Orlando: Ten Years After The Boom - orlandoedc.com Insight reflects those discussions and draws from...

8

301 E. Pine Street, Suite 900 // Orlando, FL 32801 // P/ 407.422.7159 // orlandoedc.com Orlando Insight is a publication of the Orlando Economic Forum, an initiative of the Orlando Economic Development Commission (EDC). Comprised of local industry leaders, the Forum meets quarterly to discuss both current economic conditions and issues of regional significance in the four-county Orlando Metropolitan Statistical Area (MSA). Orlando Insight reflects those discussions and draws from the most recent data available at time of preparation. Orlando: Ten Years After The Boom In early 2006, Orlando was the envy of the nation. The region had added over 50,000 jobs in 2005 and was growing at a rate second only to Phoenix. Our pipeline of development projects was full and almost all workers who wanted a job could find one. Yet Orlando was on shaky ground, which ultimately resulted in the region experiencing a harsher recession than some similarly sized metro areas. More than 100,000 jobs would be lost between late 2007 and early 2010, and unemployment would reach a new high. Ten years later, Orlando is once again at a crossroads. Growth has returned, and the region is consistently lauded as one of the nation’s leading job creators. Yet, work to rebuild Orlando’s economy remains unfinished. Return To Growth The final months of 2015 represented an extension of the recent past. The Orlando Metropolitan Statistical Area (MSA) added a seasonally-adjusted 13,000 new jobs in the fourth quarter, bringing total job creation for the year to over 38,000 and driving unemployment to its lowest level in more than seven years. At 4.3 percent, December’s unemployment rate is fast approaching the 3.0 percent of December 2005, and new claims for unemployment benefits have actually fallen below pre-recession levels. Although more muted than in 2005, 2015’s job creation has helped return us to pre-recession employment levels – and beyond. We lost over 100,000 jobs during the recession, but we’ve gained over 180,000 since. Over 80,000 jobs in Orlando today were not present before the recession. Our status as a regional growth center has resumed. In 2005, our employment growth was second among all of the country’s large regions and first in the South. In 2015, we were fourth in the U.S. and again first in the South. “We are once again one of the country’s leading growth centers and thus we are entering a year of great opportunity for our region. Now the question is, how will we seize those opportunities and forge a path to prosperity for all? The answer lies in our ability to make transformational investments in what matters most – education, infrastructure and high value industries.” –– Rick Weddle President & CEO Orlando Economic Development Commission 800 850 900 950 1,000 1,050 1,100 1,150 1,200 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Hundreds Total Payroll Employment, Orlando MSA Through December 2015, Seasonally Adjusted Nov ’07 – Jan ’10 103,700 jobs lost Jan ’10 - Present 187,200 jobs regained RECESSION Source: Florida Department of Economic Opportunity

Transcript of Orlando: Ten Years After The Boom - orlandoedc.com Insight reflects those discussions and draws from...

301 E. Pine Street, Suite 900 // Orlando, FL 32801 // P/ 407.422.7159 // orlandoedc.com

Orlando Insight is a publication of the Orlando Economic Forum, an initiative of the Orlando Economic Development Commission (EDC). Comprised of local industry leaders, the Forum meets quarterly to discuss both current economic conditions and issues of regional significance in the four-county Orlando Metropolitan Statistical Area (MSA). Orlando Insight reflects those discussions and draws from the most recent data available at time of preparation.

Orlando: Ten Years After The BoomIn early 2006, Orlando was the envy of the nation. The region had added over 50,000 jobs in 2005 and was growing at a rate second only to Phoenix. Our pipeline of development projects was full and almost all workers who wanted a job could find one.

Yet Orlando was on shaky ground, which ultimately resulted in the region experiencing a harsher recession than some similarly sized metro areas. More than 100,000 jobs would be lost between late 2007 and early 2010, and unemployment would reach a new high.

