Paper Review by: Niv Nayman Technion- Israel Institute of Technology July 2015 By Darrell Duffie and...

41

Paper Review by: Niv Nayman Technion- Israel Institute of Technology July 2015 Efficient Monte Carlo Simulation of Security Prices By Darrell Duffie and Peter Glynn, Stanford University, 1995

-

Upload

ronald-hart -

Category

Documents

-

view

215 -

download

2

Transcript of Paper Review by: Niv Nayman Technion- Israel Institute of Technology July 2015 By Darrell Duffie and...

Paper Review by:

Niv Nayman

Technion- Israel Institute of Technology

July 2015

Efficient Monte Carlo Simulation of

Security Prices By Darrell Duffie and Peter Glynn, Stanford

University, 1995

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

Definition. We say that a random process, , is a

Brownian motion with parameters (µ,σ) if

1. For 0 < t1 < t2 < …< tn-1 < tn

are mutually independent.

2. For s>0,

3. Xt is a continuous function of t.

We say that Xt is a B (µ,σ) Brownian motion with drift µ and volatility σ

Brownian Motion : 0tX t

2 1 3 2 1

, , ... ,n nt t t t t tX X X X X X

2,s t tX X N s s

Remark. Bachelier (1900) – Modeling in Finance

Einstein (1905) – Modeling in Physics

Wiener (1920’s) – Mathematical formulation

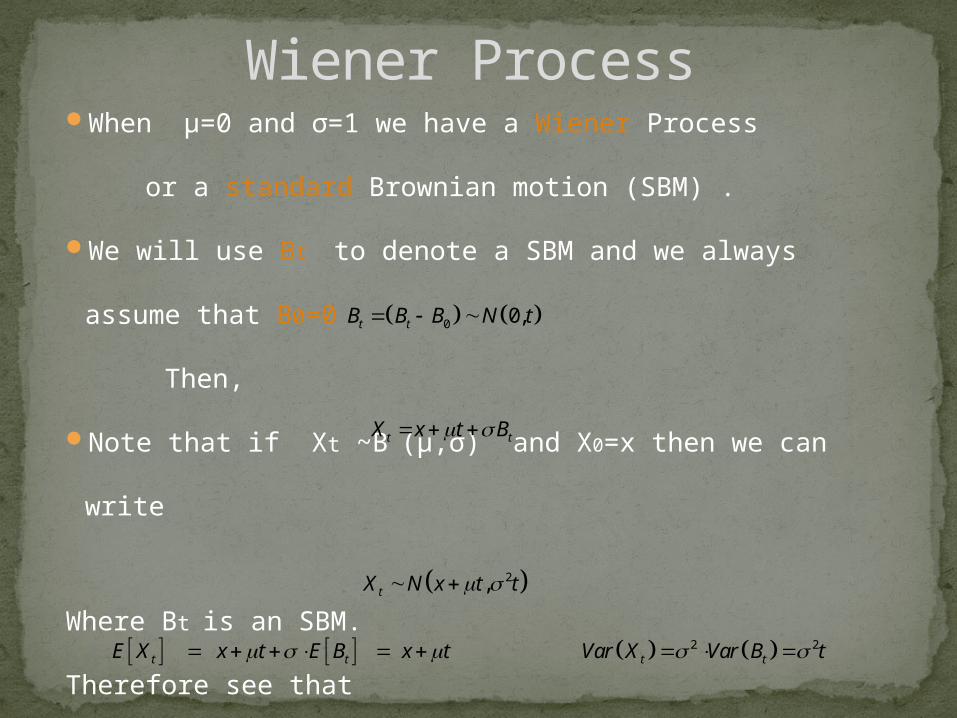

When µ=0 and σ=1 we have a Wiener Process

or a standard Brownian motion (SBM) .

We will use Bt to denote a SBM and we always assume that B0=0

Then,

Note that if Xt ~B (µ,σ) and X0=x then we can write

Where Bt is an SBM.

Therefore see that

Since,

Wiener Process

t tX x t B

2,tX N x t t

t tE X x t E B x t

0 0,t tB B B N t

2 2t tVar X Var B t

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

Definition. A partition of an interval [0,T] is a finite sequence of numbers πT of the form

Definition. The norm or mesh of a partition πT is the length of the longest of it’s subintervals, that is

Recall the Riemann integral of a real function µ

And the Riemann-Stieltjes integral of a real function µ w.r.t a real function gt=g(t)

Then the Itō integral of a random process σ w.r.t a SBM Bt

It can be shown that this limit converges in probability.

Itō Integral

1 2 1 1 2 1: , , , , 0 [( ) ] |T n n n nt t t t t t t t T

11,...,n

: maxT i ii

h t t

1 1 10 01

, lim ,nt

s i i i ih

i

s X ds t X t t

11 10 0

1

, lim ,i i

nt

s s i i t thi

s X dg t X g g

11 10 0

1

, lim ,i i

nt

s s i i t thi

s X dB t X B B

A stochastic differential equation (SDE) is of the form

Which is a short-hand of the integral equation

Where

Bt is a Wiener Process (SBM).

is a Riemann integral.

is an Itō integral.

