Pakistan strategy 2019 final6-1-2019 - imtrade.biz · +3.0% vs. a median of +1.1% for EM and FM...

45

Intermarket Securities is the Local Research Partner of Exotix Capital To find our Research on Bloomberg, please type - IMKP <GO> Pakistan Strategy 2019 Research Entity Number – REP-085 www.jamapunji.pk ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 44 7 January 2019 IMS Research [email protected] +92-21-111-467-000 Ahead of the curve Pakistan’s economy saw a major reset in 2018, leading to a sharp correction in valuation multiples. However, with the Discount Rate up a swift 425bps to 10.5% and the PKR having already depreciated by c.25% vs. the US$, we believe the adjustment phase is nearing its end. The market now trades at a 2019f P/E of 7.4x vs. its cross- cycle average of 8.6x and a peak of more than 12x at EM upgrade in mid-2017. Out of the universe of more than fifty Emerging and Frontier countries, Pakistan is among the cheapest five markets even as its projected earnings growth is in the top five. We believe this valuation gap can start to close once Pakistan enters an IMF program, likely in 1Q 2019, which can convincingly address Balance of Payments concerns and potentially trigger foreign buying. There are risks to the EM status, as well as headwinds to significant valuation rerating, but we believe it is now difficult to ignore Pakistan. The risk-reward appears favorable; we think any downside will be limited while the KSE-100 has the potential to rally up to 45,000pts in 2019, 21% higher from 2018’s close. The KSE-100’s fall in the last eighteen months was precipitated by Balance of Payment concerns. 2019 is about getting back on track and course correction has already commenced. We recommend going Overweight on Pakistan. Economic stabilization measures have already been taken 2019 is likely to feature greater fiscal consolidation but we believe interest and exchange rates are now near equilibrium levels. Having already risen by a swift 425bps in 2018, we see the Discount Rate increasing by another 50bps to 11.0%. Similarly, further PKR weakness in 2019 may be limited to 7-8%, in our view - the market’s average dividend yield is enough to account for this level of currency risk. The economy will slow in the interim – we see GDP growth at 4.0% in 2019 vs. 5.8% in 2018 – but the corrective measures taken thus far can result in recovery from 2020, particularly if international oil prices remain soft. The import cover is still below two months but, importantly, fx reserves are finding a foothold. Reserves rebuilding should gather both momentum and credibility with entry into an IMF program, which we pencil in for 1Q 2019. Historically, rising fx reserves have acted as a key catalyst for the KSE-100 Index and a repeat can occur in 2019. Pakistan is standing out against peers Given that the adjustment to interest and exchange rates has been among the swiftest in the Emerging and Frontier universe, Pakistan appears ahead of the curve relative to peers that are in the early stages of their own course corrections. Real interest rates in Pakistan are +3.0% vs. a median of +1.1% for EM and FM markets. Similarly, the PKR’s rapid devaluation in 2018 – the most after Argentina and Turkey – has brought the REER down to 104 vs. 124 in Nov’17. Pakistan’s domestic-driven economy (exports are a limited 7% of GDP vs. a median of 20% for peers) can potentially also stand out in a global environment facing challenges to growth and trade. While we flag risks to Pakistan’s EM status – it could be put on watch for downgrade to FM – this may arguably be taken as a positive by investors. A combination of corrective macroeconomic measures (that have already taken place) and cheap valuations can also attract foreign buying, for the first time since 2014, especially if an IMF program comes through. Risk-reward is attractive Valuations are supportive – Pakistan trades at a 2019f P/E of 7.4x, the lowest since Nov’13, and at a 13% discount to its cross-cycle average (2006 till date) of 8.6x. On the basis of P/B and P/S, the discount is an even sharper 33% and 23%. Pakistan is among the cheapest markets in the Emerging and Frontier universe and also offers the 2nd highest dividend yield in this space. Despite the slower economy, headline earnings growth is resilient; the IMS Universe is projected to post growth of 13% in 2019f and 16% in 2020f. Although 2019 growth will primarily be driven by Banks and E&P, it will be more broad-based across the medium-term. We think that even if the market’s P/E remains confined to a tight band in 2019, the KSE-100 has the potential to rally towards 45,000pts (21% higher than the Index’s last close). This has precedence; range-bound valuations (average P/E of 6.3x) and strong earnings growth (22%pa) last occurred during CY09-12 when the KSE-100 returned a CAGR of more than 20%. Market Snapshot As of Dec’31, 2018 KSE 100 Index 37,067 Market Cap (PKRbn) 7,693 Market Cap (US$bn) 55 Market Free Float 28% CY18 Return (US$) -27% Forward PE (x) 7.4 Avg. Daily Vol (mn shrs) 184 Avg. Daily Td Val (PKR mn) 7,872 Avg. Daily Td Val (US$ mn) 65 CY18 KSE100 Index – High (pts) 46,638 CY18 KSE100 Index – Low (pts) 36,663 Macro Projections 2018 2019F 2020F CPI - FY avg. 3.9% 7.0% 8.0% DR - CY end 10.5% 11.0% 10.0% PKR/USD - CY end 138.9 151.9 157.0 Source: IMS Research IMS Top 5 Picks TP (PKR) Upside UBL 180 37% PPL 191 27% ENGRO 379 20% LUCK 580 31% NML 180 33%

Transcript of Pakistan strategy 2019 final6-1-2019 - imtrade.biz · +3.0% vs. a median of +1.1% for EM and FM...

Intermarket Securities is the Local Research Partner of Exotix Capital To find our Research on Bloomberg, please type - IMKP <GO>

Pakistan Strategy 2019

Research Entity Number – REP-085 www.jamapunji.pk

ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 44

7 January 2019 IMS Research [email protected] +92-21-111-467-000

Ahead of the curvePakistan’s economy saw a major reset in 2018, leading to a sharp correction in valuation multiples. However, with the Discount Rate up a swift 425bps to 10.5% and the PKR having already depreciated by c.25% vs. the US$, we believe the adjustment phase is nearing its end. The market now trades at a 2019f P/E of 7.4x vs. its cross-cycle average of 8.6x and a peak of more than 12x at EM upgrade in mid-2017. Out of the universe of more than fifty Emerging and Frontier countries, Pakistan is among the cheapest five markets even as its projected earnings growth is in the top five. We believe this valuation gap can start to close once Pakistan enters an IMF program, likely in 1Q 2019, which can convincingly address Balance of Payments concerns and potentially trigger foreign buying. There are risks to the EM status, as well as headwinds to significant valuation rerating, but we believe it is now difficult to ignore Pakistan. The risk-reward appears favorable; we think any downside will be limited while the KSE-100 has the potential to rally up to 45,000pts in 2019, 21% higher from 2018’s close. The KSE-100’s fall in the last eighteen months was precipitated by Balance of Payment concerns. 2019 is about getting back on track and course correction has already commenced. We recommend going Overweight on Pakistan. Economic stabilization measures have already been taken 2019 is likely to feature greater fiscal consolidation but we believe interest and exchange rates are now near equilibrium levels. Having already risen by a swift 425bps in 2018, we see the Discount Rate increasing by another 50bps to 11.0%. Similarly, further PKR weakness in 2019 may be limited to 7-8%, in our view - the market’s average dividend yield is enough to account for this level of currency risk. The economy will slow in the interim – we see GDP growth at 4.0% in 2019 vs. 5.8% in 2018 – but the corrective measures taken thus far can result in recovery from 2020, particularly if international oil prices remain soft. The import cover is still below two months but, importantly, fx reserves are finding a foothold. Reserves rebuilding should gather both momentum and credibility with entry into an IMF program, which we pencil in for 1Q 2019. Historically, rising fx reserves have acted as a key catalyst for the KSE-100 Index and a repeat can occur in 2019. Pakistan is standing out against peers Given that the adjustment to interest and exchange rates has been among the swiftest in the Emerging and Frontier universe, Pakistan appears ahead of the curve relative to peers that are in the early stages of their own course corrections. Real interest rates in Pakistan are +3.0% vs. a median of +1.1% for EM and FM markets. Similarly, the PKR’s rapid devaluation in 2018 – the most after Argentina and Turkey – has brought the REER down to 104 vs. 124 in Nov’17. Pakistan’s domestic-driven economy (exports are a limited 7% of GDP vs. a median of 20% for peers) can potentially also stand out in a global environment facing challenges to growth and trade. While we flag risks to Pakistan’s EM status – it could be put on watch for downgrade to FM – this may arguably be taken as a positive by investors. A combination of corrective macroeconomic measures (that have already taken place) and cheap valuations can also attract foreign buying, for the first time since 2014, especially if an IMF program comes through. Risk-reward is attractive Valuations are supportive – Pakistan trades at a 2019f P/E of 7.4x, the lowest since Nov’13, and at a 13% discount to its cross-cycle average (2006 till date) of 8.6x. On the basis of P/B and P/S, the discount is an even sharper 33% and 23%. Pakistan is among the cheapest markets in the Emerging and Frontier universe and also offers the 2nd highest dividend yield in this space. Despite the slower economy, headline earnings growth is resilient; the IMS Universe is projected to post growth of 13% in 2019f and 16% in 2020f. Although 2019 growth will primarily be driven by Banks and E&P, it will be more broad-based across the medium-term. We think that even if the market’s P/E remains confined to a tight band in 2019, the KSE-100 has the potential to rally towards 45,000pts (21% higher than the Index’s last close). This has precedence; range-bound valuations (average P/E of 6.3x) and strong earnings growth (22%pa) last occurred during CY09-12 when the KSE-100 returned a CAGR of more than 20%.

