Paying International Visitors Kristina Sparks, FMS-Tax Lynn Schoch, International Services.

37

Paying International Visitors Kristina Sparks, FMS-Tax Lynn Schoch, International Services

-

date post

21-Dec-2015 -

Category

Documents

-

view

221 -

download

0

Transcript of Paying International Visitors Kristina Sparks, FMS-Tax Lynn Schoch, International Services.

Paying International Visitors

Kristina Sparks, FMS-Tax Lynn Schoch, International Services

Once upon a time . . .

. And they all lived happily(?) every after.

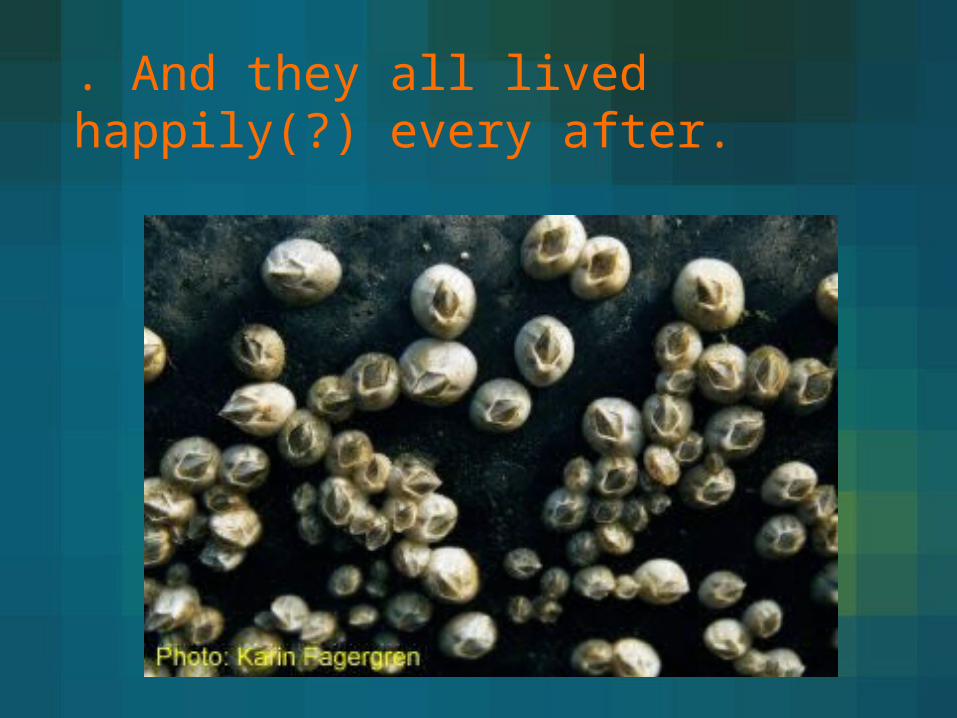

Before the visit Figure out the right visa type (OIS)

During the visit Get documents and signatures.

(Dept)

After the visit Apply tax treaty benefits and

complete payment (FMS-Tax)

Paying International Visitors

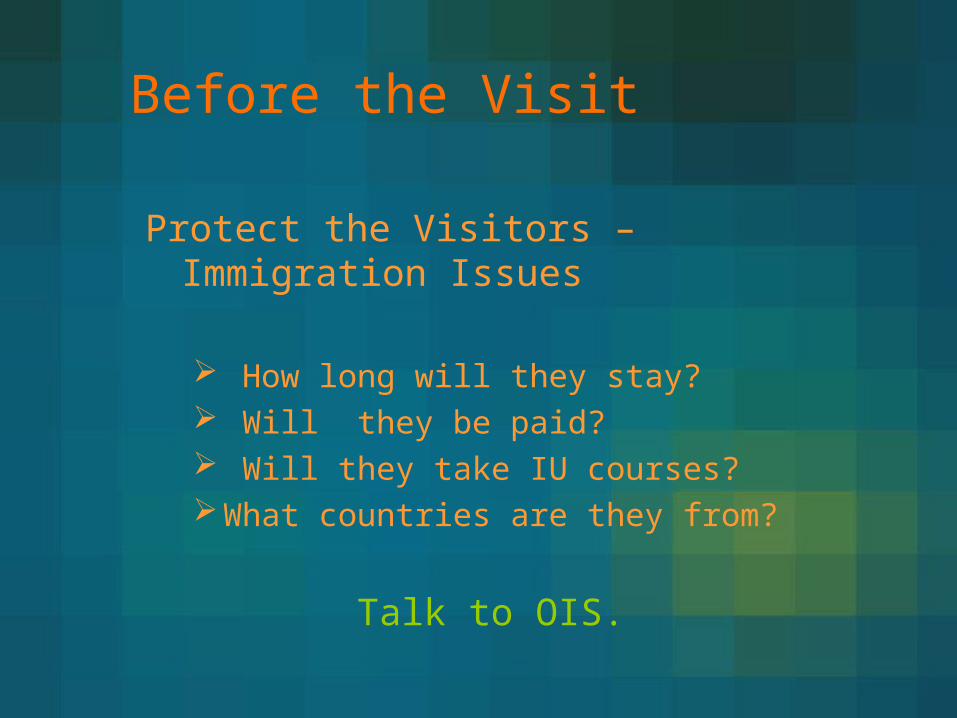

Before the Visit

Protect the Visitors – Immigration Issues

How long will they stay? Will they be paid? Will they take IU courses?What countries are they from?

Talk to OIS.

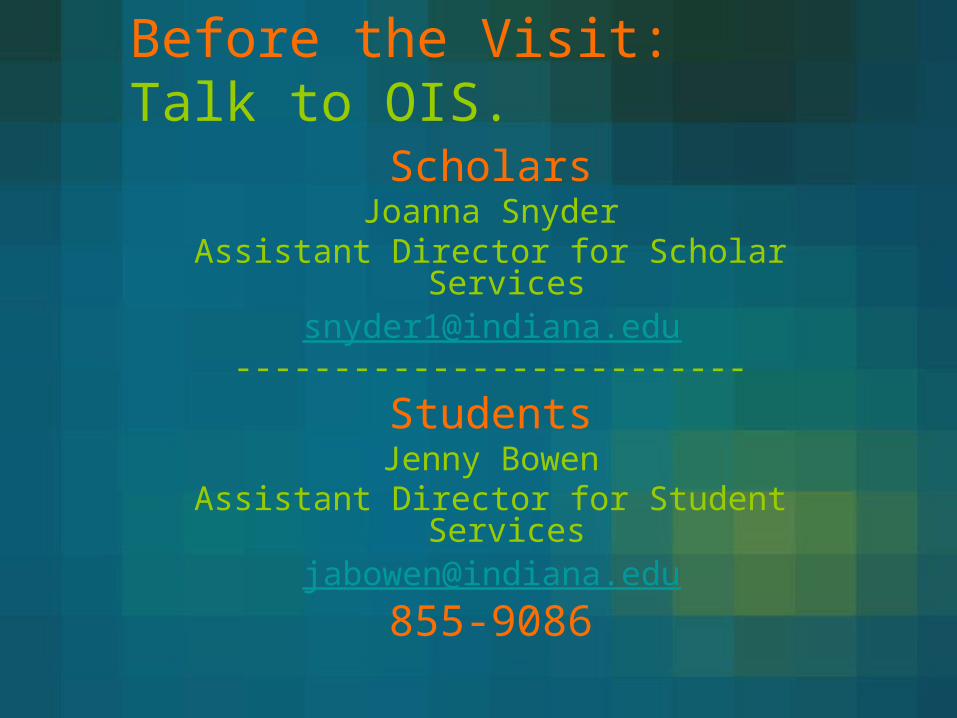

Before the Visit: Talk to OIS.

