Palm Biodiesel Industry- Navigating through the Storm. Plenary 1 UR Unnithan...Presentation Outline...

55

PRIVATE & CONFIDENTIAL Palm & Lauric Oils Price Outlook Conference & Exhibition 2018 Mar 5-7, Kuala Lumpur Palm Biodiesel Industry- Navigating through the Storm. U.R. Unnithan, SUMWIN Group

Transcript of Palm Biodiesel Industry- Navigating through the Storm. Plenary 1 UR Unnithan...Presentation Outline...

PRIVATE & CONFIDENTIAL

Palm & Lauric Oils Price Outlook Conference & Exhibition 2018 Mar 5-7, Kuala Lumpur

Palm Biodiesel Industry- Navigating through the Storm.

U.R. Unnithan, SUMWIN Group

Presentation Outline

1. Head Winds facing the Palm Biodiesel industry

2. Global Energy Outlook

3. Renewables in the energy mix

4. Global Biodiesel scenario

5. Palm Biodiesel update for Indonesia and Malaysia

6. Updates on B10 testing in Malaysia

7. Economics for Biodiesel in Malaysia and Indonesia

8. Conclusion and Palm Price Outlook

2

Head Winds Facing the Palm Biodiesel Industry.

1. EU ban on Palm Oil for Biodiesel.

2. Demand for a new common Sustainability Standard in EU.

3. American RFS2 approval still a dream.

4. Lack of Political will in Asia for Biofuel Mandates.

5. Low Crude Oil prices

3

EU BAN ON PALM OIL FOR BIOFUELS

4

5

The general perception of the MEP Resolution...

An example of what the Press (Guardian) says

6

EU parliament’s Environment Committee and Research & Energy Committee proposed a ban on Palm oil for Biofuel on Jan 17, 2018 • 492 MEPs voted in favour • 88 MEPs voted against • 107 MEPs abstentions U.K MEPs voted against the ban in view of inflationary effect on food prices and economic damage to developing countries Spain has come out against the ban as it Is a big user of Palm Oil for Biodiesel in EU.

7

8 SOURCE: MPOC

Malaysia’s Response

• MITI Minister YBM Datuk Mustafa: ban is “ potential violation of WTO Rules”

• MPIC Minister YBM Mah: ban is “ akin to Crop Apartheid”

• 650,000 small holders in Malaysia up in arms against the ban

9

10

11

Double Standards- Palm is banned by 2021 but other Food Crops can be used till 2030

• 46 % of total palm oil imported by the EU is used for the production of biofuels. • This is estimated to use of about one million hectares of tropical area. • Palm has a yield/hectare that is 10 times more than Soy and 4 times that of Rapeseed. Where is EU going to find this land to fill the void? • UK Conservative party MEP said “ The reality is that this is a vote driven by interests of Rapeseed producers here in Europe specifically the biofuels industry at home

12

• Palm Cultivation done responsibly and sustainably can deliver positive contributions to the economic development of farmers in developing countries. • The view is that the existence of different schemes RSPO, ISPO and MSPO is confusing for consumers. • The ultimate objective should be the development of a single certification scheme, which would improve the visibility of sustainable palm oil for consumers • Question is : What is the effectiveness of a sustainability standard like ISCC that all Palm Biofuel producers have been using for exports to EU

13

What does RED II say about this?

“Member States may … distinguish between different types of biofuels, bioliquids, and biomass fuels produced from food and feed crops, for instance by setting a lower limit for the contribution from food or feed crop based biofuels produced from oil crops, taking into account indirect land use change”. • Most affected would be Palm Biodiesel • This means that each individual EU Government would have the ability to pick and choose limits for different types of biofuels- Palm Oil needs friends in the EU.

Global Energy outlook

• World GDP more than doubles by 2040.

• Global energy demand is predicted to rise by 33% in the next 25 years.

• China and India will account for half of the growth in global energy demand.

• Renewable Energy is the fastest growing energy source accounting for 40% of the increase in primary energy.

