Patterson-UTI Energy, Inc. - Mark E....

46

Patterson-UTI Energy, Inc. Date Valued: April 1, 2005 Brent Foster Dan Turner Lindsey Kobmann Nathan Smith Jonathan Toliver

Transcript of Patterson-UTI Energy, Inc. - Mark E....

Patterson-UTI Energy Inc

Date Valued April 1 2005

Brent Foster Dan Turner

Lindsey Kobmann Nathan Smith

Jonathan Toliver

- 2 -

TTAABBLLEE OOFF CCOONNTTEENNTTSS

Executive Summaryhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 4 Business and Industry Analysishelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 5 -Five Forces Modelhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 5

-SWOT Analysishelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 7 Accounting Analysishelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 9 -Key Accounting Policieshelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 9 -Flexibility in Accounting Procedureshelliphelliphelliphelliphelliphelliphelliphelliphellip 10 -Accounting Strategyhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 11

-Quality of Disclosurehelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 12 -Potential Red Flagshelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 12 -Accounting Distortionhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 13

Ratio Analysis amp Forecastinghelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 14 -Ratio Analysishelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 15 -Competitor Ratio Analysishelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 17 Forecasting Assumptionshelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 22 -Income Statementhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 22 -Balance Sheethelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 23 -Statement of Cash Flowshelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 23 Patterson Valuationhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 24 -Cost of Equityhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 24 -Cost of Debthelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 25 -WACChelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 26 -Method of Comparableshelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 26 -Discounted Cash Flows Modelhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 27 -Discounted Dividends Modelhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 28 -Residual Income Modelhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 29 -Long Run Residual Income Modelhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 30 -Abnormal Earnings Growth Modelhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 31 -Altmanrsquos Z-Scorehelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 32 Intrinsic Valuationhelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 34 Appendices A-Khelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 35-45 Sourceshelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphelliphellip 46

- 3 -

Deep Drilling Investment Group Dan Turner Nathan Smith Brent Foster Lindsey Kobmann Jonathan Toliver

Investment Recommendation Sell or Sell Short Date of Valuation April 1 2005 Market Cap 402 B

Shares Outstanding (2004) 166258000 Valuation Ratio ComparisonTrailing PE 2992

Dividend Yield (3rd and 4th quarters of 2004) 016 (065) Forward PE 12243-month Avg Daily Trading Valume 2746272 Forward PEG 2Percent Institutional Ownership 88 MB 244Book ValueShare 0008$ Valuation EstimatesROE (2004) 1079 Price as of April 1 2005 2581$ ROA (2004) 822 Ratio Based ValuationsEst 5 yr EPS growth rate 15 PE Trailing 1643$ Cost of Capital Estimates PE Forward 1323$ Ke Estimate 725 PEG Forward 3366$ 5-yr Beta 15 Dividend Yield 600$ 3-yr Beta 06607 MB 1075$ 2-yr Beta 0622 Ford Epic Valuation 1295$ Published Beta 1517 Intrinsic ValuationsWACC (bt) 641 Discounted Dividends 653$ Debt Risk Free Cash Flows 2694$ Kd 376 Residual Income 1515$ Altman Z-Score 376 Abnormal Earnings Growth 1515$

Long Run RI 766$

- 4 -

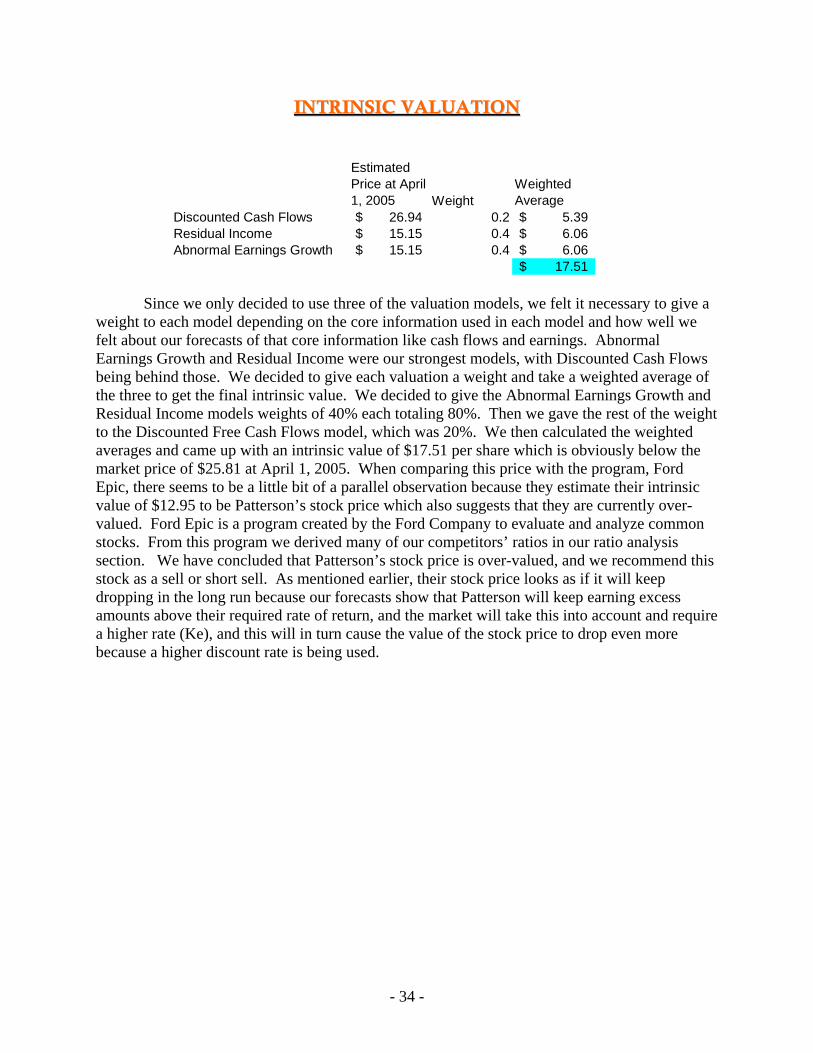

EEXXEECCUUTTIIVVEE SSUUMMMMAARRYY After carefully valuing and researching Patterson-UTI Energy Inc we have concluded that it is over-valued enough to recommend a sell or sell short position on the security On April 1 2005 the security was valued at $2581 by the market Our conclusions lead us to believe that our intrinsic valuation is $1751 Patterson is involved in the oil and gas contract drilling industry which is highly concentrated between a few large firms because they own most of the market shares However the competitors are not completely comparable to Patterson because Patterson is also involved in contract drilling pressure pumping and exploration for oil and gas Profit margins are beginning to increase with the prices of oil and gas and Patterson employs an acquisition strategy to continue its success The industry is growing extremely fast with more and more exploration companies needing drilling services Patterson has a low cost structure which gives them the potential to sustain higher profit margins than the industry The market price for oil and gas strongly dictates the profit margins of the company making it as volatile as the market itself Pattersonrsquos excellent quality of equipment and reliable service give it the second largest market share in the industry Patterson employs a strong strategy of acquiring other firmsrsquo assets for their own use Their no debt capital structure allows them to use this advantage strongly and if they ever need to they can even leverage their buyouts of other assets These assets are mainly paid for with cash and then stock if need be The ability to finance these moves in-house gives them a great advantage over other companies Patterson has increased revenue just about every year at an exceedingly high rate Their revenue in 2004 rose almost 30 and rose even higher in the years before Their profit margins are continuing to increase due to the market prices for oil but these factors can also adversely affect the company by losing business to other firms We expect about a 15 increase in earnings for the future due to acquiring more assets from firms and creating larger amounts of revenue Patterson has had a steady positive cash flow in the past and will continue to increase those in the future through selling off assets and to finance their activities Their investing activities are not very risky and are not very significant Their disclosure of activities and important material related to these activities is clearly visible within the financials The liability sections however do not disclose much information about their debt instruments and the terms of these instruments As mentioned earlier our valuation led us to believe that the stock price of $2581 was definitely over-valued Our strongest valuations came from the discounted free cash flows the residual income and abnormal earnings growth models which were each weighted accordingly The residual income and abnormal earnings models were weighted at 40 each while the discounted cash flows model was weighted at 20 We expect our earnings to constantly exceed what is expected therefore the markets required rate of return will increase and drive down the present value of these models This will ultimately result in a lower stock price giving rise to our over-valued thoughts Also their price earnings growth of about two tends to suggest that they are overvalued Patterson has certain risks when looking in the future that could potentially affect our valuations and thoughts These factors include stronger regulation of the industry substitute products that could replace oilrsquos use and volatility in the stock market and in oil prices These

- 5 -

uncertain futures could potentially cause Patterson to incur losses and not grow to its potential However analysts suggest that earnings will continue to rise and revenues will continue to grow