ScholarsJoanna Snyder

Assistant Director for Scholar [email protected]

--------------------------

StudentsJenny Bowen

Assistant Director for Student [email protected]

855-9086

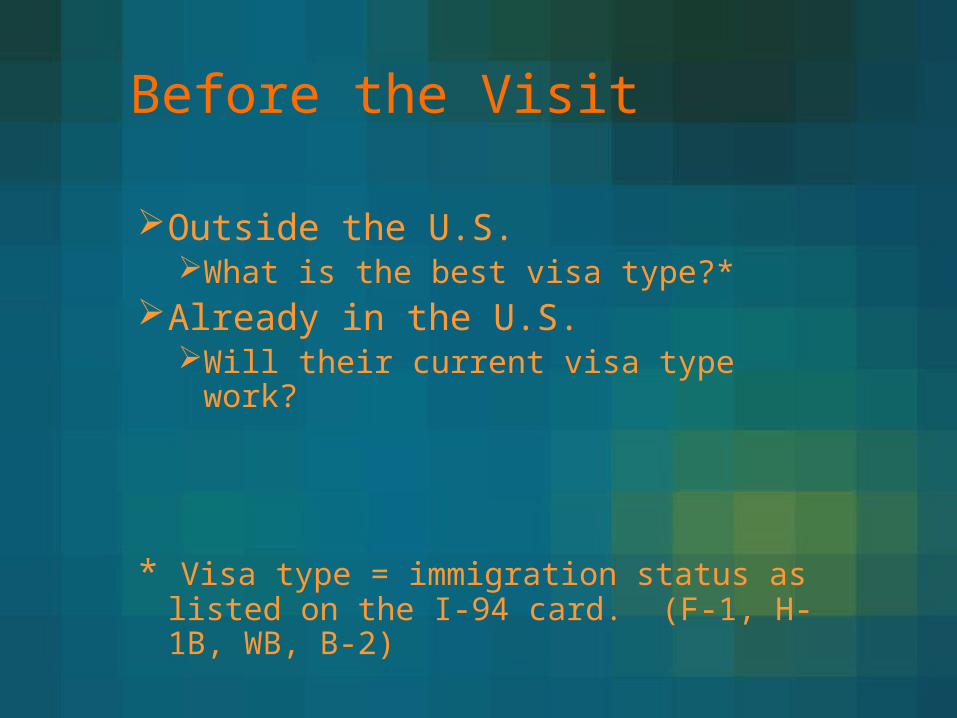

Before the Visit

Outside the U.S. What is the best visa type?*

Already in the U.S.Will their current visa type work?

* Visa type = immigration status as listed on the I-94 card. (F-1, H-1B, WB, B-2)

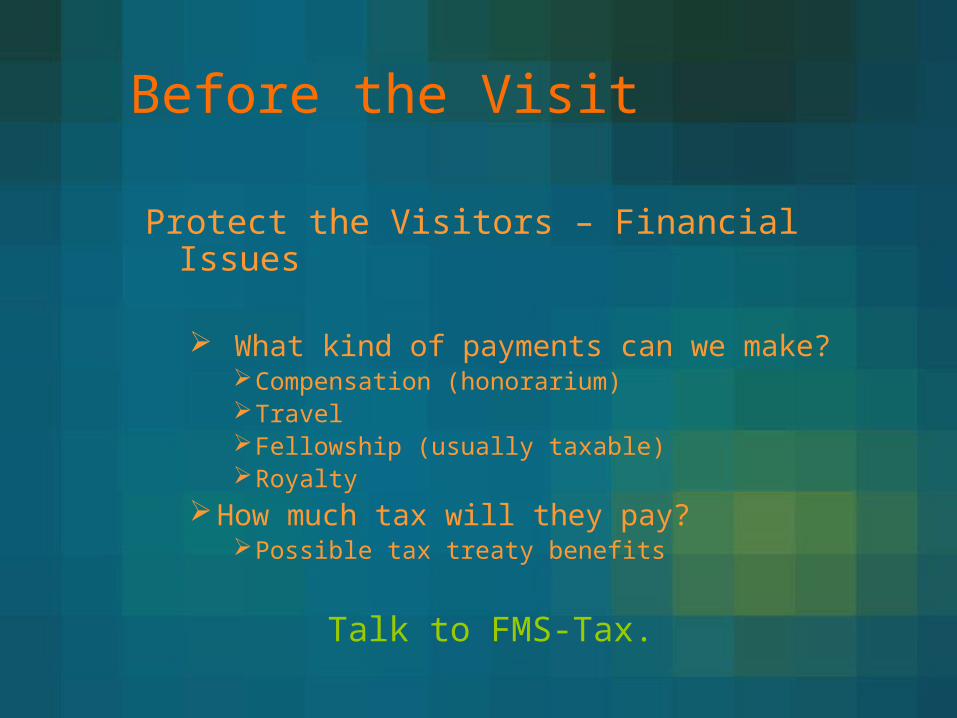

Before the Visit

Protect the Visitors – Financial Issues

What kind of payments can we make?Compensation (honorarium)TravelFellowship (usually taxable)Royalty

How much tax will they pay?Possible tax treaty benefits

Talk to FMS-Tax.

Before the Visit

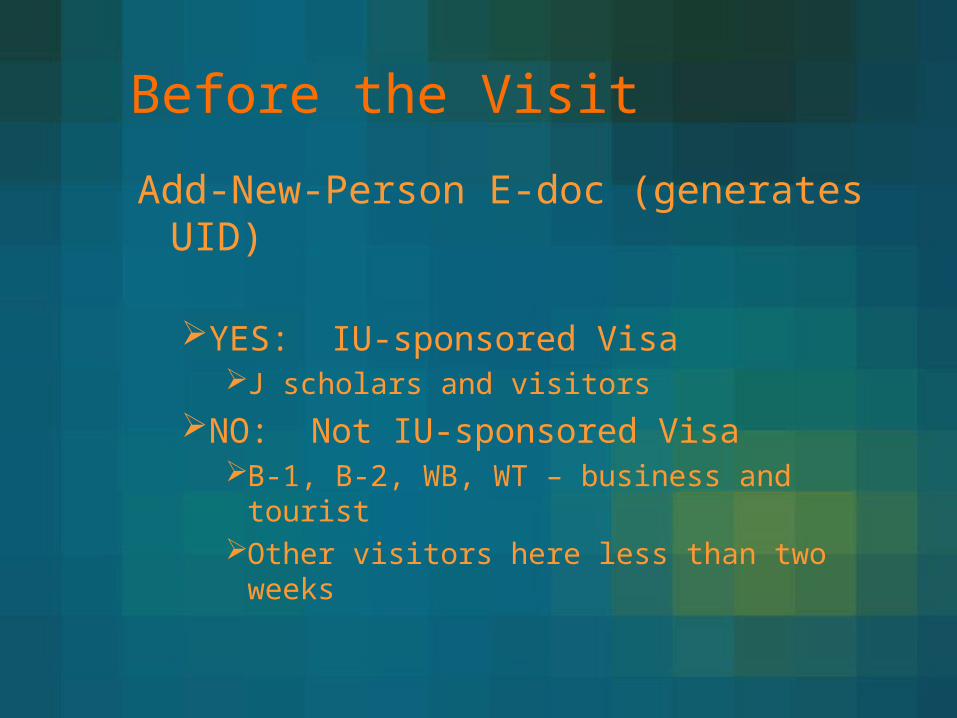

Add-New-Person E-doc (generates UID)

YES: IU-sponsored Visa J scholars and visitors

NO: Not IU-sponsored VisaB-1, B-2, WB, WT – business and touristOther visitors here less than two weeks