• Liquid biofuels constitute only about 4.1% of the total Renewable energy

14

-

0.5%

0.0

%

0.5

%

1.0

%

1.5

%

2.0

%

2.5

%

3.0

%

2030-

40

Other EU

Africa

Middle

East Other

Asia India

China

1985-2000 2000-15 2015-

30 *Industry excludes non-combusted use

of fuels

0

1

2

3

4

5

6

1990 2000 2010 2020 2030 2040

Electricity

Gas

Oil Coal

Sectors:

Industry

2018 BP Energy

Outlook

Growth in final energy consumption

in industry* by region

% per annum

Final energy consumption

in industry* by fuel

Billion toe

15

350

300

250

200

150

100

50

0

-50

-

100

India

China

Other non-

OECD OECD

Total

0.

0

0.

5

1.

0

1.

5

2.

0

2.

5

3.

0

3.

5

2000 2010 2020 2030 2040

Other*

Electricity

Gas

Oil

Transport demand continues to be dominated by oil…

Transport energy consumption by fuel type

Billion toe

Transport energy consumption

growth by region

Mtoe

*Other includes biofuels, gas-to-liquids, coal-to-liquids,

hydrogen 2018 BP Energy Outlook 16

2000- 2005- 2010- 2015- 2020- 2025- 2030- 2035-

2005 2010 2015 2020 2025 2030 2035 2040

0%

15%

30%

45%

60%

0%

2%

4%

6%

8% GDP

Other sectors

Industry*

Primary energy

India emerges as the largest growth market for global energy...

Oi

l

Coa

l

Ga

s

Renewable

s

1990-2016 2016-2040

*Excludes non-combusted fuels

2018 BP Energy Outlook 17

Other fuels

1990 2000 2010 2020

2030 2040

Growth of GDP and primary energy Shares of primary energy

% per annum

RENEWABLES IN THE MIX

18

0

5

1

0

1

5

2

0 Othe

r Africa

Other Asia

India

China

OEC

D

The energy transition…

*Industry excludes non-combusted use of fuels

0

5

1

0

1

5

2

0 Renewables

Hydro

Nuclear

Coal

Gas

Oil

Billion toe

0

5

1

0

1

5

2

0 Transport

Industry*

Non-combusted

Buildings

Primary energy demand

End-use sector Region Fuel

2018 BP Energy Outlook

19

India &

Other Asia

Differences in the fuel mix across regions...

0

1

2

3

4

201

6

20

40

201

6

204

0

201

6

204

0

20

16

204

0

201

6

204

0

Coa

l Oil

Gas

Hydro

Nuclear

Renewable

s

US EU China Middle

East

5

-400

-200 0 200 400 600 800

China India

China Other

Asia

Middle East

China India

US

India EU

Changes 2016-2040† by

fuel and region Primary energy demand by fuel and region Billion toe Mtoe

Renewables

Gas

Gas

Nuclear

Oil

Renewables

Renewables

Renewables

Coal

Oil

Coal

Oil

Coal

Coal

Coal

†Ten largest increases and five largest declines

China

2018 BP Energy Outlook

US

EU

US

EU

20

GLOBAL BIODIESEL SCENARIO

21

BIODIESELand HVO: World Production ( Mn T )

J a n u a r y / D e c e m b e r

2017 2016 2015 2014 2013

EU-28 . . . . . 12.90* 12.61 12.41 12.29 10.71

U.S.A. . . . . . 6.10 6.21 4.72 4.80 4.77

Argentina . . . 2.80* 2.66 1.81 2.58 2.00

Brazil . . . . . . 3.75 3.33 3.46 3.00 2.56

Colombia . . . .53* .51 .51 .52 .50

Singapore . . 1.05* .99 .87 .80 .81 Indonesia. . . 2.95* 3.18* 1.22 2.92 2.60

Malaysia . . . .72 .51 .67 .60 .47

Thailand. . . . 1.33* 1.16* 1.14 1.04 .94 Oth. ctries.. . 3.06* 2.95* 2.89* 2.94* 2.65*

Total . . . . . . 35.19* 34.13 29.70 31.49 28.01

Change in ( Mn T )

+1.06* 4.43 -1.79 +3.48 +3.33

Source: ISTA Mielke, Feb 2018 – www.oilworld.de

22

2005 2007 2009 2011 2013 2015 2017

0

5

10

15

20

25

30

35

40

Biodiesel & HVO: World Production (Mn T)