Ten years later, Orlando is once again at a crossroads. Growth has returned, and the region is consistently lauded as one of the nation’s leading job creators. Yet, work to rebuild Orlando’s economy remains unfinished.

Return To Growth

The final months of 2015 represented an extension of the recent past. The Orlando Metropolitan Statistical Area (MSA) added a seasonally-adjusted 13,000 new jobs in the fourth quarter, bringing total job creation for the year to over 38,000 and driving unemployment to its lowest level in more than seven years. At 4.3 percent, December’s unemployment rate is fast approaching the 3.0 percent of December 2005, and new claims for unemployment benefits have actually fallen below pre-recession levels.

Although more muted than in 2005, 2015’s job creation has helped return us to pre-recession employment levels – and beyond. We lost over 100,000 jobs during the recession, but we’ve gained over 180,000 since. Over 80,000 jobs in Orlando today were not present before the recession.

Our status as a regional growth center has resumed. In 2005, our employment growth was second among all of the country’s large regions and first in the South. In 2015, we were fourth in the U.S. and again first in the South.

“We are once again one of the country’s leading growth centers and thus we are entering a year of great opportunity for our region. Now the question

is, how will we seize those opportunities and forge a path to prosperity for all? The answer lies in our ability to make transformational investments in

what matters most – education, infrastructure and high value industries.”

–– Rick Weddle President & CEO

Orlando Economic Development Commission

800

850

900

950

1,000

1,050

1,100

1,150

1,200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Hundreds Total Payroll Employment, Orlando MSAThrough December 2015, Seasonally Adjusted

