not required.

Must earn $455/wk or $27.63/hr

This one can easily be flipped to non-exempt and paid overtime if desired.

19

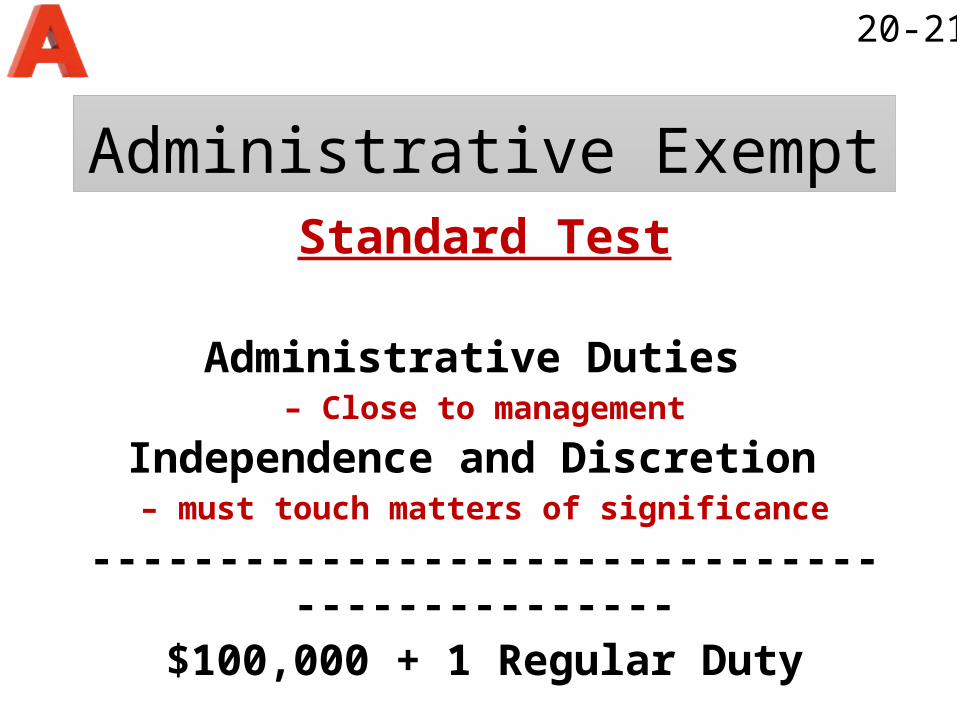

Administrative ExemptStandard Test

Administrative Duties – Close to management

Independence and Discretion – must touch matters of significance

----------------------------------------------$100,000 + 1 Regular Duty

20-21

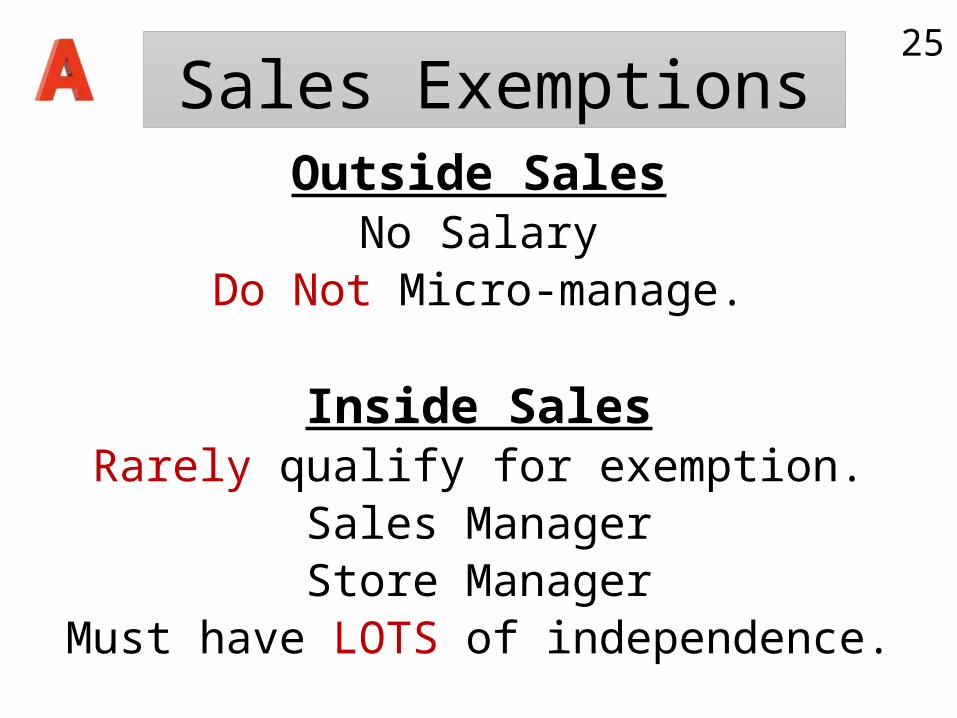

Sales ExemptionsOutside Sales

No SalaryDo Not Micro-manage.