Source: ISTA Mielke, Feb 2018 – www.oilworld.de

23

BIODIESEL Global Production

Quantity, MT

Share of Global Biodiesel

Production

PME 10.75 million 30.55%

SME 9.29 million 26.4%

RME 7.33 million 20.83%

TME 2.44million 6.93%

ALL BIODIESEL 35.19 million

Biodiesel production by Feedstock 2017

24

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0

5

10

15

20

25

30

35

40 others

used oils

tallow

rape oil

palm oil

soya oil

Biodiesel Use of Major Feedstock (Mn T)

Source: ISTA Mielke, Feb 2018 – www.oilworld.de

25

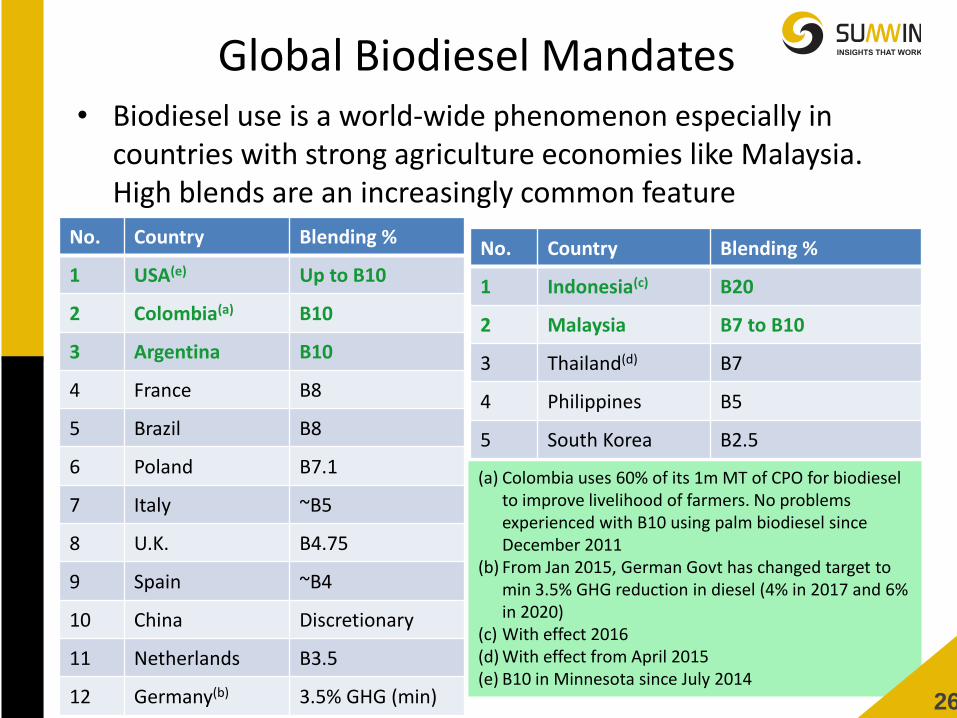

Global Biodiesel Mandates • Biodiesel use is a world-wide phenomenon especially in

countries with strong agriculture economies like Malaysia. High blends are an increasingly common feature

No. Country Blending %

1 USA(e) Up to B10

2 Colombia(a) B10

3 Argentina B10

4 France B8

5 Brazil B8

6 Poland B7.1

7 Italy ~B5

8 U.K. B4.75

9 Spain ~B4

10 China Discretionary

11 Netherlands B3.5

12 Germany(b) 3.5% GHG (min)

No. Country Blending %

1 Indonesia(c) B20

2 Malaysia B7 to B10

3 Thailand(d) B7

4 Philippines B5

5 South Korea B2.5

(a) Colombia uses 60% of its 1m MT of CPO for biodiesel to improve livelihood of farmers. No problems experienced with B10 using palm biodiesel since December 2011

(b) From Jan 2015, German Govt has changed target to min 3.5% GHG reduction in diesel (4% in 2017 and 6% in 2020)

(c) With effect 2016 (d) With effect from April 2015 (e) B10 in Minnesota since July 2014

26

BIODIESEL IN MALAYSIA AND INDONESIA

27

From Concept to Commercialization (1981-2006)

1981-1984

MPOB Starts palm biodiesel project, constructs first pilot plant

1984-1994

Palm biodiesel trials in taxis/buses

2000-2002

First commercial palm biodiesel pilot plant at Carotino

2006

First commercial palm biodiesel plant at Carotino

2008 Establishment of MBA

Source: MPOB

The MPOB began R&D into palm biodiesel from the early 1980s – constructing pilot plants and conducting vehicle engine trials

The first commercial palm biodiesel plant was built at Carotino with MPOB technology

28

Malaysian Biodiesel Mandate (2006-Present)

2008

Biofuel Industry Act 2007 comes into force

2011 Rollout of B5 Programme

2014 (November) Launch of B7

2018?

