Paul Gross

14

HISummitPAPER220713.docx 1 Health Group Strategies Pty. Limited (INC. IN NSW) ABN: 16 003 974 507 AND INSTITUTE OF HEALTH ECONOMICS AND TECHNOLOGY ASSESSMENT LE GRAND BOIS, ST CHRISTOPHE EN BRIONNAIS, SAONE ET LOIRE, 71800 FRANCE PO BOX 4232 BALGOWLAH HEIGHTS NSW 2093 AUSTRALIA PHONE 61 2 9953 7003 FAX 61 2 9953 7006 Email: [email protected] Version: 22 July 2013 Long-term and short-term priorities for health and related social care in the first term of the next government: whither private health insurance? BY Paul F. Gross PhD Director, Health Group Strategies Pty Ltd (Australia and Greater China) Director, Institute of Health Economics and Technology Assessment, Australia and Greater China Parts of this paper were delivered at the Health Insurance Summit in Sydney on 22 July 2013.

-

date post

21-Oct-2014 -

Category

Health & Medicine

-

view

486 -

download

4

description

Transcript of Paul Gross

HISummitPAPER220713.docx 1

Health Group Strategies Pty. Limited (INC. IN NSW) ABN: 16 003 974 507

AND

INSTITUTE OF HEALTH ECONOMICS AND TECHNOLOGY ASSESSMENT

LE GRAND BOIS, ST CHRISTOPHE EN BRIONNAIS, SAONE ET LOIRE, 71800 FRANCE

PO BOX 4232 BALGOWLAH HEIGHTS NSW 2093 AUSTRALIA PHONE 61 2 9953 7003 FAX 61 2 9953 7006 Email: [email protected]

Version: 22 July 2013

Long-term and short-term priorities for health and related social care in the first term of the next government: whither private health

insurance?

BY

Paul F. Gross PhD

Director, Health Group Strategies Pty Ltd (Australia and Greater China) Director, Institute of Health Economics and Technology Assessment,

Australia and Greater China

Parts of this paper were delivered at the Health Insurance Summit in Sydney on 22 July 2013.

HISummitPAPER220713.docx 2

1. SOME DISCONNECTIONS BETWEEN HEALTHCARE AND SOCIAL CARE NEED POLITICAL LEADERSHIP

The current boundaries that demarcate the financing of health care, long-term care in

retirement and retirement living are unsustainable. Those barriers should be broken

down in the first term of a new government.

First, the warnings of the Henry report (totally ignored by the last two governments

and opposition) should have driven Australian politicians to think about why we

cannot afford to maintain these boundaries.

Second, the GFC signalled to all nations that we cannot afford to satisfy demand in

health and social care using dollars from Medicare, PHI and superannuation. Instead,

Australia spent like a drunken sailor, fiddled with health reform, did nothing about

aged care but then launched a new National Disability Insurance Scheme that has

many overlaps with medical services and aged care.

As a result, with a new government imminent, we now have the worst of all worlds:

• no sustainable policies for health care reform;

• overdue budget outlays on mental health and disability but minimal attention to

either the workforce gaps or the care coordination needed to spend the new

money wisely;

• a health care system under no pressure to provide safer or more efficient care;

• a social service system and a disability services sector totally unconnected

budget-wise or service-wise from the health care system; and

• too many politicians still pushing populist carts that ignore urgent reforms that can

create more accessible and affordable health and social services in the future.

HISummitPAPER220713.docx 3

Four other factors, both facilitated by the current pattern of government subsidy and

private payment, have been looming for years as policymakers took their hands off

the tiller.

• Medical technology has improved in each decade – and its average cost is rising

with each decade. Health insurance, via Medicare or PHI, is a major driver of the

supply of, and consumer demand for, medical technology. In a world where

subsidised social insurance (Medicare) and private health insurance cushion the

financial blow to consumers and encourages the supply side (doctors) to do all

that is possible, we are now seeing a belated recognition by governments (not

Australia, sadly) that this splurge on every technology does not guarantee value

for money purchasing.

