Part 1 - Cabrillo College - Breakthroughs Happen Herecabrillo.edu/~mbooth/acct151a/Price 14th...

56

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth

Transcript of Part 1 - Cabrillo College - Breakthroughs Happen Herecabrillo.edu/~mbooth/acct151a/Price 14th...

Slide 1

Week 5, Chap 4

Part 1

The General Journal and

the General Ledger

Instructor: Michael Booth

Slide 2

The General Journal and

the General Ledger

The General Journal

Section Objectives

1. Record transactions in the

general journal.

2. Prepare compound journal

entries.

McGraw-Hill © 2007 The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 3 explained T accounts and the trial balance, and their usefulness in the preparation of financial statements. Chapter 4 introduces accounting journals, the general ledger, and shows how to use both. In the real world, transactions are not recorded using the accounting equation, nor are they recorded using T-accounts. Instead, businesses use a Journal to record business transactions. The first objective of this chapter introduces the general journal.

Slide 3

The accounting cycle is a series of steps

performed during each accounting

period to classify, record, and

summarize data for a business and to

produce needed financial information.

ANSWER:

QUESTION:

What is the accounting cycle?

This chapter introduces the steps in the accounting cycle, a series of steps performed each accounting period.

Slide 4

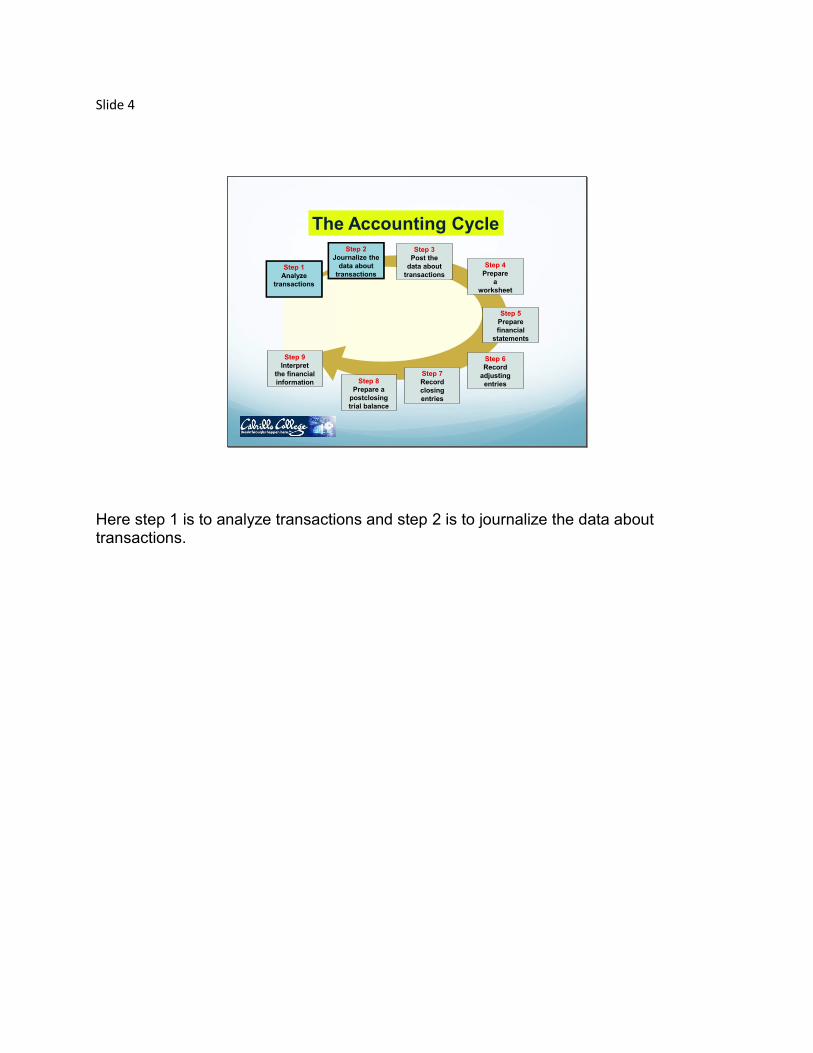

The Accounting Cycle

Step 1

Analyze

transactions

Step 2

Journalize the

data about

transactions

Step 7

Record

closing

entries

Step 3

Post the

data about

transactions

Step 4

Prepare

a

worksheet

Step 5

Prepare

financial

statements

Step 6

Record

adjusting

entriesStep 8

Prepare a

postclosing

trial balance

Step 9

Interpret

the financial

information

Step 1

Analyze

transactions

Step 2

Journalize the

data about

transactions

Here step 1 is to analyze transactions and step 2 is to journalize the data about transactions.

Slide 5

Journals

Slide 6

A journal is a record of original entry.

ANSWER:

QUESTION:

What is a journal?

Let’s begin with the business’s journal. . .A record of the original entry

Slide 7

A journal is a diary of business activities.

There are different types of journals.

Transactions are entered in the journal in

chronological order.

Journal

Just like in school when you kept a “diary” or “journal” of your activities, a business journal does the same thing.

Slide 8

Chronological order is the order in

which events occur.

ANSWER:

QUESTION:

What is chronological order?

The journal keeps a record of the business’s financial events in the order that they occurred.

Slide 9

The General Journal

Slide 10

Record transactions in the

general journal.

Our first objective is to learn how to record financial transactions in the general journal.

Slide 11

A general journal is a financial record for

entering all types of business

transactions.

ANSWER:

QUESTION:

What is a general journal?

The journal is the book of original entry where we first record business transactions.

Slide 12

Journalizing is the process of recording

transactions in a journal.

ANSWER:

QUESTION:

What is journalizing?

Journalizing, the verb, means to “record” transactions in the journal.