Launch of B10?

29

Total investments in the Malaysian biodiesel industry estimated about RM 2.2 billion

Total installed capacity is 2.1 million tonnes (based on MBA members’ capacity-17 members)

National Biodiesel mandate since 2011

Source: MPIC & MPOB

Malaysian Biodiesel Statistics

Years

Biodiesel [PME]

Production

Quantity

(MT)

Biodiesel [PME]

Export Quantity

(MT)

Biodiesel Blended

locally

(MT)

2008 171,555 102,108

2009 222,217 227,457

2010 117,173 89,609

2011 173,220 49,999 20,343

2012 249,213 28,983 113,276

2013 472,129 175,032 185,039

2014 600,524 87,856 295,451

2015 763,532 178,942 382,000

2016 500, 857 83,581 350,000

2017 720,410 235,291 358,586

30

Export Boom → Bust → Local Consumption

Source: MPOB

Period I Period II Period III Period IV

Domestic Growth

31

Domestic Consumption Dominates

Period I Period II Period III Period IV

32

Biodiesel is Going Local

Source: MPOB, MEMR, USDA, *2016 includes Malaysian local consumption figure estimate by author

33

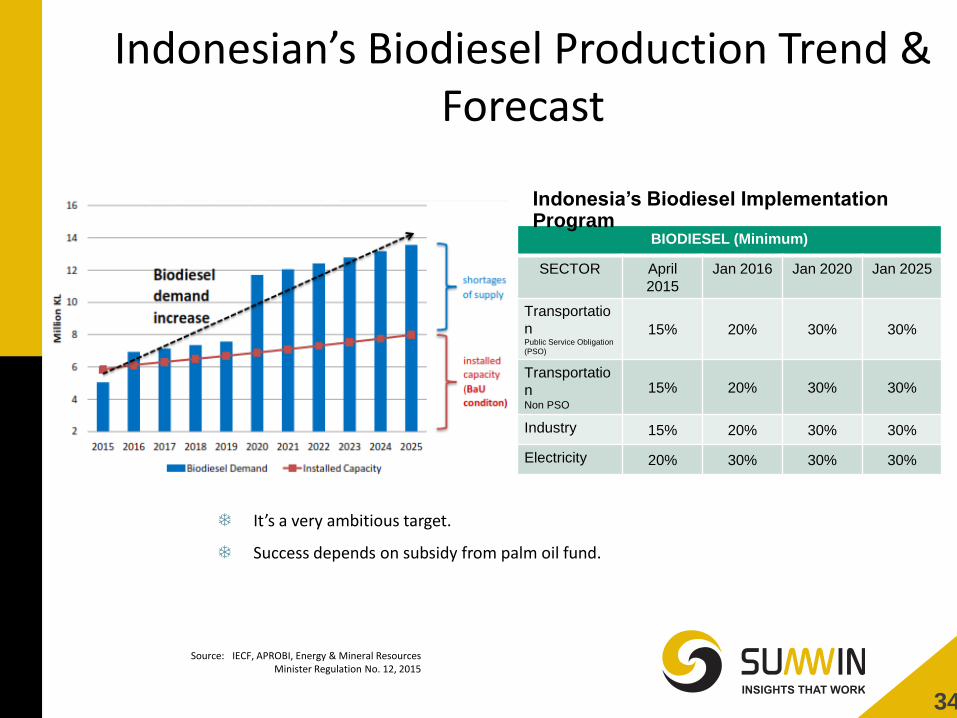

Indonesian’s Biodiesel Production Trend & Forecast

Source: IECF, APROBI, Energy & Mineral Resources Minister Regulation No. 12, 2015

BIODIESEL (Minimum)

SECTOR April

2015

Jan 2016 Jan 2020 Jan 2025

Transportatio

n Public Service Obligation

(PSO)

15% 20% 30% 30%

Transportatio

n Non PSO

15% 20% 30% 30%

Industry 15% 20% 30% 30%

Electricity 20% 30% 30% 30%

It’s a very ambitious target.

Success depends on subsidy from palm oil fund.