Stochastic Differential Equation

0

,t

ss X ds

0

,t

s ss X dB

, ,t t t tdX t X dt t X dB

0 0 0, ,

t t

t s s sX X s X ds s X dB

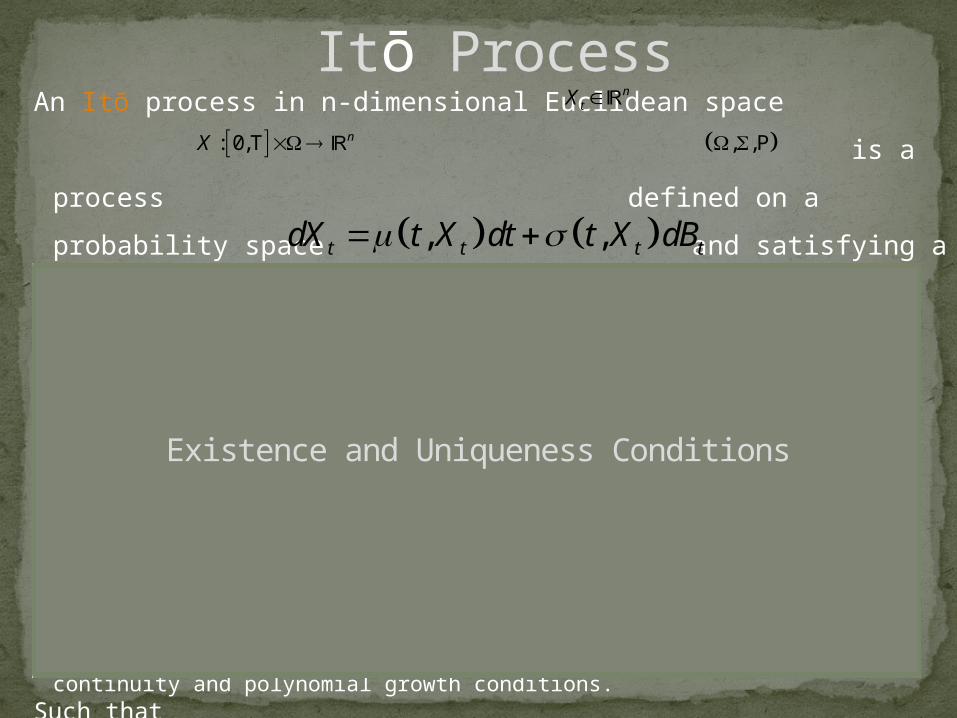

An Itō process in n-dimensional Euclidean space

is a process defined on a probability space and

satisfying a stochastic differential equation of the form

Where

T > 0

Bt is a m-dimensional SBM

satisfies the Lipschitz continuity and polynomial growth conditions.

satisfies the Lipschitz continuity and polynomial growth conditions.Such that

Where and .

These conditions ensure the existence of a unique strong solution Xt to the SDE (Øksendal 2003)