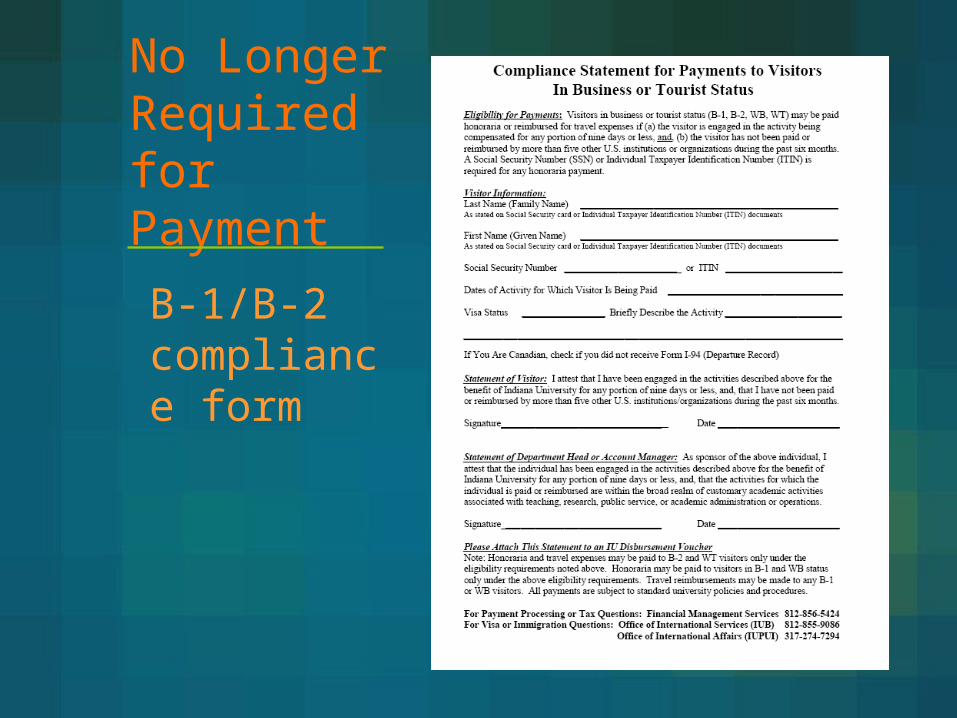

No Longer Required for Payment

B-1/B-2 compliance form

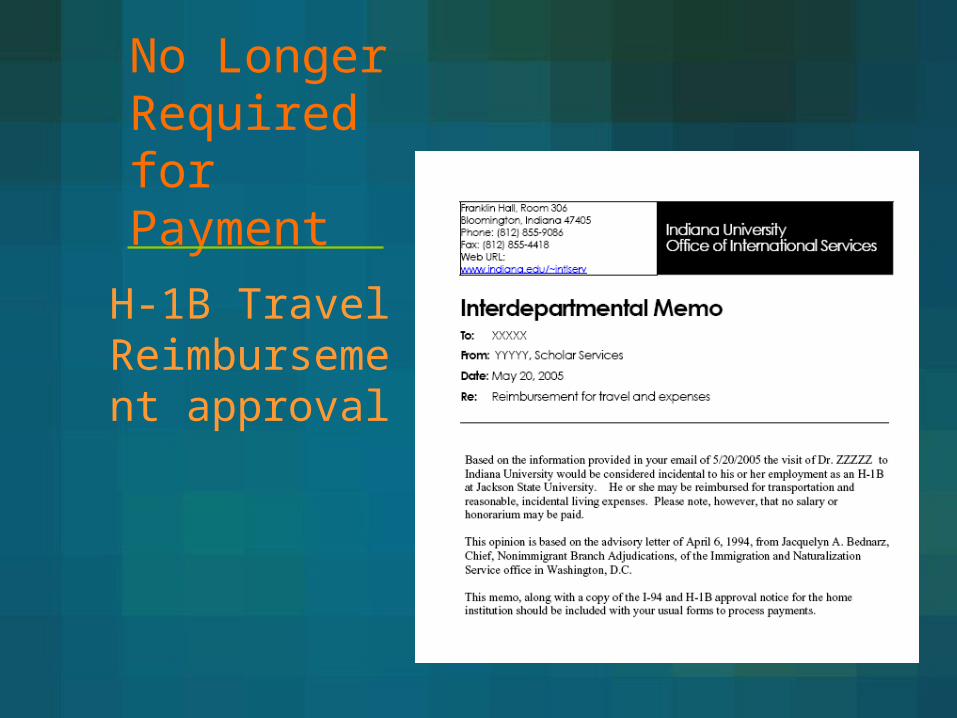

No Longer Required for Payment

H-1B Travel Reimbursement approval

No Longer Required for Payment

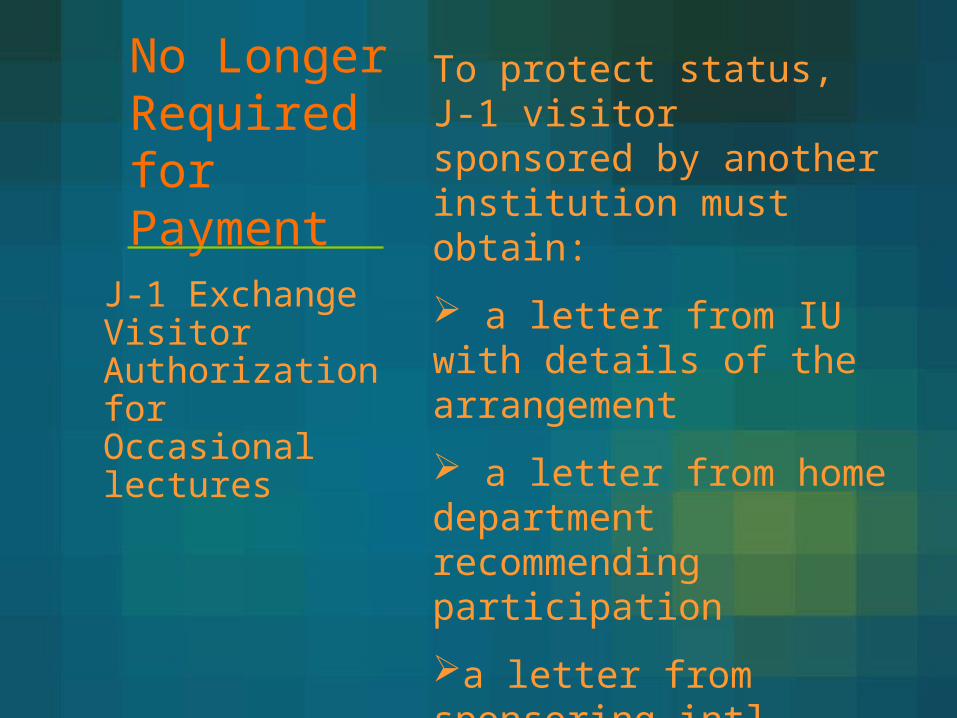

J-1 Exchange Visitor Authorization for Occasional lectures

To protect status, J-1 visitor sponsored by another institution must obtain:

a letter from IU with details of the arrangement

a letter from home department recommending participation

a letter from sponsoring intl advisor noting compliance with regulations.

