Options on stock indices, currencies, and futures.

52

Options on stock indices, currencies, and futures

-

Upload

destiney-boals -

Category

Documents

-

view

243 -

download

2

Transcript of Options on stock indices, currencies, and futures.

Options on stock indices, currencies, and futures

Options On Stock Indices

Contracts are on 100 times index; they are settled in cash

On exercise of the option ,the holder of a call option receives (S-K)*100 in cash and the writer of the option pays this amount in cash ;the holder of a put option receives

(K-S)*100 in cash and the writer of the option pays this amount in cash

S :the value of the index

K :the strike price

The most popular underlying indices in the U.S.

The Dow Jones Index (DJX) The Nasdaq 100 Index (NDX) The Russell 2000 Index (RUT) The S&P 100 Index (OEX) The S&P 500 Index (SPX)

LEAPS

Leaps are options on stock indices that last up to 3 years

They have December expiration dates Leaps also trade on some individual stocks ,they have

January expiration dates

Portfolio Insurance

Consider a manager in charge of a well-diversified portfolio whose is 1.0

The dividend yield from the portfolio is the same as the dividend yield from the index

The percentage changes in the value of the portfolio can be expected to be approximately the same as the percentage changes in the value of the index

Portfolio InsuranceExample Portfolio has a of 1.0 It is currently worth $500,000 The index currently stands at 1000 What trade is necessary to provide insurance against

the portfolio value falling below $450,000?

Portfolio InsuranceExample Buy 5 three-month put option contracts on the index

with a strike price of $900 The index drops to 880 in three months the portfolio is worth about

5*880*100 = $440,000 the payoff from the options

5*(900-880)*100 = $10,000 total value of the portfolio

440,000+10,000 = $450,000

When the portfolio beta is not 1.0Example Portfolio has a beta of 2.0 It is currently worth $500,000 and index stands at

1000 The risk-free rate is 12% per annum The dividend yield on both the portfolio and the index

is 4% How many put option contracts should be purchased

for portfolio insurance?

When the portfolio beta is not 1.0Example Value of index in three months 1040 Return from change in index 40/1000=4% Dividends from index 0.25*4=1% Total return from index 4+1=5% Risk-free interest rate 0.25*12=3% Excess return from index 5-3=2% Expected excess return from portfolio 2*2=4% Expected return from portfolio 3+4=7% Dividends from portfolio 0.25*4=1% Expected increase in value of portfolio 7-1=6% Expected value of portfolio $ 500,000*1.06= $530,000

Relationship between value of index and value of portfolio for beta = 2.0

Value of Index in 3 months

Expected Portfolio Value in 3 months ($)

1,080 570,000 1,040 530,000 1,000 490,000 960 450,000 920 410,000 880 370,000

The correct strike price for the 10 put option contracts that are purchased is 960

Currency Options

Currency options trade on the Philadelphia Exchange (PHLX)

There also exists an active over-the-counter (OTC) market

Currency options are used by corporations to buy insurance when they have an FX exposure

Currency options Example An example of a European call option

Buy $1,000,000 euros with USD at an exchange rate of 1.2000 USD per euro ,if the exchange rate at the maturity of the option is 1.2500 ,the payoff is

1,000,000*(1.2500-1.2000) = $50,000

Currency options Example

An example of a European put option

Sell $10,000,000 Australian for USD at an exchange rate of 0.7000 USD per Australian ,if the exchange rate at the maturity of the option is 0.6700 ,the payoff is

10,000,000*(0.7000-0.6700) = $300,000

Range forwardsShort range-forward contract Buy a European put option with a strike price of K1 and

sell a European call option with a strike price of K2

Range forwardsLong range-forward contract Sell a European put option with a strike price of K1 and

buy a European call option with a strike price of K2

Options On Stocks Paying Known Dividend Yields Dividends cause stock prices to reduce on the ex-dividend date b

y the amount of the dividend payment The payment of a dividend yield at rate q therefore cause the gro

wth rate in the stock price to be less than it would otherwise be by an amount q

With a dividend yield of q ,the stock price grow from S0 today to ST

Without dividends it would grow from S0 today to

STeqT

Alternatively ,without dividends it would grow from S0e–qT today to

ST

European Options on StocksProviding a Dividend Yield We get the same probability distribution for the stock

price at time T in each of the following cases:1. The stock starts at price S0 and provides a dividend yield at

rate q

2. The stock starts at price S0e–qT and pays no dividends

We can value European options by reducing the stock price to S0e–qT and then behaving as though there is no dividend

