PAYMENTS - Members Firstmembers.ccul.org/publications/cudigest/digest_issues/...credit union digest...

28

credit union Feature Story on Page 12 Western Healthcare FCU in Leader 2 Leader | Page 5 ‘Jumiya’: An Untapped Opportunity? | Page 6 CUs Engage Lawmakers on Capitol Hill | Page 8 Problem? Solved! | Page 10 PAYMENTS: the Facts and the Future Vol. 40 | No. 3 | April/May 2014 Members First

Transcript of PAYMENTS - Members Firstmembers.ccul.org/publications/cudigest/digest_issues/...credit union digest...

credit union

Feature Story on Page 12

Western Healthcare FCU in Leader 2 Leader | Page 5 ‘Jumiya’: An Untapped Opportunity? | Page 6CUs Engage Lawmakers on Capitol Hill | Page 8 Problem? Solved! | Page 10

PAYMENTS:the Facts

and

the Future

Vol. 40 | No. 3 | April/May 2014Members First

Introducing a new way for your credit union to create deeper, stronger member relationships.

To learn more visit www.TruStage.com/intro

EMPOWER YOUR MEMBERSTO PROTECT THE PEOPLE WHO MATTER MOST

CUNA Mutual Group’s MemberCONNECT® program now provides your members with access to TruStage insurance products, created exclusively for credit union members.

TruStage off ers straightforward and trustworthy information, real value and peace of mind for your members.

PROTECTING WHATMATTERS MOSTintroducing TruStage™ insurance products

TruStage™ is the marketing brand for insurance products off ered by TruStage Insurance Agency, LLC. and issued by CMFG Life Insurance Company and other leading underwriters.

CUNA Mutual Group is the marketing name for CUNA Mutual Holding Company, a mutual insurance holding company, its subsidiaries and affi liates.

10003208-1012 © CUNA Mutual Group, 2012 All Rights Reserved.

3credit union digest | april/may 2014 | members first

credit union

Feature Story on Page 12

Western Healthcare FCU in Leader 2 Leader | Page 5 ‘Jumiya’: An Untapped Opportunity? | Page 6CUs Engage Lawmakers on Capitol Hill | Page 8 Problem? Solved! | Page 10

PAYMENTS:the Facts

and

the Future

Vol. 40 | No. 3 | April/May 2014Members First

5

6

8

10

1219

20

21

22

23

25

26

April/May 2014 | Vol. 40 | No. 3

What's Inside

credit union

On The Cover:New ways of moving money are rapidly material-izing as technology makes its mark within our U.S. payments system. Are credit unions prepared? Seven leaders share their views as the industry embraces a modernized future.

leader 2 leaderWestern Healthcare Federal Credit Union

news & views‘Jumiya’: An Untapped Opportunity?

advocacyCUs Engage Lawmakers on Capitol Hill

problem? solved!Hot Topics That Won't Waste Your Time

feature storyPayments: the Facts and the Future

legalThe Fair Debt Buying Practices Act

asked & answeredLimiting Fair-Lending Risk in Autos

research & information Prepaid Cards: Expiration Disclosures

economic perspective Jobs, Wages, Confi dence, and the Future

market perspectiveWhich Lending Sectors Will Gain?

credit union solutionsMembers Dine Out While Fighting Hunger

closing thoughtsWhere do Credit Unions Stand?

Read CU Digest online by visiting www.ccul.org/publications/cudigest

Credit Union Digest publishes six bi-monthly issues per year.

Themes:

June/July 2014 IssueDEADLINE: April 17, 20142020: Will Your Credit Union Survive?

August/September 2014 IssueDEADLINE: June 19, 2014Your CU—Anytime, Anywhere

October/November 2014 IssueDEADLINE: Aug. 14, 2014 The Right Fit

December 2014/January 2015 IssueDEADLINE: Oct. 16, 2014 Land of the Giants

Themes subject to change. For more infor-mation, please contact Credit Union Digest Editor-in-Chief Carol Payne at 800.472.1702, ext. 6040, or at [email protected].

Editiorial Deadline Schedule

Congratulations, and thank you, to the fol-lowing credit unions that recently became members of the California Credit Union League:

County Schools FCUSharon Updike, [email protected]$54 million in assets7,800 membersVentura, CA

Sonoma County Grange CUPam McNatt, [email protected]$37 million in assets3,100 membersSanta Rosa, CA

Please Welcome Our New Members

4 credit union digest | april/may 2014 | members first

credit unionEDITOR-IN-CHIEFCarol E. Payne, Vice President, Communications and Marketing | [email protected]

ASSOCIATE EDITORMatt Wrye, Manager of Publications | [email protected]

ASSISTANT EDITORGeorge Sun, External Marketing & Member Communications Manager | [email protected] Tullues, Senior Marketing and Member Communications Writer | [email protected]

EXECUTIVE STAFFDiana R. Dykstra, President and Chief Executive OfficerLucy Ito, Executive Vice President and Chief Operating OfficerBob Arnould, Senior Vice President of Advocacy Cindy Cavanaugh, Senior Vice President and Chief Financial OfficerTony Kitt, Senior Vice President of Strategic Innovation and Planning Larry Palochik, Senior Vice President of Member SolutionsSharon Weber, Executive Assistant

GRAPHIC DESIGNNatalie J. Moreno, Senior Graphic DesignerDanielle Price, Graphic Designer

CONCEPTCarol Payne | Matt Wrye

EDITORIAL CONTRIBUTORSVictoria Allen | Melissa Ameluxen | Greg Badovinac | David Creager | Donna Dyer | Jeremy Empol | Rita Fillingane | Dwight Johnston | Clarissa Martin | Dianne Molvig | Arnold Ramirez | Tina Ramos-Ingold | Andrea Svoboda | Cindy Tullues | Tonja Wheatley | Thomas H. Wolfe

PHOTOGRAPHYNatalie J. Moreno | Carol E. Payne | Cindy Tullues | Matt Wrye

CONTACT INFORMATIONInternet address | www.ccul.orgMailing address | P.O. Box 51476, Ontario, CA 91761-0076Communications Department Fax | 909.390.3014

Credit Union Digest (ISSN#08921075) is published bi-monthly by the California and Nevada Credit Union Leagues, 2855 E. Guasti Road, Ste. 600, Ontario, CA 91761-1250; 1201 K Street, Suite 1050, Sacramento, CA 95814. Annual subscription rate: $48 members, $250 non-members. To subscribe, contact LaDonna Kohler at [email protected]. Periodicals postage paid at Ontario, CA and additional mailing offices.

ADVERTISINGMatt Wrye, Manager of Publications | [email protected]

POSTMASTERSend address changes to Credit Union Digest, P.O. Box 51476, Ontario, CA 91761-0076. Single issues are available; call 909.212.6044.

The California and Nevada Credit Union Leagues reserve the right to edit letters to the editor and all submissions. The Leagues do not take responsibility for the return of unsolicited materials. For more information, contact Editor-in-Chief Carol Payne at 909.212.6040.

Credit Union Digest is printed on recycled paper.

©2014 California and Nevada Credit Union LeaguesUSPS 011-679

Providing Innovative Support and Services to Member Credit Unions Since 1933.

Winner of the following:• 2012 CUNA/AACUL Pro and Blockbuster Honorable Mention• 2011 and 2012 Communicator Award of Distinction• 2011 CUNA/AACUL Pro and Blockbuster Award

CALIFORNIA LEAGUE BOARD OF DIRECTORS

At-Large Director Teresa Freeborn | 310.607.2177 | [email protected]

At-Large Director Teresa Halleck | 858.597.8690 | [email protected]

At-Large Director Eileen Rivera | 310.491.7500 | [email protected]

At-Large Director Jon Hernandez | 310.371.4242, ext. 217 | [email protected]

At-Large Director Hank Barrett | 209.549.8511, ext. 3000 | [email protected]

At-Larger Director Linda Walmsley | 323.845.4475 | [email protected]

Group A Director Chris Coursen | 714.641.5946, ext. 12 | [email protected]

Group B Director Charles Papenfus | 909.822.1810, ext. 215 | [email protected]

Group C Director Rick Hanan | 510.483.1300 | [email protected]

Group D Director Marla Shepard | 858.636.4221 | [email protected]

CALIFORNIA LEAGUE EXECUTIVE COMMITTEE

Chairman Teresa Freeborn | 310.607.2177 | [email protected]

Vice Chairman Jon Hernandez | 310.371.4242, ext. 217 | [email protected]

At-Large Charles Papenfus | 909.822.1810, ext. 215 | [email protected]

CUNA BOARD MEMBERS

Jeff York* | 805.733.7640 | [email protected]

Brett Martinez* | 707.576.5101 | [email protected]

NEVADA LEAGUE BOARD OF DIRECTORS

Chairman Wayne Tew | 702.939.3020 | [email protected]

Vice Chairman Eric Estes | 702.293.7772, ext. 183 | [email protected]

Secretary/Treasurer Wallace Murray | 775.882.2060 | [email protected]

Director Barbara Reuter | 775.945.2421, ext. 4013 | [email protected]

Director Dennis Flannigan | 775.789.3108 | [email protected]

* Ex-Officio California League Board Member

www.UniteForGood.org

5credit union digest | april/may 2014 | members first

2LEADER LEADER

President and CEO

Diana Michaels

Chairman of the Board

Cheryl Jarman

Western Healthcare FCUConcord, CA4,000 Members$35 Million in Assets

EducationI received my degree in business and health care administra-tion from St. Mary’s College.

