Overview of Indian startup ecosystem

16

Overview of Indian startup ecosystem Confidential and proprietary © Praxian Global Pvt. Ltd. September 2020 Indian startups raised $63 billion during 2016-20; making India the World’s 3rd largest tech startup hub

Transcript of Overview of Indian startup ecosystem

Overview of Indian startup ecosystem

Confidential and proprietary © Praxian Global Pvt. Ltd.

September 2020

Indian startups raised $63 billion during 2016-20; making India the World’s 3rd largest tech startup hub

2© Praxis Global Alliance |

• India has a prosperous and vibrant start-up ecosystem which is booming

‒ World’s 3rd largest tech start up hub with ~US$ 63B invested during 2016-20 in startups

‒ Total 50K+ startups in India with 9K+ created since 2014

‒ SaaS / AI vertical has dominated early stage funding deals (<US$ 10M) with ~25% investments going into SaaS / AI verticals like Fintech, IoT, logistics tech among others

‒ 27 domestic unicorns since 2014

• Significant startup activity has been created owing to:

‒ Availability of technical talent pool

‒ Changing perception around entrepreneurship

‒ Cross-pollination of learnings from global tech companies

‒ Increased government support through infra and funding, and

‒ Large amount of foreign capital flowing into India motivating domestic capital pools to participate as well

• Given the booming tech start-up eco-system in India, there is a huge demand for services across the lifecycle of tech-

enabled products like a) product designing tools, b) development platforms, c) product testing tools, d) solution hosting

and infrastructure, and e) customer support tools

Executive summary

3© Praxis Global Alliance |

India: Leading tech ecosystem in the world

Source(s): Startupblink, NASSCOM, Government portals, Inc42, Tracxn, Praxis analysis

~$63 B

Funding poured into

Indian startups during

2016 - H1 2020

3rd

Largest ecosystem in

number of technology

startups, 2020

27

Number of Unicorns till

2019, 8 additions in

2020 so far

3

Cities among top 10

startup cities in Asia –

Pacific, 2020

~$20 B

Startup funding in 2019

across 1,854 deals

Robust

ecosystem

>US$ 60BCumulative

valuation of start-

ups founded in

2014-19

1000+ Active institutional

investors as of

2019

335+ Accelerators and

incubators as of

2019

44%Startup unicorns

have overseas

market

50,000+ Startups as of

2018;

12-15% growth;

