Oshkosh Corporation (NYSE:OSK) · MOVING THE WORLD AT WORK Oshkosh Corporation (NYSE:OSK) 2014 Bank...

35

MOVING THE WORLD AT WORK Oshkosh Corporation (NYSE:OSK) 2014 Bank of America Merrill Lynch Global Industrial Conference March 18, 2014 MOVE: Strategy and Business Transformation Charlie Szews – Chief Executive Officer

Transcript of Oshkosh Corporation (NYSE:OSK) · MOVING THE WORLD AT WORK Oshkosh Corporation (NYSE:OSK) 2014 Bank...

MOVING THE WORLD AT WORK

Oshkosh Corporation (NYSE:OSK)2014 Bank of America Merrill Lynch

Global Industrial ConferenceMarch 18, 2014

MOVE: Strategy and Business TransformationCharlie Szews – Chief Executive Officer

MOVING THE WORLD AT WORK

Forward-Looking Statements

22014 BAML Global Industrial Conference March 18, 2014

This presentation contains statements that the Company believes to be “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact, including, withoutlimitation, statements regarding the Company’s future financial position, business strategy, targets, projected sales, costs,earnings, capital expenditures, debt levels and cash flows, and plans and objectives of management for future operations, areforward-looking statements. When used in this presentation, words such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “should,” “project” or “plan” or the negative thereof or variations thereon or similar terminology are generally intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties, assumptions and other factors, some of which are beyond the Company’s control, which could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These factors include the cyclical nature of the Company’s access equipment, commercial and fire & emergency markets, especially with the current outlook for the U.S. and European economic recoveries; the strength of emerging market growth and projected adoption rate of work at height machinery; the expected level and timing of DoD and international defense customers procurement of products and services and funding thereof; risks related to reductions in government expenditures in light of U.S. defense budget pressures, sequestration and an uncertain DoD tactical wheeled vehicle strategy, including the Company’s ability to successfullymanage the cost reductions required as a result of the significant projected decrease in sales levels in the defense segment; the Company’s ability to win a U.S. JLTV production contract award; the Company’s ability to increase prices to raise margins or offset higher input costs; increasing commodity and other raw material costs, particularly in a sustained economic recovery; risks related to facilities consolidation and alignment, including the amounts of related costs and charges and that anticipated cost savings may not be achieved; the duration of the ongoing global economic uncertainty, which could lead to additional impairment charges related to many of the Company’s intangible assets and/or a slower recovery in the Company’s cyclical businesses thanCompany or equity market expectations; risks related to the collectability of receivables, particularly for those businesses with exposure to construction markets; the cost of any warranty campaigns related to the Company’s products; risks related to production or shipment delays arising from quality or production issues; risks associated with international operations and sales, including foreign currency fluctuations and compliance with the Foreign Corrupt Practices Act; the Company’s ability to comply with complex laws and regulations applicable to U.S. government contractors; and risks related to the Company’s ability to successfully execute on its strategic road map and meet its long-term financial goals. Additional information concerning these and other factors is contained in the Company’s filings with the Securities and Exchange Commission, including the Form 8-K filed January 28, 2014. All forward-looking statements speak only as of the date of this presentation. The Company assumes no obligation, and disclaims any obligation, to update information contained in this presentation. Investors should be aware that the Company may not update such information until the Company’s next quarterly earnings conference call, if at all.

MOVING THE WORLD AT WORK

Oshkosh Corporation Leading provider of specialty vehicles

• Moving the World at Work

Nearly 100 years in business; incorporated in 1917

Four business segments

FY13 Revenue: $7.7 billion

Market Capitalization (1): $4.8 billion

December 2013 Net Debt (2): $380 million

15 year TSR(3): ~1,200%1 year TSR(3): ~80%

(1) As of March 10, 2014(2) Net debt is total debt less cash(3) TSR is Total Shareholder Return. Source: ThomsonONE. From September 30, 1998 to September 30, 2013 and

September 28, 2012 to September 30, 2013, respectively

Access Equipment Defense

Fire & Emergency Commercial

32014 BAML Global Industrial Conference March 18, 2014

MOVING THE WORLD AT WORK

FY15 Targets

MOVE – The Right Strategy

• Focuses on drivers that create highest shareholder value

• Expected to drive higher incremental margins across non-Defense businesses over cycle

(1) Expected benefits of market recovery captured in financial estimates vs. September 2012 Analyst Day estimate of FY12. Does notinclude benefits of other MOVE initiatives.