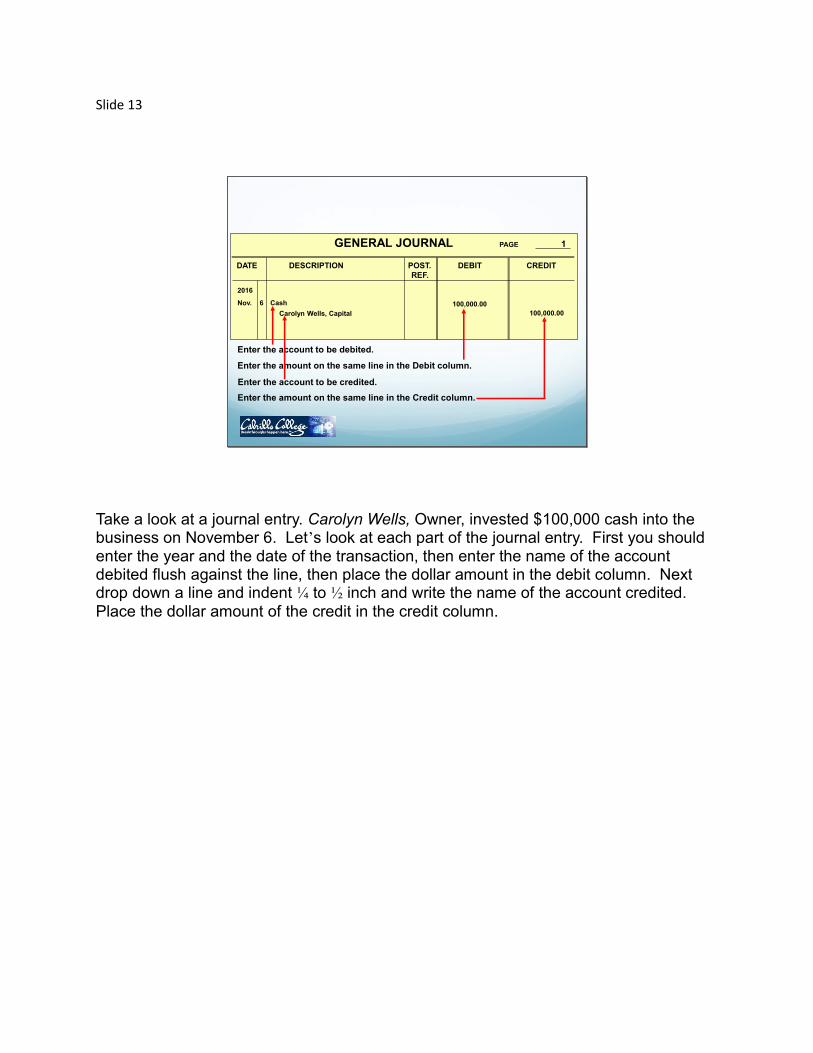

Slide 13

Enter the account to be debited.

GENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

2016

Nov. 6

Enter the account to be credited.

Enter the amount on the same line in the Debit column.

Enter the amount on the same line in the Credit column.

Cash

Carolyn Wells, Capital

100,000.00

100,000.00

Take a look at a journal entry. Carolyn Wells, Owner, invested $100,000 cash into the business on November 6. Let’s look at each part of the journal entry. First you should enter the year and the date of the transaction, then enter the name of the account debited flush against the line, then place the dollar amount in the debit column. Next drop down a line and indent ¼ to ½ inch and write the name of the account credited. Place the dollar amount of the credit in the credit column.

Slide 14

GENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

2016

Nov. 6 Cash 100,000.00

Carolyn Wells, Capital 100,000.00

Then enter a complete but concise description of the transaction.

Investment by owner

Whenever possible, the journal entry should refer to the source of the

information.

Document numbers are part of the audit trail.

, Memo 01

Once the transaction has been journalized, we need to indent a little and add an explanation of the event.

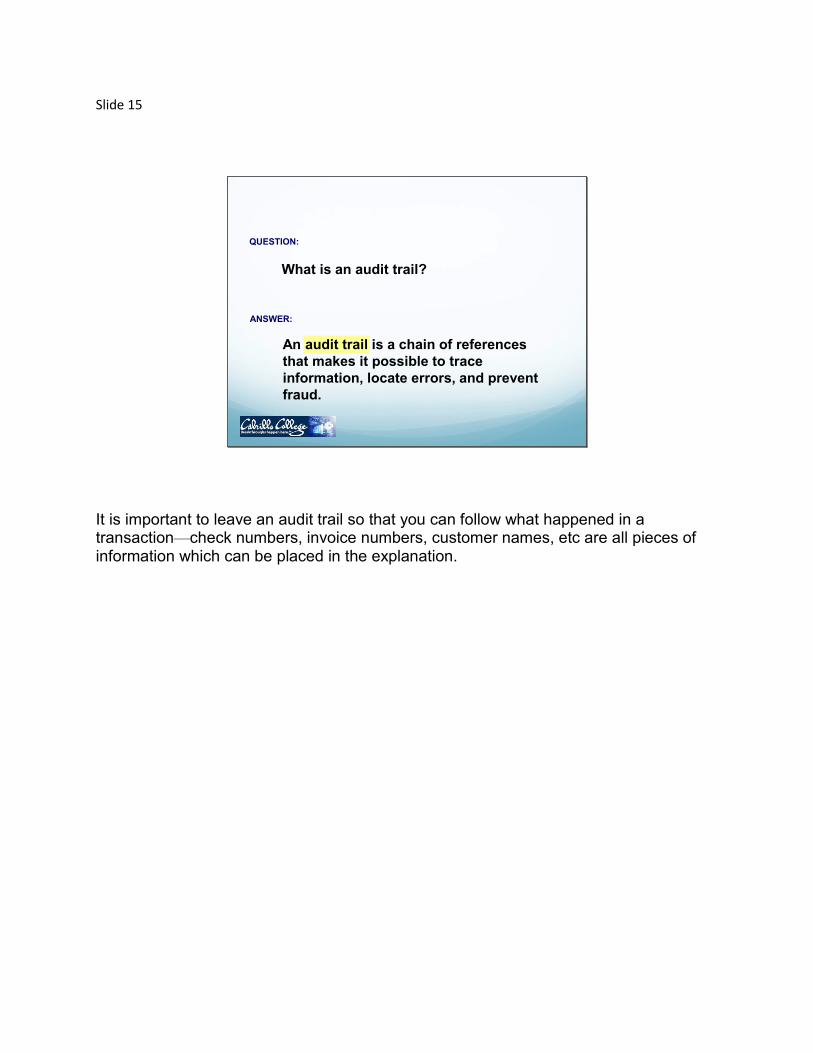

Slide 15

An audit trail is a chain of references

that makes it possible to trace

information, locate errors, and prevent

fraud.

ANSWER:

QUESTION:

What is an audit trail?

It is important to leave an audit trail so that you can follow what happened in a transaction—check numbers, invoice numbers, customer names, etc are all pieces of information which can be placed in the explanation.

Slide 16

Recording Month’s (November)Transactions in the General Journal

Slide 17

1. Analyze the financial event.

Recording a

Business Transaction

2. Apply the rules of debit and credit.

3. Make the entry in T-account form.

4. Record the complete entry in general journal form.

Identify the accounts affected.

Classify the accounts affected.

Determine the amount of increase or decrease for each account

affected.

a. Which account is debited? For what amount?

b. Which account is credited? For what amount?

Here are the steps to begin a journal entry. It is critical at this point that you have memorized and can apply the analysis process.

Slide 18

Business Transaction

1. Analyze the financial event.

On November 6 Carolyn Wells withdrew $100,000 from

personal savings and deposited it in a new business

checking account for Wells’ Consulting Services.

Let’s journalize this initial investment by the owner in the general journal.

Slide 19

Cash Investment by Owner

Which account is debited?

For what amount?

Which account is credited?

For what amount?

2. Apply the rules of debit and credit.

Do you remember using T accounts? We need to Debit Cash for $90,000 and Credit Carolyn Wells, Capital for the same amount.

Slide 20

Cash

100,000

Carolyn Wells, Capital

100,000

Cash Investment by Owner

3. Make the entry in T-account form.

This is what it looks like in T-account form.