Indonesia’s Biodiesel Implementation Program

34

Indonesian’s Biodiesel Roadmap

Source: IECF, 2015

By 2020, 26% of Indonesia’s CPO is targeted for use in Biodiesel

35

Indonesian Government Policies on Energy Mix, Biodiesel Program & NDC

Coal

29.40

%

Oil

41.40

%

Renewable Energy

2025 2050

23% 31%

Bioenergy

10% 14%

2014

B5

2006

B10

B15

B20

2016

B30

2020

Biodiesel Mandatory Program

Indonesia,

Nationally Determined

Contributions UNFCCC

2020 2030

26% 29%

GO

VE

RN

ME

NT

PO

LIC

IES

& R

EG

UL

AT

ION

S

36

Source : APROBI

Indonesian Biodiesel Facts 2016

B20 Domestic Utilization

3 M kl/ 18.867 m barrel

Upstream sector Workforce

297,000

Greenhouse Gas Emissions Saving

8.03 M Ton (-15%) CO2 eq

Exporting Capabilities 2016

8.2 Mil Ton

Sources, APROBI

BIO

DIE

SE

L F

AC

T &

CO

NC

LU

SIO

NS

37

38

Updates on B10 & B20 testing in Malaysia

Breakdown of brand of vehicles in B10 Project

Model Type No. of Vehicles Engine Maker

Mitsubishi 4 wheel drive 5 Japan

Ford 4 wheel drive 3 USA

Toyota 4 wheel drive 9 Japan

Hyundai 4 wheel drive 1 Japan

Ssangyong 4 wheel drive 1 Korea

Mercedes Benz Passenger 1 Germany

Peugeot Passenger 5 Germany

Total 25

39 Source : MPOB

B10 and B20 MPOB Vehicles • Update as of June 2017:

Consumption of B10 & B20: 400,000 Litres

The total mileage covered: 2,149,200 km (min: 5,000 km; average: 90,000 km; max: 170,000 km)

• Findings:

No problem has been reported by drivers

Normal vehicle services have been carried at recommended service interval with no specific issues.

No signs of drop in engine performance.

40

Source : MPOB

41

B10 with Kuala Lumpur City Hall

• Started in February 2014 • As of June 2017: • Consumption: 282,227 liters • Normal vehicles: 1,219,211 km • Machineries: 5,917 hours • Findings: i. Service and Maintenance Follow the recommended service interval with no technical issues. ii. Monitoring and testing Quality of B10 Collection of Data on Mileage Visual Inspection of Oil and fuel Filter Lube Oil Analysis

