OVERVIEW OF ISLAMIC FINANCE - Bank Islam Malaysia

48

OVERVIEW OF ISLAMIC FINANCE OVERVIEW OF ISLAMIC FINANCE STRICTLY PRIVATE & CONFIDENTIAL ISLAMIC FINANCE COURSE : STRUCTURE & INSTRUMENTS ISLAMIC FINANCE COURSE : STRUCTURE & INSTRUMENTS JOINTLY JOINTLY ORGANISED BY ORGANISED BY 13 13 DECEMBER 2010 DECEMBER 2010 BY AZRUL AZWAR AHMAD TAJUDIN BY AZRUL AZWAR AHMAD TAJUDIN CHIEF ECONOMIST CHIEF ECONOMIST

Transcript of OVERVIEW OF ISLAMIC FINANCE - Bank Islam Malaysia

OVERVIEW OF ISLAMIC FINANCEOVERVIEW OF ISLAMIC FINANCE

STRICTLY PRIVATE & CONFIDENTIAL

ISLAMIC FINANCE COURSE : STRUCTURE & INSTRUMENTS ISLAMIC FINANCE COURSE : STRUCTURE & INSTRUMENTS JOINTLY JOINTLY ORGANISED BY ORGANISED BY

13 13 DECEMBER 2010DECEMBER 2010

BY AZRUL AZWAR AHMAD TAJUDINBY AZRUL AZWAR AHMAD TAJUDIN

CHIEF ECONOMISTCHIEF ECONOMIST

CONTENTSCONTENTS

� FINANCE AND ISLAM

� Definition

� Essence of Islamic Finance

� Inherent Features of the IFSI and its Stability and Resilience

� Milestones of Shariah Contract Application

� RISK MANAGEMENT FOR ISLAMIC FINANCIAL INSTITUTIONS

� Four Generic Risks and Four Unique Risks

� Unique Risks for Islamic Financial Institutions

� Shariah Non-Compliance Risks

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 2

� Shariah Non-Compliance Risks

� PAST, PRESENT AND FUTURE

� Evolution of the IFSI: Early Days

� Evolution of the IFSI: Present Day

� Evolution of the IFSI: Beyond Nations with Large Muslim Populations

� Evolution of the IFSI: What the Future Holds

� Composition of the IFSI

� Islamic Financial System: Case of Malaysia

� Global IFSI Architecture: International Islamic Financial Infrastructure

CONTENTS (continued)CONTENTS (continued)

� SELECTED IFSI SEGMENT: ISLAMIC BANKING

� Fundamentals of Islamic Banking

� Overview of Islamic Banking Activities

� Review of Global Islamic Banking

� Resilience of Islamic Banking Amidst the Global Financial Crisis

� SELECTED IFSI SEGMENT: ISLAMIC CAPITAL MARKET

� Vibrancy of Islamic Capital Market

� Evolution of Sukuk

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 3

� Evolution of Sukuk

� Why Choose Islamic Securities

� MOVING FORWARD

� Challenges

� Emerging Mega-Trends in Islamic Finance

� The Islamic Finance and Global Stability Report

FINANCE AND ISLAMFINANCE AND ISLAM

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 4

DEFINITION DEFINITION

� Islamic finance, in contrast to conventional finance, involves the provision of

financial products and services by institutions offering Islamic financial services

(IIFS) for Shariah approved underlying transactions and economic activities,

based on contracts that comply with Shariah laws. Shariah, the basis for finance

that meets the religious requirements of Muslims in line with their ‘aqidah, is the

factor that distinguishes Islamic finance from conventional finance. Provision of

these Shariah compliant financial products and services must add value to the

real economy.

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 5

� These IIFS may comprise:

� full-fledged Islamic financial institutions or market intermediaries

� Islamic subsidiaries or branches of conventional financial groups

� From its original meaning of “the way to the source of life”, Shariah is now used

to refer to a legal system with rules & principles and code of behaviour. To

ensure compliance with Shariah rules & principles, IIFS rely on an external or in-

house Shariah committee or board comprising Shariah scholars.

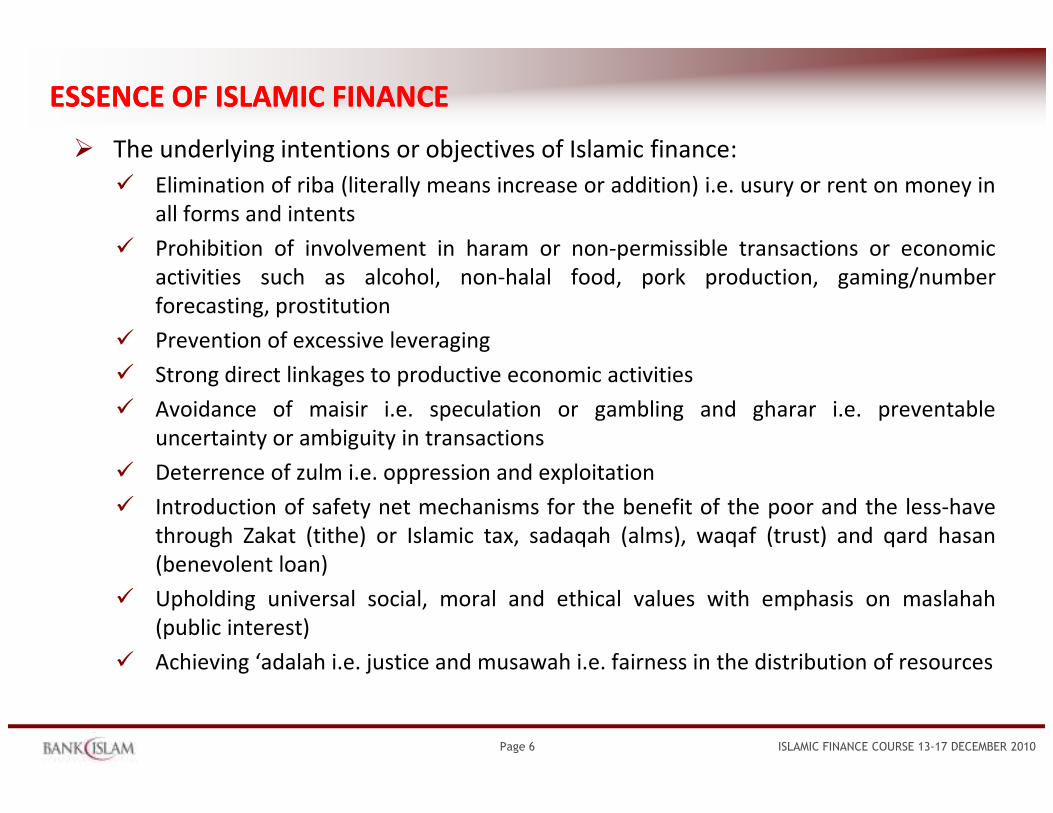

ESSENCE OF ISLAMIC FINANCEESSENCE OF ISLAMIC FINANCE

� The underlying intentions or objectives of Islamic finance:

