Paper P5 - Kaplan Publishingkaplan-publishing.kaplan.co.uk/SiteCollectionDocuments/acca-look... ·...

30

ACCA Paper P5 Advanced Performance Management Pocket notes

Transcript of Paper P5 - Kaplan Publishingkaplan-publishing.kaplan.co.uk/SiteCollectionDocuments/acca-look... ·...

ACCAPaper P5Advanced Performance Management

Pocket notes

Advanced Performance Management paper P5

ii kaplanpublishing

British library cataloguing-in-publication dataA catalogue record for this book is available from the British Library.

Published by:Kaplan Publishing UKUnit 2 The Business CentreMolly Millars LaneWokinghamBerkshireRG41 2QZ

ISBN 978-1-78415-250-5

© Kaplan Financial Limited, 2015

Printed and bound in Great Britain.

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of Kaplan Publishing.

Advanced Performance Management paper P5

kaplanpublishing iiikaplanpublishing iii

ContentsChapter 1: Introduction to strategic management accounting .......................................................1

Chapter 2: Environmental influences ..........................................................................................21

Chapter 3: Approaches to budgets ..............................................................................................37

Chapter 4: Business structure and performance management ...................................................49

Chapter 5: The impact of information technology .......................................................................63

Chapter 6: Performance reports for management ......................................................................73

Chapter 7: Human resource aspects of performance management ...........................................79

Chapter 8: Financial performance measures in the private sector .............................................89

Chapter 9: Divisional performance appraisal and transfer pricing ............................................101

Chapter 10: Performance management in not-for-profit organisations ........................................115

Chapter 11: Non-financial performance indicators .......................................................................123

Chapter 12: Corporate failure .......................................................................................................137

Chapter 13: The role of quality in performance management .....................................................147

Chapter 14: Environmental management accounting .................................................................157

Index .................................................................................................................................... I.1

Advanced Performance Management paper P5

iv kaplanpublishing

Exam guidance – keys to success in this paperThe aim of this paper is to apply relevant knowledge and skills and to exercise professional judgement in selecting and applying strategic management accounting techniques in different business contexts, and to contribute to the evaluation of the performance of an organisation and its strategic development. However it is important to remember that this paper is about application of techniques to real-life situations so you are expected not only to be able to describe and use a technique but to discuss implementation issues and the technique’s usefulness in a particular scenario.

Paper P5 also has a strong relationship with Paper P3 Business Analysis in the areas of strategic planning and control and performance measurement and expects you

to have your knowledge in place from paper F5 performance management.

Advanced Performance Management paper P5

kaplanpublishing vkaplanpublishing v

Coresyllabusareas

strategicplanningand

control

strategicperformancemeasurement

Externalinfluencesonorganisationalperformance

performanceevaluationand

corporatefailure

performancemeasurementsystemsand

design

Currentdevelopmentsandemergingissues

inperformancemanagement

Advanced Performance Management paper P5

vi kaplanpublishing

The examination

The format

The examination paper will comprise two sections.

Total time allowed – 15 minutes reading and 3 hours writing.Marks per question

Number of marks

Section A One compulsary question 50 50

Section B Answer two from three questions 25 50

Total marks 100

There will be four professional marks available.

Candidates will receive a present value table and an annuity table.

A range of topics may be covered in individual questions and the exam will contain a mix of computational and discursive elements.

Advanced Performance Management paper P5

kaplanpublishing viikaplanpublishing vii

Marks per question

Number of marks

Section A One compulsary question 50 50

Section B Answer two from three questions 25 50

Total marks 100

Examiner’skeystosuccess

clearlyunderstandtheobjectivesoftheexamasexplainedinthesyllabusand

studyguide

ensurethatpreparationfora

paperp5examhasbeenbasedona

programmeofstudysetfortherequiredsyllabusandexam

structure

practicecomputational,analytical,and

discursivequestionsunderexam

conditionsinordertoimprovespeedandpresentation

skills

carefullystudyallarticlesthat

appearinstudentaccountant(or

elsewhere),whicharerelevanttotopics

withinthesyllabusforpaperp5

beabletoclearlycommunicate

understandingandapplicationofknowledgeinthecontextofa

professonallevelexam.