Inside SalesRarely qualify for exemption.

Sales ManagerStore Manager

Must have LOTS of independence.

25

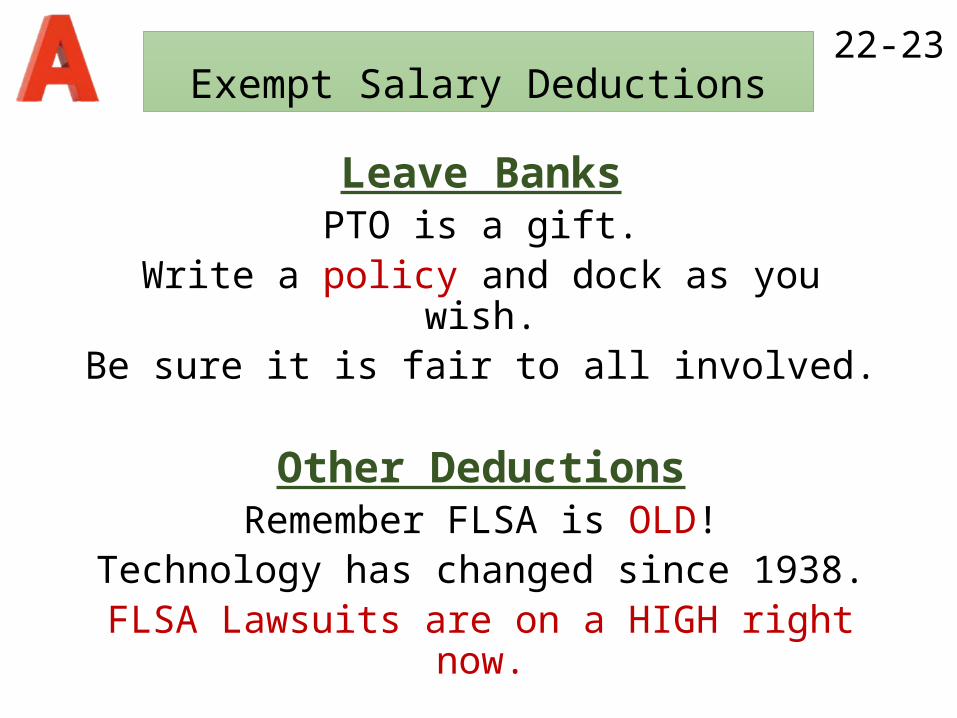

Exempt Salary Deductions

Leave BanksPTO is a gift.

Write a policy and dock as you wish.Be sure it is fair to all involved.

Other DeductionsRemember FLSA is OLD!

Technology has changed since 1938.FLSA Lawsuits are on a HIGH right now.