� Elimination of riba (literally means increase or addition) i.e. usury or rent on money in

all forms and intents

� Prohibition of involvement in haram or non-permissible transactions or economic

activities such as alcohol, non-halal food, pork production, gaming/number

forecasting, prostitution

� Prevention of excessive leveraging

� Strong direct linkages to productive economic activities

� Avoidance of maisir i.e. speculation or gambling and gharar i.e. preventable

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 6

� Avoidance of maisir i.e. speculation or gambling and gharar i.e. preventable

uncertainty or ambiguity in transactions

� Deterrence of zulm i.e. oppression and exploitation

� Introduction of safety net mechanisms for the benefit of the poor and the less-have

through Zakat (tithe) or Islamic tax, sadaqah (alms), waqaf (trust) and qard hasan

(benevolent loan)

� Upholding universal social, moral and ethical values with emphasis on maslahah

(public interest)

� Achieving ‘adalah i.e. justice and musawah i.e. fairness in the distribution of resources

ESSENCE OF ISLAMIC FINANCE (continued) ESSENCE OF ISLAMIC FINANCE (continued)

� Governing principles or applicable Shariah contracts in Islamic finance:

� Equity-based or profit-sharing contracts – Mudharabah (profit sharing and loss

bearing), Musharakah (profit-and-loss sharing), Musharakah Mutanaqisah

(diminishing Musharakah)

� Lease-based contracts – Ijarah (leasing), Ijarah Muntahia Bittamleek

� Sale-based contracts – Bai’ Bithaman Ajil (BBA), Murabahah (cost plus), Salam

(forward delivery), Bai’ Inah

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 7

(forward delivery), Bai’ Inah

� Contracts to manufacture/produce – Istisna’

� Benevolent contracts – Qard, Hibah

� Services-based contract – Wadiah (safe custody), Wakalah, Kafalah, Rahnu, Sarf,

Hiwalah

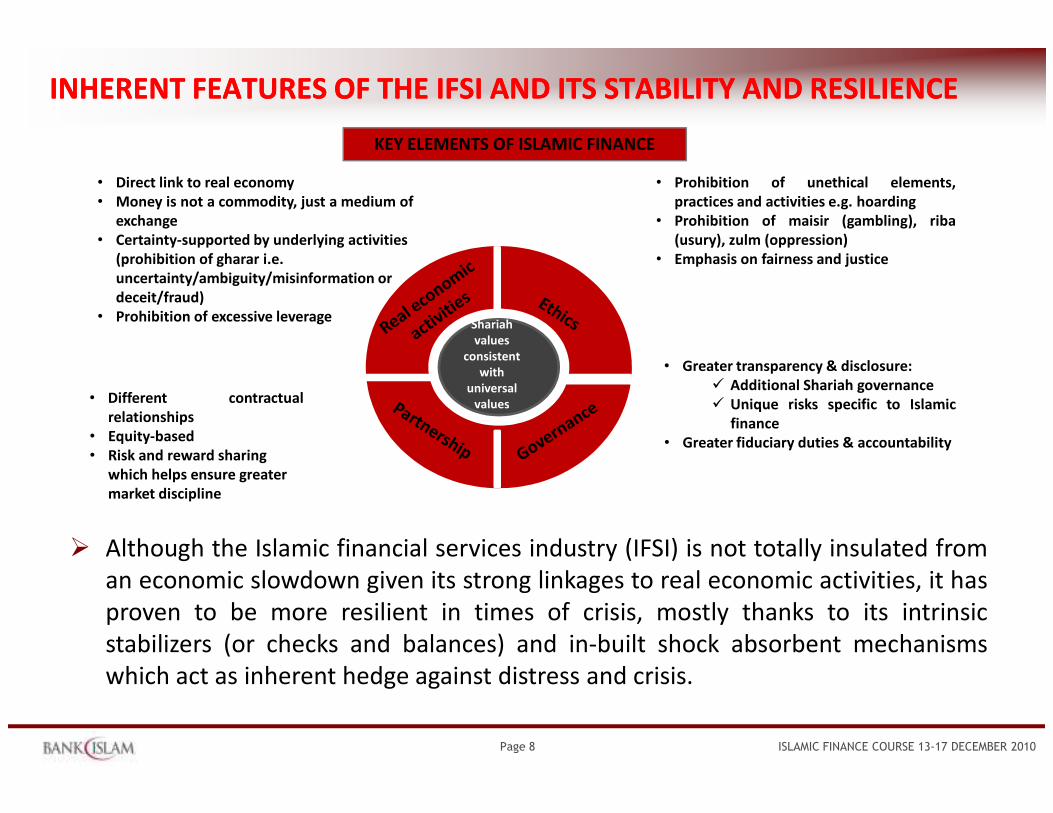

KEY ELEMENTS OF ISLAMIC FINANCE

• Direct link to real economy

• Money is not a commodity, just a medium of

exchange

• Certainty-supported by underlying activities

(prohibition of gharar i.e.

uncertainty/ambiguity/misinformation or

deceit/fraud)

• Prohibition of excessive leverage

• Different contractual

relationships

• Prohibition of unethical elements,

practices and activities e.g. hoarding

• Prohibition of maisir (gambling), riba

(usury), zulm (oppression)

• Emphasis on fairness and justice

• Greater transparency & disclosure:

� Additional Shariah governance

� Unique risks specific to Islamic

Shariah

values

consistent

with

universal

values

INHERENT FEATURES OF THE IFSI AND ITS STABILITY AND RESILIENCEINHERENT FEATURES OF THE IFSI AND ITS STABILITY AND RESILIENCE

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 8

relationships

• Equity-based

• Risk and reward sharing

which helps ensure greater

market discipline

� Unique risks specific to Islamic

finance

• Greater fiduciary duties & accountability

values

� Although the Islamic financial services industry (IFSI) is not totally insulated from

an economic slowdown given its strong linkages to real economic activities, it has

proven to be more resilient in times of crisis, mostly thanks to its intrinsic

stabilizers (or checks and balances) and in-built shock absorbent mechanisms

which act as inherent hedge against distress and crisis.

INHERENT FEATURES OF THE IFSI AND ITS STABILITY AND RESILIENCE INHERENT FEATURES OF THE IFSI AND ITS STABILITY AND RESILIENCE

(continued)(continued)

� These inherent features contribute towards the overall stability, soundness and

resilience of the IFSI. Indeed, according to the Islamic Finance and Global

Financial Stability Report, jointly published by the Islamic Financial Services Board

(IFSB), the Islamic Development Bank (IDB) and the Islamic Research & Training

Institute (IRTI) in April 2010, only 1 Islamic financial institution required

Government assistance in 2008 to restructure as a result of the then global crisis

as opposed to 5 of the world’s top conventional banks which received

Government assistance amounting to US$163 billion or 26% of their combined

equity. As at end-2009, no Islamic financial institution required any Government

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 9

equity. As at end-2009, no Islamic financial institution required any Government

rescue scheme.