• The MBS, private health insurers and other big payers of health care (such as

DVA and Workers Compensation schemes) reimburse the providers of care via a

fee-for-service (mainly doctors), a casemix payment (hospitals) and very rarely a

bundled payment for a defined claim of patient. That payment flows to the

provider regardless of the quality of the care provided – and in all nations of which

I have experience, the total payment for botched or unsafe care is higher than the

total payment for care that is of high quality. In 2013, the providers of medical and

hospital still have no incentive to be transparent about which episodes of care

regularly cause patient harm and/or higher costs to all payers. By any standard,

this is inconspicuous waste. Payment reforms worldwide – but not in Australia

where 10% of overnight stays indicate the presence of adverse events to patients.

– are attempting to reduce that waste by changing the incentives for quality care.1

• There are no incentives in the current payment system for innovations that might

change the dominant and most costly site of care, viz., the acute hospital bed. An

under-funded aged care system, threatened by the paucity of existing aged care

subsidies, has no hesitation in sending nursing home patients, mostly old, to

1 In Australia, some academics are arguing that pay-for-performance in unproven until they are given tax-payer subsidised grants to demonstrate what other nations have long known: incentives do work. 2 The Australian Medical Association is not the only medical union labeling the patient-doctor relationship as

HISummitPAPER220713.docx 4

respite care in an acute hospital, or to an emergency ward of a hospital, or to a

hospital that will be the last provider of care before the patient dies.

• Social care linked to medical care is almost invisible in Australia. In other nations,

this linkage is being strengthened (the UK health and social care legislation is an

example, albeit beset by GFC-induced budget cuts)) because the linkage has

been shown to accord with patient preferences, allow more appropriate care of

the aged and chronically ill, and allow households to make collective decisions on

the choice of care, and create competition in the market for innovations in care.

2. THE CURRENT PAYMENT CURRENCIES FOR DOCTORS AND HOSPITALS ARE OUTDATED, IMPEDE INTEGRATED CARE, INCREASE OUT-OF-POCKET COSTS, AND WEAKEN THE VALUE OF PHI

Health insurance via general tax revenue, a Medicare levy or a private health

insurance premium (and subsidised by the PHI rebate) currently exists alongside the

growing share of health expenditures funded by out-of-pocket payments by

consumers.

Often forgotten is the fact that it is the household that pays for care by all four routes.

The current mix of funding is incoherent if rising copayments are impeding access to

needed care, particularly when this rising share leaves patients vulnerable to the

charging whims of individual doctors and decisions by the federal government that

limit the rate of increases of subsidies for medical care via the Medicare Benefits

Scheme (MBS).

HISummitPAPER220713.docx 5

We now have the ludicrous situation where the formerly simple and “sacred”2

contract between the doctor and the patient is complicated by the actions of five

decision-makers:

• a government decision to hold MBS fees at levels that do not recognise the rising

costs incurred by doctors in their practices;

• a decision by the Australian Medical Association to set a higher range of fees that

doctors can charge (often 50% higher than the MBS fee);

• the decision by the Howard government, sustained by two Labor governments, to

create a new subsidy that allows patients to claim tax benefits after the Safety Net

thresholds for doctor charges and PBS outlays have been passed in any year,

thereby inspiring some medical specialists to generate more services knowing the

patient will not be paying after the threshold is exceeded in any year;

• a subsequent decision by the doctor to charge higher fees than the AMA

recommended fee and, in some cases depending on the market strength of the

individual specialist and how the Safety Net affects them, a very much higher

charge;

• decisions by health insurers on their rebates for specialist care in private

hospitals,3 with funds offering their members predictable out-of-pocket outlays

when the specialist agrees to charge PHI members “no extras”; and

• at the end of this daisy-chain of decisions, a decision by the patient to meet all or

any uninsured out-of-pocket payments, or to not seek a doctor's office-based

service, or to not attend a dental service, or to not fill a script written by any

doctor.

