Orissa Iron Ore Briefing Note - Incept Holdings · Page 7 concentrated in the 5 districts of the...

76

Orissa Iron Ore Briefing Note 16.01.11

Transcript of Orissa Iron Ore Briefing Note - Incept Holdings · Page 7 concentrated in the 5 districts of the...

Orissa Iron Ore Briefing Note

16.01.11

Page 2

Table of Contents

1. EXECUTIVE SUMMARY ............................................................................................... 6

2. ORISSA: STATE OVERVIEW ........................................................................................11

2.1. GEOGRAPHY .........................................................................................................11

2.2. DEMOGRAPHY ......................................................................................................11

2.3. STATE ECONOMY ..................................................................................................12

2.4. INDUSTRY ............................................................................................................. 13

2.5. MINING ................................................................................................................. 13

2.6. IRON ORE MINING ................................................................................................ 14

2.6.1. LOCATION OF MAJOR IRON ORE MINING AREAS ................................................. 15

3. ORISSA: GEOLOGICAL OVERVIEW ............................................................................ 16

3.1. PRECAMBRIAN SEQUENCE ................................................................................... 16

3.1.1. NORTH ORISSA - SINGHBHUM CARTON (NOC) ................................................... 16

3.1.2. WEST ORISSA CRATON (WOC) ............................................................................ 17

3.1.3. EASTERN GHATS BELT (EGB) ............................................................................. 18

3.1.4. PROTEROZOIC PLATFORM SEDIMENTS ............................................................. 18

3.1.5. GONDWANA SEDIMENTS .................................................................................. 18

3.1.6. TERTIARY - QUATERNARY – RECENT SEDIMENTS .............................................. 18

4. IRON ORE GROUP (SINGHBHUM CRATON) ................................................................ 19

4.1 SINGHBHUM CRATON: OVERVIEW ........................................................................ 19

4.2 IRON ORE GROUP (IOG) ........................................................................................ 19

4.2.1 GEOLOGICAL SETTING ...................................................................................... 19

4.2.2 ORE TYPES, GRADES AND MINERALIZATION CONTROL .....................................21

5. IRON ORE BELTS ......................................................................................................22

5.1 BONAI – KEONJHAR BELT (JAMDA – KOIRA BASIN) .................................................22

5.1.1 GEOLOGICAL SETTING .......................................................................................22

5.1.2 MINERALIZATION CONTROL ..............................................................................22

5.1.3 ORE TYPES, RESOURCE AND GRADE ..................................................................22

5.1.4 MAJOR DEPOSITS: BONAI – KEONJHAR BELT ..................................................... 23

5.1.5 GORUMAHISANI – BADAMPAHAR - SULAIPET (GBS) BELT .................................. 28

5.1.6 GORUMAHISANI – BADAMPAHAR – SULAIPET DEPOSITS .................................. 28

Page 3

5.2 TOMKA – DAITARI BELT ........................................................................................ 29

5.2.1 GEOLOGY OF BELT ........................................................................................... 29

5.2.2 MINERALIZATION CONTROL ............................................................................. 29

5.2.3 ORE TYPES, RESOURCE AND GRADE ................................................................. 29

5.3 GANDHMARDHAN BELT ....................................................................................... 30

5.4 HIRAPUR BELT ..................................................................................................... 30

5.5 IRON ORE POTENTIAL: ORISSA ............................................................................. 30

5.6 SUMMARY ............................................................................................................. 31

6. ORISSA IRON ORE MINING ....................................................................................... 33

6.1 MINING POLICY .................................................................................................... 34

6.2 INDUSTRY STRUCTURE AND MAJOR PRODUCERS OF IRON ORE ............................ 35

6.3 IRON ORE MINING IN ORISSA ............................................................................... 37

6.4 MINERAL BENEFICIATION .................................................................................... 39

6.5 OPERATIONAL RISK IN IRON ORE MINING IN ORISSA ............................................ 44

6.6 RECENT MINE CLOSURES IN ORISSA ..................................................................... 46

6.7 GREENFIELD TYPICAL MINING COST IN ORISSA ..................................................... 47

6.8 MINING OPERATION ............................................................................................. 49

7. OVERVIEW OF STEEL PRODUCTION IN ORISSA .......................................................... 51

7.1 INTEGRATED STEEL PLANTS ..................................................................................52

7.2 PIG IRON ...............................................................................................................52

7.3 SPONGE IRON ....................................................................................................... 53

7.4 ROLE OF GOVERNMENT OWNED IRON ORE MINING COMPANIES IN ORISSA .......... 54

8. ORE TRANSPORT AND LOGISTICS – RAIL AND ROAD ................................................. 55

8.1 VALUE CHAIN OF IRON ORE FROM MINES TO PORT / STEEL PLANT ......................... 55

8.2 RAIL LOGISTICS ..................................................................................................... 57

8.3 ROAD LOGISTICS .................................................................................................. 60

8.4 PORT INFRASTRUCTURE ...................................................................................... 63

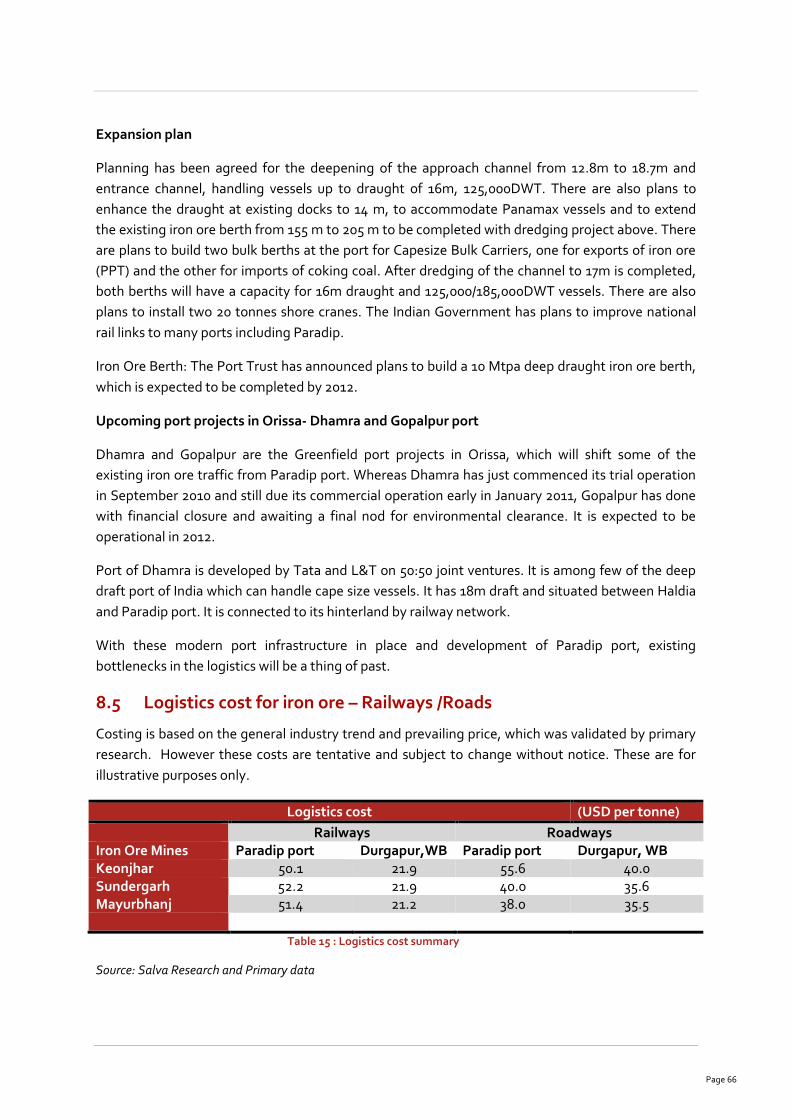

8.5 LOGISTICS COST FOR IRON ORE – RAILWAYS /ROADS ........................................... 66

9. COMPARISON OF MINING COSTS – ORISSA AND WESTERN AUSTRALIA .................... 68

10. EPILOGUE ............................................................................................................ 74

REFERENCES: .................................................................................................................. 75

Page 4

List of Tables

Table 1: Generalized stratigraphic sequence of North Orissa - Singhbhum Craton .......................... 20

Table 2: Iron ore resources of Orissa ................................................................................................ 31

Table 3: Major iron ore resource bearing districts ............................................................................ 32

Table 4: Working and non working mining areas, forest land* ........................................................ 34

Table 5 : Mining leases in major iron ore producing districts, Orissa* .............................................. 36

Table 6: Capital cost estimates ....................................................................................................... 49

Table 7 Operating cost estimates .................................................................................................... 50

Table 8: Steel companies operating in Orissa ...................................................................................51

Table 9 Steel capacity and production in Orissa .............................................................................. 52

Table 10: Integrated Steel Plants in Orissa ...................................................................................... 52

Table 11: Pig Iron Producers in Orissa .............................................................................................. 53

