Overview of Business Entities, Liabilities and Insurance for the Food and Agriculture Producer

76

Overview of Business Entities, Liabilities and Insurance GrowNYC January 8, 2015 By Cari B. Rincker, Esq.

-

Upload

cari-rincker -

Category

Law

-

view

280 -

download

0

Transcript of Overview of Business Entities, Liabilities and Insurance for the Food and Agriculture Producer

Overview of Business Entities, Liabilities and Insurance

GrowNYCJanuary 8, 2015

By Cari B. Rincker, Esq.

Who I Am

• Grew up on a beef cattle farm in Illinois– Advanced degrees in

animal science

• Chair of the ABA, General Practice, Solo & Small Firm Division’s Agriculture Law Committee

• Client base ranges from agriculture producers & food entrepreneurs to mid-size agri-businesses

We Will Be Talking New York Law Today

• Law on business entities and formations varies slightly from state-to-state

• If you are interested in the law in other states, please speak to an attorney licensed in that jurisdiction

– I’m licensed in New York, New Jersey, Connecticut, Illinois, & Washington D.C.

One More Disclaimer• I am a lawyer but not necessarily your lawyer

unless you’ve signed a retainer agreement with Rincker Law, PLLC (which creates attorney-client privilege)

• Today’s presentation is for informational purposes only should not be considered legal advice– Before making decisions for your farm or food

business, it is always best to have a candid conversation with an attorney about your specific circumstances

Overview

• 3 Big Topics– Business

Formation

– Liability

– Insurance

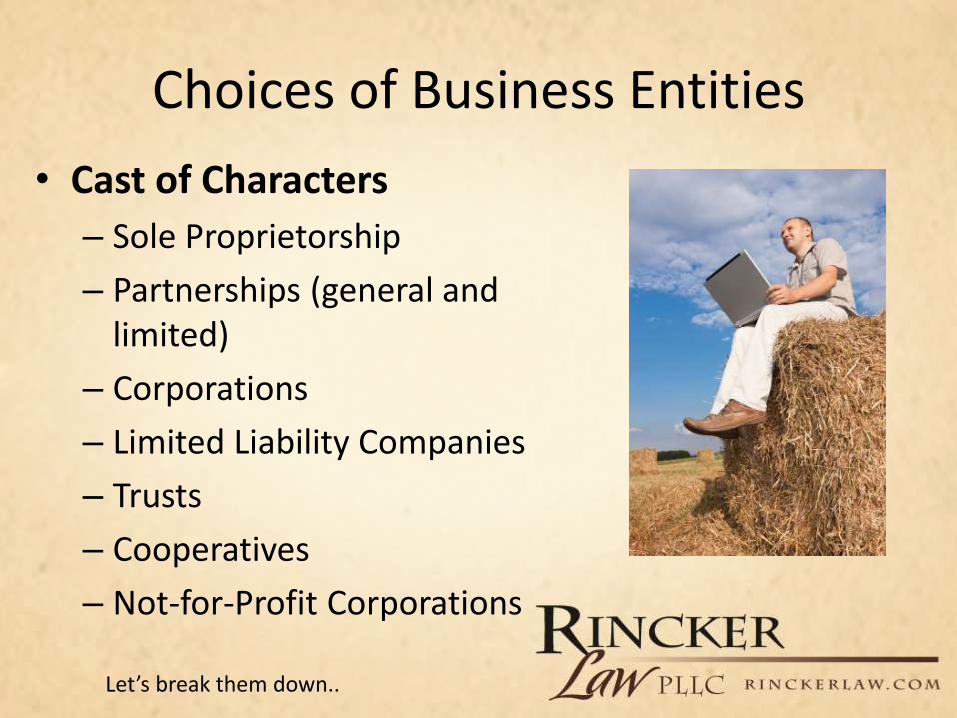

Choices of Business Entities

• Cast of Characters

– Sole Proprietorship

– Partnerships (general and limited)

– Corporations

– Limited Liability Companies

– Trusts

– Cooperatives

– Not-for-Profit Corporations

Let’s break them down..

