Payday Lending and Bank Overdrafts Dean Karlan (Yale University) and Jonathan Zinman (Dartmouth...

22

1 Payday Lending and Bank Overdrafts Dean Karlan (Yale University) and Jonathan Zinman (Dartmouth College)

-

date post

22-Dec-2015 -

Category

Documents

-

view

217 -

download

1

Transcript of Payday Lending and Bank Overdrafts Dean Karlan (Yale University) and Jonathan Zinman (Dartmouth...

1

Payday Lending and Bank Overdrafts

Dean Karlan (Yale University) and Jonathan Zinman (Dartmouth College)

2

Why Consider Payday Loans and Bank Overdrafts Together?

Product similarities:• Key sources of short-term, small dollar liquidity for

(vulnerable) households• Very expensive in annualized terms

– Interest rate in triple digits• Not necessarily expensive in dollar terms

– Typical total outlays: $15-$45 per loan• Some evidence that consumers don’t use these products

wisely, and that lenders exploit this

There is significant interest in regulating/restricting both markets

3

Why Consider Payday Loans andBank Overdrafts Together?

• Overdrafts: laissez faire → decision architecture

– Proposed Fed rules would begin changing “decision architecture” to “nudge” consumers toward better decisions

• Payday loans: wrecking ball– “Protect” consumers by shutting

down market– But behavioral economics can

work here too– If anything product structure

more amenable to nudge approach than overdrafts

Differences in federal policy approach instructive:

4

Payday Loans:Market Background

• Short-term, expensive credit– “$15 per $100” for 2 week loan » 390% APR

• Common– More payday loan outlets than McDonalds + Starbucks

combined– 5-10% of U.S. households use annually– Higher prevalence in key segments (military, working poor)

5

Payday Loans:Policy Background

• About a dozen states effectively outlaw, with licensing and/or pricing restrictions

• 36% federal ceiling on loans to military personnel effective October 2007– President Obama wants to extend this to everyone

• Congress considering 4 bills in current session that could effectively shut down market

?

6

Payday Loans:Pressing Policy Questions

• How would shutdown affect consumers?– We don’t know: evidence is mixed– Some studies: expensive short-term credit finances productive

“investments” (in job retention, health, consumption smoothing)– Other studies: expensive credit exacerbates financial distress

Given this uncertainty, why shut off a key source of liquidity when we’re pouring $trillions to get/keep credit flowing?

7

Regulating Payday Loans:A Behavioral Approach

• Mothball the wrecking ball• Improve architecture to help consumers make

better decisions– To design effective policy it helps to think a bit

more deeply about what we’re trying to fix….

8

Regulating Payday Loans: Behavioral Diagnostics

• Exactly how are consumers going awry?• How and why might consumers do themselves harm

when handling expensive short-term credit?– Note: focus is not on mistakes per se

• underborrowing rarely a concern; overborrowing is– So what cognitive biases might lead consumers to “get in

over their heads”

9

Behavioral Diagnostics and Treatments

• Cognitive bias and problem #1: consumers are impulsive and lack self-control.

• Solutions to improve decisions– Delay: build it into the borrowing process– Commitment: help consumers formulate and stick