Table 12: District wise distribution of sponge iron capacity (%) ....................................................... 53

Table 13: Sponge iron producers in Orissa ....................................................................................... 54

Table 14: Iron Ore Volume- Paradip Port (Mt) ................................................................................. 64

Table 15 : Logistics cost summary ................................................................................................... 66

Table 16: Greenfield and Brownfield capital cost-Orissa ................................................................. 69

Table 17: Karara Iron ore mine project ............................................................................................. 72

Table 18: FOB cost Orissa Greenfield and Brownfield ...................................................................... 73

List of Figures

Figure 1: Orissa ……………………………………………………………………………………………………………….8

Figure 2: District map of Orissa ....................................................................................................... 12

Figure 3: Major iron ore districts of Orissa (haematite) .....................................................................15

Figure 4: Geological Map of Orissa (Source: Geological Survey of India) .......................................... 17

Figure 5: Geological Map of North Orissa – Singhbhum Craton showing Iron Ore Group (Source:

Beukes et al., 2003) ......................................................................................................................... 23

Figure 6: Geological Map of the Horse-shoe shaped synclinorium (Jamda – Koira basin), Western

Iron Ore Group. (Source: Ghosh and Mukhopadhyay, 2007) ............................................................ 25

Figure 7: Generalized Geological map of the eastern limb of Horse-Shoe synclinorium (Source:

Acharya, S., 2008) ........................................................................................................................... 26

Figure 8 : Cross sections (not to scale) from the eastern limb of synclinorium along the lines shown

in the previous figure. (Source: Acharya, S., 2008) .......................................................................... 27

Figure 9: Generalised geological map of the Tomka – Daitari belt from Southern Iron Ore Group

(Tomka – Daitari basin) showing spread of BIF with fault bounded Iron Ore deposits. (Source:

Acharya, S. 2008) ............................................................................................................................ 30

Figure 10: Major iron ore producers in 2010, Orissa ......................................................................... 36

Figure 11: Domestic consumption vs. Exports .................................................................................. 37

Figure 12: Manual mining ................................................................................................................ 38

Figure 13: Mechanized iron ore mining ............................................................................................ 38

Figure 14: Dry Screening process, Iron ore ...................................................................................... 41

Figure 15: Wet screening process, iron ore ...................................................................................... 42

Page 5

Figure 16: Wet screening with scrubbing, iron ore ........................................................................... 43

Figure 17 : Washing and gravity separation, iron ore ....................................................................... 44

Figure 18: General process flow of Iron Ore Supply Chain ............................................................... 55

Figure 19: Flow of Iron Ore in and around Orissa ............................................................................. 56

Figure 20: Value Chain Analysis- Rail Logistics ................................................................................ 58

Figure 21: Railway Map of Orissa .................................................................................................... 59

Figure 22: Value Chain Analysis- Road Logistics .............................................................................. 61

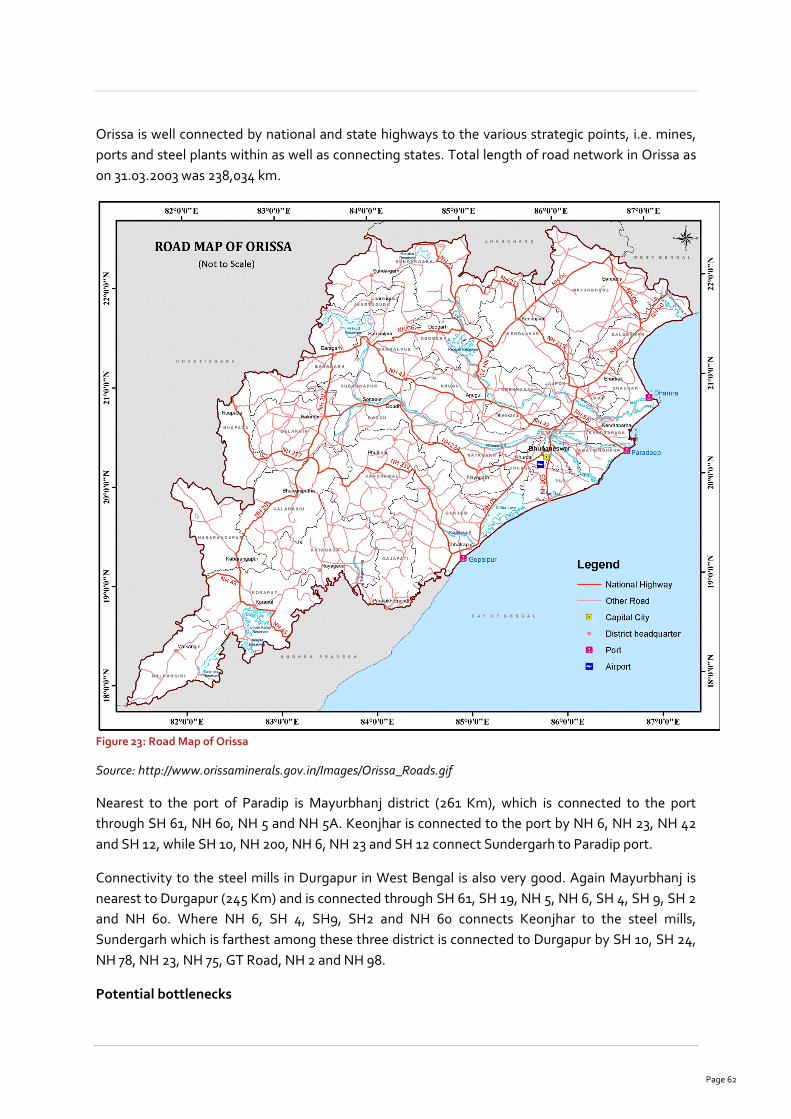

Figure 23: Road Map of Orissa ......................................................................................................... 62

Figure 24: Paradip Port- Satellite View ............................................................................................ 64

Figure 25 Paradip Port Layout ......................................................................................................... 65

Figure 26 : Gindalbie project map .................................................................................................... 71

Page 6

1. Executive Summary

Orissa is known for its rich mineral deposits and abundant source of water (both in the form of rivers

as well as an extensive coast line). In fact the state boasts of 16.92% of the total mineral reserves of

the country. However, there is fairly heavy concentration of Bauxite, Chromite, Graphite,

Manganese, Nickel ore, Coal and Iron ore in particular.

Industries in Orissa can grossly be divided in to four categories- cottage, medium, large scale and

large scale heavy industries. Since the state is rich in forest resources, it prompts the growth of

forest based industries. The cottage industry of Orissa includes- sericulture industry, cotton textile

mills, sugar mills and rice mills.

While the rich reserves of minerals in Orissa have led to establishment of several mineral based

industries in the state including- aluminium plants, charge chrome plants, sponge iron plants,

cement plants and coal based thermal power plants. With over 25% of India's iron ore reserves,

Orissa accounts for over 10% of India's steel production capacity and has a crucial advantage in the

iron & steel industry. Further, the presence of seaports in the state makes exports and imports cost

effective and more competitive. The state government has signed Memoranda of Understanding

(MoUs) with 45 companies for setting up steel plants of various capacities in the iron-ore rich parts

of the state.

India’s richest and biggest deposits are mostly confined to Banded Iron Formations (BIF) of

Precambrian age. The Iron Ore Group covers the Mayurbhanj, Keonjhar, Sundargarh and Jajpur

districts of Orissa and is exhibit the major and high grade deposits of Eastern India.

The Iron Ore deposits from Orissa are divided into five geographic belts: 1. Bonai – Keonjhar belt, 2.

Gorumahisani – Badampahar –Sulaipet belt, 3. Tomka – Daitari belt, 4. Gandhamardhan belt and 5.

Hirapur belt. The Iron Ore from these deposits are of various types as hard massive, soft laminated

and powdery blue dust though lateritic ore occur at places in the upper profile. Gradational or sharp

transition may occur from one type of ore to other type both vertically and laterally.

Mayurbhanj, Keonjhar, Sundargarh and Jajpur districts from Orissa bear the major high grade

(+60% Fe) hematitic deposits from these belts and contribute to the 60% of total Indian iron ore. As

per the information available from Director of Geology and Director of Mines, Orissa, the state has

5306 MT of iron ore deposits of which 3000 MT belong to leasehold areas and the rest 2306 MT

belongs to freehold areas thus making it worth to explore and workout for iron ore in the state.

Because of the abundant mineral resource base, its strategic proximity to major iron ore consumers

in the world market, Orissa offers an excellent investment opportunity for mining companies and

iron and steel manufactures.

As per the recent estimate of Directorate of Geology,Government of Orissa, the total iron ore

resources in the state is around 5306 Mt which is predominantly in the form of hematite and

Page 7

concentrated in the 5 districts of the state. Koenjhar being the leading district with a resource base

of around 3574 Mt.