Sole Proprietorship

• This is an informal legal entity formed with 1 person

• Unlimited personal liability

– Big disadvantage

• This is a common choice of business entity

– Default when a business only has one owner and hasn’t formed another entity

Sole Proprietorship

• Filing Requirements– No filing requirements with

the NYS Department of State – No filing fees!

– Should file a Certificate of Assumed Name with the County Clerk if a d/b/a under NY General Business Law §130 • $110 in New York County

Examples: Farmer Jane Smith d/b/aJane’s Pumpkin Patch & Hay Rides

Cari Rincker d/b/a Rincker Cattle Co.

Sole Proprietorship

• Although not required, should consider obtaining a Federal Employer Identification Number (“FEIN”)– If a sole proprietorship does not

obtain a FEIN then it will have to put its social security number on tax forms if independent contractors or employees are hired

• Also consider opening up a separate business bank account with the FEIN

Partnerships

• Definition of a Partnership

– When more than one person goes into business together to share profits (not necessarily losses)

– Can be formed inadvertently

How many of you have formed a partnership at some point? Partnerships are very commonin the food and agriculture industry.

2 Types of Partnerships

General Partnership

Limited Partnership

General Partnerships are more commonin the food and agriculture industry

General Partnerships

• Definition: Where two or more people go into business together and share profits without forming another formal entity (e.g., LLC, LLP, corporation)

• Liability: Each partner is jointly and severally liable for the debts of the partnership- no liability shield– Unless stated differently in the

general partnership agreement, each partner has the authority to bind the partnership without the express written consent of all partners

General Partnerships

• Filing Requirements– GBL § 130 requires partners

carrying on business as a partnership to file a certificatewith the county clerk in each county in which the partnership is going business

– Failure to file a certificate doesn’t affect the rights of any third persons and doesn’t limit the liability of any partners under the provisions of the New York Partnership Law

Limited Partnerships (the “LP” or “LLP”)

• A limited partnership requires at least one limited partner and at least one general partner

– Limited Partner:• Limited liability protection• Must not participate in the

management of the partnership under NY Partnership Law (“PL”) § 121-303

– General Partner:• Unlimited personal liability • Makes all the day-to-day

decision-making

Limited Partnerships

• Filing Requirements– Must file a Certificate of

Limited Partnership with the NYS Department of State pursuant to NYS Revised Limited Partnership Act (“RLPA”) § 121-201

– Costs $200

– Must be filed by the general partner(s)

Limited Partnerships

Limited Partnership Agreement– RLPA requires a limited partnership agreement

– Partnership agreements are very important for all types of partnerships but paramount for limited partnerships• Identification of the ownership units of each limited

and general partner

• Capital contribution

• How profits and losses will be divided

• Responsibilities, duties, and restrictions

Limited Partnerships• A few of you might be thinking, “what’s the

point?”

• Limited Partnerships or Family Limited Partnerships (“FLP”) are helpful succession planning tools.– The limited and general partners don’t have to be

people – they can be entities. If a farm operation has broken its business down into multiple business entities, a limited partnership can be a nice cover layer for farms concerned about the estate tax.

Corporations

• Every owner (or shareholder) is given liability protection so long as the corporation is properly capitalized and adheres to corporate formality requirements– Corporations have more

corporate formality requirements than limited liability companies

Types of Corporations for Taxes

• Taxed on its earnings and its shareholders taxed from the corporation (i.e., double taxation)

• Can be a publically traded company

C-Corporations

• Pass-through tax for shareholders (no corporate tax)

• Requires 75 or fewer shareholders who are natural persons, no non-resident alien shareholders, and only 1 class of stock

S-Corporations

• Charitable “for profit” entity – working for the public benefit

B-Corporations

Corporations• Filing Requirements

– Must file Certificate of Incorporation with the NYSDOS pursuant to NY Business Corporation Law (“BCL”) §402

– $125 plus applicable tax on shares

• Internal Documents– Bylaws discuss internal governance

• Shareholders elect Board of Directors, who manage corporate affairs

• Board of Directors elect officers under BCL § 715

– Might also choose to have a shareholder agreement

Limited Liability Companies

• Nice hybrid between partnerships and corporations – can decide how to be taxed (e.g., C-corp or S-corp)