Market Snapshot

As of Dec’31, 2018 KSE 100 Index 37,067 Market Cap (PKRbn) 7,693 Market Cap (US$bn) 55 Market Free Float 28% CY18 Return (US$) -27% Forward PE (x) 7.4 Avg. Daily Vol (mn shrs) 184 Avg. Daily Td Val (PKR mn) 7,872 Avg. Daily Td Val (US$ mn) 65 CY18 KSE100 Index – High (pts) 46,638 CY18 KSE100 Index – Low (pts) 36,663

Macro Projections 2018 2019F 2020F CPI - FY avg. 3.9% 7.0% 8.0% DR - CY end 10.5% 11.0% 10.0% PKR/USD - CY end 138.9 151.9 157.0 Source: IMS Research

IMS Top 5 Picks

TP (PKR) Upside UBL 180 37% PPL 191 27% ENGRO 379 20% LUCK 580 31% NML 180 33%

2 | P a g e

Pakistan Strategy 2019

Contents

2018 Review: Another political transition, another BoP crisis 3 Pakistan Market Timeline 3

2019 Strategy Synopsis 4 IMS Top Picks 4

Economic stabilization measures have already been taken 5 A sustainable Fx reserves buildup is a key catalyst 6 Large adjustments to interest and exchange rates are behind us 6 More is needed on the fiscal side 8 Growth will slow in 2019 but a quick rebound is not impossible 9

Pakistan is standing out against peers 10 Looking good to attract foreign buying 11 Possible downgrade to FM may act like an upgrade 12

Risk-reward is attractive 13 Attractive levels for building positions 13 The GDP-Earnings disconnect 13 Earnings growth can drive the market, even if valuations are range-bound 14 Banks to drive 2019 growth; more broad-based growth in 2020 14 KSE-100 can rally up to 45,000pts in 2019 15 Risks 16

Sector Outlook 17 Banks: Back on the growth track 18 E&P: Cheap valuations but triggers ahead 19 Fertilizer: Risk-reward in balance 20 Cement: Stay selective 21 OMCs: Tough period ahead 22 Power: Expansion projects & circular debt settlement 23 Textile: Looking good thematically 24 Autos: Bumpy ride ahead 25 Steel: Awaiting triggers 26 Pharmaceuticals: Correction has opened entry points 27 Consumer (Dairy): Challenges aplenty but long-term theme is intact 28 Insurance: Life business will mitigate the cyclicality of general business 29

Top Picks United Bank Ltd: Offers great risk-reward 31 Habib Bank Ltd: Normalization is a matter of time 32 Bank Alfalah Ltd: Play on margin expansion 33 Pakistan Petroleum Ltd: Diversification on the rise 34 Engro Corporation Ltd: Valuations are attractive 35 Engro Fertilizer Ltd: Safest bet in the fertilizer space 36 Lucky Cement Ltd: Well-positioned amid resilient core competencies 37 Attock Petroleum Ltd: Deserves a premium over peers 38 Hub Power Co. Ltd: The only way from here is up 39 Nishat Power Ltd: Efficient IPP with renewed hope of payouts 40 Nishat Mills Ltd: Worst is priced in, valuations are attractive 41 Indus Motor Co Ltd: Outperforming peers amid regulatory fallout 42

IMS Universe Summary 43 Disclaimer & Disclosures 44

3 | P a g e

Pakistan Strategy 2019

2018 Review: Another political transition, another BoP crisis The KSE-100 shed 8% in 2018 (-27% in US$ terms), deeply underperforming the MSCI EM and FM indices that were down 17% and 19%, respectively. This was the 2nd year in a row with negative returns in Pakistan, which has not happened since the mid-1990s. While the year started on a buoyant note – led by foreign buying of US$86mn in Jan’18 - sharp FPI outflow over the next 11 months took the market lower. Foreign selling for the year eventually clocked in at US$537mn, taking cumulative outflows since 2015 to US$1.7bn. Weak investor confidence showed up in daily turnover falling to US$65mn, a 7 year low. Despite transfer of power from one elected government to another (PML-N to PTI), the democratic polity appeared to cede space. That said, major state institutions appear to be better aligned now, which is a positive. Similar to past political transitions, Pakistan faced a Balance of Payments crisis that led to corrective measures; interest rates increased 425bps to 10.5% and PKR devalued by c.25%. As a result, the KSE-100’s forward P/E fell from 9.1x at the start of 2018 to 7.4x at the end.

Consecutive negative years for the first time since the 1990s

-25%

74%

-5%

-27% -1

1%31

%-4

6%49

%7%

-16%

112%

66%

39% 54

%5%

40%

-58%

60%

28%

-6%

49%

49%

27%

2%46

%-1

5% -8%

-80%

-40%

0%

40%

80%

120%

160%

CY92

CY94

CY96

CY98

CY00

CY02

CY04

CY06

CY08

CY10

CY12

CY14

CY16

CY18

KSE100 Return

Source: PSX

Foreign selling accelerated but outlook for 2019 is better

26

526

-127

126

398 383

-315 -339-488 -537-600

-400

-200

0

200

400

600

CY09

CY10

CY11

CY12

CY13

CY14

CY15

CY16

CY17

CY18

FIPI Flows - US$mn

Source: NCCPL

Market activity was subdued in 2018

0

100

200

300

400

500

600

CY00

CY01

CY02

CY03

CY04

CY05

CY06

CY07

CY08

CY09

CY10

CY11

CY12

CY13

CY14

CY15

CY16

CY17

CY18

Td. Val (US$mn) Mkt Vol (shrs mn)

Source: PSX

Defensive sectors outperformed

8%

2%

-1%

-5%

-8%

-9%

-9%

-10%

-14%

-18%

-20%

-23%

-37%

-41%

-50%-40%-30%-20%-10%

0%10%20%

Fert

ilize

r

Othe

rs

Text

ile

Bank

s

OMCs

Pow

er

Tele

com

Phar

ma.

Food E&

P

Gas U

tiliti

es

Cem

ent

Auto

s

Engi

neer

ing

Source: PSX

35,000

37,000

39,000

41,000

43,000

45,000

47,000

49,000

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18

Pakistan Market Timeline

Pak-US relations worsen

US acts on trade war

Monetary tightening begins / Fitch outlook turns negative

Senate elections2nd round of PKR depreciation

China responds on US tariffs

Amnesty scheme details announced

PML-N announces its last budget

US pulls out from Iran deal

Pak's weight stable in MSCI reblancing

Moody downgrades outlook

Nawaz Sharif sentenced to jail

PTI wins elections 3rd rate hike by US Fed

DR increased by 100bps

Gas price increased

Finance Minister states IMF is an option

Saudi Arabia announces FX support

UBL and LUCK downgraded to MSCI small cap

DR up by 150bps, cumulatively by 425bps

US China trade war truce

Fx support from UAE

Source: IMS Research

4 | P a g e

Pakistan Strategy 2019

2019 Strategy Synopsis

• Valuations are attractive: 2019f P/E of 7.4x is at a 13% discount to its cross-cycle average (since 2006) of 8.6x and a 40%+ discount from the peak of 12.0x+ at EM upgrade in mid-2017. With the bulk of the macroeconomic adjustment behind us, in our view, valuations appear to have room to expand rather than contract further.

• Headline earnings growth is resilient: The IMS Universe is projected to post 13%yoy growth in 2019f, concentrated in Banks and E&P. Earnings growth in 2020f is more inclusive and expected at 16%yoy. Even if valuation multiples fluctuate in a tight band, earnings growth has the potential to drive the market higher.

• Balance of Payment concerns are easing: We pencil in IMF program entry in 1Q 2019. Stabilization of fx reserves has already commenced due to bilateral assistance, and an IMF program will add both momentum and credibility to this exercise. Historically, rising fx reserves have acted as a strong catalyst for the market and the same can repeat in 2019.

• Foreign buying may return: Pakistan now appears attractive relative to other Emerging and Frontier market countries on (i) valuations, (ii) real interest rates, (iii) currency outlook and (iv) earnings growth. Lower oil prices are also a key positive. We believe there is a strong case for foreign buying in 2019, for the first time since 2014. It is possible that MSCI puts Pakistan on watch for downgrade to FM, but this may be taken as a positive by foreign investors.

• Domestic-driven theme: Pakistan has a limited connection to global headwinds on growth and trade, in our view. As Pakistan emerges out of its Balance of Payments issues – so often the key element of its boom and bust cycles - the market should depict a rebound even if global sentiment stays risk-off.

