Outlook on Timber Prices and End-use Markets · Outlook on Timber Prices and End-use Markets ......

40

Outlook on Timber Prices and End-use Markets Bob Flynn, Director, International Timber Timber Invest Europe Conference, London, October 23, 2012

-

Upload

duonghuong -

Category

Documents

-

view

223 -

download

1

Transcript of Outlook on Timber Prices and End-use Markets · Outlook on Timber Prices and End-use Markets ......

Outlook on Timber Prices and End-use Markets

Bob Flynn, Director, International Timber

Timber Invest Europe Conference,

London, October 23, 2012

RISI Timber

Teams of Economists,

Analysts and Editors in

Local Offices

Living In, Working In and

Knowing Every Region

A Global Perspective That

Understands Regional Impact

Regional Expertise with a Global Perspective

Agenda

• What is “the price” of timber?

• Some points on key markets

– Pulp and paper

– Logs, lumber and woodchips

– China, India, and the USA

• Lessons learned?

Wood is a fantastic material, but its

incredible diversity of uses makes it

difficult to outline the key demand drivers • Wood can be used for:

– Building your house

– Printing your newspaper or textbooks

– Packaging products ranging from industrial equipment to food

– Making your clothes

– Producing furniture for you to sit on, or floors to walk on

– Making a gazebo or fence for your backyard

– Producing biofuels to run your car, biomass power to light your

city, or thermal heat to warm your house

– Make an incredibly wide range of specialty chemicals

– Produce tissue products for numerous uses

• The point is, to understand the drivers of timber

prices you have to know the target market.

Timber prices also depend on your location:

the same product can have wildly different

price trends in different markets

20

25

30

35

40

45

50

55

60

06

-Q1

06

-Q2

06

-Q3

06

-Q4

07

-Q1

07

-Q2

07

-Q3

07

-Q4

08

-Q1

08

-Q2

08

-Q3

08

-Q4

09

-Q1

09

-Q2

09

-Q3

09

-Q4

10

-Q1

10

-Q2

10

-Q3

10

-Q4

11

-Q1

11

-Q2

11

-Q3

11

-Q4

12

-Q1

US$

pe

r C

ub

ic M

ete

r

Pine Pulpwood Prices

US South

Sweden

Source: World

Timber Price

Quarterly, RISI,

2012

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

$700

2006 2007 2008 2009 2010 2011 2012

West Coast (Doug-Fir #2)

West Coast (White Woods #2)

South (Pine)*

Inland West (White Woods)

*Assumes 7.5 short tons per MBF.

(Delivered Sawtimber Prices Compared, $/MBF, Scrib., qtrly)

Even within the same country prices for softwood logs can be moving in different directions, e.g. record lows in US South, sharp revival in PNW

Source:

North

American

Timber

Forecast,

RISI, 2012

In general, timber raw material is bulky and

cannot be transported far to market without

first adding value….however---

Wood pellets

FSC eucalyptus logs

Teak logs

Woodchips

Know your woodfiber – what products

can you make, at a competitive cost?

100

120

140

160

180

200

220

240

2006 2007 2008 2009 2010 2011

US$

pe

r B

DM

T

CIF Prices for Eucalyptus Woodchip Imports in Japan

Chile

Thailand

Source: International Pulpwood Trade Review, RISI, 2012

“Global” trends and conventional

wisdom can be misleading

4,000

5,000

6,000

7,000

8,000

9,000

Th

ou

sa

nd

To

nn

es

USA: Imports and Exports of Wood Pulp

Imports Exports

European power

producers understood

that, in general, pulp

production was shifting

from northern hemisphere

to large, new pulp

production facilities in

Brazil, Indonesia, etc.,

which would mean that

closure of pulp facilities in

the US South would free

up millions of tonnes of

wood for biomass exports

to Europe. For hardwood

(short fiber) pulp this is

largely true.