The Government of Orissa is under the process of finalizing a separate mining policy and the draft

Orissa Mining Policy will be announced very soon. As per the press release, the new mining policy

will focus more on non-ferrous sector rather than on ferrous minerals.

The existing mineral based industries have been covered under Orissa Industrial Policy 2007. Its

salient features pertaining to Mineral based industries are:

- Promotion of development of infrastructure via Public Private Partnership (PPP)

mode to support sustainable investment in the field of mining and mineral

processing.

- Strengthening of regulatory and institutional arrangement for implementation of

environment laws, formulation of Rehabilitation & Resettlement Policy by

adopting a holistic livelihood approach for rehabilitation and resettlement of

project affected families.

- Strengthening of arrangement for industrial promotion and investment

facilitation at various levels

- Creation of SEZs and more thrust on human resource development and

employment

As a matter of policy only low and medium grade ore (up to 64% Fe), fines and temporary surplus

high grade iron ore (+67 % Fe), particularly from Bailadila (Chattisgarh) is being exported to

importer countries.

Iron ore industry in Orissa is vastly fragmented. Except for few industry giants, mining in these areas

are dominated by small and marginal players with a leasehold area of as low as 1.2 hectares. These

small players generally cater the need of domestic industry and export surplus iron ore to China

mainly via Paradip port. Across districts, Koenjhar has maximum number of small mining players

particular in the region of Barbil while Jajpur has the least. Production wise Essel mining is the

biggest producer of iron ore Calibrated iron ore lumps and Iron ore fines.

Mechanization of iron ore mining was pioneered by Tata Steel, which is prevalent across the various

mines in the state. Manual mining is gradually phasing out but still some area in Orissa particularly

Barajamada region it persists. In most of the highly mechanized mines more than 50-60% fines are

being generated.

Most of the mineral deposits in the states are located in the forest land which are inhabitated by

tribal population, who heavily depends on forest land for their live hood and are least adaptive to

social and economic changes. This has resulted in significant protest and several social hurdles in

land acquisition activity. The forest cover in the State constitutes 31.38% of the geographical area.

Besides this, there exists tree cover outside the forest over 2.85% of the geographical area of the

State. While some mining activities are confined to non-forest areas, substantial portion of the

remaining mining zones come under degraded and open forest areas.

Page 8

Sourcing of skilled human resources in these remotely located sites can also be a potential

showstopper for the project in the absence of local skilled population.

Another major hurdle is to obtain all the regulatory approval for commencement of on- site

activities. This whole process is often arduous and time consuming causing major delays in project

commission resulting huge cost implication to the project proponents. However, the Government

of India has made amendments in existing Mines and Mineral Regulation and Development act

(MMDR) by way of stipulating time frame in order to minimize time elapsed in grant of mineral

concession. The Proposed MMDR Bill 2010 (expected to get approved by parliament of India) has

gone one step further and stipulates an independent mining regulator in the form of Mining

tribunal. This will not only smoothen the process flow but also bring transparency in the grant of

mineral concession.

Apart from above mentioned risks, there are also minor operational and regulatory risks involved

with iron ore mining in Orissa.

Till November 2010, government of Orissa has so far suspended the operation of 246 mines for

violation of statutory norms. This has been considered a step taken to crack down prevailing illegal

mining activities. The operation of these mines has been suspended due to various reasons

including pending environmental clearance, pending forest clearance, non-approval of Mining Plan

by IBM, non-payment of Net Present Value (NPV) for diversion of forest land for mining activities

and want of no-objection certificate from the State Pollution Control Board (SPCB).

Despite of all odds, domestic consumption of iron ore for the period of 2005-2009 grew at

compounded annual growth rate of 13.96% while the exports for the same period grew at

compounded annual growth rate of 10.33%. The pace of growth of the steel industry in Orissa is

likely to be faster in coming years.

Iron ore Supply Chain

After crushing, screening and beneficiation process iron ore fines and lumps are transferred to the

mine stocking area; thereafter it is transferred to the trucks/ trailers either to the nearest railway

siding or directly to the destination. However, most of the iron ore transits from mine area to port/

steel plants take railway route.

Rail, road connectivity and bottlenecks

Districts of Sundargarh, Keonjhar and Mayurbhanj are well connected with Paradip port and steel

plants in Durgapur, West Bengal. Most of the iron ore mines in the district have their own railway

siding and most of the transportation takes railway route, except for the smaller mine owners which

use roads for inland logistics.

In order to curb export of iron ore and to boost domestic production of downstream steel products,

rail freight for exporting iron ore is charged higher making logistics cost sometimes significantly

high compared to road. It does not only disturb iron ore pricing for short term, but also deters mine

owners from long term planning.

Page 9

Lower axle load and the heavy penalty on overloading the rakes are other pain areas in rail

transportation. Also freight traffic has low average speed leads to longer lead times, while

preference of passenger trains over cargo train creates congestion and reduces throughput at port.

Orissa is well connected by national and state highways to the various strategic points. However,

road does not constitute significantly to the coal transportation as compared to rail transportation.

Most of the highways are narrow and congested while some of the state highway or connecting

roads are not even two lanes. Apart from number of lanes, overall conditions of roads are also poor.

Due to these reasons lead time increases and safety get jeopardized.

Fragmented transportation industry in India lacks organized fleets and show no or poor

professionalism.

Port infrastructure, bottlenecks and expansion plans

Orissa has a long coast line of 480 km, with Paradip as the major all weather port. The port has its

own railway system and connected to East Coast Railways. It is also connected to NH-5A and State

Highway 42.

However, mmodernization of all machinery and mechanization of jetty is the need of the hour. As

cargo handling systems are obsolete and hence reduces overall port productivity. Also the draft at

Paradip port is 12.5, which is not sufficient to accommodate cape size vessels.

Plan is to deepen the approach channel to 18.7m and to extend the existing iron ore berth from 155

m to 205 m to be completed with dredging project above. There are also plans to install two 20

tonnes shore cranes.

Dhamra and Gopalpur are the Greenfield port projects in Orissa, which will shift some of the

existing iron ore traffic from Paradip port. Whereas Dhamra has just commenced its trial operation

in September 2010, Gopalpur is expected to be operational in 2012.

Port of Dhamra is developed by Tata and L&T on 50:50 joint ventures. It is among few of the deep

draft port of India which can handle cape size vessels. With these modern port infrastructure in

place and development of Paradip port, existing bottlenecks in the logistics will be a thing of past.

State is endowed with a range of high-grade minerals. But, these are not exploited properly. With

around 85% of its population living in the rural areas and mostly depending upon agriculture and

allied activities for their livelihood, it is imperative to alleviate its status quo. However, over a recent

past a lot of positive changes in the rural pocket have been observed. Be it literacy rate (both for

male as well as female), Gross State Domestic Product, State income, per capita income or the

development of roads, transport and communication networks; substantial improvement is evident

in all spheres. If more stress could be put on proper maintenance and supervision of different service

infrastructures, it will be easier for Orissa to accelerate its pace of economic development.

The iron and steel industry of Orissa has played a major role in bringing the industrial boom in the

state. The state government of Orissa has invited and signed various ‘Memorandum of

Page 10

Understanding’ (MoUs) with major industrialists and investors. It has achieved a considerable

amount of success and several prime companies have set up their plants in the state.

With only two steel plants till 1995, marginal growth was achieved between 1995 and 2000. But

from 2000 onwards the steel industry in the state witnessed a rapid growth in iron and steel sector.

Today Orissa hosts around 143 iron and steel plants with a combined capacity of 12.3 Mt which is

nearly 16% of the total steel capacity in India. The steel industry in Orissa consumes nearly 11 Mt of

iron ore. Nearly all the requirement of iron ore is sourced from the mines located in Orissa only.

With a planned investment of USD $ 456 billion on the infrastructure development in the current

five year planning period (2007-12) and projected 10 % growth in domestic demand in near future,

Iron ore mining in Orissa is set to achieve new industry heights in coming years. The mining scenario

in Orissa compares very favorably with Western Australian mining industry. Low cost of operation

and infrastructure costs enable mines in Orissa to operate very profitably.

Page 11

2. Orissa: State Overview

2.1. Geography

Orissa is a coastal state in the eastern region of India. It is adjacent to four other states, West Bengal

and Jharkhand to its north, Chhattisgarh to its west and Andhra Pradesh to its south. It is bounded

by the Bay of Bengal on the east and has an extensive coast line of 482 Km.

Figure 1 : Orissa, India

Source: Salva

The state is rich in mineral resources such as coal, iron-ore and bauxite, chromite amongst others.

Bhubaneshwar is the capital of Orissa. Cuttack, Rourkela, Berhampur, Baleshwar and Puri are the

other important cities of the state. With 4.74% of India's landmass Orissa coastal plains are the

depositional landforms of recent origin and geologically belong to the Post-Tertiary Period.