22-23

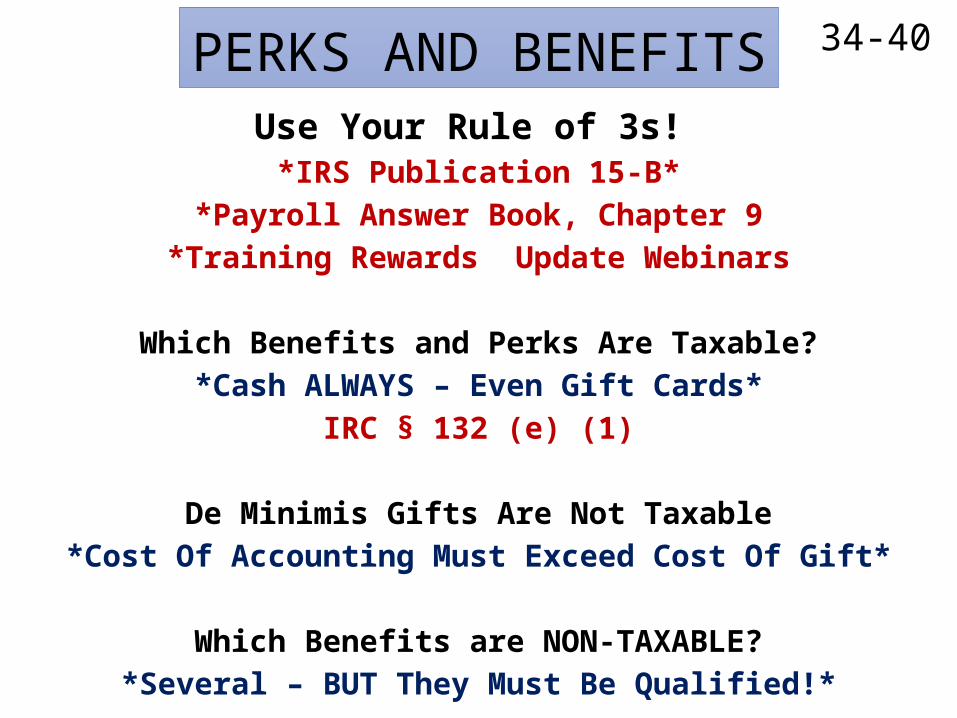

PERKS AND BENEFITSUse Your Rule of 3s! *IRS Publication 15-B*

*Payroll Answer Book, Chapter 9*Training Rewards Update Webinars

Which Benefits and Perks Are Taxable?*Cash ALWAYS – Even Gift Cards*

IRC § 132 (e) (1)

De Minimis Gifts Are Not Taxable*Cost Of Accounting Must Exceed Cost Of Gift*

Which Benefits are NON-TAXABLE?*Several – BUT They Must Be Qualified!*

34-40

EMPLOYEE LOANS/ADVANCES

Don’t Exceed $9999.00.

Charge Interest, if willing.

Have A Contract!

True Advances Are Taxable As Wages.

An Advance Becomes A Loan When An Agreement To Pay Is Signed

41

Military Pay•Supplemental Military Pay

• Compensation paid to employees while on military duty that represents the difference between employee’s regular pay and the pay provided by the state or federal government.

• Temporary assignment – FITW, FICA, Medicare and unemployment taxes

• Indefinite assignment - 1099-MISC (over $600)

42

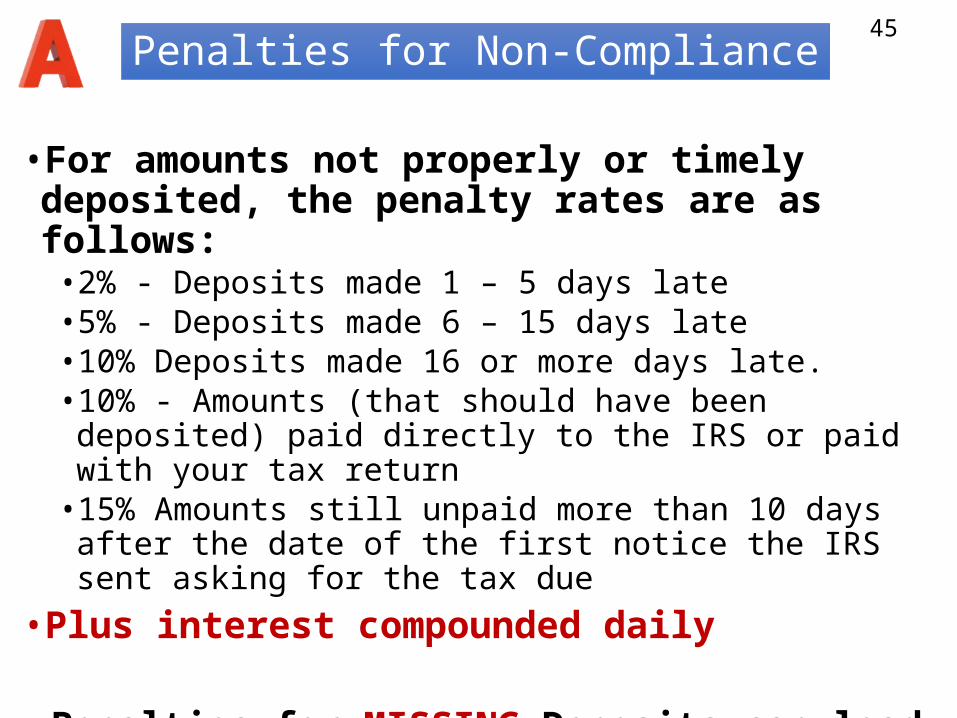

Penalties for Non-Compliance

• For amounts not properly or timely deposited, the penalty rates are as follows:

• 2% - Deposits made 1 – 5 days late• 5% - Deposits made 6 – 15 days late• 10% Deposits made 16 or more days late. • 10% - Amounts (that should have been deposited) paid directly to

the IRS or paid with your tax return• 15% Amounts still unpaid more than 10 days after the date of the

first notice the IRS sent asking for the tax due• Plus interest compounded daily

• Penalties for MISSING Deposits can lead to Jail Time.