Slide 21

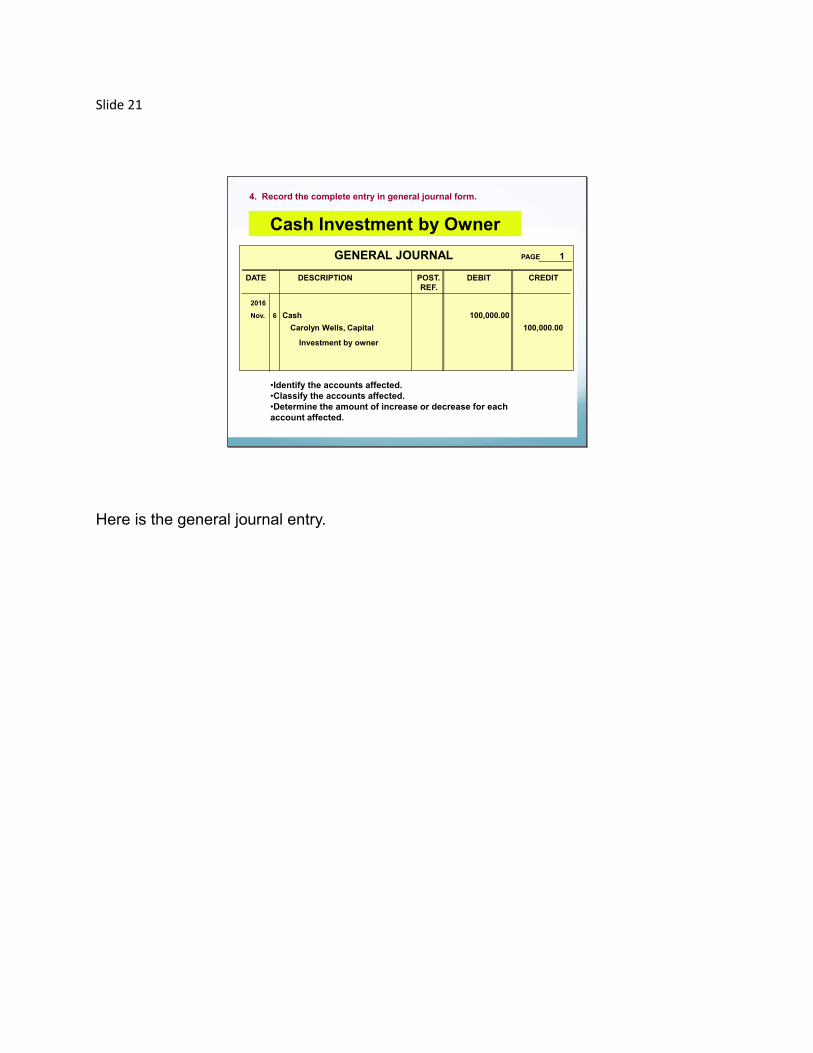

Cash Investment by Owner

•Identify the accounts affected.

•Classify the accounts affected.

•Determine the amount of increase or decrease for each

account affected.

4. Record the complete entry in general journal form.

GENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

2016

Nov. 6 Cash 100,000.00

Carolyn Wells, Capital 100,000.00

Investment by owner

Here is the general journal entry.

Slide 22

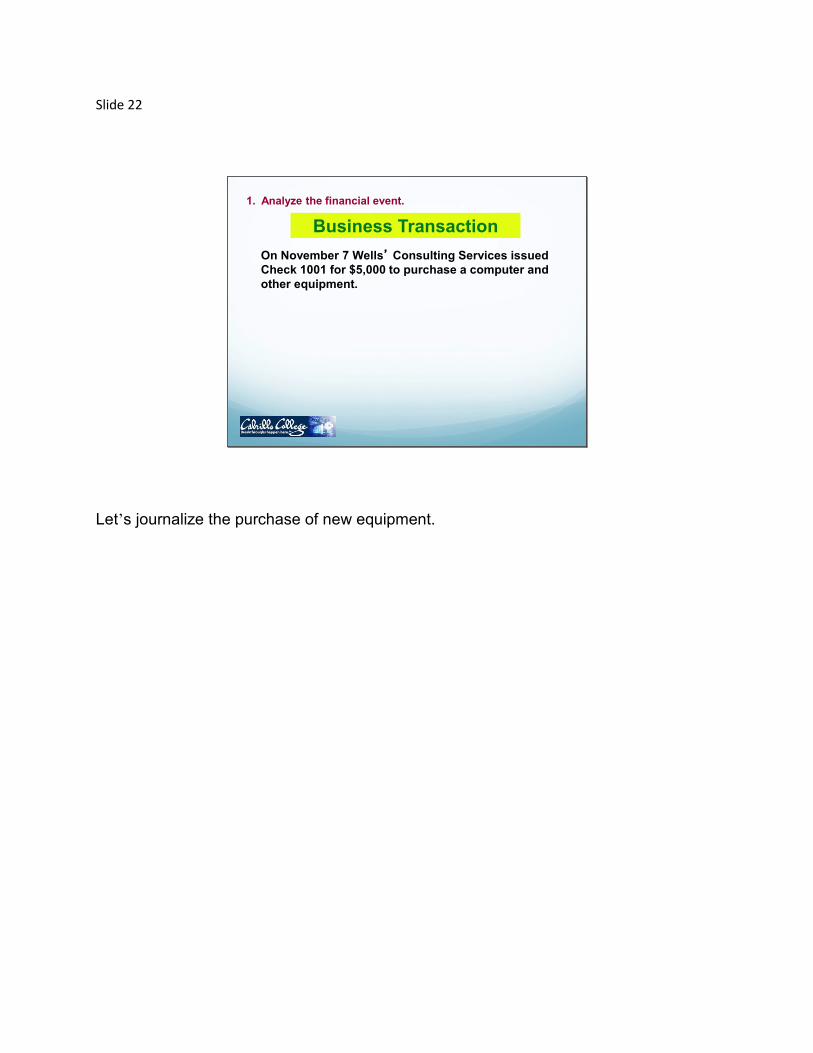

Business Transaction

1. Analyze the financial event.

On November 7 Wells’ Consulting Services issued

Check 1001 for $5,000 to purchase a computer and

other equipment.

Let’s journalize the purchase of new equipment.

Slide 23

Equipment

5,000

Cash

5,000

Cash Purchase of Equipment

3. Make the entry in T-account form.

Here is what the transaction looks like in T-account form.