2.2. Demography

The population of Orissa is 36.8 million as per the 2001 population census. Orissa has an area of

155,707 sq. km giving a population density of 236 per sq km and the density is much lower than the

all-India average of 313 per sq km. Nearly 85% of its population lives in the rural areas and mostly

depend on agriculture and allied activities for their livelihood.

Page 12

Figure 2: District map of Orissa

Orissa has 30 districts which are further subdivided into 314 blocks and 316 tehsils. The districts are

marked out in the map above.

2.3. State Economy

The Gross State Domestic Product (GSDP) at constant prices (1999-2000) of Orissa registered an

annual average growth rate of 9.5% for the 10th Five Year Plan (2002-07) as compared to 5.3%

achieved in the 9th Plan (1997-2002). In the first three years of the 11th Plan (2007-12), the state has

recorded an annual average growth rate of 8.7% in spite of the challenges of global financial crisis

and as per the advance estimates; it grew by 8.3% during 2009-10 to INR 902 bill (US $19bill). The

standard of living in Orissa has been below average since Independence. But the falling trend in real

per capita income has not only been arrested in 2004-05, but reversed as well, thus reducing the gap

of per capita income between Orissa and the all India average. The per capita net national product

of Orissa was INR 19,456 (US $410) in 2009-10. The number of people below poverty line is now

39.9% as against 47.2% in 1999-2000.

The structure of Orissa’s economy has also witnessed radical shift from being an agrarian economy

to a service economy, mirroring the transformation occurring to the Indian economy as a whole.

Service sector which used to contribute just 37% of the state GDP in 1989-90, now contributes 55%,

Page 13

while the share of agriculture has come down to just 20% in 2008-09 as compared to 49% in 1989-

90. Notable development has been achieved in the share of industry which has increased from 15%

in 1989-90 to 25% in 2008-09 mainly driven by growing mining, aluminium and steel sectors.

2.4. Industry

While agriculture remains the principal occupation of the majority of the state's population, the

state has witnessed an industrial upsurge due to the favourable industrial atmosphere, political

stability and abundance on natural resources in the state. The state government of Orissa has

invited and signed various Memorandae of Understanding (MoU) with major industrialists and

investors. It has achieved considerable amount of success and several major companies have set up

their plants in the state with a large number of projects being in the pipeline.

Industries in Orissa can be grossly divided in to four categories- cottage, medium, large scale and

large scale heavy industries.

The state is rich in forest resources, which has prompted the growth of several forest based

industrial plants. The cottage industry of Orissa includes- sericulture industry, cotton textile mills,

sugar mills and rice mills

The small scale industries of Orissa include- brass industry, tobacco industry, beverage, molasses

and aluminium utensil making plants.

The large scale medium and large scale heavy industries include- cement industry, ceramic glass

plants, refractory units, ferro manganese plants, aluminium industry, fertilizer plants, agro based

industries, chemical industries, tyre factories and aeronautical industry.

The iron and steel industry of Orissa has played a major role in bringing the industrial boom in the

state. There are several steel and sponge iron plants operational in Orissa. The Rourkela Steel Plant

of SAIL is one the best in the country.

2.5. Mining

The state is a treasure trove of minerals and natural resources. With reserves of bauxite, chrome,

iron ore, coal, manganese, Orissa has been blessed with major industrial minerals. Vast and diverse

mineral deposits make Orissa one of the largest minerals bearing states in India. In fact the state

boasts of 16.92% of the total mineral reserves of the country. Mineral reserve of Orissa in respect of

chromite, nickel ore, graphite, bauxite, iron ore, manganese and coal is about 97.37%, 95.10%,

76.67%, 49.74%, 33.91%, 28.56% and 27.59% respectively of the total deposits in India.

The rich reserves of minerals in Orissa have led to establishment of several mineral based industries

in the state including the Rourkela Steel Plant (RSP), aluminium plants by National Aluminium

Company (NALCO), and ferro chrome plants at Bahmanipal, Bhadrak and Choudwar by Orissa

Mining Corporation (OMC), Ferro Alloys Corporation (FACOR) and Indian Charge Chrome Ltd.

(ICCL) and others. At Theruvalli in Rayagada district, Indian Metals and Ferro-Alloys (IMFA) have set

up a plant for production of charge chrome / ferro chrome. The other important mineral based

Page 14

industries established include two sponge iron plants in Keonjhar district, a refractory in Dhenkanal

district and mineral sands separation and synthetic rutile plants of Indian Rare Earth Ltd. at

Chhatrapur in Ganjam district. Several cement plants have been set up in the State and four coal

based thermal power plants have been set up at Talcher, Kaniha, Ib Valley and Banharpalli. In

addition NALCO, RSP, ICCL, INDAL etc. have set up their own coal based captive power plants.

There are several ferro alloy plants in operation in the state.

Aluminum

Orissa is the largest producer of aluminum in India. In 2005-06, it produced over 415,000 tonnes of

aluminum, representing around half of India's total aluminum production, Orissa's key advantage

for aluminum industry is the fact that the state accounts for half of India's bauxite reserves. Its

location makes it close to the Chinese and South East Asian markets and the presence of large ports

makes it easier to access large export markets.

Ferro-Alloys

There are two big Ferro Manganese plants in operation in the State. First Ferro-Manganese plant

located at Joda in Keonjhar District is run by The Tata Iron & Steel Co. Ltd. The second plant at

Rayagada in Koraput District is managed by Jeypore Sugar Co. Ltd. There are several other smaller

ferro alloy plants in operation in the state.

2.6. Iron ore mining

With about 32.9% of India's iron ore reserves, Orissa accounts for over 10% of India's steel

production capacity and has a crucial advantage in the iron & steel industry. Further, the presence

of seaports in the state makes exports and imports cost effective and more competitive.

The state government has signed Memoranda of Understanding (MoU) with about 45 companies

for setting up steel plants of various capacities in the iron-ore rich parts of the state.

These include:

POSCO signed a MoU with Government of Orissa to set up a 12 Mt integrated steel plant at

Paradip with an investment of INR 510 bill (US $ 11.3 bill).

ArcelorMittal signed a MoU to set up a 12 Mt integrated steel project at Patna in Keonjhar

District with an investment of INR 400 bill (US $ 8.9 bill).

Tata Steel plans to develop a 6 Mt steel plant at Duburi with an investment of INR 154 bill

(US $ 3.4 bill).

Vedanta Resources Plc plans to set up a 5 Mt steel plant in Keonjhar district of Orissa at an

approximate cost of INR 125 bill (US $ 2.8 bill).

Page 15

Essar Steel Plans to set up a Greenfield steel plant in Orissa with a capacity of 4 Mt with a

likely investment of over INR 68.5 bill (US $ 1.5 bill).

Jindal Stainless Ltd. is setting up a Greenfield stainless steel complex in Jajpur district with

an investment of around INR 16.1 bill (US $ 357.8 mill).

2.6.1. Location of major iron ore mining areas

Figure 3: Major iron ore districts of Orissa (haematite)

Sundergarh, Keonjhar and Mayurbhanj are the three districts where large scale iron ore mining is

being carried out. These districts have rich reserves of high and medium grade iron ore which are

being mined for domestic consumption and export to China.

Page 16

3. Orissa: Geological overview

Orissa forms an integral part of Indian Peninsular Shield and portrays a complete geological

sequence ranging from Archaean to Quaternary. The complex geological history of Orissa is

attributed to Precambrian sequences which occupy most of the northern, western, central and

southern part of Orissa. Proterozoic platformal sediments cover the extreme western fringe directly

overlying the Cratonic assemblage. Gondwana Group of rocks were laid in Mahanadi Graben along

the North Orissa Boundary Fault (NOBF). Coastal part of the Orissa is covered by the Tertiary –

Quaternary - Recent sequence (Fig.4; Source: Geological Survey of India).

3.1. Precambrian Sequence

Precambrians of Orissa are discussed in three different tectonic terrains as: 1. North Orissa Craton

(NOC), 2. West Orissa Craton (WOC) or Bastar Craton and Eastern Ghats Granulite Belt (EGB)

(Fig.1). NOC occupy the northern part of Orissa and is separated from WOC and EGB by a North

Orissa Boundary Fault (NOBF). WOC occupy the western part while EGB covers the central and

southern part of Orissa separated by West Orissa Boundary Fault of Mahalik (1996).

3.1.1. North Orissa - Singhbhum Carton (NOC)

North Orissa Craton or North Orissa - Singhbhum Craton covers the Mayurbhanj, Keonjhar,

Balasore, Dhenkanal, Deogarh, Sambalpur and Sundergarh districts of Orissa along with part of

Jharkhand (previously Bihar).