2 The Australian Medical Association is not the only medical union labeling the patient-doctor relationship as sacrosanct, or warning the population that any interference by governments of health insurers in fee determination is equivalent to US “managed care”. 3 The private insurer is required to pay the 25% gap between the fee and the 75% of that fee set in health insurance legislation as the insurer's responsibility for privately insured hospital payments.

HISummitPAPER220713.docx 6

The Australian healthcare system is now vulnerable to organisation mayhem and an

unwillingness to accept that the private health system is enlarging because the public

sees a public health system weakened by political bunfights.

For as long we leave COAG and its seven advisory bodies in charge of public

hospital reform, and while we avoid restructuring of private health insurance,

• there will be no innovation outside the hospital walls;

• rising out-of-pocket costs will continue to weaken the value of health insurance

and patients will defer care and not take essential medicines;

• nearly 12% of older Australians are estimated to spend over 10% of their

income on health costs and 5% (250,000) are estimated to spend over 20%,

seriously reducing their disposable income in retirement; and

• with no innovation, higher costs, and reduced access to essential care, future

household wealth and national productivity will decline.

The last health reform commission laboured long but its 123 recommendations were

a compromise, the absence of expertise in budget financing meant that its estimates

of costs were at best aspirational, it provided no incentives for a rapid transition to

higher quality and safer care, and it barely recognised the co-existence of a growing

private sector.

Starting in September 2013, the next government must focus on fiscally responsible

priorities, and 123 recommendations are 120 too many.

The three critical recommendations relate to the fed-state divide in health and social

care, the transparency of health system performance, and the gaps in current health

insurance that require cooperative de-regulation.

I have two modest suggestions for the next government.

ACTION 1: Think about whether it is time to seek a mandate to re-organise, by 2017, all health and social care payment currencies and assess the potential impact of pooled federal funding to the states

HISummitPAPER220713.docx 7

Budget pressures in the health and education portfolios, when we add unfunded

commitments to a national disability insurance scheme and the Gonski reforms,

mean that we cannot continue to promise universal benefits to everyone.

A corollary follows: if we cannot afford to fund every political promise, we need to cut

the obvious waste of two levels of government now oversighting health and welfare,

reduce administrative costs, and ensure best use of the public and private health and

educational systems.

We need to return some control of the health care system to consumers – and that

means jettisoning left-wing dogma that consumers cannot exert sufficient power to

change the dominance of doctors and hospitals. Contrary to the Abbott view while

Health Minister many moons ago, a targeted investment in specific types of

information systems can change the balance of power by rendering the health

system transparent. As noted in a recent US defence review by the Brookings

Institution, "speed and ubiquity of information creates pressures to act."4

The symmetry between the Health and Education policy arenas is now stark. We

have the spectre of three State governments, one arguing it already has the best

education funding policies that produce the best school results, delaying the Gonski

education reforms that require all States to come up to standards that are

measurable. The paltry logic: if you need $6 billion for the NDIS, cut it from the

Gonski funding.

In the health arena, the spectacle involves a similar façade. Here the States are

delaying reforms in hospital efficiency and patient safety by arguing that the feds

have stripped promised funding from them in mid-year. The states are demanding

the money originally promised – but they have done nothing to improve patient

access, patient safety or hospital quality.

In The Age on June 17 2013, the following indictment of hospital funding and quality

emerged:

4 Hamilton Project. "Real Specifics: 15 ways to reduce the federal budget. Part 1 budgeting for a modern military". Washington DC, Brookings Institution, 22 February 2013, 105 pages (at p 42 of transcript).

HISummitPAPER220713.docx 8

“Last week, Fairfax Media reported the Royal Children's Hospital was offering

patients access to a private room with more privacy and a lower risk of infection if

they used their private health insurance.”

I merely ask: Is the patient safety situation in a teaching hospital now so bad that we need to offer access to safe rooms? A health insurance executive might ask: Is this

the latest tool we have for marketing the value of PHI? Any politician looking back at

the last four years of talk might ask: did the COAG health reforms change anything in

state-run healthcare or criteria for public hospital admission and PHI payment?