(2) Net of investment costs and compared with consolidated FY11 operating income margins.(3) Compared with FY12.

Initiative

2014 BAML Global Industrial Conference March 18, 2014 4

MOVING THE WORLD AT WORK

Transforming – More Diverse, Global Industrial Company

FY15E Sales (1)

FY11 Sales

Defense Non-Defense

Non-Defense Sales Become Majority of Revenue by FY15

FY13 Sales

(1) Based on Company estimates as of September 2012 Analyst Day

52014 BAML Global Industrial Conference March 18, 2014

MOVING THE WORLD AT WORK

MOVE is DeliveringStrong Financial Results

MOVING THE WORLD AT WORK

Strong Performance in FY13…

(1) Non-GAAP results. See Appendix: Non-GAAP to GAAP Reconciliation(2) Variance calculated from high end of range.

Analyst Day FY13 Measure FY13 Estimates Actual %Variance(2)

Revenue $7.5 - $7.8B $7.7B (1.7%) Solid non-defense growth largely offset anticipated defense decline

Adjusted Operating Income(1) $380 - $420M $535M 27.4% MOVE initiatives provide strong foundationfor growth to FY15 objectives

Adjusted EPS(1) $2.35 - $2.60 $3.74 43.8% Strong growth despite lower defense revenue

Free Cash Flow(1) $75 - $100M $386M 286.0%Consistent generator of strong FCF

72014 BAML Global Industrial Conference March 18, 2014

…Driving Toward FY15 Targets

MOVING THE WORLD AT WORK

Responsible Capital Allocation Strategy

Reinstated $0.15 quarterly cash dividend Repurchased 9.8M OSK shares for $368M; July 2012 - Feb 3, 2014 Refinanced $250M in Sr. Notes due March 2022