� All Shariah values and elements embedded in Islamic finance, which are

consistent with universal values, are similar to those that found in ethical finance

and socially responsible investing (SRI).

MILESTONES OF SHARIAH CONTRACT APPLICATION

1983-1990 1991-2000 2001-2005 2006-20082009

onwards

�Wadiah Current Account

�Wadiah Savings Account

�Mudharabah Financing

�Ijarah Financing

�BBA Financing

�Mudharabah Investment

Account

� Murabahah LC

�Sarf Forex

�Mudharabah Interbank

Investment

�Musharakah Financing

�Bay Inah Credit Card

�Bay Dayn, Musharakah,

Mudharabah ICDO

�Wadiah Debit Card

�Bay Inah Overdraft

�Bay Inah Commercial

Credit Card

�Bay Inah Personal

Financing

�Commodity Murabahah

Profit Rate Swap

�Commodity Murabahah

Forward Rate Agreement

�Ijarah Rental Swaps-i

�BBA Floating Rate

�Murabahah Floating Rate

�Istisna’ Floating Rate

�Tawarruq Business

Financing

�Tawarruq Personal

Financing

�Tawarruq Credit Card

�Murabahah with Novation

Agreement

�Istisna’ convertible to

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 10

� Murabahah LC

�Musharakah LC

�Wakalah LC

�Bay Dayn Trade Financing

�Murabahah Working

Capital Financing

Financing

�Bay Inah Negotiable

Instrument of Deposit

(NID)

�Istisna’ Floating Rate

�Ijarah Floating Rate

�Mudharabah Capital

Protected Structured

Investment

�Bay Inah Floating Rate

NID

�Mudharabah Savings

Multiplier Deposit

�Tawarruq Commodity

Undertaking

�Istisna’ convertible to

Ijarah

�Bay and Ijarah (Sale and

Lease Back)

�Musharakah Mutanaqisah

�Istisna’ with Parallel

Istisna’

Note Note -- This listing is far from being exhaustive. This listing is far from being exhaustive.

RISK MANAGEMENT FOR RISK MANAGEMENT FOR

ISLAMIC FINANCIAL ISLAMIC FINANCIAL

INSTITUTIONSINSTITUTIONS

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 11

INSTITUTIONSINSTITUTIONS

FOUR GENERIC RISKS AND FOUR UNIQUE RISKS FOUR GENERIC RISKS AND FOUR UNIQUE RISKS

� Management of the four generic risks for financial institutions, namely credit,market, liquidity and operational risks, is not straightforward in Islamic finance.The risks of financing with underlying assets such as Murabahah, Salam, Istisna’and Ijarah may transform from credit to market and vice versa at different stagesof the contract.

� For instance, under Murabahah and Ijarah contracts, an Islamic bank has toacquire a physical asset and then sell the asset back on credit or lease it. The riskto which this Islamic bank is exposed transforms from the price risk of holdingthe physical asset at the time of acquisition to credit risk at the time of sale ondeferred payment or lease.

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 12

deferred payment or lease.

� In addition to these four generic risks, Islamic financial institutions will have todeal with another four unique risks:� Shariah non-compliance risk

� Rate of return risk

� Displaced commercial risk

� Equity investment risk

UNIQUE RISKS FOR ISLAMIC FINANCIAL INSTITUTIONSUNIQUE RISKS FOR ISLAMIC FINANCIAL INSTITUTIONS

Types of risks Definition

Shariah non-compliance

risk

Risk arises from the failure to comply with the Shariah rules and

principles

Rate of return risk The potential impact on the returns caused by unexpected change

in the rate of returns

Displaced commercial risk The risk that the Bank may confront commercial pressure to pay

returns that exceed the rate that has been earned on its assets

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 13

returns that exceed the rate that has been earned on its assets

financed by investment account holders. The Bank foregoes part

or its entire share of profit in order to retain its fund providers and

dissuade them from withdrawing their funds.

Equity investment risk The risk arising from entering into a partnership for the purpose of

undertaking or participating in a particular financing or general

business activity as described in the contract, and in which the

provider of finance shares in the business risk. This risk is relevant

under Mudharabah and Musharakah contracts.

SHARIAH NONSHARIAH NON--COMPLIANCE RISK COMPLIANCE RISK

� Unlike conventional financial institutions, Shariah non-compliance i.e. risk arising

from the failure to comply with Shariah rules and principles, is among the key

risks to manage for Islamic financial institutions. Among the four generic risks for

financial institutions, Shariah non compliance falls under the operational risk

category i.e. the potential loss resulting from inadequate or failed internal

processes, people and system or external events.

� Reputational risk related to Shariah compliance perception among and acceptance by

customers vis-à-vis:

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 14

customers vis-à-vis:

� the Islamic financial institution as a whole

� specific products or services that the Islamic financial institution offers

� Enforceability and validity risk of contracts particularly in the event:

� adherence to Shariah rules and principles is disputed

� existence of multiple contracts

� absence of a singe agreed ruling (due most probably to differing Shariah interpretations

across jurisdictions)

� lack of jurisdiction

PAST, PRESENT AND FUTUREPAST, PRESENT AND FUTURE

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 15

EVOLUTION OF THE IFSI : EARLY DAYSEVOLUTION OF THE IFSI : EARLY DAYS

� While first references to interest-free finance appeared in 1940s and more

serious discussions and debates on fundamentals of Islamic finance took place in

1950s and 1960s, modern forms of Islamic financial institutions can be traced

back to:

� 1962 when the Malaysian Govt set up Tabung Haji, a pilgrimage fund board

� 1963 when a small banking experiment was set up “under cover” in Mit Ghamr,

Egypt, based on a German savings bank model but modified to comply with Shariah

principles in particular profit-sharing (lasted until 1967)

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 16

� The institutional development of Islamic finance in particular its banking segment

began to gather speed with the establishment of:

� Islamic Development Bank in 1974

� Dubai Islamic Bank, the world’s maiden Islamic in 1975

� Faisal Islamic Bank of Sudan in 1977

� Faisal Islamic Egyptian Bank and Islamic Bank of Jordan in 1978

� Islamic Bank of Bahrain in 1979

� International Islamic Bank of Investment and Development, Luxembourg in 1980

� Bank Islam Malaysia Berhad in 1983

EVOLUTION OF THE IFSI : PRESENT DAY EVOLUTION OF THE IFSI : PRESENT DAY

� The IFSI has evolved from merely an alternative form of financial intermediation

primarily to meet the Shariah compliance requirements of the Muslims in the

Muslim world to become today a complete, competitive and integral component

of the mainstream global financial system that serves both Muslims and non-

Muslims worldwide.