45

Lisa Smith

Today’s CAC# is 2382

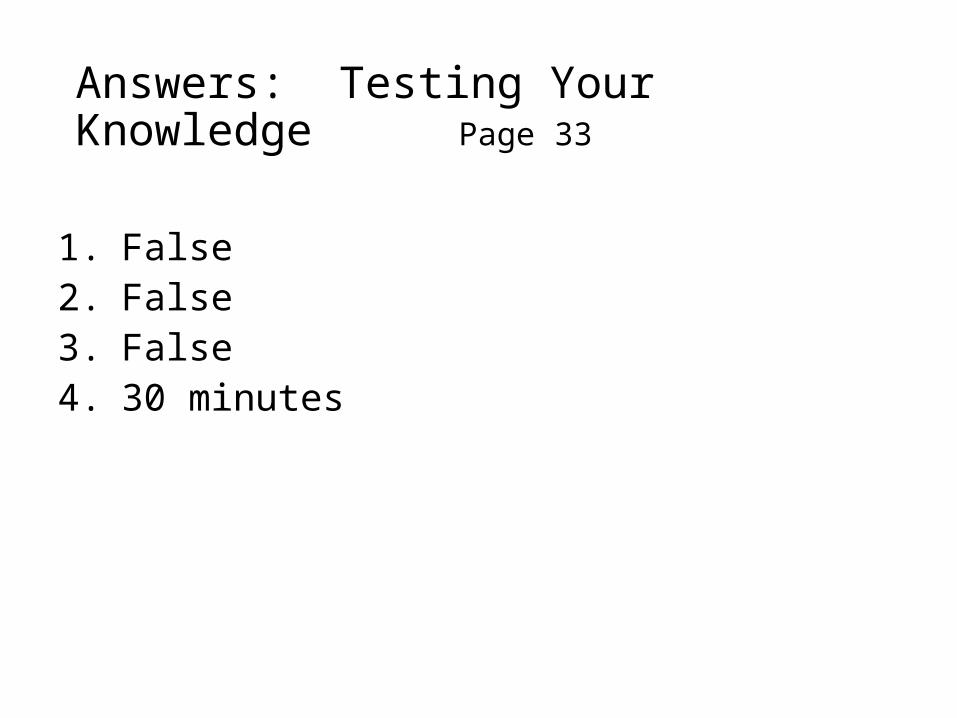

Answers: Testing Your KnowledgePage 33

1. False2. False3. False4. 30 minutes

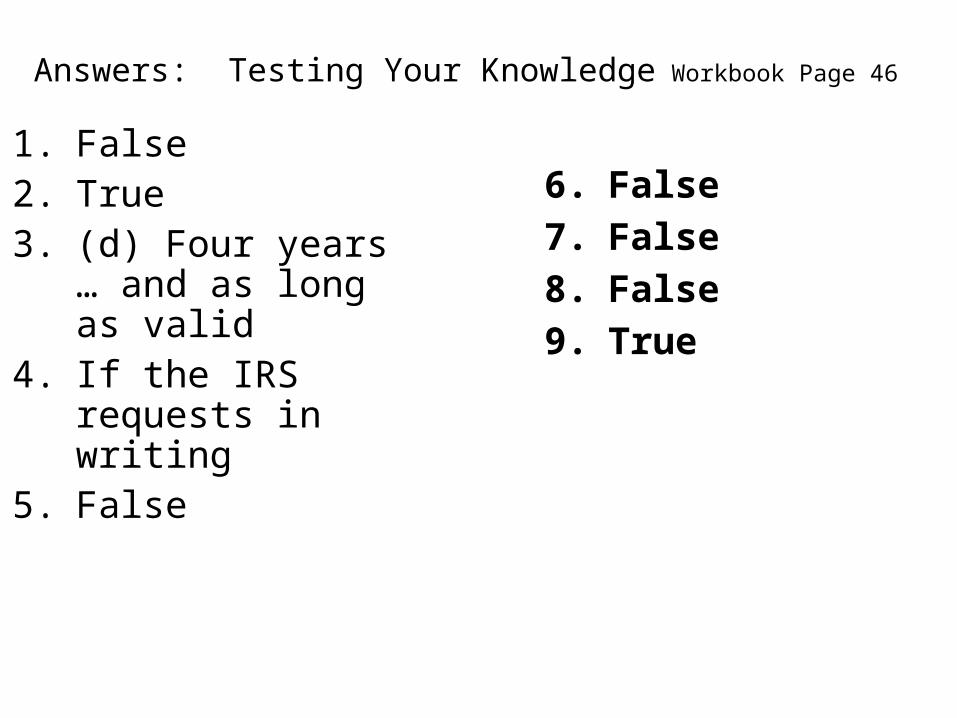

Answers: Testing Your Knowledge Workbook Page 46

1. False2. True3. (d) Four years … and

as long as valid4. If the IRS requests in

writing5. False

6. False7. False8. False9. True