• Liability protection for the owners (called “members”) so long as the LLC is properly capitalized and LLC formalities are properly adhered to

Limited Liability Companies

• Filing Requirements– Must file Articles of Organization

with the NYSDOS pursuant to Section 203 of the New York State Limited Liability Company Law (“LLCL”)

– Must also comply with publication requirement• Can be expensive in New York,

depending on the county

• Internal Documents– Operating Agreement

Piercing the Corporate Veil

• Simply because your farm or food business forms a corporation or limited liability company, does not mean that a court will not hold the owners personally liable for the company’s debt

• Court can “pierce the corporate veil” if:– Grossly undercapitalized– Flagrant disregard for corporate

formalities– Owners treat corporation as

their “alter ego”

Keeping the “Corporate Shield”

• Get a corporate formalities “check-up” – Are you up to date?

• Annual member/board of director minutes

• Look at the Operating Agreement or Bylaws to ascertain what you need

– Have you properly complied with formation requirements?• Example: I meet a lot of LLC

business owners that haven’t complied with publication requirement in New York and don’t have an Operating Agreement

Keeping the Corporate Shield

• Keep personal assets and corporation/LLC assets separate– Don’t co-mingle assets

• Put contracts and title of corporation/LLC property in the business name– Use corporation/LLC

letterhead

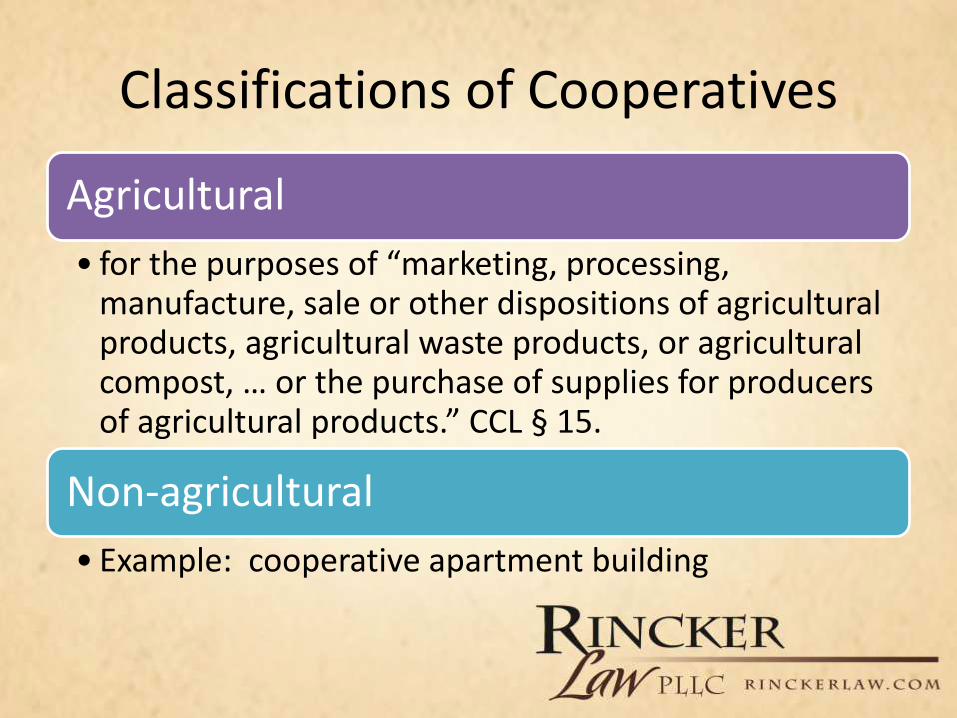

Cooperatives

• Multiple people organized to carry on business on a cooperative basis

• Cooperatives are formed for the mutual benefit of the members (owners) – CCL § 40

• Usually, cooperatives are formed so that members may procure goods and services on a collective basis or market their products through a group activity

Classifications of Cooperatives

Agricultural

• for the purposes of “marketing, processing, manufacture, sale or other dispositions of agricultural products, agricultural waste products, or agricultural compost, … or the purchase of supplies for producers of agricultural products.” CCL § 15.

