Paul Bernd Spahn, Goethe-Universität Frankfurt/Main1 Money and Inflation.

31

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 1 Money and Inflation

-

Upload

raymond-tyler -

Category

Documents

-

view

225 -

download

0

Transcript of Paul Bernd Spahn, Goethe-Universität Frankfurt/Main1 Money and Inflation.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 1

Money and Inflation

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 2

Structure

1. Introduction

2. The Costs and the Origins of Inflation

3. The Phillips-Curve and its Implications

4. Indexation - An International Comparison

5. Conclusion

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 3

Introduction

• Inflation is a rise in the general price level and is

reported in rates of change. The inflation rate is

determined by finding the difference between

price levels for the current year and the previous

given year:

t = ( Pt - Pt-1 ) / Pt-1.

• If Y and V are constant, inflation can only arise

on the condition of

( Mt - Mt-1 ) / Mt-1 > 0.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 4

Introduction

“Inflation is always and everywhere

a monetary phenomenon”

Milton Friedman Born 1912, Nobel prize in 1976

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 5

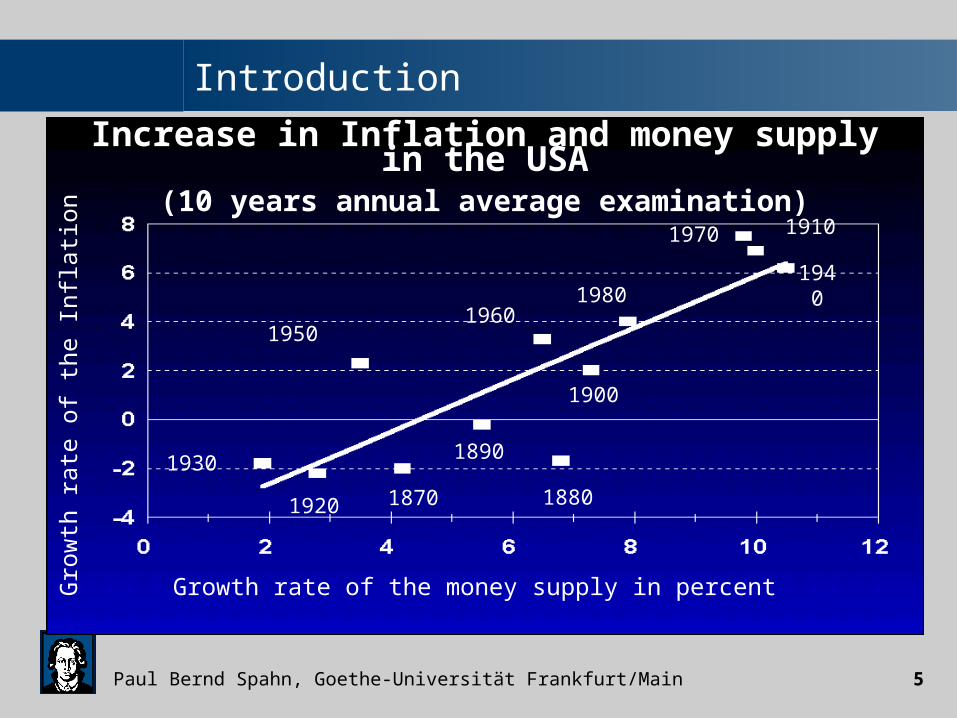

Introduction

Growth rate of the money supply in percent

Gro

wth

rate

of

the Inflati

on

1930

1920

1950

1870

1890

1880

1900

19601980

1940

1970 1910

Increase in Inflation and money supply in the USA(10 years annual average examination)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 6

