OUTLOOK OF GLOBAL PETROCHEMICAL INDUSTRY …starasia.org/img/StAR2017-Conference-Presentation/1...

29

OUTLOOK OF GLOBAL PETROCHEMICAL INDUSTRY – CHALLENGES AND OPPORTUNITIES STAR 2017 ROTOMOULDING CONFERENCE January 29, 2017 – Jaipur, India Philippe Montagne VP PolyOlefin Orient @ TOTAL PETROCHEMICALS

Transcript of OUTLOOK OF GLOBAL PETROCHEMICAL INDUSTRY …starasia.org/img/StAR2017-Conference-Presentation/1...

OUTLOOK OF GLOBAL PETROCHEMICAL

INDUSTRY – CHALLENGES AND

OPPORTUNITIES

STAR 2017 ROTOMOULDING CONFERENCE

January 29, 2017 – Jaipur, India

Philippe Montagne

VP PolyOlefin Orient @ TOTAL PETROCHEMICALS

GLOBAL SCENARIO OF

PETROCHEMICALS INDUSTRIES

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 2

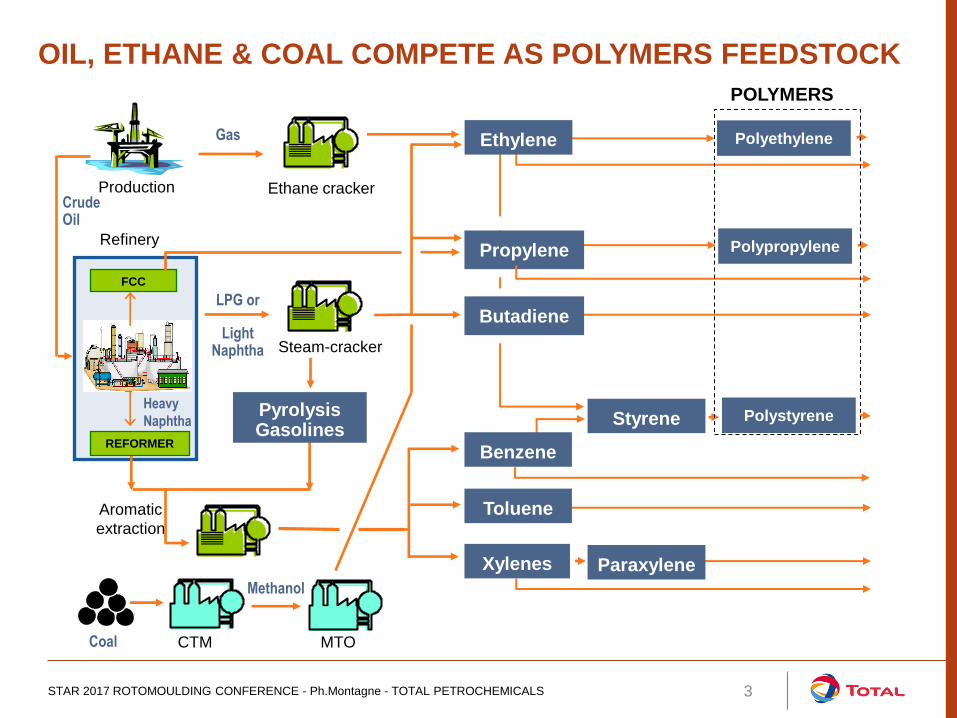

OIL, ETHANE & COAL COMPETE AS POLYMERS FEEDSTOCK

LPG or

Light Naphtha

Production

Steam-cracker

Ethane cracker

Gas

CrudeOil

Polypropylene

Polyethylene

Polystyrene

Benzene

Styrene

Toluene

Paraxylene

Xylenes

Ethylene

Pyrolysis Gasolines

Heavy

Naphtha

Butadiene

Propylene

FCC

Refinery

Aromatic

extraction

REFORMER

Coal

Methanol

MTO CTM

POLYMERS

3 STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

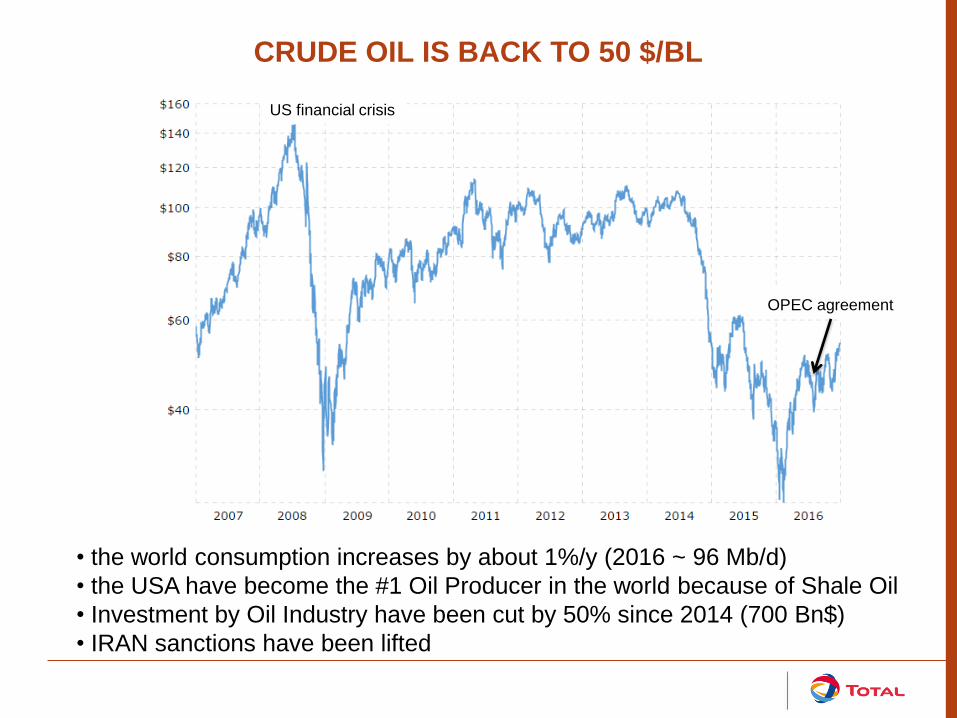

CRUDE OIL IS BACK TO 50 $/BL

• the world consumption increases by about 1%/y (2016 ~ 96 Mb/d)

• the USA have become the #1 Oil Producer in the world because of Shale Oil

• Investment by Oil Industry have been cut by 50% since 2014 (700 Bn$)