IMS Top Picks Mkt Cap Price TP Upside/ P/E (x) P/B (x) DY (%)

Top Picks (US$bn) (PKR/sh) (PKR/sh) downside 2019F 2020F 2019F 2020F 2019F 2020F UBL 1.16 131.6 180.0 37% 7.06 5.61 0.94 0.84 6.1% 7.6% HBL 1.30 123.5 175.0 42% 7.33 5.75 0.89 0.79 4.9% 6.5% BAFL 0.58 45.2 58.0 28% 5.65 5.30 0.93 0.83 6.6% 7.7% PPL 2.45 150.0 191.0 27% 6.08 5.67 1.22 1.10 4.7% 8.7% ENGRO 1.19 315.0 379.5 20% 7.55 5.68 0.79 0.68 9.2% 9.5% EFERT 0.69 72.2 89.0 23% 6.69 6.35 2.10 2.02 13.8% 13.8% LUCK 1.03 442.2 580.0 31% 9.91 9.38 1.18 1.07 2.8% 2.8% APL 0.32 450.0 606.0 35% 7.26 6.31 2.24 2.06 10.2% 12.0% HUBC 0.72 86.2 132.2 53% 7.68 4.77 2.00 1.45 5.8% 5.8% NPL 0.07 26.5 36.4 37% 2.34 2.11 0.48 0.42 7.5% 18.9% NML 0.34 135.4 180.0 33% 11.02 7.72 0.61 0.58 3.0% 5.2% INDU 0.68 1,200.0 1,580.0 32% 7.54 6.71 2.35 2.14 9.6% 10.8% Source: IMS Research

5 | P a g e

Pakistan Strategy 2019

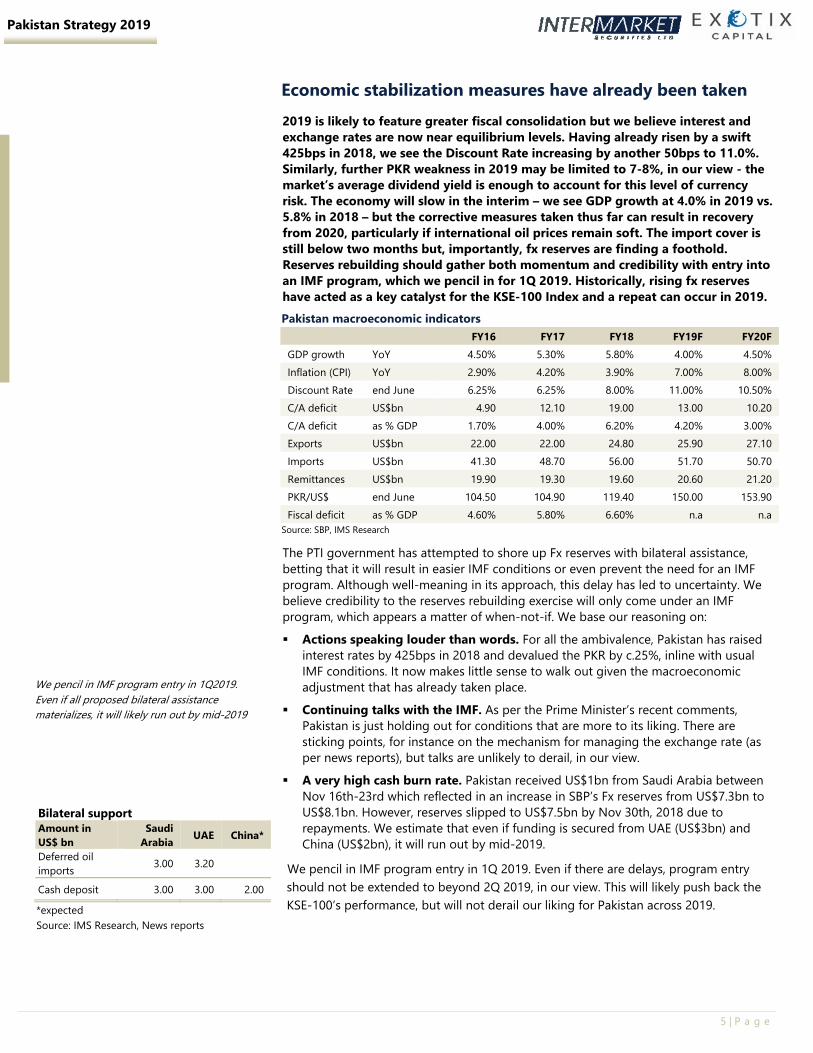

Economic stabilization measures have already been taken 2019 is likely to feature greater fiscal consolidation but we believe interest and exchange rates are now near equilibrium levels. Having already risen by a swift 425bps in 2018, we see the Discount Rate increasing by another 50bps to 11.0%. Similarly, further PKR weakness in 2019 may be limited to 7-8%, in our view - the market’s average dividend yield is enough to account for this level of currency risk. The economy will slow in the interim – we see GDP growth at 4.0% in 2019 vs. 5.8% in 2018 – but the corrective measures taken thus far can result in recovery from 2020, particularly if international oil prices remain soft. The import cover is still below two months but, importantly, fx reserves are finding a foothold. Reserves rebuilding should gather both momentum and credibility with entry into an IMF program, which we pencil in for 1Q 2019. Historically, rising fx reserves have acted as a key catalyst for the KSE-100 Index and a repeat can occur in 2019.

The PTI government has attempted to shore up Fx reserves with bilateral assistance, betting that it will result in easier IMF conditions or even prevent the need for an IMF program. Although well-meaning in its approach, this delay has led to uncertainty. We believe credibility to the reserves rebuilding exercise will only come under an IMF program, which appears a matter of when-not-if. We base our reasoning on: Actions speaking louder than words. For all the ambivalence, Pakistan has raised

interest rates by 425bps in 2018 and devalued the PKR by c.25%, inline with usual IMF conditions. It now makes little sense to walk out given the macroeconomic adjustment that has already taken place.

Continuing talks with the IMF. As per the Prime Minister’s recent comments, Pakistan is just holding out for conditions that are more to its liking. There are sticking points, for instance on the mechanism for managing the exchange rate (as per news reports), but talks are unlikely to derail, in our view.

A very high cash burn rate. Pakistan received US$1bn from Saudi Arabia between Nov 16th-23rd which reflected in an increase in SBP’s Fx reserves from US$7.3bn to US$8.1bn. However, reserves slipped to US$7.5bn by Nov 30th, 2018 due to repayments. We estimate that even if funding is secured from UAE (US$3bn) and China (US$2bn), it will run out by mid-2019.

We pencil in IMF program entry in 1Q 2019. Even if there are delays, program entry should not be extended to beyond 2Q 2019, in our view. This will likely push back the KSE-100’s performance, but will not derail our liking for Pakistan across 2019.

Pakistan macroeconomic indicators FY16 FY17 FY18 FY19F FY20F

GDP growth YoY 4.50% 5.30% 5.80% 4.00% 4.50% Inflation (CPI) YoY 2.90% 4.20% 3.90% 7.00% 8.00% Discount Rate end June 6.25% 6.25% 8.00% 11.00% 10.50% C/A deficit US$bn 4.90 12.10 19.00 13.00 10.20 C/A deficit as % GDP 1.70% 4.00% 6.20% 4.20% 3.00% Exports US$bn 22.00 22.00 24.80 25.90 27.10 Imports US$bn 41.30 48.70 56.00 51.70 50.70 Remittances US$bn 19.90 19.30 19.60 20.60 21.20 PKR/US$ end June 104.50 104.90 119.40 150.00 153.90 Fiscal deficit as % GDP 4.60% 5.80% 6.60% n.a n.a

Source: SBP, IMS Research

We pencil in IMF program entry in 1Q2019. Even if all proposed bilateral assistance materializes, it will likely run out by mid-2019

Bilateral support Amount in US$ bn

Saudi Arabia UAE China*

Deferred oil imports 3.00 3.20

Cash deposit 3.00 3.00 2.00

*expected Source: IMS Research, News reports

6 | P a g e

Pakistan Strategy 2019

A sustainable Fx reserves buildup is a key catalyst Since the 1990s, Pakistan has faced a Balance of Payments crisis with predictable regularity, typically coinciding with political transitions. The only prolonged stretch without an IMF program was across the Musharraf era; since then a change in government has always ended in an IMF program, be it in 2008, 2013 or, as we now anticipate, in 2019. This is because of weak buffers, particularly on Fx reserves - on average Pakistan has maintained an import cover of just six months (peak of ten months). If a shock occurs or if political expediency takes precedence around elections, Fx reserves quickly plummet to alarming levels. When this happens, the KSE-100 also follows suit.

This cuts both ways though. As Fx reserves begin to rebuild, the equity market also starts to perform. If an IMF program is taken, as is likely, it will unlock greater funds from other multilateral lenders such as the World Bank, and also make it easier for Pakistan to issue fresh bonds. There may be question marks on timing but a reserves buildup in 2019, is very likely, in our view. As in past instances, this will be a key catalyst for the Pakistan market. Over the medium-term, there is a need to build fx reserves through structural reforms for instance by (i) reducing the trade deficit, (ii) focusing on increasing official remittances and (iii) encouraging FDI. In the near-term however, an inflection point in fx reserves will likely imply the same for the equity market.

Large adjustments to interest and exchange rates are behind us The Discount Rate rose by 425bps to 10.5% in 2018 while the PKR’s devaluation vs. the US$ in this cycle stands at c.25%. These are large moves by any standard and we believe further adjustments on these fronts are likely to be modest. We see the Discount Rate peaking at 11.0% in 2019. This is due to: • Deeply positive real interest rates. IMF’s average CPI forecast of 7.5% for 2019

implies real interest rates are at 3%. Even going by core inflation, real interest rates are at 2%.

• Softer oil prices that are easing inflationary pressures. CPI jumped from 5.1% in Sep’18 to 6.8% in Oct’18 before easing to 6.2% in Dec’18.

• Benign outlook for food inflation which has a c 35% weight in the CPI basket. Even if non-food inflation is higher (House Rent, Education, Health and Clothing - combined 36% weight in CPI - are all growing by 1-2ppt more than their long-term rate), the outlook for overall CPI is moderate.

