Optimal Preorder Strategy with Endogenous Information Controlleonyzhu/Optimal Preorder Strategy...

23

MANAGEMENT SCIENCE Vol. 57, No. 6, June 2011, pp. 1055–1077 issn 0025-1909 eissn 1526-5501 11 5706 1055 doi 10.1287/mnsc.1110.1335 © 2011 INFORMS Optimal Preorder Strategy with Endogenous Information Control Leon Yang Chu, Hao Zhang Marshall School of Business, University of Southern California, Los Angeles, California 90089 {[email protected], [email protected]} I n this paper, we investigate the integrated information and pricing strategy for a seller who can take customer preorders before the release of a product. The preorder option enables the seller to sell a product at an early stage when consumers are less certain about their valuations. We find that the optimal pricing strategy may be highly dependent on the amount of information available at preorder and that a small change in the latter may cause a dramatic change in the proportion of consumers who preorder under optimal pricing. Furthermore, the seller’s optimal information strategy depends on a key measure, the normalized margin, which is the ratio between the expected profit margin and the standard deviation of consumer valuation. Although the seller may want to release some information or none, she should never release all information. Finally, under the optimal information and pricing strategy, the benefit of preorder is most pronounced when the normalized margin is in a medium range. Key words : preorder; advance selling; information release; consumer valuation control History : Received August 18, 2009; accepted January 23, 2011, by Martin Lariviere, operations management. Published online in Articles in Advance April 21, 2011. 1. Introduction With rapid development in information technologies, preorder has gained popularity in recent years, espe- cially for books, CDs, video games, and software items, and the practice has attracted increasing atten- tion from both practitioners and academics. Although various aspects of the preorder practice have been scrutinized by researchers, one important dimension has been largely neglected thus far. When a new prod- uct is available for preorder, consumers often do not have complete product information or clear personal preferences. A natural question arises as to whether a manufacturer (or seller) should release information to help consumers make better preorder decisions. Information plays a crucial role in shaping con- sumers’ valuation of the product, which can be rep- resented by a distribution parameterized by its mean and variance. The mean valuation of a product is driven by the product’s characteristics or features that are universally valued—e.g., the memory space of a cellular phone, the battery life of an electronic reader, and the safety ratings of an automobile. Information control over such characteristics is straightforward, as suggested by the large literature on voluntary infor- mation provision (e.g., Grossman 1981, Milgrom 1981, Okuno-Fujiwara et al. 1990). Intuitively, if the prod- uct excels on those characteristics, the seller would disclose such information without reservation; oth- erwise, a rational consumer would assume that the product is mediocre on those aspects. In the equi- librium, consumers can form a rational expectation (Muth 1961) of the product value. In other words, the mean of the consumer valuation is dictated by the design of the product, and the seller cannot sys- tematically inflate consumers’ expectation through an information strategy. 1 In contrast, the variance (or dispersion) of the con- sumer valuation is largely caused by product charac- teristics that split the consumer population—e.g., the taste of a yogurt product, the efficacy of a medicine, the screen finish (glossy versus matte) of a note- book computer, and the user interface of a smart- phone. Such characteristics are assessed according to consumers’ idiosyncratic needs and preferences. If better informed, consumers can form more accu- rate personal valuations of the product, resulting in a larger valuation dispersion from the seller’s point of view. If the information is instead concealed, the dispersion would be smaller. Thus, the seller can control the dispersion of consumer valuation by limiting the amount of taste-related information in advertisements, demonstrations, announcements, etc., or by restricting the extent of customer tryouts. In this 1 As discussed in Guo (2009), disclosure costs, information acquisi- tion costs, and other factors may lead to partial disclosure of quality information. Information-related costs are beyond the scope of this paper. We thank an anonymous referee for this point. 1055 INFORMS holds copyright to this article and distributed this copy as a courtesy to the author(s). Additional information, including rights and permission policies, is available at http://journals.informs.org/.

Transcript of Optimal Preorder Strategy with Endogenous Information Controlleonyzhu/Optimal Preorder Strategy...