The sad reality is that in health and education, the States are closer to the day-to-day

action of the schools and hospitals – and are in a better position that the feds to

apply tax dollars wisely and render hospitals safer. Under the COAG funding, they

still show no signs of so doing.

ACTION 2: Seek a mandate to render transparent with performance-based payment by 2016 the quality and safety of healthcare

At some point, we return to the real elephant in the room: the transparency of

measurement of the performance of public and private hospitals.

To date, this elephant has been put to pasture by health unions, Labor governments

and many clinicians. As in the schools, there is no appetite for transparency in a

funding system where one level of government allocates tax dollars and the other

spends the dollars in ways that defy transparent measurement.

In this conundrum, public schools and public hospitals are in the same under-funded

mess. No more money will be allocated until some improved outcomes of the funding

are visible to the feds.

The feds – with Abbott or anyone else as PM – have every right to demand

transparency in the quality of schools and hospitals – and we should not elect them

unless they are willing to man the spotlights.

HISummitPAPER220713.docx 9

3. THREE SHORT-TERM PRIORITIES FOR THE NEXT GOVERNMENT

These first two modest thoughts are a big stretch, so in the search for a relevant set

of short-term health reforms, my next three thoughts focus on the role of health

insurance in an ageing society that expects governments to provide all benefits with

no new taxes.

The next government should use its first term to

• define a vision for affordable care, creating an alternative to the Council on

Australian Governments to guide Australian priorities in healthcare funding

and reform,

• deregulate private health insurance, and push the insurance and financial

services industry towards new forms of insurance and savings that embed

incentives for appropriate use of health and social care.

ACTION 3: Give the nation a cooperative vision of affordable health and social care and a new national council to oversee reform across the health sector

With few new ideas coming from the health insurers or state governments, politicians

of all persuasions have been silent on the hard issues such as why we must

• cut back on overuse and other waste in the health system,

• harness the resources of the public and private systems,

• retain nurses and make better use of all health professionals,

• create more affordable health insurance covering all life stages, and

• help individuals and families to reduce risk factors that are driving 70% of the

health bill.

An incoming government should take no more than 12 months to

• assess specific proposals to make healthcare more affordable,

HISummitPAPER220713.docx 10

• identify the roles of governments, the private health sector and the voluntary

sector in the implementation of the proposals, and

• tell the public why patient-centred care will drive all future reforms, and why

little steps can bring about affordable care quicker than big-bang reforms.

Ignoring all exhortations for big-bang reform in its first term, the next government

should not (yet again) attempt restructuring of the roles of different levels of

government in healthcare.

An independent council should replace COAG and bring the public and private

sectors together. On the day the new Health Minister is appointed, the government

should announce an intent to replace COAG as the prime decision-maker by National

Health Priorities Council drawn from both levels of government, the private health

sector, the voluntary sector and patient support groups.

The new council should report to Parliament, as does the German equivalent that

has stood the test of time. Its reach across all parts of the health sector enables

messy reforms to be debated, honed and promulgated with at least a semblance of

cooperation between the lander (states) and the federal government.

ACTION 4. Deregulate health insurance in stages, starting with regulations whose benefits do not justify their hidden costs

Private health insurance is under threat because of costly and misplaced regulatory

zeal, its dependence on tax rebates, and the absence of incentives to insurers to

create less costly insurance or new types of insurance to cover rising copayments.