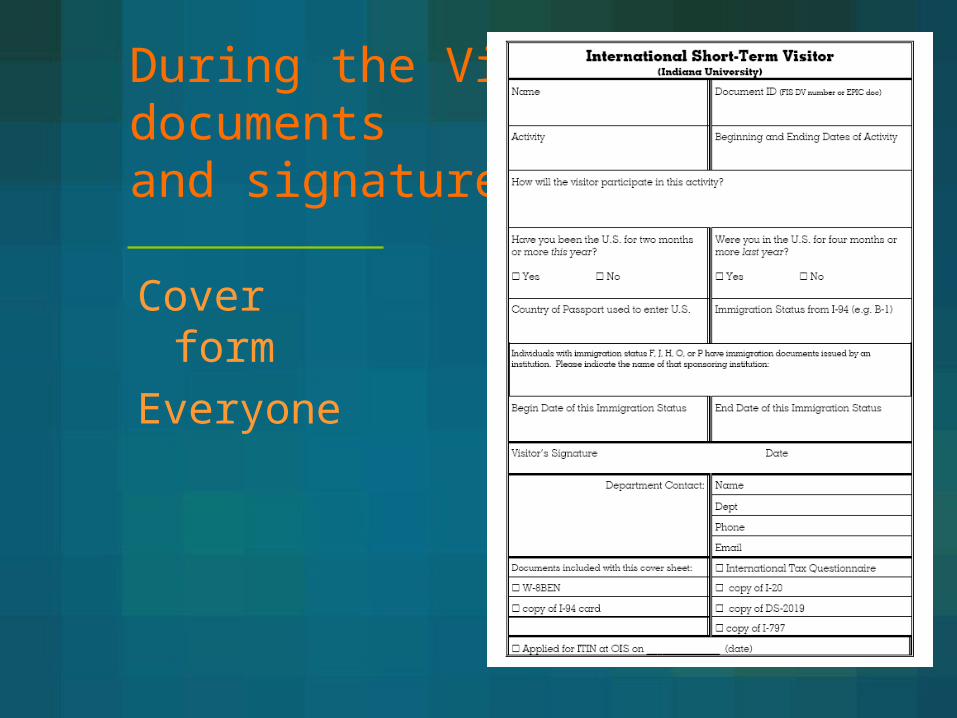

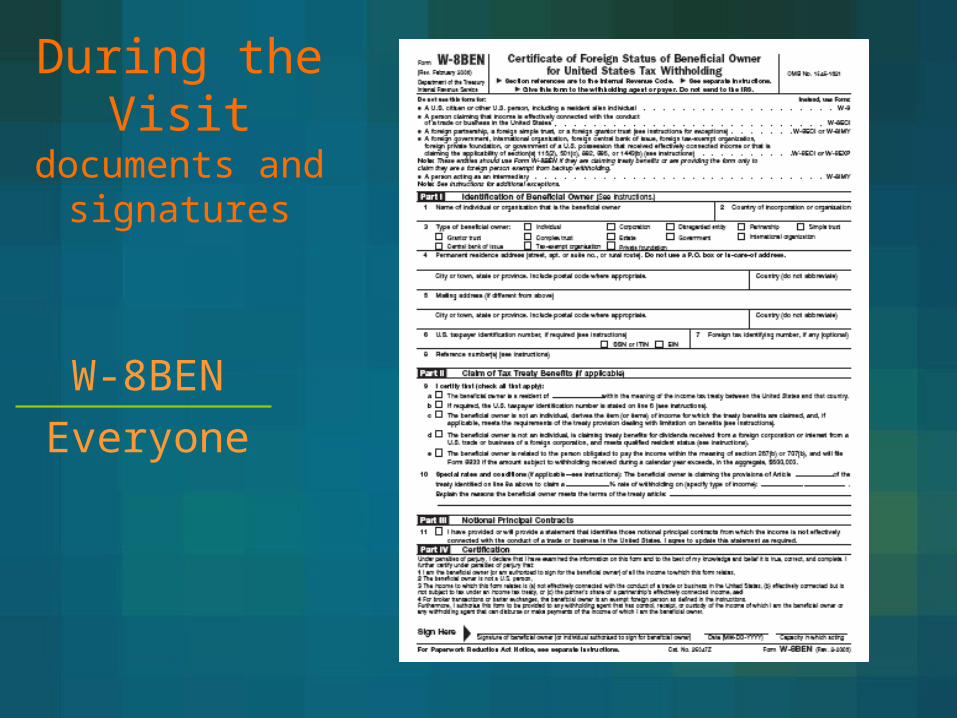

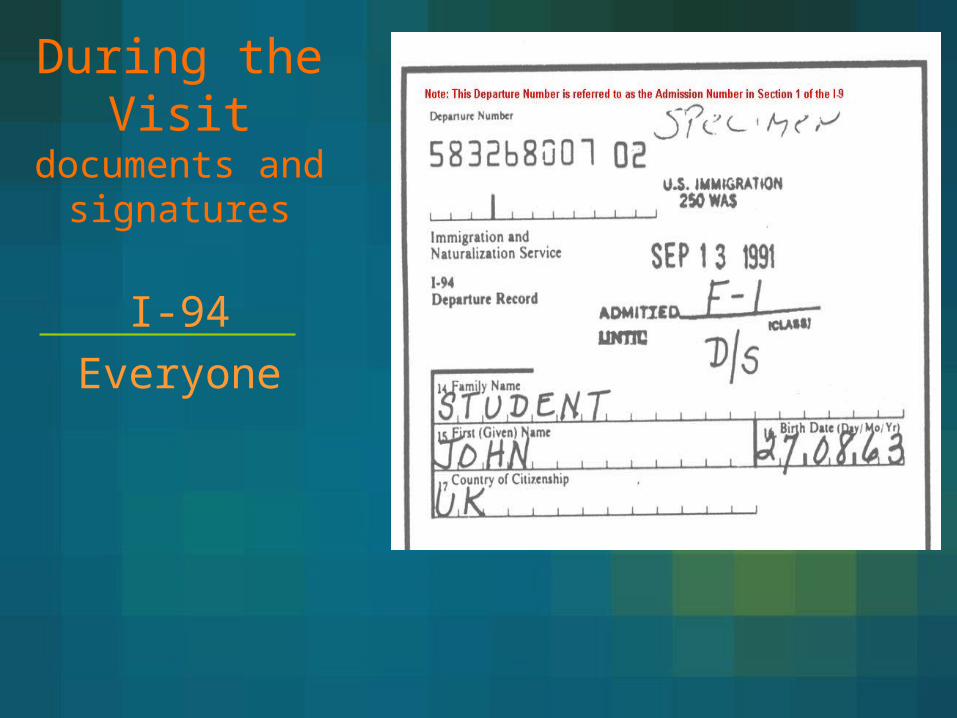

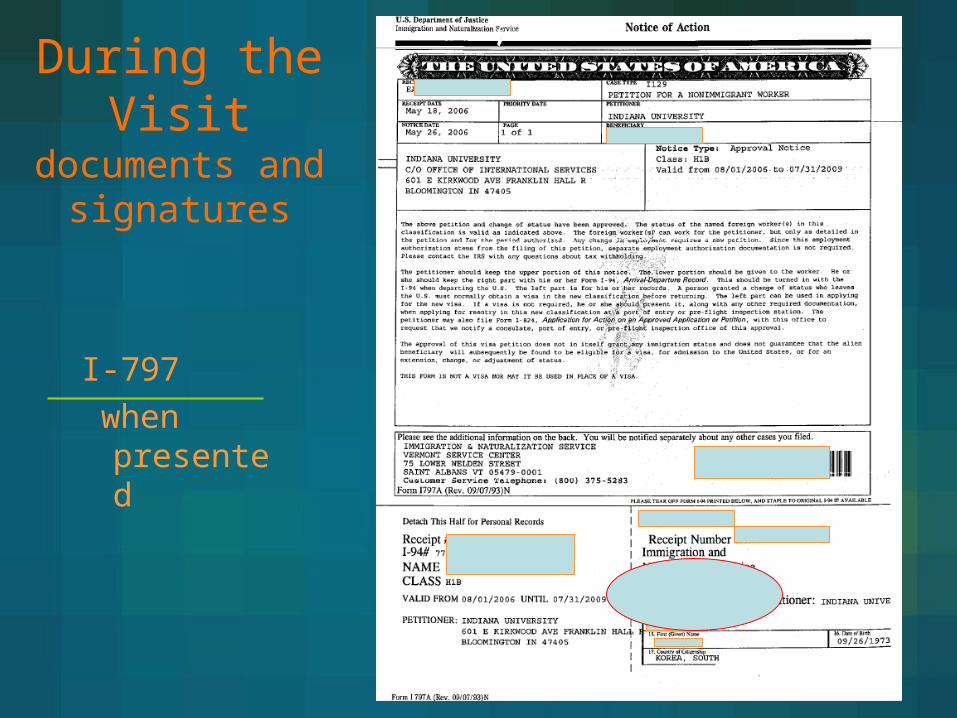

During the Visit:documents and signatures

Cover form

Everyone

During the Visit

documents and signatures

W-8BENEveryone

During the Visit

documents and signatures

I-94Everyone

During the Visit

documents and signatures

I-797 when

presented

During the Visit

documents and signatures

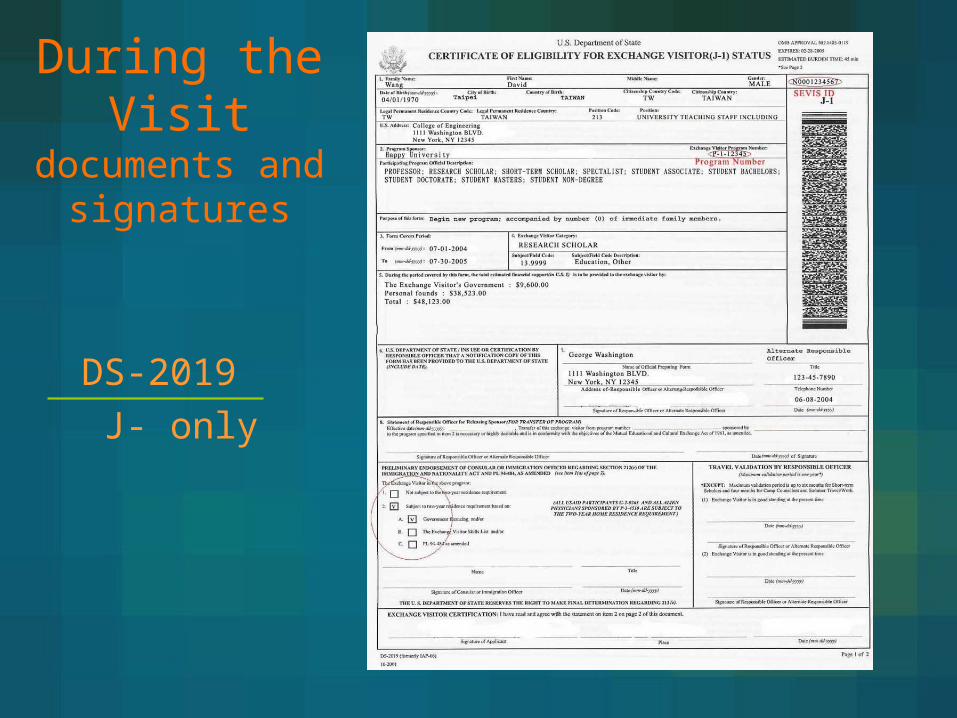

DS-2019 J- only

During the Visit

documents and signatures