� Islamic assets of the global IFSI are estimated to be worth about US$1 trillion as

at end-2009, expanding at a compounded average growth rate (CAGR) of 14.1%

from US$150 billion in the mid-1990s although the CAGR is higher in some

regions such as the Gulf Cooperation Council (GCC).

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 17

regions such as the Gulf Cooperation Council (GCC).

� Today, there are more than 600 Islamic financial institutions operating in at least

75 countries although Islamic finance in some form or another, institutionalised

or otherwise, is probably present in some 90 countries worldwide in the Muslim

and the Western world.

� About a dozen of long-established and emerging financial centres worldwide

aspire to become international centres for Islamic finance: Bahrain, Brunei, Doha,

Dubai, Hong Kong, Jakarta, London, Luxembourg, Malaysia (especially Kuala

Lumpur), Paris, Singapore, Tokyo

EVOLUTION OF THE IFSI: BEYOND NATIONS WITH LARGE MUSLIM EVOLUTION OF THE IFSI: BEYOND NATIONS WITH LARGE MUSLIM

POPULATIONSPOPULATIONS

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 18

� Burgeoning interest in Islamic finance over the past decade among:

� the so-called non-Muslim nations such as Australia, China, Germany, France, Holland,

Italy, Hong Kong, Japan, Luxembourg, New Zealand, Russia, Singapore, South Africa,

South Korea, the UK and the US

� the so-called non-traditional key Islamic finance markets in particular countries in

Central Asia such as Kazakhstan, Kyrgystan, Tajikistan, Turkmenistan and Uzbekistan;

in Eurasia such as Azerbaijan and in Africa such as the Comoros, Gambia, Kenya, Mali,

Nigeria, Senegal, Tanzania

EVOLUTION OF THE IFSI: WHAT THE FUTURE HOLDSEVOLUTION OF THE IFSI: WHAT THE FUTURE HOLDS

BREAKDOWN OF SHARIAH-COMPLIANT ASSETS

(AS AT END-2009)

82.10%

0.70%

11.70%5.50%

Islamic banking Takaful Sukuk Islamic funds

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 19

� Consensus forecasts expect the asset size of global IFSI to hit US$2 trillion in the

next 3 to 5 years while forecasts for 2012 vary between US$1.2 trillion and

US$1.6 trillion.

� There are still tremendous opportunities in the IFSI going by the Standard &

Poor’s estimates that the overall potential market is valued at US$4 trillion.

� In asset terms, Islamic banking (82.1%) is the largest IFSI segment, followed by

Sukuk (11.7%), Islamic funds (5.5%) and Takaful (0.7%) as at end-2009.

Islamic banking Takaful Sukuk Islamic funds

Source: GIFF Report 2010Source: GIFF Report 2010

Take off

Fast

growth

Maturity

Measure or

success or

profitability

High

EVOLUTION OF THE IFSI : WHAT THE FUTURE HOLDS (continued)EVOLUTION OF THE IFSI : WHAT THE FUTURE HOLDS (continued)

Maturity Curve of the IFSI

Saturation

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 20

Early start

1960 1970 2000 20xx

Islamic finance probably

stands here; best time in

terms of business

development as relatively

still early in the “fast

growth” phase

Medium

Low

COMPOSITION OF THE IFSI COMPOSITION OF THE IFSI

� Over the past 10 years, the IFSI has experienced phenomenal growth as

evidenced by the increasingly widening diversity of Islamic financial institutions,

product range as well as capabilities, resources infrastructure across the entire

Islamic financial system.

� As the Islamic financial system can perform all functions related to finance such

as fund mobilisation and reallocation, asset allocation, payment & settlement

services, remittance services, risk mitigation & transformation, among many

others, the IFSI consists of 5 major segments:

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 21

others, the IFSI consists of 5 major segments:

� Islamic banking (retail/consumer banking, commercial banking, SME banking,

corporate banking, investment banking, treasury, wealth management/private

banking, etc)

� Islamic interbank or money market

� Islamic capital market (equity market, Sukuk market, derivatives market)