Archaean Supracrustal sequence, Older Metamorphic Group (OMG), is considered as oldest unit in

the geology of Orissa. OMG comprises of meta-sedimentary and meta-basic rocks and are

synkinematically intruded by the tonalite gneisses designated as Older Metamorphic Tonalite

Gneiss (OMTG). The OMTG marks the earliest granitoid event and is considered as an anatectic

product of OMG which were later intruded into OMG at a greater depth. Both OMG and OMTG

occur as enclaves within the Singhbhum Granite (SBG) and show two phases of deformation. SBG,

which belongs to granodiorite-adamellite-granite suite, is believed to have emplaced in three

different phases designated as SBG-I, SBG-II and SBG-III. Chakradharpur granite gneiss, Nilgiri

granite and Bonai granite are considered as equivalent to the Singhbhum granite and fringe the

northern, eastern and western margin of Singhbhum granite respectively. Mahadevan (2002)

designated Singhbhum granite complex, earliest continental segment to get cratonised, together

with Archaean supracrustals as Archaean Cratonic Core Region (ACCR).

Emplacement of Singhbhum granites (SBG-I and SBG-II) and equivalent granites was followed by

the deposition and subsequent deformation of Iron Ore Group (IOG) consisting of Banded Iron

Formations (BIF), metasedimentary and metavolcanic rocks. IOG is believed to have deposited into

three major basins over OMG: 1. Gorumahisani – Badampahar basin, 2. Tomka – Daitari basin and 3.

Jamda – Koira basin, along eastern, southern and western margin of ACCR respectively. The Jamda

– Koira basin bears the abundant BIFs which display horse-shoe shaped syncline plunging gently (8°

to 10°) towards NNE. Jamda – Koira basin host the rich deposits of Iron and Manganese. The third

phase of Singhbhum granite (SBG-III) is dated younger to IOG (Fig.5).

Page 17

The volcano-sedimentary sequence of the Dhanjori group rest unconformably over Singhbhum

granite and IOG and in turn are overlain by Singhbhum Group composed of metamorphosed

psammo-pelitic and pelitic rocks. Singhbhum Group is classified into Lower Chaibasa and Upper

Dhalbhum Formation separated by an unconformity. Kolhan group of rocks were deposited in a

narrow elongated depression to the west of Singhbhum Granite and are made of shale, limestone,

sandstone and intruded granites.

Gangpur Group of rocks were laid in the Gangpur basin, described as an anticlinorium by M. S.

Krishnan (1937), is now interpreted as a reclined fold refolded into antiform by Banerji (1968). The

stratigraphic status of the Gangpur Group is disputed and was correlated with Koira Group,

Singhbhum Group and the Kolhan Group. It is made up of carbonaceous metapelites, dolomite,

limestone and gondites.

3.1.2. West Orissa Craton (WOC)

The West Orissa Craton, bounded by Mahanadi rift in the north, Godawari rift in the south and EGB

in the east, is dominantly composed of granite and granite gneisses which are overlain by the

Archaean Bengpal Group and Paleoproterozoic Bailadila group of supracrustal rocks. Bengpal group

is composed of granite, gneisses and metasedimentary rocks. Both Bengpal and Bailadila group

cover part of western Orissa and extend into state of Chhattisgarh where BIF bearing Bailadila

group bears the rich deposits of Iron Ore.

Figure 4: Geological Map of Orissa (Source: Geological Survey of India)

Page 18

3.1.3. Eastern Ghats Belt (EGB)

The Proterozoic EGMB follows the East coast of India in an arcuate fashion over 1000 km from the

Brahmani River in the north to Ongole in the south. It is crossed by two Mesozoic rift valleys,

namely Mahanadi rift in the north and Godavari rift in the south, interrupting its continuity. It is

surrounded on three sides by Archaean cratons, namely the Dharwar, Bhandara and Singhbhum

Cratons.

Ramakrishnan et al. [1998] classified the rocks of the EGMB into four zones, namely the Western

Charnockite Zone (WCZ), Western Khondalite Zone (WKZ), Central Migmatite Zone (CMZ) and the

Eastern Khondalite Zone (EKZ). WCZ consists of charnockites, mafic granulites and banded iron

formation where WKZ is dominated by typical metapelite called khondalite, with intercalations of

quartzite and calc silicate rocks and high Mg-Al granulites intruded by charnockites, enderbites and

massive anorthosite. CMZ is dominated of migmatitic gneisses, mafic granulites and calc-silicate

rocks intruded by charnockite-enderbite, granites and anorthosites. EKZ is made of khondalites.

Quartzite can be seen in all zones but occur dominantly in area north of Mahanadi lineament. They

occur in association with the diopside – garnet bearing calc-silicate rocks in several parts of the belt

especially in WKZ and EKZ.

3.1.4. Proterozoic Platform Sediments

Mesoproterozoic to Neoproterozoic platformal sediments were laid down in the different small

isolated basins named as: Abujhmar, Ampani, Khariar, Indravati and Sukma basins. These basins

occur in the western part of Orissa and bear undisturbed sequence of shale, limestone and

sandstone.

3.1.5. Gondwana Sediments

Predominantly Continental freshwater sediments belonging to Gondwana Supergroup,

accumulated during the Late Carboniferous to Early Cretaceous period, are found to occur in

number of small and isolated basins of Mahanadi rift traversing across the northern Orissa as shown

in the figure 1. These sediments bear the coal measures in Orissa.

3.1.6. Tertiary - Quaternary – Recent Sediments

Quaternary geology of the state is portrayed by the laterites of both high and low level formed

under the arid and humid climatic conditions. Laterites form a capping over the older formations

and cover a major portion of Eastern part of Orissa.Recent to subrecent sediments, charaterized by

the cyclic sedimentation of gravel, sand along with clay, occur as narrow and disconnected pockets

along the coastal plains. Over the Eastern Ghats belt, plateau capped bauxite are found over the

granulitic rocks.

Page 19

4. Iron Ore Group (Singhbhum Craton)

4.1 Singhbhum Craton: Overview

Singhbhum Craton, the Archaean nuclei, is a triangular crustal block spread over approximately

40,000 km2 and covers the part of Orissa and Jharkhand states. The Singhbhum Craton shows the

geological events ranging from Archaean to Mid-Proterozoic (Fig.2). Though there prevails

numerous controversies over the status of different groups, a generalized stratigraphic sequence of

Singhbhum Craton is given as below in Table 1.

4.2 Iron Ore Group (IOG)

4.2.1 Geological Setting

The Archaean Iron Ore Group (IOG), a well known and significant stratigraphic unit from

Singhbhum Craton, hosts the rich deposits of Iron Ore (Fig.2) of Sundergarh, Mayurbhanj, Keonjhar,

Jajpur, Nawrangpur and Sambalpur districts of Orissa along with the part of the Jharkhand state.

Iron Ore Group is a collective term coined for three discrete greenstone belts composed of

metasedimentary and metavolcanics rocks bearing extensive BIF units with subordinate banded

chert and carbonate beds. IOG is believed to have deposited over OMG in three different basins: 1.

Gorumahisani – Badampahar basin, 2. Tomka – Daitari basin, 3. Jamda – Koira basin. These three

basins fringe the Singhbhum Craton (precisely ACCR); while Tomka – Daitari basin occur to the

south, Gorumahisani – Badampahar basin and Jamda – Koira basin occur to the east and west of

ACCR respectively. They are also called Eastern, Western and Southern IOG (Fig.2). While Sarkar

and Saha (1983) include all the three basins in a single IOG, Banerji (1974) proposed two fold

classification and divided them into older Badampahar Group and younger Koira Group separated

by Jagannathpur Volcanics. Badampahar Group includes the Gorumahisani – Badampahar and

Tomka – Daitari basins while younger Koira Group includes the western Jamda – Koira basin.

Page 20

Table: Generalized Stratigraphic sequence of the North Orissa – Singhbhum Craton

Newer Dolerites

Kolhan Group

---------------------Unconformity------------------------

Jagannathpur Lava

Singhbhum Group

Dhanjori Group

----------Unconformity, Disconformity and Angular unconformity------

Jamda – Koira Basin (Western IOG)

---------------------Unconformity------------------------

Tomka - Daitari Basin (Southern IOG)

---------------------Unconformity------------------------

Gorumahisani – Badampahar Basin (Eastern IOG)

-------------------Non-conformity------------------------

Singhbhum Granite (SBG) Phase I and II

Older Metamorphic Tonalite Gneiss (OMTG)

Older Metamorphic Group (OMG)

No

rth

Ori

ssa

- S

ing

hb

hu

m C

rato

n

Pre

-IO

G S

eq

ue

nce

Ir

on

Ore

Gro

up

(IO

G)

Table 1: Generalized stratigraphic sequence of North Orissa - Singhbhum Craton

Page 21

Badampahar Group

Badampahar group, also called as Gorumahisani Group by some authors, is a 120 km long belt

trending NNE to NW with a maximum width of 10 km. The group is chiefly composed of mafic to

ultramafic, metabasics, metapelites, BIF, quartzite and calcareous sediments.

Koira Group

Koira Group, deposited in the Jamda – Koira basin, exhibits the most spectacular BIF defining a well

known broad Horse Shoe shaped synclinorium plunging gently towards NNE. Though, all three

basins hosts the Iron Ore deposits, Jamda – Koira basin (Koira Group) or Western Iron Ore Group

bear the major Iron Ore deposits of India.