Itō Process : 0,T nX

ntX

, , P

, ,t t t tdX t X dt t X dB

: 0,T n n

: 0,T n n m

, : 0,T ; ,

, , , , ; , , 1

nC D t x y

t x t y t x t y C x y t x t x D x

22

,

: iji j

2 2: i

i

Existence and Uniqueness Conditions

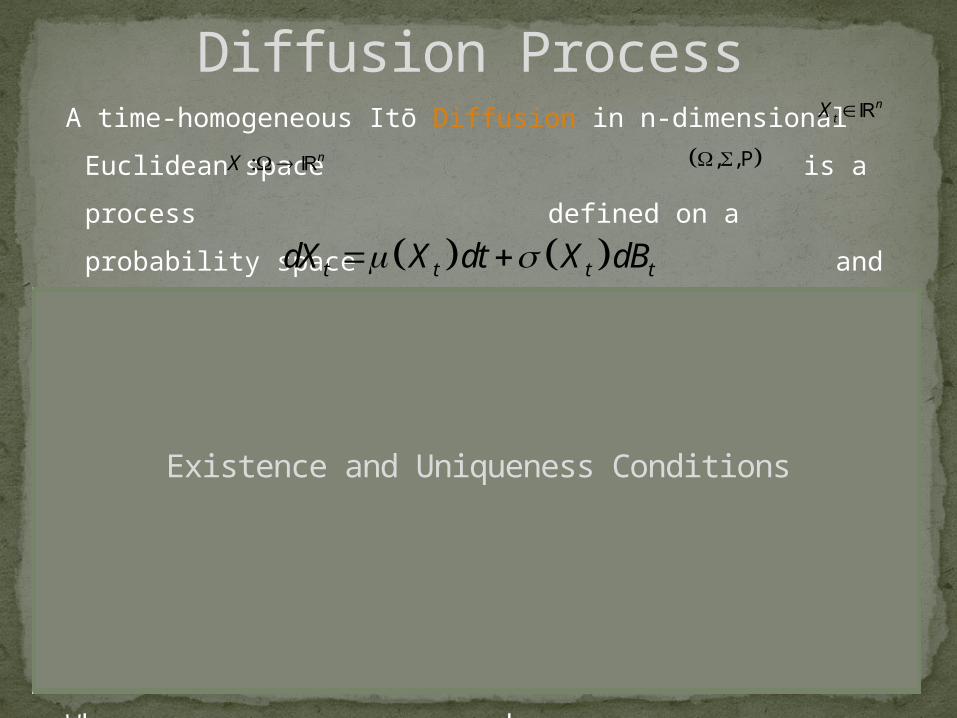

A time-homogeneous Itō Diffusion in n-dimensional Euclidean space

is a process defined on a probability space

and satisfying a stochastic differential equation of the form

Where

Bt is a m-dimensional SBM

is Lipschitz continuous.

is Lipschitz continuous.

Meaning

Where and .

This condition ensures the existence of a unique strong solution Xt to the SDE (Øksendal 2003).

Diffusion Process

: nX

ntX

, , P

t t t tdX X dt X dB

: n n

: n n m

. . , nC s t x y x y x y C x y

22

,

: iji j

2 2: i

i

Existence and Uniqueness Conditions

Suppose Xt is an Itō process satisfying the SDE

And f(t,x) is a twice- differentiable scalar function.

Then

In more detail

Sketch of proof

The Taylor series expansion of f(t,x) is

Recall that

Substituting and gives

As the terms and tend to zero faster. Setting and we are done.

Itō's Lemma , ,t t t tdX t X dt t X dB

2

2

2

1, , , , , , , ,

2t t t t t t t t t

f f f fdf t X t X t X t X t X t X dt t X t X dB

t x x x

2 2

22 t

f f f fdf dt dB

t x x x

22

2

1...

2

f f fdf dt dx dx

t x x

2

2 2 2 22

12 ...

2t t t

f f fdf dt dt dB dt dtdB dB

t x x

tx X tdx dt dB

0dt

~ 0,t t dt tdB B B N dt O dt

2dt2tdB dt

1.5tdtdB O dt

Sketch of Proof

Suppose Xt satisfies following SDE

With and

Thus the SDE turns into

Since is a twice- differentiable scalar function in (0,∞)

By Itō Lemma we have

Then

The integral equation

Finally

Geometric Brownian Motion , ,t t t tdX t X dt t X dB

2 2 2

2

1 1 1log 0

2 2t

t t t t tt t t

Xd X X dt X dB dt dB

X X X

, t tt X X , t tt X X

t t t tdX X dt X dB

, logt tf t X X

2 2

22 t

f f f fdf dt dB

t x x x

2 2

0 00 0log log log

2 2

t t

t s tX X ds dB X t B

2

2

0

tt B

tX X e

If X0 >0 then Xt > 0 for all t> 0

Definition. We say that a random process, , is a

geometric Brownian motion (GBM) if for all t≥0

Where Bt is an SBM.

We say that Xt ~GBM (µ,σ) with drift µ and volatility σ

Note that

Geometric Brownian Motion : 0tX t

2

2

0

tt B

tX X e

-a representation which we will later see that is useful for simulating security

prices.