� Islamic insurance/re-insurance or Takaful/re-Takaful

� Islamic asset management/fund management

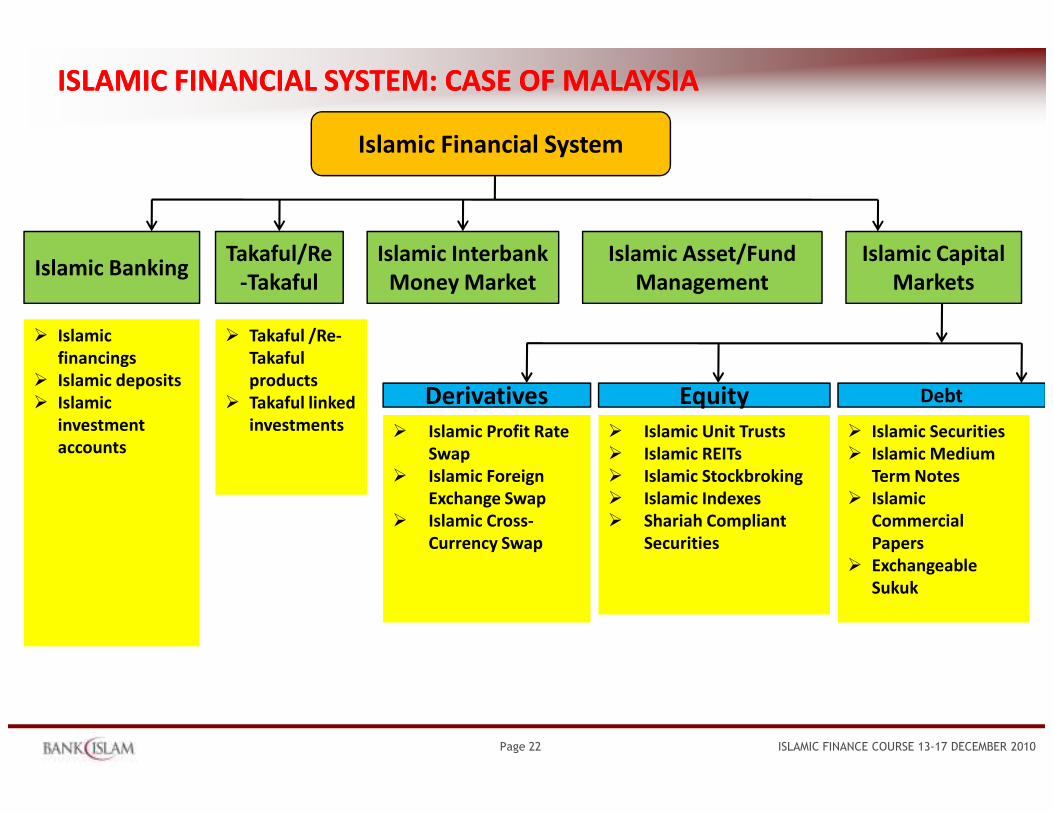

ISLAMIC FINANCIAL SYSTEM: CASE OF MALAYSIAISLAMIC FINANCIAL SYSTEM: CASE OF MALAYSIA

Islamic Financial System

Islamic BankingIslamic Capital

Markets

Equity DebtDerivatives

� Islamic

financings

� Islamic deposits

� Islamic

Islamic Interbank

Money Market

Takaful/Re

-Takaful

Islamic Asset/Fund

Management

� Takaful /Re-

Takaful

products

� Takaful linked

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 22

EquityDerivatives� Islamic

investment

accounts� Islamic Profit Rate

Swap

� Islamic Foreign

Exchange Swap

� Islamic Cross-

Currency Swap

� Islamic Unit Trusts

� Islamic REITs

� Islamic Stockbroking

� Islamic Indexes

� Shariah Compliant

Securities

� Islamic Securities

� Islamic Medium

Term Notes

� Islamic

Commercial

Papers

� Exchangeable

Sukuk

� Takaful linked

investments

GLOBAL IFSI ARCHITECTURE: INTERNATIONAL ISLAMIC FINANCIAL GLOBAL IFSI ARCHITECTURE: INTERNATIONAL ISLAMIC FINANCIAL

INFRASTRUCTUREINFRASTRUCTURE

� Apart from market players in the 5 major segments, namely Islamic banking,

Islamic interbank money market, Islamic capital market, Takaful/Re-Takaful and

Islamic asset management/fund management, the architecture of the Islamic

financial system also includes its institutional infrastructure organisations, which

can be categorised under the following areas:

� Payment-settlement system

� Financial markets including market microstructures, trading and clearance systems

� Support facility providers, legal institutions and framework, safety net, liquidity

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 23

� Support facility providers, legal institutions and framework, safety net, liquidity

support providers

� Regulators and supervisors including monetary authorities/central banks, licensing

authorities and industry regulators

� Governance infrastructure, including Shariah governance institutions

� Standard setters for financial supervision and infrastructure, including financial

reporting, accounting and auditing, capital adequacy & solvency, risk management,

transparency & disclosure and corporate governance, among others

� Rating and external credit assessment institutions

� Financial statistics and information providers

GLOBAL IFSI ARCHITECTURE: INTERNATIONAL ISLAMIC FINANCIAL GLOBAL IFSI ARCHITECTURE: INTERNATIONAL ISLAMIC FINANCIAL

INFRASTRUCTURE (continued)INFRASTRUCTURE (continued)

� At the global level, these international Islamic financial infrastructure

organisations which are mostly international organisations or multilateral

agencies are concentrated in 4 countries, namely Bahrain, Malaysia, Saudi Arabia

and United Arab Emirates.

� Bahrain:

� Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI)

� International Islamic Ratings Agency (IIRA)

� Liquidity Management Centre (LMC)

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 24

� Liquidity Management Centre (LMC)

� International Islamic Financial Market (IIFM)

� General Council for Islamic Banks and Financial Institutions (CIBAFI)

� Malaysia:

� Islamic Financial Services Board

� International Centre for Education in Islamic Finance (INCEIF)

� International Shariah Research Academy for Islamic Finance (ISRA)

� International Islamic Liquidity Management Corporation

GLOBAL IFSI ARCHITECTURE: INTERNATIONAL ISLAMIC FINANCIAL GLOBAL IFSI ARCHITECTURE: INTERNATIONAL ISLAMIC FINANCIAL

INFRASTRUCTURE (continued)INFRASTRUCTURE (continued)

� Saudi Arabia:

� OIC Fiqh Academy

� Islamic Development Bank (IDB) and Islamic Research & Training Institute (IRTI)

� United Arab Emirates:

� Arbitration and Reconcialiation Centre for Islamic Finance

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 25

SELECTED IFSI SEGMENT : SELECTED IFSI SEGMENT :

ISLAMIC BANKINGISLAMIC BANKING

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 26

ISLAMIC BANKINGISLAMIC BANKING

FUNDAMENTALS OF ISLAMIC BANKINGFUNDAMENTALS OF ISLAMIC BANKING

� Islamic banking is the most mature IFSI segment:� having grown and is expected to continue growing at a faster pace than that of

conventional banking

� strong presence in the Middle East, South East Asia, Northern & East Africa and SouthAsia while making inroads into Europe and North America

� Financial relationship in Islamic banking is participatory in nature with risk-reward profile is guided by socio-economic principles:� Risk sharing through partnership in ventures – building expertise and understanding

of ventures being financed, importance of viability of ventures instead of solelycreditworthiness of customers and know-your-customer culture

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 27

of ventures being financed, importance of viability of ventures instead of solelycreditworthiness of customers and know-your-customer culture

� Balancing act between pursuit of profit and fair and equitable distribution ofwealth/income

� The debtor-creditor or borrower-lender relationship in conventional bankingtransforms to mudarib (entrepreneur/capital user or investment manager)-rabbul mal (capital owner/provider or financier/investor) or more specifically:� Entrepreneur-investor or joint-venture relationship for Mudharabah and Musharakah

contracts

� Buyer-seller relationship for Murabahah and Ijarah contracts

� Agent-principal relationship for Wakalah contracts

OVERVIEW OF ISLAMIC BANKING ACTIVITIESOVERVIEW OF ISLAMIC BANKING ACTIVITIES

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 28

REVIEW OF GLOBAL ISLAMIC BANKINGREVIEW OF GLOBAL ISLAMIC BANKING

SHARE OF GLOBAL ISLAMIC BANKING ASSETS BY COUNTRY (AS AT END-2009)

36.0%

16.0%10.0%

10.0%

8.0%

6.0%

3.0%2.0%2.0%

7.0%

Iran Saudi Arabia Malaysia UAE Kuwait Bahrain Qatar UK Turkey Others

Source: GIFF Report 2010Source: GIFF Report 2010

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 29

� As at end-2009, according to the Banker Top 500 Islamic Institutions, Islamic

banking assets are mostly concentrated in Iran (36%), followed by Saudi Arabia

(16%), Malaysia (10%), UAE (10%), Kuwait (8%) and Bahrain (6%). Region-wise,

the 5 GCC countries hold the most Islamic banking assets with 43%. Top 7

countries account for 89% of global Islamic banking assets.

� Having grown by 15%-20% p.a. on average over the past decade to about US$780

billion in 2009 from around US$150 billion in the mid-1990s, Islamic banking

assets are expected to expand by more than 20% in 2010 to reach US$956 billion

to contribute more than 80% to IFSI assets.