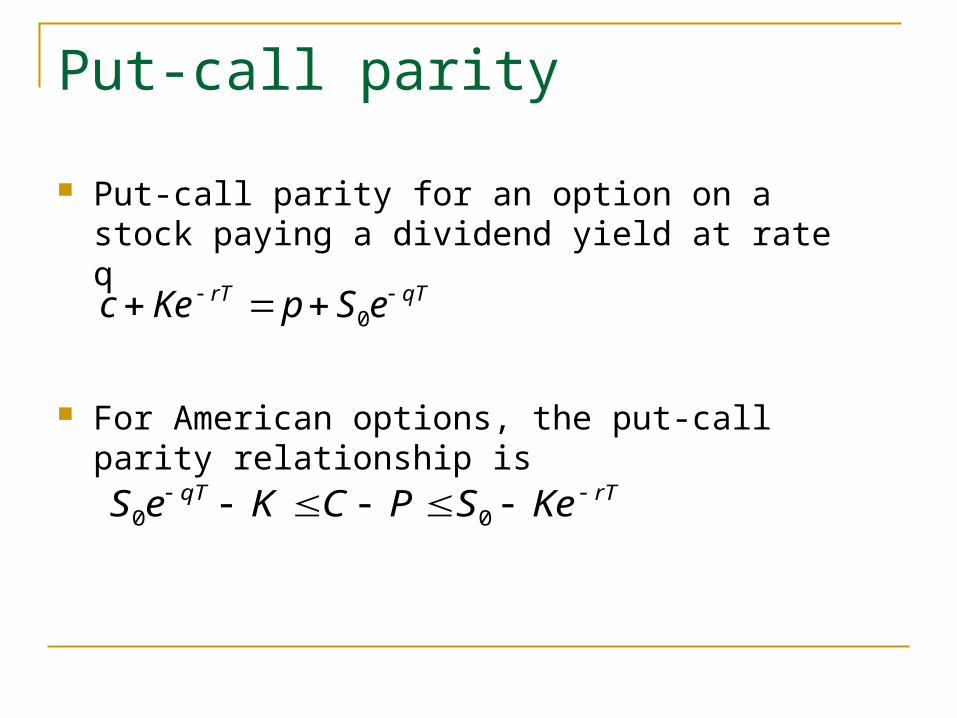

Put-call parity

Put-call parity for an option on a stock paying a dividend yield at rate q

For American options, the put-call parity relationship is

qTrT eSpKec 0

rTqT KeSPCKeS 00

Pricing Formulas

By replacing S0 by S0e–qT in Black-Sholes formulas ,we obtain that

T

TqrKSd

T

TqrKSd

qTK

S

K

eS

dNeSdNKep

dNKedNeSc

qT

qTrT

rTqT

)2/2()/ln(

)2/2()/ln( where

ln ln since

)()(

)()(

02

01

00

102

210

Risk-neutral valuation

In a risk-neutral world ,the total return must be r ,the dividends provide a return of q ,the expected growth rate in the stock price must be r – q

The risk-neutral process for the stock price

SdzSdtqrdS

Risk-neutral valuation continued

The expected growth rate in the stock price is

r –q ,the expected stock price at time T is S0e(r-q)T

Expected payoff for a call option in a risk-neutral world as

Where d1 and d2 are defined as above Discounting at rate r for the T

)()( 210)( dKNdNSe Tqr

)()( 210 dNKedNeSc rTqT

Valuation of European Stock Index Options We can use the formula for an option on a stock

paying a dividend yield

S0 : the value of index

q : average dividend yield

: the volatility of the index

)()(

)()(

102

210

dNeSdNKep

dNKedNeScqTrT

rTqT

Example

A European call option on the S&P 500 that is two months from maturity

S0 = 930, K = 900, r = 0.08

= 0.2, T = 2/12

Dividend yields of 0.2% and 0.3% are expected in the first month and the second month