2

2 2

2

2

0

2 2

0

2

t s

t s t t

s t t

t s B

t s

t B s B B

s B B

t

X X e

X e

X e

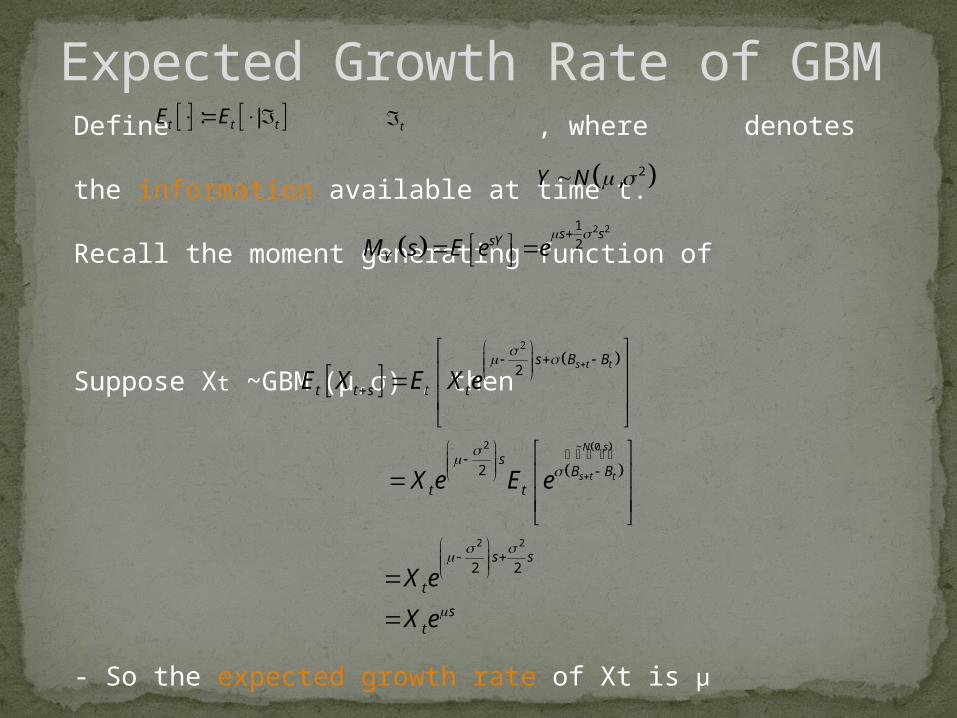

Define , where denotes the information available at time t.

Recall the moment generating function of

Suppose Xt ~GBM (µ,σ) , then

Expected Growth Rate of GBM : |t t tE E

- So the expected growth rate of Xt is µ

2

2 ~ 0,

2 2

2

2

2 2

s t t

N s

s t t

s B B

t t s t t

sB B

t t

s s

t

st

E X E X e

X e E e

X e

X e

2 21

2s ssY

YM s E e e

t

2,Y N

Note that,

Thus

1. Fix t1 < t2 < …< tn-1 < tn . Then

are mutually independent.

2. Paths of Xt are continuous as a function of t, i.e. they do not jump.

3. For s>0,

Properties of GBM

22

2 log2

t s ts B Bt s t s

t s tt t

X Xe s B B

X X

32

1 2 1

, ,..., n

n

t tt

t t t

X XX

X X X

22log ~ N ,

2t s

t

Xs s

X

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

The Black-Scholes equation is a partial differential equation (PDE) satisfied by a derivative (financial) of a stock price process that follows a deterministic volatility GBM, under the no-arbitrage condition and risk neutrality settings.

Starting with a stock price process that follows GBM

We represent the price of the derivative of the stock price process as Where a twice- differentiable scalar function at St>K.

We apply the Itō lemma

The arbitrage-free condition serves to eliminate the stochastic BM component, leaving only a deterministic PDE.

Risk neutrality is achieved by setting µ = r

With we have the celebrated BS PDE:

The Black-Scholes Model

2

2

0

tt B

t t t t tdS S dt S dB S S e

: 0tS t

, rtt tf t S e S K

2:f

2 2 2

22t

t t t

Sf f f fdf S dt S dB

t s s s

2 2 2

22t

t

Sf f fdf S dt

t s s

2 2 2

22t

t

Sf f frS rf

t s s

dfrf

dt

r – interest rateK- strick price

A more elaborated model, dealing with a stochastic volatility stock price process that follows a GBM

Where , the instantaneous variance, is a Cox–Ingersoll–Ross (CIR) process

and are SBM with correlation ρ, or equivalently, with covariance ρdt.

μ is the rate of return of the asset. θ is the long variance, or long run average price variance:

as t tends to infinity, the expected value of νt tends to θ.

κ is the rate at which νt reverts to θ.

σ is the volatility of the volatility.

The Heston Model

St t t t tdS S dt v S dB

vt t t t tdv v dt v S dB

tv

,S vt tB B

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

Suppose is an Itō process satisfying the SDE

and one is interested in computing

Sometimes it is hard to analytically solve the SDE or to determine its distribution.

Although numerical computations methods are usually available(i.e. the Kolmogorov backward equation (KBE) via some finite-difference algorithm),

in some cases it is convenient to obtain a Monte Carlo approximation

This requires simulation of the system.