First Credit Union ExperienceIt was with the credit union serving Southern Pacifi c Railroad 31 years ago. My soon-to-be husband and I didn’t have enough for our honeymoon. He applied for a loan and received $700. He surprised me with airline tickets for a small getaway. We ended up opening a joint account. That credit union holds a special place in my heart.

Biggest Challenge as a Board MemberMaking sound and informed decisions regarding routine busi-ness operations and strategic initiatives—as well as under-standing our credit union’s fi nancial footing—is important. You must have the ability to identify and manage risk in all major operational areas. You have to accomplish all this while engaging, facilitating, managing, and guiding the board pro-cess and the other directors, and still allow the CEO to focus on the credit union, its mission, and strategic plan execution.

League’s Role in the California CU MovementThe California League is a well-informed resource for management and volunteers. We look to the League for timely information, and to be our advocate for legislative change that is imperative for success.

Leisure ActivitiesMy time is divided between serving as the credit union’s board chairman and as “crew supervisor” for The Marine Mammal Center in Sausalito, where I help rehabilitate injured and sick marine mammals.

Personal PhilosophyBeing human is being inquisitive. I strive to learn today what I did not know yesterday. I believe when someone is allowed to think outside the pre-defi ned constraints of society, the directions in which you can travel are infi nite.

Advice for Future Credit Union LeadersKnow your strengths and weaknesses so you’re not only able to direct yourself effectively and powerfully, but your credit union as well. Have passion for what you are doing. Be honest, focused, have integrity, lead by example, and listen as well as you speak.

EducationI have a bachelor’s in management and have also attended West-ern CUNA Management School and CUNA Financial School.

First Credit Union ExperienceI’m a second-generation CEO, so I grew up understanding how credit unions are different. I received my fi rst auto loan for a 1965 Ford Mustang at age 16. My career path was inevitable.

Biggest Challenge as a CEOIt’s balancing what you want to do with what you have to do. You want to make sure your credit union has the needed resources to provide all desired products and services. How-ever, you have to choose, based on demand and resources, what you’re able to accomplish. Also, keeping up with regulatory stresses and the constant demand to evaluate our relevancy adds a tremendous burden.

League’s Role in the California CU MovementThe California League is a true partner, working to ensure the cooperative spirit remains fi rst and foremost in our minds. Its support of Shapiro credit unions and others demonstrates a true partnership with an eye toward creating the best possible legislative environment.

Leisure ActivitiesI enjoy reading, shopping, decorating my home, and spend-ing quality time with family and my twin grandchildren.

Personal PhilosophyIf you don’t take the risk and put yourself out there, you’ll never know what’s possible. Be honest in all dealings, both personally and professionally, and be willing to fail greatly.

Advice for Future Credit Union LeadersHave the desire and passion to help people succeed, and have the ability to understand that happy team members make happy members. Create a culture that engages your team. Be tenacious about culture and talent development—it’s what sets credit unions apart from other fi nancial alternatives. Encourage others to think outside the box, seeking innovation that changes the fundamental way we do business. Lead by living the vision, because others will look to you to display that leadership.

‘Jumiya’: An Untapped Opportunity?by Matt Wrye, Associate Editor

Joe BrancucciCEOGTE Financial

What ‘Jumiya’Revealed to CUs• Healthy behavior leads to good fi nancial outcomes.• Non-healthy behavior leads to poor fi nancial outcomes.• 62 percent of individual bankruptcies are linked to medical debts.• “Massive amounts of rich, untapped data lodes”— How Jumiya researchers described the information credit unions have accumulated, which holds promise for creating new self-servicing tools and personalized fi nancial recommendations.• 80 percent—the level of certainty regarding a consumer’s fi nancial health that the Jumiya team could predict based on medical health data.

In what could be a revolutionary business model for California, Nevada, and elsewhere, a Florida-based credit union is putting into practice some solid tangibles coming out of a recent discovery: The healthier your members, the better their fi nancial outlook—and the greater opportunity for building exceptional relationships.

“We have a lot of retirees in Florida, but we also have a very young, fi t population as well,” said Joe Brancucci, CEO of Tampa Bay-headquartered GTE FCU, which re-branded itself as GTE Financial in 2012. “In California you have similar positives. People want to be fi t and healthy, especially baby boomers. There’s a whole culture around it.”

In January, GTE Financial implemented a pilot project that was originally conceived by Singularity University researchers and tested with credit unions in Texas, Washington, Iowa, and Canada. The team was commissioned by the National Credit Union Roundtable (NCUR) in 2012 to help develop a forward-looking roadmap for increasing credit unions’ value to society. Filene Research Institute in Madison, WI, managed the project, named “Jumiya,” which means “union” in Swahili.

Funded by six California credit unions—and 41 others across the nation, as well as fi ve state credit union leagues—the study’s results show that when individuals are healthier, they’re less likely to slide into delinquency, default, or bankruptcy.

“This could be attractive for a number of credit unions, but it would probably have to fi t within a credit union’s overall alignment and strategy,” said

Nader Moghaddam, CEO of Financial Partners CU and chairman of NCUR, a group of the largest U.S. credit unions that spearheaded the project’s inception. “At our credit union, we’re certainly exploring possible implementation.”

He said a national announcement with specifi cs on how credit unions can apply the Jumiya concept is coming sometime in 2014.

Keeping fi nancial diffi culties at bay is where the heart of GTE Financial’s “Get Fit” program comes into play. Members can use a smartphone app to track how much they walk every day, merging the results into their account online. They can redeem “steps” for rewards, so more steps equal

6 credit union digest | april/may 2014 | members first

Eli MohamadCEOWalkmore

George HofheimerChief Research and Innovation Offi cerFilene Research Institute

7credit union digest | april/may 2014 | members first

more incentives, such as special coupons to local businesses or cash.

“In January and February, our members logged 78.7 million steps, or about 39,350 miles,” Brancucci said. “We’re also trying to attract a younger set of members with this. So far, they think it’s the coolest thing since sliced bread.”

Although “Get Fit” was created to add value to current members, the program is attracting new members almost daily.

As of March, GTE Financial was the only credit union in the country offi cially rolling out a customized version for its members with the help of Walkmore, a company headquartered at NASA Research Park near Mountain View, CA, and located on the same campus as Singularity University.

Walkmore is a team of Silicon Valley technologists led by Singularity student and entrepreneur Eli Mohamad. An original member of the Jumiya research team, he’s now looking to execute the concept for credit unions and community banks.

Mohamad says the initial study proved more than a link between a member’s physical health and fi nancial health.

“It was also proof that a signifi cant impact on a credit union’s bottom line can be achieved with basic data analytics, using transactional data—something large banks have been doing for 40 years,” he said. “Currently, nearly all credit unions do not use any kind of data analytics on their members’ transactional data. Only a small number of credit unions can say they understand

the behavior and needs of their members, which is enabling them to be a true member advocate.”

The broader implications from what GTE Financial is testing show it’s important credit unions become more “data driven” if they want to serve members better, Mohamad said.

“We’re correlating members’ physical activity and transactional data to produce highly accurate predictions of behavior,” he said. “Credit unions will see retention of existing members and creation of new leads, particularly Gen Y.”

This correlation could be the tip of the iceberg. The Walkmore team is also investigating how sleep, diet, mood, social behavior, and stress levels are related to fi nancial behavior.

“It’s time for credit unions to stop thinking of their members’ fi nancial behavior as an isolated aspect, and start looking at them from a more holistic perspective,” Mohamad said. “With new digital entrants, credit unions will have to fi ght to retain and attract members—openly and very hard.”