BBUUSSIINNEESSSS AANNDD IINNDDUUSSTTRRYY AANNAALLYYSSIISS

Patterson-UTI Energy Inc is a West Texas based company that operates in the oil well services and equipment industry They primarily operate as a contracted drilling company for various businesses throughout the southwestern United States They specialize in drilling for oil and natural gas in select regions throughout the United States including Western Canada New Mexico Texas Oklahoma Louisiana Mississippi and the Gulf of Mexico They also provide completion fluid services to these operators which consist of using products that cool and lubricate the bit during drilling operations Another service that is provided is pressure pumping services for oil and natural gas wells which they mainly concentrate around the Appalachian Basin region These services mainly consist of inserting fluids into new or existing wells in order to enhance the flow of the oil out of the well They also specialize in cementing between the wall of the well bores and the casing to stabilize and center the casing While providing services to major and independent oil companies they also compete in their own exploration development and acquisition of oil and natural gas As a competing leader in land-based drilling Patterson has acquired equipment from various companies such as Key Energy Services Inc allowing them to grow in size and strength in the contracting market With a $34 billion market capitalization Patterson currently controls 396 rigs located in their regions of business while possessing a moving fleet of 45 trucks and 100 trailers making the company the second largest drilling fleet in North America The acquisition of many oil rigs and large amounts of equipment has enabled them to steadily grow and expand while increasing revenues and market share Most of the drilling contracts are continuations of existing customers while the rest are negotiated or acquired through a competitive bid

Five Forces Model

Competitors

While there are large amounts of firms involved in the oil well services and equipment

industry there are quite a few competitors that have high market shares making it a relatively high concentrated industry in the main areas of the southwest region in which their business is conducted The leading market capitalization competitor for Patterson is Nabors Industries Ltd which operates a fleet of almost 600 land-based oil drilling rigs Nabors also competes offshore giving them extra room for potential growth and market share Other major competitors for Patterson include Helmerich amp Payne Inc and Grey Wolf who each specialize in land drilling services to major and independent operators With market capitalizations of $2 billion and $1

- 6 -

billion respectively they are continuously competing to gain market share in the industry With the large amounts of existing firms involved in the oil industry as a whole there is little room for new firms to enter due to many factors Large amounts of capital are needed to start up and succeed or even compete with already established companies One of the only major threats is not the entrance of new potential competitors but the merging of already established companies to increase revenue and create an even larger corporation much like Patterson has already taken action in doing

Threat of Substitutes

Since oil is a commodity and oil is oil there arenrsquot too many threats of substitute oils

that could be used instead of the kind being drilled during business However there are future threats to the industry as a whole for quite a few reasons First of all because of the dependence on foreign oil we are forced to accept even outrageous prices for barrels of oil It has also hurt our net exports in that our imports outweigh our exports which lowers our GDP In response to these issues as well as certain environmental issues many companies and even governmental agencies are starting to pursue research and development of alternative fuel sources One of the alternative fuels in use is hydrogen based energy which is less harmful to the environment costs less and is all around more efficient Evidence of these new alternatives can be seen by the automobile industry which is a main user of petroleum products Many main automobile manufacturers have already produced or are in the process of designing hydrogen fuel cell cars Another alternative fuel source which could reduce demand for oil and ultimately reduce demand for Patterson oil services is the development of biomass products that consist of wood crops or animal waste Cellulose which makes up about half of all the organic carbon on the planet is particularly a main potential substitute product because ldquoadvances in genomics and industrial biotechnology promise to convert cellulosic biomass to fermentable sugars that can be used as feedstock for a new type of lsquocarbo-hydrate crude oilrsquordquo

Bargaining Power of Buyers

The bargaining power of buyers is relatively high because unless you have a close on-

going relationship for service and drilling the deal goes to the lowest bidder which in Pattersonrsquos case would result in lower profit potential Unless brand new state of the art equipment is possessed by other companies there is no real solid way for Patterson to differentiate themselves from competing firms which makes competition even stronger Also customers have the ability to cancel drilling contracts on short notice which would decrease Pattersonrsquos oil rig utilization Another factor that gives the buyers bargaining power is the contract lengths Most are short-term contracts consisting of only one or a few drillings on one well which gives a rise to the uncertainty of future business While demand for drilling services has declined over the past few years there have been more available rigs than what are needed to meet demand putting Patterson and other firms at the mercy of buyers Finally many large producers of oil such as Exxon have almost completely abandoned the exploration and development of oil giving less business to contractors like Patterson

- 7 -

Bargaining Power of Suppliers

The bargaining power of Pattersonrsquos suppliers is relatively low This is important because it helps Patterson to achieve a desired profit margin One of Pattersonrsquos main sources of suppliers and a major expense for them is contract welding In most areas where Patterson does business there is an abundance of welders and the contract generally goes to the lowest bid Another example of the power that Patterson has over suppliers is their ongoing partnership with General Motors Because they buy pickups in mass quantities General Motors offers them highly discounted rates

Competitive Strategy

Pattersonrsquos overall corporate strategy is to increase cash flow and earnings per share by

continuing to increase its position as a leading player in domestic land drilling Patterson believes it has a strong reputation for providing high quality service an experienced workforce and for providing well maintained equipment Patterson supplies highly technical drilling equipment and provides quality service which will help to build on existing customer relations as well as developing new business opportunities They will also provide superior service by placing an emphasis on efficiency dependability and safety Pattersonrsquos rigs are maintained in good operating condition through an in-house process capable of manufacturing and repairing its fleet of drilling rigs They consider this to be one of their top competitive advantages Having top quality equipment allows Patterson to maximize its rig utilization as well as help with pricing strategies Patterson plans to continue to grow through acquisition This is evident by its recent purchases of TMBRSharp Drilling and Key Energyrsquos drilling rigs The company sees attractive opportunities to expand its drilling rig fleet Following an acquisition the company overhauls the purchased rigs to meet its standards of quality and dependability Another major strategy is to operate an efficient cost structure Patterson uses its own fleet of trucks and trailers to rig down transport and rig up its drilling rigs This helps them to be more efficient by reducing the time associated with the costs The companyrsquos oil and natural gas activities are designed to complement its land drilling operations and diversify their overall strategy They plan to increase their oil and natural gas reserves through developmental and exploratory drilling The focus of these operations will be in the Austin Chalk Trend the Permian Basin of West Texas and Southeastern New Mexico and in South Texas To further its diversification Patterson also provides contract drilling fluid services These services were added in 1998 and coincide well with its other operating activities

SWOT Analysis

Strengths

The number one strength for Patterson is their reputation They are well known in the

drilling industry for providing quality and reliable service Another major strength for Patterson is the fact that they have zero long term debt This is a key factor that helps in their strategy to pursue mergers and acquisitions Pattersonrsquos recent acquisitions have been paid for in cash This shows that the company plans to remain debt free Pattersonrsquos fleet of rigs is well accommodated for shallower oil drilling This is important because recent high oil prices have

- 8 -

significantly increased the demand for shallow oil drilling Also Patterson generally has a high rig utilization rate At any given point in time the majority of their rigs are being utilized Another strength for Patterson is that they are continuing to grow and maintain their strong position in the industry For example in the third quarter of 2004 Net Income rose 93 to 703 million The last major strength for Patterson is the fact that the company is still operated by the original founders The company like most new companies started out very small The same people have grown the business into what it is today Their experience and knowledge of the industry is a major strength

Weaknesses

The number one weakness for Patterson is the fact that their business is highly geared

toward oil and gas prices If prices of oil and gas take a significant downturn then the demand for the services that they offer will also decrease Another weakness for Patterson is that they do not have an offshore or international presence in the drilling industry Natural gas deposits in the US area are shrinking rapidly and they donrsquot have an international presence to protect against this decline The last major weakness for Patterson is a potential shortage of skilled labor In times of high demand the demand for labor significantly increases and there could potentially be a shortage of workers who are qualified

Opportunities

When oil and gas prices are high and the drilling industry is in high demand many

opportunities exist for Patterson A major opportunity would be for them to continue their strategy of acquiring other companies Continuing to add to their fleet of rigs that they already have established is an opportunity for them to expand even further Another opportunity that Patterson has not taken advantage is trying to expand to off-shore drilling and take part in international markets The majority of the worldrsquos oil is in foreign countries so services that Patterson offers are needed overseas The last opportunity would be for Patterson to gain market share in its divisions of pressure pumping services and production and acquisition of oil

Threats

Patterson also faces serious threats that could hurt their business A major threat for

Patterson is a potential decline is oil and gas prices They have absolutely no control over this and if prices were to take a large tumble then they would face a significant decline in demand for services Another threat would be is if there strategy of acquisitions backfired When you acquire another company there is a great amount of risk involved The last threat for Patterson would be the threat of a new entrant into the industry Another large company could potentially be a threat if they were to try to compete in the drilling industry

- 9 -

AACCCCOOUUNNTTIINNGG AANNAALLYYSSIISS

Patterson uses many different accounting procedures that are significant to the company

The consolidated financial statements include everything from Patterson-UTI and its wholly owned subsidiary companies Due to its unique nature of business Patterson utilizes many accounting procedures that involve many estimates These estimates include and are not limited to allowance for doubtful accounts depreciation depletion asset impairment costs yet to be incurred on current drilling projects reserves and fair values of assets All the reported estimates just discussed greatly impact reported financial statements Many components of the Assets and liabilities section are based on these estimates Along with the balance sheet the income statement is also strongly influenced by these estimates As one might infer actual results could be slightly or even significantly different than on the reported statements giving rise to possible adjustments