Monte Carlo Evaluation

Tl E f X

ntX

, ,t t t tdX t X dt t X dB

1

1 ˆT

Ni

i

l f XN

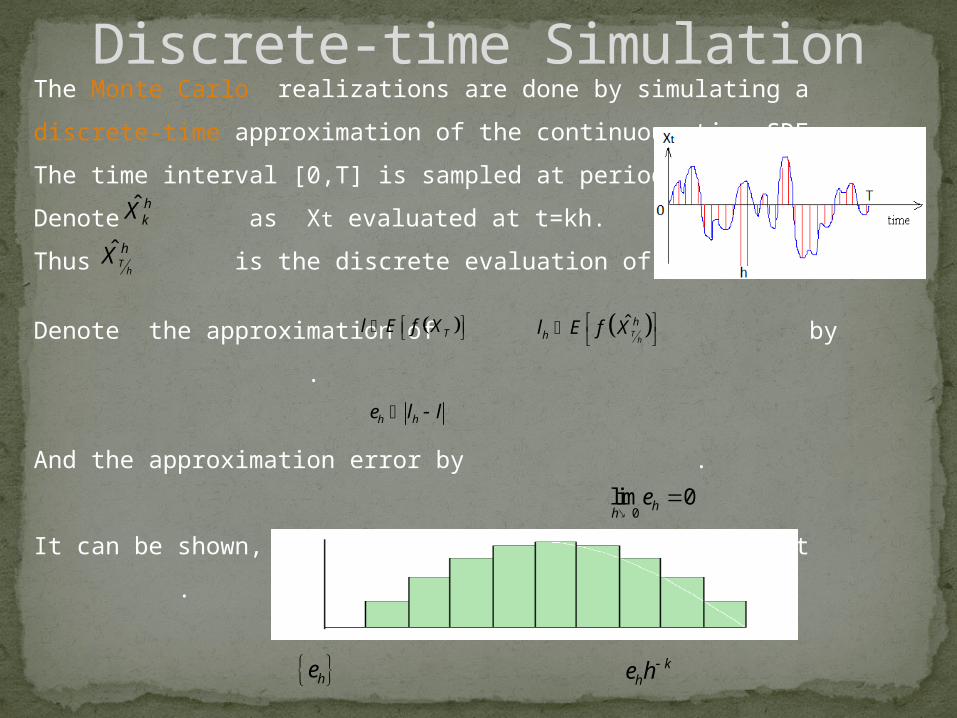

The Monte Carlo realizations are done by simulating a discrete-time

approximation of the continuous-time SDE.

The time interval [0,T] is sampled at periods of length h>0.

Denote as Xt evaluated at t=kh.

Thus is the discrete evaluation of XT.

Denote the approximation of by .

And the approximation error by .

It can be shown, under some technical conditions, that .

Definition. A sequence has order-k convergence if is

bounded in h.

Discrete-time Simulation

ˆ hkX

ˆTh

hX

ˆTh

hhl E f X

Tl E f X

h he l l

0lim 0hh

e

he khe h

The integral equation form of the SDE

The Euler method approximates the integrals using the left point rule.

With ε~N(0,1).

Thus, one can evaluate XT with by starting at and proceeding by

For k=0,…, T/h-1.Where ε1,ε2,… are N(0,1) i.i.d.

Note. The processes Xt and are not necessarily defined on the same probability space (Ω,Σ,Ρ).

The Euler Approximation

, ,t h t h

t h t s s st tX X s X ds s X dB

, ,

,

t h t h

s tt t

t

s X ds t X ds

t X h

, ,

,

,

t h t h

s s t st t

t t h t

t

s X dB t X dB

t X B B

t X h

ˆTh

hX 0ˆ hX x

1 1ˆ ˆ ˆ ˆ, ,h h h hk k k k kX X kh X h kh X h

ˆTh

hX

Is said to be a first-order discretizaion scheme

In which eh has order-1 convergence.

There is an error coefficient s.t. has a order-2 convergence.

The error coefficient gives a notion of bias in the approximation.

Although usually unknown it can be approximated to first order by

Under the polynomial growth condition of f (Talay and Tubaro, 1990).