He added: “It’s convenient to walk into a large retailer, pay for your purchase through one mobile app, pay your store bills at the same time, and qualify for a loan on the spot. The retailer can do this because it has your payment and behavior data, which will enable it to drive down loan delinquency.”

Even so, there’s a “wild west” undercurrent to all this, especially with consumers getting antsy about sharing their information, according to George Hofheimer, chief research and innovation offi cer at Filene.

He said some credit unions involved in a recent big-data analytics project for Filene were apprehensive. They weren’t sure how much member information they could share, which shows the cautionary stance the industry is taking.

“Credit unions don’t generally have the expertise to do data analytics,” Hofheimer said. “Some struggle with the idea of it. If you ask credit union executives, they’ll say they have a lot of info that’s valuable, but quite honestly they don’t know how to act on it.”

The Jumiya concept “may turn into something huge, or it might not,” he said. “But it provides credit unions an opportunity to learn and complete testing at a level that many organizations aren’t equipped to carry out.”

Brancucci said programs similar to “Get Fit” have the potential to change how credit unions engage members in the future. There’s no guarantee it will work, but GTE Financial wouldn’t have implemented the approach if it didn’t believe “Get Fit” holds promise. The credit union’s pilot ends in September.

“In the long run, our goal is to continue to promote and facilitate the impact of fi nancial and physical fi tness on individuals,” Brancucci said. “This makes us a better credit union for our members, and supports the betterment of our community.”

Nader MoghaddamCEO—Financial Partners CUChairman—National Credit Union Roundtable

8 credit union digest | april/may 2014 | members first

advocacy

CUs Engage Lawmakers on Capitol Hill

This year’s 2014 Governmental Affairs Conference (GAC) in Washington, D.C. was a piv-

otal event for credit union leaders who advocated with legislators on behalf of their members as Congress continued its review of tax reform, data security, regu-latory relief, and other important issues.

Nearly 200 attendees from California and Nevada attended the Credit Union National Association’s (CUNA) annual event, which drew a record audience of more than 4,400 credit union advocates.

The general sessions, keynote speakers, and “Hike the Hill” visits proved invaluable as executives and

board members discussed how their credit unions are actively working in legislators’ communities to improve the lives of families and individuals through the credit union philosophy.

Several members of Congress arranged time in their schedules to sit down and discuss the industry’s most important issues—first and foremost, why credit unions should remain exempt from federal corporate income tax, as well as other hot topics. Legislators and their staff aides noted the accomplishments of credit unions with respect to financial literacy and modifying members’ loans.

Even lawmakers who were brand new to Capitol Hill showed their support for credit unions, saying they understood the unique role the movement plays within the financial services industry.

“Many attendees were encouraged by the positive feedback they received from lawmakers at every visit,” said Diana Dykstra, president and CEO of the California and Nevada Credit Union Leagues. “We want to thank those who participated, and those of you at home who sent your staff and volunteers.”

1: At Credit Union House near Capitol Hill (L-R): Teresa Freeborn, Chairman of the California Credit Union League and CEO of Xceed Financial FCU; Diana Dykstra, President and CEO of the California and Nevada Credit Union Leagues; Rep. Brad Sherman, D-CA; Rep. Eric Swalwell, D-CA; Rep. Doug LaMalfa, R-CA; and Bill Cheney, President and CEO of the Credit Union National Association (CUNA); 2: Linda White (second from right), CEO of United Health CU, and Chuck Papenfus (far right), CEO of Inland Valley FCU, were recognized with the CUNA Member Benefits Award; 3: Ashley Rooney (second from left), Political Management Graduate Student at George Washington University Graduate School of Political Management, accepts the Kelly J. Purcell Credit Union Memorial Fund Scholarship; 4: SchoolsFirst FCU CEO Rudy Hanley (center) is recognized with CUNA’s Buck Levins Award for his efforts in political advocacy on behalf of credit unions; 5: Andy Hunter, CEO of Silver State Schools CU, was recognized with the Desjardins Youth Financial Education Award by CUNA; 6: House Oversight Committee Chairman Darrell Issa, R-CA (center); 7: Rep. Ed Royce, R-CA (second from left); 8: Pete Aguilar, Mayor of Redlands and congressional candidate; 9: Rep. David Valadao, R-CA (center); 10: Rep. Scott Peters, D-CA (front center); 11: Rep. Raul Ruiz, D-CA, speaks at Credit Union House; 12: House Majority Whip Kevin McCarthy, R-CA (center); 13: Rep. Mark Amodei, R-NV (left); 14: Rep. Linda Sanchez, D-CA (center); 15: Rep. Eric Swalwell, D-CA (front left-center); 16: Rep. Paul Cook, R-CA (center); 17: Rep. Mark Takano, D-CA (center)

To view all photos of California and Nevada participants at this year’s GAC, visit www.ccul.org/publications/galleries

Want to See More?

1 2

3 4 5

9credit union digest | april/may 2014 | members first

6 7 8

9 10 11

12 13

14 15

16 17

10 credit union digest | april/may 2014 | members first10 credit union digest | april/may 2014 | members first

Hot Topics That Won't

Waste Your Time

Questions? Contact Mark Klinkert, Vice President of Education and Training for the Leagues, at 909.212.6002 or [email protected]

A ‘Possible’ Versus ‘Given’

FutureIn a tremendously fast-changing and uncertain world, should organizational leaders strive to craft long-term plans for success, or focus on becoming very good at reacting quickly to

near-term changes in the environment?

The answer is “yes.”

Long-term strategy can (and should) be developed and ex-ecuted based upon an exploration

of possible future outcomes. This exploration will help to

surface some competitive traits that will likely be re-quired in most any future

scenario.

Develop competency in these areas and your credit union will be

better positioned to succeed, regardless of what future outcome ultimately emerges.

Once you’ve identifi ed longer term success characteristics common to a variety of pos-sible futures, you might want to place a bet on a given future. But remember, in an un-certain world, such bets are just that—bets.

Be alert to environmental indicators that either support or oppose your envisioned future, and be ready to make course adjust-ments as reality unfolds.

Perhaps J. Paul Getty, the famous entrepre-neur and industrialist, said it best: “Without the element of uncertainty, the bringing off of even the greatest business triumph would be dull, routine, and eminently unsatisfying.”

11credit union digest | april/may 2014 | members first 11credit union digest | april/may 2014 | members first

Leverage Your DataDigital marketing, however elaborate, really comes down to three fundamental channels: the Internet, your social presence, and e-mail—with mobile apps being the exception. Focus on the cross-collabora-

tive efforts across these elements and you’re talking about a solid marketing plan.

But statistically speaking, a website and social media presence alone are not effective conversion tools. Both web and social media are general broadcast tools, where information is pushed and pulled back and forth to an audience with no particular segmenting capabilities. When was the last time you saw a Twitter post addressing you by name?

With your database at your disposal, there’s no excuse to not leverage that information with targeted e-mails to nurture growth. It’s no surprise that click-through rate statistics are higher when

communications use the recipient’s fi rst name in the subject line. Knowing how to make the most of your data with the right execution should be part of your marketing plan.

The time needed to plan and execute, the broad knowledge and technical skills required to do so quickly, and the actual ability to implement speedily are vital to the

success and bottom line of any credit union looking to keep up with the competition.

Those First 10 SecondsI notice more and more credit unions interested in producing a viral video to get noticed by the masses. Harnessing this visual power might seem like an attractive option, but there’s a tall order to fi ll if you want to “go viral.”

Consider the following:• Viral videos have an extremely short shelf life, and they are diffi cult to capture by nature

of their spontaneity.• Most of them are not educational or fi nancial-related.• Most viral videos kind of “just happen”—they aren’t planned.

Instead, credit unions should consider creating promotional videos showing the benefi ts of membership. These videos can be emotional, serious, or funny, but they still have the educational aspect.

Research shows you have about 10 seconds to capture the attention of someone watching your video. If they are intrigued, they’ll keep watching for another 20 seconds. What impact do you want to make in those fi rst 10 seconds? And more importantly, are you showcasing your brand promise?

Going viral will deliver your short window of fame, but viewers probably won’t understand your message. Creating a video that educates, enhances your brand promise, and is entertaining is the way to go.

I notice more and more credit unions interested in producing a viral video to get noticed by the masses. Harnessing this visual power might seem like an attractive option, but there’s a tall order to fi ll if you

addressing you by name?addressing you by name?addressing you by name?addressing you by name?addressing you by name?addressing you by name?addressing you by name?addressing you by name?