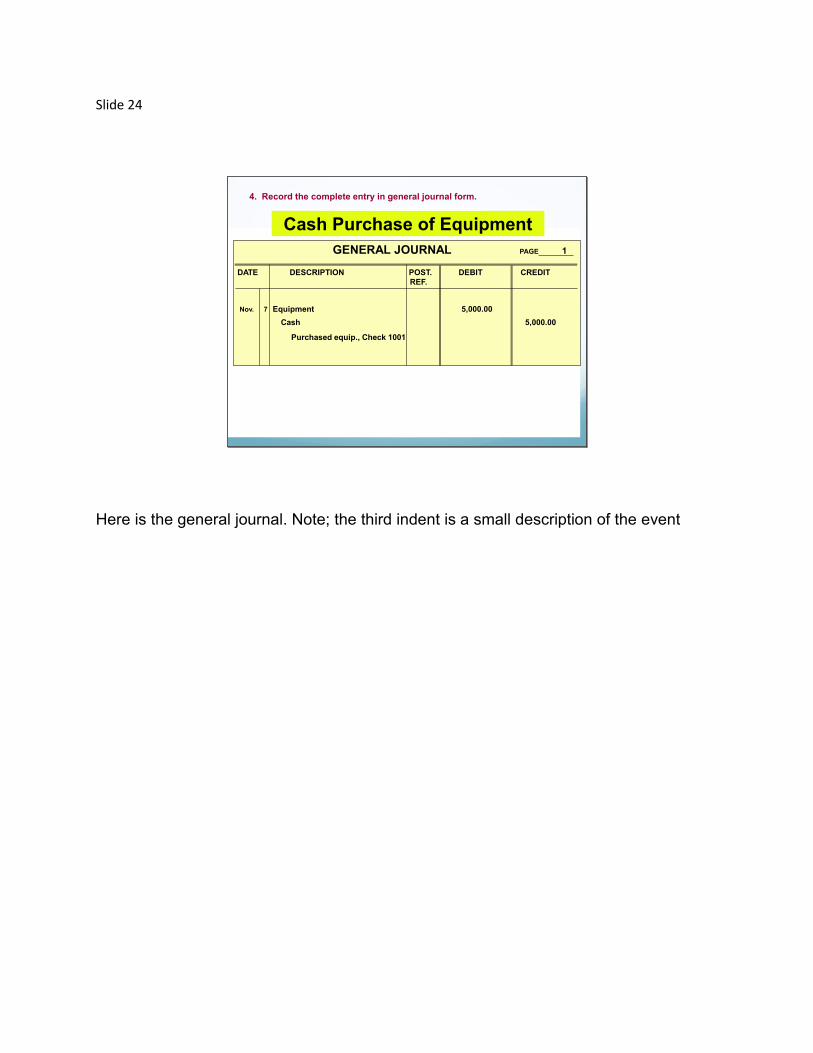

Slide 24

GENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Nov. 7 Equipment 5,000.00

Cash 5,000.00

Purchased equip., Check 1001

Cash Purchase of Equipment

4. Record the complete entry in general journal form.

Here is the general journal. Note; the third indent is a small description of the event

Slide 25

Business Transaction

1. Analyze the financial event.

On November 10, Wells’ Consulting Services purchased

office equipment on account for $6,000.

Our next transaction is the purchase of equipment on account.

Slide 26

Credit Purchase of Equipment

Equipment

6,000

Accounts Payable

6,000

3. Make the entry in T-account form.

Here is the transaction in T-account form.

Slide 27

Credit Purchase of EquipmentGENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Nov. 10 Equipment 6,000.00

Accounts Payable 6,000.00

Purchased equipment on

account from Office Plus,

Inv. 2223, due in 60 daysAll required information

should be included

in the explanation.

4. Record the complete entry in general journal form.

Here is the journal entry. Remember to include all important information in the explanation, the third indent after the credit entry. This improves the audit trail.

Slide 28

Business Transaction

Which account is debited? Which account is credited?

For what amount? For what amount?

2. Apply the rules of debit and credit.

1. Analyze the financial event.

On November 28, Wells’ Consulting Services

purchased supplies for $1,500, Check 1002.

Next, we purchased supplies for $1,500 cash, so we need to debit Supplies for $1,500 and credit Cash for the same amount.

Slide 29

Cash Purchase of Supplies

Supplies

1,500

Cash

1,500

3. Make the entry in T-account form.

Here is the transaction in T-account form.

Slide 30

GENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Nov. 28 Supplies 1,500.00

Cash 1,500.00

Purchased supplies, Ck. 1002

Cash Purchase of Supplies

4. Record the complete entry in general journal form.

Here is the general journal entry for the transaction, once again see the third indent, the note with the check #.

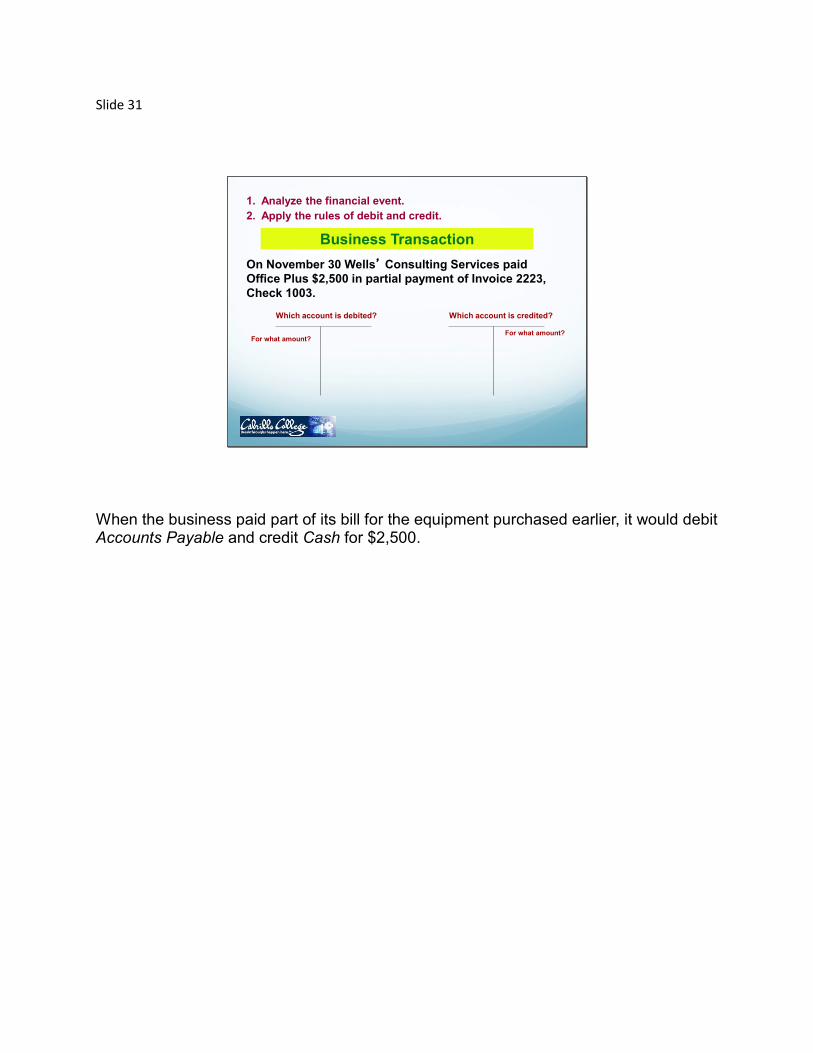

Slide 31

Business Transaction

Which account is debited?

For what amount?

Which account is credited?

For what amount?

1. Analyze the financial event.

2. Apply the rules of debit and credit.

On November 30 Wells’ Consulting Services paid

Office Plus $2,500 in partial payment of Invoice 2223,

Check 1003.

When the business paid part of its bill for the equipment purchased earlier, it would debit Accounts Payable and credit Cash for $2,500.