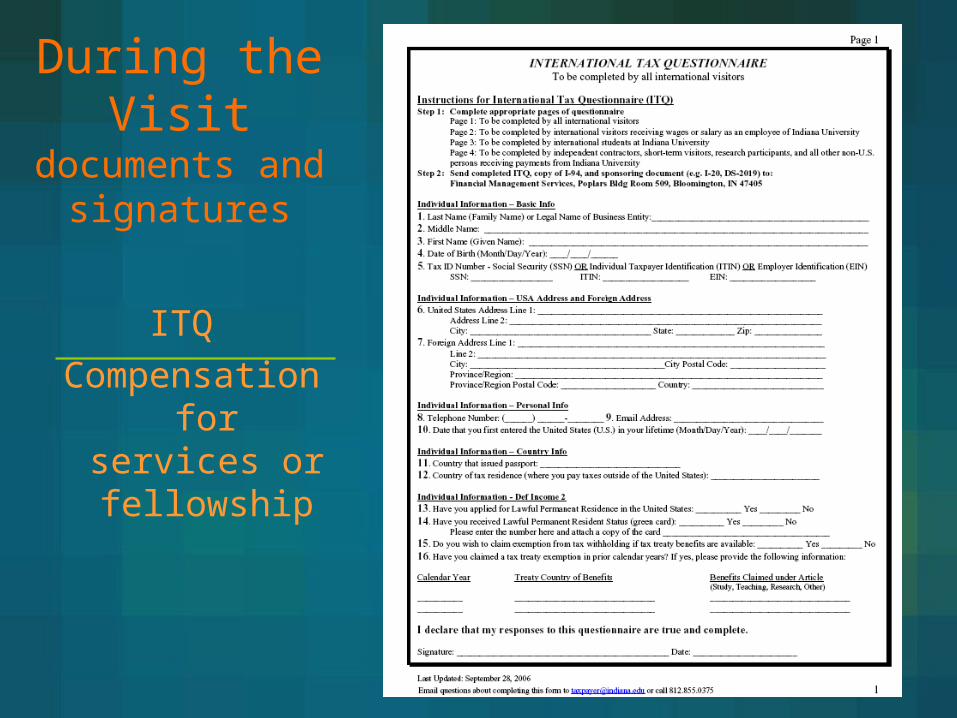

ITQ Compensatio

n for services or fellowship

During the Visit

documents and signatures

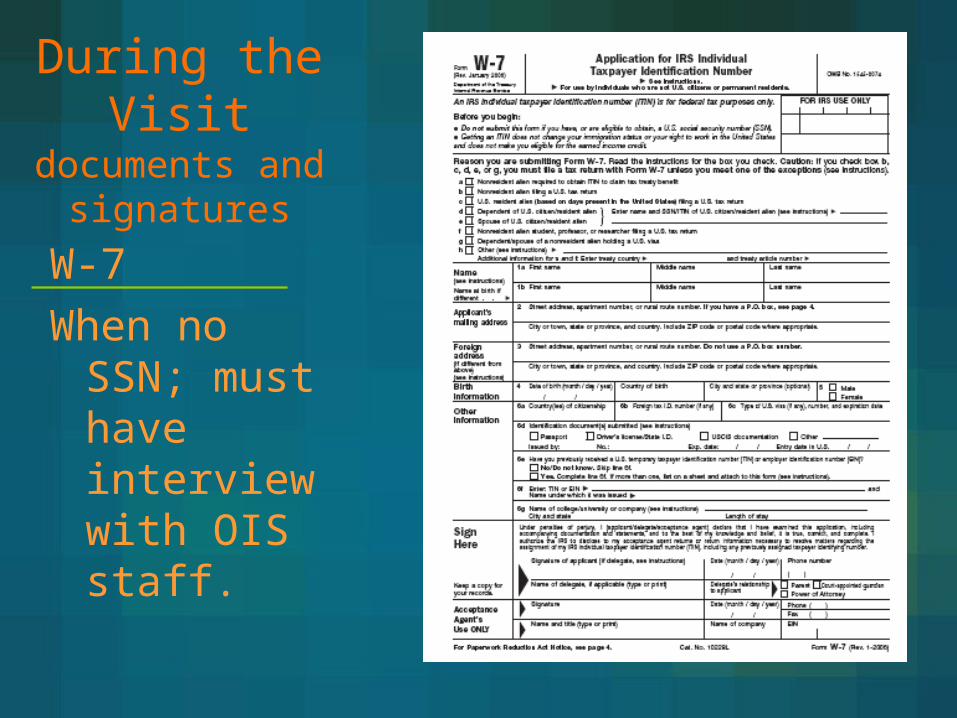

W-7When no

SSN; must have interview with OIS staff.

During the Visit

documents and signatures

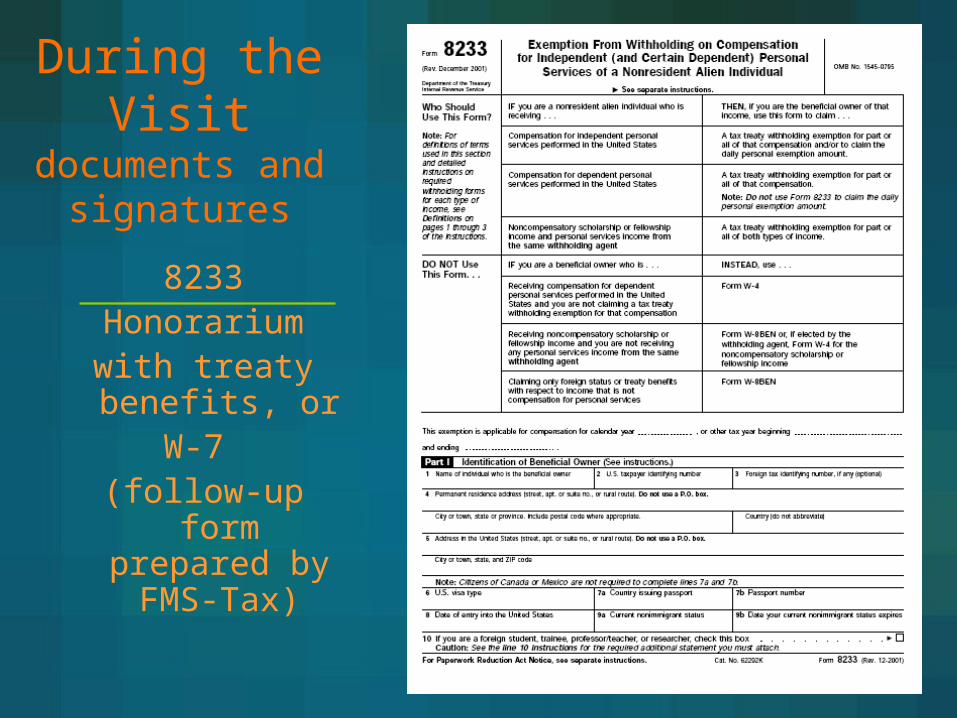

8233Honorariumwith treaty benefits, or

W-7 (follow-up

form prepared by

FMS-Tax)

After the Visit

Protect the Institution – Payment and Tax Issues

Do we have what we need to make a payment?

How much has to be withheld?