Non-agricultural

• Example: cooperative apartment building

Management of Cooperatives• Analogous to business

corporations– Few differences

• Owned by members (vs. shareholders)

• May be formed with or without capital stock (returns are limited under the law)

• Democratically controlled – One member = one vote; or– Proportional voting system

– Like corporations, managed by a Board of Directors, elected by the members

Trusts

• Vocabulary– Creator

– Trustee

– Beneficiary

• Trusts are another form of business entity for food and agriculture businesses and can be utilized in a variety of scenarios

• Can also be a useful estate planning tool

2 Basic Trusts

• Trusts should almost always be revocable

• Retain control of all the assets in the trust

• Example: Living Revocable Trust

Revocable Trusts

• Can be beneficial in limited circumstances, such as Medicaid

• Assets are no longer yours and you cannot make changes without the beneficiary’s consent

• Appreciated assets are not subject to estate taxes

• Example: Irrevocable life insurance trust

Irrevocable Trusts

Example of Revocable Living Trust

• A farm family who wants to give their child livestock, land, and/or cash property in the from of a trust– Graduated control (age 22,

26, 30)

– Could open up own bank account

– Name on registration papers for livestock had to be in the name of the trust

Example of Revocable Living Trust

• Grandparents put the farmland in a RLT– Grandparents are the trustees– Children are the beneficiaries– Grandchildren are the contingent

beneficiaries

• Like a LLC or corporation, trusts have to maintain various formalities

• Big advantage with trusts: passes by operation of law and avoids probate– Private– Transfer is automatic –this is helpful

if the farm is involved in federal farm programs

Examples Specialized Trusts

• Created in a Last Will and Testament

Testamentary Trusts

• Also created in a Last Will and Testament

• Bequeath an amount to the trust up to but not exceeding the estate-tax exemption; then pass the rest of the estate to your spouse tax-free

• Forever free of estate tax, even if it appreciates

Credit Shelter Trust (a/k/a Bypass or Family Trust)

• Allows one to transfer a substantial amount of money tax-free to beneficiaries who are at least two generations younger (i.e., grandchildren)

Generation-Skipping Trusts (“Dynasty Trust”)

• For the benefit of companion animals, including horses

Pet Trusts

Not-for-Profit Corporations

• A nonprofit corporation doesn’t mean that the entity doesn’t make profit – its profit is just not distributed with the shareholders/owners– Not-for-profit does not mean no