4.2.2 Ore Types, Grades and Mineralization Control

Banded Iron Formations represented by Banded Hematite Quartzite (BHQ) / Banded Hematite

Jasper (BHJ) host the high grade Iron Ore from the IOG. The Iron Ore from IOG are dominantly of

stratabound type while detrital colluvial and recent alluvial deposits also can be found at some

places. Beukes et al., (2003) have suggested supergene-modified hydrothermal processes for the

origin of these Iron Ores deposits.

Iron Ore from IOG can be classified broadly into massive, laminated and powdery ore. Massive ore is

hard, compact and may vary in grade from 64% to 68% Fe. High grade massive ore bodies grade

into partly mineralized BIF to completely unmineralized BIF, vertically as well as laterally.

Laminated Iron Ore, which is porous, soft and friable, sometime occurs in close association with

massive ore with Fe content varying from 62% to 65%. Powdery Ore is fine, grayish blue colored

and occurs as small pockets or bands and may vary in grade from 65% to 68% (Fe). Hematite,

Magnetite, Goethite, siderite and maritite are the ore minerals which make the varieties of Iron Ore

though Hematite and Magnetite are dominant ore minerals along with subordinate amount of

goethite and martite as alteration product. High grade Iron Ore deposits from Koira Group or

Western IOG are chiefly composed of Hematite while those from Badampahar Group are

dominated by Magnetite along with subordinate amount of other iron ore minerals. Hard massive

variety of Iron Ore may bear mainly Hematite along with subordinate amount of magnetite and

martite; this massive variety at places grades along with depth into soft blue dust variety chiefly

composed of Hematite with small amount of goethite and martite. Upper levels of deposits

generally bear the oxidation product and are chiefly composed of goethitic ore.

The mineralization in the IOG is more or less controlled by the Structural patterns developed by the

three phases of deformation that the area has undergone. Different generation of folds and faults

play important role in disposition of the ore bodies, their size, shape and their subsurface extent.

Superimpositions of different generations of folds give rise to different interference patterns and

thus form the suitable locale for the migration of ore material. While tight and isoclinal folds of later

generation superimposing over the earlier generation give rise to minor faults which dislocates the

ore body forms the isolated pockets enriched in iron ore. It is believed that the different sets of

faults marks the pathway for the mobilization of ore material which is further evidenced by the rich

iron ore deposits bounded by fault sets.

Page 22

5. Iron Ore Belts

Iron Ore deposits of Orissa, which occur in three isolated but interconnected basins belonging to

IOG, are divided geographically into five belts or zones as follow: 1. Gorumahisani – Badampahar -

Sulaipet Belt, 2. Tomka – Daitri Belt, 3. Bonai – Keonjhar or Jamda – Koira Belt, 4. Gandhamardhan

Belt and 5. Hirapur Belt.

5.1 Bonai – Keonjhar Belt (Jamda – Koira basin)

Bonai – Keonjhar Belt occurs to the west of ACCR covering Keonjhar and Sundargarh district of

Orissa. The BIF from Bonai – Keonjhar belt display spectacular form of horse shoe and hence the

term was coined by Jones in his pioneer work as Horse – shoe synclinorium. Bonai – Keonjhar belt is

the most significant belt and bear the major iron ore deposits of Eastern India (Fig.3)

5.1.1 Geological Setting

The rocks from Bonai – Keonjhar belt, laid in a Jamda – Koira basin, overlie the OMG to the East and

Bonai granite to the west. Jamda – Koira basin bear essentially three units: Lower shale, BIF and

Upper shale where BIF host the high grade iron ore deposits of the belt (Fig.3).

5.1.2 Mineralization Control

The mineralization in the deposits from Bonai – Keonjhar belt is structurally controlled. The entire

belt is described as northeasterly plunging synclinorium by Jones (1934). The western limb of the

synclinorium has got overturned while eastern limb (Fig.4) has been folded into several anticlines

and synclines as shown in the cross section along the section line AB, CD and EF (Fig.5). The basin

has undergone three phases of deformation leading to three generation of folds. The tight to open,

upright and NS (gently) plunging folds of F1 generation are superimposed by tight to open, upright

and EW (gently) plunging folds of F2 generation resulting into type -1 interference pattern or dome

– basin patterns. The D2 phase of deformation gave rise to E-W to WNW – ESE striking minor faults.

D3 deformation has resulted into NS to NNE-SSW trending reverse faults dipping moderate to

steeply towards west. This later set of faults affected the F1 and F2 folds.

The western limb of the Horse-shoe synclinorium is isoclinally folded dipping steeply towards west

and control the depth of the ore bodies in the deposits from the western limb. In the eastern limb,

the major deposits are located in the shallow dipping strata from the hinge part of asymmetric

anticline. The dome and basin structure produced by the superimposition of F2 over F1 controls the

extension of ore bodies. In general, the entire belt is traversed by at least seven faults trending

NNE-SSW running almost parallel to each other. These faults control the shape and depth of the

localized small basins hosting the iron ore deposits.

5.1.3 Ore Types, Resource and Grade

Bonai – Keonjhar belt host the high grade and huge size deposits each having a strike length of

more than 1 km. The belt exhibit the various types of ore bodies ranging from hard – massive, to

Page 23

soft laminated and powdery – blue dust composed chiefly of hematite, magnetite with subordinate

amount of goethite and martite. Soft laminated varieties of iron ore may grade into powdery blue

dust along depth at places. Lateritic ore also can be found in the upper part of the deposit at places.

The grade of ore increases along the depth and may vary from 58% to 65% (Fe). Total indicated

resource of the major deposits from the Bonai – Keonjhar belt estimates to approximately 2300 MT

estimated by Geological Survey of India, Indian Bureau of Mines, Directorate Geology and Mining

(Orissa).

Figure 5: Geological Map of North Orissa – Singhbhum Craton showing Iron Ore Group (Source: Beukes et al., 2003)

5.1.4 Major Deposits: Bonai – Keonjhar Belt

Thakurani Deposit

The deposit is located over the northern most tip of the eastern limb of horse-shoe shaped

synclinorium and covers an area of 19.95 km2. BHQ host the high grade hematitic ore of massive,

laminated and powdery types. BHQ, underlain by tuffs and shale, are capped by lateritic soil. GSI

estimated indicated resource of 395 MT up to a depth of 55 m with an average grade 63%.

Malangtoli Deposit

Malangtoli is a big sector comprising of 19 deposits with a total covering area of approximately 200

km2 located over the southern tip of the horse-shape synclinorium. Schists, shale, tuffs, phyllites,

Page 24

basic rocks, BHQ and BHJ make the lithological assemblage of the deposits with BHQ and BHJ as

host for laminated iron ore with small patches of massive iron ore. GSI estimated indicated resource

of 608 MT with an average grade of 63% from the entire sector.

Bolani Deposit

Bolani deposit is part of NNE-SSW trending ridge extending for about 5 km along the strike length

and lies over the central northern part of the western limb of the horse-shoe synclinorium. Shale,

metavolcanics,BHQ, phyllites and tuffs . BHQ hosts the massive, soft friable, powdery and lateritic

types of ore with Fe content varying from 58% to 65%. Mineralization is controlled by extensively

folded and faulted structural setup of the area.

Hormoto – Guali Deposit

Located near Barbil the deposits cover an area of approximately 137 km2 and bear phyllite, chert,

sandstone, dolomite and BHJ with a regional trend varying from NNE-SSW to NE-SW dipping

gently to moderately towards NW. Deposits exhibit massive iron ore grading into soft lateritic

variety. Total reconnaissance resource estimated by DGM comes to 27.7 MT with an average grade

of 63% (Fe).

Joda and Khondbandh deposits

The deposit, occurring on the NS trending hill, belongs to the eastern limb of the horse-shoe

synclinorium consisting of phyllitic shale, BHJ and shale with basic lava in the upper part. The

deposit bears soft laminated iron ore with an average Fe content of 64%. GSI has estimated 252 MT

of indicated resource up to depth of 100 m.

Jhilling – Langalotta deposit

Jhilling and Langalotta deposit occur over Jhilling and Langalotta hills from the eastern limb of

broad Horse-shoe synclinorium. Sandwitched between the upper and lower shale units, BHJ hosts

the massive iron ore chiefly composed of hematite with small amount of goethite which occur as

alteration product by replacing the hematite. The total indicated resource, with an average grade of

62% Fe, was estimated by GSI comes to 96.7 MT up to a depth of 25 m from the surface.