But for softwood (long-fiber) pulp, US

producers are among the most competitive

in the world, with exports reaching record

levels in 2011

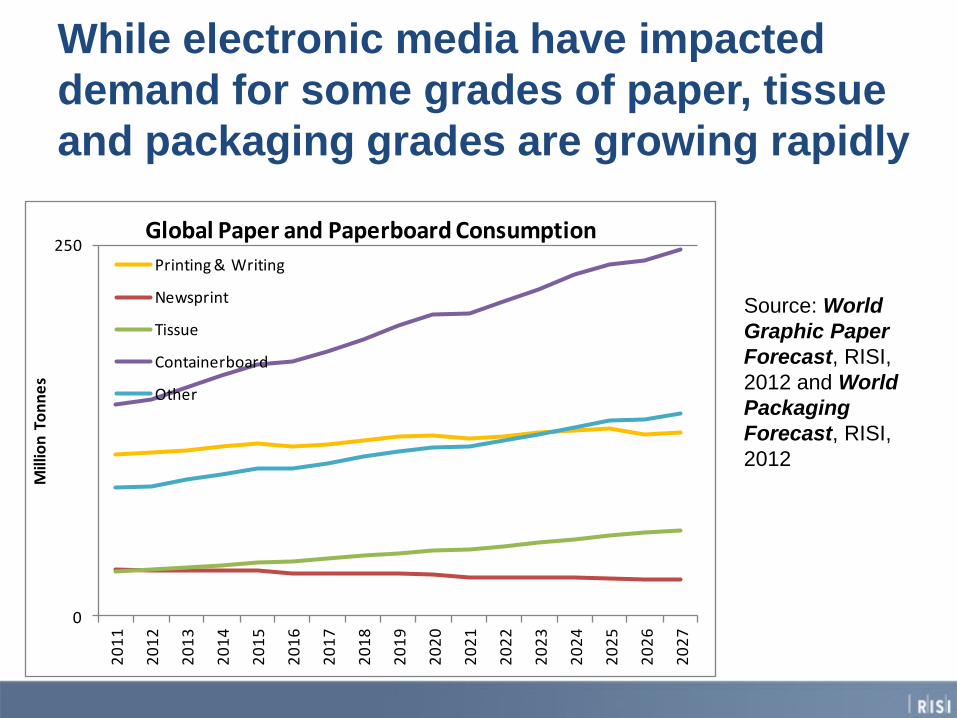

While electronic media have impacted

demand for some grades of paper, tissue

and packaging grades are growing rapidly

0

250

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

Mill

ion

To

nn

es

Global Paper and Paperboard Consumption

Printing & Writing

Newsprint

Tissue

Containerboard

Other

Source: World

Graphic Paper

Forecast, RISI,

2012 and World

Packaging

Forecast, RISI,

2012

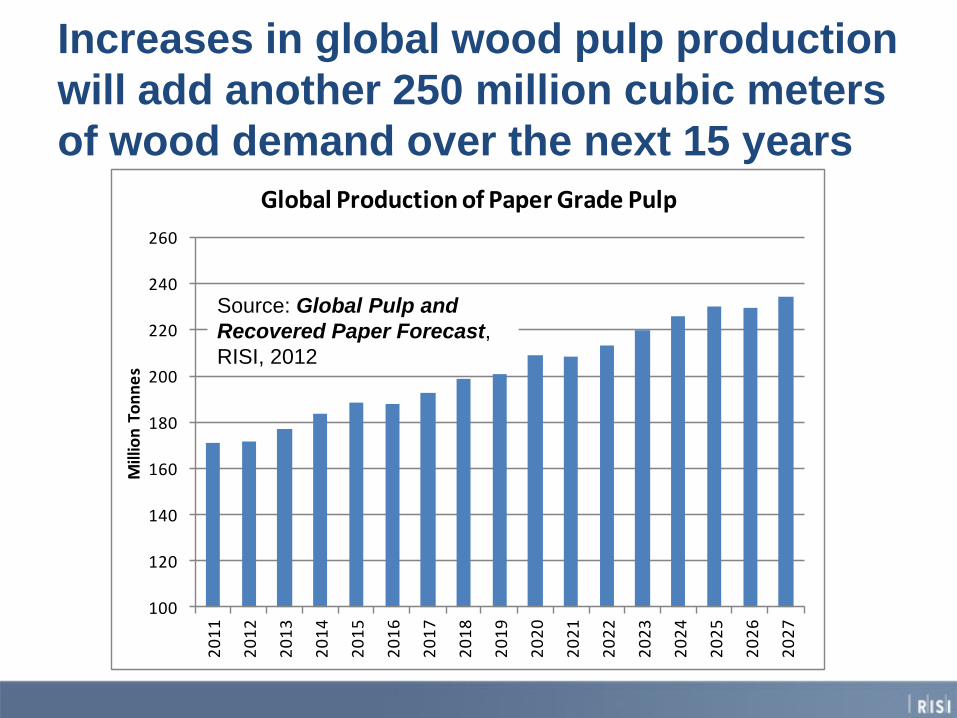

Increases in global wood pulp production

will add another 250 million cubic meters

of wood demand over the next 15 years

100

120

140

160

180

200

220

240

260

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

Mill

ion

To

nn

es

Global Production of Paper Grade Pulp

Source: Global Pulp and

Recovered Paper Forecast,

RISI, 2012

The location of new pulp production is highly

variable, & does not necessarily correspond with

the location of wood resources or pulp demand

0

10

20

30

40

50

60

Mill

ion

To

nn

es

Wood Pulp Production Forecast, 2011-2027

2011 2027

Japan is the biggest woodchip market, but it is

increasing Chinese imports that are pushing the

hardwood chip trade in Asia to record levels

0

4

8

12

16

20

24

2006 2007 2008 2009 2010 2011 2012E 2013F 2014F

Mill

ion

BD

MT

Asian Hardwood Chip Imports, 2006-2014F

Korea Taiwan

China Japan

Woodchip imports will hit another all-time high

in 2012, but only 10% is softwood and that

share has been shrinking

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

E

Tho

usa

nd

BD

MT

Asian Woodchip Imports, 1991-2012E

Softwood Hardwood

Source:

International

Pulpwood

Trade

Review,

RISI, 2012

China’s timber deficit grew at nearly 17%

CAGR from 1997-2011, but has slowed to only

4.1% through the first 8 months of 2012

0

20

40

60

80

100

120

140

160

180

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12E