42 Source : MPOB

B10 with Kuala Lumpur City Hall

43

Source : MPOB

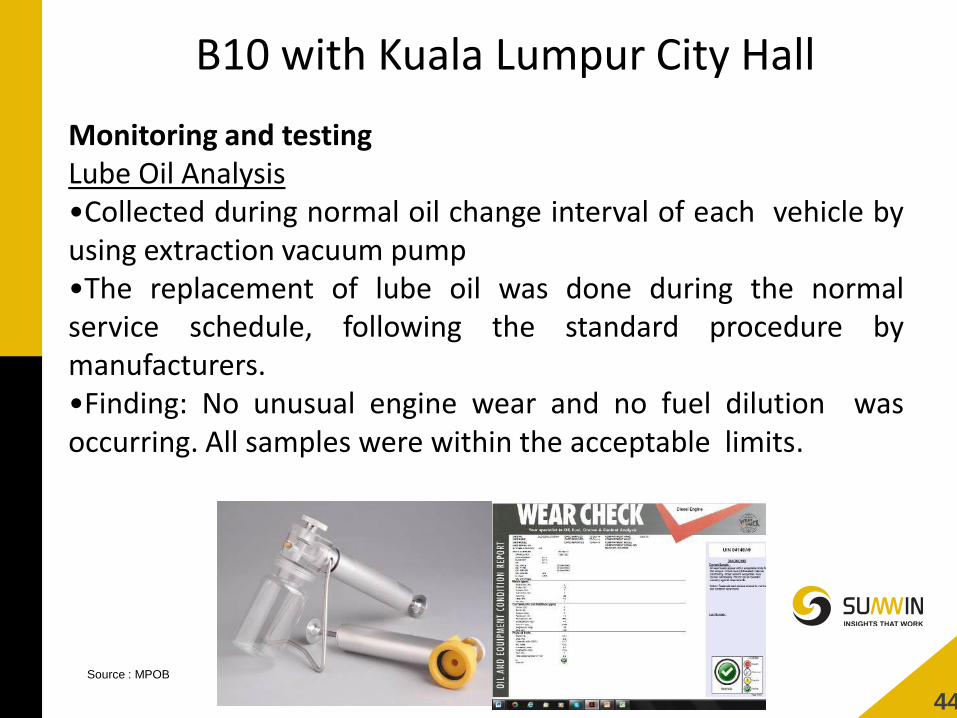

B10 with Kuala Lumpur City Hall

Monitoring and testing Lube Oil Analysis •Collected during normal oil change interval of each vehicle by using extraction vacuum pump •The replacement of lube oil was done during the normal service schedule, following the standard procedure by manufacturers. •Finding: No unusual engine wear and no fuel dilution was occurring. All samples were within the acceptable limits.

44

Source : MPOB

Findings of the recommended test: i. The exhaust emissions test: Nissan Navara and Nissan UD Truck LKA211N complied with the maximum opacity limit set by DOE. ii. Injector diagnostic test: The injector of Nissan Navara (WXK 3673) was in normal working condition after running 60,000 km. iii.Compression test: Compression pressures for six (6) engine cylinders of Nissan UD truck LKA211N were within standard specification and no excessive wear and tear noticed after running 100,000 km.

Engine Assessment

45

Report on Injector and Emission Test for 2 DBKL vehicles

(60,000km and 100,000km) in April – May 2017

Smoke test by Department of Environment (DOE)

Diagnostic test by Nissan Group Compression test by Nissan Group

46 Source : MPOB

Driver Survey

Estimated performance for vehicle using B10

Most of the respondents agreed that B10 is giving more power, more

pick-up, less noise, no engine jerking, less engine maintenance and

service, lower the engine temperature, less tailpipe emission and lower

fuel consumption as compared to normal diesel.

47 Source : MPOB

Conclusion (DBKL)

• B10 does not cause any problem to the engine of

vehicle and machinery

• B10 does not affect daily operations and

maintenance costs.

48 Source : MPOB

• Energy security – reducing dependency on foreign imported fuel

• GHG reduction – helping to meet the national target. GHG reduction is also a KPI for industries in improving its image in export markets

• No subsidies required (if B10 is built into formula pricing)

• The cost effectiveness of biodiesel would be even better as Malaysia moves to more stringent Euro 5 standard for diesel with 10 ppm sulfur. Here, palm biodiesel will further improve lubricity at lower sulfur levels (hence saving on an additional lubricity additive which would raise the price of ULSD)