MANAGEMENT SCIENCEVol. 57, No. 6, June 2011, pp. 1055–1077issn 0025-1909 �eissn 1526-5501 �11 �5706 �1055 doi 10.1287/mnsc.1110.1335

© 2011 INFORMS

Optimal Preorder Strategy with EndogenousInformation Control

Leon Yang Chu, Hao ZhangMarshall School of Business, University of Southern California, Los Angeles, California 90089

{[email protected], [email protected]}

In this paper, we investigate the integrated information and pricing strategy for a seller who can take customerpreorders before the release of a product. The preorder option enables the seller to sell a product at an early

stage when consumers are less certain about their valuations. We find that the optimal pricing strategy may behighly dependent on the amount of information available at preorder and that a small change in the latter maycause a dramatic change in the proportion of consumers who preorder under optimal pricing. Furthermore,the seller’s optimal information strategy depends on a key measure, the normalized margin, which is the ratiobetween the expected profit margin and the standard deviation of consumer valuation. Although the seller maywant to release some information or none, she should never release all information. Finally, under the optimalinformation and pricing strategy, the benefit of preorder is most pronounced when the normalized margin is ina medium range.

Key words : preorder; advance selling; information release; consumer valuation controlHistory : Received August 18, 2009; accepted January 23, 2011, by Martin Lariviere, operations management.

Published online in Articles in Advance April 21, 2011.

1. IntroductionWith rapid development in information technologies,preorder has gained popularity in recent years, espe-cially for books, CDs, video games, and softwareitems, and the practice has attracted increasing atten-tion from both practitioners and academics. Althoughvarious aspects of the preorder practice have beenscrutinized by researchers, one important dimensionhas been largely neglected thus far. When a new prod-uct is available for preorder, consumers often do nothave complete product information or clear personalpreferences. A natural question arises as to whether amanufacturer (or seller) should release information tohelp consumers make better preorder decisions.

Information plays a crucial role in shaping con-sumers’ valuation of the product, which can be rep-resented by a distribution parameterized by its meanand variance. The mean valuation of a product isdriven by the product’s characteristics or features thatare universally valued—e.g., the memory space of acellular phone, the battery life of an electronic reader,and the safety ratings of an automobile. Informationcontrol over such characteristics is straightforward, assuggested by the large literature on voluntary infor-mation provision (e.g., Grossman 1981, Milgrom 1981,Okuno-Fujiwara et al. 1990). Intuitively, if the prod-uct excels on those characteristics, the seller woulddisclose such information without reservation; oth-erwise, a rational consumer would assume that the

product is mediocre on those aspects. In the equi-librium, consumers can form a rational expectation(Muth 1961) of the product value. In other words,the mean of the consumer valuation is dictated bythe design of the product, and the seller cannot sys-tematically inflate consumers’ expectation through aninformation strategy.1

In contrast, the variance (or dispersion) of the con-sumer valuation is largely caused by product charac-teristics that split the consumer population—e.g., thetaste of a yogurt product, the efficacy of a medicine,the screen finish (glossy versus matte) of a note-book computer, and the user interface of a smart-phone. Such characteristics are assessed accordingto consumers’ idiosyncratic needs and preferences.If better informed, consumers can form more accu-rate personal valuations of the product, resultingin a larger valuation dispersion from the seller’spoint of view. If the information is instead concealed,the dispersion would be smaller. Thus, the sellercan control the dispersion of consumer valuation bylimiting the amount of taste-related information inadvertisements, demonstrations, announcements, etc.,or by restricting the extent of customer tryouts. In this

1 As discussed in Guo (2009), disclosure costs, information acquisi-tion costs, and other factors may lead to partial disclosure of qualityinformation. Information-related costs are beyond the scope of thispaper. We thank an anonymous referee for this point.

1055

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information Control1056 Management Science 57(6), pp. 1055–1077, © 2011 INFORMS

Table 1 Preorder Information-Release Methods and Discounts for Top Video Games in 2010

Game Information release

Online Beta PreorderName Platform mode Trailer Demo (online) discount ($)

Star Trek Online Windows Yes Yes Yes 0BioShock 2 Xbox 360/PS3/Windows Yes Yes 15Heavy Rain PS3 Yes Yes 5Final Fantasy XIII Xbox 360/PS3 Yes Yes 10God of War III PS3 Yes Yes 10Crackdown 2 Xbox 360 Yes Yes Yes 10Starcraft II OS X/Windows Yes Yes Yes 0Halo Reach Xbox 360 Yes Yes 20

paper, we focus on the control of consumer valua-tion dispersion at the preorder stage to maximize theseller’s total profit.