Nov ’07 – Jan ’10103,700 jobs lost

Jan ’10 - Present187,200 jobs regained

RECESSION

Source: Florida Department of Economic Opportunity

An Incomplete Recovery

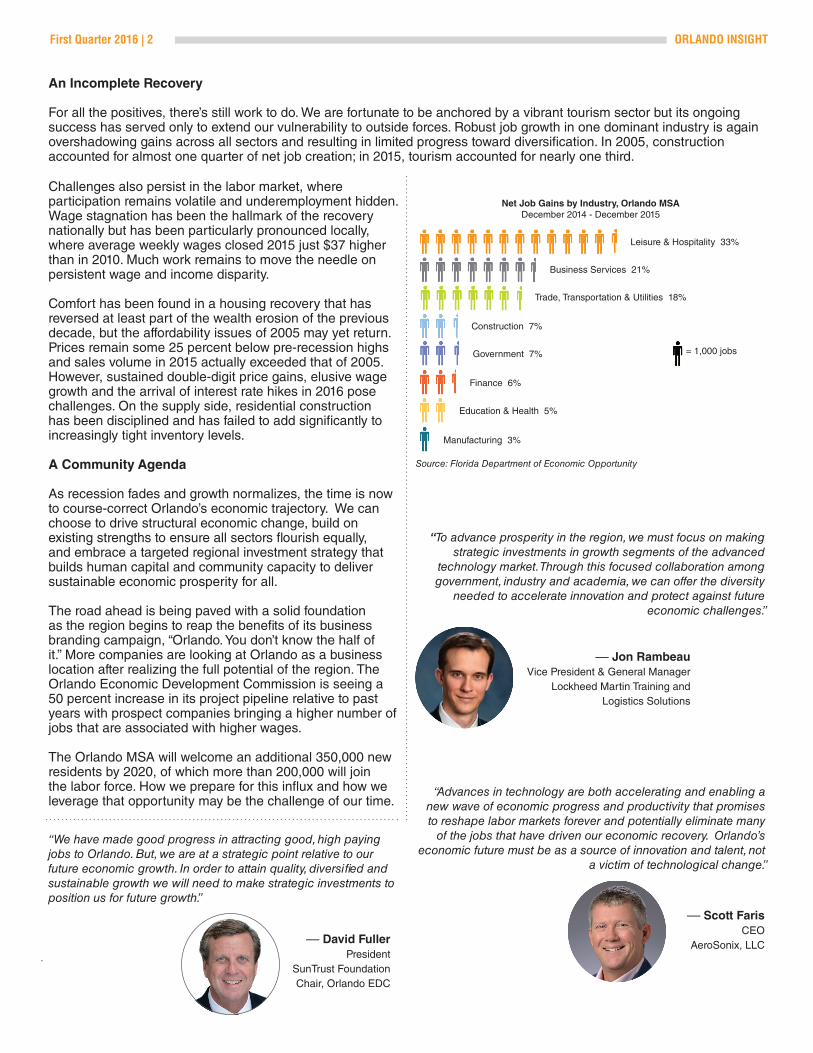

For all the positives, there’s still work to do. We are fortunate to be anchored by a vibrant tourism sector but its ongoing success has served only to extend our vulnerability to outside forces. Robust job growth in one dominant industry is again overshadowing gains across all sectors and resulting in limited progress toward diversification. In 2005, construction accounted for almost one quarter of net job creation; in 2015, tourism accounted for nearly one third.

“We have made good progress in attracting good, high paying jobs to Orlando. But, we are at a strategic point relative to our future economic growth. In order to attain quality, diversified and sustainable growth we will need to make strategic investments to position us for future growth.”

First Quarter 2016 | 2 ORLANDO INSIGHT

–– Scott FarisCEO

AeroSonix, LLC

“To advance prosperity in the region, we must focus on making strategic investments in growth segments of the advanced

technology market. Through this focused collaboration among government, industry and academia, we can offer the diversity

needed to accelerate innovation and protect against future economic challenges.”

“Advances in technology are both accelerating and enabling a new wave of economic progress and productivity that promises to reshape labor markets forever and potentially eliminate many

of the jobs that have driven our economic recovery. Orlando’s economic future must be as a source of innovation and talent, not

a victim of technological change.”

–– David FullerPresident

SunTrust FoundationChair, Orlando EDC

Challenges also persist in the labor market, where participation remains volatile and underemployment hidden. Wage stagnation has been the hallmark of the recovery nationally but has been particularly pronounced locally, where average weekly wages closed 2015 just $37 higher than in 2010. Much work remains to move the needle on persistent wage and income disparity.

Comfort has been found in a housing recovery that has reversed at least part of the wealth erosion of the previous decade, but the affordability issues of 2005 may yet return. Prices remain some 25 percent below pre-recession highs and sales volume in 2015 actually exceeded that of 2005. However, sustained double-digit price gains, elusive wage growth and the arrival of interest rate hikes in 2016 pose challenges. On the supply side, residential construction has been disciplined and has failed to add significantly to increasingly tight inventory levels.

A Community Agenda

As recession fades and growth normalizes, the time is nowto course-correct Orlando’s economic trajectory. We canchoose to drive structural economic change, build on existing strengths to ensure all sectors flourish equally, and embrace a targeted regional investment strategy that builds human capital and community capacity to deliver sustainable economic prosperity for all.

The road ahead is being paved with a solid foundation as the region begins to reap the benefits of its business branding campaign, “Orlando. You don’t know the half of it.” More companies are looking at Orlando as a business location after realizing the full potential of the region. The Orlando Economic Development Commission is seeing a 50 percent increase in its project pipeline relative to past years with prospect companies bringing a higher number of jobs that are associated with higher wages.

The Orlando MSA will welcome an additional 350,000 new residents by 2020, of which more than 200,000 will join the labor force. How we prepare for this influx and how we leverage that opportunity may be the challenge of our time.

= 1,000 jobs

Net Job Gains by Industry, Orlando MSADecember 2014 - December 2015

Source: Florida Department of Economic Opportunity

Leisure & Hospitality 33%

Business Services 21%

Trade, Transportation & Utilities 18%

Construction 7%

Government 7%

Finance 6%

Education & Health 5%

Manufacturing 3%

–– Jon RambeauVice President & General Manager

Lockheed Martin Training and Logistics Solutions

Around the Region - Coming in 2016

Osceola County: Construction on the $200 million Florida Advanced Manufacturing Research Center (FAMRC) should be substantially complete by the end of 2016. The first industry-led smart-sensor research and development center in the nation is a cooperative effort of Osceola County, the University of Central Florida, The Corridor, the Orlando EDC and Enterprise Florida.