to a sensible plan, in their less-impulsive moments

10

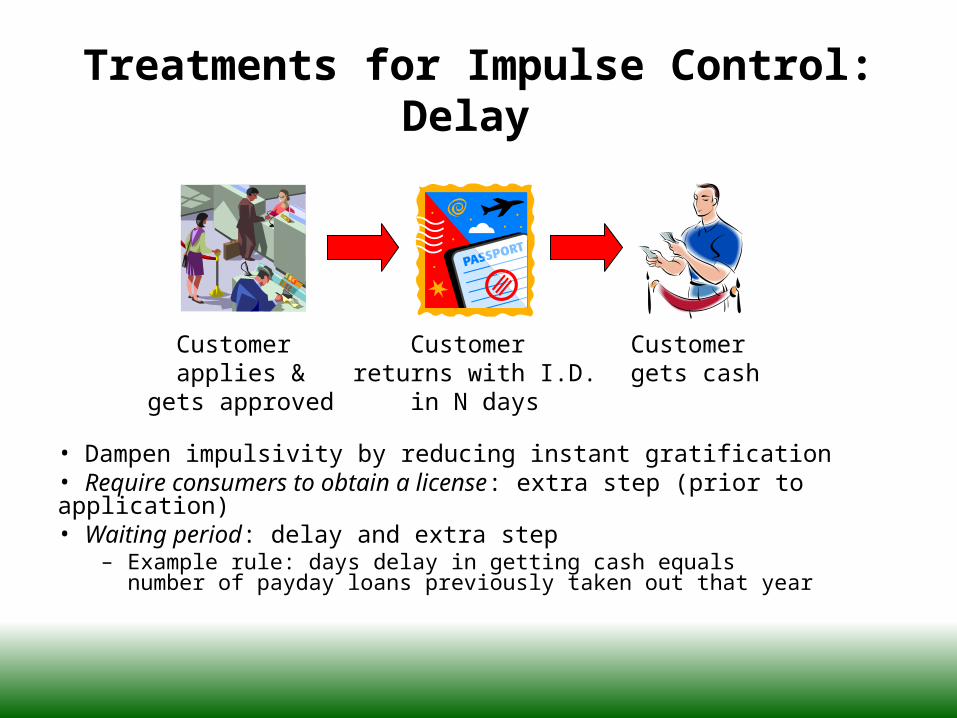

Treatments for Impulse Control:Delay

Customer applies &

gets approved

Customer returns with I.D.

in N days

Customer gets cash

• Dampen impulsivity by reducing instant gratification• Require consumers to obtain a license: extra step (prior to application)• Waiting period: delay and extra step

– Example rule: days delay in getting cash equals number of payday loans previously taken out that year

11

Treatments for Impulse Control:Self-Regulation

Allow consumers to sign contract(s) that voluntarily restrict their own borrowing

12

Behavioral Diagnosticsand Treatments

• Cognitive bias and problem #2: consumers do not anticipate the doo doo they’re getting into– Debt appears deceptively cheap: underestimate costs– Future appears overly bright: overestimate prospects

• Solutions to improve decisions at point-of-borrowing:– Bundle loan products with financial counseling– Change disclosures to better highlight true costs, realistic prospects

13

Treatments for Poorly Informed Consumers: Financial Advice

• Make completion of financial counseling a precondition for (repeat) borrowing– Medicine, not education: advise people, and help

them come up with a healthy plan– Would need to subsidize advice

• Nonprofits & trade associations key players here

14

Treatments for Poorly Informed Consumers: New Disclosures

• Highlight true costs of borrowing in terms that consumers can actually understand– Expected total dollar cost

• Over multiple loans, compounded

Customer borrows $300 at $15 per $100 for 2 weeks

Customer rolls loan over

twice

Customer pays $156 in total interest

15

Treatments for Poorly Informed Consumers: New Disclosures

• Show typical borrowing experiences (reality check for the overly optimistic)

• “Borrowers like you typically take N loans, pay $X in interest, and default Y% of the time”

16

Bank Overdrafts: Supply-Side Background

• Big source of revenue for banks– 74% of explicit revenue on deposit accounts– 6% of net operating income

• Current regulation: malevolent neglect– Inadequate disclosures

• Elephant in room: (already struggling) banks making unsustainable profits off poor consumer decisions?...

17

Bank Overdrafts: Consumer-Side Background

• Preliminary evidence says “yes”, banks profiting off consumer inattention– Consumers could avoid nearly all overdrafts with simple

changes in behavior• Big cost for many consumers• Can be even pricier than payday loans

– Median fee in $20-$30 range, regardless of size of the loan (i.e., of the amount of overdraft)

18

Bank Overdrafts:Regulatory Environment

• Problem: upfront disclosure lacking• Solution: mandate upfront disclosure

– A la Federal Reserve Board proposed rule!• Model disclosure presentation is quite dry though

• Simple product so disclosure should be effective– But for how long?– Upfront disclosure probably insufficient given nature of the product

• Probably also need….

19

Bank Overdrafts:Regulatory Environment

• Problem: no disclosure at point-of-overdraft• Unlike a payday loan, customer may not even know

they’re entering into a separate, borrowing transaction!

“Warning: if you complete this transaction you will overdraft by __$ and incur an NSF fee of $35”

20

Bank Overdrafts:Regulatory Environment

• Problem: most programs opt consumers in• Solution: change default to opt-out, require

“active decision” by consumer to opt-in

Federal Reserve Board proposed rule would make this change!

21

Treatments Beyond thePoint-of-Borrowing

• Many households need to reduce debt before they start saving– I.e., their highest investment return comes from paying

down expensive debt• So offer new products and programs for debt

reduction: “Borrow Less Tomorrow”– Automatic payroll withdrawals– Other SMaRT-like features

22

Summary of Behavioral Approach to Regulating Payday Loans and Bank Overdrafts

• Decision architecture, not wrecking ball• Tools

– Delay (waiting periods and consumer licensing)– Self-regulation (commitment contracts)– Financial advice– New disclosures (true costs, typical experiences)– New products (“Borrow Less Tomorrow”)