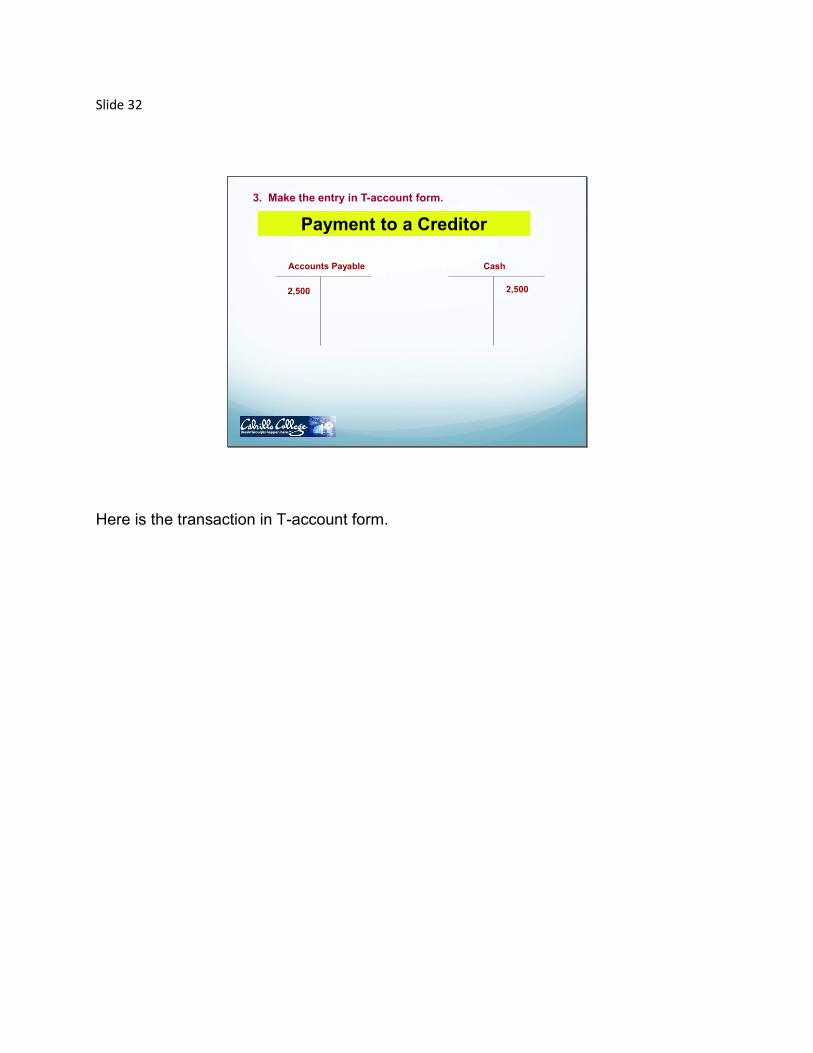

Slide 32

Payment to a Creditor

Accounts Payable

2,500

Cash

2,500

3. Make the entry in T-account form.

Here is the transaction in T-account form.

Slide 33

GENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Nov. 30 Accounts Payable 2,500.00

Cash 2,500.00

Paid on account, Office Plus,

Invoice 2223, Check 1003

Payment to a Creditor

4. Record the complete entry in general journal form.

Remember, in the general journal, always enter debits before credits, followed by the note with the summary information for the business transaction.

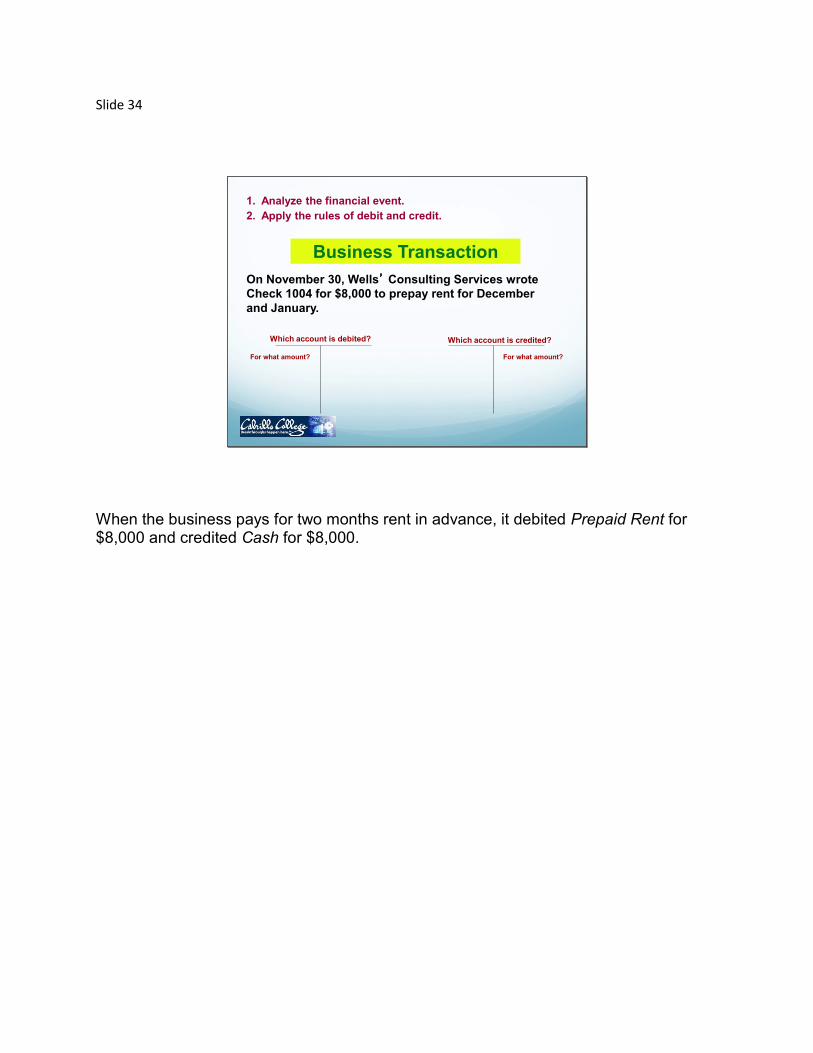

Slide 34

Which account is debited?

For what amount?

Which account is credited?

For what amount?

Business Transaction

1. Analyze the financial event.

2. Apply the rules of debit and credit.

On November 30, Wells’ Consulting Services wrote

Check 1004 for $8,000 to prepay rent for December

and January.

When the business pays for two months rent in advance, it debited Prepaid Rent for $8,000 and credited Cash for $8,000.

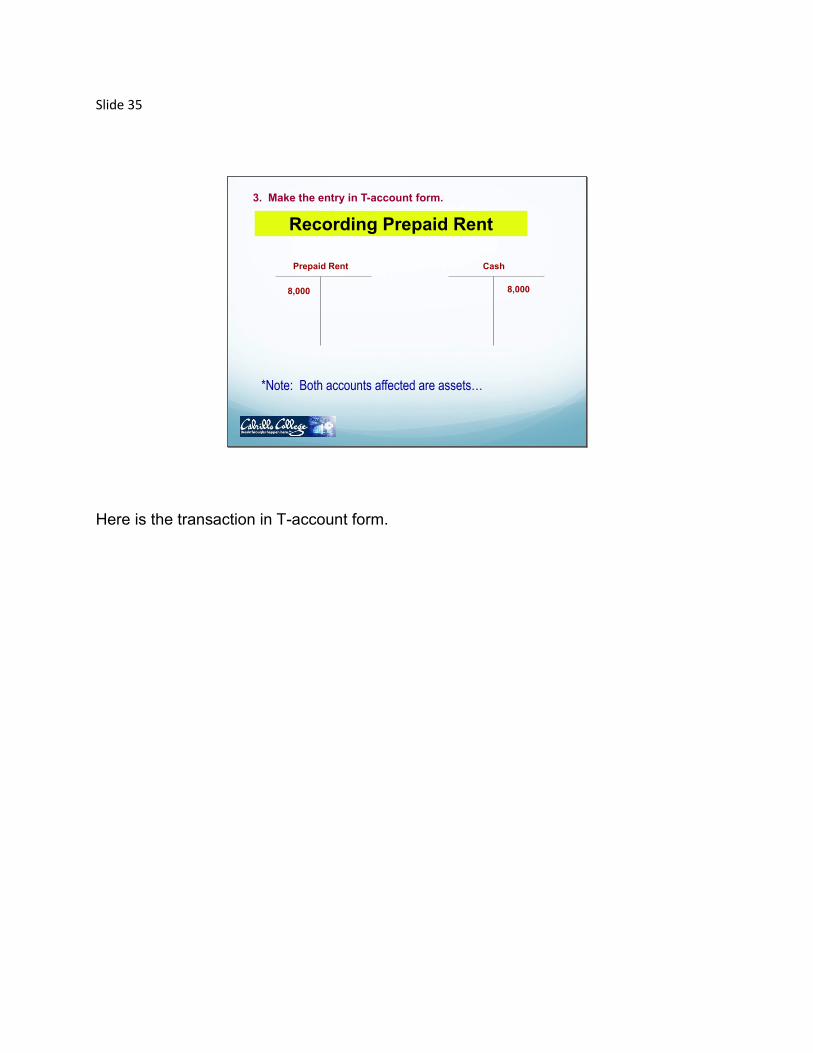

Slide 35

Recording Prepaid Rent

Prepaid Rent

8,000

Cash

8,000

*Note: Both accounts affected are assets…

3. Make the entry in T-account form.

Here is the transaction in T-account form.