Orange County: Mayor Teresa Jacobs and the National Center for Simulation will host the second annual Florida Simulation Summit September 22 at the Orange County Convention Center. The Summit highlights Florida’s growing simulation industry as well as opportunities for commercialization.

City of Orlando: The fourth annual Lake Nona Impact Forum

will take place February 24-26, convening more than 200

thought leaders from business, academia, government and

industry. The Forum provides a platform to highlight Lake

Nona Medical City and the City of Orlando to global leaders of industry as a leader in health,

product development and scientific research.

Seminole County: In May Seminole County will celebrate the opening of the new Seminole County Sports Complex.

The facility will offer 102 acres of premier tournament-quality fields across 15 lighted athletic fields, including nine synthetic turf fields. The complex will be home to more than

40 sporting events by the end of 2016 and is expected to generate 13,100 hotel room nights.

Lake County: The Minneola Interchange on Florida’s Turnpike began construction in January 2016. Less than 30 minutes to downtown Orlando and the tourist corridor, the interchange will bring 9,000 new homes and over 3 million square feet of new non-residential space to the City of Minneola.

ORLANDO INSIGHT First Quarter 2016 | 3

Labor Market

Labor Force1,222,042

Unemployment Rate4.3%

Initial Claims2,810

New Job Postings21,818

Arrows indicate change from previous year. Data for December 2015 unless otherwise specified.

• At 4.3 percent, unemployment closed 2015 at its lowest level in more than 7 years and down eight-tenths of a percentage point from year-end 2014. Declines in the unemployment rate have occurred throughout the region and in all four counties. Neighboring Ocoee and Winter Garden have the lowest rates.

First Quarter 2016 | 4 ORLANDO INSIGHT

Source: Florida Department of Economic Opportunity

Source: Florida Department of Economic Opportunity

• New claims for unemployment benefits have fallen below pre-recession levels. Claims are normalizing at a 12-month moving average of approximately 3,300.

“The success of Central Florida moving forward relies extensively, and perhaps exclusively, on our ability as a region to diversify and expand our economy into sectors that focus as much on high-tech, healthcare, and advanced manufacturing as they do on our benchmark industries of tourism and construction. This region is dedicated to training and growing our already talented pool of career seekers to sustain and encourage these emerging industries in our community.”

–– Pamela NaborsPresident & CEO

CareerSource Central Florida

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

New Claims12-MMA

Unemployment Rate (%, SA)

Unemployment Rate vs. New UI Claims, Orlando MSAThrough December 2015

Unemployment Rate New UI ClaimsRECESSION

60

65

70

75

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

%

Labor Force Participation Rate, Orlando MSAThrough Fourth Quarter 2015

Source: Moody’s

• Labor force participation decreased through 2015 and has helped accelerate declines in the unemployment rate. However, declines may prove more difficult to sustain moving forward as improving job prospects encourage workers to rejoin the labor force.

3.5%

3.6%

3.8%

3.8%

3.9%

3.9%

4.0%

4.0%

4.1%

4.1%

4.2%

4.8%

5.0%

3.9%

4.4%

4.2%

4.6%

4.7%

4.8%

4.5%

5.2%

4.4%

4.8%

4.9%

5.4%

5.7%

0% 2% 4% 6%

Winter Garden

Ocoee

Oviedo

Apopka

Orlando

Winter Springs

Winter Park

Casselberry

St. Cloud

Altamonte Springs

Clermont

Kissimmee

Sanford

Orlando MSA Area Unemployment RatesDecember 2015, Not Seasonally Adjusted

Dec-15Dec-14

ORLANDO MSA: 4.3%

Source: Florida Department of Economic Opportunity

Payroll Employment / Consumer Spending

Total PayrollEmployment1,183,300

Business ServicesEmployment195,500

ConstructionEmployment61,300

ManufacturingEmployment41,300

Taxable Sales$4.9 billion(October 2015)