9000+ in 2014-19

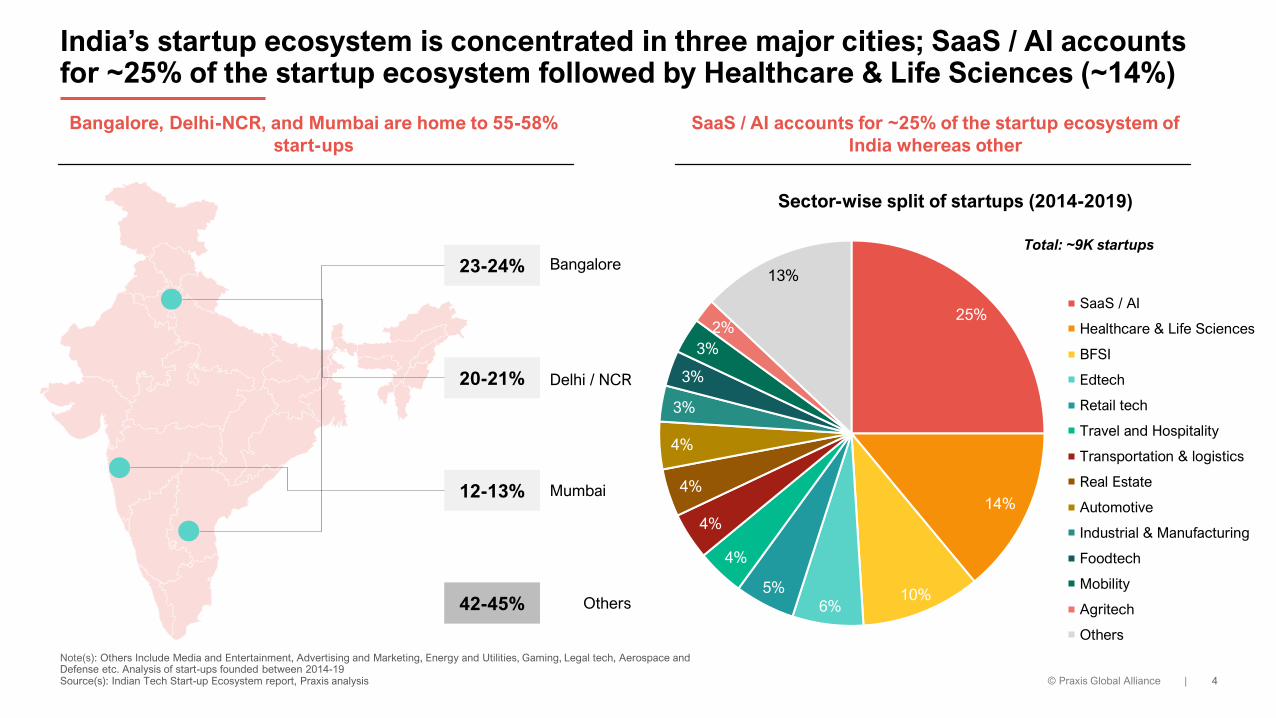

4© Praxis Global Alliance |

India’s startup ecosystem is concentrated in three major cities; SaaS / AI accounts for ~25% of the startup ecosystem followed by Healthcare & Life Sciences (~14%)

Note(s): Others Include Media and Entertainment, Advertising and Marketing, Energy and Utilities, Gaming, Legal tech, Aerospace and Defense etc. Analysis of start-ups founded between 2014-19Source(s): Indian Tech Start-up Ecosystem report, Praxis analysis

23-24%

20-21%

12-13%

42-45%

Bangalore

Delhi / NCR

Mumbai

Others

Bangalore, Delhi-NCR, and Mumbai are home to 55-58%

start-ups

25%

14%

10%6%

5%

4%

4%

4%

4%

3%

3%

3%

2%

13%

Sector-wise split of startups (2014-2019)

SaaS / AI

Healthcare & Life Sciences

BFSI

Edtech

Retail tech

Travel and Hospitality

Transportation & logistics

Real Estate

Automotive

Industrial & Manufacturing

Foodtech

Mobility

Agritech

Others

SaaS / AI accounts for ~25% of the startup ecosystem of

India whereas other

Total: ~9K startups

5© Praxis Global Alliance |

~US$ 34B invested in Indian ecosystem during 2019 and ~US$ 17B in 2020 (till May); Tech enabled players driving investor’s interest

Note(s): Construction and manufacturing sectors are excluded from the analysisSource(s): Praxis investment database, Praxis analysis

2019 and H1 2020 have seen huge investments in

telecomTech enabled startups have dominated the funding landscape

2.8

5.3 5.87.2

1.1

1.7

7.3 5.85.2

0.9

1.4

1.82.6

4.2

0.5

0.5

3.7

9.30.5

0.91.1

3.0

1.0

1.5

1.5 3.1

2.7

1.4

1.0

2.31.7

2.3

1.9

0.4

1.0 0.7

1.4

0.3

0.2

1.0 0.7

0.4

0.2

1.5

0.7 1.0

0.2

0.1

1.1

2.83.7

4.0

0.1

12.1

25.226.3

34.2

16.7

2016 2017 2018 2019 2020

Investments in India by sector2016- 2020 (Jan-May), US$ B

BFSI Online Services (MP/LP/AG) Energy Telecom SaaS/AI Healthcare & Life Sciences Online Services (Consumer app / platform) Transportation & logistics FMCG IT services Others

Company Vertical

Funding in

2019 – 20,

(US$ M)

Cumulative

funding,

(US$ B)