To maximize profit, the seller should integrateinformation control with strategic pricing. As anexample, Table 1 lists the top video games in 2010with their information-release methods and preorderdiscounts, ordered by their release dates.2 Game pub-lishers release game information through three com-mon forms: (1) trailers, (2) playable demos, and (3)open beta versions (for online network play if thegame has an online mode). Similar to the releaseof movies, trailers are provided for all video gamesto impress consumers with visual and sound effects.A playable demo enables consumers to experiencethe user interface and explore a small portion of thecontent. It can be distributed in various ways—e.g.,the God of War III demo was preloaded on the Blu-ray disc of District 9. Finally, for games with a mul-tiplayer online mode, an open beta version offers acomprehensive (sometimes nearly complete) previewof a game and familiarizes consumers with not onlythe user interface but also team dynamics of the game.For the eight games listed in Table 1, the retail priceis $49.99 for Star Trek Online and $59.99 for all others.

An interesting observation from Table 1 is thatthe preorder discount decreases as more informationis released, i.e., as the information-release methodchanges from trailer to demo and to online beta. Pre-order discount is commonly used to stimulate the pre-order demand and compensate consumers for theirpossible losses due to valuation uncertainty. Intu-itively, a small discount would be sufficient if con-sumers are well informed, whereas a large discountmay be needed to attract consumers if the seller with-holds information.

2 The list consists of the top three 2010 games on Xbox 360, PS3,and PC platforms, respectively, according to the video game web-site 1UP.com (the game Star Wars: The Old Republic has beendelayed to 2011, and no preorder information is available). Theinformation-release methods and preorder discounts are obtainedthrough gaming website http://www.gamingbits.com, deal websitehttp://www.dealcatcher.com, etc.

Given numerous options for releasing informationand setting prices, what is the seller’s optimal strat-egy? More information at preorder can help matchconsumers with the product better and improve socialwelfare but may also yield more surplus to the con-sumers, which poses an intriguing trade-off for theseller. In this paper, we investigate the seller’s opti-mal preorder strategy with endogenous informationcontrol. We are particularly interested in the followingquestions: How much information should the sellerrelease at the preorder stage? How do the optimalpreorder and retail prices depend on the amount ofinformation released? And when will preorder bemost beneficial to the seller? Our main findings andcontributions are summarized below.

• We propose a two-period, continuous-valuation,dispersion-control model based on solid microfoun-dations, with applications in advertising and con-sumer experiencing. It substantially extends thetwo-type valuation model predominant in the existingadvance-selling literature and seamlessly integratesthe seller’s information and pricing strategies.

• We find that the seller’s optimal pricing strategymay be highly dependent on the amount of infor-mation available at preorder. A small perturbation ofthe latter may trigger a sudden switch of the formerbetween two competing strategies at preorder: oneaims at the high end of the market and the other aimsfor high market participation.

• The seller’s optimal information strategy at pre-order is determined by the nature of the product andthe consumer population, represented by the ratiobetween the expected profit margin and the standarddeviation of consumer valuation (referred to as the“normalized margin”). When the ratio is large, theseller should withhold information and offer a largepreorder discount to capture a large portion of con-sumers at preorder; when the ratio is small, the sellershould release a great deal of information and offera small preorder discount to attract only high valu-ation consumers; and when the ratio is in between,the optimal strategy also depends on the amount ofinformation consumers initially have. In any case, the

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information ControlManagement Science 57(6), pp. 1055–1077, © 2011 INFORMS 1057

seller should never release all information, in contrastto the extreme information strategy in the literature.

• We further find that the benefit of preorder tothe seller is most pronounced when the normalizedmargin lies in a medium range.

The remainder of this paper is organized as fol-lows. In §2, we review the literature related to pre-order. In §3, we discuss the model, its applications,and microfoundations. We study the seller’s optimalpricing strategy in §4 and optimal information strat-egy in §5. Section 6 provides some extensions of theresults, and §7 concludes.