• IRAN sanctions have been lifted

US financial crisis

OPEC agreement

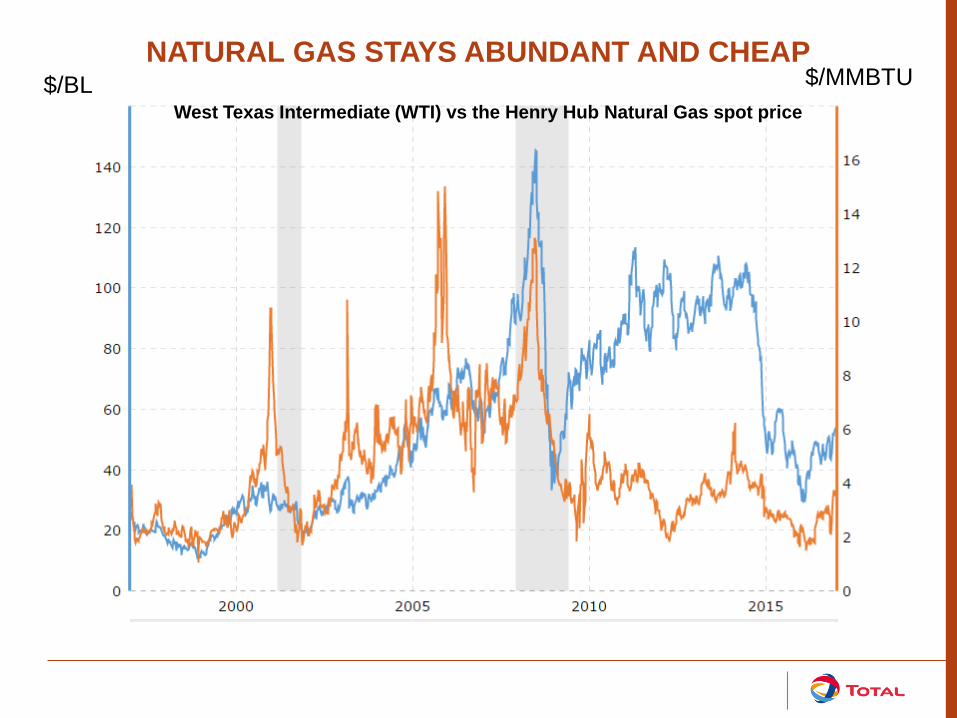

NATURAL GAS STAYS ABUNDANT AND CHEAP

West Texas Intermediate (WTI) vs the Henry Hub Natural Gas spot price

$/MMBTU $/BL

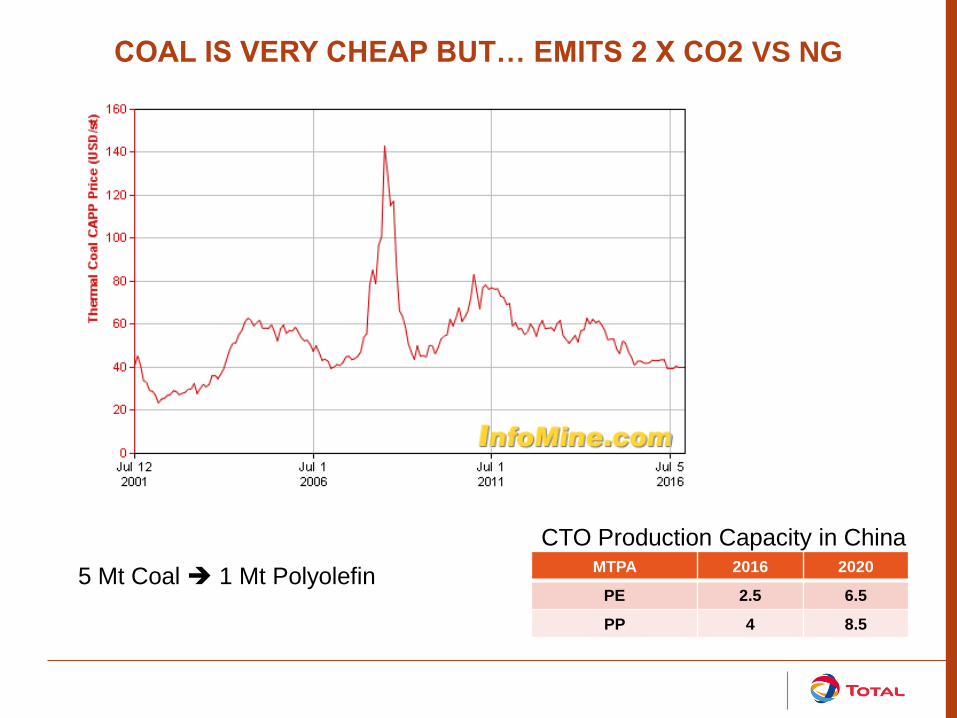

COAL IS VERY CHEAP BUT… EMITS 2 X CO2 VS NG

$/MT

MTPA 2016 2020

PE 2.5 6.5

PP 4 8.5

CTO Production Capacity in China

5 Mt Coal 1 Mt Polyolefin

7 STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

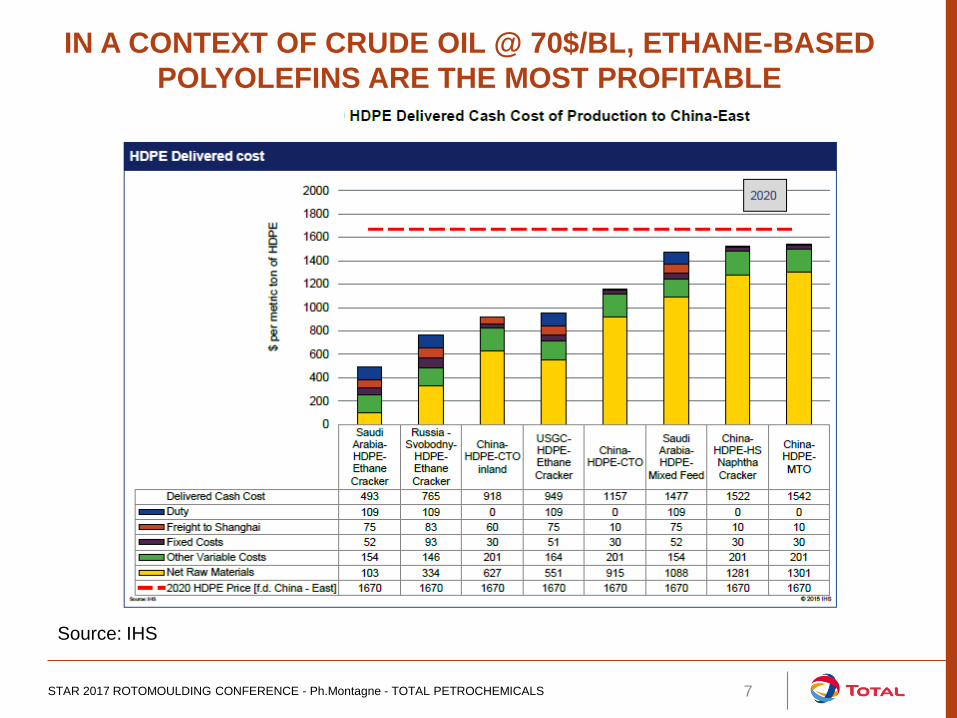

IN A CONTEXT OF CRUDE OIL @ 70$/BL, ETHANE-BASED

POLYOLEFINS ARE THE MOST PROFITABLE

Source: IHS

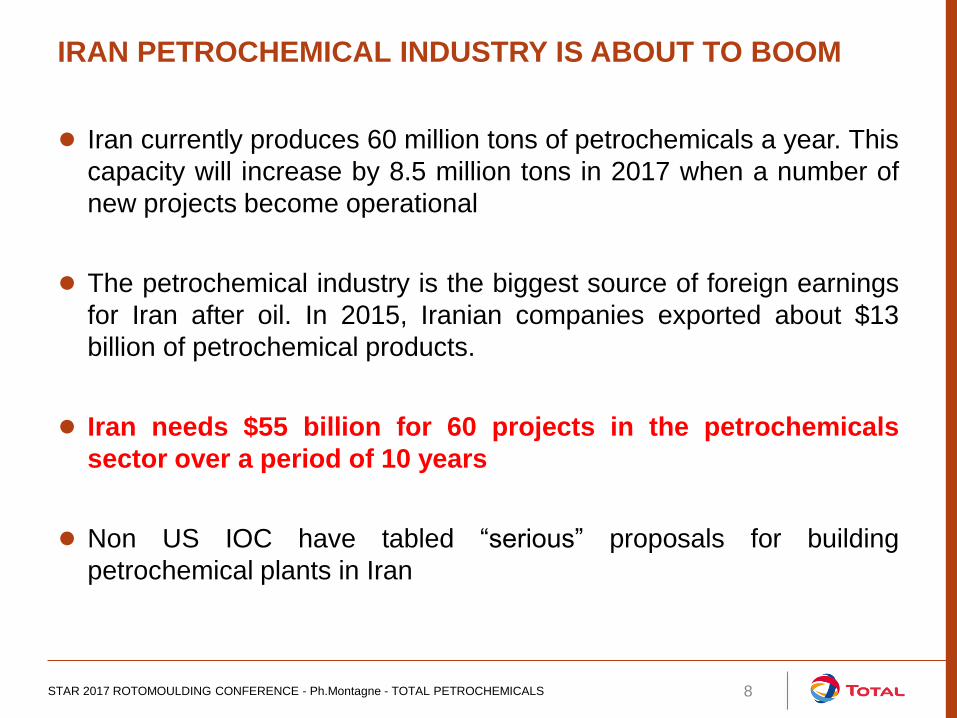

IRAN PETROCHEMICAL INDUSTRY IS ABOUT TO BOOM

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 8

● Iran currently produces 60 million tons of petrochemicals a year. This

capacity will increase by 8.5 million tons in 2017 when a number of

new projects become operational

● The petrochemical industry is the biggest source of foreign earnings

for Iran after oil. In 2015, Iranian companies exported about $13

billion of petrochemical products.

● Iran needs $55 billion for 60 projects in the petrochemicals

sector over a period of 10 years