Advanced Performance Management paper P5

viii kaplanpublishing

There will not always be a unique or correct solution to questions in Paper P5 examinations. Alternative solutions will be valid if they are supported by appropriate evidence and workings. Therefore if assumptions are made concerning a given scenario, they should be clearly stated.

Examination tips

Spend the first few minutes of the examination reading the paper.

Where you have a choice of questions, decide which ones you will do.

Divide the time you spend on questions in proportion to the marks on offer. One suggestion for this examination is to allocate 1.8 minutes to each mark available, so a 10-mark question should be completed in approximately 18 minutes.

Spend some time planning your answer. Stick to the question and tailor your answer to what you are asked. Pay particular

attention to the verbs in the question.

Spend the last five minutes reading through your answers and making any additions or corrections.

If you get completely stuck with a question, leave space in your answer book and return to it later.

If you do not understand what a question is asking, state your assumptions. Even if you do not answer in precisely the way the examiner hoped, you should be given some credit, if your assumptions are reasonable.

Do everything you can to make things easy for the marker. The marker will find it easier to identify the points you have made if your answers are legible.

Advanced Performance Management paper P5

kaplanpublishing ix

Key study tips

Ensure you review prior knowledge from earlier papers.

Revise the course as you work through it and leave sufficient time before the exam for final revision.

Cover the whole syllabus and pay attention to areas where your knowledge is weak.

Practice exam standard questions under timed conditions. Attempt all the different styles of questions you may be asked.

Read good newspapers and professional journals.

The examiner expects:1. assumed knowledge to be in place2. candidates to use the scenario3. general business knowledge4. a rounded view of the whole subject5. candidates to be able to tackle

calculations but the emphasis will not be on these

6. candidates to add value, for example by quantifying comments or discussing commercial implications

7. implications to be considered from a business manager’s perspective.

Pass rates are still low. The examiner recommends:1. using the scenario2. avoiding question spotting3. good time management – get the paper

marked out of 1004. answering the question asked5. planning answers6. that before the exam, students should

study the whole syllabus, revise assumed knowledge and practice lots of past exam questions.

Advanced Performance Management

x kaplanpublishing

Quality and accuracy are of the utmost importance to us so if you spot an error in any of our products, please send an email to [email protected] with full details, or follow the link to the feedback form in MyKaplan.

Our Quality Co-ordinator will work with our technical team to verify the error and take action to ensure it is corrected in future editions.

1

Introduction to strategic management accounting

In this chapter

• Planning and control.• The strategic planning process.• The role of corporate planning.• Critical success factors and key performance indicators.• Long-term and short-term conflicts.• The changing role of the management accountant.• Strategic management accounting in multinational companies.• Benchmarking.• SWOT analysis.• Gap analysis.

chapter

1

Introduction to strategic management accounting Chapter 1Introduction to strategic management accounting

2 kaplanpublishing

Exam focus

The emphasis of this section is on understanding the role of performance management in an organisation, to understand strategic management accounting and specific tools. It is important that, in addition to understanding the tools, you can also apply the tools to specific scenarios.

This section also explores the changing role of the management accountant and discusses contemporary issues and trends in performance management.

Introduction to strategic management accounting Chapter 1

kaplanpublishing 3

Introduction to strategic management accounting

Planning and control

Strategic Planning is concerned with:

• where an organisation wants to be (usually expressed in terms of its objectives) and

• how it will get there (strategies)

Control is concerned with monitoring the achievement of objectives and suggesting corrective action.

The performance hierarchy

Definition

Mission statement

Strategic plans and objectives

Tactical plans and objectives

Operational plans and objectives

general,broadaims

Morespecificobjectives

Detailedplansandtargets

Introduction to strategic management accounting Chapter 1

4 kaplanpublishing

Strategic and operational planning and control

Strategic planning & control Operational planning & controlLong-term, considering the whole organisation.

Short-term, based on a set of assets and resources.

Match activities to external environment and identify future requirements.

Rarely involves any major change.

High degree of uncertainty. Unlikely to involve major elements of uncertainty.

Control by monitoring the strategy and how well objectives are achieved.