Millio

n C

ub

ic M

ete

rs, R

WE

China's Growing Timber Deficit, 1997 - 2012E

Woodchips

Pulp

Wood Panels

Lumber

Logs

Source: China

Timber Supply

Outlook, RISI,

2011

China’s demand for imported woodfiber

is equal to 10% of TOTAL world industrial

roundwood production

0

20

40

60

80

100

120

140

160

China USA Germany India

Mill

ion

Cu

bic

Me

ters

2011 Woodfiber Import Demand for Primary Products

Market shares can shift over time due to

government policies, changes in ocean freight

rates, Fx rates, available wood supplies, etc

0

2

4

6

8

10

12

14

16

Russia N Zealand USA Canada Australia Other

Mill

ion

Cu

bic

Me

ters

China Softwood Log Imports, January-Aug

2007 2011 2012

In the past, almost all of Canada’s lumber exports

went to the USA, but with that market in a deep

depression, producers found an outlet in China

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Canada Russia USA Chile N Zealand Other

Mill

ion

Cu

bic

Me

ters

China Imports of Softwood Lumber, January-Aug

2007 2011 2012

Why are European producers the leading

suppliers of softwood lumber to Japan, but

have only a tiny share of the Chinese market?

0%

5%

10%

15%

20%

25%

30%

35%

40%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Shar

e o

f Lu

mb

er

Imp

ort

s

European Share of Asian Softwood Lumber Market

Japan

China

China’s log and lumber imports: rebound likely

in 2013-2014

• China’s domestic softwood timber harvest is

constrained due to past over-harvesting and mandated

timber harvest reductions in softwood timber regions.

• Economic and construction activity mostly treading

water until new leadership takes over at year's end.

• Despite past over-building in some regions, economic

stimulus in 2013 is likely to provide a boost to housing

and other construction activity, requiring greater

imports of softwood logs and lumber.

• Despite much lower sawmilling costs in China, lumber

is likely to maintain or slightly increase its share of

softwood log and lumber imports to about 50% by

2014.