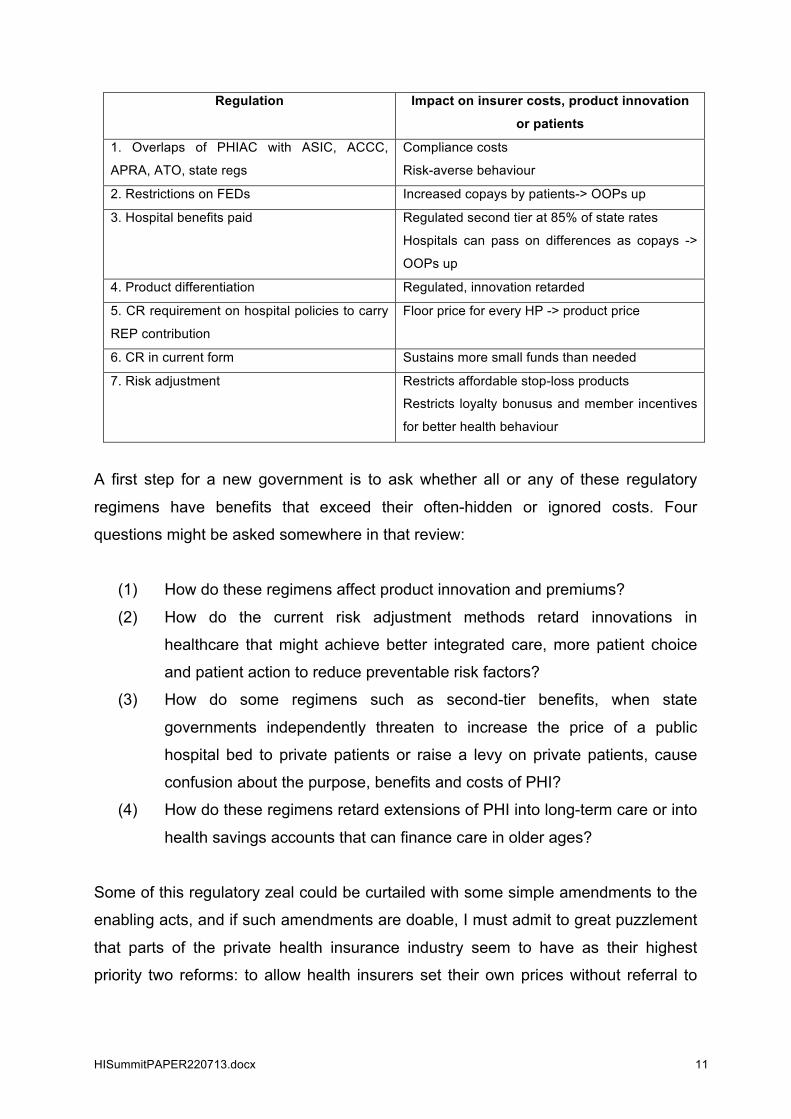

The regulatory armamentarium is illustrated, not exhausted, in the following table

whose acronyms and terminology should be familiar to this conference.

HISummitPAPER220713.docx 11

Regulation Impact on insurer costs, product innovation

or patients

1. Overlaps of PHIAC with ASIC, ACCC,

APRA, ATO, state regs

Compliance costs

Risk-averse behaviour

2. Restrictions on FEDs Increased copays by patients-> OOPs up

3. Hospital benefits paid Regulated second tier at 85% of state rates

Hospitals can pass on differences as copays ->

OOPs up

4. Product differentiation Regulated, innovation retarded

5. CR requirement on hospital policies to carry

REP contribution

Floor price for every HP -> product price

6. CR in current form Sustains more small funds than needed

7. Risk adjustment Restricts affordable stop-loss products

Restricts loyalty bonusus and member incentives

for better health behaviour

A first step for a new government is to ask whether all or any of these regulatory

regimens have benefits that exceed their often-hidden or ignored costs. Four

questions might be asked somewhere in that review:

(1) How do these regimens affect product innovation and premiums?

(2) How do the current risk adjustment methods retard innovations in

healthcare that might achieve better integrated care, more patient choice

and patient action to reduce preventable risk factors?

(3) How do some regimens such as second-tier benefits, when state

governments independently threaten to increase the price of a public

hospital bed to private patients or raise a levy on private patients, cause

confusion about the purpose, benefits and costs of PHI?

(4) How do these regimens retard extensions of PHI into long-term care or into

health savings accounts that can finance care in older ages?

Some of this regulatory zeal could be curtailed with some simple amendments to the

enabling acts, and if such amendments are doable, I must admit to great puzzlement

that parts of the private health insurance industry seem to have as their highest

priority two reforms: to allow health insurers set their own prices without referral to

HISummitPAPER220713.docx 12

the Health Minister or some umpire, or endorsement of a Medicare Select or a Dutch

health insurance model based on private health insurance competition.