With your database at your disposal, there’s no excuse to not leverage that information with targeted With your database at your disposal, there’s no excuse to not leverage that information with targeted With your database at your disposal, there’s no excuse to not leverage that information with targeted e-mails to nurture growth. It’s no surprise that click-through rate statistics are higher when e-mails to nurture growth. It’s no surprise that click-through rate statistics are higher when e-mails to nurture growth. It’s no surprise that click-through rate statistics are higher when e-mails to nurture growth. It’s no surprise that click-through rate statistics are higher when

communications use the recipient’s fi rst name in the subject line. Knowing how to make the communications use the recipient’s fi rst name in the subject line. Knowing how to make the communications use the recipient’s fi rst name in the subject line. Knowing how to make the communications use the recipient’s fi rst name in the subject line. Knowing how to make the most of your data with the right execution should be part of your marketing plan.most of your data with the right execution should be part of your marketing plan.most of your data with the right execution should be part of your marketing plan.

The time needed to plan and execute, the broad knowledge and technical skills required to do so quickly, and the actual ability to implement speedily are vital to the

success and bottom line of any credit union looking to keep up with the competition.

Questions? Contact George Sun, Manager of Image Arc Marketing Solutions, at 909.212.6047 or [email protected]

Viral videos have an extremely short shelf life, and they are diffi cult to capture by nature

Research shows you have about 10 seconds to capture the attention of someone watching your video. If they are intrigued, they’ll keep watching for another 20 seconds. What impact do you want to make in those fi rst 10 seconds? And more importantly, are you showcasing your

Questions? Contact Joe Keller, Vice President of C-Sun Studios and Digital Media for the Leagues, at 909.212.6020 or [email protected]

By Matt Wrye, Associate Editor

PAYMENTS:the Facts

and

the Future

feature

12 credit union digest | april/may 2014 | members first

feature

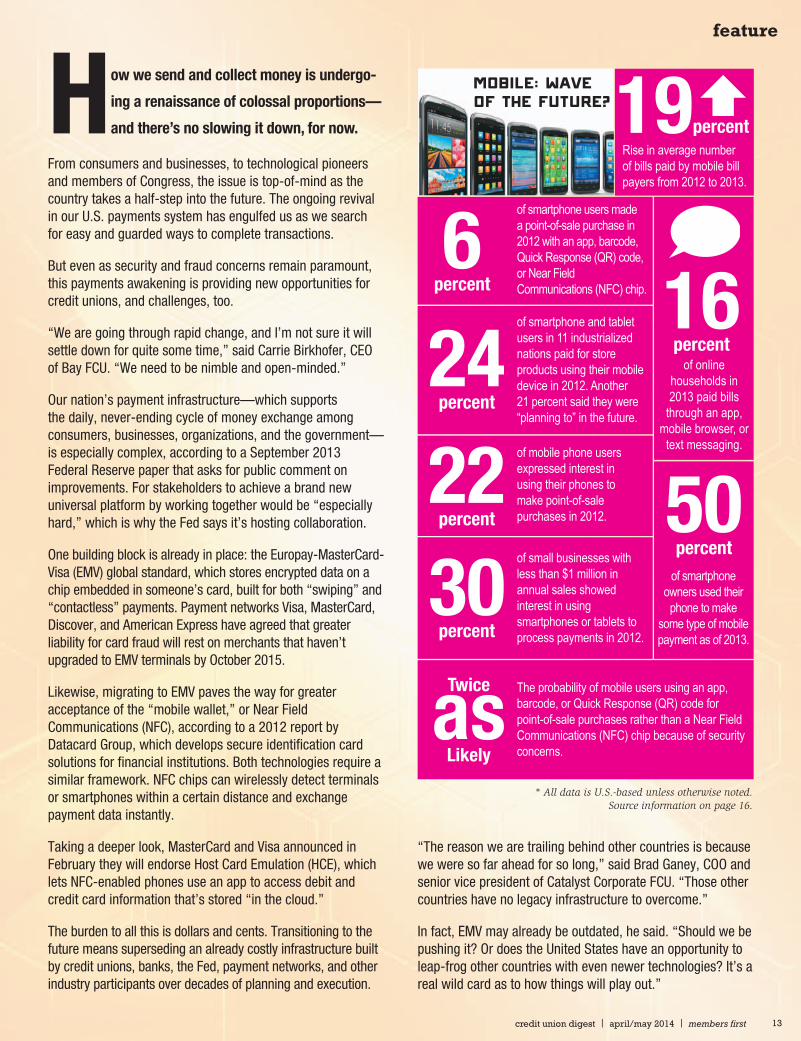

Mobile: WAVEof the Future?

6percent

of smartphone users made a point-of-sale purchase in 2012 with an app, barcode, Quick Response (QR) code, or Near Field Communications (NFC) chip.

19Rise in average number of bills paid by mobile bill payers from 2012 to 2013.

percent

16percent

of online households in 2013 paid bills

through an app, mobile browser, or

text messaging.

of smartphone and tablet users in 11 industrialized nations paid for store products using their mobile device in 2012. Another 21 percent said they were “planning to” in the future.

24percent

50percent

of smartphone owners used their

phone to make some type of mobile payment as of 2013.

of mobile phone users expressed interest in using their phones to make point-of-sale purchases in 2012.

22percent

of small businesses with less than $1 million in annual sales showed interest in using smartphones or tablets to process payments in 2012.

30percent

* All data is U.S.-based unless otherwise noted.Source information on page 16.

Twice

asLikely

The probability of mobile users using an app, barcode, or Quick Response (QR) code for point-of-sale purchases rather than a Near Field Communications (NFC) chip because of security concerns.

How we send and collect money is undergo-

ing a renaissance of colossal proportions—

and there’s no slowing it down, for now.

From consumers and businesses, to technological pioneers and members of Congress, the issue is top-of-mind as the country takes a half-step into the future. The ongoing revival in our U.S. payments system has engulfed us as we search for easy and guarded ways to complete transactions.

But even as security and fraud concerns remain paramount, this payments awakening is providing new opportunities for credit unions, and challenges, too.

“We are going through rapid change, and I’m not sure it will settle down for quite some time,” said Carrie Birkhofer, CEO of Bay FCU. “We need to be nimble and open-minded.”

Our nation’s payment infrastructure—which supports the daily, never-ending cycle of money exchange among consumers, businesses, organizations, and the government—is especially complex, according to a September 2013 Federal Reserve paper that asks for public comment on improvements. For stakeholders to achieve a brand new universal platform by working together would be “especially hard,” which is why the Fed says it’s hosting collaboration.

One building block is already in place: the Europay-MasterCard-Visa (EMV) global standard, which stores encrypted data on a chip embedded in someone’s card, built for both “swiping” and “contactless” payments. Payment networks Visa, MasterCard, Discover, and American Express have agreed that greater liability for card fraud will rest on merchants that haven’t upgraded to EMV terminals by October 2015.

Likewise, migrating to EMV paves the way for greater acceptance of the “mobile wallet,” or Near Field Communications (NFC), according to a 2012 report by Datacard Group, which develops secure identifi cation card solutions for fi nancial institutions. Both technologies require a similar framework. NFC chips can wirelessly detect terminals or smartphones within a certain distance and exchange payment data instantly.

Taking a deeper look, MasterCard and Visa announced in February they will endorse Host Card Emulation (HCE), which lets NFC-enabled phones use an app to access debit and credit card information that’s stored “in the cloud.”

The burden to all this is dollars and cents. Transitioning to the future means superseding an already costly infrastructure built by credit unions, banks, the Fed, payment networks, and other industry participants over decades of planning and execution.

“The reason we are trailing behind other countries is because we were so far ahead for so long,” said Brad Ganey, COO and senior vice president of Catalyst Corporate FCU. “Those other countries have no legacy infrastructure to overcome.”

In fact, EMV may already be outdated, he said. “Should we be pushing it? Or does the United States have an opportunity to leap-frog other countries with even newer technologies? It’s a real wild card as to how things will play out.”

13credit union digest | april/may 2014 | members first

feature

* All data is U.S.-based unless otherwise noted.Source information on page 16.

Cash:Still ‘King’for Some

28minutes

Time consumers spend each month traveling to a cash-

access point.

37percent

of consumers in late January were making an effort to pay with cash instead of credit or debit cards due to the large-scale Target stores security breach.

$8billion

Fees collected by ATMs for cash

withdrawalsevery year.