2. Literature ReviewThough not precisely defined, preorder is commonlyregarded as a special form of advance selling, and thetwo bodies of literature are intertwined. As defined byXie and Shugan (2009), advance selling refers to thegeneral practice that a seller induces buyers to com-mit to purchasing a good before the time of consump-tion, which can take many different forms. In contrast,preorder usually refers to the practice that the sellerallows buyers to purchase a product at a particularprice until a specified time prior to its release. Forexample, Hui et al. (2008) analyze the preorder andsales pattern for DVDs through a consumer behav-ior model with optimal stopping. Because preorder isoften associated with the introduction of new prod-ucts, the study of preorder pricing is related to theliterature on strategic pricing of new products andservices, as in Chaterjee (2009).

Sellers engage in advance selling (or preorder) formany plausible reasons. It may help them updatedemand forecasts and manage inventory, as discussedby Chen (2001), Moe and Fader (2002), Tang et al.(2004), and Li and Zhang (2010). It may also helpthe sellers effectively segment the market, especiallyunder limited capacity. Capacity control is crucial tothe field of revenue management, which has wideapplications in the hospitality industry where latecustomers are often willing to pay higher prices; seeBoyd and Bilegan (2003) and Talluri and van Ryzin(2004) for comprehensive reviews of this literature.Xie and Shugan (2009) demonstrate that if capac-ity is limited and rationing is possible, the optimalprice scheme may entail shutdowns or preorder pre-miums rather than discounts. DeGraba (1995) showsthat a seller may even benefit from purposely restrict-ing its capacity and generating buying frenzies. Liuand Xiao (2008) study a seller’s optimal return pol-icy and inventory rationing policy when inventoryis endogenously determined through a newsvendormodel. Zhao and Stecke (2009) and Li and Zhang(2010) both study the advance selling (preorder) strat-egy of a newsvendor retailer who must procure all

units before the regular selling season starts. Liu andvan Ryzin (2008) and Su and Zhang (2008) show thatcapacity and inventory considerations may enhancethe seller’s credibility in charging a high retail price.In contrast to the above studies, we focus on situa-tions such as the Windows 7 upgrade, a Harry Potterbook release, and a video game release, in which theseller has ample capacity.

If the seller can match the demand through con-tinuous production and is not restricted by capac-ity or inventory, the problem can be framed as asequential screening problem in which consumer val-uation is private information at both the preorder andrelease dates. In this setting, Courty and Li (2000)show that the seller’s optimal pricing policy con-sists of a menu of refund contracts, pairing differ-ent preorder prices with different cancellation fees.Akan et al. (2009) show that a menu of refund con-tracts with various expiration dates is optimal wheneach consumer learns his or her valuation at somerandom time. Xie and Shugan (2001) also note thata well-designed refund option can benefit the seller,and the topic is investigated further by Gallego andSahin (2010). However, optimal refund contracts dif-fer noticeably from the simple transactions prevalentin the preorder practice, in which a single preorderprice and a single retail price are announced at thepreorder date. We restrict our attention to the latterform of price mechanism in this paper.

All of the above papers assume exogenous informa-tion structures and focus on the seller’s pricing deci-sion. In reality, the seller can often influence consumervaluation through information control. Few papersin the literature have studied the seller’s informa-tion strategy. Among the few exceptions, Lewis andSappington (1991, 1994) examine an extension of thestandard screening model such that the seller can alterthe probability that consumers receive perfect privateinformation. They find that the seller will always setthe probability at zero or one, corresponding to zeroor full information release. Johnson and Myatt (2006)find that the seller’s profit is typically a U-shapedfunction of the dispersion of consumer valuation,which again leads to extreme information release.However, these papers only consider the static set-ting in which the seller interacts with consumersonce, unlike the two-period setting when preorderis allowed. Recently, extreme information release hasalso been studied in the operations management lit-erature. For instance, Shulman et al. (2009) investi-gate whether a seller should inform customers of theirmatch with the product before their purchase giventhat they can return or exchange the product later,subject to a restocking fee. In this paper, we adopt atwo-period continuous-valuation model and investi-gate the optimal (possibly intermediate) level of infor-mation release.