Key Accounting Policies

One key principle of their accounting policies includes the recognition of revenue For

general purposes revenue is recognized when services are performed The main method of recognizing revenue is under the percentage of completion method which recognizes revenues earned and expenses incurred over the life of the drilling project These values are proportionately recognized over subsequent periods and are based on managementrsquos estimates of costs yet to be incurred by the project This method is mainly used for footage contract drilling On the other hand when dealing with a turnkey contract the company uses the completed contract method A turnkey contract is a fixed contract that specifies a certain amount to be paid to Patterson and in return the drilling could incur more expenses than estimated and result in potential loses or lower profit margins For this reason the completed contract method is used as it recognizes all of the revenues gained and expenses incurred at the end of the project completion

As for assets of the company there are different ways of accounting for each one that is common to Patterson and the industry it is in First of all the inventory for Patterson is not very large because they are a service providing company The main component of their inventories is primarily a combination of chemical fluids These fluids assist in the servicing of wells and in the completing of wells and are expensed on a first in first out method

The bulk of the companyrsquos equipment consists of drilling rigs and related equipment which is all depreciated using the straight-line method This method best suits the companyrsquos interests because many times rigs go unused and may remain idle for certain periods of time It would seem illogical to assess an increasing or decreasing cost to an asset by using accelerated methods when these assets are sitting idle

In relation to what the inventory of rigs actually produces oil and gas drilling does not always end successfully For this reason the successful efforts method of accounting is used

- 10 -

during the projects This method of accounting entails that all explorations costs are capitalized to the project when there is discovery of oil or gas At times when it is determined that certain exploration costs do not directly result in the discovery of oil or gas management expenses those costs accordingly Wells that are in progress are reviewed quarterly for reserve classification At these times judgments on impairment are made Impairment can result for many reasons For example the revision of reserves could result in a downward estimate of reserves left giving grounds for impairment and the writing down of that asset Another important factor affecting the judgment for impairment is oil and gas prices A decline in these prices reduces the carrying value of the oil and gas properties and results in impairment In a related situation if the net carrying book value of an oil field is more than the undiscounted cash flows it is expected to produce then it is written down for the difference between the book value and the discounted cash flows

The company also has credible name of goodwill for many reasons First of all they are the second largest on shore drilling company in the United States and have established goodwill for that Another reason and the most important one for their goodwill standing is their strategy of merging with other smaller companies or acquiring their assets Goodwill is defined as the excess amount between the purchase price and the fair value of the net assets being acquired Prior to 2002 goodwill was amortized over the expected benefit of 15 years but after adopting SFAS No 142 it was determined that goodwill was indefinite In adoption of this statement it is no longer required to amortize goodwill if its usefulness is indefinite but goodwill must be tested annually for impairment in any instance that indications of its fair value may fall below its carrying value

Another key policy that deals with their employees and stock compensation is the fact that instead of applying the fair value method to granting stock options the company uses the recognition method under APB Opinion No25 which states that net income is not affected by the costs of granting these options because all of the options have exercise prices equal to or above the market value of the stock on the date of the grant

Flexibility in Accounting Procedures

Any company has a reasonable amount of flexibility that they are able to use due to

FASB allowing the use of different accounting methods First of all they use a straight-line method of depreciation on their equipment which represents an average cost each period to assets The estimates of these useful lives vary greatly and give a lot of flexibility to the amount of depreciation expense to cost in the period after actuaries review these assets Also according to SFAS No 19 exploration costs are initially capitalized to the well until it is known if it will actually result in the extraction of oil or gas If not then the cost is expensed The ability to initially overstate your assets would help push strong asset ratios which may not be true This could also lower expenses in times where there is a need of high income They may wait longer than when it is determined if the well is a success or not to actually charge the explorations costs to the expense account which does not represent the true nature of the business

The inventory method of FIFO gives the ability to manipulate a higher net income because old and deflated prices are expensed to cost of goods sold instead of newer inflated prices

The use of the asset and liability method for tax purposes gives extreme flexibility to Patterson For example if a temporary difference exists and Patterson paid more in taxes than

- 11 -

they recognized they will have a deferred tax asset for future periods This means that there is extreme flexibility in how internal reporting can differ from external reporting which results in temporary differences These flexibilities may be used for example to pay more income taxes in a good year of good business by recognizing less revenue than what the government recognizes for tax purposes This allows you to pay those taxes now when you havenrsquot accounted for them fully on the books giving rise to a deferred tax asset in some future time when business may not be so good

Another flexibility that Patterson has is the ability to minimize expenses due to no longer amortizing goodwill After adopting SFAS No 142 the company no longer expenses goodwill annually but instead checks for impairment each year The fact that there is such great judgment allows flexibility in the decision for impairing the goodwill of the company or not In times where there could potentially be an impairment the actuaries may deem it necessary to not impair the goodwill maybe because the impairment is not significant in amount Over time these little impairments that would not be recognized could add up to be one significant impairment that would never have been recognized but would significantly show the underlying nature of their name to the industry

In dealing with their employees benefits of stock compensation there is a lot of room for flexibility Due to the decision of using APB Opinion No 25 the companyrsquos net income is not affected by the cost of granting stock options In 2003 if the company had adopted and used FASB Statement No 123 net income would have been affected and it would have decreased by about 10 million which is very significant The ability to not show this effect gives them great flexibility in manipulating their net income

Reserve estimates also give extreme flexibility to the industry and especially Patterson These estimates change every year and are based upon various assumptions such as oil and natural gas prices operating costs reservoir performance and economic conditions The main flexibility of these estimates arises in the natural gas area For example there were changes in estimates of gas reserves of $609000 $2103000 and $-1123000 in the years 2001 2002 and 2003 respectively

Accounting Strategy

Overall the accounting strategy of Patterson fits the norms of the industry For example

in the exploration for oil and natural gas exploration costs are initially capitalized until it is determined if oil or natural gas is discovered and extracted This is a practice that other oil and gas drilling companies use because of the nature of the industry However while their depreciation policies match that of the industry Patterson does not use a provision for salvage value which makes them differ in that respect This decision would give a higher depreciation expense each year resulting in lower net income This approach is taken because the company expects full utilization of their equipment until the asset is inoperable or completely used up This also leaves little room for very aggressive or even conservative depreciation accounting because straight-line is an average expense and they do not try and lower expenses by involving a salvage value in their depreciation expense

Another strategy adopted by Patterson that is used strategically is the recognizing of employee stock options This compensation is used in a way that costs of granting the options to employees is not deducted from net income resulting in a higher income which one year was a $10 million amount but not deducted because of the adoption of APB Opinion No 25

- 12 -

Patterson leases equipment facilities and acreage to outside parties while also leasing themselves They do not consider these non-cancelable operating leases to be a material part of the operations because they mainly rent equipment for less than 75 of the equipments useful life

Quality of Disclosure

Patterson does a thorough job of disclosing the firms accounting quality and financial

statements Patterson goes beyond what is required by GAAP and does a good job of describing the true financial position of the company Patterson operates in four business segments including contract drilling pressure pumping drilling and completion fluids and oil and natural gas exploration Patterson does an excellent job in breaking down each business segment They do a thorough evaluation of each segment and show how much of a percentage it was of their total revenue for the quarter or year Patterson chooses to show the costs associated with each segment and also how profitable each segment is Patterson also gives a detailed explanation of the positive and negative factors that affects each particular business segment

Patterson also chooses to go into great detail when disclosing information in the footnotes They make this information very easy to decipher through When a new FASB regulation is issued they go into great detail about how it affected them and their industry and the overall affect that it had on Net Income An example of this is the fact that Patterson showed what the affect on Net Income would be if they were to use FASB No 123 instead of APB Opinion No 25 in regards to their employee benefits regarding stock compensation Patterson even chooses to disclose new accounting regulations that do not have an impact on its operating or financial position but it potentially could

Throughout their financial statements Patterson does a fairly good job of disclosing negative information that could potentially be harmful to their business and industry They clearly state that their operations are extremely dependent on the market price of oil and natural gas Also they disclose that each segment that they operate in is highly competitive which can adversely affect their operating results They also state that in times of increased demand it is common to have labor shortages and shortages of drill pipe and replacement parts

Patterson is also very transparent in their reporting of related party transactions They conduct business regularly with family of the CEO COO and CFO They go into great detail about the type of business conducted with these related parties and even show how much money is paid out to each entity

Potential Red Flags

The ratio of net sales to inventory has been pretty consistent over the past five years but

in 2000 there was an unusual ratio of 263 This is because there was a large amount of inventory available to the amount of sales that year The increase in sales of completion fluids was 174 from 1999-2000 while the increase in inventory was 518 However from the year 2000-2001 the inventory only increased 33 compared to an almost 200 increase in sales This means that lots of inventory in 2000 was sitting around not being used and may have been used in the large increase in 2001 sales This large increase in inventory compared to sales from 1999-2000 could be to possibly inflate the asset account to achieve certain ratios