The Euler Approximation Error

1 1ˆ ˆ ˆ ˆ, ,h h h hk k k k kX X kh X h kh X h

h he hh

22 h hh

l l

h

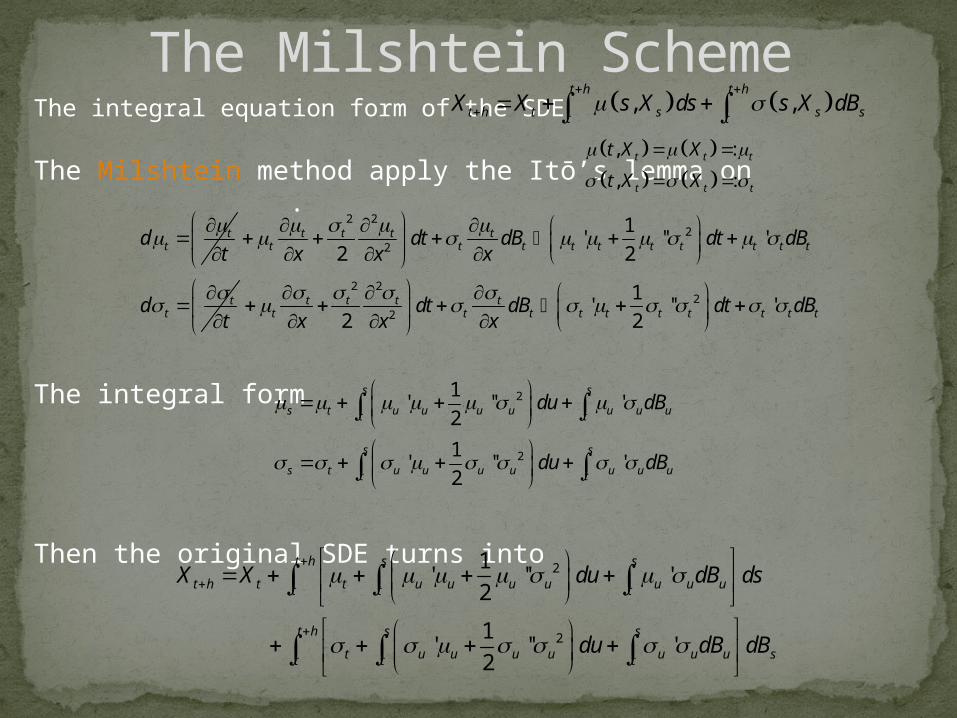

The integral equation form of the SDE

The Milshtein method apply the Itō’s lemma on .

The integral form

Then the original SDE turns into

The Milshtein Scheme , ,

t h t h

t h t s s st tX X s X ds s X dB

, :

, :

t t t

t t t

t X X

t X X

ttd

t

2 22

2

1' '' '

2 2t t t t

t t t t t t t t t t

tt

dt dB dt dBx x x

dt

2 22

2

1' '' '

2 2t t t t

t t t t t t t t t tdt dB dt dBx x x

2

2

1' '' '

2

1' '' '

2

t h s s

t h t t u u u u u u ut t t

t h s s

t u u u u u u u st t t

X X du dB ds

du dB dB

2

2

1' '' '

2

1' '' '

2

s s

s t u u u u u u ut t

s s

s t u u u u u u ut t

du dB

du dB

As the terms and are ignored.

Thus

Applying the Euler approximation to the last term we obtain

Define and suggest a solution .Indeed,

Thus,

and

The Milshtein Scheme0h 2dsdu O h 1.5

udsdB O h

't h t h t h s

t h t t t s u u u st t t tX X ds dB dB dB

2

' ' '

' '

t h s t h s t h

u u u s t t u s t t s t st t t t t

t h t h

t t s s t t h t t t s s t t h tt t

dB dB dB dB B B dB

B dB B B B B dB B B B

21

2t tY B t

tt t

YdY a

t

2 2

2

1 10 1 1

2 2 2t t t t

t t

Y b Y Ydt b dB

B B B

1 t t t tdt B dB B dB

, ,t t t t t t t tdY a t Y dt b t Y dB B dB

2 21 1

2 2

t h t h

s s s t h t t t h tt tB dB dY Y Y Y B B h

22 2 2 21 1 1 1' ' ' ' 1

2 2 2 2

t h s

u u u s t t t h t t t h t t t t h t t tt tdB dB B B h B B B B B h h

Thus

Then

Turns into the Milshtein discretization

With ε~N(0,1).

Thus, one can evaluate XT with by starting at and proceeding by

For k=0,…, T/h-1.Where ε1,ε2,… are N(0,1) i.i.d.

The Milshtein Scheme

22 2 21 1 1' ' '

2 2 2

t h s

u u u s t t t h t t t h t t t t h tt tdB dB B B h B B B B B h

't h t h t h s

t h t t t s u u u st t t tX X ds dB dB dB

21' 1

2t h t t t t tX X h h h

ˆTh

hX 0ˆ hX x

21 1 1

1ˆ ˆ ˆ ˆ ˆ ˆ' 12

h h h h h hk k k k k k k kX X X h X h X X h

If the terms and are to be visible.

We have

Where

And

Remark. Euler and Milshtein deal with first and second-order discretization schemes respectively for 1-D SDE with .

as Talay (1984,1986) provides second-order discretization schemes for multidimensional SDE with .