After the Visit

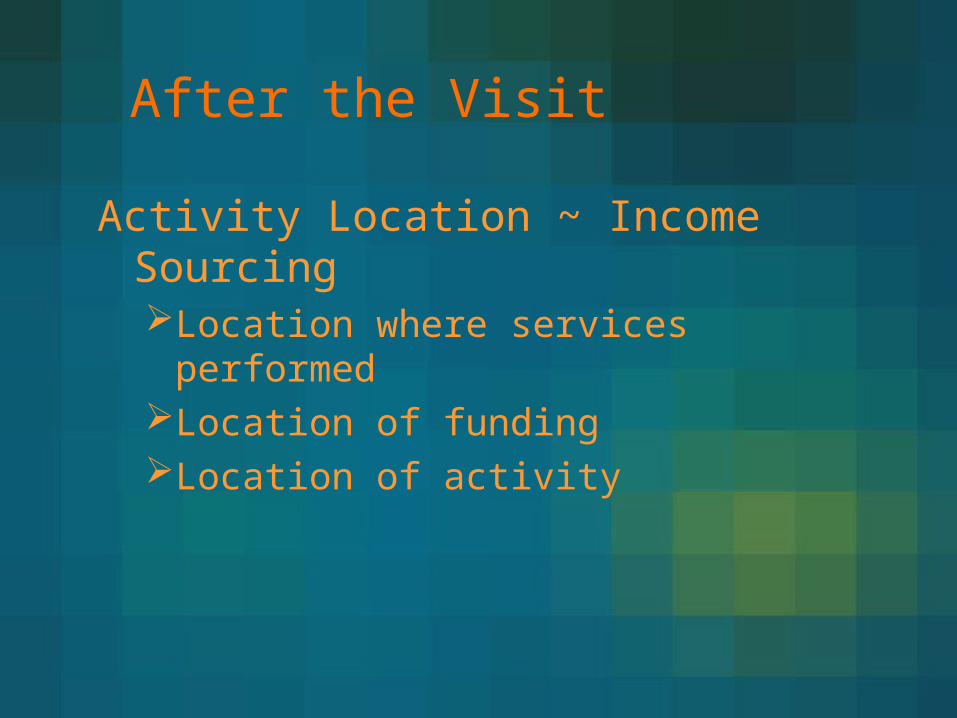

Do we have what we need to make a payment?

Documentation ~ Tax status Purpose ~ Classification of incomeActivity location ~ Income sourcing

After the Visit

Documentation ~ Tax statusEstablish tax status in U.S.Determine eligibility for tax

treaty benefitsNotify visitor of limitations

After the Visit

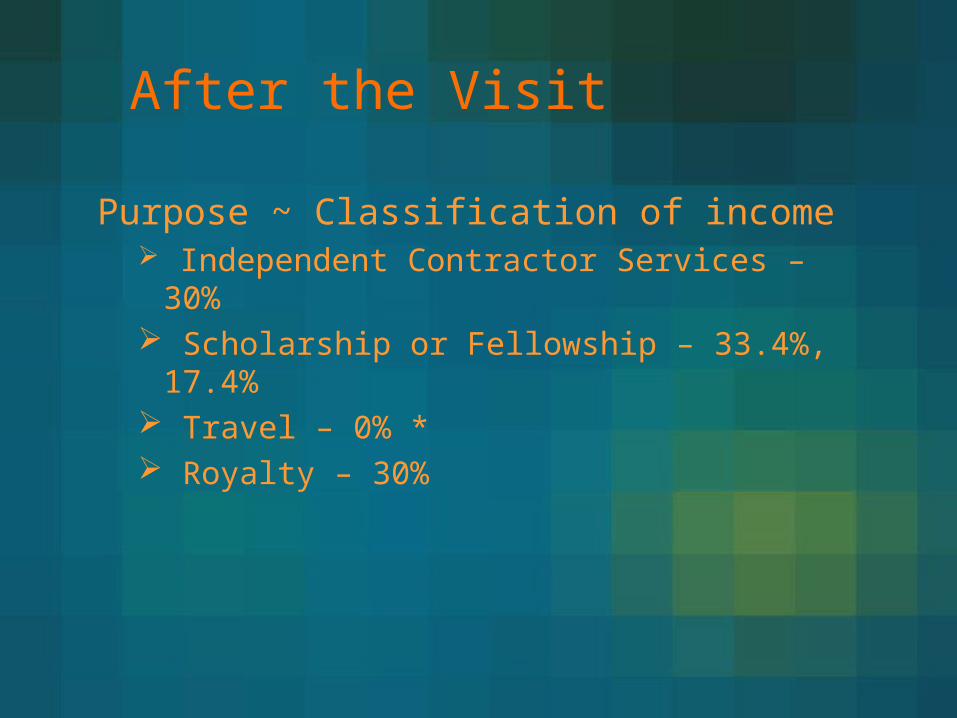

Purpose ~ Classification of incomeIndependent Contractor ServicesScholarship or FellowshipTravelRoyalty

Activity Location ~ Income SourcingLocation where services

performedLocation of fundingLocation of activity

After the Visit

After the Visit

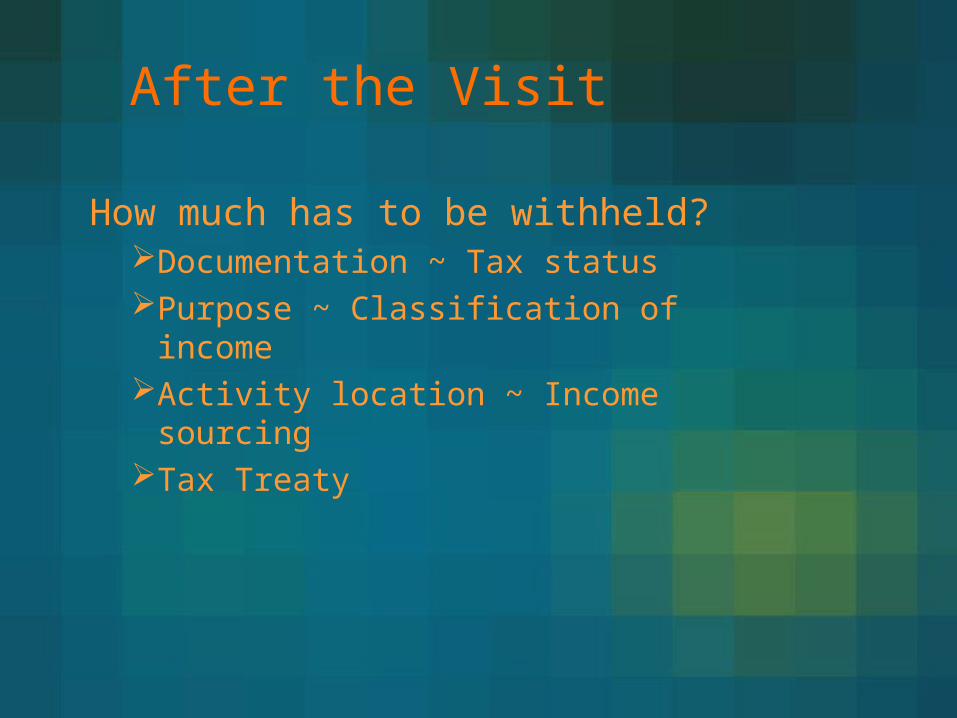

How much has to be withheld?Documentation ~ Tax status Purpose ~ Classification of incomeActivity location ~ Income sourcingTax Treaty