Slide 36

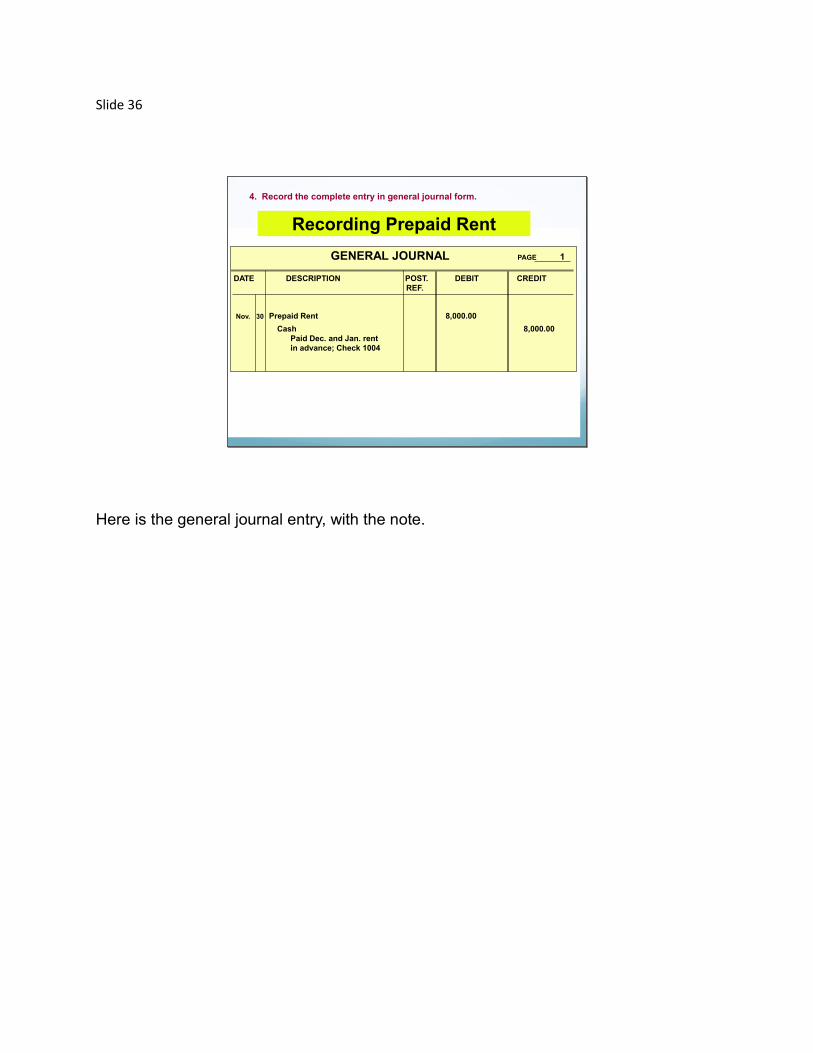

GENERAL JOURNAL PAGE 1

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Nov. 30 Prepaid Rent 8,000.00

Cash 8,000.00

Paid Dec. and Jan. rent

in advance; Check 1004

Recording Prepaid Rent

4. Record the complete entry in general journal form.

Here is the general journal entry, with the note.

Slide 37

Recording Month’s (December)Transactions in the General Journal

Slide 38

Which account is debited?

For what amount?

Which account is credited?

For what amount?

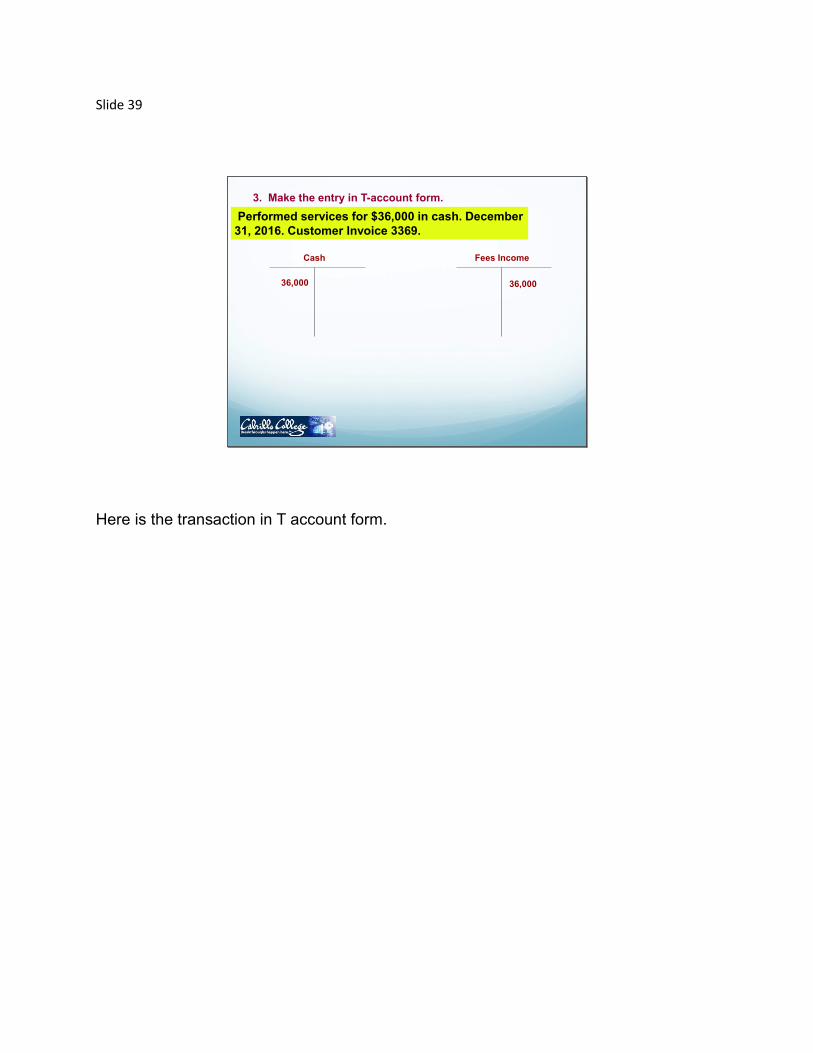

Performed services for $36,000 in cash. December

31, 2016. Customer Invoice 3369.

1. Analyze the financial event.

2. Apply the rules of debit and credit.

When the business performs consulting services and gets paid immediately, Well’s Consulting will debit Cash for $36,000 and credit Fees Income for the same amount.