• Interest rate reduced from 8.25% to 5.375%

8

Return capital to shareholders

Re-invest in core business

Invest in external growth

opportunities

Hold cash

Reduce debt

Long-term targeted capital

structure

2014 BAML Global Industrial Conference March 18, 2014

MOVING THE WORLD AT WORK

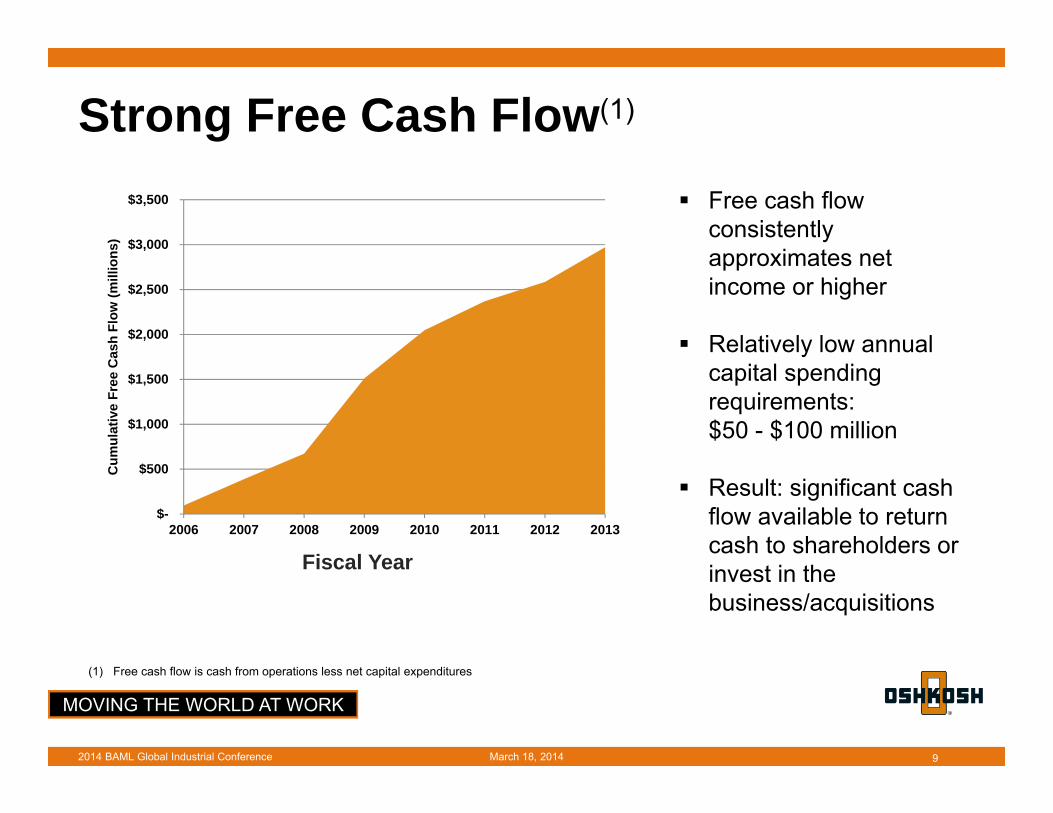

Strong Free Cash Flow(1)

9

Fiscal Year

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2006 2007 2008 2009 2010 2011 2012 2013

Cum

ulat

ive

Free

Cas

h Fl

ow (m

illio

ns)

2014 BAML Global Industrial Conference March 18, 2014

Free cash flow consistently approximates net income or higher

Relatively low annual capital spending requirements:$50 - $100 million

Result: significant cash flow available to return cash to shareholders or invest in the business/acquisitions

(1) Free cash flow is cash from operations less net capital expenditures

MOVING THE WORLD AT WORK

March 18, 20142014 BAML Global Industrial Conference 10

MOVE is Delivering a Business Transformation – To Serve and

Delight Customers

MOVING THE WORLD AT WORK

Powering Our Transformation –The Oshkosh Operating System Customer-centric application

of lean principles• Develops talent to deliver value

for customers

Improves processes needed todeliver key elements of MOVE

Supports drive to improve cash flow

Implementation gaining momentum

Company-wide foundation for building shareholder value

112014 BAML Global Industrial Conference March 18, 2014

MOVING THE WORLD AT WORK

Customer Supporting Systems

12

Leaders Cascade Training

Driving Our Customer-Centric CultureOOS Foundational Training

Customer Satisfaction

Launched September 2013

Launched December 2013

Customer First

Launched November 2012

2014 BAML Global Industrial Conference March 18, 2014

MOVING THE WORLD AT WORK

Transforming Operations –Continuous Improvement Events

132014 BAML Global Industrial Conference March 18, 2014

Using Problem Solving Tools to Improve Paint Quality

Developing Customer-Centric Key Performance Indicators

Using Process Mapping to Reduce Lead Time

Improving Station Layout to Reduce Non-Value Added Motion

MOVING THE WORLD AT WORK

Continue to Advance OOS Culture

142014 BAML Global Industrial Conference

The OOS Journey

Phase Zero:Exploration

Phase One:Building the foundation

Phase Two:Expanding with tools and deeper thinking

Phase Three:Integration and reinforcement

Phase Four:Building the momentum

March 18, 2014

MOVING THE WORLD AT WORK

Favorable Near Term Market Outlook to Support Business

Transformation

MOVING THE WORLD AT WORK

Access Equipment Replacement demand continues to

drive North American market• NRCs: ~flat; IRCs up• Fleet growth with a few customers Improving in select global markets

• Europe and Middle East stronger• Positive conditions in Latin America• Australia remains weak Extensive new product launch

activity at ConExpo

March 18, 20142014 BAML Global Industrial Conference 16

MOVING THE WORLD AT WORK

North American Metrics Remain SolidRefreshing Fleets, Increasing Penetration

Residential and Non-Residential Spending(Y-O-Y % Change)

N.A. Rental Equipment Access - Fleet Age(AWP & TMH)

N.A. Rental Equipment Company Fleet Utilization

Recent Used Equipment Value Trends(OLV)

Source: Global Insight Estimates, December 2013

Based on International Rental News/Dan Kaplan sample of medium to large NA rental equipment companies (United Rentals, RSC, H&E, HERC).