● Non US IOC have tabled “serious” proposals for building

petrochemical plants in Iran

GROWTH DRIVERS

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 9

STAR

2017

ROTO

MOUL

DING

CONFE

RENCE

-

Ph.Mon

● 10

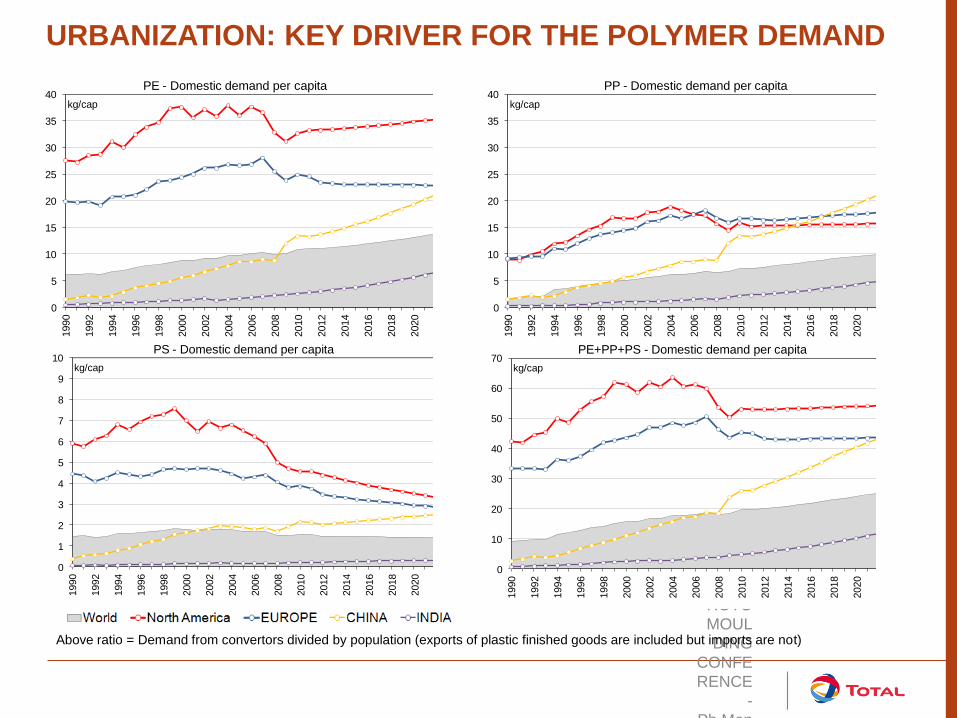

URBANIZATION: KEY DRIVER FOR THE POLYMER DEMAND

0

5

10

15

20

25

30

35

40

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

kg/cap

PE - Domestic demand per capita

0

5

10

15

20

25

30

35

40

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

kg/cap

PP - Domestic demand per capita

0

1

2

3

4

5

6

7

8

9

10

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

kg/cap

PS - Domestic demand per capita

0

10

20

30

40

50

60

70

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

kg/cap

PE+PP+PS - Domestic demand per capita

Above ratio = Demand from convertors divided by population (exports of plastic finished goods are included but imports are not)

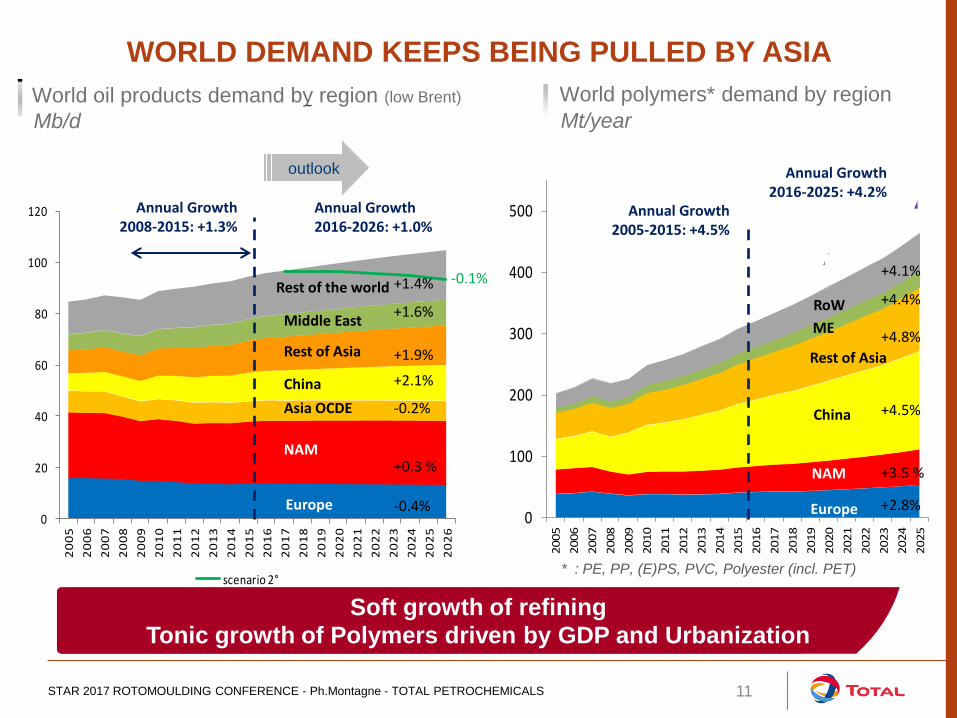

WORLD DEMAND KEEPS BEING PULLED BY ASIA

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 11

0

20

40

60

80

100

120

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

scenario 2° MS

World oil products demand by region (low Brent)