• Create additional demand for CPO and its likely positive price impact

Benefits of B10

49

ECONOMICS FOR BIODIESEL IN MALAYSIA AND INDONESIA

50

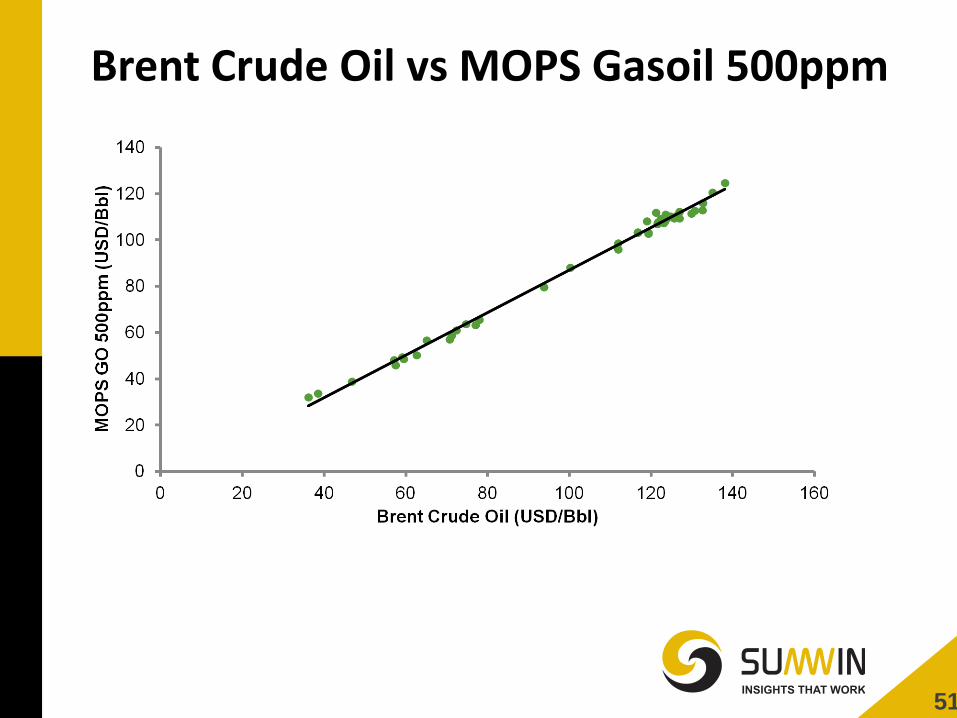

Brent Crude Oil vs MOPS Gasoil 500ppm

51

Brent

Crude

(USD/Bbl)

MOPS GO

500ppm

(USD/MT)

MOPS

GO 500

ppm

(MYR/L)

APM Formula

Malaysian

Retail EURO2

Diesel

(MYR/L)

Additional

Cost

(MYR/L) for

APM

Formula

Malaysian

Retail

EURO5

Diesel

(MYR/L)

B7 B10

25.00 244.29 0.79 1.02 0.11 0.17 1.12

30.00 284.70 0.92 1.15 0.11 0.15 1.25

35.00 325.10 1.05 1.28 0.10 0.14 1.38

40.00 365.51 1.19 1.42 0.09 0.13 1.52

50.00 446.33 1.45 1.68 0.07 0.10 1.78

60.00 527.15 1.71 1.94 0.05 0.08 2.04

70.00 607.97 1.97 2.20 0.03 0.05 2.30

80.00 688.78 2.23 2.46 0.02 0.02 2.56

CPO = RM2500/MT

PME = RM2.70/L

Exchange Rate 3.91

Retail price of Diesel will increase by MYR0.26/L for every USD10/bbl increase in Crude Oil price.

Until Nov 2014, subsidized diesel retail price in Malaysia was already at MYR2.1/L

Economics for Biodiesel Mandate in Malaysia

52

Malaysian retail price of Diesel in March 2018 is MYR2.18/L

Indonesia’s Biodiesel Support Fund

1. Biofuels Business Entities supply biodiesel to Pertamina / PT ANEKA KIMIA RAYA (AKR). 2. Pertamina / AKR will pay for the Biodiesel based on the Diesel Fuel Market Price Index

assigned by the Director General of Oil and Gas, Ministry of Energy and Mineral Resources.

3. Ministry of Energy and Mineral Resources cq DG EBTKE verify the delivery of Biodiesel from Biofuels Business Entities to Pertamina / AKR

4. IECF will disburse the Biodiesel financing funds based on the verification results. 5. Biodiesel Support Funds = The difference between the Market Price Index of Biodiesel

and Diesel Fuel Market Price Index determined by the Ministry of Energy and Mineral Resources.

6. As of December 2015, IECF disbursed 460 billion Rupiah.

Source: IECF, 2015

March 2016

53

Conclusions & Price Outlook

1. The EU ban on Palm Oil in Biofuel from 2021 will affect overall sentiment but unlikely to affect Price of CPO in 2018.

2. Protectionist policies from EU & US will restrict exports of PME.

3. The lifting of the Anti-dumping duties on Biodiesel exports from Indonesia and Argentina will lead to much higher Biodiesel exports in 2018.

4. 2018 could see an increase in mandates in Malaysia( B7 to B10) after the General Elections.

5. With Palm production picking up from the 2nd half of the year could see a drop in Palm Oil prices resulting in lower POGO spreads will provide support for the Indonesian B20 & Malaysian B10

6. On Balance, I see Palm Oil price not likely to drop below RM 2300 in 2018 and might average about RM 2450 in 2018.

54

Suite No. 3, Business Wing,X-Sentral within Bio-XCell Biotechnology Park No.2, Jalan Bioteknologi 1, Kawasan Perindustrian SiLC

79200 Iskandar Puteri, Johor, Malaysia

SUMWIN SOLUTIONS MALAYSIA SDN BHD

www.sumwinglobal.com Office: +607 300 5132/33 Fax:- +607 300 5130

THANK YOU