Much slower economic growth in India has

also slowed demand for logs in India in 2012

0

300

600

900

1200

1500

1800

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

E

Th

ou

sa

nd

Cu

bic

Me

ters

India: Imports of Softwood Logs by Source, 1999 - 2012E

Other Australia New Zealand

India’s economy in 2011 was the same size as

China’s in 2002….but its timber deficit was only

one-fifth the size of China’s, due largely to

differences in the level of housing construction

0

20

40

60

80

100

120

140

160

180

2002 2011 2012E

Mil

lio

n c

ub

ic M

ete

rs

Timber Deficit in China and India

China

IndiaSource: India’s

Forest Products

Industry, RISI,

Jan. 2013

3-year old clonal Casuarina plantation

in Andhra Pradesh, developed by

International Paper for their farm

forestry program

RISI Base Case Outlook for US Housing Starts

% Millions

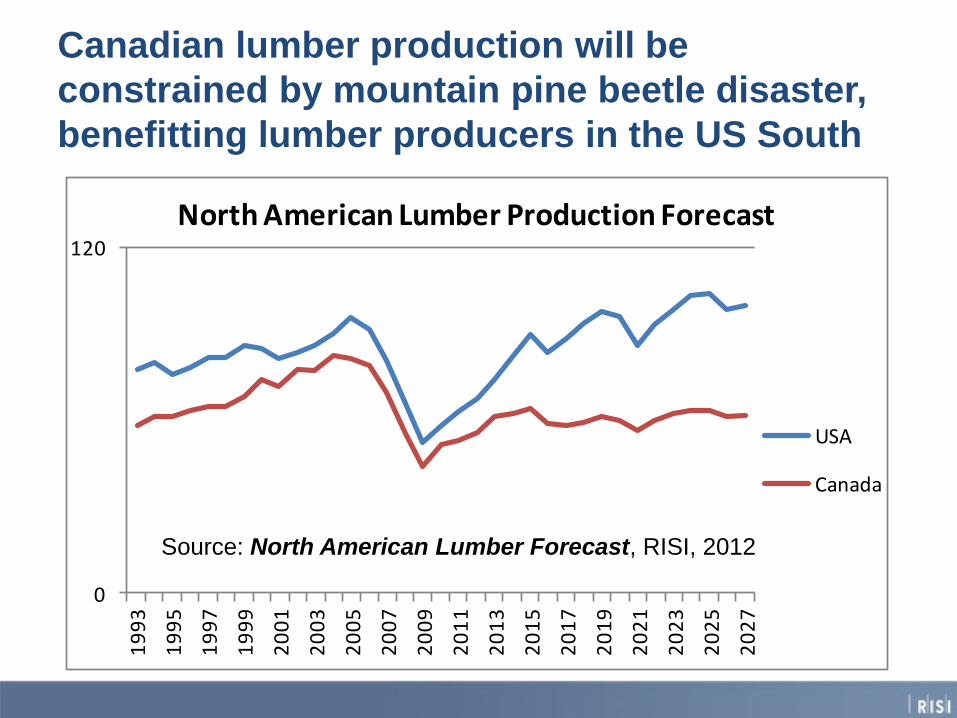

Canadian lumber production will be

constrained by mountain pine beetle disaster,

benefitting lumber producers in the US South

0

120

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

North American Lumber Production Forecast

USA

Canada

Source: North American Lumber Forecast, RISI, 2012

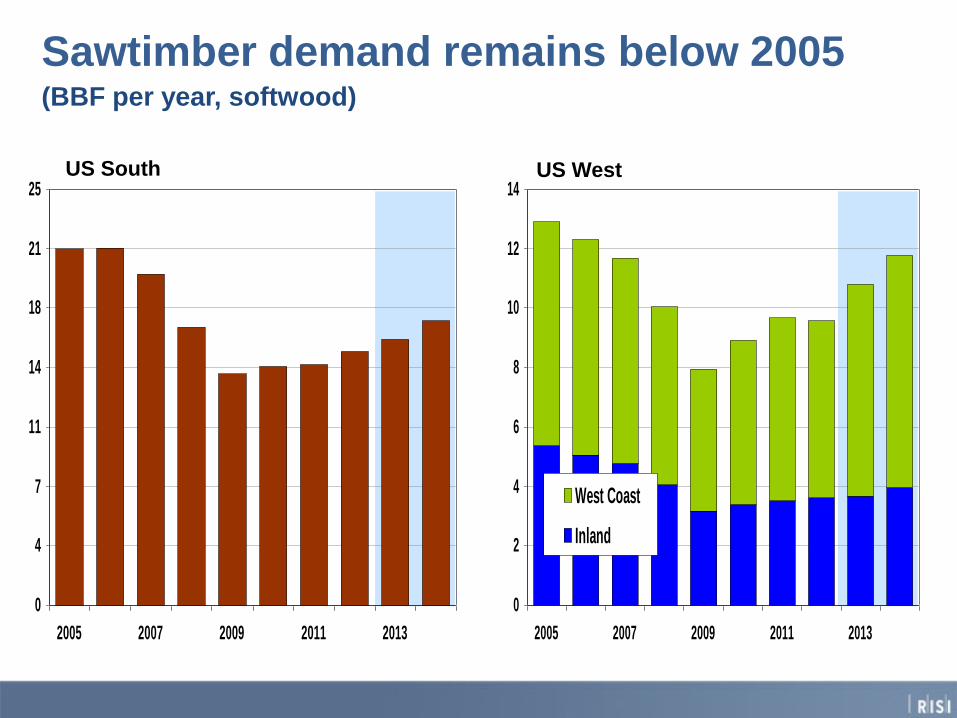

0

2

4

6

8

10

12

14

2005 2007 2009 2011 2013

West Coast

Inland

0

4

7

11

14

18

21

25

2005 2007 2009 2011 2013

Sawtimber demand remains below 2005 (BBF per year, softwood)

US West US South

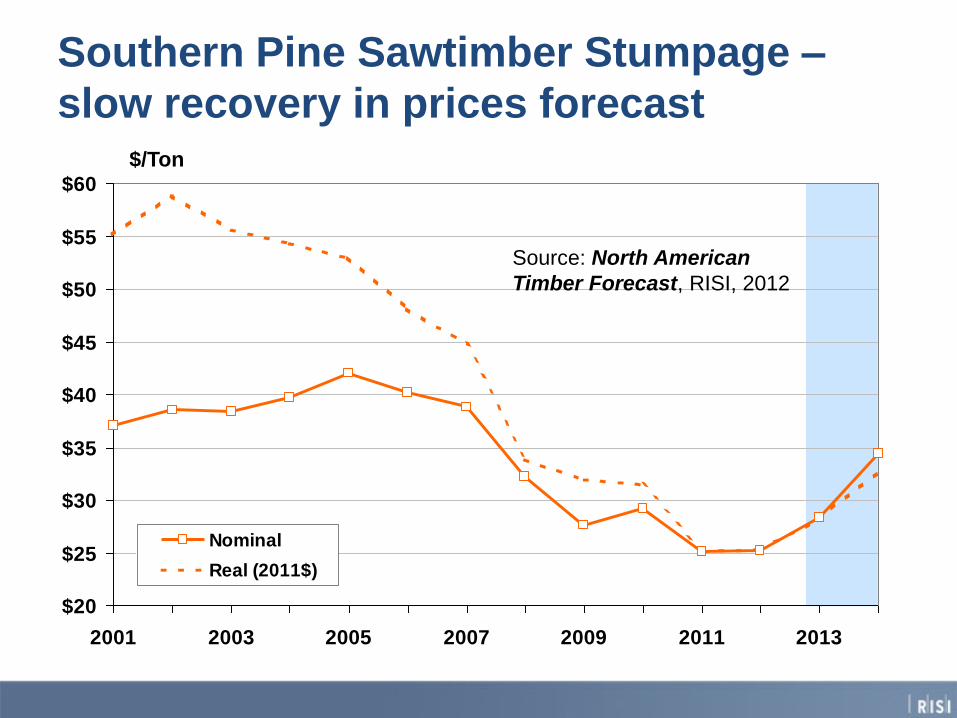

$20

$25

$30

$35

$40

$45

$50

$55

$60

2001 2003 2005 2007 2009 2011 2013

Nominal

Real (2011$)