Index of Retail Activity181.6(October 2015)

• Orlando’s net job creation of 38,100 in 2015, while less than in 2014, brought total net gains since late 2010 to over 180,000. Almost one in six jobs in the region today did not exist in 2010.

Arrows indicate change from previous year. Data for December 2015 unless otherwise specified.

ORLANDO INSIGHT First Quarter 2016 | 5

Source: Florida Department of Economic Opportunity

Source: U.S. Department of Labor, Bureau of Labor Statistics

• Although job growth has been uneven across sectors, the region nevertheless added over 25,000 jobs outside of our headline tourism industry, most prominently in the business services sector.

• Year-over-year employment growth closed 2015 at 3.3 percent. Among large regions, this was the highest rate in the South and the fourth highest in the country.

–– Sean Snaith, Ph.D.Director, Institute for Economic

Competitiveness University of Central Florida

Chair, Orlando Economic Forum

15.4

-23.4

25.0

15.3

56.050.9

40.0

12.0

-51.9 -50.9

12.1

19.4

31.937.9

50.3

38.1

-60

-40

-20

0

20

40

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Thousands Net Job Gain, Orlando MSANot Seasonally Adjusted

“I expect 2016 will see a continuation of Orlando’s strong job growth. Construction and business services will be key contributors.”

3.3%

3.2%

2.2%

3.0%

0.8%

3.0%

0% 1% 2% 3% 4%

Orlando

Tampa

Miami

Atlanta

Houston

Dallas

% Change in Payroll Employment, Southern MSAs > 1 Million JobsDecember 2014 to December 2015, Not Seasonally Adjusted

More

Number of Employees

Less

UNITED STATES: 1.9%

Source: Florida Department of Economic Opportunity

Commercial / Residential Real Estate

Office Vacancy13.6%(Q4 2015)

Office Asking Rate$20.94(Q4 2015)

Industrial Vacancy7.3%(Q4 2015)

Industrial Asking Rate$6.43(Q4 2015)

Existing Home Sales2,552

Median Home Price$185,000

Arrows indicate change from previous year. Data for December 2015 unless otherwise specified.

First Quarter 2016 | 6 ORLANDO INSIGHT

• All industrial submarkets except Lake Mary/Sanford recorded positive absorption in 2015, pushing vacancy down to 7.3 percent from 8.5 percent at year-end 2014. Leasing volume has been driven in part by demand from convention supply firms.

Source: Cushman & Wakefield, JLL

Source: Cushman & Wakefield, JLL

• Absorption in the office market closed 2015 at 1.4 million square feet, its highest level in over nine years. Market fundamentals may now support new speculative office development. Demand for Class A space is far outpacing the rest of the market, accounting for almost 60 percent of all leasing volume in 2015.

$0

$100,000

$200,000

$300,000

0

10,000

20,000

30,000

40,000

50,000

60,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Home Sales vs. Median Sales Price, Orlando MSA2000-2015

Sales Median Sale Price

Source: Orlando Regional Realtor Association

0

5,000

10,000

15,000

20,000

25,000

30,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015YTD*

Housing Permits, Orlando MSAUnits Authorized, 2000-2015

Single-Family Multi-Family

• Over 35,000 homes were sold in the region in 2015, a level surpassing even 2005 activity. Despite consecutive years of double-digit price growth, 2015’s median sales price of $178,500 remains almost 30 percent lower than the market’s peak of $248,000 in 2006.