Will not lead to changes in strategy.

succint Memorable Enduring

aguideforemployees

toworktowardsthe

accomplishmentofthemission

addressedtoanumberofstakeholder

groups

Characteristics of a mission statement:

Introduction to strategic management accounting Chapter 1

kaplanpublishing 5

The strategic planning process

Strategic analysis• External analysis to identify opportunities and threats.• Internal analysis to identify strengths and weaknesses.• Stakeholder analysis to identify key objectives and to assess power and interest of different groups.• Gap analysis to identify the difference between desired and expected performance.

Strategic choice• Strategies are required to ‘close the gap’.• Competitive strategy – for each business unit.• Directions for growth – which markets/products should be invested in.• Whether expansion should be achieved by organic growth, acquisition or some form of joint arrangement.

Strategic implementation• Formulation of detailed plans and budgets.• Target setting for KPIs.• Monitoring and control.

Introduction to strategic management accounting Chapter 1Introduction to strategic management accounting

6 kaplanpublishing

The role of corporate planning

The term corporate planning refers to the formal process which facilitates the strategic planning framework described above.

• The results of the plans are compared against stated objectives.

• Action taken to remedy short falls in performance.

• This is an ongoing process.

Definition

Role of corporate planning in evaluating potential strategies

Suitability

• Doesthestrategyhaveastrategicfit?

Acceptability

• isthestrategyacceptabletostakeholders?

Feasibility

• Canthenecessaryresourcesandcompetenciesbe.

Introduction to strategic management accounting Chapter 1

kaplanpublishing 7

Introduction to strategic management accounting

Critical success factors and key performance indicators

Critical success factors (CSFs) are the vital areas where ‘things must go right’ for the business in order for them to achieve their strategic objectives. The achievement of CSFs should allow the organisation to cope better than rivals with any changes in the competitive environment.

Definition

somethingthattheorganisationisabletodothatisdifficult

forcompetitorstofollow.Theorganisationwillneedtohave

thecorecompetenciesinplacetoachievetheCsFs.

Core competencies

TheachievementofCsFscanbemeasuredbyestablishingkpisforeachCsFandmeasuringactualperformance

againstthesekpis.kpisareessentialtostrategysincewhat gets measured gets done.

Key performance indicators(KPIs)

Introduction to strategic management accounting Chapter 1

8 kaplanpublishing

pressuresonmanagersareforshort-termresults

strategyisconcernedwiththelong-term

strictadherencetoastrategycanlimitcreativityandflair

Potential for conflict

Theadoptionofcorporatestrategyrequiresthattheinterestsofdepartments,activitiesandindividuals

aresubordinatetothecorporateinterests

Divisionalautonomy–individualmanagersoperatetheirbusinessunitsasiftheywere

independentbusinesses–seekingandexploitinglocalopportunitiesastheyarise

Rigidlong-termplanscanpreventtheorganisationrespondingtoshort-term

opportunitiesorcrises

Long-term and Short-term conflicts

Introduction to strategic management accounting Chapter 1

kaplanpublishing 9

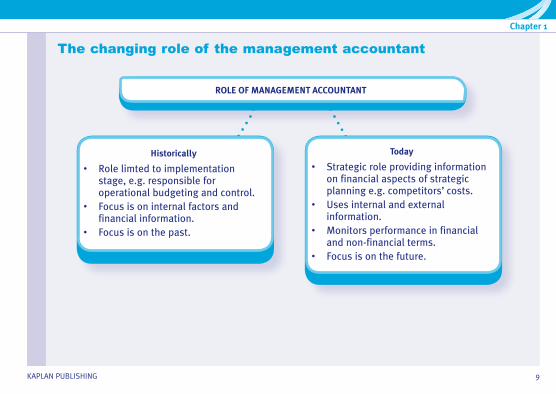

ROLE OF MANAGEMENT ACCOUNTANT

Historically

• Role limted to implementation stage, e.g. responsible for operational budgeting and control.

• Focus is on internal factors and financial information.

• Focus is on the past.

The changing role of the management accountant

Today

• Strategic role providing information on financial aspects of strategic planning e.g. competitors’ costs.

• Uses internal and external information.

• Monitors performance in financial and non-financial terms.

• Focus is on the future.

Introduction to strategic management accounting Chapter 1

10 kaplanpublishing

Burns and Scapens studied how the role of the management accountant has changed over the last 20 years.

Driving forces for change:

• Technology.• Management

structure.• Competition.