profit! It’s okay to make money– Can pay employees a salary like any

other type of business– Restrictions and oversight on how

money can be spent– Corporate formalities similar to for-

profit entities– Filing fee in New York is $75 for the

Certificate of Incorporation– Must also comply with federal tax

code

Not-for-Profit Corporations

• Like for-profit corporations, it must have Bylaws– Examples of Bylaws for

farmers’ markets can be found on the Farmers Market Coalition website

– Should be drafted broadly, but should include:• Purpose

• Board of Directors

• Methods of operation

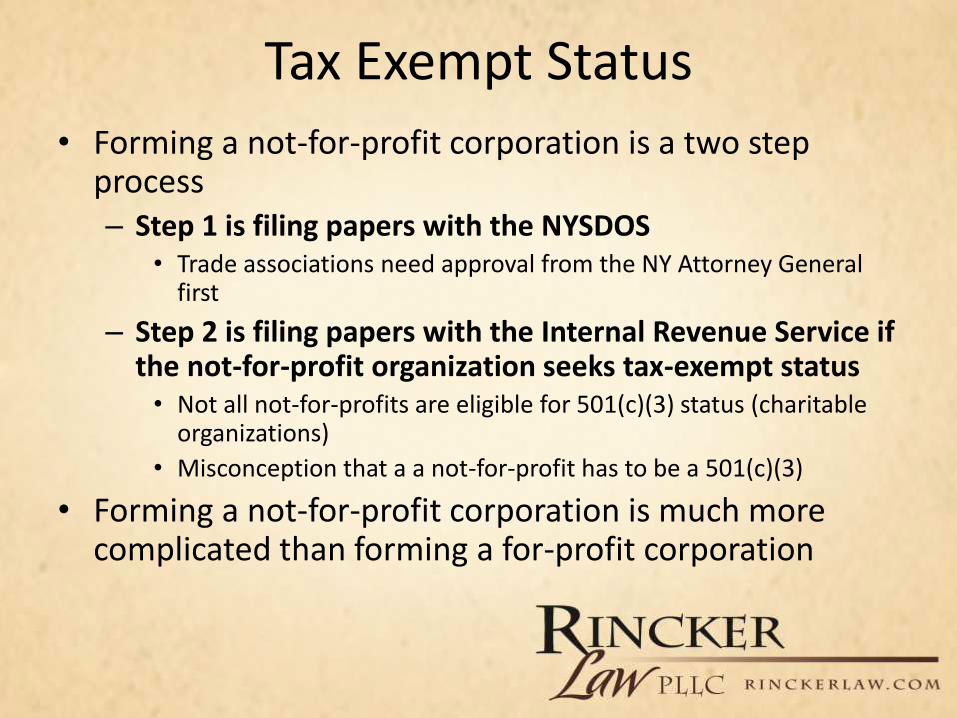

Tax Exempt Status

• Forming a not-for-profit corporation is a two step process– Step 1 is filing papers with the NYSDOS

• Trade associations need approval from the NY Attorney General first

– Step 2 is filing papers with the Internal Revenue Service if the not-for-profit organization seeks tax-exempt status• Not all not-for-profits are eligible for 501(c)(3) status (charitable

organizations)

• Misconception that a a not-for-profit has to be a 501(c)(3)

• Forming a not-for-profit corporation is much more complicated than forming a for-profit corporation

Tax Exempt Status

• Food and agriculture organizations have 3 primary choices in becoming a tax-exempt organization– 501(c)(3)-Charitable organization– 501(c)(4)– 501(c)(5)

• These are sections in the tax code under 26 United States Code (“USC”).

• Section 501(c) enumerates the list of tax exempt organizations

501(c)(3) – Charitable Organizations

“Corporations, and any community chest, fund, or foundation, organized and operated exclusively for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or to foster national or international amateur sports competition (but only if no part of its activities involve the provision of athletic facilities or equipment), or for the prevention of cruelty to children or animals, no part of the net earnings of which inures to the benefit of any private shareholder or individual, no substantial part of the activities of which is carrying on propaganda, or otherwise attempting, to influence legislation (except as otherwise provided in subsection (h)), and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office.”

(Emphasis Added)

Charitable Deduction

• Being able to form a 501(c)(3) offers several advantages for a not-for-profit organization, primarily that donations will be considered charitable contributions

Example: New York Agri-Women

• I am the Founding Member of New York Agri-Women.

• Its purpose is three-fold. To educate:– The fellow agriculture

community – Consumers – Elected Officials

• Are we eligible for 501(c)(3) status?

501(C)(4)- Civic Organizations

“(A) Civic leagues or organizations not organized for profit but operated exclusively for the promotion of social welfare, or local associations of employees, the membership of which is limited to the employees of a designated person or persons in a particular municipality, and the net earnings of which are devoted exclusively to charitable, educational, or recreational purposes.(B) Subparagraph (A) shall not apply to an entity unless no part of the net earnings of such entity inures to the benefit of any private shareholder or individual.”

(Emphasis Added)

501(c)(5)- Labor, Agriculture or Horticulture Organizations

“Labor, agricultural, or horticultural organizations.”• Usually designed to encouraged

improvement in animal breeding and farming.