Source: GIFF Report 2010Source: GIFF Report 2010

RESILIENCE OF ISLAMIC BANKING AMIDST THE GLOBAL FINANCIAL CRISISRESILIENCE OF ISLAMIC BANKING AMIDST THE GLOBAL FINANCIAL CRISIS

� Apart from intrinsic stabilisers and in-built shock absorbent mechanisms, othermain contributing factors to the resilience of Islamic banking during the 2008-2009 global financial crisis:

� Credit portfolios are mostly domestic – concentration of credit portfolios in domesticcustomers

� Focus on retail banking – rather low risk of a bank run due to high consumer loyaltyand deposit stability

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 30

� Most Islamic banks are highly capitalised and have ample liquidity – limited risk ofsolvency or crisis of confidence among counterparts in the interbank money market

SELECTED IFSI SEGMENT : SELECTED IFSI SEGMENT :

ISLAMIC CAPITAL MARKETISLAMIC CAPITAL MARKET

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 31

ISLAMIC CAPITAL MARKETISLAMIC CAPITAL MARKET

VIBRANCY OF ISLAMIC CAPITAL MARKETVIBRANCY OF ISLAMIC CAPITAL MARKET

� Islamic capital market which comprises equity, Sukuk and derivatives markets,remains the fastest growing IFSI segment globally with a CAGR of 40%. CurrentIslamic capital market assets are estimated to be worth US$130 billion.

� While the derivatives market has lagged far behind the other 2 Islamic capitalmarket subsets, the Sukuk market assets saw a CAGR of between 10%-15% overthe past decade to hit approximately US$100 billion at present.

� Based on Zawya’s Sukuk Quarterly Bulletin for the 3Q2010, some US$27.857billion were raised worldwide via Sukuk issuance during the first 9 months of2010, a 62% jump from a year ago.

� Global Sukuk issuance is expected to top the US$30 billion mark by end-2010 and

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 32

� Global Sukuk issuance is expected to top the US$30 billion mark by end-2010 andcould even exceed the all-time high of US$35.5 billion set in 2007 in the best-casescenario given:� continuous global economic recovery despite at a much slower pace since the 2H2010

� more sovereign issues expected reflecting continued Government fundraising tofinance fiscal spending and for benchmarking purposes

� still low levels of interest rates despite monetary tightening or normalisation processin developing Asia while most developed economies maintain record low interestrates

� gradual private investment revival

VIBRANCY OF ISLAMIC CAPITAL MARKET (continued)VIBRANCY OF ISLAMIC CAPITAL MARKET (continued)

� In some jurisdictions such as Malaysia, the Sukuk market is even much biggerthan the conventional bond market, reflecting increasing investor appetite anddemand for Shariah-compliant assets.

� In fact, Malaysia has the world’s largest Sukuk market, in both denominationscombined (MYR and non-MYR). As at end-June 2010, Malaysia’s local currencySukuk outstanding stood at RM246.5 billion or equivalent to US$76.42 billion.

� Whether from the perspectives of issuers or investors, the Sukuk yield seemsmore attractive than its conventional counterpart. In general, investors are moreeager to grab Islamic offerings rather than their conventional peers as evidencedby the customary high over-subscription for new Sukuk issues.

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 33

by the customary high over-subscription for new Sukuk issues.

EVOLUTION OF SUKUK

� Introduction & market

familiarisation

� Development of

markets, players &

products

� Very limited growth

� Confined to some

countries only e.g.

� Better growth in

market size players

� Additional product

features/structures:

* Istisna’

* Salam

* Ijarah

* Intifa’

� Acclelerated growth in

market size & players

� Broader & deeper

market

� Better market

understanding

� Innovative & new

product structures

� Maturing &

globalisation

� More breadth & depth

� More accelerated

growth

� Moving towards globally

accepted & highly

competitive structures

20001990 2004 2008 and beyond

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 34

countries only e.g.

Malaysia

� Limited structures (debt

bonds):

* Bai Bithaman Ajil

* Murabahah

* Qard Hasan

* Intifa’

� Intoduction of Sukuk in

the global market

* Malaysia Global

Sukuk (2002)

* Qatar Global Sukuk

(2003)

� Stronger growth of the

Sukuk market globally

product structures

(non-debt)

* Mudharabah,

Musharakah

* Islamic ABS

* Istisna’-Ijarah

* Convertible Sukuk

* Exchangeable Sukuk

competitive structures

� Activating the

secondary market for

Sukuk

� More & more product

innovation

� Unlocking new asset

classes

� Development of Sukuk

yield curve & pricing

benchmark

Source: Securities Commission MalaysiaSource: Securities Commission Malaysia

WHY CHOOSE ISLAMIC SECURITIES?WHY CHOOSE ISLAMIC SECURITIES?

� Islamic securities are increasingly gaining popularity as the preferred financing

option in view of the following benefits or appeal factors in general:

• Better yield given greater demand from a wider investor base and lower cost of funds. Spread differentials are by about 15-30 bsp.

• No stamp duty. Lower all-in costs

• Better yield given greater demand from a wider investor base and lower cost of funds. Spread differentials are by about 15-30 bsp.

• No stamp duty. Lower all-in costs

Cost effectiveness

• Tax deduction for issuers

• Tax neutrality for SPVs

• Tax deduction for issuers

• Tax neutrality for SPVs

Tax incentives (for both issuers and investors)

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 35

• An array of Shariah contracts to cater to varying investors’ risk appetites

• An array of Shariah contracts to cater to varying investors’ risk appetitesFlexibility

• Larger investor base, both local & global players• Larger investor base, both local & global playersDiverse investor base

• Obligation of full disclosure to investors

• Prohibition of excessive leveraging

• Obligation of full disclosure to investors

• Prohibition of excessive leveragingGreater transparency

• Collateralized or backed by assets• Collateralized or backed by assetsEnhanced security for investors