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information Control1058 Management Science 57(6), pp. 1055–1077, © 2011 INFORMS

Figure 1 Sequence of Events

Seller decidesinformation-releaseand pricing strategies.

Seller releases productinformation andannounces prices p0 and p

1.

Each buyer formsher initial type �0information and prices.

Each buyer decideswhether to preorderat price p0.

Seller releasesthe product.

Each buyer discoversher final type �1.

Each remaining buyerdecides whether topurchase at price p1.

Preorder stage Retail stage

3. The ModelIn this section, we introduce the model, with anemphasis on the evolution of the consumer valua-tion and the seller’s control over it. We discuss twoapplications of the model, in advertising and con-sumer experiencing, and two microfoundations of themodel.

3.1. Sequence of Events, Consumer ValuationEvolution, and Seller’s Information Control

In the model, a monopolistic seller sells a product toa set of consumers (the seller will be referred to as“she” and a consumer as “he” hereinafter). A con-sumer has a unit demand and an idiosyncratic utilityfrom consumption. The seller’s marginal productioncost is constant, denoted by c > 0. The seller releasesthe product at time (or stage) 1 but can take preordersat time (stage) 0. The preorder price p0 and retailprice p1 are announced in advance and all consumersare informed.3 We assume that the seller can committo the retail price at the preorder stage because shecan earn a higher expected profit in doing so.4

Consumers are risk-neutral and maximize theirexpected utilities. Each consumer learns his utility intwo steps: at time (stage) 0, he learns the initial valu-ation �0; then a random shock � occurs, and he learnshis final valuation �1 = �0 + � at time (stage) 1. Thefinal valuation is the consumer’s true utility from con-suming the product. Without loss of generality, we

3 The model can be easily extended to accommodate the situation inwhich only a subset of consumers is aware of the preorder opportu-nity. The optimality of adopting preorder will continue to hold, andthe discontinuity in the optimal pricing and information-releasestrategies will continue to exist.4 To establish credibility, the seller may (1) announce the preorderdiscount and offer a refund to preorder consumers if the retail priceis later reduced (e.g., Amazon offers a preorder price guarantee),(2) build the reputation for a high spot price (Xie and Shugan 2009),or (3) artificially set capacity and inventory limitations.

assume that � has a zero mean. Thus, a consumer’sinitial valuation �0 can be viewed as an expectationof his true valuation �1, given the available informa-tion at the preorder stage. This dynamic valuationprocess describes a common phenomenon that con-sumers learn their valuations of a product graduallyover time. Both �0 and �1 are consumers’ private infor-mation and will also be referred to as their initial typeand final type, respectively. The distributions of �0 and�1 � �0 (or �) are common knowledge, denoted by F 4�05and G4�1 � �05, respectively. The sequence of events isillustrated in Figure 1.

A consumer’s initial valuation of a product, �0,before he actually owns or even sees the product, canbe influenced by many factors, one of which (per-haps the most important) is how much informationthe consumer has about the product. The seller canplay a crucial role in this by selectively releasingproduct information, through advertisements, exhi-bitions, professional reviews, etc. However, a con-sumer’s intrinsic valuation of a product, representedby his final valuation �1, can hardly be altered by theseller’s information handling. To capture these impor-tant facts, we assume that the distribution of the finalvaluation �1 is exogenously determined but the sellercan alter the distributions of the initial valuation �0and the valuation shock �. For analytical tractabilityand consistency with the tradition of the literature (tobe discussed soon), we focus on the normal-normalsetting described below.

1. The unconditional distribution of a consumer’sintrinsic valuation �1 follows a normal distributionN4�1�25, with � > 0. The variance �2 measures thedispersion of the true consumer valuation (we will use“dispersion,” “variance,” and “heterogeneity” inter-changeably hereinafter). This distribution is deter-mined by the characteristics of the product and theconsumer population and is independent of the infor-mation available at the preorder stage.

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information ControlManagement Science 57(6), pp. 1055–1077, © 2011 INFORMS 1059

2. The seller can control the variances of �0 and �via a variable � ∈ 40115 such that �0 ∼ N4�1��25and � ∼ N401 41 − �5�25. The variable � measuresthe amount of information available at the preorderstage, and we call � the preorder information inten-sity parameter. By changing �, the seller can allocatevaluation uncertainty between �0 and �1 � �0.