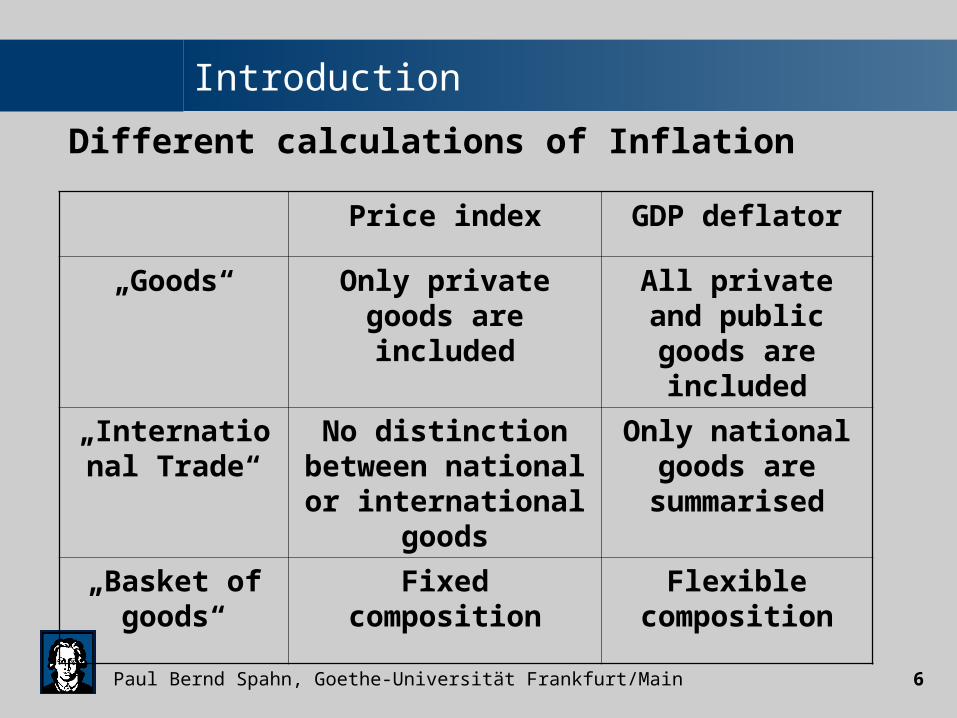

Introduction

Price index GDP deflator

„Goods“ Only private goods are included

All private and public goods are

included

„International Trade“

No distinction between national or international goods

Only national goods are

summarised

„Basket of goods“

Fixed composition Flexible composition

Different calculations of Inflation

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 7

The Costs and the Origins of Inflation

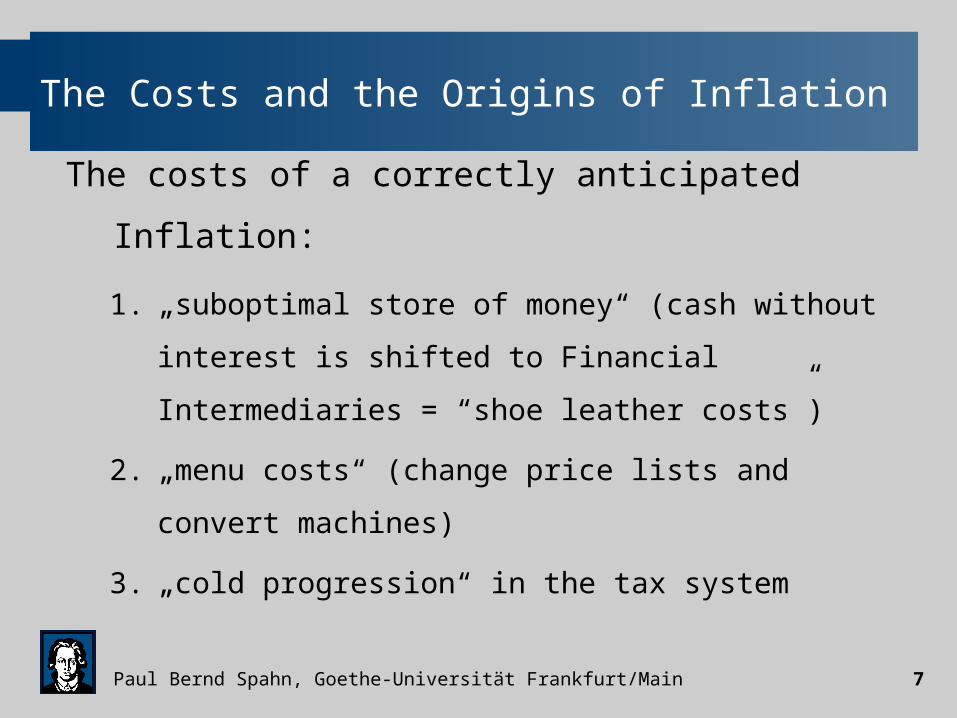

The costs of a correctly anticipated Inflation:

1. „suboptimal store of money“ (cash without interest

is shifted to Financial Intermediaries = “shoe

leather costs”)

2. „menu costs“ (change price lists and convert

machines)

3. „cold progression“ in the tax system

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 8

The Costs and the Origins of Inflation

The costs of an incorrectly anticipated Inflation:

1. profit income earners benefit more than wage

earners,

2. nominal income earners lose and

3. debtors benefit at the expense of creditors.

The results are high allocation costs and an arbitrary

distribution of income and wealth.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 9

The Costs and the Origins of Inflation

• Inflation could result from an activist economic

policy.

• There are two types of Inflation:

Supply induced Demand induced

Cost-push Inflation Demand-pull Inflation

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 10

Cost-push Inflation

Price level

Aggregate output

Inflation is dueto accommodating

fiscal policy

Yn

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 11

Demand-pull Inflation

Price level

Aggregate outputYtYn

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 12

Another Reason for Inflation:Government budget constraint

• To see how fiscal policy is related to monetary policy, we have to look at the government’s budget constraint.

• DEF = G - T = MB + B

• When the public’s bond holdings do not increase, a given deficit will have to be financed by monetizing public debt.

• Financing a persistent deficit by money creation will lead to sustained inflation.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 13

The Monetarist versus the Keynesian view

• The modern quantity theory of money (Milton Friedman) concludes that changes in aggregate spending are determined primarily by the money supply.

• Keynesian analysis indicates that high inflation cannot be driven by fiscal policy only.

• But both viewpoints tell us that high inflation can occur only with a high rate of money growth.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 14

The Phillips-Curve and its Implications

• Inflation () and unemployment (u) both have a relative negative impact on the economy as a whole.

• In 1958 A. W. H. Phillips discovered a relationship between unemployment and Inflation. Phillips´ research was focused on the economic statistics between 1861 and 1957. He looked at the rate of change in ages, and the level of unemployment.

• He found a stable, inverse relationship between these two variables.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 15

The Phillips-Curve and its Implications

The Phillips curve can be interpreted as a „trade-off“:

To get reduced unemployment, the economy must suffer from more Inflation, and to get reduced Inflation, the economy must suffer from more unemployment.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 16