Fx reserves vs. the KSE-100

0

10,000

20,000

30,000

40,000

50,000

60,000

-

5,000

10,000

15,000

20,000

Jan-

01

May

-02

Oct-0

3

Feb-

05

Jul-0

6

Nov-

07

Apr-0

9

Aug-

10

Jan-

12

Jun-

13

Oct-1

4

Mar

-16

Jul-1

7

Dec-

18

SBP Reserves (USD 'Mn) KSE100 Index - Rhs

Source: SBP, IMS Research

A sustainable rise in fx reserves will trigger market performance

7 | P a g e

Pakistan Strategy 2019

Similarly, we expect further PKR weakness this year to be limited to a modest 5%-7%. This is due to: • Significant improvement in the REER, which stood at 104 in Dec’18 vs. 124 in

Nov’17. The PKR’s c.25% devaluation since mid-Dec’17 has also made up for the managed rates during the PML-N term as the PKR is now back on its long-term average depreciation run rate vs. the US$ (c 7%pa).

• Fx reserves finding a foothold. The import cover is estimated at a c 1.7 months but should not fall further in our view, given expectations of assistance from UAE (US$3bn) and China (US$2bn). Sustainable fx reserves buildup is unlikely to happen without an IMF program, but there appears to be a floor on reserves.

• Improving current account: The CA deficit averaged US$1.6bn per month in FY18. It has averaged US$1.2bn per month in 5MFY19 and the monthly run rate is likely to fall below US$1bn due to the benefit of deferred oil payments, falling commodity prices and lower non-essential imports (e.g. machinery imports are reducing as early-stage CPEC projects are mostly complete).

Preemptive monetary tightening…

-

4.0

8.0

12.0

16.0

20.0

Jan-

10M

ay-1

0Se

p-10

Feb-

11Ju

n-11

Nov

-11

Mar

-12

Aug-

12De

c-12

Apr-

13Se

p-13

Jan-

14Ju

n-14

Oct

-14

Mar

-15

Jul-1

5De

c-15

Apr-

16Au

g-16

Jan-

17M

ay-1

7O

ct-1

7Fe

b-18

Jul-1

8N

ov-1

8

(%)

DR CPI

Source: SBP

…has led to positive real interest rates

(4.0)

(2.0)

-

2.0

4.0

6.0

8.0

Dec-

09Ju

n-10

Dec-

10Ju

n-11

Dec-

11

Jun-

12De

c-12

Jun-

13De

c-13

Jun-

14

Dec-

14Ju

n-15

Dec-

15Ju

n-16

Dec-

16Ju

n-17

Dec-

17

Jun-

18De

c-18

(%)

against Core against CPI Avg. Core Avg. CPI

Source: SBP

SBP Reserves vs. PKR

40.0

60.0

80.0

100.0

120.0

140.0

160.0

-

5,000

10,000

15,000

20,000

Jan-

01

Jun-

02

Dec-

03

Jun-

05

Dec-

06

Jun-

08

Dec-

09

Jun-

11

Dec-

12

Jun-

14

Dec-

15

Jun-

17

Nov-

18

FX Reserves (USD 'Mn) PKR/US$ - Rhs

Source: SBP

REER is now close to 100

90

100

110

120

130

140

150

Jul-1

4Se

p-14

Nov-

14Ja

n-15

Mar

-15

May

-15

Jul-1

5Se

p-15

Nov-

15Ja

n-16

Mar

-16

May

-16

Jul-1

6Se

p-16

Nov-

16Ja

n-17

Mar

-17

May

-17

Jul-1

7Se

p-17

Nov-

17Ja

n-18

Mar

-18

May

-18

Jul-1

8Se

p-18

Nov-

18

REER PKR-US$

Source: SBP

8 | P a g e

Pakistan Strategy 2019

More is needed on the fiscal side We believe that much of the monetary tightening and exchange rate adjustment has already completed but more needs to be done on the fiscal side. The fiscal deficit stood at a high 6.6% of GDP in FY18 and, while there is some improvement, the 1QFY19 deficit is also a high 1.4% of GDP. We see more emphasis on revenue generation across 2019 but it is possible that spending – both discretionary as well as developmental – also comes in for cuts. Possible revenue raising measures for 2019 could include: • Increasing GST (current rate is 17%) and removing GST exemptions on petroleum

products, tractors, agricultural machinery and urea. • Reinstating taxes on cellular services, subject to Supreme Court approval. This may

lift annual revenue by up to 0.3% of GDP. • Enhancing FED, possibly on Cements. This has been increased for the last few years

and currently stands at US$11/ton. • Further increase in energy tariffs; Circular debt of PKR750bn (2% of GDP) still

remains an issue and the recent increase in electricity prices will not address it completely.

• Further raising import duties. This can include raising custom duties on imports or hiking regulatory duties on imports deemed non-essential. More than 40% of FBR revenues already comes from the import stage.

• Pushing provinces to raise taxation on services they provide. In the medium-term, there is a need to revisit the distribution of the federal revenue pool to provinces (57.5% at present, which is arguably too high) but it appears unlikely for 2019, especially as PTI does not have a majority in the Senate.

• Potentially increasing the corporate sector tax rate or freezing at current rate. For companies other than banks, it stands at 29% currently, down from 35% in 2013 and will be lowered by 1% annually to 25%.

Possible cuts to spending in 2019 could emanate from: • PSDP cuts. Total public sector development spending (federal + provinces) is

budgeted at PKR725bn or 2% of GDP. It is possible that this figure comes in for downward revision.

• Making some cuts to current expenditures even as we flag that it is difficult to adjust chunky debt servicing and the defense budget.

• Stricter cost control at the provincial level to achieve surpluses. Other than Sindh, all provinces are under the PTI.

Fiscal deficit to GDP (%)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18Fiscal Deficit to GDP (%)

Source: IMS Research, SBP

The thrust of a new IMF program could be on fiscal consolidation. Government is expected to announce another mini-budget soon.

9 | P a g e

Pakistan Strategy 2019

Growth will slow in 2019 but a quick rebound is not impossible From 5.8% in 2018, real GDP growth is likely to reduce to 4.0% or lower in 2019. This deceleration is likely to be driven by the Manufacturing sector where a slowdown is already visible in key LSM sectors such as Iron & Steel, Food, Pharmaceuticals and Automobiles. This is corroborated by prior Balance of Payment crises - which necessitated measures to cool the economy and eventually concluded with entry into an IMF program. The first years of an IMF program are the most difficult, before a rebound sets in and picks pace. In this case, while the economy looks weak for 2019, corrective measures are largely in place and can result in a rebound from 2020. While we expect modest GDP growth of 4.5% in 2020, factors that could result in a V-shaped recovery include: • Continued softness in international oil prices where Pakistan is a large oil importer

(crude and refined products constitute c.25% of the import bill). Quick progress on structural reforms such as (i) curtailing the trade deficit, (ii) clamping down on informal channels for remittances and (iii) attracting FDI, will also help.

• A successful reversal in inflation trajectory which may lead to an earlier than expected commencement in monetary easing. Our base-case is that interest rates will begin to gradually reduce in 2020.

• Emergence of fiscal space that could allow the government to embark on construction projections such as the Prime Minister's low cost housing scheme and mega dams. Linkages to multiple sectors can drive GDP growth higher, similar to the PML-N government.

GDP growth to recover from 2020f

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2012 2013 2014 2015 2016 2017 2018 2019f 2020f

GDP Growth (%) Source: IMS Research, SBP

10 | P a g e

Pakistan Strategy 2019

Pakistan is standing out against peers Given that the adjustment to interest and exchange rates has been among the swiftest in the Emerging and Frontier universe, Pakistan appears ahead of the curve relative to peers that are in the early stages of their own course corrections. Real interest rates in Pakistan are +3.0% vs. a median of +1.1% for EM and FM markets. Similarly, the PKR’s rapid devaluation in 2018 – the most after Argentina and Turkey – has brought the REER down to 104 vs. 124 in Nov’17. Pakistan’s domestic-driven economy (exports are a limited 7% of GDP vs. a median of 20% for peers) can potentially also stand out in a global environment facing challenges to growth and trade. While we flag risks to Pakistan’s EM status – it could be put on watch for downgrade to FM – this may arguably be taken as a positive by investors. A combination of corrective macroeconomic measures (that have already taken place) and cheap valuations can also attract foreign buying, for the first time since 2014, especially if an IMF program comes through.

Real interest rates are among the highest

-1.3

%

-0.3

%-0

.1% 0.5% 0.6% 0.7% 1.0% 1.1% 1.

5% 1.6% 2.

2% 2.3%

2.3% 2.4% 2.8% 3.0% 3.3% 3.4%

7.3%

-2%

0%

2%

4%

6%

8%

Pola

ndCh

ileBa

ngla

desh

Nige

riaTh

aila

ndPe

ruM

alay

siaM

oroc

coSo

uth

Afric

aIn

dia

Indo

nesia

Viet

nam

Braz

ilRu

ssia

Egyp

tPa

kist

anSr

i Lan

kaKe

nya

Turk

ey

Source: Bloomberg, IMS Research

Bulk of PKR devaluation is behind us

1.3%

0.1%

0.0%

-0.6

%

-0.7

%

-2.1

%

-2.1

%

-2.4

%

-4.1

%

-5.1

%

-5.7

%

-8.5

%

-14.

6%

-16.

1%

-17.

9%

-20.

5%

-28.

2%

-50.