Example continued

The total dividend yield per annum is q = (0.2% + 0.3%)*6 = 3%

one contract would cost $5,183

83.516782.09007069.0930

6782.0)(

7069.0)(

4628.012/22.0

12/2)2/22.003.008.0()900/930ln(

5444.012/22.0

12/2)2/22.003.008.0()900/930ln(

12/208.012/203.0

2

1

2

1

eec

dN

dN

d

d

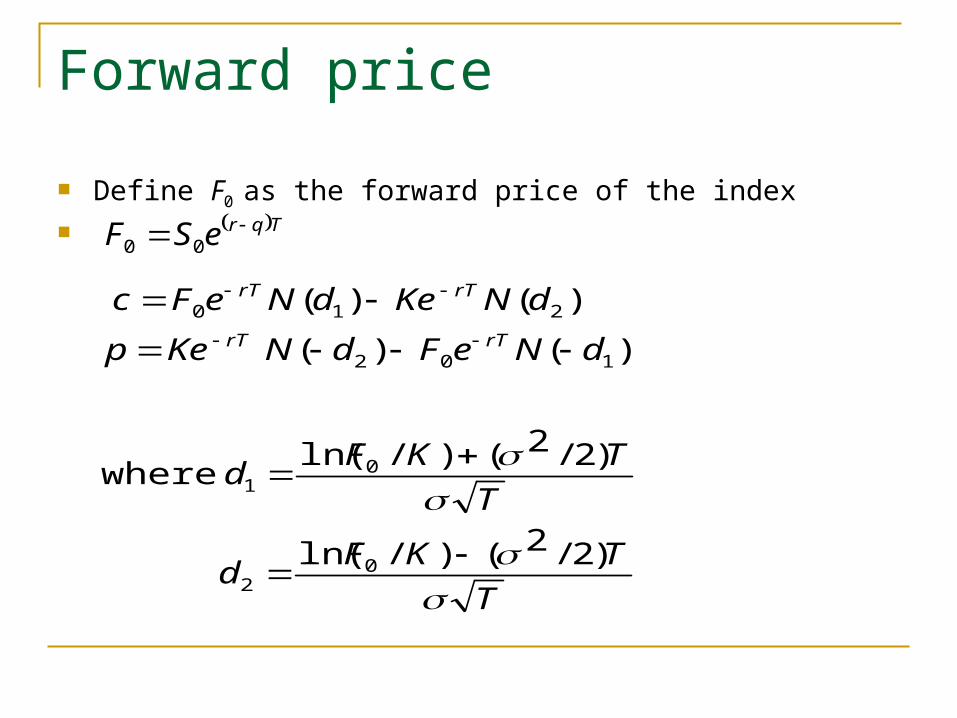

Forward price

Define F0 as the forward price of the index 00

TqreSF

T

TKFd

T

TKFd

dNeFdNKep

dNKedNeFcrTrT

rTrT

)2/2()/ln(

)2/2()/ln( where

)()(

)()(

02

01

102

210

Implied dividend yields

By qTrT eSpKec 0

0

0

0

0

ln1

ln

S

Kepc

Tq

S

KepcqT

S

Kepce

KepceS

rT

rT

rTqT

rTqT

Valuation of European Currency Options

A foreign currency is analogous to a stock paying a known dividend yield

The owner of foreign receives a yield equal to the risk-free interest rate, rf

With q replaced by rf , we can get call price, c, and put price, p

T

TrrKSd

T

TrrKSd

dNeSdNKep

dNKedNeSc

f

f

TrrT

rTTr

f

f

)2/2()/ln(

)2/2()/ln( where

)()(

)()(

02

01

102

210

Using forward exchange rates Define F0 as the forward foreign exchange rate

T

TKFd

T

TKFd

dNFdKNep

dKNdNFecrT

rT

)2/2()/ln(

)2/2()/ln( where

)()(

)()(

02

01

102

210

00

Trr feSF

American Options

The parameter determining the size of up movements, u, the parameter determining the size of down movements, d

The probability of an up movement is

In the case of options on an index

In the case of options on a currency

tqrea

trr fea

du

dap

30

Nature of Futures Options

A call futures is the right to enter into a long futures

contracts at a certain price.