- 13 -

0

1

2

3

4

5

6

2003 455

2002 456

2001 58

2000 263

1999 59

Net SalesInventory

In 2001 the declining asset turnover ratio is a lot higher and this could be due to a few reasons In the case of Patterson though the sales compared to assets ratio can be attributed to the fact that there was an increase in sales of 221 compared to an increase of about 19 in current assets This unusually high ratio can be attributed to the fact that in 2001 Patterson experienced an unusually high increase in demand for their services compared to what they have been used to in the past Therefore not enough assets were available for the increase in sales resulting in the high ratio

252 217

496

184

258

0

1

2

3

4

5

2003 2001 1999

NetSalesCurrentAssets

Accounting Distortions

After reviewing Pattersonrsquos financial data and providing an accurate accounting analysis we have concluded that there are no major distortions in the accounting numbers due to accounting policies and strategies The transparent reporting of Patterson allows us to accurately visualize the impact of all accounting numbers on the economics of the business Therefore we do not believe any changes should be made that would significantly change the accounting data

- 14 -

RRAATTIIOO AANNAALLYYSSIISS AANNDD FFOORREECCAASSTTIINNGG

After studying and identifying a firmrsquos key accounting policies and strategies it is necessary to start accessing the firmrsquos performance based on its goals and strategies This can be accomplished by comparing financial statements from this year and years past Once drawn together a ratio analysis can be performed that provides past occurrences and trends for the company These trends can be analyzed and molded into forward looking assumptions that will help in the forecasting process of a firmrsquos performance Many different performance measures are used in the ratio analysis and these include liquidity profitability operating efficiency and capital structure The profitability ratios can be used to determine the constraints of the companyrsquos liquidity and the operating efficiency ratios can be tied to how profitable a firm is which relates to the overall capital structure These trends and forecasting assumptions can be compared to not only the past and future performance of a firm but to the performance of its competitors and even its industry of competition This will further enhance the true performance of the firm if there are different benchmarks to which you can compare performance

In the following sections Patterson-UTI Energy will be evaluated to assess its current past and future performance Fourteen ratios will be used that contribute to either the liquidity profitability operating efficiency or capital structure Then these ratios will be evaluated over the past five years to determine if there are any trends and if so what path these trends could continue or cease to follow As with all profit seeking companies the only way to make more is to sell more and the only way to sell more is to grow Therefore growth is a key element in determining a firmrsquos future performance We will now take a look at these fourteen ratios for the past five years of Pattersonrsquos operations

- 15 -

Ratio Analysis

2004 2003 2002 2001 2000 Sales Growth 2894 4701 -4667 7000 8900 Liquidity Analysis Current Ratio 258 270 323 223 215 Quick Asset Ratio 218 219 241 188 185 Inventory Turnover 3827 3733 2628 3649 3317 Accounts Receivable Turnover 467 496 533 740 425 Working Capital Turnover 422 389 315 899 457 Profitability Analysis Gross Profit Margin 3216 2687 2372 4003 2622 Operating Profit Margin 1711 1123 064 2699 1178 Net Profit Margin 1086 726 44 1658 639 Asset Turnover 076 072 056 114 079 Return on Assets 822 52 250 1888 503 Return on Equity 1079 688 320 2389 773 Capital Structure Analysis Total LiabilitiesTotal Equity 031 032 028 027 054 Times Interest Earned 24635 29860 639 000 000 Debt Service Margin 0 0 0 0 0 SGR 98 0 0 0 0 Dividend Payout Ratio 00 00 00 00 922

These ratios provide adequate information for investors but can be a little misleading This is because of the industry that Patterson is involved in which is very volatile to market conditions These market conditions determine prices of commodities such as oil and gas which are keys to Pattersonrsquos business When the market hurts and there is a rise in the price of oil producers tend to want to supply more at that higher price and an increase in the demand for oil drilling and completion services results Conversely a drop in oil prices negatively impacts this industry because exploration companies do not find it to be profitable to spend such large expenditures on cheap ldquosalesrdquo A prime example of the just mentioned scenario has occurred within the past five years resulting in large increases and decreases in sales growths for Patterson

Liquidity Analysis

Everything else remaining constant they have a very good liquidity structure Their current ratios tend to suggest that they have more than enough assets to cover any upcoming liabilities Even when that ratio is broken down further into only cash and cash equivalents as in the quick ratio evidence still shows that any upcoming liabilities are easily covered These ratios tend to rise steadily each year become stronger and stronger Now when liabilities are discussed it is important to realize that Patterson has no long term liabilities such as notes payable They pay for most of their assets in cash or in stock options as is the common case when dealing with mergers and acquiring another companyrsquos assets Also their times interest

- 16 -

earned ratio suggests that their interest expense is next to nothing also giving rise to no long term debt In conclusion their liquidity is very strong and improving as they become more and more debt-free and increase the use of their acquired assets because their rig utilization is a large factor of their profitability

Profitability Analysis

Looking at the next section of profitability we see that the results are as volatile as the

sales Once again these are due to the market conditions that drive the demand for Pattersonrsquos products and services Overall it seems that the three different profit margins seem to be on the rise suggesting possible larger growth patterns in the future These larger profit margins are possibly the result of increased oil prices and increased demand for drilling services For almost the past year oil prices have been very strong and high giving way for one of their highest margins of profitability in the past five years Their asset turnover is staying strong but shows no signs of any significant future increases This is a downside to their future profitability though because in order to have more sales and thus higher revenue a firm must turnover its assets faster and faster by using them during operations Also their returns on investments of assets and equity tend to be strong for the moment after some very bad years in the past These ratios especially return on equity must be strong and continuously improving in order to meet expected future growth opportunities Their overall profitability has a stronghold right now but can take either a drastic cut or increase due to future market conditions

Capital Structure Analysis

Pattersonrsquos overall capital structure seems to be very strong but historyrsquos debt to equity

ratio is suggesting that their equity portion is slowly declining However the absence of any long-term debt makes up for this decline because no large future decisions about expenditures on interest and principal payments must be taken into account Another key factor that suggests a strong capital structure is the four years of blank dividend payout ratios These may be in part because there were not very large incomes in a few years like 2000 2002 and 2003 They could also be blank because the company wanted to expand its growth at a faster rate by acquiring more assets to boost sales and profitability The dividend payouts in 2004 could be a result to the success in acquiring more assets and profits and they might have deemed it necessary to share these earnings with their shareholders The capital structure of Patterson suggests that they are planning for future growth and finance their own large acquisitions of assets

By comparing these ratios over the five year spread and omitting any random variations we can derive estimates for future ratios based on any gradual increases sustainability or decreases in these past ratios These will then be used to predict future liquidity profitability and capital structure assessments used in valuing Patterson For now we will take a closer look at these ratios and how they compare to the competitors of Patterson and the industry of oil well drilling as a whole When analyzing a company it is important to remember that their performance is not solely based on the amount of money they produce or how many sales they have but how they benchmark against their competitors and the industry Therefore it is important to find trends in the competitorsrsquo ratios and the industryrsquos ratios and forecast a future performance of these ratios

- 17 -

Then we can compare Pattersonrsquos forecasted ratio performance to their competitorsrsquo and the industryrsquos in order to predict future competitiveness and success Competitor Ratio Analysis

Liquidity Analysis

Current Ratio 2000 2001 2002 2003 2004 Nabors NA 312 182 253 25 Helmerich amp Payne 336 393 245 225 41 Grey Wolf 205 295 325 235 23 Patterson 215 223 223 270 258 Industry Avg 252 305 243 245 287

When looking at the liquidity of Pattersonrsquos three competitors and the industry most of

the ratios seem pretty head on There are a few variable differences but Patterson matches in well with the industry average The current ratio for Patterson is the highest which suggests that they have a smaller amount of current liabilities andor a larger amount of current assets allowing them to contribute greatly towards any possible debt in the future

Quick Asset Ratio 2000 2001 2002 2003 2004 Nabors NA 273 159 222 249 Helmerich amp Payne 272 321 191 146 331 Grey Wolf 199 292 318 226 235 Patterson 185 188 241 219 218 Industry Avg 218 268 227 203 258

On the other hand their quick asset ratio is the smallest of the group which suggests that their current assets arenrsquot as strong as the industryrsquos or their competitorsrsquo This becomes true because Patterson also has income from completion services and other well servicing activities When eliminating the inventory from the current assets section along with prepaid expenses we see that it pulls Patterson below the competitors This suggests that these portions of current assets are greater for Patterson

Inventory Turnover 2000 2001 2002 2003 2004 Nabors NA 7383 4745 5483 8256 Helmerich amp Payne 915 131 1497 1533 2001 Grey Wolf NA NA NA NA NA Patterson 3317 3649 2628 3733 3827 Industry Avg 2116 2479 2957 3583 4694

Days Supply of Inv 2000 2001 2002 2003 2004

- 18 -

Nabors NA 494 769 663 442 Helmerich amp Payne 3989 2786 2438 238 1824 Grey Wolf NA NA NA NA NA Patterson 11 10 1389 977 954 Industry Avg 1725 1472 1234 1018 778