Southern Pine Sawtimber Stumpage –

slow recovery in prices forecast $/Ton

Source: North American

Timber Forecast, RISI, 2012

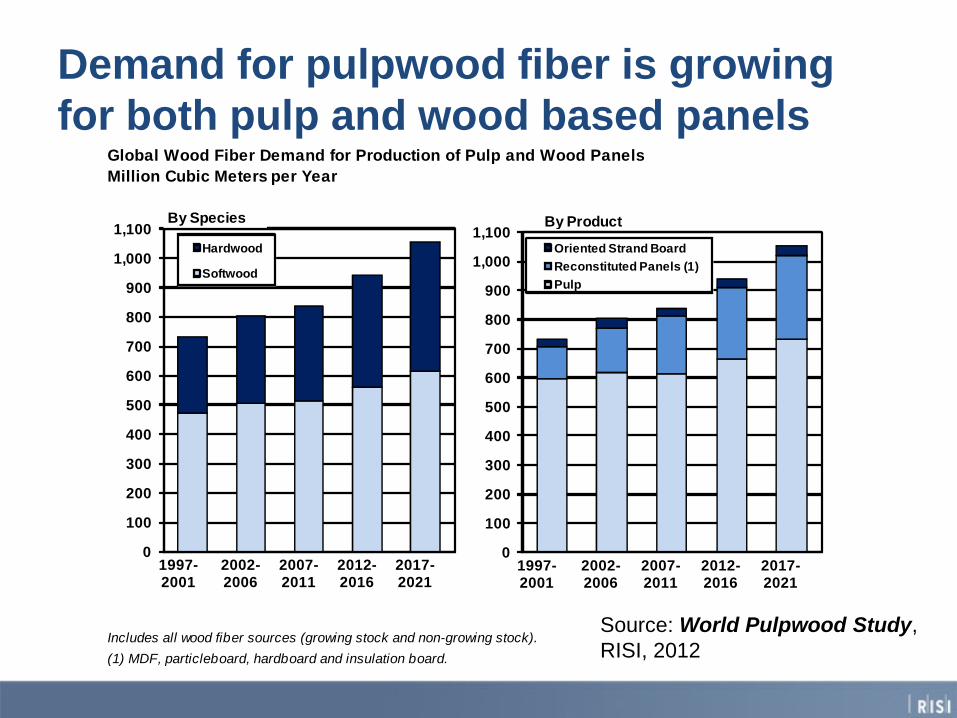

Demand for pulpwood fiber is growing

for both pulp and wood based panels Global Wood Fiber Demand for Production of Pulp and Wood Panels

Million Cubic Meters per Year

Includes all wood fiber sources (growing stock and non-growing stock).

(1) MDF, particleboard, hardboard and insulation board.

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1997-2001

2002-2006

2007-2011

2012-2016

2017-2021

Hardwood

Softwood

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1997-2001

2002-2006

2007-2011

2012-2016

2017-2021

Oriented Strand Board

Reconstituted Panels (1)