A put futures is the right to enter into a short futures

contracts at a certain price.

Most are American; Be exercised any time during the

life .

31

Nature of Futures Options

When a call futures option is exercised the holder acquires :

If the futures position is closed out immediately:

Payoff from call = F0 – K

where F0 is futures price at time of exercise

1. A long position in the futures

2. A cash amount equal to the excess of

the futures price over the strike price

32

Example

Today is 8/15, One September futures call option on copper,K=240(cents/pound), One contract is on 25,000 pounds of copper.

Futures price for delivery in Sep is currently 251cents 8/14 (the last settlement) futures price is 250

IF option exercised, investor receive cash:

25,000X(250-240)cents=$2,500

Plus a long futures, if it closed out immediately:

25,000X(251-250)cents=$250

If the futures position is closed out immediately

25,000X (251-240)cents=$2,750

33

Nature of Futures Options When a put futures option is exercised the holder acquires :

If the futures position is closed out immediately:

Payoff from put =K–F0

where F0 is futures price at time of exercise

1. A short position in the futures

2. A cash amount equal to the excess of

the strike price over the futures price

34

Reasons for the popularity on futures option

Liquid and easier to trade

From futures exchange, price is known immediately.

Normally settled in cash

Futures and futures options are traded in the same exchange.

Lower cost than spot options

35

European spot and futures options

Payoff from call option with strike price K on spot price of an asset:

Payoff from call option with strike price K on futures price of an asset:

When futures contracts matures at the same time as the option:

)0,Smax( T K

)0,Fmax( T K

TSTF

36

Put-Call Parity for futures options Consider the following two portfolios:

A. European call plus Ke-rT of cash

B. European put plus long futures plus cash equal to F0e-rT

They must be worth the same at time T so that

c+Ke-rT=p+F0 e-rT

37

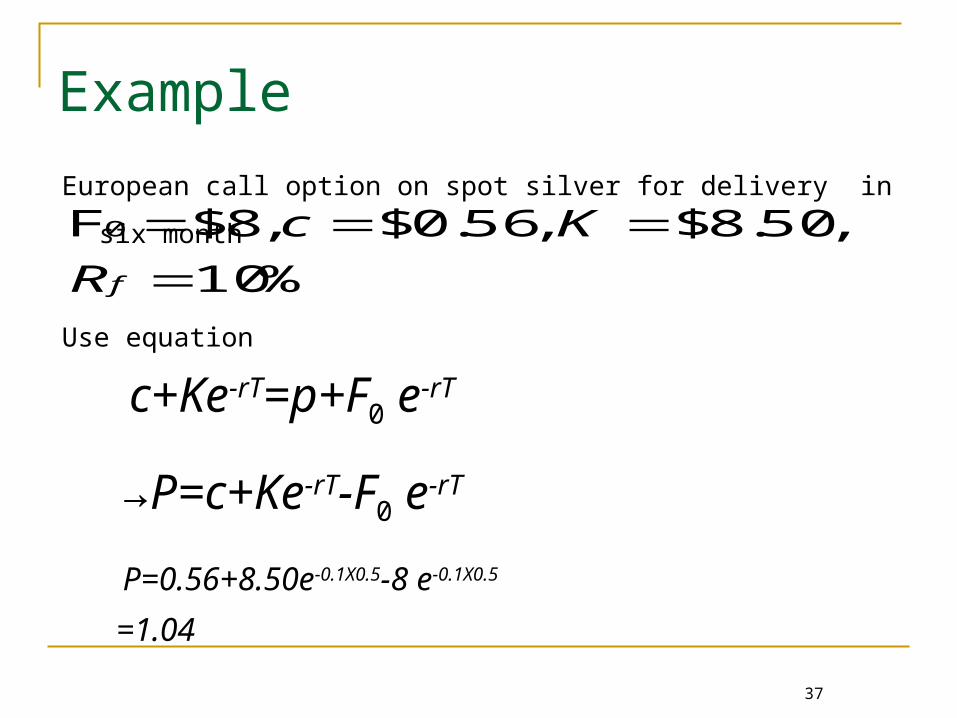

Example

%10

,50.8$,56.0$,8$F0

fR

KcEuropean call option on spot silver for delivery in six month

c+Ke-rT=p+F0 e-rT

Use equation

→P=c+Ke-rT-F0 e-rT

P=0.56+8.50e-0.1X0.5-8 e-0.1X0.5

=1.04

38

Bounds for futures options

rTrT eKec 0F

PeKe rTrT 0F

rTeKc )F( 0

rTeKP )F( 0

c+Ke-rT=p+F0 e-rT

Similarly

or

or

By

39

Bounds for futures options

Kc 0F

0FKP

Because American futures can be exercised at any time,

we must have

40

Valuation by Binomial trees

A 1-month call option on futures has a strike price of 29.

Futures Price = $33Option Price = $4

Futures Price = $28Option Price = $0

Futures price = $30Option Price=?

41

Valuation by Binomial trees

• Consider the Portfolio: long futuresshort 1 call option

• Portfolio is riskless when 3– 4 = -2 or = 0.8

3– 4

-2

42

Valuation by Binomial trees

• The riskless portfolio is:

long 0.8 futures

short 1 call option• The value of the portfolio in 1 month

is -1.6• The value of the portfolio today is

-1.6e – 0.06/12 = -1.592

43

A Generalization

• A derivative lasts for time T and

is dependent on a futures price

F0u ƒu

F0d ƒd

F0

ƒ

44

A Generalization

dFuF

ff du

00

F0u F0 – ƒu

F0d F0– ƒd

• Consider the portfolio that is long Δ futures and short 1 derivative

• The portfolio is riskless when

45

A Generalization

• Value of the portfolio at time T is F0u Δ –F0 Δ – ƒu

• Value of portfolio today is – ƒ

• Hence ƒ = – [F0u Δ –F0 Δ – ƒu]e-rT

46

A Generalization

• Substituting for Δ we obtain

ƒ = [ p ƒu + (1 – p )ƒd ]e–rT

where

pd

u d

1

47

Drift of a futures price in a risk-neutral word

Valuing European Futures Options We can use the formula for an option on a stock

paying a dividend yield

Set S0 = current futures price (F0)

Set q = domestic risk-free rate (r ) Setting q = r ensures that the expected growth of F

in a risk-neutral world is zero

48

Growth Rates For Futures Prices

• A futures contract requires no initial investment• In a risk-neutral world the expected return