MOVING FORWARDMOVING FORWARD

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 36

CHALLENGESCHALLENGES

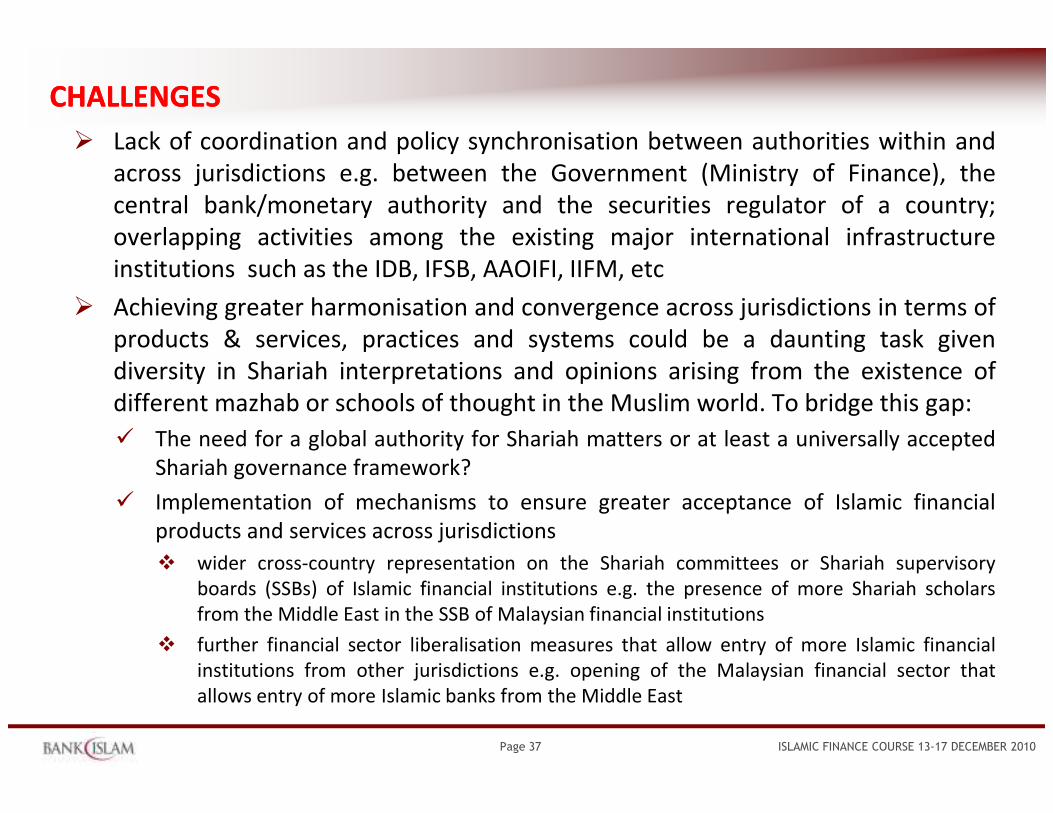

� Lack of coordination and policy synchronisation between authorities within and

across jurisdictions e.g. between the Government (Ministry of Finance), the

central bank/monetary authority and the securities regulator of a country;

overlapping activities among the existing major international infrastructure

institutions such as the IDB, IFSB, AAOIFI, IIFM, etc

� Achieving greater harmonisation and convergence across jurisdictions in terms of

products & services, practices and systems could be a daunting task given

diversity in Shariah interpretations and opinions arising from the existence of

different mazhab or schools of thought in the Muslim world. To bridge this gap:

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 37

different mazhab or schools of thought in the Muslim world. To bridge this gap:

� The need for a global authority for Shariah matters or at least a universally accepted

Shariah governance framework?

� Implementation of mechanisms to ensure greater acceptance of Islamic financial

products and services across jurisdictions

� wider cross-country representation on the Shariah committees or Shariah supervisory

boards (SSBs) of Islamic financial institutions e.g. the presence of more Shariah scholars

from the Middle East in the SSB of Malaysian financial institutions

� further financial sector liberalisation measures that allow entry of more Islamic financial

institutions from other jurisdictions e.g. opening of the Malaysian financial sector that

allows entry of more Islamic banks from the Middle East

CHALLENGES (continued)CHALLENGES (continued)

� Given the specialist nature of Islamic finance, the IFSI requires well-trained and

high calibre workforce with specific skills sets to cater to specificity of Islamic

finance. The global IFSI suffers from a shortage of Islamic finance talents at

almost all levels especially the middle and senior management. The IFSI in

particular Islamic financial institutions face the difficulty of building a talent pool

with the right combination of knowledge in Islamic law and modern finance while

addressing the issue of “poaching” by competitors within the country and other

aspiring Islamic financial hubs given their lucrative remuneration packages. The

IFSI needs to find the most effective ways of how to attract, retain and develop

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 38

IFSI needs to find the most effective ways of how to attract, retain and develop

Islamic finance experts.

� Shortage of Shariah scholars with adequate financial acumen or expertise required to

apply Shariah law to financial products & services

� Shortage of financial experts with adequate Shariah knowledge to accelerate product

innovation

CHALLENGES (continued)CHALLENGES (continued)

� Market related issues that could hamper growth of the IFSI

� Inexistence or limited existence of a secondary market in many jurisdictions -

although growing, the secondary market for Islamic securities/financial instruments in

particular Sukuk remains generally sparse, illiquid and inactive due to the tendency to

hold them until maturity.

� Virtual absence of a domestic Islamic money market as well as practical and tradable

Shariah compliant short-term money instruments for both monetary operations (as a

transmission channel for the implementation of central banks’ monetary policy) and

liquidity management of Islamic financial institutions in many jurisdictions.

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 39

liquidity management of Islamic financial institutions in many jurisdictions.

� Controversy surrounding most derivatives contracts among Shariah scholars in some

jurisdictions in particular in the Middle East although nobody can deny how crucial

Shariah compliant derivatives instruments for liquidity management and hedging

purposes. Hence, the establishment of a joint working group in 2006 between the

International Swaps and Derivatives Association (ISDA) and IIFM towards creating a

standardised master agreement for Shariah compliant derivatives transactions with

the hope of reaching a common ground eventually.

CHALLENGES (continued)CHALLENGES (continued)

� Absence of conducive legal and regulatory environment as well as supportive tax

framework in many countries with keen interest in Islamic finance.

� No enabling legislation that allows and facilitates activities of Islamic financial

institutions. In early Nov 2010, the Kerala High Court ruled the legal impossibility for

banks in India or their branches abroad to undertake Islamic banking activities.

� Absence of tax neutrality regime to facilitate Islamic financial transactions in some

jurisdictions.

� A far-reaching shift in product development and innovation model towards

conception of original and unique Shariah based Islamic financial products and

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 40

conception of original and unique Shariah based Islamic financial products and

services from merely a re-engineering of conventional financial products and

services (adapted and modified just to meet Shariah requirements and

circumvent its prohibitions) i.e. Shariah compliant financial products and services

that “mimic” or “replicate” or “mirror” their conventional peers. Product

innovation and sophistication or Islamic financial engineering based on market

dynamics should constantly:

� Meet the ever-changing customer needs and expectations of all walks of life without

compromising adherence to Shariah rules and principles

� Offer an increasingly diversified range of competitively priced, cost-effective, reliable

and high quality Shariah compliant financial solutions

CHALLENGES (continued)CHALLENGES (continued)

� Although the number of Muslims is estimated to total around 1.57 billion or

equivalent to about 22.9% of the world’s population at present, the size of the

IFSI is only a fraction of the global financial system as most Islamic financial

institutions have small capital structure. The presence of more highly capitalised