Slide 39

Cash

36,000

Fees Income

36,000

3. Make the entry in T-account form.

Performed services for $36,000 in cash. December

31, 2016. Customer Invoice 3369.

Here is the transaction in T account form.

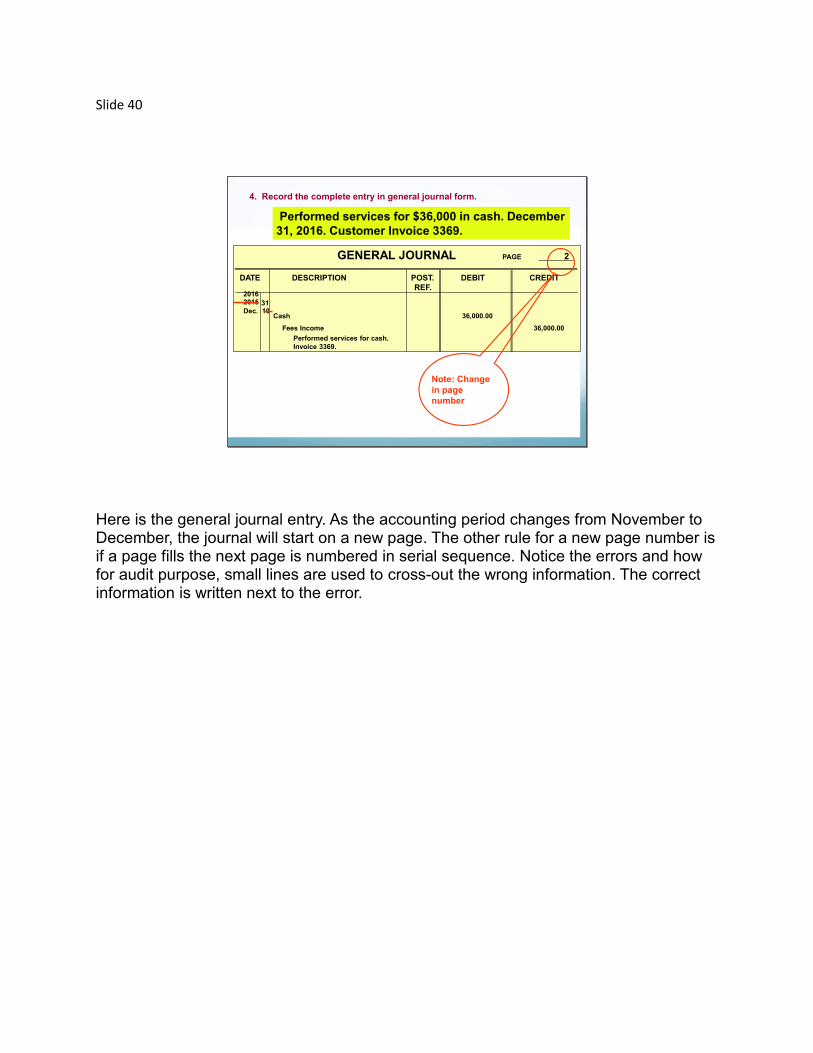

Slide 40

GENERAL JOURNAL PAGE 2

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

2015

Dec. 10Cash 36,000.00

Performed services for cash.

Invoice 3369.

Fees Income 36,000.00

4. Record the complete entry in general journal form.

Note: Change

in page

number

2016

31

Performed services for $36,000 in cash. December

31, 2016. Customer Invoice 3369.

Here is the general journal entry. As the accounting period changes from November to December, the journal will start on a new page. The other rule for a new page number is if a page fills the next page is numbered in serial sequence. Notice the errors and how for audit purpose, small lines are used to cross-out the wrong information. The correct information is written next to the error.

Slide 41

Performed services for $11,000 on credit.

December 31, 2016. Customer Invoice 3370.

Which account is debited?

For what amount?

Which account is credited?

For what amount?

1. Analyze the financial event.

2. Apply the rules of debit and credit.

When the firm performs services for credit clients, it will debit Accounts Receivable and credit Fees Income for $11,000.

Slide 42

Accounts Receivable

11,000

Fees Income

11,000

Record the revenue

as earned even if

you haven’t

received the cash.

3. Make the entry in T-account form.

Performed services for $11,000 on credit.

December 31, 2016. Customer Invoice 3370.

Remember to record the revenue even if you haven’t gotten paid because you have EARNED the money. The three elements required for revenue recognition: 1. Known Price 2. Transfer of title of good or Acceptance by customer of service 3. High probability of payment; Cash or Accounts Receivable

Slide 43

GENERAL JOURNAL PAGE 2

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Accounts Receivable 11,000.00

Fees Income 11,000.00

Performed services on credit.

Invoice 3370

4. Record the complete entry in general journal form.

Performed services for $11,000 on credit.

December 31, 2016. Customer Invoice 3370.

Here is the general journal entry on the 31st. Notice the invoice number in the note

Slide 44

Received $6,000 in cash from credit clients on their accounts, December 31, 2016.

Which account is debited?

For what amount?

Which account is credited?

For what amount?

1. Analyze the financial event.

2. Apply the rules of debit and credit.

When the firm collects $6,000 from credit customers, it needs to debit Cash and credit Accounts Receivable.

Slide 45

GENERAL JOURNAL PAGE 2

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Cash 6,000.00

Accounts Receivable 6,000.00

Received cash from credit

clients on account

4. Record the complete entry in general journal form.

Received $6,000 in cash from credit clients on their accounts, December 31, 2016.

Here is the general journal entry. What is missing? The Note should have the invoice number for the original sale

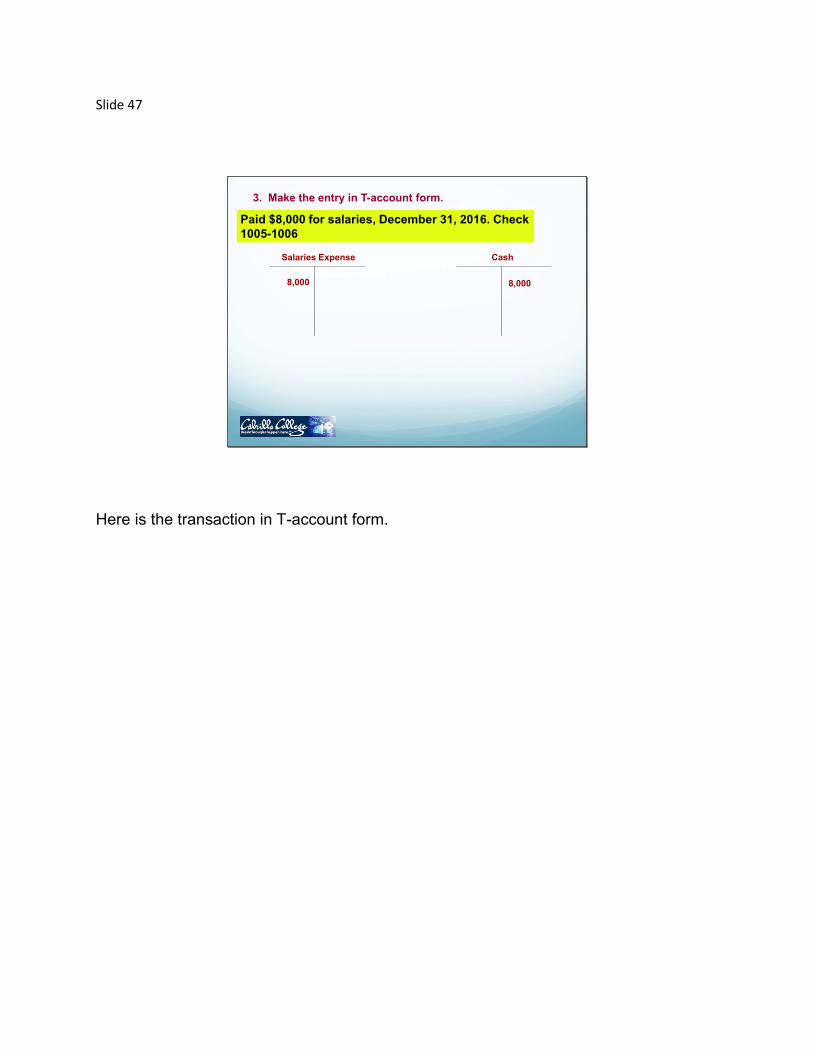

Slide 46

Paid $8,000 for salaries, December 31, 2016.