How much the three middle household quintiles (those earning $20,000-$100,000

per year) carry and use everymonth in U.S. dollars.

$100 or less

$40billion

How much retailers lost in 2010due to cash theft.

Cost to the government, businesses, consumers, and stakeholders every year

to produce currency, move it, maintain it, and pay for related expenses.

$200 billionHow the Federal

Reserve describes society’s use of

cash going forward.

‘An important

component’

I don’t see credit unions as the innovators of new payment channels. However, we need to fi nd a way to remain relevant. There will be a lot of experiments before we see a new mainstream payment system take hold, but once something catches on, it’s possible it could spread fast.

We’re watching new innovations to see what sticks. Internally, we’ve tried Square Cash, an e-mail and debit card platform for person-to-person payments. We’re also on the wait list for “Coin” cards, where all cards are stored on one device. I encourage my team to try out products and see how they work.

EMV cannot come fast enough. Merchants have no liability for fraud and lack the incentive for good security controls, so credit unions pay the price. We issue new cards almost daily due to compromises. We expect to see a reduction in merchant compromises once the upcoming EMV requirement is adopted.

With so many new innovators, credit unions will hopefully still be relevant as a secure place to save and borrow money. We are going through rapid change, and I’m not sure it will settle down for quite some time. We need to be nimble and open-minded.

Bay FCU

CEO: Carrie Birkhofer

Assets: $695 million

Members: 55,000

Headquarters: Capitola, CA

Our credit union is doing the best we can with what we’ve got. We’re getting person-to-person transfer capability on our mobile app soon. Members will see “PayPal,” but that doesn’t bother me. It would be nice to see credit unions collaborate to address opportunities like this.

Society needs transactions settled in “real time.” If money moves faster, individuals and businesses will move even more money around. I think Google, Apple, Microsoft, and others will force the payments issue. Credit unions might have to partner with some of these companies to fi nd a solution.

I truly believe you can forget about EMV chips. The future will be using your smartphone—or NFC technology—as your credit

Contra Costa FCU

CEO: David Green

Assets: $616 million

Members: 28,000

Headquarters: Martinez, CA

or debit card. We’re trying to fi nd ways to reduce payment costs, but there’s a lot of legacy infrastructure out there. Any new equipment needs to be affordable for merchants.

Our system is archaic, but I also recognize that the big banks run it. Banks need to spend billions of dollars to upgrade, and I don’t think they want to. I wouldn’t count on them partnering with credit unions. This is something credit unions need to do on their own.

14 credit union digest | april/may 2014 | members first

feature

* All data is U.S.-based unless otherwise noted.Source information on page 16.

Automated Clearing House (ACH) payments made in 2012, up from

19.1 billion in 2009.

Checksand ACH:A MixedBag 22.1

billion

18.3billion

Number of checks used for payment by consumers and businesses in 2012, representing $26 trillion.

$49trillion

Check payments by businesses worldwide in 2013. Companies across the globe used checks

for 75 percent of payments that year.$135

billionGlobal money “in fl ight” every day that hasn’t reached its destination (consumers, businesses, and other entities). The money riding these checks can’t be used until payments are settled.

toHow the Federal Reserve describes society’s use of

checks going forward.

‘Expected

decline’

Some large retailers are now demanding instant access to sales proceeds so they can immediately use those dollars for replenishing inventory and making investments.

-dayAccess’

‘Intra

American First CU

CEO: Jon Shigematsu

Assets: $504 million

Members: 39,000

Headquarters: La Habra, CA

The trend is clearly mobile, and smartphones are the likely mechanism. With our members looking for ease of use, safety, and fast delivery, the signs are pointing in this direction. Credit unions need to stay abreast of changes in the payments arena to offer services their members demand.

We began offering remote deposit capture last year, and going forward we’ll be offering person-to-person transfers for internal and external payments. We need to stay competitive, especially when large banks are targeting our members.

A wide variety of payment choices may be inevitable for the foreseeable future. There’s always going to be cash, and checks and cards will stay around as well. The percentage of transactions in these areas will shrink, but I’m confi dent these options will still be available for members who want them.

It’s diffi cult to say how the future of payments should be structured given the speed of technological innovation. I’m not so sure payment uniformity is what’s best for the consumer. I’d prefer to see individual entrepreneurs create products that match the needs of consumers. Innovators will dictate the future of payments.

It’s clear that fewer consumers are thinking “account fi rst, transaction second.” To remain relevant, we will likely have to stop asking members to open checking accounts and instead talk to them about what we offer in the way of secure, inexpensive access points for their money.

The payments landscape is moving too quickly for the system to stop and take necessary steps to collectively achieve ubiquity, if that were even feasible to begin with. Consumers and payment entrepreneurs aren’t interested in waiting.

The situation becomes exacerbated by their opinions that many historical providers of payment services are

Greater Nevada CU

CEO: Wally Murray

Assets: $470 million

Members: 45,000

Headquarters:

Carson City, NV

“dinosaurs.” They feel these providers are less interested in meeting increasing payments requirements and more focused on leveraging the infrastructures they’ve built over the years to milk additional profi ts.

Our credit union needs to migrate to a more strategic approach, while ensuring we remain strong from the transaction side. It means reassessing things from an organizational perspective to ensure proper authority is given to the people responsible for monitoring the payments area, and making sure we remain relevant.

15credit union digest | april/may 2014 | members first

feature

Security, Convenience, and Cost

As credit unions get a handle on the payments juggernaut commanding the public’s attention, it all comes down to security, convenience, and cost.

So which one takes precedence?

“Security is riding along with the motivation for change, but it’s not the impetus,” said Brad Ganey, COO and senior vice president of Catalyst Corporate FCU in Plano, TX. “What consumers and businesses really want is convenience.”

About 23 percent of online households missed a bill payment or paid late in 2013 due to cash fl ow diffi culties or waiting until the last minute, according to Fiserv’s Annual Billing Household Survey. It’s just one of several “convenience” issues that real-time payments technology can help address.

As retailers, innovative start-ups, technology giants, and fi nancial institutions slowly upgrade the U.S. payments system, the cost of transactions to consumers is being eyed, Ganey said, especially those who are under-banked or unbanked. A surge in prepaid cards has swept the nation, oftentimes providing a cheaper alternative to checking accounts and debit cards.

But lost revenue in one area for credit unions can stimulate new opportunities elsewhere. “Credit unions cannot afford to ignore mobile technology,” he said.

Payment services is just one opportunity within mobile banking, yet increasingly important. From paying a monthly bill on the Internet to purchasing a cup of coffee in person, a credit union member’s smartphone has the potential to act as the all-in-one payment instrument, able to access credit and checking accounts.

Ganey thinks new regulations will shape how the mobile wallet world evolves more than any other factor.

“It’s reasonable to think there’s concern at the Federal Reserve and Consumer Financial Protection Bureau as to when the next big data breach will come down the pipeline,” Ganey said. “The perception could be that, on their watch,

Brad Ganey,

COO and SVP of

Catalyst Corporate FCU

new payments players have entered the fi nancial services space with nothing close to the oversight fi nancial institutions have.”

He added: “For any regulatory body trying to get their hands around this, it’s going to be a real challenge to catch up. Every credit union should have this on their watch list to see how it plays out.”

16 credit union digest | april/may 2014 | members first

The View from Down Under

Adrian Lovney touts a leading fact when discussing payments in “the land down under.” Over the past three years, the share of face-to-face Visa card payments in Australia that are contactless—via mobile phone, EMV-chip card, or another means—grew from zero to nearly 50 percent.

“Many successful innovations quickly make their way to Australia because of its self-contained geography, progressive business environment, and heavy penetration of technology by Australian consumers,” said Lovney, general manager of products and services for Credit Union Services Corporation Australia (CUSCAL), a Sydney-based credit union service organization.

As CUSCAL helps blaze a new trail on this giant island, it’s igniting the curiosity of credit union leaders in America. Lovney and his colleagues have stayed busy addressing U.S. credit unions on payments technology.

Where America is lagging in the payments progress department, it’s making up for elsewhere.

“Having recently spent time in Silicon Valley, I think the United States has a sophisticated and energetic start-up culture versus Australia,” Lovney said. “It’s a signifi cant factor.”

The mobile channel is progressively catching on in America. “Look at the experience consumers get from everyday applications, like shopping or streaming music and video,” Lovney said. “If they can get it from other organizations, why can’t they get it from their fi nancial institution? Why should it take 24 hours to receive a payment?”