6%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

Keny

aTh

aila

nd UAE

Egyp

tNi

geria

Viet

nam

Mal

aysia

Mor

occo

S. K

orea

Phili

ppin

esIn

done

siaIn

dia

Braz

ilSr

i Lan

kaTu

nisia

Paki

stan

Turk

eyAr

gent

ina

2018 Currency performance

Source: Bloomberg

The SBP increased the DR by 425bps to 10.5% in 2018. Based on IMF’s projected CPI of 7.5% in 2019, real interest rates in Pakistan are +3.0%, one of the highest in the EM & FM space.

The PKR depreciated by 20%+ vs. the US$ in 2018, one of the highest among peers. With rebuilding of fx reserves underway, further PKR slippage is likely to be modest in our view.

Less exposed to global trade headwinds

5.9% 7.1%

7.9% 9.1% 10.1

%11

.1%

11.3

%11

.5%

14.6

%15

.8%

17.8

%20

.1%

20.3

%20

.4%

21.1

%24

.9% 38

.1%

43.5

%50

.5%

80.4

%

0%

20%

40%

60%

80%

100%

Keny

aPa

kist

anEg

ypt

Nige

riaIn

dia

Sri L

anka

Braz

ilBa

ngla

desh

Arge

ntin

aIn

done

siaPe

ruM

oroc

coSo

uth

Afric

aRu

ssia

Chile

Turk

eyPo

land

Thai

land

Mal

aysia

Viet

nam

Source: World Bank, IMS Research

Soft oil prices are a positive

0.1%

1.2%

2.2% 2.3% 2.5%

2.5% 2.7% 2.

9% 3.0% 3.1% 3.

4% 3.8% 4.

2%

5.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Russ

ia

Arge

ntin

a

Nige

ria

Peru

Turk

ey

Indo

nesia

Pola

nd

Chile

Egyp

t

Sout

h Af

rica

Sri L

anka

Paki

stan

Indi

a

Mal

aysia

Source: World Bank, IMS Research

Pakistan’s Exports to GDP is 7% vs. a 20% median for peers. Exports need to grow and diversify but, given near-term headwinds, low exposure to global trade can enable Pakistan to stand out in 2019.

Fuel imports are c.4% of Pakistan’s GDP. If oil prices continue to tread lower, in keeping with the “lower for longer” outlook, Pakistan will likely be a key beneficiary.

11 | P a g e

Pakistan Strategy 2019

Looking good to attract foreign buying Pakistan is standing out relative to other Emerging and Frontier markets, in terms of both valuations and the pace with which it has adjusted interest and exchange rates. Pakistan has seen foreign selling of US$1.7bn over 2015-18 (US$537mn in 2018 alone) but we think foreigners can turn net buyers in 2019, for the first time since 2014. This foreign buying is likely to be led by returning frontier market fund managers, in our view. Foreigners recorded gross sell of US$534mn on the EM upgrade day, money that has yet to flow back into Pakistan. These were mostly active FM funds that may now find Pakistan again to their liking. Pakistan stands out due to: • Better placed relative to peers: Pakistan’s macroeconomic adjustment began

twelve months ago and appears to be largely complete. Real interest rates are among the highest in the EM and FM space, and only Argentina and Turkey have seen sharper currency devaluation in 2018. Limited exposure to global trade headwinds and softer oil prices support Pakistan’s case.

• Attractive valuations and a strong bottom-up argument: Pakistan trades at a 30% discount to the MSCI EM Index. The discount to its own cross-cycle valuation averages stands at 13%. The earnings growth on offer – 13% and 16% in 2019 and 2020, respectively – is higher than 6% and 14% growth in the MSCI EM and FM spaces. Pakistan also offers the highest dividend yield in the region, enough to cover for any further PKR weakness, in our view.

The valuation set is attractive

RussiaTurkey UAE

PakistanChinaHungary

Colombia

MSCI EMPoland

Brazil

Czech Republic

Taiwan PeruMexico

South Africa QatarThailand

Greece

IndonesiaMalaysia Philippines

India

-

5.0

10.0

15.0

20.0

25.0

-4.0% 0.0% 4.0% 8.0% 12.0% 16.0% 20.0% 24.0%

P/E

(x) 2

019f

EPS Growth 2019f (%) Source: Bloomberg

Dividend yield is very high – 2019f 1.

5% 1.7% 2.

5%2.

4% 2.9% 3.0%

3.0% 3.2% 3.3% 3.5%

3.4% 3.5%

3.4%

3.4% 4.

2%4.

1% 4.3%

4.3% 5.

1% 5.3% 5.5% 6.

2% 7.2%

0%1%2%3%4%5%6%7%8%

Indi

aPh

ilipp

ines

Kore

aIn

done

siaHu

ngar

yCh

ilePe

ruM

exico

Gree

ceCh

ina

MSC

I EM

Thai

land

Pola

ndM

alay

siaSo

uth

Afric

aBr

azil

Qata

rCo

lom

bia

Taiw

anCz

ech…

Turk

eyUA

EPa

kist

an

Source: Bloomberg

Pakistan’s offers a better risk-reward Dividend yield provides downside protection

Discount to EM can contract

-50%

-45%

-40%

-35%

-30%

-25%

-20%

-15%

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

f

Disc. to EM Source: Bloomberg

There is room to stock up on Pakistan

15%

20%

25%

30%

35%

40%

Jul-0

7Ja

n-08

Jul-0

8Ja

n-09

Aug-

09Fe

b-10

Aug-

10Fe

b-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Oct-1

3Ap

r-14

Oct-1

4Ap

r-15

Nov-

15M

ay-1

6No

v-16

May

-17

Nov-

17Ju

n-18

Dec-

18

Securities held by Foreigners (as % of F.MCAP (All Share) Mean

Source: SBP, IMS Research

Cheap on both standalone and relative basis It is now difficult to ignore Pakistan completely

12 | P a g e

Pakistan Strategy 2019

Possible downgrade to FM may act like an upgrade Pakistan was upgraded to the MSCI EM Index in mid-2017. At the time, six Pakistani stocks (OGDC, HBL, MCB, UBL, LUCK, ENGRO) were part of the Standard Index. Since then, UBL, LUCK and ENGRO have been downgraded to small cap status. Of the remaining companies in the Standard Index, HBL is currently below the minimum market capitalization criteria while all three of OGDC, MCB and HBL are below the required free float market capitalization. Even after imposing buffers (2/3rd of minimum levels), HBL appears vulnerable where a fall in its market price and/or rapid PKR depreciation from current levels could threaten a downgrade to small cap status. This, in turn, could imperil Pakistan’s EM status given that at least three companies have to meet Standard Index criteria at all times. If HBL fails to meet EM criteria, it is possible that Pakistan is put on watch for possible downgrade in the May 2019 MSCI Review. This usually lasts for twelve months and the earliest Pakistan can be downgraded to FM, in our view, is effective end-Nov’20. The previous two downgrades from EM to FM have been Morocco (2013; low liquidity + dynamics were more consistent with FM than EM) and Argentina (in 2009; capital controls). Similar to Morocco, Pakistan’s characteristics are arguably also more in line with frontier countries rather than the emerging market classification. However, downgrade to FM or even being put on watch for downgrade is not a given. Peru was put on watch for downgrade in 2015 but stayed in EM as regulators exempted CGT, eased trading restrictions/fee, and gave a medium-term year plan to boost volumes. In Pakistan’s case, since EM upgrade took place in 2017, MSCI may give it more time. Technical exemptions are possible even if less than three companies meet EM Standard Index criteria.

A downgrad

Downgrade to FM status would not be the worst outcome, in our view. From a negligible weight in EM, Pakistan would likely have a c.10% weight in the FM space particularly as Argentina will be upgraded to the EM space next year. Based on our interaction with both local and foreign institutional investors, eventual downgrade to FM may work out in Pakistan’s favor given its large size in the FM Index will make it impossible to ignore. In this case, a downgrade may actually play out as an upgrade.

MSCI Criteria A Economic Development Frontier Emerging

A.1 Sustainability of economics development No requirement No requirement

B Size and Liquidity Requirements B.1 Number Of Companies meeting the following Standard Index criteria 2 3

Company size (full market cap) USD 741 mm USD 1482 MM Security size (float market cap) USD 69 MM USD 741 mm

Security liquidity 2.5% ATVR 15% ATVR

HBL OGDC MCB Ord. Mkt Cap

(US$mn) Free float Mkt Cap (US$mn) Ord. Mkt Cap (US$mn) Free float Mkt Cap (US$mn) Ord. Mkt Cap

(US$mn) Free float Mkt Cap (US$mn)

1,304.2 652.1 4,024.4 603.7 1,609.1 563.2

C Market Accessibility Criteria Frontier Emerging C.1 Openness to foreign ownership At least some Significant C.2 Ease of capital inflows / outflows At least partial Significant C.3 Efficiency of the operational framework Modest Good And tested C.4 Competitive landscape High High C.5 Stability of the institutional framework Modest Modest

Source: IMS Research, MSCI

Even if EM criteria is not met, it may be too soon for downgrade to FM and Pakistan may receive technical exemptions if needed.