Because � < 1, the distribution of �0 is more con-centrated around the mean than that of �1, and con-sumers are more homogeneous at stage 0 than atstage 1.

3.2. Consumer Valuation Control ApplicationsWe discuss two applications of the valuation con-trol model, to search goods and experience goods.In economics, a “search good” refers to a productthe characteristics of which can be evaluated throughinformation acquisition prior to its purchase (Stigler1961)—e.g., the style of a dress and the hardwarespecifications of a computer. In contrast, an “experi-ence good” is dominated by characteristics that canonly be evaluated through consumption (Nelson 1970,1974)—e.g., the taste of a yogurt product, the userexperience of a software product, and the effective-ness of a medicine.

Advertising is a common and effective way forreleasing information on a search good. The sellercan influence the dispersion of consumer valuation atthe preorder stage through advertisements. As mod-eled by Johnson and Myatt (2006), the seller maysend an advertisement signal � to consumers attime 0; conditional on a consumer’s intrinsic valua-tion �1 ∼ N4�1�25, the distribution of � is given byN4�11 �

25. Consumers form their expectation of �1 attime 0 based on the advertisement signal; that is, aconsumer’s initial type �0 is his conditional expecta-tion of �1 given �. Notice that the same advertise-ment can send distinct signals to different consumers,depending on their intrinsic preferences. Standard cal-culation yields �0 = E4�1 � �5 = 4��2 +��25/4�2 +�25,and hence �0 ∼ N4�1�4/4�2 +�255 and �1 � �0 ∼

N4�01 �2�2/4�2 +�255. The variance �2 measures the

noise in the advertisement signal, which can be con-trolled by the seller. At one extreme, a perfectly infor-mative advertisement helps consumers learn theirtrue valuations of the product—i.e., sending a per-fect signal � = �1 to a consumer with intrinsic valua-tion �1; at the other extreme, a totally uninformativeadvertisement sends a completely noisy signal � ∼

N4�11�5 to the same consumer. By defining � =

�2/4�2 +�25, we have �0 ∼ N4�1��25 and �1 � �0 ∼

N4�01 41−�5�25, which is consistent with the valuationcontrol model.

A preorder setting differs from a typical experience-good situation because consumers do not actuallyown the product at the preorder stage. However,

as argued by Klein (1998), the Internet can “vir-tually” transform certain experience characteristicsinto search characteristics and experience goods intosearch goods. Such transformations may be done atthe preorder stage, especially for software productsthat can be easily distributed through the Internet.As in the video game example discussed in the intro-duction, the seller can grant consumers limited accessto the product prior to its launch and enable themto gain partial experience. Dynamic consumer val-uation is central to the experience-good literature,and a key building block in many of the consumerlearning models (e.g., Ackerberg 2003, Crawford andShum 2005, Osborne 2011) is the following: the priorbelief (actual distribution) of the consumer valuationof the product is given by �1 ∼ N4�1�25, a signal� ∼ N4�11 �

25 is generated from the trial of the prod-uct, and consumers update their beliefs subsequently.This is a special hierarchical Bayesian model, and nor-mal distributions are chosen according to the theoryof conjugate distributions (DeGroot 1970). Becausethis model is mathematically identical to the adver-tising model discussed above, the discussion follow-ing that model is also applicable here. The variable� = �2/4�2 +�25, negatively related to �2, measuresthe effectiveness of the experience in revealing theidiosyncratic consumer valuations (or resolving thevaluation uncertainty).

3.3. Consumer Valuation ControlMicrofoundations

In this subsection, we provide two microfounda-tions (mechanisms) for controlling the preorder infor-mation intensity � in the valuation control model(or signal noise �2 in the advertising and con-sumer experiencing models). They justify the pro-posed continuous-valuation model; a simple two-typemodel as commonly seen in the preorder literaturewould be too coarse to fully describe the seller’s infor-mation control capability.