• Can promote agriculture, horticulture and civic activities among rural residents

Liability

Liability

• 2 Main Types of Liability

– Premises Liability

– Products Liability

Premises Liability • Applicability with Local Food

– Farmers’ Markets– Roadside stands– Pick-Your-Own – Agri-Tourism/ Agri-Tainment– On-Farm Sales

• Livestock• Produce• Meat• Dairy

– Farm Tours– Cooking Classes

Premises Liability

• Property Owner Has Different Standards of Care

– Trespassers

– Children

– Licensees

– Invitees

• This is what we’ll focus on

Premises Liability: Invitees

• Landowners owe the highest duty of care to an invitee, or members of the public that enter the land for the purpose of business dealings.

• Examples include the following: (1) farmstands, (2) pick-your-own produce, (3) cooking classes, (4) on-farm horse or livestock sales, (5) corn mazes, (6) hay rides, (7) petting zoos, and (8) farm tours.

Premises Liability: Invitees• Landowner will be subject to liability for

physical harm caused by invitees by a condition on the land if he/she failed to exercise reasonable care and he/she knew or should have known about the harmful condition and it would be expected that the public would not discover the dangerous condition. – Landowners have the duty to warn invitees of

potentially dangerous conditions.

Premises Liability: Invitees

• Landowners who have members of the public come on their property should use barriers to prevent the public from entering areas of the property that may be potentially hazardous. There should be signs warning invitees of potential hazards.

• Landowners with pets should be particularly mindful of potential injuries (e.g., dog bites).

My dog, Taylor

Products Liability• Products liability is the legal

responsibility for personal injuries and property damage caused by defective products.

– Potential liability attaches to every set of hands that touch a food product until it gets to the consumer.

• Farms and food entrepreneurs selling food directly to the consumer increase their likelihood for potential products liability issues.

Products Liability

• States differ in the products liability theory they employ – New York is a strict liability state. – To illustrate, if a consumer at a

pick-your-own farm picks and then consumes berries and becomes ill because the berries were contaminated, a New York court will likely hold the producer strictly liable for the consumer’s injuries.

Some products like meat and dairy,have more products liability risk.

Common Risk Management Methods

• Business Organizations– Limited Partnerships

– Limited Liability Companies

– Corporations

• Insurance– We’ll talk more about this

next

• Food safety/sanitation

Insurance

Insurance is a Contract

• Drafted in favor of the insurance company

• Not all insurance products are the same– Food and agriculture lawyers

should review insurance policies for the client to ensure there are not any concerns

– Pay attention to the duties of the client under the insurance policy

Insurance is a Contract

• Insurance Company – Duty to indemnify the

insured – Duty to defend the

farmer/food entrepreneur in a law suit for a covered risk

• Insured– Duty to pay the premium– Duty to cooperate– Duty to disclose toe the

insurance company relevant information

Duty to Defend• The insurance company’s duty

to defend is carried out by hiring an attorney chosen by the company and controlling that attorney’s right to settle.

• If the farmer or food entrepreneur is dead set against settling, the insurance company has the right to do so anyway.

• Once the insurance company pays out its policy limits, it has no further duty to defend the farmer or food entrepreneur.

Insurance is a Risk Management Tool

• Put simply, the purpose of an insurance policy is to shift the financial risk of the food and agriculture operation to the insurance company.

• The insurance company will pay any covered claim (up to the limit) and defense costsin a lawsuit (including attorneys’ fees and court costs).

Insurance is a Risk Management Tool

Clients might be tempted to save money on insurance premiums (the cost of the insurance) by hand-selecting only limited coverages that they think they are likely to need with high deductibles (the out-of-pocket amount they’re responsible for if a loss occurs).

Insurance is a Risk Management Tool

Inadequate amounts of insurance that won’t pay out what the farmer or food entrepreneur will need to stay up and running if a loss occurs.

Claims-Made vs. Occurrence Based

Claims-Made

• Will only cover the insured for claims made within the window of time the insurance policy is in effect so long as the claim is made within the specified time

Occurrence-Based

• Covers anything that happens within a certain window of time and will “pay out” regardless of when the claim is made to the insurance company

Educate your client on the type of policy they have

Pay Attention to Exclusions• An insurance contract almost

always carves out exclusionsfrom coverage. – intentional acts, such as theft

by employees – assaults, – alcohol-related events

• Other exclusions may relate more specifically to the type of insurance involved. – For example, a typical

farmowners policy might not be adequate to insure against losses suffered from the flooding of a nearby creek

Know the Type of Coverage

• intended to compensate for losses from causes like fire, lightning, explosion, windstorm, hail, riot or civil commotion, aircraft or vehicle, vandalism, theft, sinkhole collapse, and volcanic action.