Pulp

By Species By Product

Source: World Pulpwood Study,

RISI, 2012

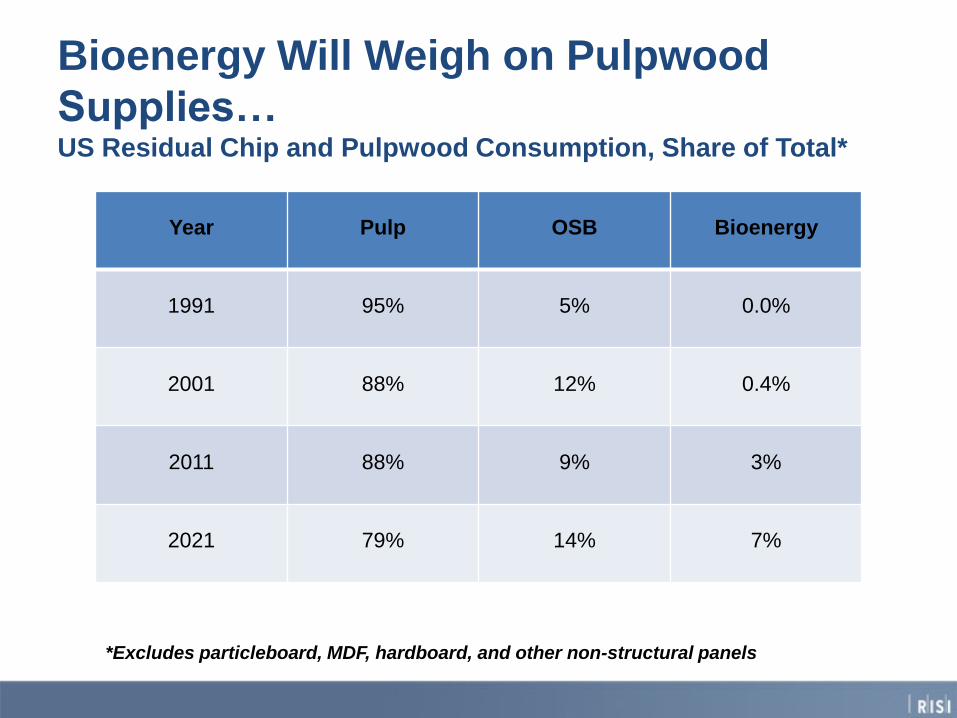

Bioenergy Will Weigh on Pulpwood

Supplies… US Residual Chip and Pulpwood Consumption, Share of Total*

*Excludes particleboard, MDF, hardboard, and other non-structural panels

Year Pulp OSB Bioenergy

1991 95% 5% 0.0%

2001 88% 12% 0.4%

2011 88% 9% 3%

2021 79% 14% 7%

Wood Pellet Exports from North America Million Tonnes

• North American wood

pellet exports exceeded

2 million tonnes in 2011

• Exports expected to

increase to 10 million

tonnes in 2017

• 2017 Forecast

– USA: 5.6 million tonnes

– Canada: 4.8 million tonnes

0

2

4

6

8

10

12

20

07

20

08

20

09

20

10

2011

20

12

20

13

20

14

20

15

20

16

20

17

USA Canada

Source: North American Bioenergy

Forecast, RISI, 2012

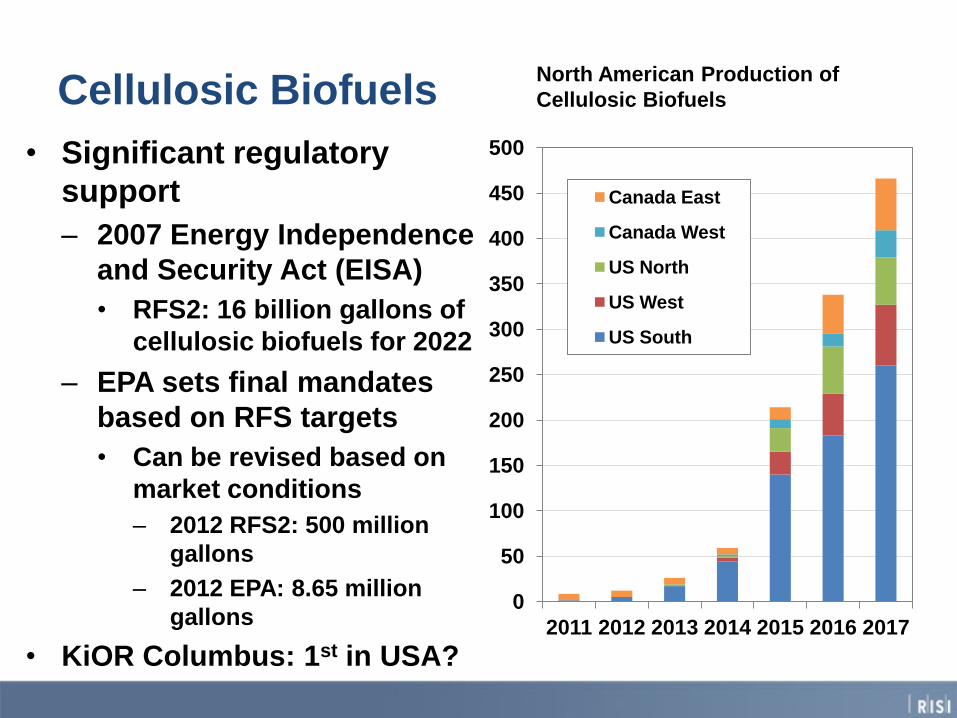

Cellulosic Biofuels

• Significant regulatory

support

– 2007 Energy Independence

and Security Act (EISA)