Europe

Mb/d

Annual Growth 2008-2015: +1.3%

+1.9%

+1.4%

+1.6%

+2.1%

-0.2%

+0.3 %

-0.4%

Annual Growth 2016-2026: +1.0%

NAM

Asia OCDE

China

Rest of Asia

Middle East

Rest of the world

outlook

-0.1%

0

100

200

300

400

500

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

ICIS gross demand

World polymers* demand by region

Mt/year

NAM

China

Rest of Asia

ME

RoW

Europe

Annual Growth 2005-2015: +4.5%

+4.4%

+4.1%

+4.8%

+4.5%

+3.5 %

+2.8%

Annual Growth 2016-2025: +4.2%

Soft growth of refining

Tonic growth of Polymers driven by GDP and Urbanization

* : PE, PP, (E)PS, PVC, Polyester (incl. PET)

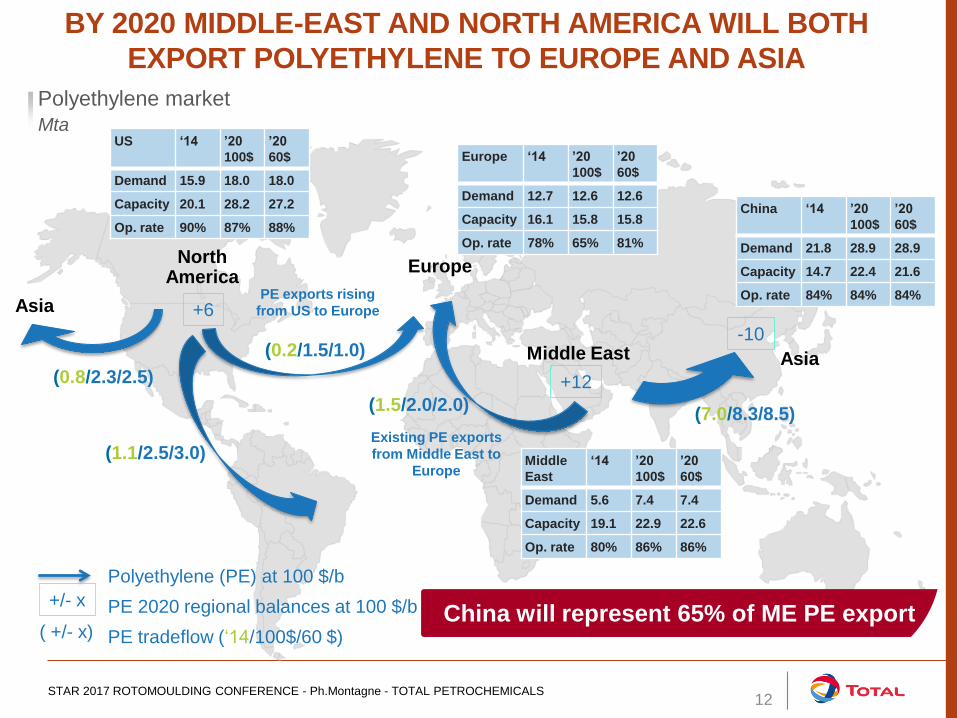

BY 2020 MIDDLE-EAST AND NORTH AMERICA WILL BOTH

EXPORT POLYETHYLENE TO EUROPE AND ASIA

12

North America

Europe

Middle East Asia

PE exports rising

from US to Europe

Polyethylene (PE) at 100 $/b

PE 2020 regional balances at 100 $/b

PE tradeflow (‘14/100$/60 $)

Asia

Existing PE exports

from Middle East to

Europe

Europe ‘14 ’20

100$

’20

60$

Demand 12.7 12.6 12.6

Capacity 16.1 15.8 15.8

Op. rate 78% 65% 81%

(0.8/2.3/2.5)

+/- x

Polyethylene market

Mta

( +/- x)

US ‘14 ’20

100$

’20

60$

Demand 15.9 18.0 18.0

Capacity 20.1 28.2 27.2

Op. rate 90% 87% 88%

China ‘14 ’20

100$

’20

60$

Demand 21.8 28.9 28.9

Capacity 14.7 22.4 21.6

Op. rate 84% 84% 84%

+6

+12

-10

(1.1/2.5/3.0)

(0.2/1.5/1.0)

(1.5/2.0/2.0) (7.0/8.3/8.5)

Middle

East

‘14 ’20

100$

’20

60$

Demand 5.6 7.4 7.4

Capacity 19.1 22.9 22.6

Op. rate 80% 86% 86%

China will represent 65% of ME PE export

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

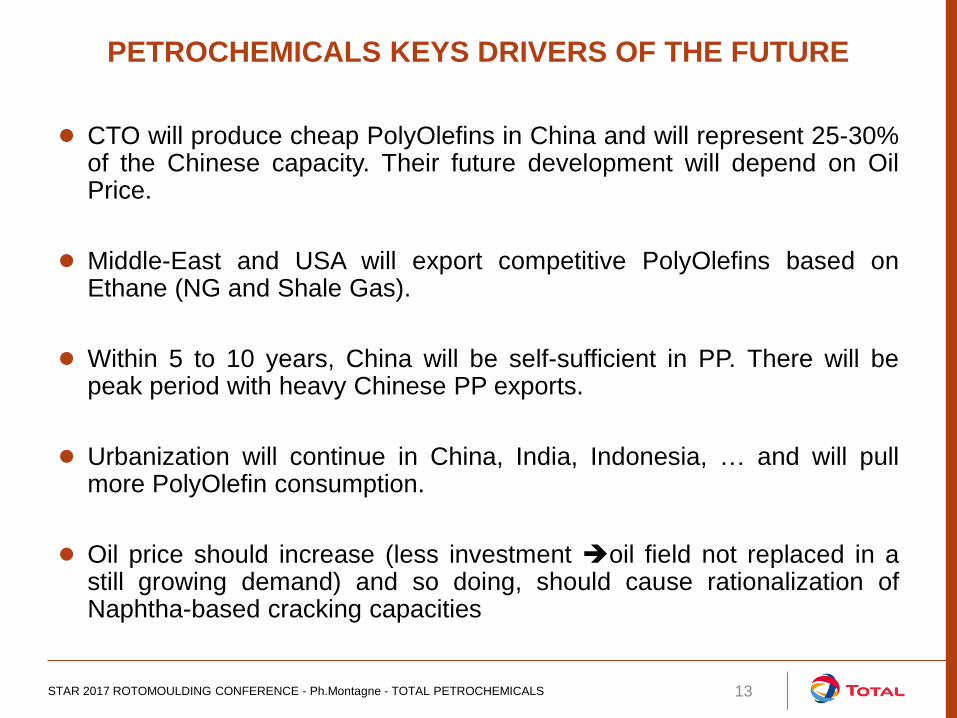

PETROCHEMICALS KEYS DRIVERS OF THE FUTURE

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 13

● CTO will produce cheap PolyOlefins in China and will represent 25-30% of the Chinese capacity. Their future development will depend on Oil Price.