13 | P a g e

Pakistan Strategy 2019

Risk-reward is attractive Valuations are supportive – Pakistan trades at a 2019f P/E of 7.4x, the lowest since Nov’13, and at a 13% discount to its cross-cycle average (2006 till date) of 8.6x. On the basis of P/B and P/S, the discount is an even sharper 33% and 23%. Pakistan is among the cheapest markets in the Emerging and Frontier universe and also offers the 2nd highest dividend yield in this space. Despite the slower economy, headline earnings growth is resilient; the IMS Universe is projected to post growth of 13% in 2019f and 16% in 2020f. Although 2019 growth will primarily be driven by Banks and E&P, it will be more broad-based across the medium-term. We think that even if the market’s P/E remains confined to a tight band in 2019, the KSE-100 has the potential to rally towards 45,000pts (21% higher than the Index’s last close). This has precedence; range-bound valuations (average P/E of 6.3x) and strong earnings growth (22%pa) last occurred during CY09-12 when the KSE-100 returned a CAGR of more than 20%. Attractive levels for building positions Outliers aside, the Pakistan market has historically traded at a forward P/E range of 6x-12x. Significant de-rating has taken place over the last 18 months, with the forward P/E falling from more than 12.0x at MSCI upgrade (mid-2017) to 7.4x at present. Current valuations levels are 13% lower than the historical cross-cycle average of 8.6x; on the basis of P/B and P/S, the discount is an even sharper 33% and 23%, respectively. Given our view that the macroeconomic adjustment in Pakistan has largely taken place, we reason that it is already in the price and that valuations allow for positions to be built. The GDP-Earnings disconnect Over the last five years, despite the acceleration in GDP growth under the PML-N, earnings growth lost momentum. This is due to the composition of the KSE-100 Index where Banks and E&P together have a 40% weight. Lower oil prices leading to lower interest rates benefitted the economy but pressed down on earnings for both heavyweight sectors. With demand compression measures in place, 2019 will likely see a slower economy (and lower profitability for sectors such as Cements and Automobiles). However, headline earnings growth stands to improve, driven by Banks (higher interest rates) and E&P (weaker PKR). The GDP-profit growths disconnect should thus persist, particularly in the next 1-2 years.

Historical P/E band

3.0

6.0

9.0

12.0

15.0

Jul-0

6

Jun-

07

May

-08

May

-09

Apr-1

0

Apr-1

1

Mar

-12

Mar

-13

Feb-

14

Feb-

15

Jan-

16

Jan-

17

Dec-

17

Dec-

18

(X)

SD-2 SD-1 FWD-PER SD+1 SD+2 Mean

Source: IMS Research

Valuation discount to long-term average

FWD-

P/B (x) FWD-P/S

(x) FWD-

PER (x) L.T average 1.79 0.94 8.57 2019f 1.20 0.72 7.44 Disc. To L.t -33% -23% -13% Source: IMS Research

14 | P a g e

Pakistan Strategy 2019

Earnings growth can drive the market, even if valuations are range-bound With the Discount Rate coming down to a record low 6.25%, valuation rerating was the key market driver during the PML-N government, at least until ex-PM Nawaz Sharif’s disqualification. While valuation multiples may stay in a tight band, precedence suggests this is not prohibitive for market returns. Between end-CY09 and end-CY12 (under the PPP government), the KSE-100 delivered a CAGR of more than 20% despite the market’s P/E averaging just 6.3x (vs. a cross-cycle average of 8.6x). Earnings growth during this period averaged 22% per annum, despite below par GDP growth of 3.8%. A similar situation appears to be unfolding now. If interest rates remain in double-digits (the DR currently stands at 10.5%), significant valuation rerating may not take place. However, headline earnings growth can drive the market higher.

Banks to drive 2019 growth; more broad-based growth in 2020 For the IMS Universe, we expect 13%yoy earnings growth in 2019f and 16%yoy growth in 2020f. Banks will be the key growth drivers this year with margin expansion expected to more than offset higher cost of risk. The ex-banks growth for 2019f is a more moderate 5%yoy, with major drag coming from Automobiles and Cements. In 2020f, however, growth should be more inclusive. Banks will continue to do well and will be joined by a rebound in Cements, Steel and Oil Marketing – sectors that will reflect the expected improvement in the economy after the consolidation in 2019.

GDP growth vs. Earnings growth

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

-20%

-10%

0%

10%

20%

30%

40%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019f

IMS Universe Growth (%) GDP Growth (%) - Rhs

Source: IMS Research, SBP

Earnings growth to take precedence over valuation rerating

-80%-60%-40%-20%

0%20%40%60%80%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Earnings Growth (%) P/E expansion Index Return

Source: IMS Research

15 | P a g e

Pakistan Strategy 2019

KSE-100 can rally up to 45,000pts in 2019 The KSE-100 shed 8% in 2018 (-27% in US$ terms) and delivered a negative return for the second year in a row, which has not occurred since the mid-1990s. We think the Pakistan market will depict a rebound in 2019 on a combination of: (i) cheap valuations (7.4x forward P/E), (ii) easing Balance of Payment concerns, (iii) a quick adjustment in interest and exchange rates that places Pakistan ahead of other EM & FM countries, (iv) limited exposure to global trade headwinds, (v) softer oil prices and (vi) resilient headline earnings growth.

Although the economy will slow in 2019, we believe the improvement on the external side in particular can act as a major trigger. We think the KSE-100 has limited downside, while it can rally up to 45,000pts in 2019 (21.4% higher than 2018’s closing of 37,067pts). We base this on:

Index Target (pts) TP Mapping Analysts map their target prices on underlying companies of the KSE-100 45,000

E/Y vs. T-bill yield We assume that the differential reverts to long-term level of 2.9% 41,000 Target P/E We assign a target P/E of 8.5x vs. 7.4x at present 43,000

We would turn more bullish if: • It becomes clear that the IMF program will not face further inordinate delays • Regulatory policies turn more conducive especially on market leverage • New buyers such as local state-owned institutions or foreigners enter the market • There are signs that the macroeconomic environment can quickly turn for the

better

IMS Universe Sectors Earnings growth in 2019f and 2020f

-50%

-25%

0%

25%

50%

2019F 2020F Source: IMS Research

16 | P a g e

Pakistan Strategy 2019

Risks We think resorting to the IMF is inescapable, where we pencil in program entry in 1Q 2019. However, given that Pakistan is on course to receive bilateral assistance – which will temporarily lift Fx reserves - it is possible that the government continues to delay program entry. This will likely keep a lid on investor confidence and prevent foreign institutional money from flowing into Pakistan. We think the adjustments to the interest and exchange rates are largely complete. A large increase in interest rates and further sharp weakness in the PKR, over and above our estimates, would be a key downside risk particularly if it leads to an upward revision in the risk-free rate (currently assumed at 11.0%). This could potentially lead to the market’s P/E breaking below 7x. The thrust of macroeconomic adjustment in 2019 is likely to be on the fiscal side, particularly revenue generation. While not our base-case, it is possible that the government raises corporate income tax (currently 29% for companies and 35% for banks; ex-super tax). This would negatively affect our earnings estimates and reduce target prices. Double-digit interest rates have led to a shift of domestic liquidity from equities into fixed income where we understand the process is not yet complete. This was a key reason why local mutual funds were net sellers in 2018, albeit by a small quantum. If fresh inflows do not materialize – for instance from foreigners or from state owned institutions - weak liquidity dynamics could take the market lower. Global equity markets have been weak recently. Notwithstanding Pakistan’s domestic-driven economy, if global sentiment towards risk assets remains weak in 2019, it is possible that the KSE-100’s performance is also affected. Pakistan has to meet FATF conditions in 2019. Failure to do so may result in Pakistan being blacklisted which would be a significant negative. Security conditions have significantly improved over the last few years. However, with the US looking to withdraw from Afghanistan, it is possible that security conditions in Pakistan are adversely affected. That said, a more conciliatory stance by the US is a positive development.

17 | P a g e

Pakistan Strategy 2019

Sector Outlook

18 | P a g e

Pakistan Strategy 2019

Banks

Back on the growth track Margin expansion to drive profitability: The full effect of the 425bps

increase in interest rates in 2018 will be visible in 2019f. We see NIMs expanding by 40-104bps across our coverage universe (MEBL and BAFL are most sensitive). Even though loan growth is expected to decelerate from 11%yoy in 2018 to 8%yoy in 2019, rising margins will drive c 45% profit growth in 2019f (c 35% ex-HBL). Increasing yields on PIBs – 10yr paper in the last auction yielded more than 13% - is an upside risk.

Cost of risk should be manageable: Cost of risk will rise but should remain within manageable limits in our view (50-60bps). This is due to (i) high provisioning coverage of c 90%, (ii) limited consumer exposure (7% of the loan mix) and (iii) loans to the public sector (government guaranteed) having a c 20% share in total loans.

2018 bad news unlikely to repeat: This will be particularly positive for the large banks. Pension fund top-ups are over, UBL’s loan book cleanup in the GCC is nearly complete and HBL’s profitability should also begin to return to normalcy.

ROEs to enter secular expansion phase: ROEs for the banks we cover will rise by 4ppt to 14.0% in 2019f. Even if interest rates come off over the medium term, ROEs should retain their upward trajectory and cross 18% by 2022f. This should help rerate valuations where the sector trades at a median 2019f P/B of 1.0x and P/E of 7.5x.

Risks: (i) Major asset quality deterioration, (ii) fines on the US operations of HBL & UBL, (iii) FATF blacklisting, and (iv) IFRS 9 implementation.