Islamic financial institutions will contribute positively to the soundness and

stability of the financial system as a whole. In a highly competitive environment,

being big may translate into:

� Larger economies of scale, better cost-efficiency, greater capacity (deeper pockets) to

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 41

� Larger economies of scale, better cost-efficiency, greater capacity (deeper pockets) to

finance larger and riskier projects

� Greater capability to innovate due to more extensive financial muscles

� Increased potential for regional or even global expansion

� Increased ability to withstand systemic occurrences such as a bank run

EMERGING MEGAEMERGING MEGA--TRENDS IN ISLAMIC FINANCETRENDS IN ISLAMIC FINANCE

� “Battle of deposits” in particular the pursuit of current and savings accounts

(CASA) and other types of low-cost deposits as a cheaper funding source for

Islamic banks and a shield against risk of liquidity crunch, which was encountered

at the height of the global financial crisis in 2008-2009 when banks were

reluctant to lend to each other in the interbank market. With more Islamic

financial institutions of diverse backgrounds joining the bandwagon, the ensuing

heightened level of competition should benefit customers particularly in terms of

pricing and variety of Islamic financial products and services.

Promoting Islamic finance as ethical and responsible finance and/or socially

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 42

� Promoting Islamic finance as ethical and responsible finance and/or socially

responsible investing (SRI) as a next stage to reach non-Muslim clientele

especially in the Western world, as a response to concerns among some non-

Muslims over the terms “Islamic” and “Shariah” as well as to build the bridges

between Islamic finance and conventional finance with emphasis on:

� fairness and justice concepts

� wealth preservation and sustainable development for the benefit of humankind

� other social, moral and humanitarian values

EMERGING MEGAEMERGING MEGA--TRENDS IN ISLAMIC FINANCE (continued)TRENDS IN ISLAMIC FINANCE (continued)

� Leveraging on the immense opportunities of the halal food industry, estimated to

be worth US$640 billion currently and anticipated to make up at least 20% of the

world’s food product trade in the near future. The so-called halal industry should

incorporate both food and non-food including Islamic finance to enable halal

end-to-end processes.

� Increasing popularity of microfinance or financing for SMEs and micro-

enterprises among Islamic banks especially as an entry point to penetrate into

new non-key traditional Islamic finance markets with sizeable Muslim

populations in Asia and Africa given their large portion of low-income group –

capitalising on the underbanked or underserved segment of the population that

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 43

capitalising on the underbanked or underserved segment of the population that

may have shunned (conventional) financial services all this while partly because

of the religious reasons. Since only 5% of low-income households worldwide

have access to financial services, Islamic banks, through microfinance will help

achieve greater financial inclusion, which is one of the essential pre-requisites for

creating a balanced and sustainable economic development. Out of 8 Millennium

Development Goals that the World Bank introduced in September 2000, at least

three, namely “Eradicating Extreme Poverty and Hunger”, “Promoting Gender

Equality and Empowering Women” and “Developing a Global Partnership for

Development” can be achieved through increased financial inclusion.

EMERGING MEGAEMERGING MEGA--TRENDS IN ISLAMIC FINANCE (continued)TRENDS IN ISLAMIC FINANCE (continued)

� Gradual phase-out of Bai’ Inah and Bai’ Inah-like contracts while minimising

Tawarruq contracts in developing universally acceptable Islamic financial

products and services, to replace with alternatives such as Murabahah,

Musharakah Mutanaqisah or Ijarah Muntahia Bittamleek or Wakalah where

applicable.

� More in-depth studies and research work to prove that equilibrium is possible in

an interest-free open economy i.e. in an economy where there are no interest-

bearing assets, only equity shares exist while all financial arrangements are

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 44

bearing assets, only equity shares exist while all financial arrangements are

based on risk and reward sharing. In this model, since all financial assets are

contingent claims that represent ownership claims to real capital i.e. no debt

instruments with fixed and/or predetermined rates of return, return to financial

assets must be determined by return of the real economy.

THE ISLAMIC FINANCE AND GLOBAL FINANCIAL STABILITY REPORTTHE ISLAMIC FINANCE AND GLOBAL FINANCIAL STABILITY REPORT

� The Islamic Finance and Global Stability Report published in April 2010

highlighted 3 key areas of priority to further strengthen and enhance the IFSI:

� Strengthening the infrastructural building blocks of the IFSI to further enhance its

resilience

� Accelerating the effective implementation of Shariah and prudential standards & rules

to facilitate the creation of a more stable, efficient and internationally integrated IFSI

� Creating a common platform for the regulators of the IFSI to enhance constructive

dialogue

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 45

dialogue

� Strengthening Islamic financial infrastructure

� Comprehensive set of cross-sectoral prudential standards and supervisory framework

� Development of a robust national and international liquidity management

infrastructure

� Strengthening financial safety nets – Shariah-compliant lender of last resort facilities,

emergency financing mechanisms and deposit insurance

THE ISLAMIC FINANCE AND GLOBAL FINANCIAL STABILITY REPORT THE ISLAMIC FINANCE AND GLOBAL FINANCIAL STABILITY REPORT

(continued)(continued)

� Effective crisis management and resolution framework – Bank insolvency laws and the

arrangements for dealing with non-performing assets, asset recovery and bank

restructuring as well as bank recapitalisation

� Accounting, auditing and disclosure standards, supported by adequate governance

arrangements

� Development of the macro-prudential surveillance framework and financial stability

analysis

� Strengthening rating processes by re-examining and improving the related core

processes to encourage greater transparency on the risks involved

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 46

processes to encourage greater transparency on the risks involved

� Capacity building and talent development

� Accelerating effective implementation

� Implementation of prudential standards issued by the IFSB

� Mutual understanding of Shariah views on key issues across jurisdictions

� Emphasis for Islamic finance to be a more inclusive system within a broader Islamic

financial ecosystem

THE ISLAMIC FINANCE AND GLOBAL FINANCIAL STABILITY REPORT THE ISLAMIC FINANCE AND GLOBAL FINANCIAL STABILITY REPORT

(continued)(continued)

� Establishment of a platform for constructive dialogues

� A strategic forum for conducive and constructive dialogues among

regulators/supervisors and other stakeholders of the international Islamic financial

system in particular Islamic financial institutions

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 47

Wassalam

وا���موا���مThank You

ا� ا�

The information contained in this presentation may be meaningful only with the oral presentation and is of the

ISLAMIC FINANCE COURSE 13-17 DECEMBER 2010Page 48

The information contained in this presentation may be meaningful only with the oral presentation and is of the

personal view of the presenter and does not necessarily represent an official opinion of Bank Islam Malaysia

Berhad.

For further information, please contact:

Azrul Azwar Ahmad Tajudin

Chief Economist

Strategic Planning, Managing Director’s Office

Bank Islam Malaysia Berhad

Email: [email protected]

Direct Line: +603-20888075