When looking at the inventory turnover ratio it is obvious that Patterson has a turnover that is twice as slow as the rest of the industry This can be due to a few reasons First of all Pattersonrsquos inventory mainly consists of completion fluid products This segment of business is very minimal compared to the total operations of the company therefore it is not used as often This logic leads us to conclude that since this part of business is not utilized as often as their drilling then the turnover of inventory should not be very high either The number of days that inventory sits idle seems to be about even with the industry This seems to be on average about 10 days at a time that inventory sits idle given a 365 day year

Accts Rec TO 2000 2001 2002 2003 2004 Nabors NA 61 458 458 43 Helmerich amp Payne 338 427 521 557 445 Grey Wolf 436 642 532 475 475 Patterson 425 740 533 496 467 Industry Avg 3996 604 511 496 454

Days Supply of Rec 2000 2001 2002 2003 2004 Nabors NA 598 796 796 848 Helmerich amp Payne Grey Wolf 837 568 686 768 768 Patterson 858 493 684 735 782 Industry Avg 837 583 741 741 808

Their accounts receivable turnover is also one of the higher out of its competitors due to

its lower amount of receivables Overall the past five years show they have been about as consistent in their accounts receivable turnover as the rest of the industry The amount of days that receivables are outstanding compare quite nicely with the rest of the industry This now suggests that no company has an overly strict policy of receivable turnovers and it is taking an average of around 70 days to collect on unpaid accounts

Working Capital TO

2000 2001 2002 2003 2004

Nabors NA 314 237 205 21 Helmerich amp Payne 194 223 456 458 319 Grey Wolf 448 383 219 416 41 Patterson 475 899 315 389 422 Industry Avg 372 455 306 367 34

- 19 -

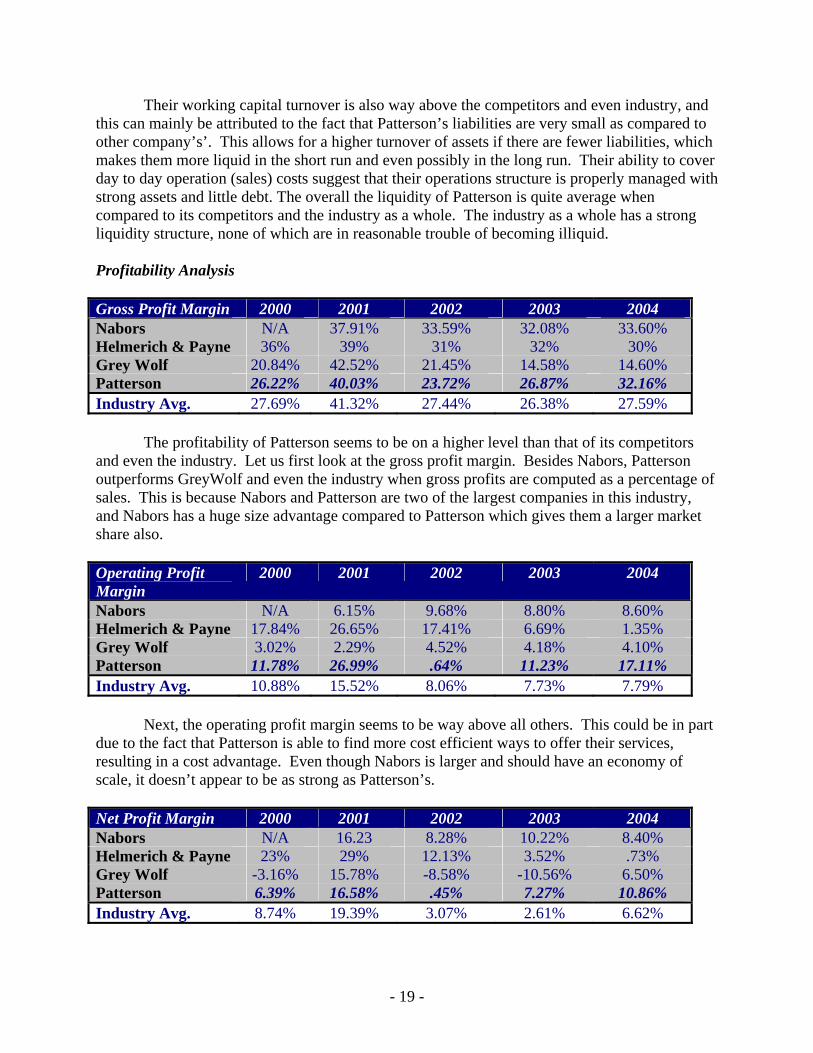

Their working capital turnover is also way above the competitors and even industry and this can mainly be attributed to the fact that Pattersonrsquos liabilities are very small as compared to other companyrsquosrsquo This allows for a higher turnover of assets if there are fewer liabilities which makes them more liquid in the short run and even possibly in the long run Their ability to cover day to day operation (sales) costs suggest that their operations structure is properly managed with strong assets and little debt The overall the liquidity of Patterson is quite average when compared to its competitors and the industry as a whole The industry as a whole has a strong liquidity structure none of which are in reasonable trouble of becoming illiquid Profitability Analysis

Gross Profit Margin 2000 2001 2002 2003 2004 Nabors NA 3791 3359 3208 3360 Helmerich amp Payne 36 39 31 32 30 Grey Wolf 2084 4252 2145 1458 1460 Patterson 2622 4003 2372 2687 3216 Industry Avg 2769 4132 2744 2638 2759

The profitability of Patterson seems to be on a higher level than that of its competitors

and even the industry Let us first look at the gross profit margin Besides Nabors Patterson outperforms GreyWolf and even the industry when gross profits are computed as a percentage of sales This is because Nabors and Patterson are two of the largest companies in this industry and Nabors has a huge size advantage compared to Patterson which gives them a larger market share also

Operating Profit Margin

2000 2001 2002 2003 2004

Nabors NA 615 968 880 860 Helmerich amp Payne 1784 2665 1741 669 135 Grey Wolf 302 229 452 418 410 Patterson 1178 2699 64 1123 1711 Industry Avg 1088 1552 806 773 779

Next the operating profit margin seems to be way above all others This could be in part

due to the fact that Patterson is able to find more cost efficient ways to offer their services resulting in a cost advantage Even though Nabors is larger and should have an economy of scale it doesnrsquot appear to be as strong as Pattersonrsquos

Net Profit Margin 2000 2001 2002 2003 2004 Nabors NA 1623 828 1022 840 Helmerich amp Payne 23 29 1213 352 73 Grey Wolf -316 1578 -858 -1056 650 Patterson 639 1658 45 727 1086 Industry Avg 874 1939 307 261 662

- 20 -

Then the net profit margin sums all of these other profit margins up and Patterson is still one of the leaders One of the factors in a higher net income is the cost advantage Patterson seems to hold Another reason is that there are very little interest expenses because Patterson has no long term debt and long term debt can generate large amounts of interest expenses and disable expenditures that could otherwise be spent for investing activities to make more profits

Asset Turnover 2000 2001 2002 2003 2004 Nabors NA 53 29 34 34 Helmerich amp Payne 29 38 39 36 42 Grey Wolf 53 69 42 54 54 Patterson 79 114 56 72 76 Industry Avg 54 69 41 49 52

The asset turnover ratio for Patterson seems to dominate all others This is in part

because Pattersonrsquos business success depends on their rig utilization rate and the higher the rate the more assets they turnover Basically we think that Pattersonrsquos strategy of acquiring other drilling assets and merging with other similar companies will result in higher sales and higher profits commenced by a higher asset turnover rate

ROA 2000 2001 2002 2003 2004 Nabors NA 861 240 343 290 Helmerich amp Payne 653 111 518 126 31 Grey Wolf -167 1094 -364 -571 350 Patterson 503 1888 25 52 822 Industry Avg 330 1238 104 105 373

The return on assets also seems to rise far above any of the competitors This means that

more of their assets contributed towards net income and a high asset turnover entails a higher return on assets as each of those assets contribute more towards each sales dollar Patterson will continue to have a high return on assets as they stick to their strategy of acquiring other companiesrsquo assets in the future

ROE 2000 2001 2002 2003 2004 Nabors NA 1924 563 772 870 Helmerich amp Payne 861 1405 71 195 48 Grey Wolf -491 2791 -953 -1544 880 Patterson 773 2389 32 688 1079 Industry Avg 381 2127 88 28 719

Finally the ROE seems to be a little higher than the othersrsquo due to the fact that their

overall profit margins are also slightly higher The overall profitability of Patterson seems to be greater than their competitors and the industry and it suggests that this is a good indication of their liquidity needs Their ability to out perform their expected return allows for the higher ROE then their competitors

- 21 -

Capital Structure Analysis The capital structure of Patterson also suggests that they are one of the leading competitors in the industry DebtEquity 2000 2001 2002 2003 2004 Nabors NA 123 135 125 8 Helmerich amp Payne 32 27 37 55 54 Grey Wolf 195 155 162 17 122 Patterson 54 27 28 32 31 Industry Avg 94 83 91 96 72