● Middle-East and USA will export competitive PolyOlefins based on Ethane (NG and Shale Gas).

● Within 5 to 10 years, China will be self-sufficient in PP. There will be peak period with heavy Chinese PP exports.

● Urbanization will continue in China, India, Indonesia, … and will pull more PolyOlefin consumption.

● Oil price should increase (less investment oil field not replaced in a still growing demand) and so doing, should cause rationalization of Naphtha-based cracking capacities

FOCUS ON INDIA

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 14

15 STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

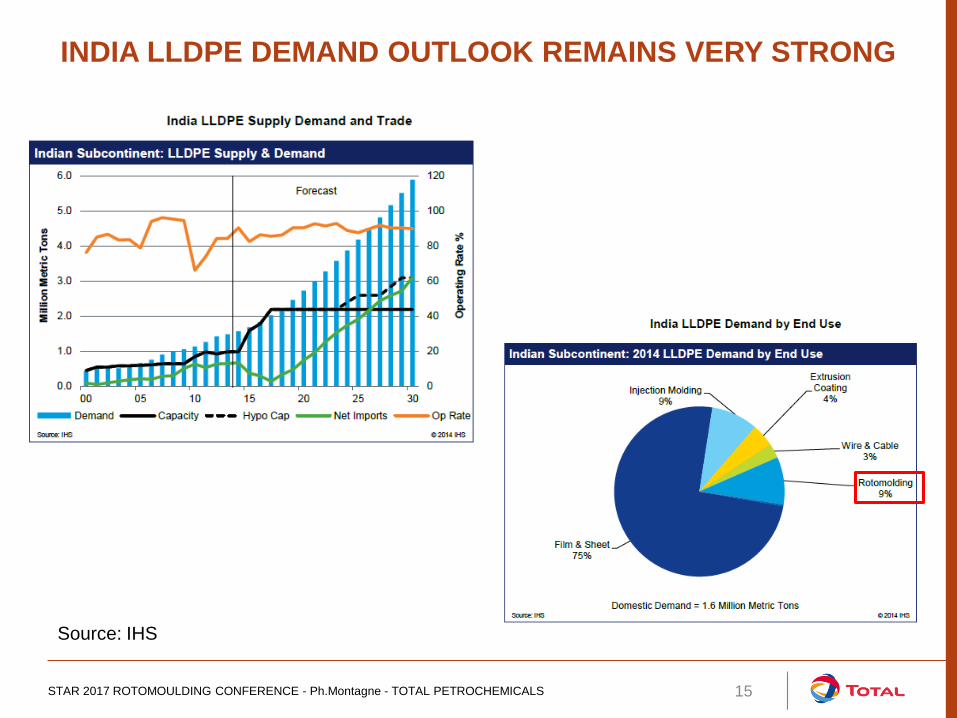

INDIA LLDPE DEMAND OUTLOOK REMAINS VERY STRONG

Source: IHS

16 STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

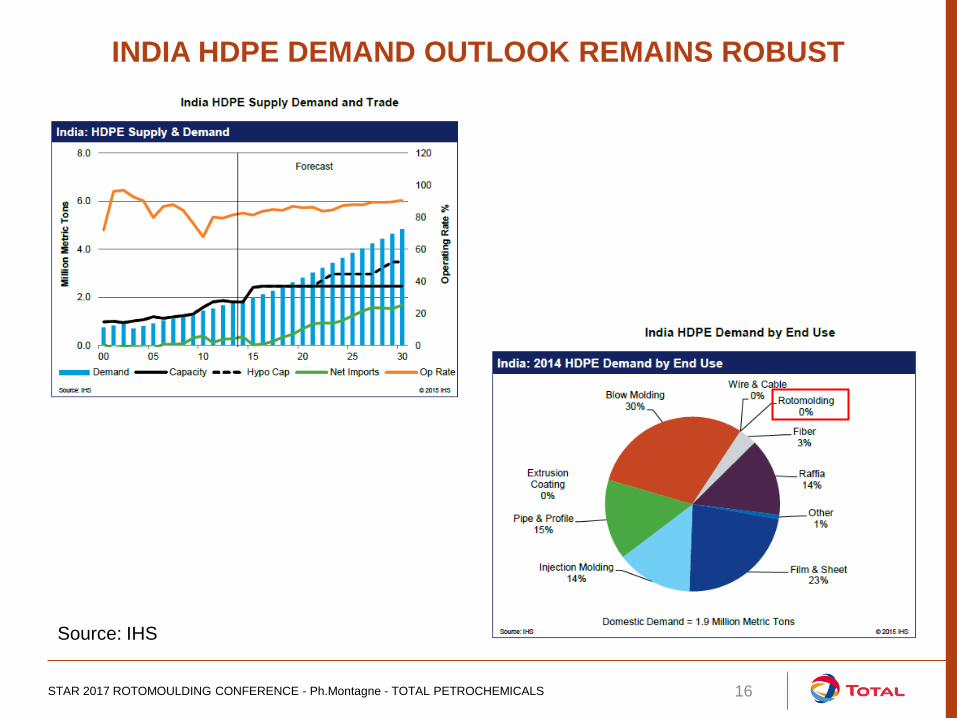

INDIA HDPE DEMAND OUTLOOK REMAINS ROBUST

Source: IHS

17 STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

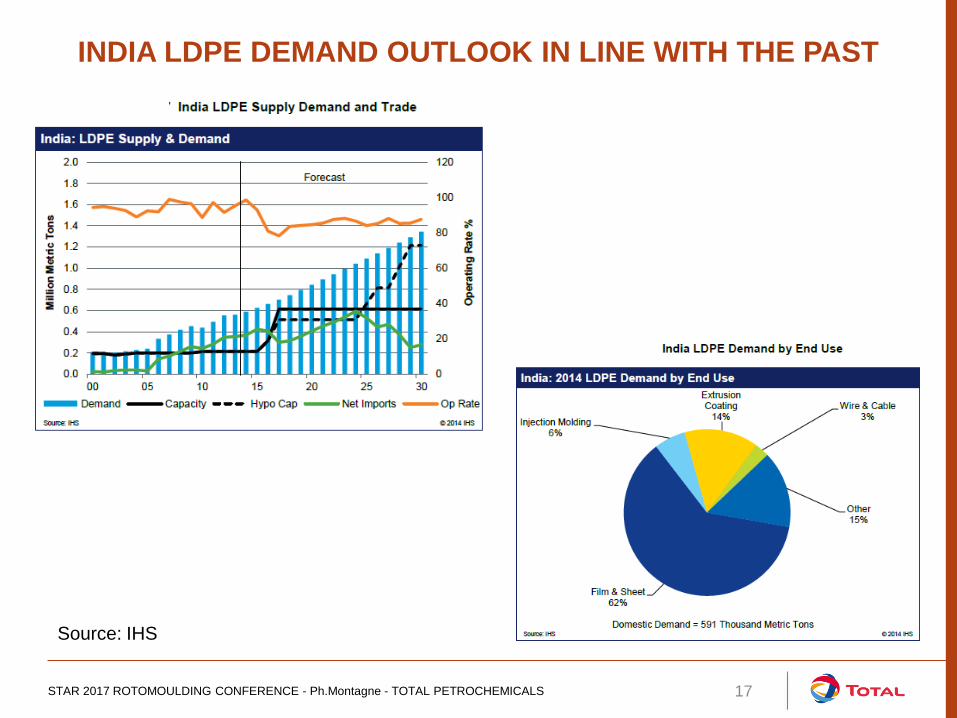

INDIA LDPE DEMAND OUTLOOK IN LINE WITH THE PAST

Source: IHS