• The role has changed from financial control to business support.

• The new role has been called a hybrid accountant.

• Accountants may no longer work in a separate accounting department.

• Accountants ensures strategic goals are reflected in performance management.

• Management accountant helps the strategic business unit to get the most from their information system.

• Management accountant can develop a range of performance measures to capture factors that will drive success.

Lead

ing

to th

e

follo

win

g ch

ange

s

Lead

ing

to th

e

follo

win

g be

nefit

s

Introduction to strategic management accounting Chapter 1

kaplanpublishing 11

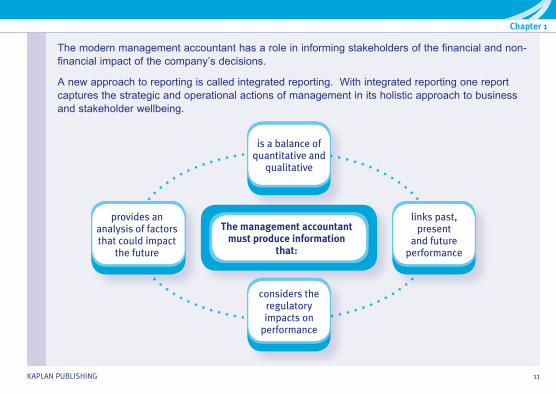

The modern management accountant has a role in informing stakeholders of the financial and non-financial impact of the company’s decisions.

A new approach to reporting is called integrated reporting. With integrated reporting one report captures the strategic and operational actions of management in its holistic approach to business and stakeholder wellbeing.

The management accountant must produce information

that:

is a balance of quantitative and

qualitative

links past, present

and future performance

considers the regulatory impacts on

performance

provides an analysis of factors that could impact

the future

Introduction to strategic management accounting Chapter 1

12 kaplanpublishing

Process specialisation

• Costadvantagesinlocatingcertaintypesofactivityincertaincountries.

Economic risk

• issuessuchasexchangeratefluctuations.

Key characteristics of multinational organisations requiring consideration by

strategic management accounting

Product specialisation

• particularcountrieshavecharacteris-tictastesthatthemultinationalmustcaterto.

Political sensitivities

• Riskfactorsassociatedwithoperatingacrossstateboundaries.

Administrative issues

• impactoninternaltransactionsofexchangeratemovements,currencyexchangecontrolsandinternationaltaxtreaties.

Strategic management accounting in multinational companies.

Introduction to strategic management accounting Chapter 1

kaplanpublishing 13

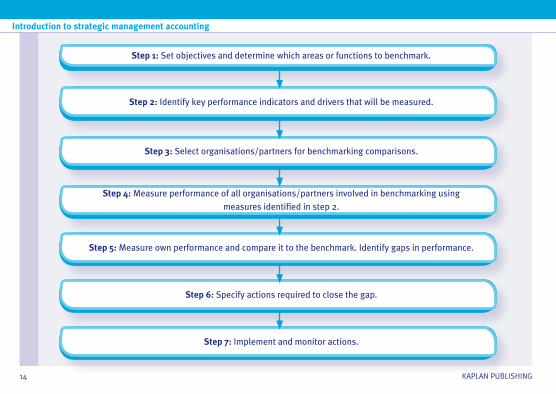

Once the organisation has established which aspects of its performance should be benchmarked, it must establish metrics for these.

Benchmarking The objective of benchmarking is to understand and evaluate the current position of a business organisation in relation to best practice and to identify areas and means of performance improvement.

Types of benchmarking

Internal benchmarking

Thisiswhereanotherfunction

ordepartmentofthe

organisationisusedasthebenchmark.

Competitor benchmarking

usesadirectcompetitorinthesameindustrywiththesameorsimilarprocessesas

thebenchmark.

Process or activity

Focusesonasimilarprocess

inanothercompanywhichisnotadirectcompetitor.

Introduction to strategic management accounting Chapter 1

14 kaplanpublishing

Step 1: Set objectives and determine which areas or functions to benchmark.

Step 2: Identify key performance indicators and drivers that will be measured.

Step 3: Select organisations/partners for benchmarking comparisons.

Step 4: Measure performance of all organisations/partners involved in benchmarking using

measures identified in step 2.