The Phillips-Curve in the USA for 1950-1960

Unemployment Rate in %

Infl

ati

on

2 3 4 5 6 7

8

7

6

5

4

3

2

1

Source: Economic Report to the President, 1985

Phillips-Curve

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 17

The Phillips-Curve in Germany

Unemployment Rate in %

Phillips-Curve

from 1961 to 1996

Unemployment Rate in %

I

ncr

ease

in t

he

pri

ce in

dex

in %Phillips-Curve

from 1961 to 1973

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 18

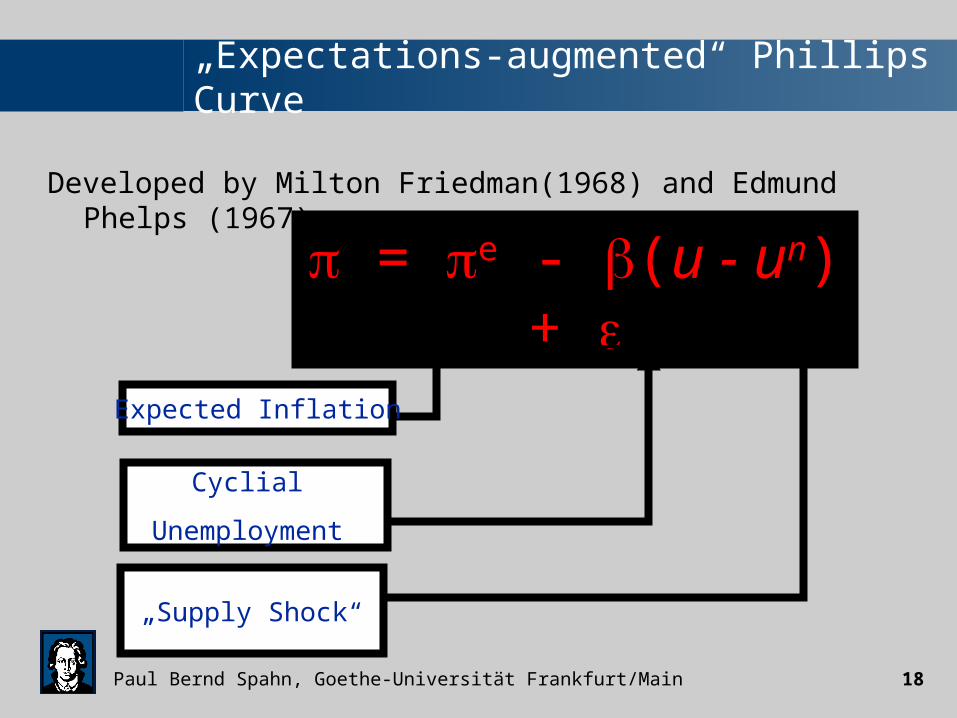

„Expectations-augmented“ Phillips Curve

Developed by Milton Friedman(1968) and Edmund Phelps (1967)

= e - (u - un) +

Expected Inflation

Cyclial

Unemployment

„Supply Shock“

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 19

„expectations-augmented“ Phillips Curve in the short and long run

• At a short notice Friedman and Phelps

“accepted” a trade-off between Unemployment

and Inflation.

• But in their view the Philips curve will be

generated in a vertical line in the long run.

– Demand management is useless and leads only to

Inflation (Deflation)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 20

„expectations-augmented“ Phillips Curve in the short and long run

Long run Phillips-Curve

Short run Phillips-Curve with high

inflation expectation

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 21

Indexation – An International Comparison

• Changes in price indices are sometimes used

to adjust wage rates or transfer payments.

This is called “Indexation”.

• “Full Indexation” occurs when the wages or

payments are increased at the same rate as the

price index used to measure the inflation rate.

• “Indexation” is especially widespread in

developing countries with high inflation rates.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 22

Indexation – An International Comparison

• Keeping up with inflation: real income stays constant.

1. an arbitrary distribution of income and wealth.

2. Elimination of “Inflation Costs” in the field of national savings and wages.

“Indexation: Are you beating inflation Indexation: Are you beating inflation or is inflation beating you?”or is inflation beating you?”