Adrian Lovney, General

Manager of Products and

Services for Credit Union

Services Corporation

Australia (CUSCAL)

* All data is U.S.-based unless otherwise noted.

Prepaid Cards:Already

Popular—and growing

90 percent

of consumers use some type of payment card in a

given year.

$9.7percent

Growth of private-label payments from 2009 to 2012 (including Electronic Benefi ts Transfer transactions), an area that’s dominated by retailer gift cards.

Rise in both general-purpose and private-label payments from 2009 to 2012, which outpaced gains in all other noncash categories (credit, debit, ACH, and check).

16percent

33percentGrowth of

general-purpose payments from

2009 to 2012 (the fastest growing noncash form of

payment).

Sources: 2013 Fiserv Household Billing Survey; 2013 Accenture Consumer Electronics Products and Services Usage report; 2013 Federal Reserve

Payment Improvement Consultation Paper; 2013 Federal Reserve Consumers and Mobile Financial Services report; 2013 Retail Payments Global Consulting (RPGC) Group report; joint 2014 GFK Public Affairs and Corporate Communications/Associated Press survey results; 2013 Tufts University (Fletcher School) report; 2014 Credit Union National

Association (CUNA) Mobile Payments Survey; and 2012 Phoenix Marketing International survey.

feature

17credit union digest | april/may 2014 | members first

He said credit unions should collaborate on a mobile-payments system to share costs and enable fl exibility. The industry could leverage its trusted position to build a “comprehensive and rich user experience” so members can accomplish anything through one application.

“They could do this across multiple platforms and versions of software, yet be individually branded and tailored for specifi c credit unions,” Lovney said. “Cooperation and sharing of the relevant infrastructure costs among those who stand to benefi t is the best approach.”

The Omni-Channel Experience

In their quests for a payments solution, credit unions face an opportunity to unite together, according to Samantha Paxson, vice president of marketing for CO-OP Financial Services, a fi nancial technology company in Rancho Cucamonga, CA, and the nation’s largest credit union service organization.

“Credit unions should think of themselves as a category fi rst, and as individual innovators second,” Paxson said. Doing so would forge a powerful bond and help the industry as it modernizes its payment offerings.

CO-OP is one of several companies instigating change and assisting credit unions in payments transformation. In February it partnered with Alkami Technology, a digital-banking solutions provider, to give credit union members a fully integrated online and mobile banking bill-payment experience.

CO-OP says it’s also working to provide similar EMV functionality that was recently announced by Visa and First Data’s STAR Network. Those two organizations have agreed to share Visa’s common debit solutions licensing agreement to give card issuers, acquirers, and merchants “a streamlined and cost-effective approach” for EMV card adoption, a news release states.

Additionally, “CardNav by CO-OP” will be released later this year, Paxson said. The card-control-and-alert product is new to the credit union industry. Members will be able to customize security parameters and receive an alert via smartphone when their card information is used for an

Samantha Paxson,

VP of Marketing for

CO-OP Financial Services

unauthorized transaction, giving them the option of turning the card off immediately.

CO-OP is reminding credit unions that consumers are looking for an “omni-channel experience—something that empowers them, is beautiful, and effortless,” Paxson said.

“We’re fi nding that an enhanced experience is worthwhile creating, but you can’t get to it unless you develop quick-and-easy access,” Paxson said. “If you can achieve something that’s frictionless, then you can start thinking about the ‘wow factor’ next.”

She added: “The consumers credit unions are trying to reach are hungry for experiences similar to the types of companies and brands they interact with all the time. And when it comes to payments, they want solutions that are simple and easy—the most convenient way of interacting.”

: California & Nevada Credit Union Leagues’ Largest Event of the Year!What’s in it for you?

• Collaborate with industry leaders• Hear from thought-provoking, future-focused strategists • Gain insights on innovative solutions• Engage in breakout sessions targeting hot-topics • Explore new partnership opportunities • Get the big picture perspective

Featuring Earvin “Magic” Johnson, NBA legend and successful entrepreneur.More information to come soon: amc.ccul.org

REACH 2014 | Annual Meeting & ConventionOctober 20–22 | JW Marriott L.A. Live

Earvin “Magic” Johnson

19credit union digest | april/may 2014 | members first

The Fair Debt Buying Practices ActBy Thomas H. Wolfe, Managing Partner of Moore Brewer Wolfe Jones Tyler & North

legal

California Senate Bill 233, effec-tive Jan. 1, 2014, enacted the Fair Debt Buying Practices Act.

It added new Civil Code §1788.50, et seq., which sets out the conditions that must be met before purchasers of charged-off consumer debt (“debt buy-ers”) can begin collection efforts.

It is intended to address concerns about the adequacy of documentation required to be maintained to support the collection of debt purchased by debt buyers.

Who Is a ‘Debt Buyer’?A debt buyer is a person or entity

regularly engaged in the business of purchasing charged-off consumer debt for collection purposes, whether it col-lects the debt itself, hires a third party for collection, or hires an attorney for collection litigation.

It does not include any person or entity that acquires a charged-off con-sumer debt incidental to the purchase of a portfolio predominantly consisting of consumer debt that has not been charged off.

A credit union would not be con-sidered a debt buyer.

Why Does It Matter to CUs?Although credit unions are not

debt buyers, it impacts the type and quality of documentation that initial creditors must have.

In the event a loan goes into default and is ultimately sold as charged-off debt, failure to have the necessary docu-mentation would negatively impact the

ability of a potential debt buyer to collect on it, reducing its value.

Credit unions can expect con-tracts with a prospective debt buyer to include these minimum documentation requirements.

Initial DocumentationBefore they can take action to col-

lect, a debt buyer must have documen-tation showing the following:

• Proof that it is the sole owner of the debt, or has the right to assert such rights.

• Account balance at charge-off, and an explanation of the amount, nature, and reason for any and all post-charge-off interest and fees.

• Date of default or last payment.• Name and address of both the

creditor and debtor, and the origi-nal charged-off account number.

• Complete chain of title on the account, if bought and sold mul-tiple times.

A debt buyer cannot make any written statement to the debtor in an effort to collect unless it has a copy of the contract or other document evi-dencing the debtor’s agreement to the debt. If no signed contract is available, the debt buyer can be provided with a copy of a document provided to the debtor while the account was active, demonstrating that the debt was incurred by the debtor, e.g., a state-ment showing last payment or pur-chase on a revolving credit account.

Debt Buyer ObligationsDebt buyers must provide the

information and documents above to the debtor at no charge within 15 calendar days of receipt of the debtor’s written request for proof. If they can-not, the debt buyer must cease all collection efforts until it can.

In addition, a debt buyer must provide all debtors with whom it has contact an active mailing address for such requests, and it may also pro-vide an e-mail address through which information and documents can be delivered, if the parties agree.

Initial Notice/Disclosures and Time-Barred Debt

The new law requires debt buyers to include a separate prominent notice (minimum 12-point type) with its fi rst written communication with a debtor explaining his or her rights.

An additional notice must be included for any time-barred debt informing the debtor that, because of the age of the debt, they cannot be sued for it, and whether or not it can still be reported to a credit report-ing agency per §605 of the Fair Credit Reporting Act (FCRA). The specifi c text of the notices is set out in Civil Code §1788.52(d).

If a language other than English is principally used by the debt buyer in the initial oral contact with the debtor, the notice must be provided in that language within fi ve working days.

In addition, the new law sets out the conditions for settlement agree-ments between a debt buyer and a debtor, as well as what information and supporting documentation must be presented in any action brought by a debt buyer on a consumer debt.

Any waiver of the provisions with-in FCRA is contrary to public policy, and is void and unenforceable.

20 credit union digest | april/may 2014 | members first

By Clarissa Martin, Research and Information Consultant

asked & answered

Limiting Fair-Lending Risk in Autos

Asked: How can credit unions limit their fair-

lending risk in indirect lending?

Answered: Institutions subject to Consumer Financial Pro-tection Bureau (CFPB) juris-

diction, including credit unions and indirect auto lenders, should take steps to ensure they are operating in compli-ance with the Equal Credit Opportu-nity Act (ECOA) and Regulation B as applied to dealer-markup and compen-sation policies.

These steps may include, but are not limited to:

• Imposing controls on dealer-markup and compensation policies, or otherwise revising dealer-markup and compensa-tion policies; and monitoring the effects of those policies in the manner described below, so as to address unexplained pricing disparities on a prohibited basis.

• Eliminating dealer discretion to mark up buy rates, and fairly compensating dealers using another mechanism—such as a flat fee per transaction—that does not result in discrimination.