First of all their debt to equity ratio is a lot smaller across the board especially when compared to the competitors This is mainly because of the afore mentioned fact that Patterson has a very small amount of liabilities almost all of which are current They acquire their assets with cash and try and keep a very liquid structure This strategy holds true for just about every year the past five years suggesting that Patterson has never run into a credit problem because their debt is cheap and minimal and they can possibly finance their own money needs through the company

Times Interest Earned

2000 2001 2002 2003 2004

Nabors NA 882 254 308 347 Helmerich amp Payne 1336 4731 9308 276 63 Grey Wolf 47 1248 -32 -75 NA Patterson NA NA 639 2986 24635 Industry Avg 692 2287 2542 7592 8348

Also their times interest earned ratio completely overtakes all the others Once again this due to the fact that Patterson has very little interest expense if any at all The fact that they have such little interest to pay gives way to the huge ratio that is nearly 30 times all the others Their small amounts of liabilities allow them to incur these small amounts of interest payments giving rise to a large ratio

Debt Service Margin

2000 2001 2002 2003 2004

Nabors NA 5397 13 73 17 Helmerich amp Payne NA NA NA 322 NA Grey Wolf 1492 16271 191 -75 15 Patterson NA NA NA NA NA Industry Avg 1492 10834 1605 107 16

Another ratio that deals with their no-debt capital structure is the debt-service margin It is at zero because Patterson has no type of long term notes payables This strengthens their capital structure in such a way that if they ever got into trouble it would be very easy to borrow

- 22 -

money This would help them cover any expenses that need to be covered or even grow even more by leveraging Lending companies would be more than happy to lend to Patterson because they have very little risk and they do not have any other debt obligations which gives them a first lien on the company Next Pattersonrsquos SGR or sustainable growth rate is above all of the competitors because of a couple of reasons First of all their return on equity is higher which contributes to this ratio Second the profit margins of Patterson seem to dominate giving way to a greater ROE Another amazing fact is that with a newly created dividend payout ratio of about 92 the SGR is still higher This further strengthens the notion that Patterson has the ability to grow especially with debt leverage In the end Patterson has one of the strongest capital structures in the industry giving way to a larger opportunity for growth and success

FFOORREECCAASSTTIINNGG AASSSSUUMMPPTTIIOONNSS

When analyzing and valuing a company it is not wise to only rely on current and past information because that will soon be irrelevant as time passes Furthermore the past does not tell the future it can only predict it and thatrsquos what the next step is Forecasting is a mechanism that allows analysts to assess whether the competitive advantages and successes of the company are able to be maintained or even enhanced Therefore we have taken these previously mentioned ratios and extended them out for ten years in order to forecast future income statement balance sheet and cash flow numbers Once again the previously mentioned ratios were all picked on the basis that they will likely be the future ratios These ratios are based on trends of the companies for the past five years and are encouraged to accurately describe their possible future Income Statement

We decided to start with the income statement by predicting sales because sales entail the ability to profit acquire assets rid liabilities and gain cash flow We first forecasted an increase in sales of 15 each year for Patterson due to a few reasons First of all it is a very conservative number because the growth in sales could easily be twice as much or even zero This is due to the fact that the oil industry and anything related to it is very dependent on market conditions and oil prices This makes the industry very volatile and explains the large increases and decreases in sales We chose 15 because the trend right now seems to be rising oil prices and it seems as though they will continue to rise and not lower This means that companies are willing to supply oil at this higher price and it calls for an increased demand in Pattersonrsquos services With the increased demand in services there will surely be a rise in sales to accompany our predictions Now when compared with the SGR it is questioned if the company can sustain a 15 growth rate while they are only able to grow at 98 annually This is why we forecasted a 100 asset turnover rate because we believe that with these rising prices and rising sales Patterson will acquire more assets turn them over and use them to generate more sales giving grounds for our higher than normal growth rate forecast Also the higher asset turnover rate will increase ROE and contribute to a larger SGR Once forecasting the sales growth we were able to predict the sales all the way through 2004 Next we took our gross profit margin and figured out what gross profit would be each year From that number we were able to find cost of good sold which is also a percentage of sales We then took the forecasting one step further and forecasted each segment of operations as a percentage of sales in order to see if the segments would also

- 23 -

proportionately grow Operating income was then forecasted based on our assumption that it was on average 13 of sales Finally we were able to arrive at net income using our forecasted net profit margin of 28 The forecasting of the income statement is necessary to do first because it allows everything else to fall in place Balance Sheet

With the income statement in place we are able to first derive our forecasted balance

sheet This first involves forecasting the total assets from 2004 to 2014 We accomplished this task by using our forecasted asset turnover ratio to find the missing variable of total assets By dividing the forecasted sales for each year by the asset turnover ratio one we were able to derive the total forecasted assets To get the shareholderrsquos equity part of the balance sheet we used our return on equity ratio which is net income divided by total shareholderrsquos equity By dividing the net income by the ROE we were able to derive the shareholderrsquos equity and then we took the difference between total assets and equity to forecast the total liabilities We then used our trends in what current assets on the average have been as a percentage of total assets to forecast the current assets portion of the balance sheet Once we derived our current assets we could put to use our current ratio to find the missing variable of current liabilities We also calculated other assets liabilities and equity portions as a percentage of total assets because they were also very consistent in the past and showed visible trends With the forecasted balance sheet in place we are one step closer to being able to perform valuations on the company

Statement of Cash Flows

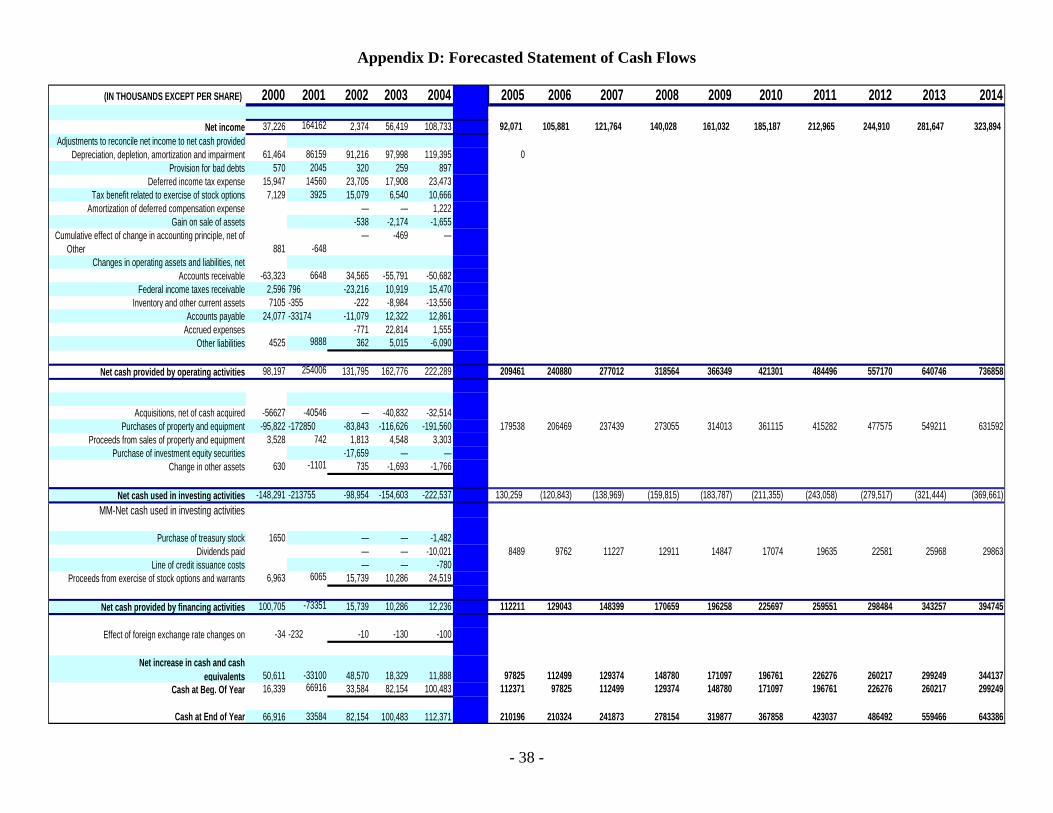

The statement of cash flows is the final forecasting element needed before valuations

We went about forecasting the cash flows almost in the same manner as the prior two financials We started with forecasting cash flows from operating activities by using our trend analysis We common sized the entire cash flow sheet into percentages of operating income and derived the cash flows from operations based on this trended percentage of operating income We proceeded to use the same procedure for the investing and financing cash flow sections and then we calculated the cash at the beginning of the year and at the end of the year in the same manner also One of the important cash flow numbers we calculated was the amount of dividends to be paid out in the future The company just adopted a policy of paying dividends in the second quarter of 2004 which turned out to be 922 of their net income Patterson also recently changed their dividend policy to pay out 4 cents per share instead of the two cents per share paid in 2004 One might wonder why we didnrsquot forecast an increase in the payout ratio if the actual dividend itself increased This is because the payout ratio depends on net income and if they increased the dividend to be paid out on each share then they must also be expecting an increase in net income This forward looking assumption strengthens our arguments on the expected growth rate of the company in sales and in ROE Therefore the dividends are expected to increase along with net income which leaves the ratio to stay somewhat steady and it may fluctuate a little bit However this is our intrinsic thought on what will happen in the future Now that the cash flow statement has been forecasted the foundation for the company valuation has been laid