18 STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

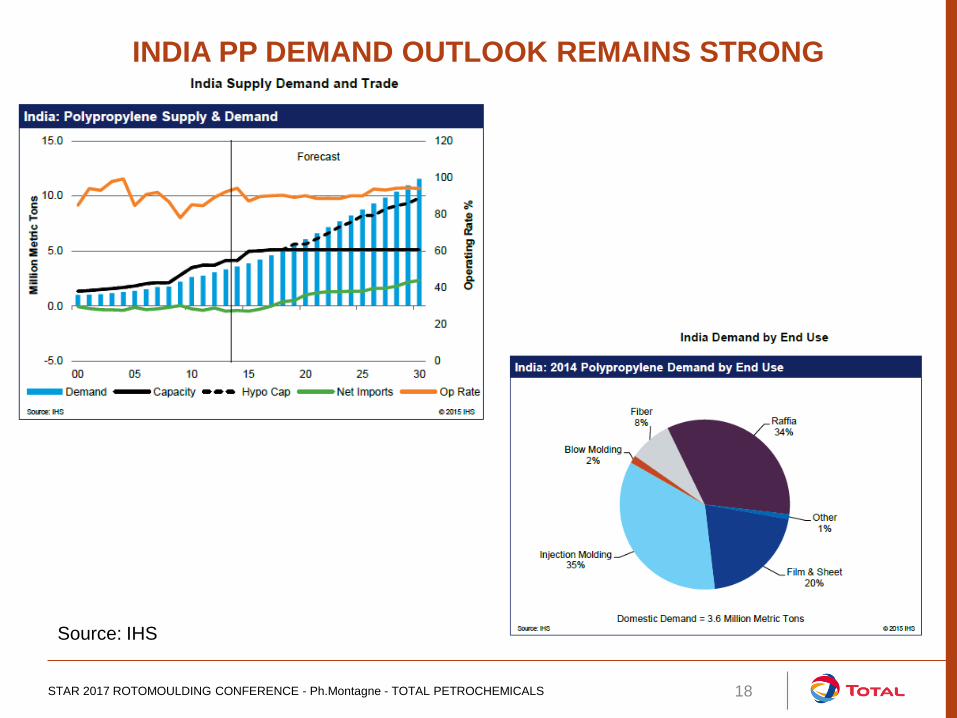

INDIA PP DEMAND OUTLOOK REMAINS STRONG

Source: IHS

SPECIALTY PRODUCTS TO MAKE THE

WORLD BETTER

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 19

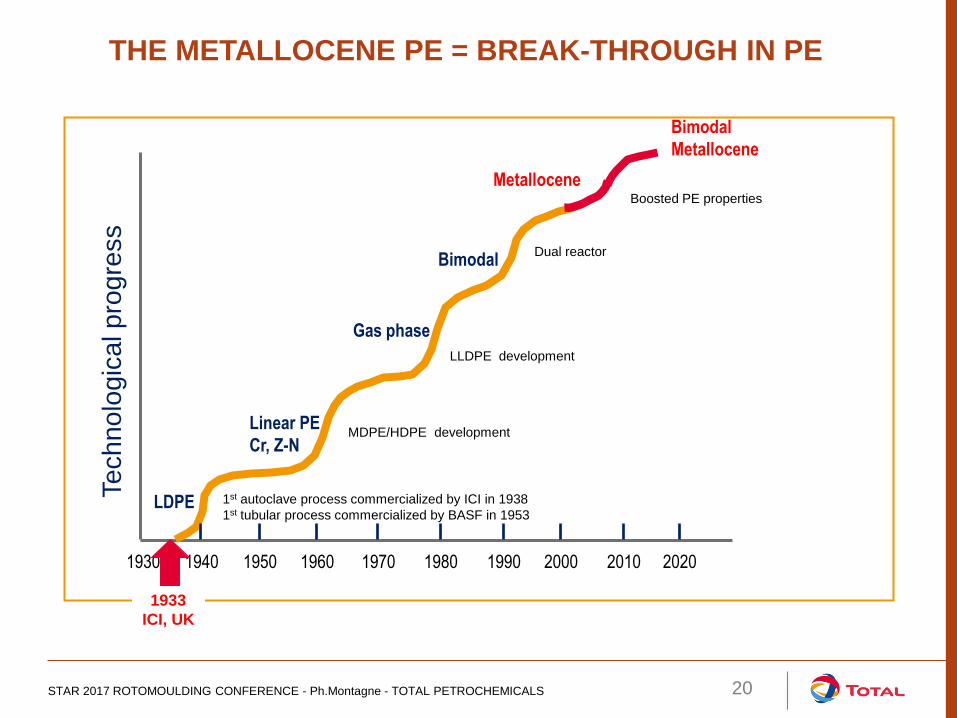

LDPE

Linear PE

Cr, Z-N

Gas phase

Metallocene

Bimodal

1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

20

Bimodal

Metallocene

1933

ICI, UK

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

1st autoclave process commercialized by ICI in 1938

1st tubular process commercialized by BASF in 1953

MDPE/HDPE development

LLDPE development

Dual reactor

Boosted PE properties

THE METALLOCENE PE = BREAK-THROUGH IN PE

Te

ch

no

log

ica

l p

rog

ress

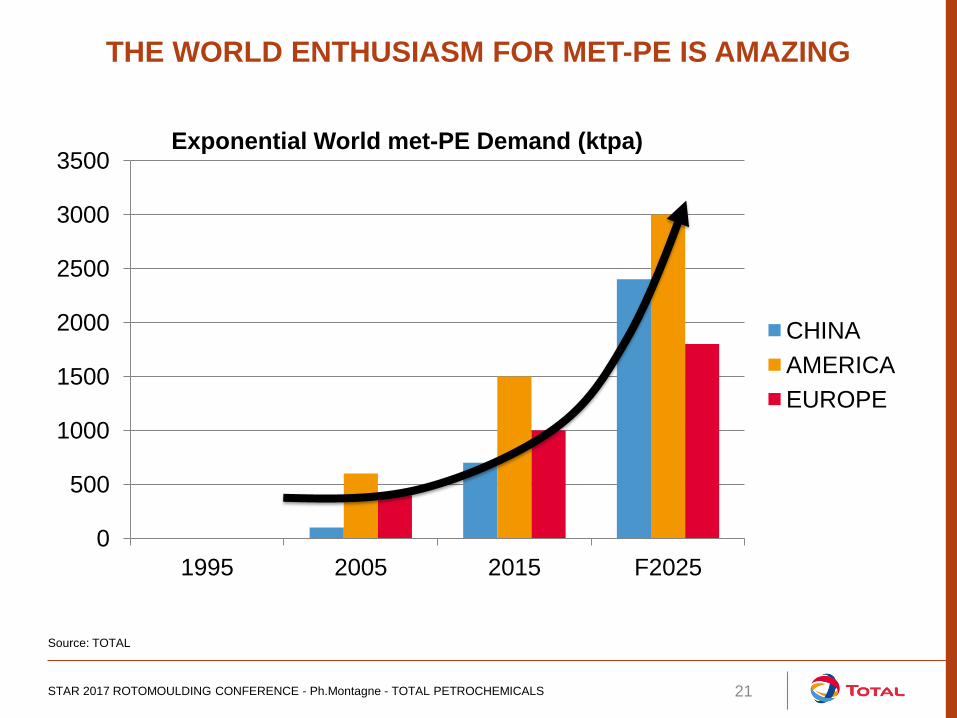

THE WORLD ENTHUSIASM FOR MET-PE IS AMAZING

0

500

1000

1500

2000

2500

3000

3500

1995 2005 2015 F2025

CHINA

AMERICA

EUROPE

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

Exponential World met-PE Demand (ktpa)