Basic Coverage

• include all of the above and adds additional coverage for damage from causes like the weight of ice, snow, or sleet, falling objects and accidental discharges of water.

Broad Form Coverage

• Includes the same protections in basic and broad coverage

• Also offers open peril coverage under which other causes of damage are covered unless they are specifically excludedunder the farm policy (e.g., flood loss).

Special Coverage

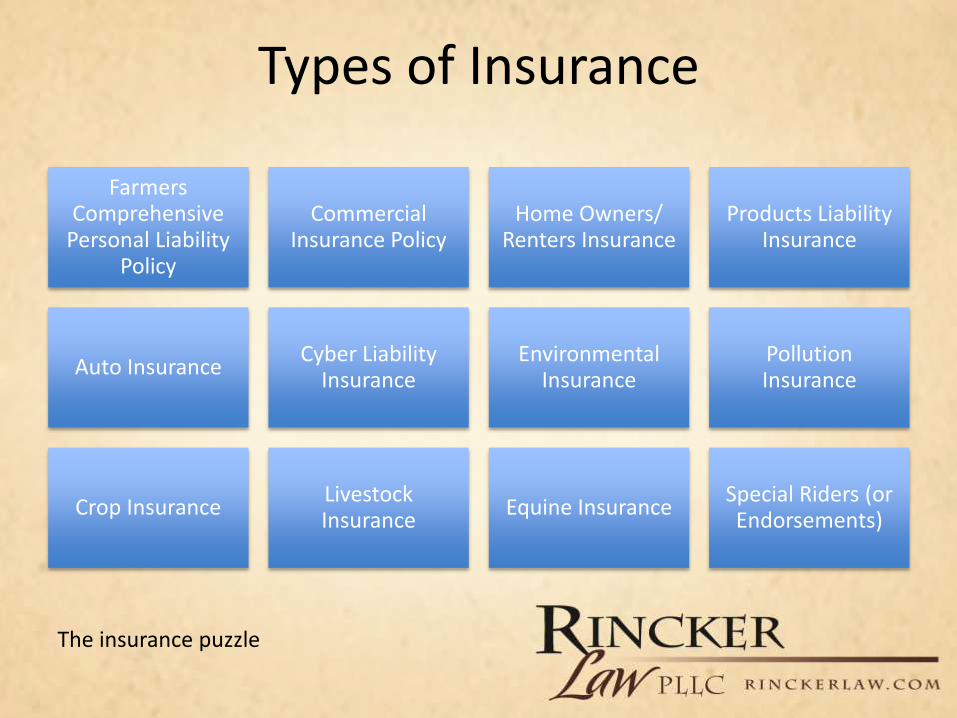

Types of Insurance

Farmers Comprehensive

Personal Liability Policy

Commercial Insurance Policy

Home Owners/ Renters Insurance

Products Liability Insurance

Auto InsuranceCyber Liability

InsuranceEnvironmental

InsurancePollution Insurance

Crop InsuranceLivestock Insurance

Equine InsuranceSpecial Riders (or Endorsements)

The insurance puzzle

Farmers Comprehensive Personal Liability (“FCPL”) Policy

• A/k/a “Farmowner’s Insurance”• Most farms use a farmowner’s insurance policy to cover the

ordinary risks of a farming operation. • This type of policy normally only covers activities ancillary

to farming (i.e., not agri-tourism or cottage food operations).

• Pay special attention to the exclusions section in this policy to see what is not covered. – Sale of processed vegetables or meat products at a farmers’

market or roadside stand – Injuries to the policyholder or family member– Property damage by the insured him/herself.

Homeowner’s/ Renters Insurance

• Homeowner’s insurance usually does not cover business activities.