- 24 -

Room for Errors

The forecasting assumptions made were all based off of our belief that sales will consistently grow at about 15 per year from here on out All other information was derived by our estimates of future ratios which were then used to compute the forecasted values This shows that historical trends of the ratios incorporate actual dollar amounts of information while the forecasts made off of other forecasts tend to be biased by the previous forecast This leaves a lot of room for error in calculations of cash flow net income sales and even projected dividends

PPAATTTTEERRSSOONN VVAALLUUAATTIIOONN

After forecasting Pattersonrsquos financial statements ten years into the future we now

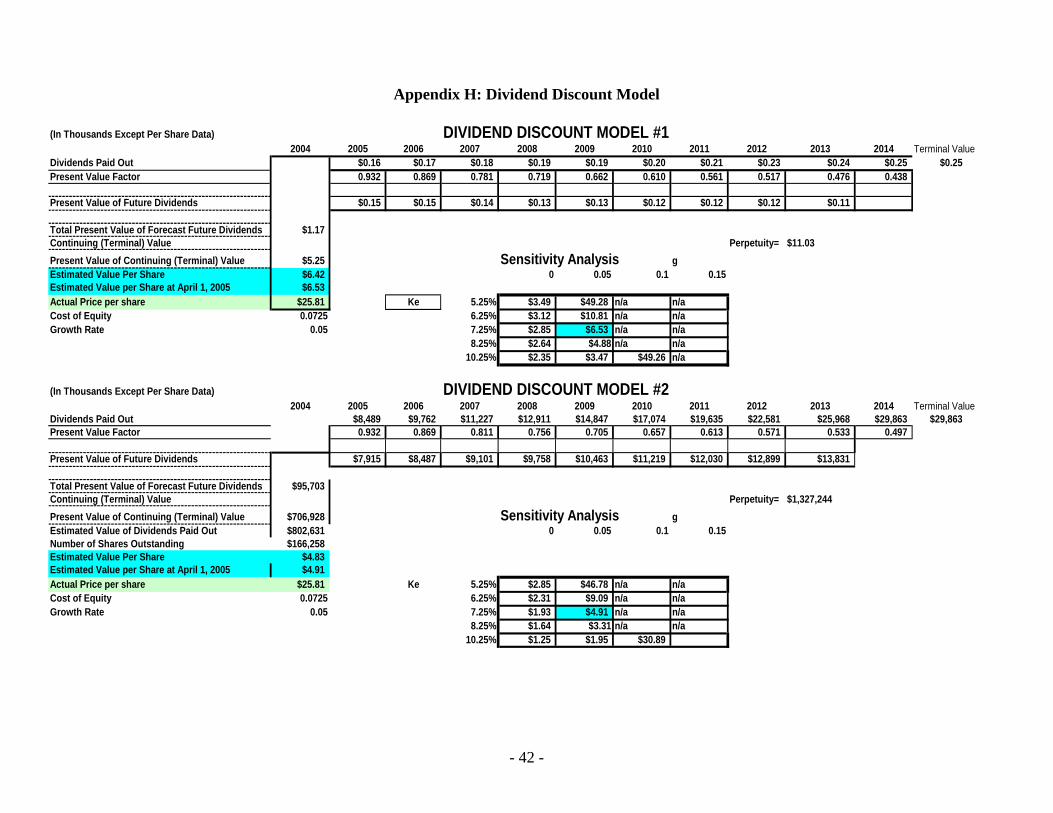

assume them to be correct and will put these numbers into various models and come up with an estimated share price Our forecasts are based on the future performance of the company and the information that will be of most importance in these valuations includes the following earnings growth rates dividend payments cash flows and the costs of capital These values will be discounted to present day dollars in order to obtain the share price There are five valuation models that we will use They include the following method of comparables discounted free cash flows discounted dividends residual income and abnormal earnings growth model These models will give us an estimated share price which we will compare to Pattersonrsquos actual market price on April 1 2005 The market price of the stock will be compared to our intrinsic valuations and we will make a judgment on whether or not we believe our estimated prices why there is room for flexibility what different costs of capital could have produced better or even worse results and if there is investment opportunity or not We will then be able to state whether the stock is under-valued over-valued or fairly-valued Some models will carry more weight than others because we feel that they more accurately describe the true financial position of Patterson For example Patterson has a newly created dividend policy that is not very strong or attractive but distributes dividends nonetheless Therefore it would seem illogical to heavily weight the results from a dividend model when the terminal value of those dividends are not significant to the company The oil and gas contract drilling industry has close to a zero percent payout ratio in dividends with Patterson being the only main competition that pays dividends Certain models will be more applicable to the oil and gas industry but it is still necessary to include all the valuations

Cost of Equity

Before we can use the models to estimate the share price we must first figure out what

discount rate we will use to discount the numbers back to 2004 To employ these methods we must estimate Pattersonrsquos cost of equity cost of debt and the companyrsquos beta These are important numbers to the financial infrastructure for the firm because they represent the opportunity costs forgone on capital and in the absence of debt Pattersonrsquos ratio of equity to liabilities is extremely high giving rise to a low debt structure and a very strong equity based structure After finding the cost of equity and the cost of debt we will then be able to compute the weighted average cost of capital The weighted average cost of capital is used in the discounted free cash flows model because that deals with cash flows to both debt and equity holders Other models like the dividend discount model the abnormal earnings growth model

- 25 -

and the residual income deal with the equity portion of the firm and are discounted using the cost of equity because it most significantly represents the return equity holders would demand A slight degree of difference in each of these costs of capital can significantly influence our estimated value of the equity portion of the firm

The first number that we wanted to estimate is the cost of equity (Ke) To get Pattersonrsquos estimated cost of equity we used the Capital Asset Pricing Model First we gathered information on the closing share prices of the firm at the end of each month for the past five three and two years We then calculated the return from each month to the next to get a macro look at the returns Then we needed to get an appropriate risk free rate Pattersonrsquos beta and a market risk premium To calculate the risk free rate we also looked at the rates of t-bills at the close of each month and then took an average over the past five years That gave us the monthly average of rates that are risk free and then we annualized them to get an annual rate Then we got a professionally estimated beta on Yahoo Finance for comparison of our calculated beta Their published beta was 1517 We then computed our own beta by running a regression analysis In this regression we used the market risk premium and Pattersonrsquos monthly returns The market risk premium was found by subtracting the risk free rate from the market return which has historically been at about 3 for the past five years We chose to use the market return as the return of the SampP 500 over five years and the risk free rate as the rate of a treasury bill We then calculated the slope of Pattersonrsquos return to the market risk premium to obtain a beta of 1504 and a R squared of 188 However we also calculated a three year and two year beta that produced a systematic risk a lot lower than that taken over the past five years These betas are 66 and 62 respectively We feel comfortable in using our five year beta because of the fact that it is so close to the professionally estimated beta given by other analysts Also it takes into account the effects on the market that 911 brought giving rise to volatility which describes our industry By using these rates and the beta we used the CAPM model to calculate the return for Patterson which was about 86 meaning that this is what equity holders demand as their return for their investment This is the first step in calculating the three costs of capital that ultimately give rise to our valuation models

Cost of Debt (Kd)

When we began to analyze the liabilities that Patterson has we found that their

accounting disclosure was very poor for a few reasons First of all they donrsquot classify their principal debts each in their own class but rather they stuff them all into a couple different categories all representing the same debt but just named differently for accounting purposes Furthermore there were no time horizons on the actual debt For example no length of time was shown on when their debt was due but we ultimately used one year or less due to the nature of their debt There is no long term debt for Patterson and their short term debt is very short probably no more than 30 days by way of their credit card facility and it is very cheap The main rate we used in the short term debt categories was LIBOR plus up to 1 for other fees and charges We decided to keep it at one percent due to them having a 15 charge on outstanding balances not yet paid The LIBOR rate we used was about 379 giving us a 479 rate to use on accrued revenue distributions and accrued expenses We then used about a 2 rate for their trade accounts payable section due to the nature of business These terms are usually to pay the full balance within thirty days and have an interest rate incorporated into the sale prior to business dealings like a zero coupon bond would This two percent was used as the average

- 26 -

interest rate on 30 day certificates of deposit As earlier mentioned we stated that Patterson has no long term debt but there is one exception and that is their obligations to the government in deferred tax liabilities that have been building up over time It is evident to us that these obligations will not likely be fulfilled at least not anytime soon if at all Therefore we decided to omit this obligation and treat it almost as an equity holding Finally we weighted all of the short term debts as a percentage of the total liabilities and then multiplied those weights by their corresponding rates The sum of these weighted averages became our cost of debt which is 376 This implies that the cost of debt these days especially for Patterson is very cheap and this could be due to their good nature of paying off debt or not even ever having very much to deal with By calculating this number we are able to move on to get our weighted average cost of capital