(% C

hang

e)(%

Tim

e U

tiliz

atio

n)

OLV

(% o

f Cos

t)

Source: Rouse Rental Report. Calendar year-end data for 2008-13

(Age

in M

onth

s)

17

Source: Rouse Asset Services, January 2014Note: Rouse rebased the Rouse Value IndexTM in January 2014

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

2008 2009 2010 2011 2012 2013E 2014E 2015E

Residential Non‐Residential

50

55

60

65

70

75

Ind. Avg.

March 18, 20142014 BAML Global Industrial Conference

40

45

50

55

60

2008 2009 2010 2011 2012 2013

25.0

30.0

35.0

40.0

45.0

Articulating Booms Scissor LiftsTelescopic Booms Telehandlers

MOVING THE WORLD AT WORK

Aerial Work Platform Innovation New 56.5 meter Ultra Boom Extends work height to 19 stories Industry’s largest work envelope

• Reach envelope increases from 2.3 million cubic feet to ~3.0 million cubic feet

Transportable without oversize permit

10.3 meter Hybrid Articulated Boom LiftHybrid technology for construction and industrial sectors with diesel-like performance Highly efficient Two operating power modes

• More than 7 hours of continuousbattery-only operation in electric mode

Low environmental impact

March 18, 20142014 BAML Global Industrial Conference 18

MOVING THE WORLD AT WORK

Telehandler Innovation -

March 18, 20142014 BAML Global Industrial Conference 19

Rental Series Telehandlers – Designed for the rental market, by the rental market Stage IIIb engines Low cost of ownership Simple design Easily serviced

SkyTrak – Refreshing North America’s #1 Telehandler Brand Modernizes operator controls/comfort; sustains ease of operation and reliability

• Single joystick design• Improved operator control• Faster boom speeds• Enhanced cab layout

MOVING THE WORLD AT WORK

March 18, 20142014 BAML Global Industrial Conference 20

• Managing programs with lower expected funding• Operations continue to improve

• Working on multiple international upside opportunities- Middle East: M-ATV, Medium & Heavy TWV platforms- Canada MSVS SMP

Defense Team Driving Hard Through Downturn

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

FY11 FY12 FY13 FY14E FY15E

Sale

s in

Bill

ions

$4.4$4.0

$3.0

$1.75 - $1.80$1.5 Target (1)

0.0%

5.0%

10.0%

15.0%

FY11 FY12 FY13 FY14E FY15E

12.4%

6.0%7.5%*

3.75% – 4.0% Baseline~2.0% (1)

Ope

ratin

g In

com

eM

argi

n

DoD Funding Drives Lower Outlook Through FY15

(1) FY15 estimates as of September 2012 Analyst Day

$0.8 Baseline (1)

MOVING THE WORLD AT WORK

March 18, 20142014 BAML Global Industrial Conference 21

Competing in Light TWV MarketJoint Light Tactical Vehicle Program

JLTV represents opportunity to rebuildthe business• One of three potential suppliers • Large unit potential

o Initial contract ~17,000o Total U.S. requirements of ~55,500o Attractive global customer prospects

• Leverages Oshkosh strengths• Contract award scheduled for 2015

MOVING THE WORLD AT WORK

Fire & Emergency

Municipal fire truck demand continues to improve

Expecting market growth in 2014

Federal market remains weak• Lower equipment funding

Improvements in operations underway, driven by MOVE• Expect greater benefit in 2H 2014

and throughout 2015 Strong new product launches at

FDIC show next month

March 18, 20142014 BAML Global Industrial Conference 22

MOVING THE WORLD AT WORK

Domestic Fire Market Drivers Stabilizing • Municipal fire truck orders improving with recovering tax receipts• Stronger customer activity