Page 25

Figure 6: Geological Map of the Horse-shoe shaped synclinorium (Jamda – Koira basin), Western Iron Ore Group. (Source: Ghosh and Mukhopadhyay, 2007)

Page 26

Figure 7: Generalized Geological map of the eastern limb of Horse-Shoe synclinorium (Source: Acharya, S., 2008)

Page 27

Figure 8 : Cross sections (not to scale) from the eastern limb of synclinorium along the lines shown in the previous figure. (Source: Acharya, S., 2008)

Bamebari, Gorubera, Jolohuri and Palsa deposits

This group of iron ore deposits occur in the central part of the asymmetric anticline developed over

the Horse-shoe shaped synclinorium. BHQ / BHJ, locally overlain by sandstone and capped by

lateritic soil, host the soft laminated iron ore composed chiefly of hematite with subordinate

amount of goethite. Total reconnaissance resource estimated by GSI accounts to 29 MT with Fe

content varying from 63% to 66%.

Page 28

Balia Pahar, Kherjurdihi and Badamgarhpahar deposits

This cluster of deposits extending over a strike length of 2.5 km, lie in the SE part of eastern limb of

Horse-shoe synclinorium and to the east of Malangtoli. Ferruginous shale, BHJ and chert makes the

litho assemblage of the deposits and exhibit the iron ores of massive, soft laminated and blue dust

type with small upper part bearing the lateritic iron ore. Hematite occurs as the chief ore mineral

with goethite as alteration product along the fractures. Total indicated resource, estimated by GSI,

comes to 169 MT with Fe content varying from 58% to 62%.

Barsuan, Taldihi and Kalta Deposits

The Barsuan, Taldihi and Kalta deposits lies over the western limb of Horse-shoe synclinorium

comprises NE-SW trending ferruginous shale and BHQ / BHJ units and exhibit the hard massive and

soft laminated iron ore with occurrence of blue dust at places. Total inferred resource estimated by

IBM and DGM accounts to 232 MT with Fe content varying from 58% to 63%.

Jumka – Pathiriposhi Deposits

Jumka Pathiriposhi deposits, lying in the eastern limb of Horse-shoe synclinorium, comprises of

volcanics, tuffs and BHQ / BHJ overlain by upper shale. BHQ / BHJ makes the prominent ridges in

the area and host soft laminated iron ore along with the blue dust at depth. Hematite is the chief

ore mineral along with goethite and limonite along the fractures. Total resource potential estimated

by DGM accounts for 5.0 MT with Fe content varying from 50% to 60%.

5.1.5 Gorumahisani – Badampahar - Sulaipet (GBS) Belt

GBS belt, located in the NE part of the North Orissa – Singhbhum Craton, extends from

Badampahar in the south to Gorumahisani in the north through Sulaipet in an arcuate pattern. The

belt bears the well known deposits of Gorumahisani, Badampahar and Sulaipet.

5.1.6 Gorumahisani – Badampahar – Sulaipet Deposits

Gorumahisani – Badampahar and Sulaipet deposits of GBS belt lies in the Mayurbhanj district of

Orissa and run as three parallel bands over a strike length of 2.3 km, 1.0 km and 1.8 km respectively

with width varying from 100 – 250 m.

Geological Setting

The belt comprises chiefly Banded Magnetite Quartzite along with Banded Hematite Quartzite,

Banded Magnetite Grunerite Quartzite and Banded Chert Quartzite. This assemblage is intruded by

the ultrabasics and dolerite dykes. Though, magnetite is dominant ore mineral in this belt,

hematite, goethite and martite occurs in small quantity.

Mineralization Control

The Iron Ore bearing Banded Iron Formations from the GBS belt were laid in a fault bounded basin

and show a general NE-SW trend in the south while N-NNW trend in the northern part. The GBS

belts exhibit three phases of deformation represented by the three generation of folds: F1, F2 and

Page 29

F3. The tight – isoclinals folds of F1 generation are coaxially folded by F2 generation of folds giving a

general NE-SW trend. F3 generations of folds are locally developed represented by local warps. The

mineralization in the belt is controlled by the pattern of faults and the discontinuous – lenticular

pattern of the iron ore bodies is attributed to the different generation of folds.

Ore Types, Resource and Grade:

The Gorumahisani, Badampahar and Sulaipet deposits, in general, exhibit the hard massive and

laminated varieties of Iron Ore which may grade some time into blue dust at deeper level. Total

indicated resource from these three deposits comes to 61 MT with major contribution from the

Gorumahisani and Badampahar deposits. The Fe content of deposits generally varies from 58% to

66%.

5.2 Tomka – Daitari Belt

Tomka – Daitari Iron Ore Belt (Fig.6) is located in the southern part of the North Orissa –

Singhbhum Craton and covers the part of Jajpur and Keonjhar districts of Orissa. The 50 km long

Tomka – Daitari belt extends from Tomka in the East to Madhyapur in the NW through Ghotang

and Pongaposhi. The Tomka – Daitari belt exhibits the well known deposits of Tomka, Daitari,

Ghutang, Pongaposhi and Madhyapur deposits.

5.2.1 Geology of Belt

Tomka – Daitari belt, once considered as part of Gorumahisani – Badampahar – Sulaipet Belt, is

now kept as separate entity due to its different metamorphic history, mineralogical and structural

style from the former. The belt is dominated by mafic – ultramafic rocks, metapelites, BIF,

quartzites and calcareous sediments. BIF host the high grade hematite iron ore deposits of this belt.

5.2.2 Mineralization Control

The BIF units from E-W trending Tomka – Daitari Belt form a tightly folded syncline with its

southern limb overturned. This synclinal structure is traversed by N-S, NNE-SSW and NW-SE

trending faults. It is believed that these deposits have formed by the ore material supplied along

these faults from depth as enrichment of Iron Ore occurs within the areas bounded by these faults.

The occurrence of iron ore deposits in the form of isolated pockets is attributed both to tight folding

and faulting (Fig.6).

5.2.3 Ore Types, Resource and Grade

The iron ore from Daitari deposit exhibit the high grade hematite ore of laminated and blue dust

variety with Fe content varying from 60% to 63%. On contrary, Tomka, Ghutang, Pongaposhi and

Madhyapur deposit are chiefly composed of magnetite with subordinate amount of goethite and

martite and ranges in grade from 55% to 58% Fe. Total indicated resource for Tomka deposit was

estimated to 40 MT by IBM and DGM while GSI and IBM has estimated 10 MT of total indicated

resource for Daitari deposit. Ghutang, Pongaposhi and Madhyapur deposits collectively were

estimated to 0.048 Mt as total resource potential by independent bodies.

Page 30

5.3 Gandhmardhan Belt

The Gandhmardhan deposit from the Gandhmardhan belt is located to the SE of broad

synclinorium from Jamda – Koira valley. Gandhmardhan deposit with an aerial extent of 3 km2,

occur as isolated unit, it is interpreted as continuation of asymmetric anticline hinge from the

Jamda – Koira valley. BHQ, BHJ, phyllite and shale with intercalation of lava flows and dolerite

made the litho-assemblage. The deposits bear massive, laminated and powdery iron ores with

grades generally above 63%.

Figure 9: Generalised geological map of the Tomka – Daitari belt from Southern Iron Ore Group (Tomka – Daitari basin) showing spread of BIF with fault bounded Iron Ore deposits. (Source: Acharya, S. 2008)

5.4 Hirapur Belt

Hirapur Iron Ore Belt, which is located in Nawrangpur district of the Orissa, belongs to the

stratigraphic units within the Western Orissa Craton and equivalent to the Bailadila group. The

litho- assemblage of this belt comprises of BHQ, ferruginous schist, shale and is capped by lateritic

cover. Hirapur and Umrakot iron ore deposits from this belt show hard massive and laminated

varieties of iron ore with Fe content ranging from 50% to 62%.

5.5 Iron Ore Potential: Orissa

Iron Ore in India occur in different geological settings belonging to different groups and formations

but the major deposits are confined to Precambrian banded iron formations of greenstone belts. In

Page 31

India, hematite and magnetite are the prominent Iron Ores of which high grade Hematite Ore

occurring as massive, laminated, friable and in powdery form are the major source. Major Iron Ore

of deposits of India are demarcated geographically into five zones from I to V. Deposits of Orissa

and adjoining areas belong to Zone – I which contribute to 60% of high grade Hematite Iron Ore (>

60 wt% Fe) of India. Orissa bear the largest resource of Iron Ore followed by Jharkhand. Iron Ore

Group, bearing dominantly Banded Iron Formations, hosts the rich and major deposits of

Mayurbhanj, Sundargarh, Keonjhar and of Jajpur districts of Orissa. As per the information available

from Director of Geology, Orissa, IOG bears 5306 Million Tonnes (MT) of Iron Ore Resource out of

which 3000 MT belongs to Leasehold areas while 2306 MT belongs to Freehold areas. The detail of

district wise distribution of Iron Ore Resources is as follow, as per the data updated till 2007:

Sr.

No.