Another important tool for limiting fair-lending risk in indirect auto lend-ing is developing a robust fair-lending compliance management program. The following are features of a strong program:

• An up-to-date policy statement.• Regular training for all employ-

ees involved with any aspect of the institution’s credit transac-tions, as well as all officers and board members.

• Ongoing monitoring for compli-ance with policies and proce-dures.

• Ongoing monitoring for compli-

ance with other poli-cies and procedures that are intended to reduce risk (such as controls on dealer discretion).

• Review of lending policies for potential violations, including potential disparate impact.

• Depending on the size and complex-ity of the financial institution, a regular analysis of loan data in all product areas for potential disparities on a prohibited basis in pricing, underwriting, or other aspects of the credit transaction.

• Regular assessment of the mar-keting of loan products.

• Meaningful oversight of compli-ance by management and, where appropriate, the financial institu-tion’s board of directors.

For some lenders, additional compliance-management components may be necessary to address signifi-cant fair-lending risks. For example, indirect auto lenders that retain dealer-markup and compensation policies may wish to address the fair-lending risks of such policies by implementing systems for monitoring and corrective action by:

• Sending communications to all participating dealers explaining the ECOA, stating the lender’s expectations with respect to ECOA compliance, and articu-lating the dealer’s obligation to mark up interest rates in a non-discriminatory manner in instances where such mark-ups are permitted.

• Conducting regular analyses of both dealer-specific and portfolio-wide loan pricing data for potential disparities on a

prohibited basis resulting from dealer mark-up and compensa-tion policies.

• Commencing prompt corrective action against dealers—includ-ing restricting or eliminating their use of dealer mark-up and compensation policies or exclud-ing dealers from future transac-tions—when analysis identifies unexplained disparities on a prohibited basis.

• Promptly remunerating affected consumers when unexplained disparities on a prohibited basis are identified either within an individual dealer’s transactions or across the indirect lender’s portfolio.

Consumer Financial Protection Bureau’s Auto Finance Bulletin: http://files.consumerfinance.gov/f/201303_cfpb_march_-Auto-Finance-Bulletin.pdf

CU PolicyPro model policy (Equal Credit Opportunity Act): https://policypro.leagueinfosight.com/mem/ops_manual/adm

National Credit Union Administration’s Fair-Lending Examination and Compliance Assistance: www.ncua.gov/Resources/Pages/LFCU2013-02.aspx

Helpful Resources

21credit union digest | april/may 2014 | members first

By Arnold Ramirez, Research and Information Consultant

research & information

Prepaid Cards: Expiration Disclosures

My niece recently found a Visa prepaid card at home and asked me if it was still valid,

but I wasn’t sure what to tell her. I knew there were rules regarding the expiration of general-use prepaid cards, yet wasn’t too familiar with them.

A little research gave me my answer. According to Regulation E §1005.20, there are certain conditions that must be met for an issuer or seller of a general-use prepaid card which determine whether an expiration date may be applied.

Before a general-use prepaid card is purchased, the issuer or seller must disclose to the consumer the informa-tion about dormancy, inactivity, service fee, expiration date, and the toll-free telephone number. If the issuer or seller has a website, it must also disclose that site so the consumer can obtain fee information.

These disclosures must be made on the card. A disclosure made in an accompanying terms-and-conditions document—or on the packaging sur-rounding a certificate or card, or on a sticker or other label affixed to the certificate or card—does not constitute a disclosure on the certificate or card.

The fees—and terms and condi-tions of expiration—that are required

to be disclosed prior to purchase may not be changed after purchase.

Generally speaking, a general-use prepaid card may not have an expira-tion date, unless:

• The credit union has established policies and procedures to pro-vide consumers with a reason-able opportunity to purchase a card with at least five years remaining until the card expira-tion date.

• The expiration date for the underlying funds is at least the later of:º Five years after the date the

gift certificate was initially issued, or the date on which funds were last loaded to a general-use prepaid card.

º The card expiration date, if any.

• The following disclosures are provided on the card, as appli-cable:º The expiration date for the

underlying funds; or if the underlying funds do not expire, then that fact must be stated.

º A toll-free telephone number and, if one is maintained, a website that a consumer may

use to obtain a replacement card after the card expires if the underlying funds are available.

º Except where a non-reload-able card bears an expiration date that is at least seven years from the date of manu-facture, a statement that’s disclosed with equal promi-nence and in close proximity to the card expiration date that states:– The card expires, but the

underlying funds either do not expire or expire later than the card.

– The consumer may contact the issuer for a replacement card.

• No fee or charge is imposed on the cardholder for replacing the general-use prepaid card or for providing the cardholder with the remaining balance in some other manner prior to the funds expiration date, unless such card has been lost or stolen.

Since the expiration of the card may vary from that of the underlying funds, credit unions will need to be sure the expiration date rules are prop-erly applied when establishing the poli-cies and procedures for the credit union regarding general-use prepaid cards.

These requirements apply to any general-use prepaid card sold to a consumer on or after Aug. 22, 2010, or provided to a consumer as a replace-ment for such card.

General-use prepaid cards issued by the credit union before the effective date of the rules may expire in accor-dance with the original terms of the cards.

As for the card my niece found, it turns out the funds had already been exhausted—she had just neglected to dispose of it.

22 credit union digest | april/may 2014 | members first

Dwight Johnston, Vice President and Chief Economist

economic perspective

Jobs, Wages, Confidence, and the Future

People borrow money for many purposes. Buying a home, remod-eling, purchasing a new car, vaca-

tions, and weddings come to mind.But what gives consumers confi-

dence to borrow when the expenditure in mind isn’t absolutely necessary?

It comes down to job security and prospects for higher wages. Job secu-rity comes from holding one, or from the sense that other jobs—perhaps even better jobs—are available.

Feeling More SecureThe U.S. job market isn’t exactly

on fire, but one component of The Con-ference Board’s consumer confidence report paints a positive picture. The Employment Trend Index is derived from several questions regarding job security and prospects. The index peaked in 2006 at 122 and plunged to a low of 87 in 2009. It’s now 116. Work-ers are clearly feeling more secure.

Wage growth has been stuck at 2 percent for three years. Since the reces-sion, businesses have been rewarded for their ability to squeeze labor costs. With so much “slack” in the labor market, they didn’t have to worry about employ-ees leaving for better-paying jobs.

Most economists believe this “slack” condition will persist and hold down wages. They point to the low participation rate and argue it is evidence of “slack.”

However, demographic trends impacting the available labor pool can change, and no change is bigger than the wave of baby boomers, with approx-imately 1.5 million retiring every year.

Another trend is materializing from the 3.6 million longer-term unemployed (more than six months). According to a recent Princeton University study, the rate of permanent labor-force dropouts has risen to 24 percent from 10-15 per-cent, historically. It is likely to escalate as unemployment benefits expire.

Before 2005, economists estimated the United States needed to produce

an average of 150,000 nonfarm payroll jobs per month for the job market to remain steady. That presumed level was lowered to between 100,000 and 125,000 that year.

Nonetheless, a study last year by the Federal Reserve Bank of Chicago estimates that monthly growth of only 80,000 meets current demographic needs. The Philadelphia and St. Louis Fed banks recently confirmed that study.

It means the nation has exceeded our demographic job growth needs by 100,000 jobs on a monthly basis for the past three years and counting.

Anecdotally, we are already seeing a tighter labor market. Many manufac-turers are reporting difficulty in hiring workers and are resorting to ramping up wages to steal laborers while retain-ing existing workers.

Technology wages are estimated to have increased by 10 percent last year. The squeeze is also on in the construc-tion industry as construction ramps up.

Silver Linings for CA and NVWhat does this mean for Califor-

nia and Nevada?California is at the forefront of

technology, and gains in the trade sec-tor are expected to continue.

But perhaps one of the best stories of 2014 will be in construction, and not just residential. I expect strong gains in home construction this year. Since 2007, builders have been “under-building” after a four-year overbuild-ing binge.

However, let’s look at the big picture, including non-residential construction. Building permits for both residential and commercial in the last quarter of each year are a strong indicator of activity in the upcoming year. A build-up in permits in late 2012 accurately predicted a construction gain in 2013, and the permit numbers for late 2013 surged, according to the California Department of Finance.

Also, the annualized value of residential permits for the last three months of 2012 jumped from an average of $17 billion to $22 billion in 2013. The value of non-residential permits jumped off the charts from $14 billion to $26 billion. This means more job growth in an already tight job sec-tor, which means higher wages.