After the Visit

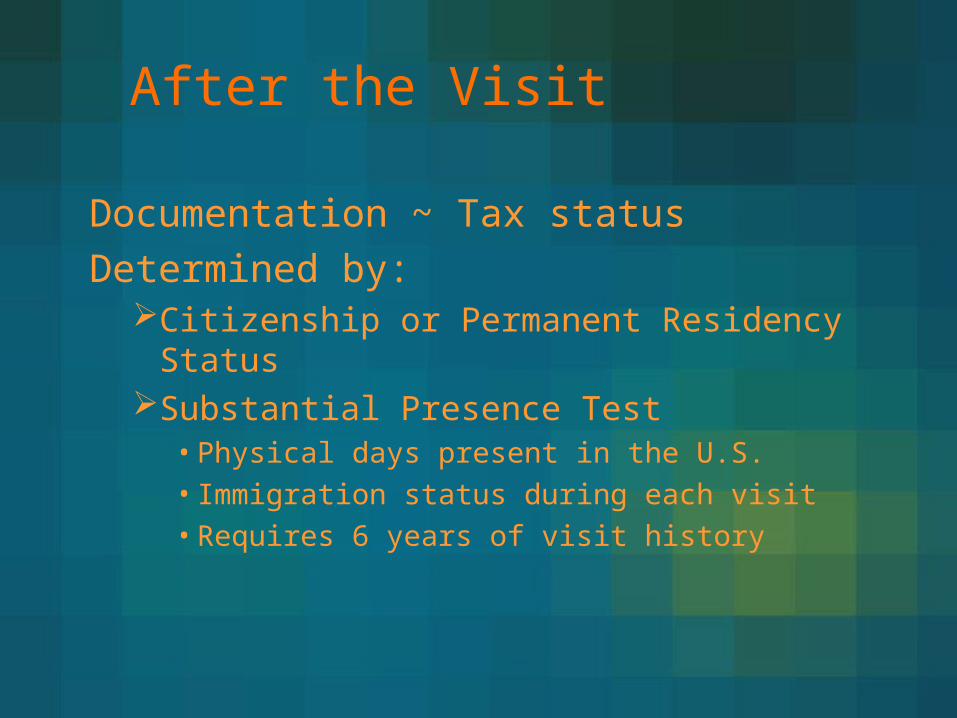

Documentation ~ Tax statusDetermined by:

Citizenship or Permanent Residency Status

Substantial Presence Test• Physical days present in the U.S.• Immigration status during each visit• Requires 6 years of visit history

After the Visit

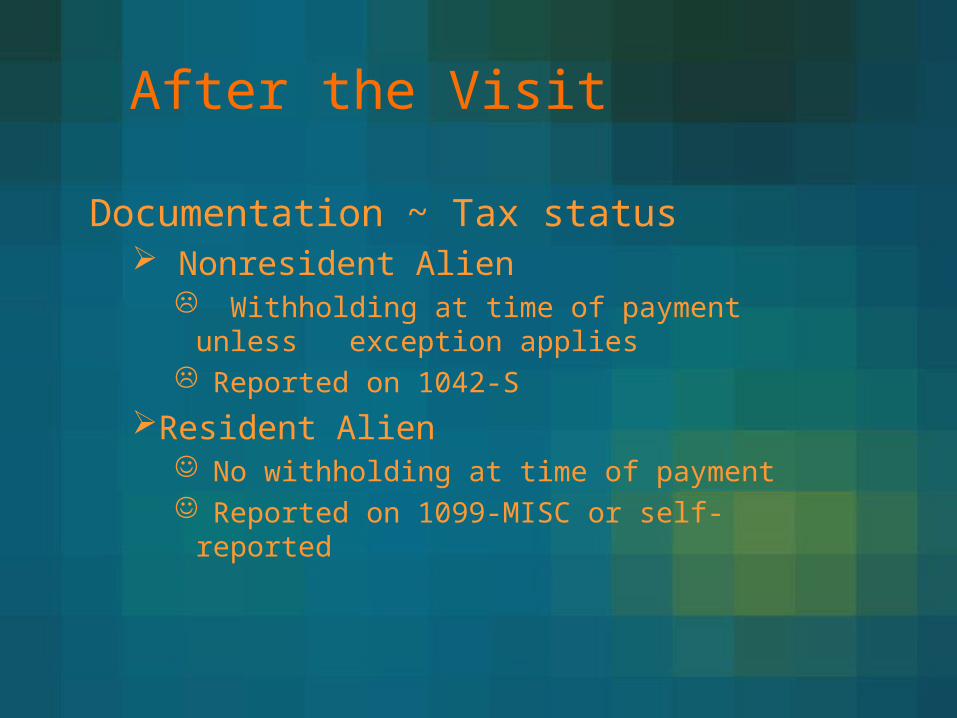

Documentation ~ Tax status Nonresident Alien

Withholding at time of payment unless exception applies

Reported on 1042-S

Resident Alien No withholding at time of payment Reported on 1099-MISC or self-

reported

After the Visit

Purpose ~ Classification of income Independent Contractor Services –

30% Scholarship or Fellowship – 33.4%,

17.4% Travel – 0% * Royalty – 30%

After the Visit

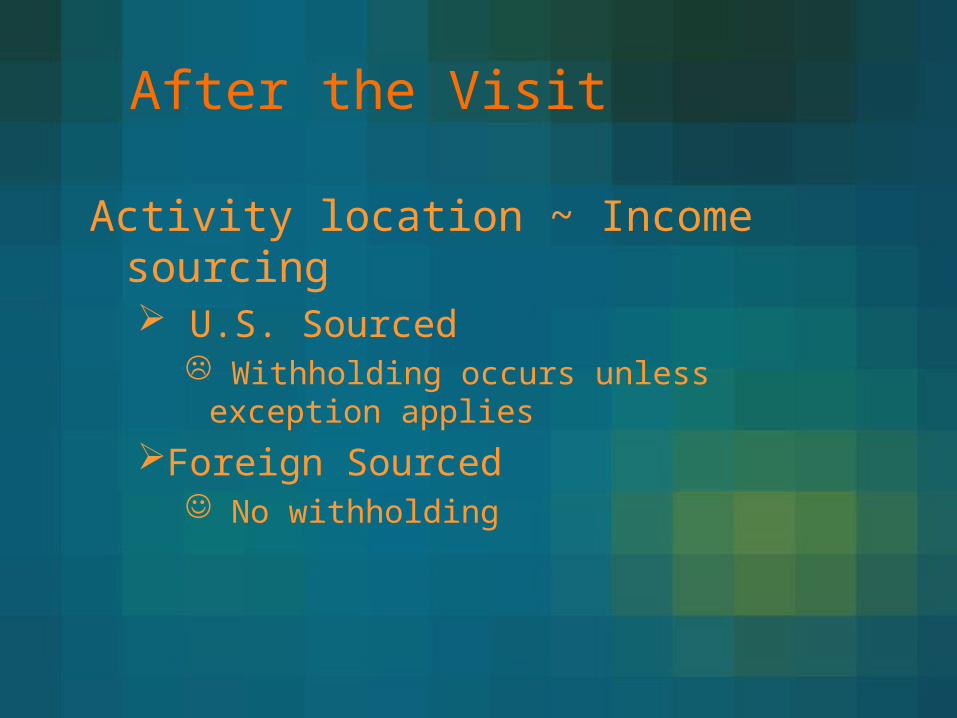

Activity location ~ Income sourcing U.S. Sourced

Withholding occurs unless exception applies

Foreign Sourced No withholding

After the Visit

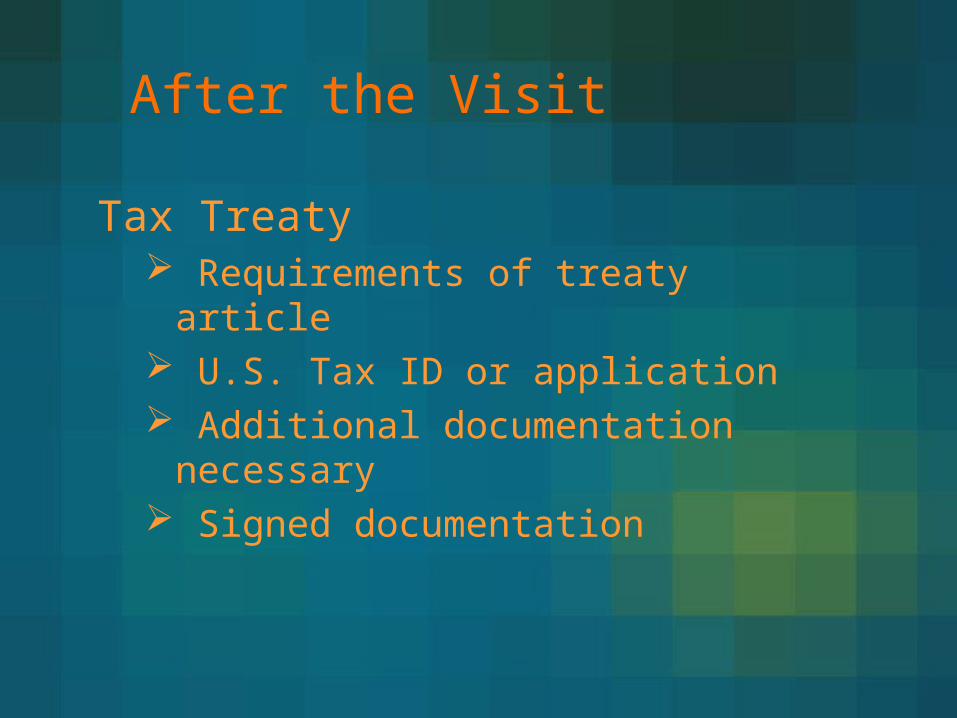

Tax Treaty Requirements of treaty article U.S. Tax ID or application Additional documentation

necessary Signed documentation

After the Visit

Payment ProcessCreate foreign vendor

• W-8BEN• Foreign Individual/Entity Certification

Create Payment Request• Forward documentation• FMS-Tax will notify you with any

additional documentation requirements.