Recent Headlines

Construction Spending Highest in Nearly Five Years- Reuters, January 2, 2014

Home prices rise more than expected- USA Today, February 25, 2014

Solid new-home sales lift hopes for housing market Washington Post, February 26, 2014

HOUSING PRICES & LOCAL PROPERTY TAXES

23March 18, 20142014 BAML Global Industrial Conference

MOVING THE WORLD AT WORK

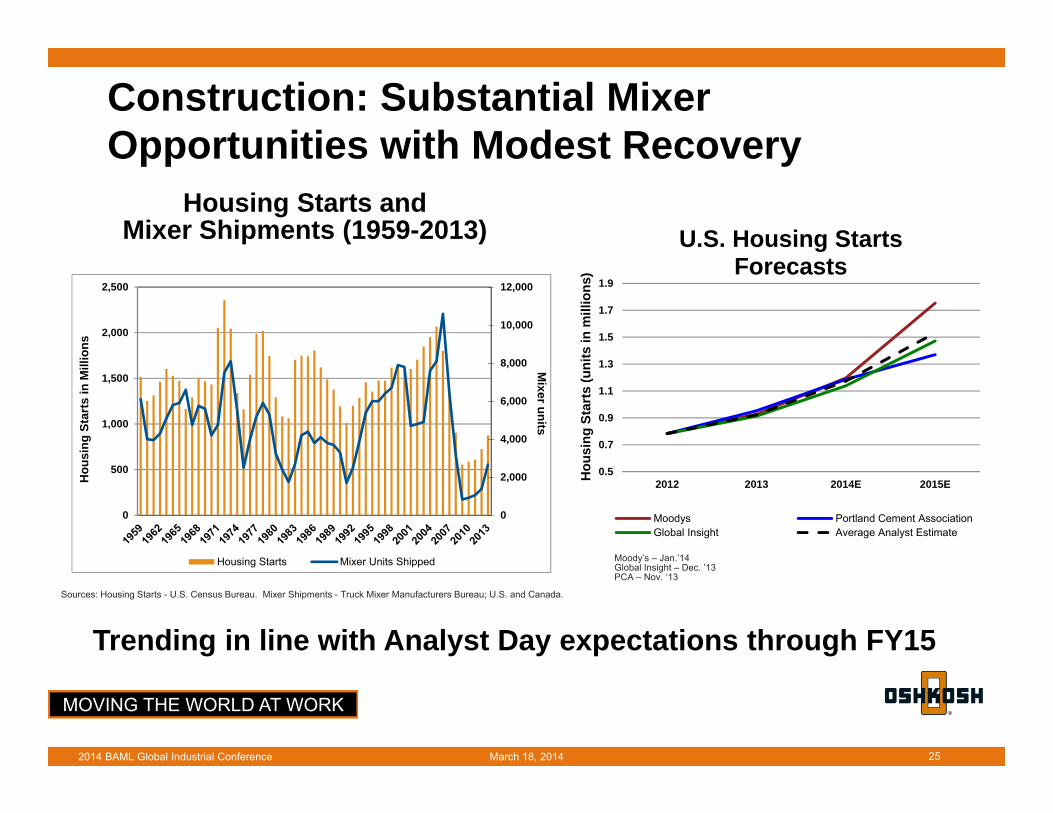

Commercial

U.S. housing recovery driving concrete mixer sales

Remain focused on operational improvements to deliver higher margins• Expect greater benefit in 2H 2014

and throughout 2015 Expect RCV market to return to

growth in 2014

March 18, 20142014 BAML Global Industrial Conference 24

MOVING THE WORLD AT WORK

Trending in line with Analyst Day expectations through FY15

Construction: Substantial MixerOpportunities with Modest Recovery

Housing Starts and Mixer Shipments (1959-2013)

25

Sources: Housing Starts - U.S. Census Bureau. Mixer Shipments - Truck Mixer Manufacturers Bureau; U.S. and Canada.