The bottom line is, California is not only looking at perhaps a surpris-ingly strong year of job growth in industries that pay well, but one where wages exceed expectations.

For Nevada, the picture is less clear, but construction does appear to be trending up as fenced-off develop-ments in Las Vegas restart and apart-ment construction is revived. Nevada will benefit the most when rising wages in California and the rest of the country bring more visitors to the state.

For credit unions, the impact of job growth accompanied by rising wages means consumers will finally be more confident about borrowing for a wide array of postponed needs and wants.

23credit union digest | april/may 2014 | members first

$0$5mil

$10mil$15mil$20mil$25mil$30mil$35mil$40mil

Dec

-200

2

Dec

-200

3

Dec

-200

4

Dec

-200

5

Dec

-200

6

Dec

-200

7

Dec

-200

8

Dec

-200

9

Dec

-201

0

Dec

-201

1

Dec

-201

2

Dec

-201

3

By Dwight Johnston, Vice President and Chief Economist

market performance

Which Lending Sectors Will Gain?

In my companion column, we make our case that the California and Nevada economies will exceed

expectations in 2014.However, which loan sectors should

credit unions focus on?Looking at the pie chart, it’s obvi-

ous the mortgage sector is the largest and most likely area for growth given the positive outlook for housing. But when you look at the concentration level of first mortgages and consider interest rate risk, credit unions in our two states will not likely add significantly to these portfolios.

The second largest category is auto lending, but sales have reached equilibrium. After a four-year depres-sion in sales, the three-year recovery has returned them to a “normal” level.

I expect auto sales will be roughly equivalent to their 2013 level. Credit union auto loans have become the “star” sector in overall growth, but a rising tide has lifted all boats. Contin-ued growth will be difficult.

So far, this doesn’t sound very good for loan growth. Let’s look at the smaller pieces of the pie.

One Stand-Out SectorOne stand-out sector is “Other Real

Estate Loans,” a category that’s primarily home equity loans or home equity lines of credit (HELOC). At the end of 2006, this sector constituted 17.28 percent of all credit union loans, but now makes up only 12 percent, as HELOCs dropped 40 percent from their peak (see the Other Real Estate Loans: CA and NV CUs chart).

There was a small uptick in fourth quarter 2013, but this could be just the beginning. DataQuick reported that HELOCs jumped 48 percent in 2013 from 2012. That sounds impressive, but compare the 48,000 HELOCs granted last year to the 550,000 lines granted at their peak. There is room to grow.

With the dramatic improvement in home prices in California and Nevada, the pool of eligible borrowers has increased exponentially. If jobs and

wages continue rising, homeowners are more likely to borrow against their homes for improvements.

This won’t be similar to the boom days. Credit unions will have much more conservative loan-to-value maximums. But the growth potential is there.

For every mortgage loan you made on a home purchase from 2008 or 2009 until early 2013, you have a member who likely has a significant amount of equity built in. That’s a great pool to tap into.

Other Bright AreasCredit card debt should finally

begin to grow consistently again as con-

sumers gain on the wage front. Busi-ness lending has been good and will get better as the economy improves.

I would also expect to see greater demand for personal loans. This is borne out by a surge in person-to-per-son loans on various websites—loans that should be going to credit unions. But credit unions seem to have lost interest in the “old-fashioned” loans. This might be the time to get reac-quainted.

The backdrop for loan growth is perhaps better than it has been in several years, but it’s up to each credit union to identify and seize the opportunity.

Other Real Estate Loans: CA and NV CUs

$12,093,448(6%)

$5,859,654(2.9%)

$47,196,775(23.6%)

$104,545,321(52.2%)

$23,990,621(12%)

$1,950,927(1%)

$382,328(<1%)

$4,099,132(2%)

Unsecured Credit CardsOther Unsecured Loans

Auto LoansFirst Mortgages

Other Real Estate Loans

Non-Real Estate MBLsStudent Loans

Other Loans

*Source: Callahan and Associates. Data as of Dec. 31, 2013.

Loan Composition: CA and NV CUs

24 credit union digest | april/may 2014 | members first

credit union solutions

25credit union digest | april/may 2014 | members first

Members Dine Out While Fighting Hunger

credit union solutions

In today’s economy, giving a little can go a long way.

The California and Nevada Credit Union Leagues, along with mem-ber credit unions and their members, are actively fighting hunger in their local communities. In 2013, more than 11,800 meals were provided by credit unions and their members across California.

The secret? MOGL.MOGL is the largest restaurant

rewards platform in California where users earn 10 percent cash for dining out at their favorite restaurants, while donat-ing meals to people in need. Since its inception, close to 500,000 meals have been donated through MOGL, and this year is already off to a phenomenal start.

Here’s a breakdown of meals donated by MOGL-participating restau-rants in California in January 2014:

* San Francisco—3,545* Los Angeles—2,141

* Orange County—1,046* San Diego—12,990* Ventura—4,383 The process is simple: MOGL is a

mobile app with no coupons, punch cards, or check-in hassles, and works seamlessly with a credit union’s exist-ing card-reward program. Members simply sign up by linking their pay-ment cards to MOGL.

When they dine at a participat-ing restaurant and pay with that card, they earn dollars back. The app then prompts the member to decide how much of that cash they want to keep or donate to feed the hungry. Every 20 cents donated equals one meal.

More than a dozen League-mem-ber credit unions have either launched or plan to use MOGL, representing more than 900,000 members who take advantage of earning money or helping

others in need. Nearly 2,000 restau-rants are currently enrolled in MOGL.

In addition to social good, MOGL allows credit unions to provide more benefits to their members at no additional cost, facilitating loyalty by encouraging them to use their credit union cards more often.

Founded in 2010, MOGL is the proud recipient of the Best Food APP of 2012 by Food & Beverage Magazine, as well as named one of the Best Mobile Startups of 2012 by LAPTOP Magazine.

For more information, contact Leagues Business Analyst Lou Lou Degadillo at 909.212.6019 or [email protected].

Where do Credit Unions Stand?

“Credit unions have been there to protect our

member-owners, both their information and

their money. We should be demanding the same of the retailers who have

been receiving a free ride in protecting their

customers’ information.”

By Greg Badovinac Compliance Officer, Western FCU

Closing Thoughts

26 credit union digest | april/may 2014 | members first

Recently, credit unions (and banks) have experienced more breaches of information at large

national retail organizations. These were not the first (T.J. Maxx comes to mind) and, unfortunately, probably will not be the last.

Credit unions cancelled and reordered thousands and thousands of debit and credit cards as a result. Member protection was publicly the reason for this action.

But reducing our losses due to the use of stolen information was the primary reason.

During the height of the media attention following the Target breach, I read about one of the victims. Her large New York-based money center bank (with five letters) had not reis-sued her debit card.

But her credit union had changed her debit card number three times. She found that hard to deal with since she had set up payments to her credit union account using the debit card. She was strongly considering giving up her credit union account for one at the bank.

This is one of the hard business decisions credit union executives have to deal with: protecting the credit union (because federal consumer protection law imposes those losses on the finan-cial institution rather than the member) versus member convenience. I am glad that compliance professionals do not have to make those decisions, or deal with the affected members.

It is anticipated the move to encrypted “chip” cards before the 2015 EMV (Europay-MasterCard-Visa) deadline will help reduce fraud losses

from more sources than just informa-tion breaches. However, credit unions will have to absorb costs for new cards, member education, and back-office functions as part of this process. Mer-chants will have similar increased costs for new terminals and devices that can work with the “new” technology.

But two questions remain to be answered. Will credit unions devote the time and resources to issue the cards even though the features of that chip card cannot be fully utilized? Second, will the merchants pay for the special terminals when the cards are not widely used in the interim?

I do not know. But I expect finan-cial institutions will step up first for the protection of their customers and members, while knowing the financial benefits will be earned at a later time.

The question in the meantime that credit unions and banks should be asking policymakers at the federal and state level is: “When are retailers going to be required to secure the private, non-public personal information of their customers?”

We have been required to do so for the last decade or so. We absorb the costs involved when a breach occurs. We are the ones that find out six or eight months after a breach that it occurred and have to reissue the cards without any solid information to tell our members.

Credit unions have been there to protect our member-owners, both their information and their money. We should be demanding the same of the retailers who have been receiving a free ride in protecting their customers’ information.

+ Curriculum covers Strategic Planning, Operations, Finance, Marketing, Lending, Human Resources, Technology, Business Development, Economics, Business Law, Communications, Leadership, and much more

+ Highly concentrated academic training over three yearly two-week terms