• RFS2: 16 billion gallons of

cellulosic biofuels for 2022

– EPA sets final mandates

based on RFS targets

• Can be revised based on

market conditions

– 2012 RFS2: 500 million

gallons

– 2012 EPA: 8.65 million

gallons

• KiOR Columbus: 1st in USA?

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014 2015 2016 2017

Canada East

Canada West

US North

US West

US South

North American Production of

Cellulosic Biofuels

Dedicated biomass crops – really just getting

started in many countries, but for some a way

to add new diversity to portfolio

• In the USA, great potential but little planted to date

• Remember that “biomass” also includes non-woody

sources, e.g., miscanthus, switchgrass, Arundo donax

• Integrated biomass and sawlog cropping (e.g.,

Greenwood Resources in Oregon) seems promising

• Some TIMOs (Greenwood, Regions) are planting

dedicated biomass crops in Europe, driven by EU

renewable energy targets and policies

• But in parts of South America (Brazil, Chile, Uruguay)

biomass crops are being established without subsidies,

based on the high cost of fossil fuels in some regions

Brazil and biomass tree crops: diversified

approach

• Foreign and domestic investors have been pursuing charcoal

options for the pig iron industry

• But industrial fuelwood consumption, much of it from dedicated

plantations, was 33 million m3 in 2011!

• Example: Energia Florestal is planting eucalyptus for fuelwood for

Cargill, Galvani and other major grain traders

• Example: ERB is growing dedicated eucalyptus for fuelwood, but

will sell steam (to Dow Chemical) and electricity into the grid from

its own CHP plant

• Projects also developing in other South American countries, e.g.

Greenwood in Chile

• Some projects still looking at dedicated plantations for pellet

production in NE Brazil, for export to Europe, but most biomass

production will be consumed within South America

Large-scale test of high-density eucalyptus

planting for biomass production, near Lins,

Sao Paulo state, Brazil

Photo from Dr.

Laercio Couto, aka

“Mr. Biomass Brazil”

A number of companies, including North American “TIMOs”,

are planting poplar or willow in Germany, Hungary, Poland

and other countries to produce biomass fiber

Photo from Michael

Weitz

RISI analyzed dedicated biomass

plantations as part of its 2012

report, Global Tree Farm

Economics Review

Greenwood Resources,

integrated sawlog and

biomass plantations,

Oregon

Summary: Lessons learned?

• There is no global price for “timber”, depends on:

– Target market (product + individual market preferences)

– Location of forest

– Fiber characteristics and processing technology

– Impact of exchange rates

– Fluctuations in ocean freight rates and other logistics factors

– Changes in government policies

– Housing is a major driver in many countries

– Exogenous factors – e.g. global warming and the pine beetle

– Evolution of markets, e.g. biomass

www.woodfibreconference.com

for online registration, conference program,

speakers, field trips and tours

Conference program includes:

1. Optional pre conference tour of Gallipoli

(5-7 April)

2. Optional pre conference field trip to Yildiz

Entegre, world's largest single site MDF

production complex (8 April)

3. Two days of Conference (9 & 10 April)

4. Optional post conference field trip to

Western Hungary to visit short rotation

hybrid poplar plantations managed by

Regions Timberland Group (11 & 12 April)

5. Partner’s tours

Questions?

• Bob Flynn

• Director, International Timber, RISI

• Phone: 1-253-565-4846

• Mobile: 1-360-471-6578

• Email: [email protected]

• Web site: www.risi.com

Presentation based on

• China’s Timber Supply Outlook, 2011-2015

www.risi.com/chinatimber

• International Pulpwood Trade Review, 2012

www.risi.com/pulpwood

• Global Tree Farm Economics Review, 2012

www.risi.com/treefarm