Source: TOTAL

21

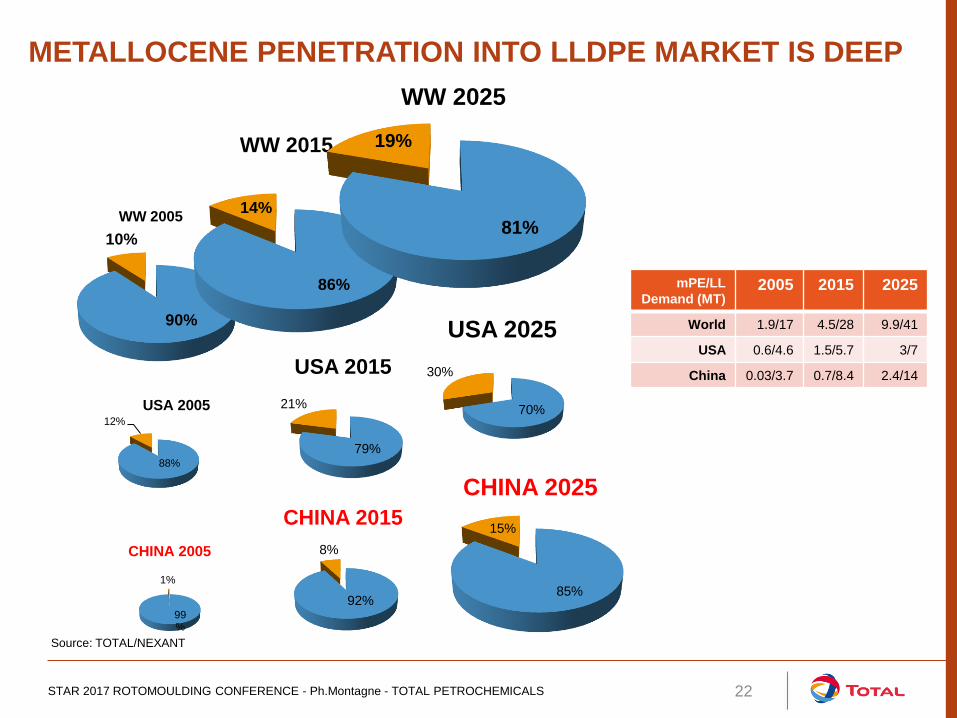

METALLOCENE PENETRATION INTO LLDPE MARKET IS DEEP

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

90%

10%

WW 2005

86%

14%

WW 2015

81%

19%

WW 2025

99%

1%

CHINA 2005

92%

8%

CHINA 2015

85%

15%

CHINA 2025

mPE/LL

Demand (MT) 2005 2015 2025

World 1.9/17 4.5/28 9.9/41

USA 0.6/4.6 1.5/5.7 3/7

China 0.03/3.7 0.7/8.4 2.4/14

88%

12%

USA 2005

79%

21%

USA 2015

70%

30%

USA 2025

22

Source: TOTAL/NEXANT

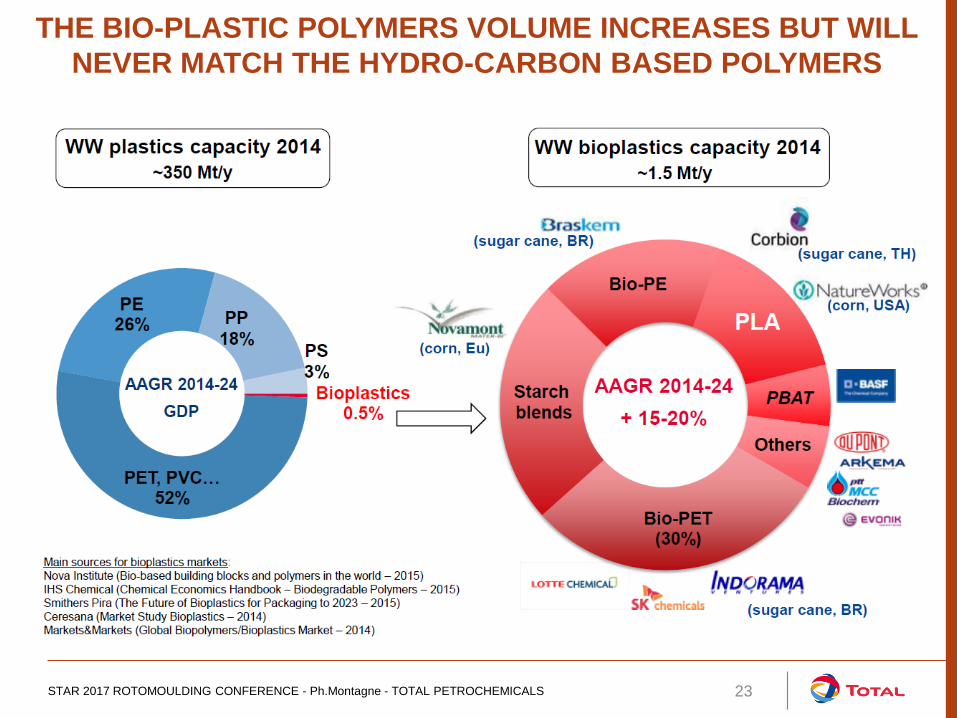

THE BIO-PLASTIC POLYMERS VOLUME INCREASES BUT WILL

NEVER MATCH THE HYDRO-CARBON BASED POLYMERS

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 23

TOTAL – A KEY PLAYER IN

PROVIDING SPECIALTY PRODUCTS

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 24

An Oil & Gas Company

- 2.3 Mb/d - 2nd

global player in LNG

- Net Income of 22 billion $ (2015)

- Operations in 130 countries, with 96,000 employees

A Leader in Refining & Marketing

-16 refineries worldwide. 2.2 Mb/d of refining capacity

-Network of 17,000 service stations (Europe + Africa + Asia)

A Global Petrochemical Integrated Player

-One of top 10 Producers of PP, PE and PS

A Leader in Renewable Energy

-Top 3 Solar Player with SunPower. 6GW+ already deployed

worldwide

-Developing Energy Storage with Saft Acquisition (1bn $)

-World-Class BioRefinery (La Mede, France) in construction to produce 500KT/y of bio-fuels