In my view, the first argument is risible for a long as the prime task of the survival of

both PHI and the PHI rebate is to define a new role for PHI that makes care more

affordable and leads to better health outcomes.

The second argument is a political landmine. The cost of the Dutch health system

has doubled since 2000 as five health insurers controlled over 80% of the market,

hospitals ramped up the volume of hospital care under “free pricing”, and a rapid

surge in the cost of long-term care forced the government to think about moving

some of the insurer costs to local governments. The Dutch now spend over 13% of

GDP on health, and our 10% share would breech similar levels if we adopted the

current Dutch model.

There is also the small issue of the premiums charged in the Netherlands. My guess

is that insured Australians might ask why an community-rated, income-related

premium of 7% is something to be desired when they pay less than half that rate for

Medicare and PHI.

Because of other strengths (including its integration of care for certain chronic

conditions and its coverage of ‘exceptional expenses), we should be having an

informed debate about the Dutch model.

Burt we should also be assessing the new German models (given Germany’s

decisive action in January to provide subsidies for long-term care insurance or LTCI),

and Belgium’s risk-adjustment formula to encourage insurers not risk-select against

LTCI enrolees. Though I fully comprehend why insurers are not racing into LTCI

promulgation when the market demand is almost zilch and the pricing of future care

benefits almost impossible to predict, aged care funding without some form of tax-

incentivised insurance for care outside the institutional walls and self-care will be very

expensive.

HISummitPAPER220713.docx 13

ACTION 5: Provide the incentives for relevant health insurance and engender a new mentality of saving for healthcare in retirement

The debate about desirable changes in PHI ought to take place once we have had a

prior debate about broad principles that should underpin any health insurance reform:

• what outcomes are we seeking to achieve with any new approach,

• what options are feasible for achieving those goals,

• what ought to be covered,

• how shall it be paid for, tax-protected or tax incentivised

• how it fits with Medicare, disability insurance and aged care funding,

• what quality assurance methods should underpin payments to providers of

care,

• what existing subsidies should be modified,

• what safeguards are needed to ensure that it achieves its outcomes.

So here is my modest suggestion that is consistent with reforms that seek affordable

care and deregulated PHI. Assuming that the government wants to contain future

budget expenditures on the aged and chronically ill, by the end of the first week of

the new government the Productivity Commission should be given a mandate to

complete, within 12 months, a costed feasibility study of tax-subsidised health

savings accounts within private superannuation accounts, with those HSAs used to

pay for

• insurance against the risks of catastrophic costs in retirement, as in

Singapore, or

• supplementary insurance that triggers cash benefits once a doctor indicates

loss of independency as in Germany, or

• gap insurance that allows access to additional preference-sensitive benefits

above a basic level of benefits available to all citizens.

HISummitPAPER220713.docx 14

4. CONCLUSION

There is good reason to avoid big-bang healthcare reforms. The UK, US and

Australian reforms were all big-bang, all had some GFC-induced slow-downs and all

created new bureaucracies that were resented by clinicians and not fully applauded

by the citizenry. The private health sector was not visible in two of these

restructurings.

There are a swag of reasons to seek more affordable health and related social care

in bite-size chunks that engage all actors in reforms that are painful and difficult, such

as cutting adverse events, rather than the usual plea to wait for culture change in

hospitals or leave the problem for slow resolution by the ACSQHC.

The article in The Age on 17 June 2013, quoted above, tells us that we still have a

mess that has not been touched by the last health reform process.

The next reform process requires coalition-building and priorities, and a vision that

more of the same is a criminal waste of the nation’s resources and a threat to healthy

ageing.

My five modest suggestions are not intended to leave politicians tranquil about the

requirements of leadership, team-building and consensus-gathering across the

health and welfare sectors. I also have cautious hopes that leaders will emerge in the

PHI and related industries to inform the public that there are affordable alternatives.