Banks to see rapid margin expansion in 2019

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17 CY18F CY19F

Source: IMS Research

Valuations have room to expand, particularly for the big banks

Jan-

08

Feb-

09

Mar

-10

Apr-1

1

May

-12

Jun-

13

Jul-1

4

Aug-

15

Sep-

16

Oct-1

7

Dec-

18

(x)IMS Universe Banks Pbv (x) Band

2.00

1.50

1.00

0.50

Source: IMS Research

TP Upside P/E (x) P/B (x) DY (%) (PKR) (%) 19F 20F 19F 20F 19F

Banks 7.6 6.2 1.1 1.0 6.5% ABL 118 11% 7.9 6.9 1.1 1.0 7.5% MCB 210 11% 9.6 7.3 1.4 1.3 8.5% HBL 175 42% 7.3 5.8 0.9 0.8 4.9% UBL 180 37% 7.1 5.6 0.9 0.8 6.1% BAFL 58 28% 5.6 5.3 0.9 0.8 6.6% MEBL 107 19% 7.6 6.4 1.9 1.6 4.5%

Sector performance

-20%

-10%

0%

10%

20%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS Banks Uni. Source: IMS Research

Raza Jafri, CFA [email protected] Yusra Beg [email protected]

19 | P a g e

Pakistan Strategy 2019

Cheap valuations but triggers ahead Significant undervaluation: Oil prices fell 17% during 2018 and E&P

stocks fell 19%, but this is more than warranted given low sensitivity to oil prices in case of OGDC and PPL. The two stocks are trading at an EV/EBITDA of just 2.5x and we estimate their stock prices imply oil prices of US$25/32 per barrel. Triggers during 2019 include (i) high-potential off-shore drilling and (ii) potentially, progress on a new Petroleum Policy.

PKR devaluation will drive earnings growth: Earnings growth in the sector will be a handsome 20% yoy on average, led mostly by PKR depreciation, as well as production growth in case of PPL. E&Ps are deploying a significant portion of their capex on mature fields to plateau production levels. PPL is slightly better because it is able to meaningfully grow production in large old fields like Kandkhot and Adhi.

New entrants to intensify competition: Exploration is key for future production growth. We think the opportunity in Khyber Pakhtunkhwa and Baluchistan still remains untapped and can be capitalized on in future. Most importantly, Pakistan’s second offshore well will commence drilling in Jan’19 in Indus G block, which promises large gas reserves. On the other hand, the government may mull upgrading the Petroleum Policy to encourage greater risk taking in the sector.

Risks: Key risk is oil prices which can further depress sentiment in the sector. Continued divestment by foreign investors in OGDC and PPL could keep these stocks under pressure. Furnace oil phase out will intermittently disrupt the energy chain and cut production.

E&Ps

Sector performance

-30%-20%-10%

0%10%20%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS E&P Uni.

Source: IMS Research

Oil price outlook is “lower for longer” again

41 48

62 60 60 65

-

10

20

30

40

50

60

70

FY16 FY17 FY18 FY19f FY20f FY21f

US$/bbl

Source: IMS Research, Bloomberg

Implied oil prices suggest significant undervaluation

2532

48

0

10

20

30

40

50

60

OGDC PPL POL

US$/bbl

Current oil price

Source: Bloomberg, IMS Research

Muhammad Saad Ali, CFA [email protected]

TP Upside P/E (x) P/B (x) DY (%) (PKR) (%) 19F 20F 19F 20F 19F

E&P 6.3 5.9 1.1 1.0 7.8% OGDC 175 35% 6.0 5.7 0.9 0.9 9.2% PPL 191 27% 6.1 5.7 1.2 1.1 4.7% POL 497 16% 9.5 8.0 3.7 3.6 10.0%

20 | P a g e

Pakistan Strategy 2019

Sector performance

-20%-10%

0%10%20%30%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS Fertilizer Uni. Source: IMS Research

Risk-reward in balance High retention prices may continue: The IMS Fertilizer Universe

outperformed the KSE-100 by 18% in 2018 due to improved pricing power. Urea inventory declined to 245K tons (down 86% since the May’17 peak) and subsidy removal in May’18 lifted retention prices. Given fiscal constraints, we foresee limited risk of subsidies in 2019, which may be earnings positive for the sector.

Risks to weigh on price performance: In 2019, risks of further gas price hike and/or GIDC removal may keep the sector’s price performance in check. The recent 10%-143% gas price hike raised PKR90bn, short of the initial target of PKR150bn. Pricing power in case of another gas price hike may be limited especially if demand supply dynamics become unfavorable (allocation of gas to FATIMA for year-round production and/or further urea imports). Our estimates only incorporate 50% (PKR60/bag) of the recent gas price hike pass-on in Urea prices, to reflect the aforementioned risks.

We like selected names: ENGRO is our top pick where we like its diversified exposure to fertilizer, power, consumer, and chemical sectors. ENGRO’s cash position of PKR62bn is a major potential upside trigger, if deployed in new investment avenues. In the event of further gas price hikes, companies with concessionary gas pricing (EFERT and FATIMA) may outperform.

Risks: (i) Subsidy on fertilizers, (ii) GIDC removal (iii) further gas price hikes and (iv) lower pricing power.

Recovery in Urea prices amid lower inventory

0

400

800

1,200

1,600

2,000

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep-

17

Nov-

17

Jan-

18

Mar

-18

May

-18

Jul-1

8

Sep-

18

Nov-

18

1,200 1,300 1,400 1,500 1,600 1,700 1,800 PKR/kgK tons

Urea Prices (PKR/Kg)- Rhs Urea Inventory (K tons) Source: NFDC, IMS Research

GMs have improved as a result

15%

18%

21%

24%

27%

30%

33%

800900

1,0001,1001,2001,3001,4001,5001,6001,700

2QCY17 3QCY17 4QCY17 1QCY18 2QCY18 3QCY18

Urea Prices FFC GMs (%) - Rhs Source: IMS Research, Company Accounts

Fertilizer Ailia Naeem [email protected]

TP Upside P/E (x) P/B (x) DY (%) (PKR) (%) 19F 20F 19F 20F 19F

Fertilizer 7.4 6.4 1.3 1.2 10.1% FFC 106 13% 8.4 7.8 3.6 3.5 10.7% EFERT 89 23% 6.7 6.4 2.1 2.0 13.8% FFBL 36 -1% 32.1 21.1 2.4 2.3 4.7% FATIMA 39 12% 5.0 4.7 1.1 1.0 8.7% ENGRO 379 20% 7.6 5.7 0.8 0.7 9.2%

21 | P a g e

Pakistan Strategy 2019

Cement

Stay selective Concerns on local demand growth: Deceleration in local demand seems

likely amidst an unfavorable macro environment. Local demand in 5MFY19 is down 4% yoy, where work on large private schemes in Karachi has reportedly been stopped after the Supreme Court’s crackdown against private scheme patrons. This can play a key role in decelerating private sector led demand, in our view. Furthermore, constrained fiscal space may limit the scale of PSDP spending.

Export growth is a much needed outlet: A positive sign, especially for the South players is the significant rise in sea exports, propelled by c.25% weaker PKR and slowing local demand. The significance of exports lies in managing the supply in the local market. With fresh sanctions on Iran, Pakistan can tap regional export markets.

More expansions are nigh: Next round of capacity expansions (CHCC and MLCF) will come online in 4QFY19. From the listed space, PIOC, LUCK and KOHC are next in-line to bring their respective expansions online. Rising cost of production has helped sustain pricing discipline. Though margin compression has stalled price declines, the industry’s true pricing power will be tested when upcoming expansions are online.

Risks: (i) Replay of pricing discounts by CHCC when its Line 3 is commissioned, (ii) further PKR depreciation and increase in coal prices, (iii) GoP levying more taxes on the sector. Upside risks include: (i) decline in coal prices amid global slowdown and US-China trade war, and (ii) commencement of Naya Pakistan Scheme and/or construction of mega dams.

Sector performance

-40%

-20%

0%

20%

40%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS Cement Uni.

Source: IMS Research

Industry utilization rate expected to remain above 70% until FY21

0%

20%

40%

60%

80%

100%

120%

-

10

20

30

40

50

60

70

FY13 FY14 FY15 FY16 FY17 FY18 FY19f FY20f FY21f

mn tons

Local Exports Utilization-Rhs Source: Company Accounts, APCMA

Margin compression has dissuaded price competition

2832

3633

2521 20 19

0

5

10

15

20

25

30

35

40

FY14 FY15 FY16 FY17 FY18 FY19F FY20F FY21FEBITDA Margin

%

Source: Company Accounts, IMS Research

Muhammad Saad Ali, CFA [email protected]

TP Upside P/E (x) P/B (x) DY (%) (PKR) (%) 19F 20F 19F 20F 19F

Cement 9.1 7.7 0.9 0.8 4.6% DGKC 112 36% 12.1 9.8 0.4 0.4 3.9% LUCK 580 31% 9.9 9.4 1.2 1.1 2.8% MLCF 56 31% 6.3 4.0 0.8 0.7 7.0% CHCC 91 26% 7.4 6.4 1.0 0.9 5.6% FCCL 21 0% 8.2 8.6 1.4 1.3 9.5% ACPL 127 19% 9.2 7.4 0.8 0.8 7.5% KOHC 115 38% 7.5 4.7 0.9 0.8 5.4%

22 | P a g e

Pakistan Strategy 2019

OMCs

Tough period ahead Growth period is behind us: After four years of strong sales growth –

propelled by declining prices and a growing economy – OMCs are bracing for negative demand in 2019, and potentially slow recovery thereafter. Petrol and HSD volumes have declined by 1% and 21% yoy respectively, in 1HFY19. Amidst the recent slide in international crude oil prices, the GoP is likely to contain the decline in local prices to maintain its tax revenues.