25

TOTAL: A LEADING ENERGY GROUP

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS

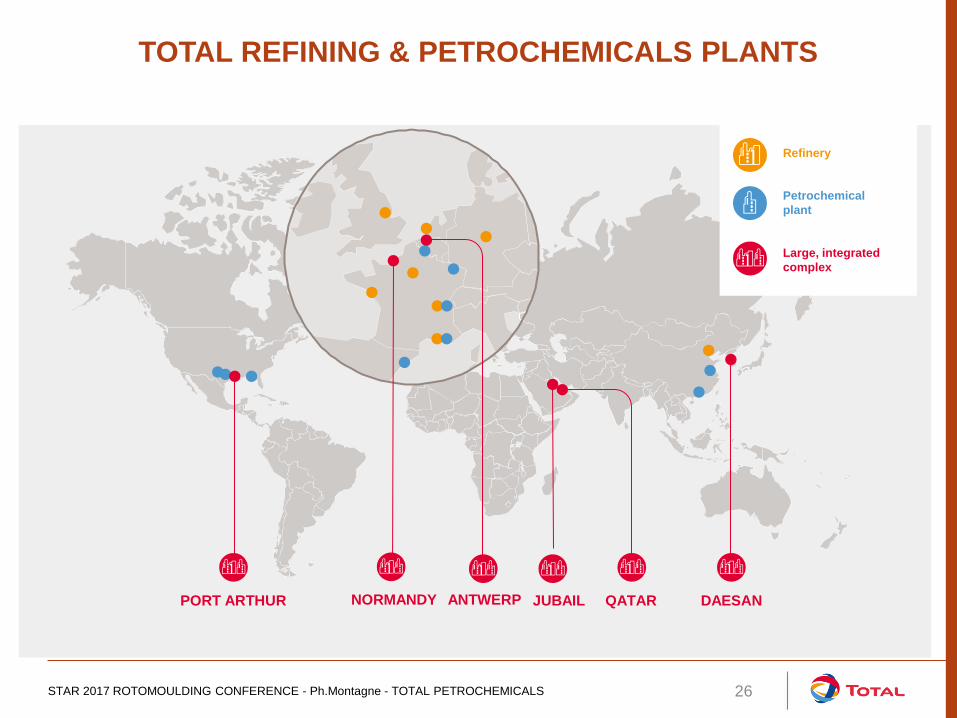

TOTAL REFINING & PETROCHEMICALS PLANTS

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 26

Refinery

Petrochemical

plant

Large, integrated

complex

PORT ARTHUR QATAR DAESAN

JUBAIL ANTWERP NORMANDY

0

1

2

3

4

5

6

Rest

of the world

Asia Middle East North America Europe

Refining capacities Mb/d

Petrochemical capacities Mt/y

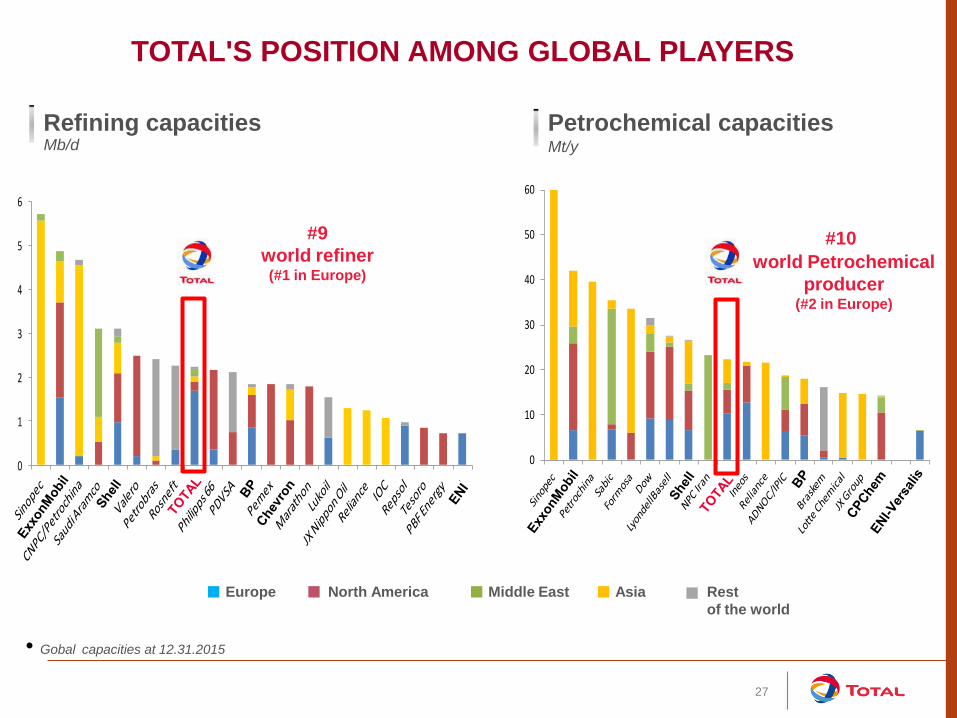

27

0

10

20

30

40

50

60

TOTAL'S POSITION AMONG GLOBAL PLAYERS

#10 world Petrochemical

producer (#2 in Europe)

#9

world refiner (#1 in Europe)

• Gobal capacities at 12.31.2015

STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS 28

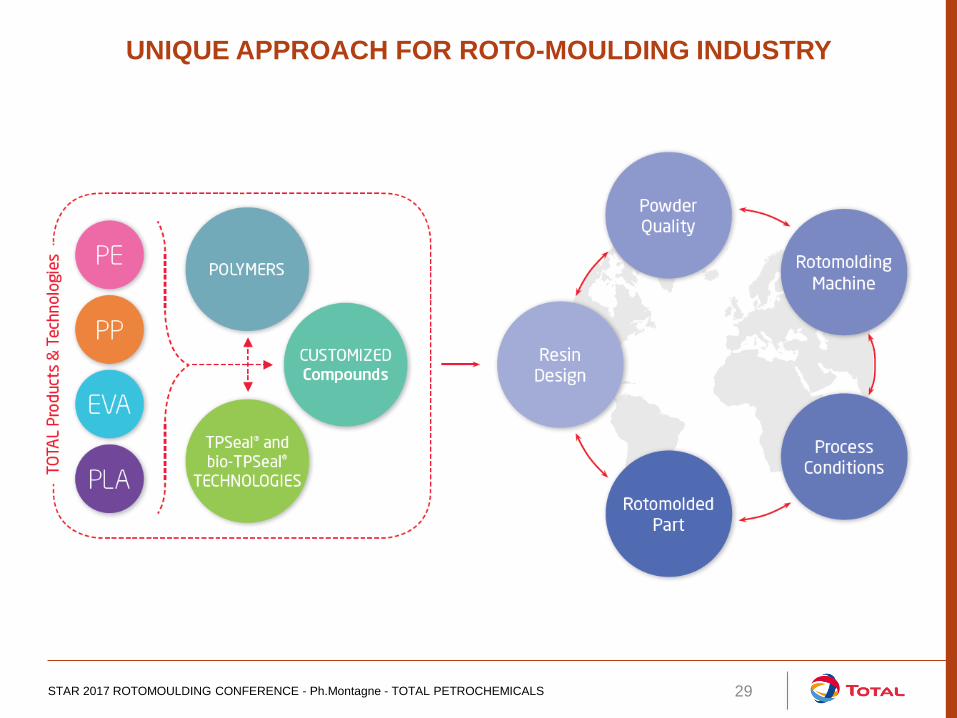

UNIQUE APPROACH FOR ROTO-MOULDING INDUSTRY

29 STAR 2017 ROTOMOULDING CONFERENCE - Ph.Montagne - TOTAL PETROCHEMICALS