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 23

Indexation – An International Comparison

• The Business Rates in England

• “Scala mobile” in Italy

• The Prohibition of Indexation in Germany

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 24

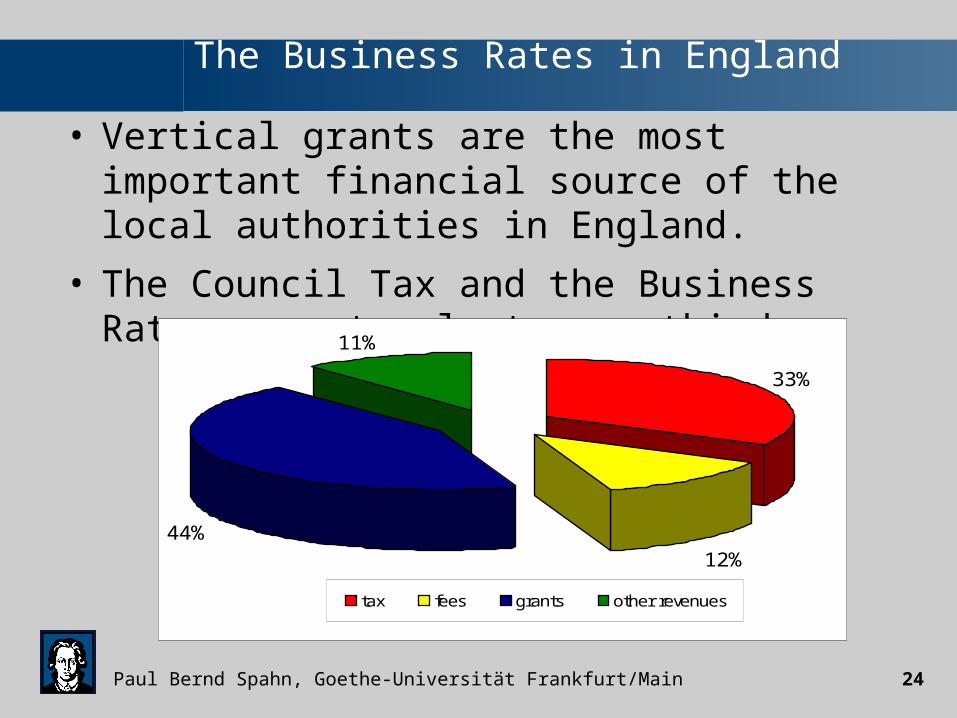

The Business Rates in England

• Vertical grants are the most important financial source of the local authorities in England.

• The Council Tax and the Business Rates amount only to one third.

33%

12%44%

11%

tax fees grants other revenues

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 25

The Business Rates in England

• The Business Rates replaced the Domestic Rates on 1st April 1990.

• The complete tax revenues belong to the local authorities, but the respective yield of the municipalities is not dependent on the collected tax. In fact all cities and municipalities „assign“ the collected tax to a fund of the central government. The central government distributes the revenues with a local equalisation system - mostly based on the number of inhabitants – back to the local authorities. – „Re-Distributed Business Rates“

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 26

The Business Rates in England

• The Business Rates tax only Non-Domestic Property.

• Two factors determine the tax burden of the Business Rates:

1. The Rateable Value of the property, which is fixed by the Valuation Office Agency (VOA).

2. The Multiplier, which is fixed annually by the central government.

• Example: A Rateable Value of 10,000 £, in the tax year 2001-2002 the Multiplier amounted to 43 Pence = 4,300 £ tax burden.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 27

The Business Rates in England

• The „political“ task of the Multiplier is to minimize the tax burden for the population (voters) and on the other side to generate a constant tax yield for the local authorities.

– The Multiplier is is fixed annually by the central government, but it is forbidden by law to raise the Multiplier to a higher figure than the inflation rate.

• An „ Indexation“, but not a “full indexation”

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 28

“Scala mobile” in Italy

• In Italy the relationship between employer and trade unions was extremely tense.

• Therefore from 1946 until 1992 the wages increased at the same rate as the price index.– “scala mobile”– In the majority of the years a “Full Indexation”

• In 1992 the scala mobile were repealed:– 1993 „Ciampi protocol“– 1996 „Accordo per il Lavoro“

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 29

The Prohibition of Indexation in Germany

• In 1948 every form of Indexation was abolished in Germany.– confidence-building measure

• It was only allowed by permission of the Bundesbank to index some price levels. These permissions were rare.

• Because of the introduction of the €, the abolishment of the indexation of loans was cancelled in 1999.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 30

The Prohibition of Indexation in Germany

• Today the indexation of wages, leasing and fees is still forbidden.

• The central government has heralded an inflation-indexed bond with a volume of 10 billion € for the year of 2005.

• Nowadays more than 26 countries worldwide offer an inflation-indexed bond.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 31

Conclusion

• Inflation is a sustained increase in the general

level of prices for goods and services.

• Variations on inflation include deflation,

hyperinflation and stagflation.

• Two theories as to the cause of inflation are

demand-pull inflation and cost-push inflation.

• No inflation (or deflation) is not necessarily a

good thing.