The Milshtein Scheme 2dsdu O h 3

2udsdB O h

tX

: 1ntX n

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

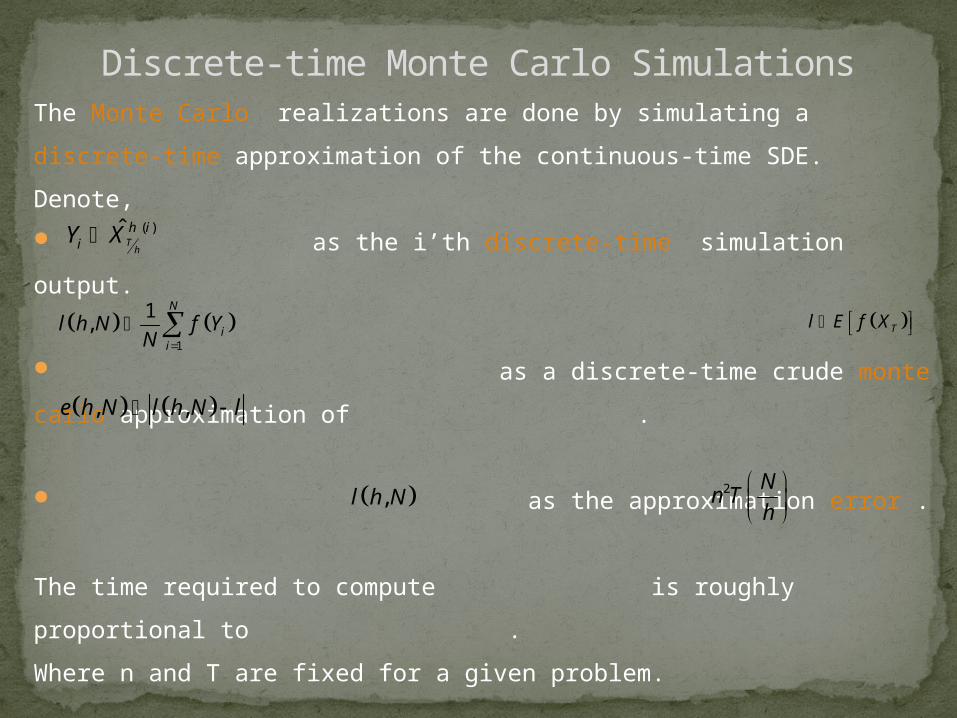

The Monte Carlo realizations are done by simulating a discrete-time

approximation of the continuous-time SDE.

Denote,

as the i’th discrete-time simulation output.

as a discrete-time crude monte carlo approximation

of .

as the approximation error .

The time required to compute is roughly proportional to

.

Where n and T are fixed for a given problem.

This paper pursues the optimal tradeoff between N and h

given limited computation time.

Discrete-time Monte Carlo Simulations

( )ˆTh

h iiY X

Tl E f X 1

1,

N

ii

l h N f YN

, ,e h N l h N l

,l h N 2 Nn T

h

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

This paper provides an asymptotically efficient algorithm for

the allocation of computing resources to the problem of

Monte Carlo integration of continuous-time security prices.

The tradeoff between increasing the number of time intervals

per unit of time and increasing the number of simulations,

given a limited budget of computer time, is resolved for first-

order discretization schemes (such as Euler) as well as

second- and higher order schemes (such as those of Milshtein

or Talay).

Abstract

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

f is and satisfies the polynomial growth condition.

i. as .

ii. as (i.e. is

uniformly integrable ).

iii. as , where β≠0 and p>0.

iv.The (computer) time required to generate is given the

deterministic

as , where γ>0 and q>0.

v.If or as then

as .

ii.If , where 0<c<∞, as then

as , where ε is N(0,1)

and

Assumptions ˆ

Th

hTf X f X 0h

2

2ˆTh

hTE f X E f X

0h 2ˆ 0Th

hf X h

p phl l h O h 0h

ˆTh

hf X

q qh h O h 0h

1

2q p

th t

12 0q p

th t t

2 ,p

q p

t tt e h N t

1

2q p

th t c 1

2 0q p

th t t

1

22 ,

pq p p

qt tt e h N cc

t

Theorem

2TVar f X

Given t units of computer time.