• Although on the uptick, residential construction continues to prove relatively muted. Approximately 12,000 single-family homes are expected to be permitted in 2015, less than half the region’s peak of 27,000 in 2004. Multi-family activity is expected to finish the year closer to historic averages at 7,000 units.

*through NovemberSource: U.S. Census Bureau

Tenant Type Submarket SF

CVS Health New Tourist Corridor 112,329

Continental Casualty Company New Lake Mary 108,000

Synchrony Financial Services New Maitland 102,339

Wells Fargo Renewal Central Business District 81,857

Deloitte New Lake Mary 74,000

Akerman Renewal Central Business District 54,000

Office Market, Orlando MSASignificant Lease Transactions, 2015

Tenant Type Submarket SF

Freeman Expositions New Regency/Turnpike/Beeline 451,823

Tech Packaging New Silver Star/Apopka 200,000

Publix Food Markets New Regency/Turnpike/Beeline 190,100

Smart Warehousing Renewal Michigan/South Orange 144,000

J.J. Haines & Co. Renewal/Expansion Silver Star/Apopka 136,655

Shepard Exposition Services New Regency/Turnpike/Beeline 99,100

Industrial Market, Orlando MSASignificant Lease Transactions, 2015

Transportation / Visitor Industry

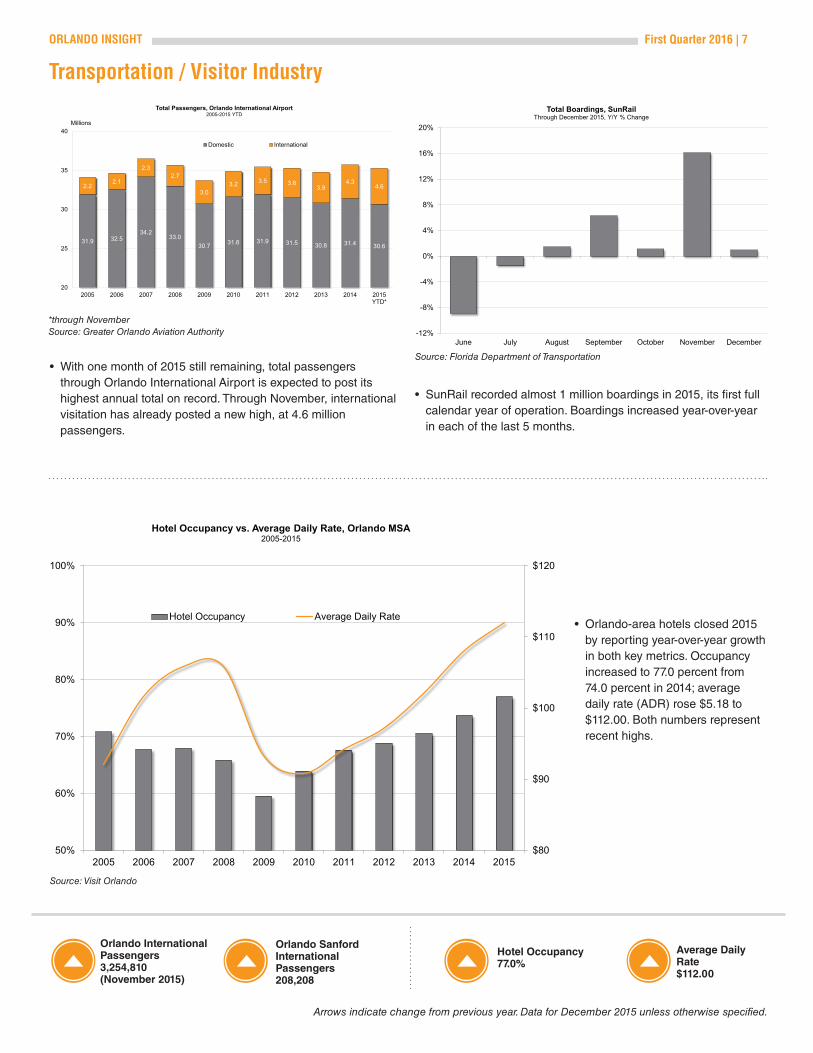

Orlando InternationalPassengers3,254,810 (November 2015)

Orlando Sanford InternationalPassengers208,208

Hotel Occupancy77.0%

Average Daily Rate$112.00

• With one month of 2015 still remaining, total passengers through Orlando International Airport is expected to post its highest annual total on record. Through November, international visitation has already posted a new high, at 4.6 million passengers.