Checks 1005-1006

Which account is debited?

For what amount?

Which account is credited?

For what amount?

1. Analyze the financial event.

2. Apply the rules of debit and credit.

When the business pays $8,000 salaries expense to its employees, they would debit Salaries Expense for $8,000 and credit Cash for the same amount.

Slide 47

Salaries Expense

8,000

Cash

8,000

3. Make the entry in T-account form.

Paid $8,000 for salaries, December 31, 2016. Check

1005-1006

Here is the transaction in T-account form.

Slide 48

GENERAL JOURNAL PAGE 2

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Salaries Expense 8,000.00

Cash 8,000.00

Paid monthly salaries to

employees, Check 1005-1006

4. Record the complete entry in general journal form.

Paid $8,000 for salaries, December 31, 2016.

Checks 1005-1006

And, here is the general journal entry. Notice the sequence of checks used to pay the employees

Slide 49

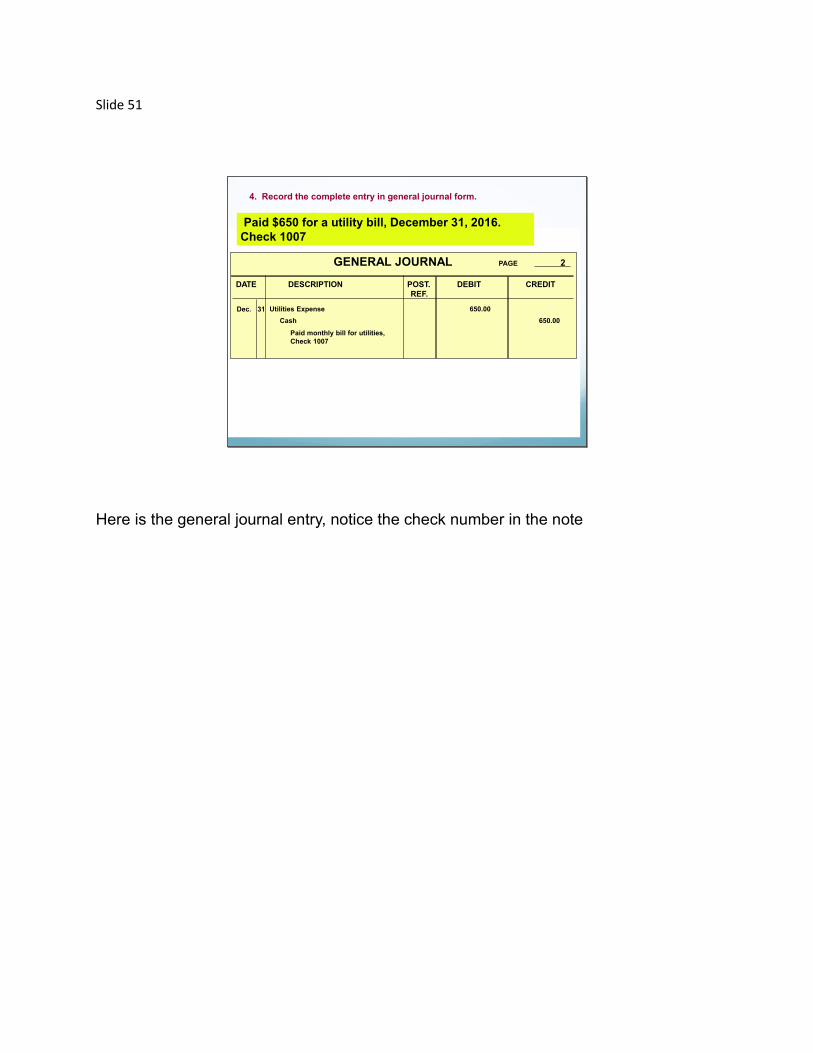

Paid $650 for a utility bill.

Which account is debited?

For what amount?

Which account is credited?

For what amount?

1. Analyze the financial event.

2. Apply the rules of debit and credit.

When the business pays a utility bill of $650, it will debit Utilities Expense and credit Cash for the $650.

Slide 50

Paid $650 for a utility bill, December 31, 2016.

Check 1007

Utilities Expense

650

Cash

650

3. Make the entry in T-account form.

Here is the transaction in T account form.

Slide 51

GENERAL JOURNAL PAGE 2

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Utilities Expense 650.00

Cash 650.00

Paid monthly bill for utilities,

Check 1007

4. Record the complete entry in general journal form.

Paid $650 for a utility bill, December 31, 2016.

Check 1007

Here is the general journal entry, notice the check number in the note

Slide 52

The owner withdrew $5,000 for personal expenses,

December 31, 2016, Check 1008.

Which account is debited?

For what amount?

Which account is credited?

For what amount?

1. Analyze the financial event.

2. Apply the rules of debit and credit.

When the owner withdraws $5,000 for personal use, the accountant will debit the Carolyn Wells, Drawing account and credit the Cash account for the $5,000 withdrawal.

Slide 53

Carolyn Wells, Drawing

5,000

Cash

5,000

3. Make the entry in T-account form.

The owner withdrew $5,000 for personal expenses,

December 31, 2016, Check 1008.

In T account form, this is what the transaction looks like.

Slide 54

GENERAL JOURNAL PAGE 2

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Carolyn Wells, Drawing 5,000.00

Cash 5,000.00

Owner withdrew cash for

personal expenses,

Check 1008

4. Record the complete entry in general journal form.

The owner withdrew $5,000 for personal expenses,

December 31, 2016, Check 1008.

Here is the general journal entry on the 31st, including the check # for the cash event

Slide 55

Received $6,000 in cash from credit clients on their accounts, December 31, 2016.

Which account is debited?

For what amount?

Which account is credited?

For what amount?

1. Analyze the financial event.

2. Apply the rules of debit and credit.

When the firm collects $6,000 from credit customers, it needs to debit Cash and credit Accounts Receivable.

Slide 56

GENERAL JOURNAL PAGE 2

DATE DESCRIPTION POST. DEBIT CREDIT

REF.

Dec. 31 Cash 6,000.00

Accounts Receivable 6,000.00

Received cash from credit

clients on account

3. Record the complete entry in general journal form.

Received $6,000 in cash from credit clients on their accounts, December 31, 2016.

Here is the general journal entry, once again should have the invoice number of the original sale included in the note.