Key investors

Jio Platforms Telecom 9,871 15.2 Vista Equity Partners, ADIA,

Silver Lake, TPG Capital

Byju’s Classes Education 1,050 10.8 Tiger Global

CitiusTech HealthTech 880 1 Baring Asia

Oyo Rooms Hotel aggregator 807 3.2 SoftBank, RA Hospitality

UdaanE-commerce

(B2B)616 1.6

GGV Capital, Altimeter

Capital, Tencent

Ola Taxi booking 534 3.2Hyundai Motor Company, Kia

Motors

Delhivery Logistics 528 0.8 CPPIB

CureFit Wellness 351 0.4 Temasek, Accel, Epiq Capital

Postman SaaS/AI 200 0.2 Insight Partners

Lenskart.comE-Commerce

(Eyewear)330 0.5 SoftBank

Bounce Scooter rentals 329 0.4 Accel, Sequoia Capital

Ola Electric MobilityMobility

(Electric)324 0.3

Matrix Partners India, Tiger

Global, Ratan Tata

ZomatoRestaurant

aggregator310 1.1 Baillie Gifford

FirstCryE-commerce

(Baby products)300 3.2 SoftBank

CardekhoClassifieds

(Cars)299 0.5

Sequoia Capital, Hillhouse

Capital Group, CapitalG

6© Praxis Global Alliance |

Key factors driving startup ecosystem in India

Source(s): Secondary research, Praxis analysis

Large domestic market

Increased political will

and government support

Demand from global

players

Ever increasing talent

pool

• Government of India is advocating

entrepreneurial mindset by introducing

regimes:

– ‘Make in India’ -> aims to make

India a global manufacturing hub

– ‘Stand Up India’ -> aims at

promoting entrepreneurship and

job creation

– ‘Startup India’ -> aims at

promoting bank financing for

startups

• Enablers and incubators are also

providing startups with growth advice

and decision-making tools• Increase in # universities, followed by increasing

enrolment rate has led to a rise the talent pool with

~10% of the population being graduates

• India has a population ~1.37B in 2020 and is expected

to reach ~1.47B by 2025 with ~80% working

population

• With such a high population, even niche products have

significant market potential

• Increase in economy led to increase in incomes and

purchasing power -> increase in consumption

Changing perception

towards entrepreneurship

• The success stories of remarkable exits and India’s first unicorns have

received much media attention

• Subsequently, some founders have become India’s “startup heroes”,

contributing to a current image of entrepreneurship as “cool” and

“glamorous”

• Despite some hype, the social acceptability of entrepreneurial

careers is increasing

Drivers of Indian

startup ecosystem

• Reasons for increase in foreign tech investment -> Strong bilateral ties

with several countries and perception of an alternative to China

• Companies like American Express, Microsoft and Apple investing

heavily to open their R&D centers in India

• India is now the tech garage of the world with US and EU offshoring

~80% of their IT operations to India

7© Praxis Global Alliance |

Later stage funding accounted for ~35% of the total funding during 2016-20

~28% of total investments during 2016-20 were in US$ 50M–100M ticket size

Indian startups raised ~US$ 63B during 2016-20 with ~65% investment in growing startups i.e. seed-series D rounds

Source(s): Tracxn, Praxis analysis

0.6 0.6 0.7 0.7 0.3

1.6 1.3 1.6 1.8

0.6

1.5 2.4 2.33.3

1.0

1.1

2.22.7

2.8

1.0

1.4

1.3

1.8

3.9

0.5

1.3

7.6 5.7

7.2

1.9

7.4

15.414.8

19.7

5.2

2016 2017 2018 2019 H1 2020

Investments in Indian startups by stagesUS$ B, 2016 – H1 2020

Seed Series A Series B Series C Series D Later

0.51.31.31.21.1

1.0

3.12.62.12.2 0.9

2.6

1.71.21.0

0.9

2.5

1.8

1.81.42.0

5.8

4.7

2.9

1.8

4.5

3.0

6.4

5.2

19.8

15.015.5

7.4

20202019201820172016

Investments in India startups by deal sizeUS$ B, 2016 – H1 2020

< US$ 5M US$ 5M - 25M US$ 25M - 50M US$ 50M - 100M

US$ 100M - 500M > US$ 500M

8© Praxis Global Alliance |

Tech enabled startups have dominated the early stage funding landscape in India

Notes: MP – Marketplaces, LP – Listing platforms, AG – AggregatorsSource(s): Praxis investment database, Praxis analysis

SaaS / AI

Fintech, 16%

IoT, 8%

Logistics tech, 7%

Analytics, 7%

HR services, 7%

Security, 7%

CRM, 6%

Healthtech, 6%

Digital marketing, 5%

AI / ML, 5%

Chat bots, 3%Edtech, 2%

Others, 22%

Fintech, 13%

Horizontal, 11%

Real Estate tech, 9%

Foodtech, 9%

B2B MP, 8%

Agritech, 7%

Apparel, 7%

Mobility tech, 6%

Logistics tech, 6%

Auto tech, 5%

Travel & leisure, 5%Furniture / appliances, 2%

Personal care, 2%

Others, 10%

Fintech, 48%

Media & entertainment, 29%

Edtech, 19%

Travel & leisure, 2%Others, 2%

Online Services

(MP/LP/AG)