District Leasehold Resource

(MT)

Freehold Resource

(MT)

Total Resource

(MT)

1 Keonjhar 2316 1258 3574

2 Sundergarh 574 1031 1605

3 Mayurbhanj 28 07 35

4 Jajpur 82 0 82

5 Jaipur 0 10 10

Total 3000 2306 5306

Table 2: Iron ore resources of Orissa

Source: Director of Geology, Orissa and Director of Mines, Orissa. (Year: 2007)

5.6 Summary

Iron Ore occurs in different groups and formations of different geological settings but the India’s

richest and biggest deposits are mostly confined to Banded Iron Formations (BIF) of Precambrian

age. Major Iron Ore deposits of India are distributed into five distinct geographic zones from Zone –

I to Zone - V. Major high grade Iron Ore deposits from Eastern India are located in the North Orissa

and part of Jharkhand corresponding to Zone – I. The Archaean Singhbhum Craton comprises the

well known Iron Ore Group (IOG) deposited in the three isolated basins namely: Gorumahisani –

Badampahar basin, Tomka – Daitari basin and Jamda – Koira basin. All three basins are made up of

volcano-sedimentary sequence and comprises of Banded Iron Formations that host the iron ore.

The Iron Ore Group covers the Mayurbhanj, Keonjhar, Sundergarh and Jajpur districts of Orissa and

is exhibit the major and high grade deposits of Eastern India.

The Iron Ore deposits from Orissa are divided into five geographic belts: 1. Bonai – Keonjhar belt, 2.

Gorumahisani – Badampahar –Sulaipet belt, 3. Tomka – Daitari belt, 4. Gandhamardhan belt and 5.

Hirapur belt. The Iron Ore from these deposits are of various types as hard massive, soft laminated

and powdery blue dust though lateritic ore occur at places in the upper profile. Gradational or sharp

Page 32

transition may occur from one type of ore to other type both vertically and laterally. Hematite and

magnetite are the chief ore minerals while goethite and martite also occur as alteration product

along the fractures and other weak planes. Hard massive varities are mostly composed of hematite

along with subordinate amount of goethite and martite. Powdery blue dust is chiefly composed of

hematite. The high grade deposits from the different belts are structurally controlled. The region

show three phases of deformation and display the different generation of folds and faults. The

superimposition of the folds from different generation creates the repository for the ore material

while transecting faults creates the path for the ore material to get mobilised. Tight isoclinal folds

and different sets of faults thus control the size, shape and subsurface extent of the ore bodies.

Table 3: Major iron ore resource bearing districts

Source: Directorate of Geology, Government of Orissa

Mayurbhanj, Keonjhar, Sundargarh and Jajpur districts from Orissa bear the major high grade

(+60% Fe) hematitic deposits from these belts and contribute to the 60% of total Indian iron ore. As

per the information available from Director of Geology and Director of Mines, Orissa, the state has

5306 MT of iron ore deposits of which 3000 MT belong to leasehold areas and the rest 2306 MT

belongs to freehold areas thus making it worth to explore and workout for iron ore in the state.

3574

1605

82 35 10 0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Keonjhar Sundergarh Jajpur-Koenjhar Mayurbanj Jajpur

Iron ore resource (Mt)

Page 33

6. Orissa Iron ore mining

Orissa, a major producer and exporter of Iron ore occupies an important position on the mineral

map of India. It is endowed with high grade haematite, and other essential minerals for the steel

making like coal, dolomite, limestone and manganese. Because of the abundant mineral resource

base, its strategic proximity to major iron ore consumers in the world market, Orissa offers an

excellent investment opportunity for mining companies and iron and steel manufacturers. As per

the recent estimate of Directorate of Geology, Government of Orissa, the total iron ore resources in

the state is around 5306 Mt which is predominantly in the form of haematite and concentrated in

the 5 districts of the state, Keonjhar being the leading district with a resource base of around 3574

Mt. However, the official estimated figure provided by GSI is 4760.67 Mt (as on 1:4:2005, detailed

information dossier, 2010). GSI has estimated iron ore reserve on the basis of Fe cut off grade of

55%. Because of recent development of lean ore beneficiation technology, iron ore of Fe 45% -50%

can also be upgraded and utilized for steel making process, Government of India has reduced the

cut off grade for iron ore to Fe 45%. However, the additional Iron ore resources have not been

officially included in the total iron ore reserve base.

Except for a few industry majors, iron ore mining in the state is dominated mainly by small and

marginal players with a leasehold area of as low as 1.2 hectares. These small players generally cater

the need of domestic industry and export surplus iron ore to China mainly via Paradip port.

As per the report of the Forest Survey of India, the forest cover in the state is 48,855 sq. km of which

7,073 sq. km is very dense forest. The moderately dense forest extends over 21,394 sq. km while

open forest is over 20,388 sq. km. The forest cover in the state constitutes 31.38% of the

geographical area. Besides this, there exists tree cover outside the forest over 2.85% of the

geographical area of the State. Thus the forest and tree cover in the State is 34.23% of the

geographical area. While some mining activities are confined to non-forest areas, substantial

portion of the remaining mining zones come under degraded and open forest areas.

Because of afforestation taken up by the mines and their concern as organized sector for forest

conservation, in and around of these mining areas forest cover exists today which has been

confirmed even by satellite imagery of mining belts of Koraput, Keonjhar Sundergarh & Angul.

Deforestation and degraded forest areas are much more in the districts or parts of the state, where

there are no mining activities. While about 10% of the forest area has been lost in the last 50 years,

only 0.09% forest area comes under mining lease and 0.01 % under active mining operation.

(Source: Ministry of environment and forest, Government of Orissa)

Page 34

Working mining lease hold areas

(Ha)

Non Working mining lease hold areas (Ha)

Districts Forest Area Non Forest

Area

Forest Area Non Forest Area

Jajpur 190.2 0.0 0.0 0.0

Keonjhar 21,924.5 89,167.3 2,756 1,542.9

Sundergarh 34,033.2 98,767.1 686.4 12.9

Total 56,147.9 187,934.4 3,442.4 1,555.8

Table 4: Working and non working mining areas, forest land*

* As on April 2010 Source: Department of Steel and Mines, Government of Orissa

6.1 Mining policy

Till date, the state of Orissa does not have any separate mining policy. However, the Government of

Orissa is under the process of finalizing the same and the draft Orissa Mining Policy will be

announced very soon. As per a recent press release, the new mining policy will focus more on non-

ferrous sector rather than on ferrous minerals. It will be emphasized on development of low volume,

high value non-ferrous minerals like gold, nickel, platinum, beach sand as the state has a reserve of

174 million tonnes of Nickel ore and 82 million tonnes of beach sand. The preliminary mineral

investigation has also indicated occurrences of gold and diamond bearing minerals in the western

part of Orissa. In the ferrous sector, more emphasis will be given on promotion of beneficiation,

pelletization, sintering, and calibration of minerals so that low grade ore can be utilized. The policy

will promote state-of-the-art technology and good management practices in mining of minerals in

the state with a view of protecting human and natural resources.( source: press release,

Government of Orissa). This is being done primarily to increase employment opportunities in the

state.

The existing mineral based industries have been covered under Orissa Industrial Policy 2007.

The salient features of Orissa Industrial Policy pertaining to Mineral based industries have been

elucidated below:

Promotion of development of infrastructure via Public Private Partnership (PPP) mode

to support sustainable investment in the field of mining and mineral processing.

Planning and Coordination Department has been designated as the nodal department

and the Orissa Industrial Infrastructure Development Corporation (IDCO) as the

technical secretariat for promoting PPP Projects. In context of the above, three (3) new

ports are being promoted, Dhamra and Kirtania in the north and Gopalpur in the south

on PPP mode. Similarly, Gopalpur port is being developed in Southern Orissa, which is

expected to have a cargo handling capacity of over 40 mtpa in the long run. Gopalpur

would serve the industrial corridor of Southern Orissa, especially for the mining and

Page 35

mineral processing zone covering Kalahandi, Rayagada and Koraput District and

special economic Zone at Gopalpur itself.

Maximum emphasis will be given on process and industries which have sound

management practice. To achieve this objective the State Government among other

things is actively promoting investments in new cement plants based on blast furnace slag and fly ash, which would be available in abundance due to the large number of steel and power plants coming up in the state.

Strengthening of regulatory and institutional arrangement for implementation of

environment laws, formulation of Rehabilitation & Resettlement Policy by adopting a holistic livelihood approach for rehabilitation and resettlement of project affected families.

Strengthening of arrangement for industrial promotion and investment facilitation at

various levels including District Industries Center (DIC) as District Level Nodal Agency, Corporation of Orissa Limited (IPICOL) as the State Level Nodal Agency (SLNA) Team

Orissa as the Common Focal Point for extending single window and A high level clearing authority chaired by Chief minister.

Creation of SEZs and more thrust on human resource development and employment

6.2 Industry Structure and major producers of Iron ore

Iron ore mining players in Orissa can be categorized into two main types;

Industrial houses like Tata , Essel mining ,SAIL, OMC ,OMDC catering to domestic as well as export market

Small players mainly catering to smaller firms and export market