Competition among incumbents will increase: Falling oil prices fueled discounting by smaller players such as HASCOL to gain market share. This will increase competition, particularly for PSO. APL and HASCOL may benefit from increased storages, while SHEL has regained much of its market share. We think the government will not table deregulation of OMC margins in 2019 given macroeconomic concerns. Deregulation will be negative for competition in a slowing demand scenario.

Sukuk issue for circular debt resolution: A key event could be the government raising PKR200-300bn from Islamic banks for partial resolution of outstanding balance of circular debt. While it will be a major positive for PSO, we advocate exiting the position in case of a rally, as we are not optimistic about its ability to contain market share loss.

Risks: (i) GoP allocating more LNG to the CNG sector, at subsidized rates (probable if oil prices fall further or LNG offtake becomes problematic) and, (ii) deregulation on OMC margins as it will lead to unhealthy competition, in our view. Upside risks include: (i) demand recovering stronger than expected, and (ii) sector ramps up payouts given lack of growth opportunity.

Sector performance

-20%-10%

0%10%20%30%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS OMCs Uni.

Source: IMS Research

OMCs sales on a decline

9.09.6

7.4

4.2 3.92.9

7.88.5 9.0

7.7 7.4 7.6

5.86.6

7.4 7.78.1 8.6

-

2

4

6

8

10

FY16 FY17 FY18 FY19f FY20f FY21f

mn tons

FO HSD MS Source: OCAC, IMS Research

OMCs market share; smaller OMCs growing against PSO

0%

20%

40%

60%

80%

100%

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

4Q18

1Q19

PSO SHEL APL HASCOL Others Source: OCAC, IMS Research

Muhammad Saad Ali, CFA [email protected]

TP Upside P/E (x) P/B (x) DY (%) (PKR) (%) 19F 20F 19F 20F 19F

OMCs 8.2 6.8 1.1 1.1 6.4% PSO 255 12% 7.4 6.3 0.7 0.7 4.8% APL 606 35% 7.3 6.3 2.2 2.1 10.2% HASCOL 161 13% 14.2 9.1 2.1 1.9 4.2% SHEL 289 4% 10.0 7.7 2.5 2.4 7.6%

23 | P a g e

Pakistan Strategy 2019

Power

Expansion projects & circular debt settlement Circular debt settlement on the cards: The government is reportedly

planning to issue Sukuk Energy Bonds amounting to PKR200bn initially, in early 2019. The money will likely be used to clear some portion of the outstanding circular debt (reportedly over PKR600bn). We believe the beneficiary companies will immediately deleverage as much as possible (earnings positive) and potentially resume stalled payouts (NPL, NCPL).

Pure D/Y plays may lag behind… For large payouts, we believe a greater than PKR200bn settlement will be needed. The sector’s earnings will rise but dividends need significantly improved cash flow. The average FY19F D/Y of the IMS Power Universe (ex-KAPCO), is c350bps lower than current 3yr PIB rate of 12.2%. As a result, investors looking for just dividends may not find current share prices to their liking.

…but growth projects to bring select names in limelight: There is more excitement on expansion projects (early harvest projects of CPEC), which may bring names such as HUBC into the limelight. While high debt resulting from project financing may keep bottomline growth in check for HUBC in 2019 (425bps higher interest rates), investor focus on earnings growth in the medium term can drive price performance.

Risks: (i) Delay in commissioning of upcoming power projects of IPPs under coverage, (ii) delay in materialization of Energy Sector Sukuks, and (iii) reemergence of circular debt if structural issues remain unresolved.

Sector performance

-20%

-10%

0%

10%

20%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS Power Uni. Source: IMS Research

Trade Debts have been on a rising trend since 2013 settlement

243

72

168 162 162

194238

0%

20%

40%

60%

80%

100%

120%

0

50

100

150

200

250

300

FY12 FY13 FY14 FY15 FY16 FY17 FY18

Trade Debts - IMS Universe IPPs (PKRbn) As % of Sales - Rhs

Source: Company Accounts

Cash payouts have started feeling the pinch

1

6

12

17

23

28

FY12 FY13 FY14 FY15 FY16 FY17 FY18

NCPL NPL HUBC KAPCO

(%)

Source: Company Accounts

Ailia Naeem [email protected]

TP Upside P/E (x) P/B (x) DY (%) (PKR) (%) 19F 20F 19F 20F 19F

Power 5.2 3.9 1.3 1.1 10.2% NPL 36 37% 2.3 2.1 0.5 0.4 7.5% HUBC 132 53% 7.7 4.8 2.0 1.5 5.8% KAPCO 53 7% 4.1 3.7 1.2 1.1 20.2% NCPL 29 24% 2.3 2.1 0.6 0.5 12.8%

24 | P a g e

Pakistan Strategy 2019

Textile

Looking good thematically Weak beginnings… The textile sector enters 2019 on a weak note,

despite the 25% PKR devaluation in 2018. Demand from China (destination for 10% of Pakistan’s textile exports) has declined, indicated by a sharp 74/20% yoy dip in cotton/yarn volumes in 5MFY19. As a result, textile exports remained flattish at US$5.5bn in 5MFY19, after posting 5% yoy growth in FY18.

… but negatives are priced in: We believe the market has priced in the negatives given NML and NCL have corrected by 5/9% in 1m. We believe the operating environment favors players with higher contribution from value added products (NML). At the same time, sharp price correction has also opened up valuation upside for manufacturers with product mix skewed towards non-value added products (NCL).

Government incentives – potential upside trigger: The government has earlier hinted at an exports incentive package for the textile sector but has not followed through on it. Duty drawbacks could be an upside trigger – if they are announced at similar conditions as in the past, we estimate our earnings estimates for NML/NCL could rise by 33/21% in the 12mth period that drawbacks are in place. Meanwhile, PKR devaluation has led to continued upwards momentum in core earnings for IMS textile universe.

Risks: (i) Continued uptick in raw material prices, (ii) further slowdown in demand from China, and (iii) failure of government incentives to come through.

Sector performance

-20%

-10%

0%

10%

20%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS Textiles Uni. Source: IMS Research

Textile exports on a downtrend, again…

-15%-10%-5%0%5%10%15%20%

900

950

1,000

1,050

1,100

1,150

1,200

Jan-

16

Apr-1

6

Jul-1

6

Oct-1

6

Jan-

17

Apr-1

7

Jul-1

7

Oct-1

7

Jan-

18

Apr-1

8

Jul-1

8

Oct-1

8

US$MN

3M Moving Avg. Textile Exports YoY increase (Rhs) Source: IMS Research, SBP

…but core earnings continue their momentum

-200

0

200

400

600

800

1,000

1QFY18 2QFY18 3QFY18 4QFY18 1QFY19

(PKRmn)

NML NCL Source: Company Reports

Ailia Naeem [email protected]

TP Upside P/E (x) P/B (x) DY (%) (PKR) (%) 19F 20F 19F 20F 19F

Textiles 8.2 8.2 6.7 0.6 0.6 4.1% NML 180 33% 11.0 7.7 0.6 0.6 3.0% NCL 69 42% 4.0 4.4 0.8 0.8 8.8%

25 | P a g e

Pakistan Strategy 2019

Autos

Bumpy ride ahead Sedans can outperform amid demand contraction: Higher car prices

(up 15% on average in 2018) and higher interest rates will negatively affect auto sales. We expect the industry’s unit sales to decline by 10%yoy in 2019. However, sedans (Corolla, Civic and City) can ride out a tougher macroeconomic environment with their demand less sensitive to pricing, in our view. The tractor space will also witness volumetric decline amidst a subdued agricultural outlook (higher fertilizer prices and water shortage concerns).

Margins to stay under pressure: Despite higher prices, the industry’s GMs fell to 9.5% in Jul-Sep’18 vs. 13.4% in Jul-Sep’17. We think margins have yet to bottom out, even in the premium cars segment, particularly if the PKR continues to weaken. For the auto sector, we expect profits to decline by c 25% in 2019f before 11% growth in 2020f and then 23%yoy in 2020f.

Trading below replacement values: Market capitalizations for HCAR (capacity: 50k units) and PSMC (capacity: 150k units) have come down to c.PKR25bn and c.PKR15bn, respectively. Despite the challenging macroeconomic backdrop, this appears cheap given that new investments in the auto space (e.g. Kia and Hyundai) for plant capacities of 30k units cost PKR15-20bn. INDU’s market capitalization is c PKR95bn but we still like it due to its relatively resilient earnings and high 10% dividend yield.

Risks: (i) Sharp PKR depreciation eroding margins further, (ii) falling profits leading to applicability of turnover tax, (iii) entry of new players over the medium term, (iv) delays in new model launches.

Sector performance

-60%

-40%

-20%

0%

20%

Dec-

17

Jan-

18

Mar

-18

Apr-1

8

May

-18

Jun-

18

Jul-1

8

Aug-

18

Sep-

18

Oct-1

8

Nov-

18

Dec-

18

KSE-100 Index IMS Autos Uni.

Source: IMS Research

GM squeeze amid PKR depreciation but INDU stands out

95

100

105

110

115

120

125

130

0%

4%

8%

12%

16%

20%

1QFY18 2QFY18 3QFY18 4QFY18 1QFY19