Online Services

(Consumer apps/platforms)

Healthtech, 52%

Pharma &

biotech, 17%

MedTech &

supplies, 12%

Private healthcare

delivery, 8%

Consumer

healthcare, 8%

Others, 3%

Consumer

products

Food &

beverages,

32%

Personal

care, 21%

Apparel,

19%

Consumer

durables,

13%

Others, 15%

NBFC

, 71%

MFI,

15%

MFI,

15%

Logistics tech, 7%

Food & beverages, 5%

Co-working, 5%

IT services, 5%

Agriculture, 4%

Education, 3%

Deal value by sub-sectors (<US$ 10M ticket size)2017-2020*, US$ M

Total: US$ 2.5B

Others, 40%

~US$ 617M ~US$ 507M ~US$ 453M ~US$ 241M ~US$ 181M ~US$ 406M

Energy

Rene

wable

soluti

ons,

69%

Equip

ment,

28%

Others

~US$ 83M

~US$ 55M

Others, 3%

Tech enabled products,

23%

Manufacturing, 8%

Healthcare &

life sciences

BFSI

9© Praxis Global Alliance |

Startup Industry Founded Funding How is it disrupting the industry?

Payments 2012 Acquired• Digital payments app based on Unified Payments Interface (UPI) available in 11 regional

languages with over 10M merchants

Defence,

military, and

others

2011 Acquired

• Uses robotics and AI to develop drone-based solutions to military, parliamentary and police

forces

• Also provides drone-based solutions for autonomous surveys, inspection, and to monitor assets

Foodtech 2014 US$ 1.62B

• Enhanced customer experience by developing an app that seamlessly connects the user to

local restaurants and delivery partners

• Leveraging AI / ML to create models that will personalize user experience

Healthtech 2015 US$ 323M

• Aids to connect local pharmacy stores and diagnostic centers in order to fulfill extensive

medical needs

• Uses wide variety of open source and proprietary technology to verify prescriptions and make

the customer experience seamless

Shared

mobility2017 US$ 212M

• Leverages IoT and analytics to provide electric bikes to its customers in dense places and

solves two problems at once – traffic congestion and air pollution

Media &

Entertainment2007 US$ 205M

• Leveraging machine learning to curate hyperlocal news content in vernacular languages

based on user profiling, pivoting towards a social platform

Home

interiors2015 US$ 200M

• Uses their proprietary technology platform to deliver end-to-end home interior project

• Designers can manage the entire design project using the software - create designs, access a

digital catalogue, plan the budget, chat with clients, place manufacturing orders, etc.

Agritech 2012 US$ 17M

• Technology-based platform offering end-to-end agricultural services to farmers

• Services may include distribution agri inputs, customized farm advisory, access to financial

services, and market linkages for selling their produce

Agritech 2010 US$ 16M• Enable data-driven farming which helps derive real-time insights on standing crop projects

across geographies based on local wealth information and high-resolution satellite imagery

Tech-led startups are disrupting industries across India

Source(s): Secondary research, Praxis analysis

10© Praxis Global Alliance |

Startup Industry Founded Funding How is it disrupting the industry?

Edtech 2011 US$ 2.1B

• Created an app to deliver high impact lectures in an engaging way to make difficult concepts

easy

• Caters to India’s large K-12 market by providing subscription model and has slowly advanced

into the US

Foodtech 2008 US$ 975M

• Enhanced customer experience by developing an app that seamlessly connects the user to

local restaurants and delivery partners

• Expanded overseas into multiple countries within a few years

SaaS 2010 US$ 649M• Create software management products that help sales, marketing, support, IT, and HR teams

to deliver the best customer experiences

Gaming 2008 US$ 160M*

• Pioneered the Fantasy Sports Gaming market of India and are the leader with ~90% market

share

• Tapped into the enthusiastic Indian cricket market by introducing an app that is easy to use

SaaS 2010 US$ 91M

• Enables customers and employees to use personal devices, assuring safety and convenience

• Leverages AI to increase convenience, with intuitive booking, less wait-times, and automatic

check-ins and payments

SaaS 2013 US$ 77M• Leverages machine learning, it offers an engagement suite that enables brands to convert,

engage, retain, and grow their mobile user base

Payments 2014 US$ 60M

• Creating a transparent, convenient, and cost-efficient process using their website / app for

individuals by redefining the remittance industry

• Grabbing market share from the traditional players that have high hidden costs

SaaS 2016 US$ 29M• Uses artificial intelligence and deep learning algorithms for medical imaging