should be zero• The expected growth rate of the futures price is

therefore zero• The futures price can therefore be treated like a

stock paying a dividend yield of r

49

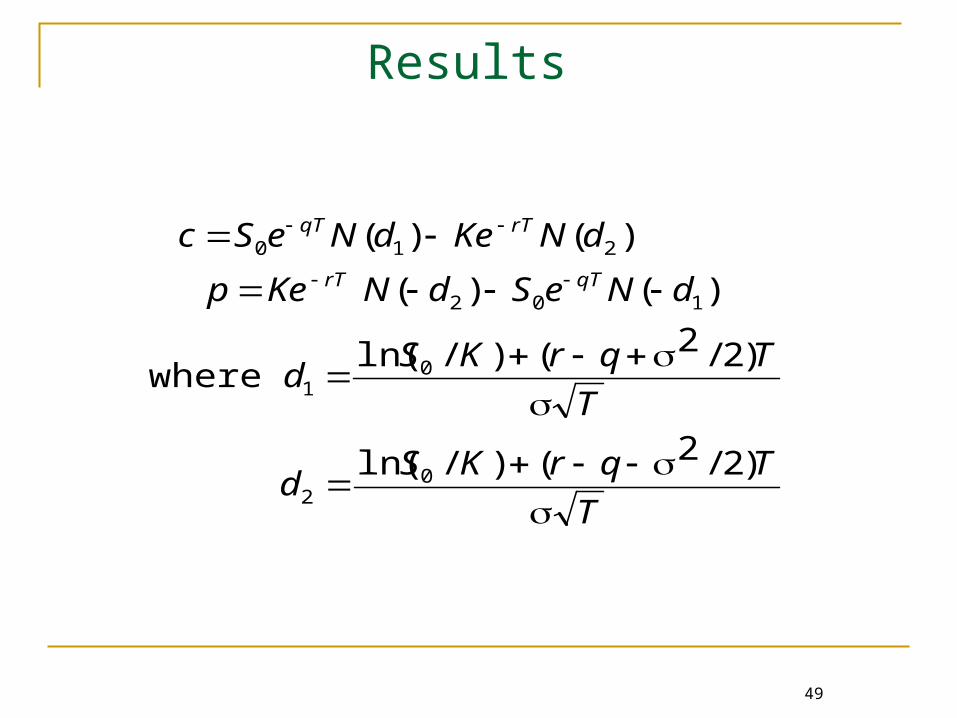

Results

T

TqrKSd

T

TqrKSd

dNeSdNKep

dNKedNeScqTrT

rTqT

)2/2()/ln(

)2/2()/ln(

)()(

)()(

02

01

102

210

where

50

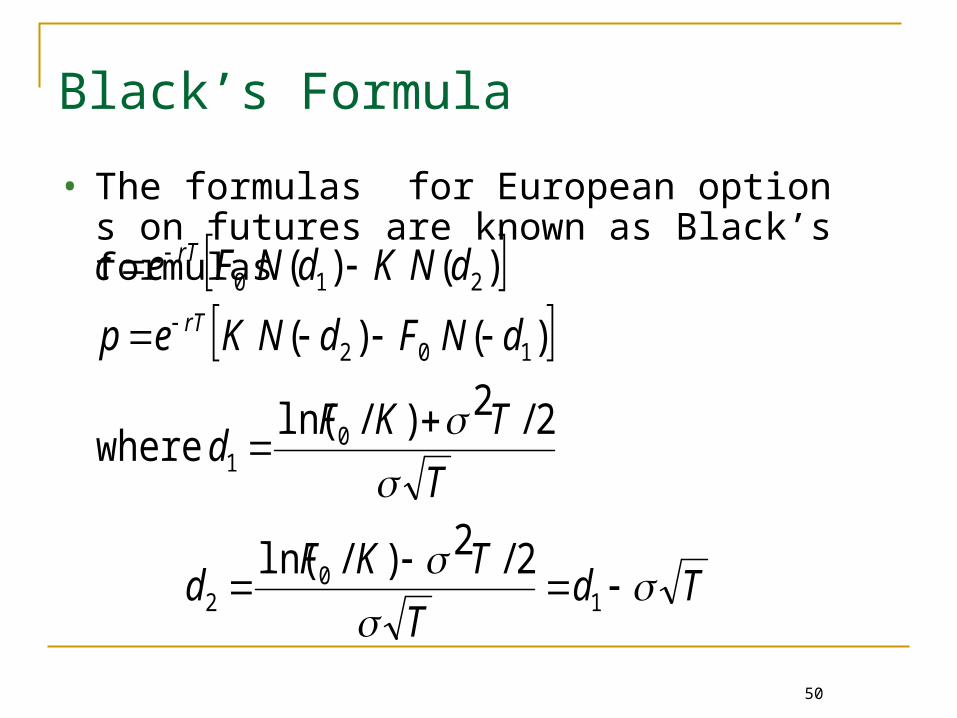

Black’s Formula

• The formulas for European options on futures are known as Black’s formulas

TdT

TKFd

T

TKFd

dNFdNKep

dNKdNFecrT

rT

10

2

01

102

210

2/2)/ln(

2/2)/ln( where

)( )(

)( )(

51

Example

European put futures option on crude oil,…Fo=20,K=20, r=0.09,T=4/12,σ=0.25,ln(F0=K)=0,So that

12.1$4712.0205288.020

5288.0)(

4712.0)(

07216.02

07216.02

12/409.0

2

1

2

1

Xep

dN

dN

Td

Td

52

American futures options vs spot options

• If futures prices are higher than spot prices (normal market), an American call on futures is worth more than a similar American call on spot. An American put on futures is worth less than a similar American put on spot

• When futures prices are lower than spot prices (inverted market) the reverse is true