WACC

The weighted average cost of capital is exactly what its name suggests It is an average

of the cost of debt and the cost of equity based on their weights in the total value of the firm As noted the minimal liabilities of Patterson allows for a strong biased weight of the cost of equity since that is a major part of their capital structure When calculated WACC comes out to be 745 when using a 376 cost of debt (Kd) and a 86 cost of equity (Ke) This was different to our first assumption of a WACC which was driven by information off their financial statements stating that they discount their assets (oil reserves) at 10 to get their present day worth This struck us as a possible WACC due to assets being manageable by both debt and equity holders In the first valuation model we did involving the discounted free cash flows this number brought us very close to the actual market price as of April 1 2005 which was $2581 However we used that possible WACC to calculate our cost of debt and it turned out that the cost of debt would have been almost twice as much in this situation sitting at somewhere between 14 and 15 Therefore we had to re-strategize and come up with a better way of explaining our intrinsic values so we ruled out that 10 as being a possible WACC Now that we have all the costs of capital in place we are able to put them to use in the valuation models to estimate our intrinsic value of the firm

Method of Comparables

The method of comparables method is achieved by benchmarking Patterson against its competitors We chose the competitors that we feel most resemble the type of industry that Patterson competes in and competes directly with Patterson These competitors include Nabors Grey Wolf and Helmerich amp Payne After the competitors were selected several ratios were performed on each We used each companies earningsshare book valueshare dividendsshare and priceshare in order to compute a priceearnings ratio marketbook ratio and a dividendprice ratio After these numbers were figured we were then able to get an industry average for each ratio These numbers were computed for fiscal year ended 2004 and a one year forecast into the future The observed share prices for Patterson were then found by comparing the industry averages to Pattersonrsquos actual 2004 data and our one year forecasted prediction Also when computing industry averages any obvious outliers should be thrown out and not included in the average When computing the PE ratio for 2004 Grey Wolf and Helmerich amp Payne were viewed as outliers and Patterson was compared directly to industry leader Nabors

- 27 -

As you can see by the wide range of share prices that were obtained we do not feel the method of comparables is one of the more accurate measures to use when trying to value a particular company but seems to come close to our other estimated prices using other valuations such as the residual income and abnormal earnings growth models The method has its obvious downfalls First of all when finding the industry average for the dividendsprice ratio we were only able to use Helmerich amp Payne since they are the only competitor that has a policy that pays dividends to its shareholders The share price using the method of comparables and its components ranged from $600 to $3360 The price earnings growth was a little more difficult to compute because we were not sure what types of growth estimates to use We decided to use the estimates off of httpfinanceyahoocom on the estimated earnings growth from the end of December 2005 to December 2006 We took the growth in earnings from 2005 to 2006 to derive our growth rate for each of the competitors Helmerich amp Payne was obviously an outlier in the group so we decided to take an average PEG from Grey Wolf and Nabors By multiplying the average PEG by Pattersonrsquos expected growth rate that we forecasted of 15 and then multiplying that by the earnings per share we get our valuation based on the PEG which is $3360 As a rule of thumb any PEG above one estimates that the stock is generally over-valued and anything under one tends to say that the stock price is undervalued

Method of Comparables 2004 (Trailing)EPS BPS DPS PPS

Patterson UTI 065 796 006 1945Nabors 203 3936 NA 5129Grey Wolf 004 342 NA 527Helmerich amp Payne 009 2796 032 3404

PE PB DP PEG EPS GrowthNabors 2527 130 NA 195 1292Grey Wolf 13175 154 NA 494 2667Helmerich amp Payne 37822 122 001 114 3292Industry Average(excluding outliers) 2527 135 001 345Patterson UTI Estimated Price $1643 $1075 $600 $3360

1 Yr ForwardEPS PPS

Patterson UTI 055Nabors 291 6484Grey Wolf 035 755Helmerich amp Payne 169 4780

PENabors 2228Grey Wolf 2157Helmerich amp Payne 2828Industry Average(excluding outliers) 2405Patterson UTI Estimated Price $1323

Key PE(priceearnings) PB(pricebook) DP(dividendsprice)

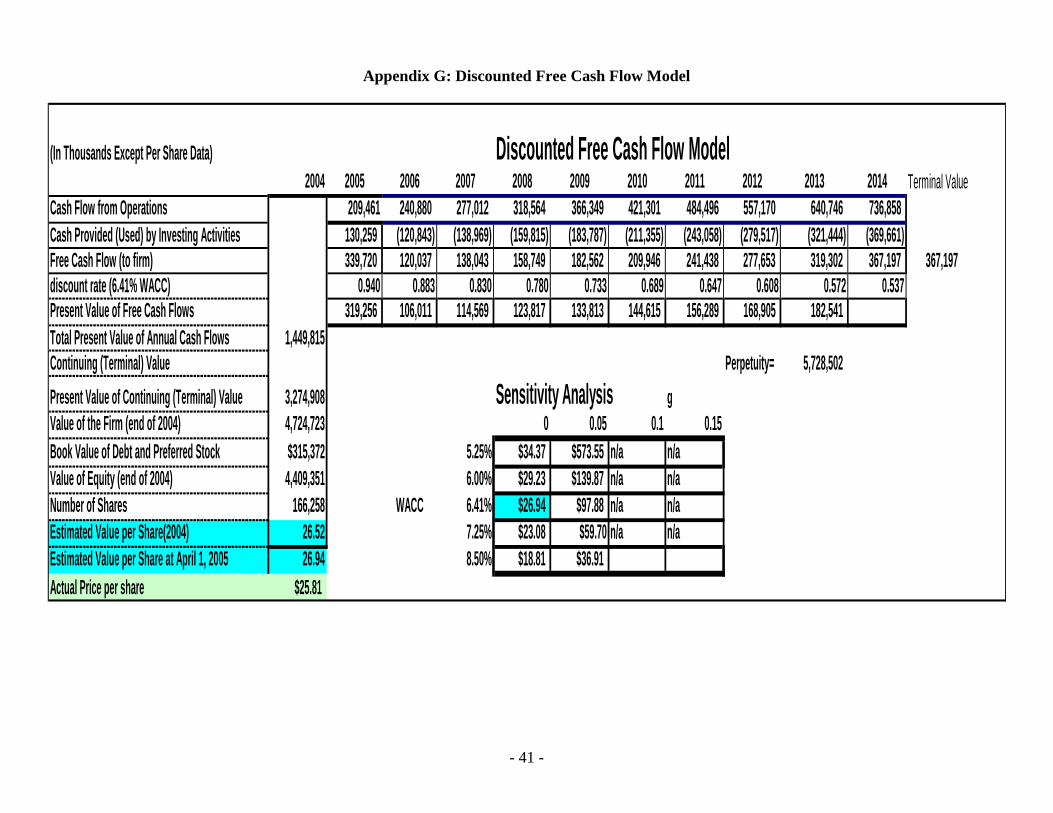

Discounted Free Cash Flows Model

The discounted free cash flows model was one of our favorite models to use because it used proxies that were actually significant to the firmrsquos business which is the inflows and outflows of cash We started off by using our forecasted amounts of cash flows from operating and investing activities in order to obtain the free cash flows to the firm which are ultimately used After calculating the free cash flows we discounted them to the end of 2004 to get their present values in todayrsquos dollars The rate we used to discount these dollars was a WACC of 641 This is different from the WACC that we originally calculated earlier with an 86 cost of equity and it gave us a weighted average cost of capital of 745 The reason for this change

- 28 -

was that the 641 was an implied rate that gave us the results we were looking for This rate also came into being because we used an implied cost of equity of 725 in other models because it also yielded better results for our valuation methods This new implied cost of equity obviously changed the previous WACC which is why we used 641 instead of 745 Also we feel that using the new cost of equity is completely rational because our R squared or explanation ratio in computing the beta was very small which says that not very much of the cost of equity is explained by the firmrsquos returns over the past five years as compared to the market risk premium If the explanation had been much higher then we would have little room to argue that a different cost of equity could be used but since there is little explanation we feel that our implied cost of equity is the proper number to use based on our observed share prices Once each yearrsquos free cash flows were discounted to present day we added them all up from the forecasted 10 years Then we assumed that the cash flows would ultimately level off for the infinite life of the corporation and stay at a steady $367197000 for each continuing year after 2014 We then calculated the present value of this perpetuity assuming a zero percent growth rate Our reasons for using a zero percent growth rate in this model were due to the fact that cash flows do not increase significantly over time but instead only increase or decrease with changes in sales income etc Also the zero percent growth rate very closely describes the market value of the firm as stated by the public markets This price of $2694 is captured by combining the present value of forecasted cash flows and the present value of the terminal value from year 2014 on out We then divided this total by the number of shares outstanding at the end of 2004 to get an end of 2004 intrinsic value Then we used the WACC to figure the first quarter forward price so that we could value the firm as of April 1 2005 This so far is our strongest model and suggests that the cash flows of the firm accurately describe its value

Sensitivity Analysis g

0 005 01 015525 $3437 $57355 na na600 $2923 $13987 na na

WACC 641 $2694 $9788 na na725 $2308 $5970 na na850 $1881 $3691