• Helping cut down the diagnostic time for chest and brain problems

SaaS 1996 - • Web-based online application suite for the businesses

And Indian innovation is going global…

Note(s): *Uptil April 2019Source(s): Secondary research, Praxis analysis

11© Praxis Global Alliance |

Tech outsourcing service demand from global majors present in India has further boosted startup ecosystem in India

Source(s): Secondary research, Praxis analysis

BFSI

Online Services

(MP/LP/AG)

Telecom

SaaS/AI

Healthcare & Life

Sciences

Online Services

(Consumer app /

platform)

Transportation &

logistics

FMCG

IT services

12© Praxis Global Alliance |

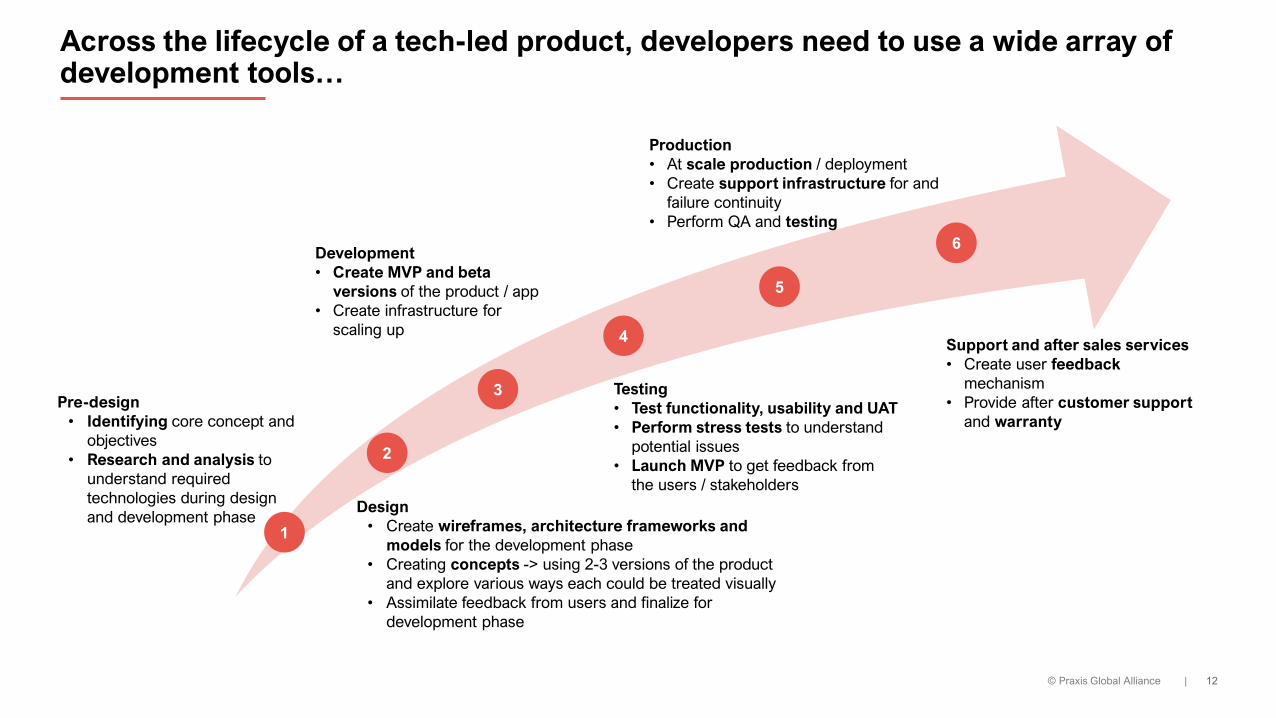

Across the lifecycle of a tech-led product, developers need to use a wide array of development tools…

Pre-design

• Identifying core concept and

objectives

• Research and analysis to

understand required

technologies during design

and development phase Design

• Create wireframes, architecture frameworks and

models for the development phase

• Creating concepts -> using 2-3 versions of the product

and explore various ways each could be treated visually

• Assimilate feedback from users and finalize for

development phase

Development

• Create MVP and beta

versions of the product / app

• Create infrastructure for

scaling up

1

2

3

4

Testing

• Test functionality, usability and UAT

• Perform stress tests to understand

potential issues

• Launch MVP to get feedback from

the users / stakeholders

5

Production

• At scale production / deployment

• Create support infrastructure for and

failure continuity

• Perform QA and testing

6

Support and after sales services

• Create user feedback

mechanism

• Provide after customer support

and warranty

13© Praxis Global Alliance |

About IVCA

This is a wonderful report covering data and insights on the booming Indian tech startup

ecosystem, carrying a fresh perspective about developers and service demand.