After the Visit

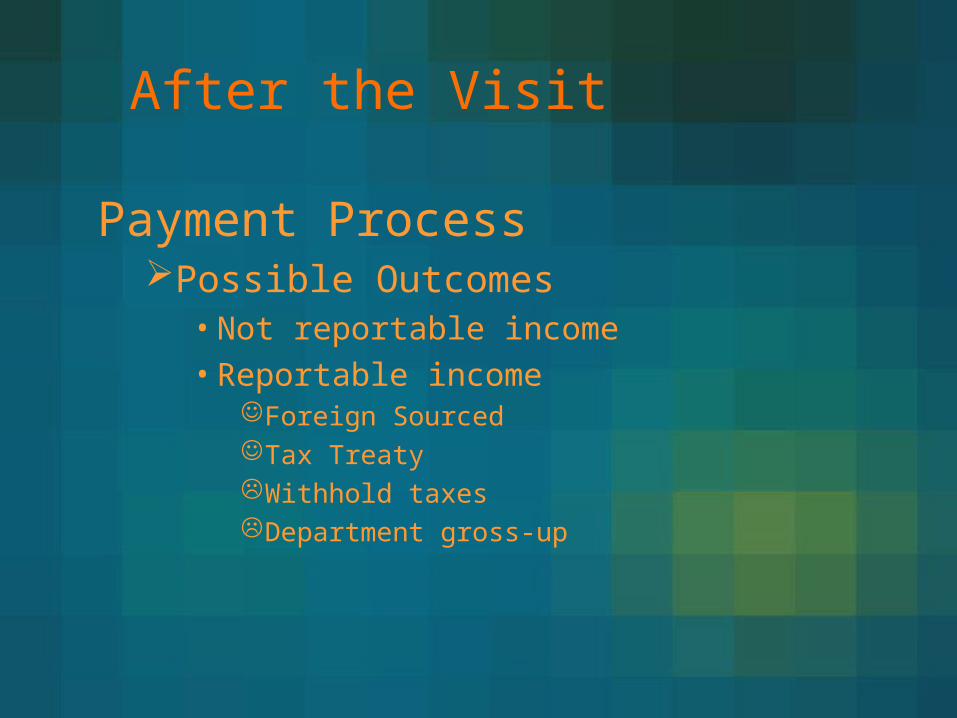

Payment ProcessPossible Outcomes

• Not reportable income• Reportable income

Foreign SourcedTax TreatyWithhold taxesDepartment gross-up

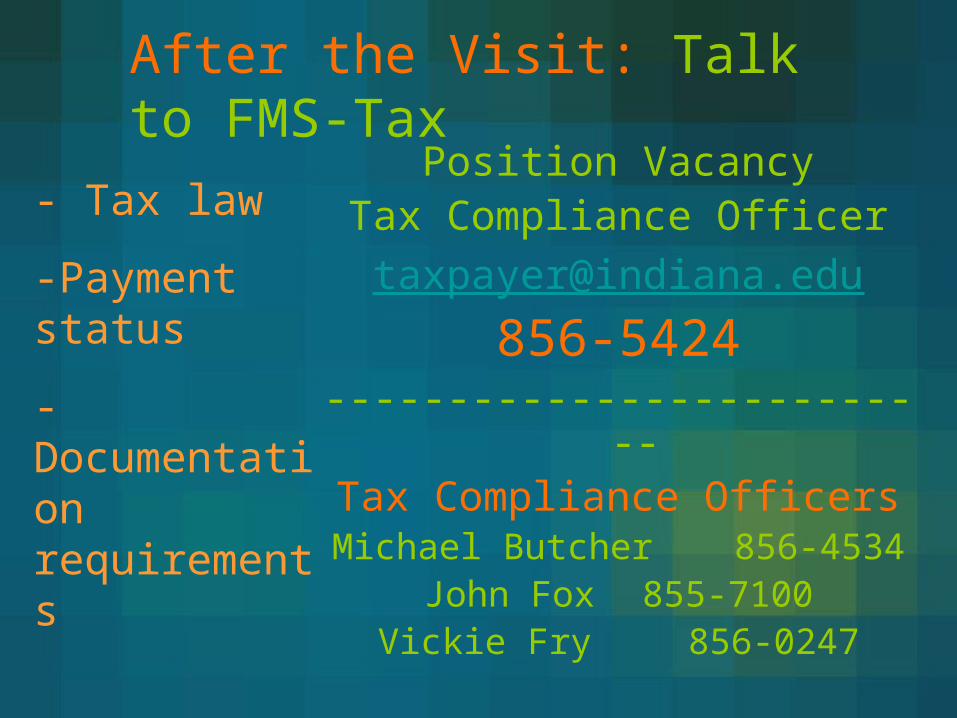

After the Visit: Talk to FMS-Tax

Position VacancyTax Compliance [email protected]

856-5424--------------------------

Tax Compliance OfficersMichael Butcher 856-4534John Fox 855-7100Vickie Fry 856-0247

- Tax law

-Payment status

-Documentation requirements

Paying Short-Term Visitors:A work in progress• Liability of payee• Liability of payor• Systemic abuse

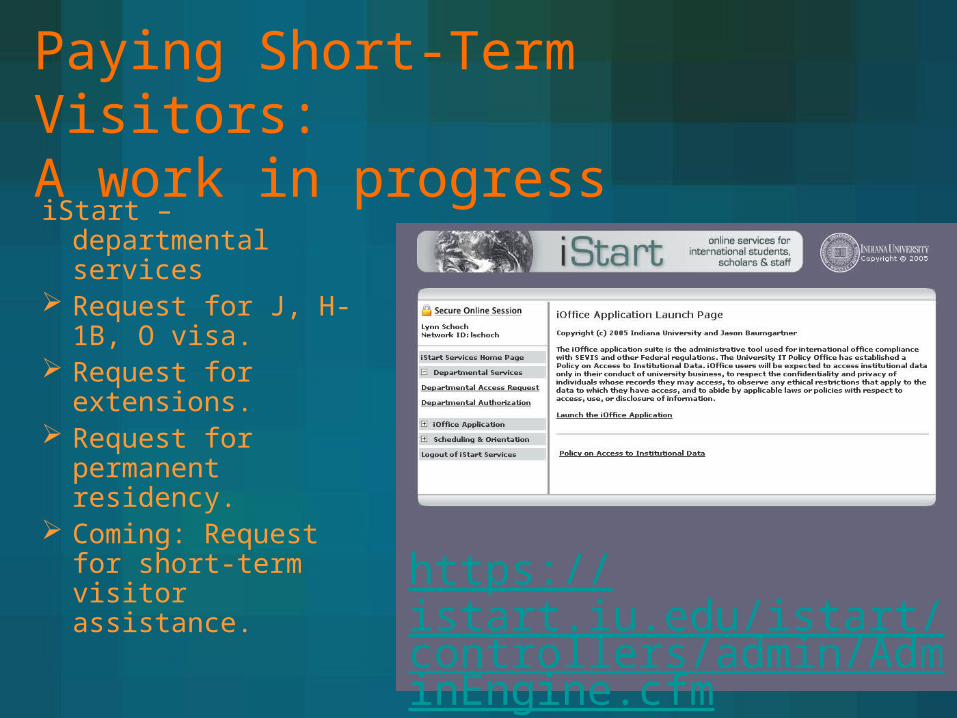

Paying Short-Term Visitors:A work in progressiStart – departmental

services Request for J, H-

1B, O visa. Request for

extensions. Request for

permanent residency.

Coming: Request for short-term visitor assistance.

https://istart.iu.edu/istart/controllers/admin/AdminEngine.cfm