Arrows indicate change from previous year. Data for December 2015 unless otherwise specified.

ORLANDO INSIGHT First Quarter 2016 | 7

*through NovemberSource: Greater Orlando Aviation Authority

Source: Visit Orlando

• Orlando-area hotels closed 2015 by reporting year-over-year growth in both key metrics. Occupancy increased to 77.0 percent from 74.0 percent in 2014; average daily rate (ADR) rose $5.18 to $112.00. Both numbers represent recent highs.

• SunRail recorded almost 1 million boardings in 2015, its first full calendar year of operation. Boardings increased year-over-year in each of the last 5 months.

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

June July August September October November December

Total Boardings, SunRailThrough December 2015, Y/Y % Change

Source: Florida Department of Transportation

31.9 32.534.2

33.030.7 31.6 31.9 31.5 30.8 31.4 30.6

2.22.1

2.32.7

3.03.2 3.5 3.8

3.94.3

4.6

20

25

30

35

40

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015YTD*

Millions

Total Passengers, Orlando International Airport2005-2015 YTD

Domestic International

$80

$90

$100

$110

$120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 201550%

60%

70%

80%

90%

100%

Hotel Occupancy vs. Average Daily Rate, Orlando MSA2005-2015

Hotel Occupancy Average Daily Rate

301 E. Pine Street, Suite 900 // Orlando, FL 32801 // P/ 407.422.7159 // orlandoedc.com

ABOUT THE EDCThe Orlando Economic Development Commission (EDC) is a not-for-profit, public-private partnership that works to aggressively attract, retain and grow jobs for the Orlando region while advocating, championing and educating in support of efforts to improve competitive position. The EDC serves Orange, Seminole, Lake and Osceola counties and the City of Orlando in Florida.

For more information, contact:

NEIL HAMILTONDirector, Business Intelligence [email protected]

Orlando Economic Forum

ELIZABETH GODWINAssociate Director, Business Intelligence [email protected]

Kimberly MakiBright House Networks

Leslie Molony, Ph.D.Sanford Burnham Prebys Medical Discovery Institute

Bill MossCBRE Co-Chair, EDC Business Development Committee

Pamela NaborsCareerSource Central Florida

Bob ProvitolaMitsubishi Hitachi Power Systems Americas, Inc.Chair, Manufacturers Association of Central Florida

Jon RambeauLockheed Martin Training and Logistics Solutions

Jerry RossNational Entrepreneur Center

Thomas K. SittemaCNL Financial GroupPast Chair, Orlando EDC

Jacob StuartCentral Florida Partnership

Rasesh ThakkarTavistock Group

Rick WeddleOrlando EDC

Vickie WhiteFlorida Hospital

CHAIRSean Snaith, Ph.D.University of Central Florida

MEMBERSThomas Baptiste, Lt. Gen., USAF (Ret.)National Center for Simulation

Cecelia BonifayAkerman, LLPChair, EDC Economic Strategy Committee

Phillip BrownGreater Orlando Aviation Authority

Bill MartinGreater Osceola Partnership for Economic ProsperityChair, Regional Economic Developers (RED) Team

Orlando EvoraGreenberg Traurig, LLP

Scott FarisAeroSonix, Inc.

David FullerSunTrust Foundation Chair, Orlando EDC

Larry HenrichsVisit Orlando

Daryl Holt Electronic Arts (EA Studios)

Steven JamiesonThe Mall at Millenia

Tony JenkinsFlorida Blue