The growth stage startup and venture capital ecosystem is poised for the next leap with an

increasing number of unicorns, soonicorns and minicorns, even amidst the current crisis of

Covid19. The ecosystem has been relentlessly working to boost the investment environment,

the Government of India is playing a crucial role in this, but most importantly, the growth stage

investors are continuing the momentum, filling a void for startups that have just crossed their

mid life or are at the inflexion point where they, very much need this capital to scale and

expand.

IVCA is the oldest and most influential PE & VC industry body in India, its

purpose is to promote the Alternative Investment Asset class. IVCA

supports the ecosystem by facilitating advocacy discussion with the

Government of India, policymakers, regulators, and supports the

entrepreneurial activity, innovation, and job creation in India.

Rajat Tandon

President, IVCA

14

(FIG)

About Praxis

Praxis Global Alliance is the next-gen management consulting and business research services firm revolutionizing the way consulting

projects are delivered. We deliver practical solutions to the toughest business problems, by uniquely combining domain practitioner

expertise, AI-led research approaches, and digital technologies.

Pre-deal support, commercial

due diligence, post-acquisition

value creation

(BET) Next-gen practitioner-led

business advisory and consulting

offering lean-cost and long

duration engagement

Data engineering and

analytics, AI, ML, Open Data

and visualization solutions

Cutting-edge technology-led

business and market

research and tools

Organization and Talent

effectiveness

Praxis is ‘Practical’

We bring the best domain expertise with our deep pool of industry

practitioners and implementation teams as two-in-a-box

We work with agility, flexibility and embed with your teams to enable

SUPERIOR OUTCOMES

We leverage technology deeply to enable higher ROI on your

consulting and analytics spend

© Praxis Global Alliance |

15© PGA Labs |

We work with leading financial sponsors and strategic investors to identify

opportunities, build investment thesis and maximize shareholder value. Our agile

business delivery model coupled with our deep network of industry practitioners

enables clients to deploy our capabilities on any deal.

Fund strategyHelp investors in identifying growth drivers, investment themes, attractive

sub-sectors and potential targets and build thesis

Full scale commercial due diligenceAssessment of market potential, customer proposition, competitive

positioning, operational efficiency, channel value creation & risk

mitigation

Operational due diligenceHelp investors to understand the operational strengths and weaknesses

of the target to scale up and meet the B-plan goals

Tech due diligence / Digital diligenceAssessment of current capabilities and future requirements of tech &

infrastructure of the target

Fund retainerHelp investors in end-to-end fund operations from maintaining deal

pipeline, evaluating shortlisted deals to deal closure support

How we help our clients

Value creation blueprintingAdvise portfolio companies on business transformation, go-to-market

strategy, enhancing organization productivity etc.

Madhur Singhal

Practice Leader

Ex-Partner at Bain & Co., BCG

MBA (IIM Ahmedabad), B.Tech.

(IIT Delhi)

Aryaman Tandon

Practice Leader

Ex-Bain & Co.

B.Tech. (IIT Delhi)

Vibhor Gupta

Practice Member

Ex-Samsung, Aditya Birla Group

PGDBM (XLRI, Jamshedpur),

B.Tech (DCE, Delhi)

Shishir Mankad

Practice Leader

Ex-EVP Axis Bank, BCG

MBA (IIM Ahmedabad),

Chartered Accountant, M.Com

Abhishek Maiti

Practice Member

Ex- Reval

MBA (IIM Indore),

B.Tech (IIT Delhi)

Varsha Agrawal

Practice Member

Ex-Nomura

Masters in Finance (Esade

Business School, Spain)

CA, CS, B.com. Hons. (NMIMS)

Charul Agrawal

Practice Member

Ex- PwC US Advisory

MBA (IIM Ahmedabad),

B.Tech (IIT Delhi)

Sumit Agrawal

Practice Member

Ex-Nomura

MBA (IIM Bangalore),

B.Tech (IIT Madras)

THANK YOU