• Therefore, clients should consider a commercial policy if they have a home business office, cottage food operation, a rooftop garden, offer in-home cooking classes, or sell produce from their home.

Commercial Insurance• A commercial insurance policy or endorsement is

appropriate for operations engaging in business outside the scope of the basic farmowners’ insurance policy. – For example, most farmowners’ policies cover products

liability for the sale of raw food products, whereas the commercial insurance policy may cover personal injuries (such as slip and falls and other types of injuries not related to defective products) resulting from the sale of processed food products (e.g., slicing vegetables, cutting meat products, making beef jerky).

• A commercial insurance policy should be purchased if a business is being run out of a home, has agri-tourism activities, or engages in on-farm poultry slaughter.

Products Liability Policy

• Products liability policies help provide coverage for liability resulting from an illness or death due to contaminated food products sold by the purchaser.

• It is highly suggested that farms involved with the direct marketing of food products to consumers, schools or restaurants have products liability insurance.

• Farms selling raw milk should also consider a products liability policy.

Crop Insurance

• Federal crop insurance is subsidized by the U.S. Department of Agriculture (“USDA”) Risk Management Agency (“RMA”).

• It protects the producer against crop losses due to natural disasters such as drought or flood.

• It is available for nearly every type of commodity ranging from sweet corn to raisins.

Livestock Insurance

• There are two types of livestock insurance:

– RMA reinsured livestock insurance (similar to the federal crop insurance program)

• Natural causes only

– private livestock insurance

• Wider coverage, including theft

• Common with horses

Cyber Insurance• This is a fairly new type of

insurance, relatively speaking, and it addresses risks associated with doing business over the Internet (or e-Commerce).

• Covered risks can include privacy issues, infringement of intellectual property (trademark or copyright infringement), stolen credit card information (from PayPal, Google Checkout or other online credit card processor) or computer viruses.

Motor Vehicle Insurance

• Food and agriculture operations should pay special attention to their auto insurance policies if vehicles are used to transport goods, livestock or special equipment.

• A commercial automobile policy or special rider might be needed.

Special Riders/ Endorsements• There are many special activities on

agriculture or food operations that require amendments to the underlying policies.

• Examples of these special activities may include agri-tourism/agri-tainment, petting zoos or other activities where the public is in direct contact with animals, equine, custom farm work, on-farm poultry slaughter, production of processed foods, use of ATV’s, and the transportation of frozen genetics (e.g., embryos, semen).

Umbrella Insurance• The name “umbrella” improperly infers that

umbrella insurance adds coverage in the “holes” of existing insurance policies; instead, umbrella insurance should be viewed as a “top hat.” – It essentially raises your already existing limits and

existing coverage. – For example, if you have a $1 million farmowner’s

insurance policy with the $2 million umbrella, the umbrella policy would protect the farm against a $2 million court judgment.

• Umbrella insurance does not “fill in holes” in your existing insurance policies – it simply increases the limits.

How Much Insurance Coverage Does a Farm or Food Entrepreneur Need?

• Depends on budget and risk appetite

• Most operations should have at least $1 million

– Rule of thumb: should be more than the amount of assets that you have

• Depends on

– Type of operation

– Assets to protect

– Other risk management techniques

Oh, P.S. – I Just Wrote a Book

Cari B. Rincker & Patrick B. Dillon, “Field Manual: Legal Guide for New York Farmers & Food Entrepreneurs” (2013)

Available at http://www.amazon.com/Field-Manual-Legal-Farmers-Entrepreneurs/dp/1484965191

Also available on Kindle

Please Stay in Touch• Send Me Snail Mail: 535 Fifth Avenue, 4th Floor,

New York, NY 10017

• Call Me: (212) 427-2049 (office)

• Email Me: [email protected]

• Visit My Website: www.rinckerlaw.com

• Read My Food & Ag Law Blog: www.rinckerlaw.com/blog

• Tweet Me: @CariRincker @RinckerLaw

• Facebook Me: www.facebook.com/rinckerlaw

• Link to Me: http://www.linkedin.com/in/caririncker

• Skype Me: Cari.Rincker