March 18, 20142014 BAML Global Industrial Conference

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2012 2013 2014E 2015EHou

sing

Sta

rts

(uni

ts in

mill

ions

)

U.S. Housing Starts Forecasts

Moodys Portland Cement AssociationGlobal Insight Average Analyst Estimate

0

2,000

4,000

6,000

8,000

10,000

12,000

0

500

1,000

1,500

2,000

2,500

Mixer units

Hou

sing

Sta

rts

in M

illio

ns

Housing Starts Mixer Units Shipped Moody’s – Jan.’14Global Insight – Dec. ’13PCA – Nov. ‘13

MOVING THE WORLD AT WORK

Slowly Recovering RCV Market• Slight market contraction in FY13‒ Lower unit volumes in western U.S.

• Municipal tax receipts continue to improve• Fleet age reduction, construction and municipal spending

increase drive demand through FY15

26

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

Mar

ket S

ize

(uni

ts)

Source: WASTEC Industry Data

March 18, 20142014 BAML Global Industrial Conference

MOVING THE WORLD AT WORK

What to Look for in FY14

MOVING THE WORLD AT WORK

MOVE Investments Providing Returns Recovering demand for

non-defense businesses in North America• Europe looking stronger Additional cost take-out

• Focus on product, process and overhead costs

• Dedicated teams leveraging the Oshkosh Operating System

Innovations improving customers’ performance at work Increased international

orders/sales

28March 18, 20142014 BAML Global Industrial Conference

MOVING THE WORLD AT WORK

A Strong Start to FY14 EPS of $0.63 exceeded expectations

• Disciplined execution• Favorable product mix

Improved performance in all non-defense segments offset defense earnings decline• MOVE drove higher operating income

margins

Repurchased 3.0 million shares for $146 million in Q1

Paid first dividend under reinstated program

Increased FY14 EPS expectations to a range of $3.40 to $3.65

Net

Sal

es(b

illio

ns)

Adjusted EPS

OSK Fiscal Q1 Performance

* Non-GAAP results. See appendix for reconciliation to GAAP results.

March 18, 20142014 BAML Global Industrial Conference 29

$1.53

$1.75

$0.63 $0.62

$0.00

$0.25

$0.50

$0.75

$1.00

$0.0$0.2$0.4$0.6$0.8$1.0$1.2$1.4$1.6$1.8$2.0

FY14 FY13*Net Sales EPS

MOVING THE WORLD AT WORK

Expectations for FY14

Additional expectations Corporate expenses flat with adjusted FY13* Tax rate of ~32% CapEx of ~$80 million Free cash flow* ~$200 million Assumes share count of ~85.5 million

Segment information

Measure Access Equipment Defense Fire &

Emergency Commercial

Sales(billions) $3.35 - $3.40 $1.75 - $1.80 $0.80 - $0.825 $0.85 - $0.90

Operating Income Margin 14.25% - 14.5% 3.75% - 4.0% 4.0% - 4.5% 6.75% - 7.0%

• Revenues of $6.65 billion to $6.85 billion• Operating income of $490 million to $520 million• EPS of $3.40 to $3.65

Comments on FY14 Second Quarter Some impact due to severe climate activity Expect improved year-over-year results in non-

defense segments Expect significantly lower defense segment sales

and operating income Prior year quarter had strong

M-ATV sales

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

March 18, 20142014 BAML Global Industrial Conference 30

MOVING THE WORLD AT WORK

Our Commitment to Shareholders Continue executing MOVE to drive shareholder value

• Impressive FY13 results, strong start to FY14• Benefiting from improved housing starts; expect follow on growth

in non-residential construction and municipal recovery• MOVE initiatives driving margin expansion• On track to achieve FY15 EPS of $4.00 to $4.50

Oshkosh Operating System developing processes and talent to sustain superior growth for shareholders

31

Transforming to Sustain Long-Term Value Creation for Shareholders

2014 BAML Global Industrial Conference March 18, 2014

MOVING THE WORLD AT WORK

For informationcontact:

Patrick N. DavidsonVice President, Investor Relations001 (920) [email protected]

Jeffrey D. WattDirector, Investor Relations001 (920) [email protected]

MOVING THE WORLD AT WORK

Appendix: Commonly Used Acronyms

33March 18, 20142014 BAML Global Industrial Conference

ARFF Aircraft Rescue and Firefighting LVSR Logistic Vehicle System ReplacementAWP Aerial Work Platform M-ATV MRAP All-Terrain VehicleCapEx Capital Expenditures MECV Modernized Expanded Capability VehicleCNG Compressed Natural Gas MRAP Mine Resistant Ambush ProtectedDGE Diesel Gallon Equivalent MSVS Medium Support Vehicle System (Canada)DoD Department of Defense NOL Net Operating LossEAME Europe, Africa & Middle East NPD New Product DevelopmentEMD Engineering & Manufacturing Development NRC National Rental CompanyEPS Diluted Earnings Per Share OI Operating IncomeFHTV Family of Heavy Tactical Vehicles OOS Oshkosh Operating SystemFMS Foreign Military Sales PLS Palletized Load SystemFMTV Family of Medium Tactical Vehicles PUC Pierce Ultimate ConfigurationHEMTT Heavy Expanded Mobility Tactical Truck R&D Research & DevelopmentHET Heavy Equipment Transporter RCV Refuse Collection VehicleHMMWV High Mobility Multi-Purpose Wheeled Vehicle RFP Request for ProposalIRC Independent Rental Company ROW Rest of WorldIT Information Technology SMP Standard Military Pattern (Canadian MSVS)JLTV Joint Light Tactical Vehicle TACOM Tank-automotive and Armaments CommandJPO Joint Program Office TDP Technical Data PackageJROC Joint Requirements Oversight Council TPV Tactical Protector VehicleJUONS Joint Urgent Operational Needs Statement TWV Tactical Wheeled VehicleL-ATV Light Combat Tactical All-Terrain Vehicle UCA Undefinitized Contract ActionLRIP Low Rate Initial Production UIK Underbody Improvement Kit (for M-ATV)

MOVING THE WORLD AT WORK

Appendix: Non-GAAP to GAAP Reconciliation

34

The table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures (in millions, except per share amounts):

Fiscal Year EndedSeptember 30,

2013

Non-GAAP operating income 534.8$ Tender offer and proxy contest costs (16.3) Impairment charge (9.0) Union contract ratification costs (3.8) GAAP operating income 505.7$

Non-GAAP earnings per share from continuing operations-diluted 3.74$ Tender offer and proxy contest costs, net of tax (0.12) Impairment charge, net of tax (0.06) Union contract ratification costs, net of tax (0.03) GAAP earnings per share from continuing

operations-diluted 3.53$

Net cash flows provided by operating activities 438.0$ Additions to property, plant and equipment (46.0) Additions to equipment held for rental (13.9) Proceeds from sale of property, plant and equipment 0.1 Proceeds from sale of equipment held for rental 7.5 Free cash flow 385.7$

Non-GAAP operating expenses-Corporate (147.6)$ Tender offer and proxy contest costs (16.3) GAAP operating expenses-Corporate (163.9)$

March 18, 20142014 BAML Global Industrial Conference

MOVING THE WORLD AT WORK

Appendix: Non-GAAP to GAAP Reconciliation

35

The table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures (in millions, except per share amounts):

Fiscal 2014Expectations

Net cash flows provided by operating activities 293.0$ Additions to property, plant and equipment (80.0) Additions to equipment held for rental (13.0) Proceeds from sale of equipment held for rental - Free cash flow 200.0$

2013 2012

Non-GAAP earnings per share from continuing operations-diluted 0.63$ 0.62$ Tender offer and proxy contest costs, net of tax - (0.11) GAAP earnings per share from continuing operations-diluted 0.63$ 0.51$

Three Months EndedDecember 31,

March 18, 20142014 BAML Global Industrial Conference