C

Proof

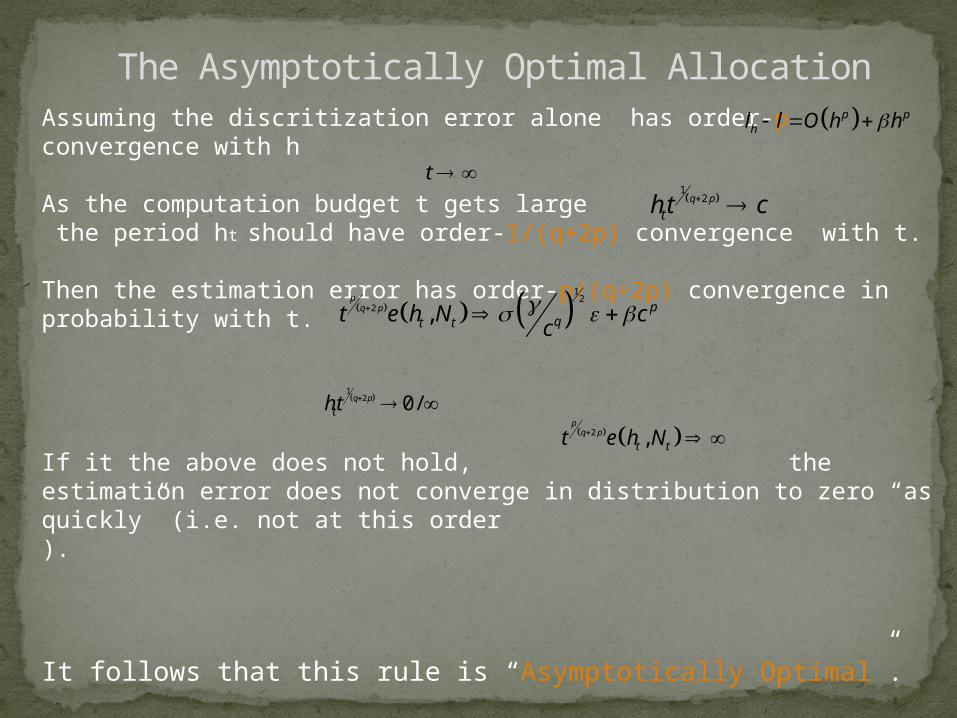

Assuming the discritization error alone has order-p convergence with h

As the computation budget t gets large the period ht should have order-1/(q+2p) convergence with t.

Then the estimation error has order-p/(q+2p) convergence in probability with t.

If it the above does not hold, the estimation error does not converge in distribution to zero “as quickly” (i.e. not at this order ).

It follows that this rule is “Asymptotically Optimal”.

The Asymptotically Optimal Allocation

t

12q p

th t c

1

22 ,

pq p p

qt tt e h N cc

p phl l O h h

1

2 0 /q p

th t

2 ,p

q p

t tt e h N

Informally, if then , where .

Thus,

Let be the number of time intervals, as ht is the period.

For the Euler scheme (p=1) : For the Milshtein or Talay schemes (p=2):

For the asymptotically optimal allocation, if thenThus

Thus,

As the root-mean-squared estimation error is and the error bias is β.

For the Euler scheme (p=1) : For the Milshtein or Talay schemes (p=2):

Interpertation

12q p

th t c 2q pth t c q q

t t tt N h N h O h

2 pt th N Const

12: 2 : : 16t t t t t tn n h h N N

12: 2 : : 4t t t t t tn n h h N N

tt

Tn

h

1

22 ,

pq p p

qt tt e h N cc

1 12 4: 2 : :t t t tn n h h e e

1 12 2: 2 : :t t t tn n h h e e

1

21 12 2 2, , , ,

pq p q p q p

p pp p p p p

qt t t t t t t t t t t t tt e h N h h t e h N h h t e h N h c e h N cc

2, q pp

t t t ce h N h

1

2q p

th t c

2q pp

t ce h

Consider the SDE with .

The diffusion process Xt>0 which satisfies the constant-elasticity-of-variance model (Cox,1975)

with , can be simulated by the Euler or Milshtein Schemes.

A European call option on the asset with strike price K and expiration date T is , has we would try to estimate its initial price by .

For γ=1 we obtain the Black-Scholes model.

Technical Details.For which f is and satisfies the polynomial growth conditions everywhere but at x=K.

Then it can be uniformly well approximated for above by .

If we take δ to be of order-2p convergence we preserve the quality of aproximation.For we have as (Yamada, 1796 and dominated convergence).

Experiments - Settings , ,t t t tdX t X dt t X dB

t t t tdX rX dt X dB

,

, 0

t t t

t t t t

t X X rX

t X X X X

0.5,1

rTTY e X K

TE f X rTT Tf X e Y X K

2

0,12

x K x Kf x

C

ˆTh

hTf X f X 0.5,1 0h

Technical Details

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

For the particular case: We take

The following results are obtained,

CommentsFor the Euler scheme (p=1) : For the Milshtein scheme (p=2):

The assumption hold with other but normal i.i.d increments with zero mean and unit variance uder technical conditions (Talay, 1984,1986).

Experiments - Results

12: 2 : 4 , :n n N N e e 1

4: 2 : 16 , :n n N N e e

-Brownian Motion - Wiener Process (SBM)

-Stochastic Calculus (Itō’s Calculus)- Stochastic Integral (Itō’s Integral)- Stochastic Differential Equation (SDE)- Itō Process- Diffusion Process- Itō’s Lemma- Example : Geometric Brownian Motion

(GBM)

-Security Price Models - The Black-Scholes Model (1973)- The Heston Model (1993)

Background The Paper-Introduction- Discretization Schemes- Euler- Milshtein (1978) - Talay (1984, 1986)

-Motivation-Abstract-Assumptions-Theorem

- Proof- Interpretation

-Experiments-More to go

What are we going to speak about ?

More monte carlo methods for asset pricing problems: Boyle (1977,1988,1990) Jones and Jacobs (1986) Boyle, Evnine and Gibbs (1989)

An Alternative large deviation method for the optimal tradeoff : chapter 10 of Duffie (1992).

Extensions

Path dependent security payoffs

Stochastic short-term interest rates (Duffie,1992)

A path dependent “lookback” payoff

Extension of the general theory of weak convergence for more general path-dependent functionals

More discretization schemes: Slominski (1993,1994), Liu (1993)

Adding a memory constraint

More to go

0

T

T tX X dt

t tr R X

infT t tX X

Thank you for listening