Step 5: Measure own performance and compare it to the benchmark. Identify gaps in performance.

Step 6: Specify actions required to close the gap.

Step 7: Implement and monitor actions.

Introduction to strategic management accounting Chapter 1

kaplanpublishing 15

Convertthreatsintoopportunities

Theorganisation’sstrengths,

weaknesses,opportunities

andthreatsareascertained.

itcanhelpidentifyCsFsandkpis

itprovidesasummarisedanalysis

ofthecompany’spresentpositioninthemarketplace.

assistinclosingthegap

SWOT

ANALYSIS

pursueopportunities

Matchstrengthswithmarket

opportunities

Converta

weakness

intoastrength

SWOT analysis (corporate appraisal)

Introduction to strategic management accounting Chapter 1

16 kaplanpublishing

Earn

ings

Times(years)0 1 52 3 4 6 7 8

T

F2

F1

F0

Diversificationgap

Expansiongap

Efficiencygap

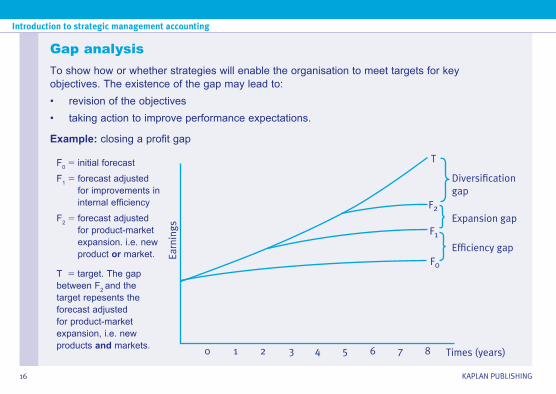

Gap analysisTo show how or whether strategies will enable the organisation to meet targets for key objectives. The existence of the gap may lead to:• revision of the objectives• taking action to improve performance expectations.

Example: closing a profit gap

F0 5 initial forecast

F1 5 forecast adjusted for improvements in internal efficiency

F2 5 forecast adjusted for product-market expansion. i.e. new product or market.

T 5 target. The gap between F2 and the target repesents the forecast adjusted for product-market expansion, i.e. new products and markets.

Introduction to strategic management accounting Chapter 1

kaplanpublishing 17

High LowRelative market share

Mar

ket g

row

th

Low

Hig

h

Star

• Is the high reinvestment being spent effectively?

• Is market share being gained, held or eroded?

• Is customer perception improving?• Are customer CSFs changing as the

market grows?• Net cash flow.• Is the star becoming a cash cow.

Cash cow

• Net cash flow.• Is market share being eroded –

could the cash cow be moving towards becoming a dog?

Problem child

Investment strategy

• Is market share being gained?• Effectiveness of promotional spend.

Divestment strategy

• Monitor contribution to see whether to exit quickly or divest slowly.

Dog

• Monitor contribution to see whether to exit quickly or divest slowly.

• Monitor market growth as an increase in the growth rate could justify retaining the product.

Boston Consulting Group (BCG) matrix

• thematrixshowswhetherthefirmhasabalancedportfolio.

• itcanbeusedtoassessbusinessperformanceandperformancemanagementissuesofanentity.

Introduction to strategic management accounting Chapter 1

18 kaplanpublishing

Exam sitting Area examined Question number Number of marksDecember 2014 Benchmarking 1(iii) 16

June 2014 Mission 1(v) 6

December 2013 KPIs, CSFs and gap analysis 1(i)(iii)(iv)(v) 35

December 2012 Changing role of management accountant

5(a) 12

June 2012 Benchmarking 4 17

June 2012 KPIs 2(a) 12

December 2011 KPIs 2(a) 7

June 2011 BCG 4 20

December 2010 CSFs and KPIs 1(a)(c) 20

December 2010 KPIs 4(a) 4

December 2009 KPIs 2(b)(i) 12

December 2009 Mission, CSFs and KPIs 5 17

December 2008 Planning gap 3(a) 5

June 2008 Benchmarking 1(b) 7

Exam focus

Introduction to strategic management accounting Chapter 1

kaplanpublishing 19

December 2007 CSFs 3(b) 10

Pilot paper Mission 2(a)(i) 5

Introduction to strategic management accounting

20 kaplanpublishing