As commonly assumed in the marketing litera-ture, a product can be described by a set of charac-teristics and consumers form their valuations basedon their preferences for these characteristics. As dis-cussed in the introduction, we focus on the disper-sion of consumer valuation and on characteristics thatmay appeal to some consumers but displease others.These characteristics can be either advertised (e.g., theshape, color, keyboard type, and carrier of a cellularphone) or experienced (e.g., subtle features of the userinterface of an operating system or a video game).Thus, the following model can serve as a microfoun-dation for both the advertising and consumer experi-encing models.

Assume that a product has n characteristics andthat a consumer’s true valuation of the product is

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information Control1060 Management Science 57(6), pp. 1055–1077, © 2011 INFORMS

V = � +∑n

i=1 Xi, where � is the mean valuationand each Xi ∈ 811−19 captures the variation in thevaluation of characteristic i. If the consumer learnsthe specification of characteristic i, his actual Xi

is realized; otherwise, he only knows its expecta-tion. For simplicity, assume that each characteristicof the product polarizes the consumer populationindependently—i.e., P4Xi = 15 = P4Xi = −15 = 005. Atstage 0, the seller may release information on (or limita consumer’s access to) n0 ≤ n characteristics. Thena consumer’s valuation of the product at stage 0 isgiven by V0 =�+

∑n0i=1 Xi and that at stage 1 is V � V0 =

V0 +∑n

i=n0+1 Xi, contingent on V0. The valuations V0and V � V0 follow the distributions �+2B4n010055−n0and V0 + 2B4n−n010055− 4n−n05, respectively, whereB4n1p5 represents the binomial distribution with n tri-als and success probability p. When n is large enoughand p is not near 0 or 1 (e.g., both np and n41 − p5 aregreater than 5), B4n1p5 can be closely approximatedby the normal distribution N4np1np41−p55 (Box et al.2005). Therefore, V0 and V � V0 can be approximatedby the normally distributed �0 and �1 � �0 in the basicmodel. When the number of characteristics n is fixed,the distribution of a consumer’s total valuation V(approximated by �1) is fixed. The amount of informa-tion available at preorder is determined by the num-ber of characteristics n0 revealed at preorder, and n0/ncorresponds to � exactly.

The above model is essentially a simple random walkmodel with +1 and −1 steps and is a special caseof the additive martingale model of forecast evolution(Graves et al. 1986, 1998; Heath and Jackson 1994).

The next model provides an alternative micro-foundation for controlling consumer experience, inthe spirit of the hierarchical Bayesian random-effectsmodel (e.g., Lenk et al. 1996). Assume that the sellercan control the extent of consumer experience bylimiting the time of experience or the contents tobe experienced. Suppose that the distribution ofthe intrinsic consumer valuation is �1 ∼ N4�1�25and the ith unit of “experience time” or “expe-rience sample” yields a signal xi ∼ N4�11�

25 (xi’sare independent of each other given �1). If theseller limits the total experience time (or contents)at n units per consumer, then a consumer’s pos-terior valuation given 4x11 0 0 0 1 xn5 follows the dis-tribution �1 � x11 0 0 0 1 xn ∼ N4�01�

2�2/4�2 +n�255, with�0 = 4��2 + 4

∑ni=1 xi5�

25/4�2 +n�25 (DeGroot 1970).Because

∑ni=1 xi = n�1 +

∑ni=1 �i for �i ∼ N401�25, �0

is distributed according to �0 ∼N4�1 4n�4/4�2 +n�255.Define � = n�2/4�2 +n�25, and we again arrive atthe basic model, with �0 ∼ N4�1��25 and �1 � �0 ∼

N4�01 41 − �5�25. The seller can control � through n:the more experience is allowed at the preorderstage (n increases), the more valuation uncertainty isresolved early (� increases). The basic notion behind

this model is that more thorough experience createsmore heterogeneous valuations following the expe-rience, which is backed by empirical studies. Forinstance, Osborne (2011) finds that consumers in alaundry detergent market have similar expectationsprior to experience but become very heterogeneousafterward. In the video game example presented inthe introduction, after selecting a basic method ofinformation release (trailer, demo, or beta version,corresponding to different ranges of �), the seller canfurther fine tune the extent of consumer experience—e.g., by carefully choosing the size and contents of thedemo (the demos of Heavy Rain and Crackdown 2 are1.3 GB and 0.9 GB large, respectively).

4. Seller’s Optimal Pricing StrategyIn this section, we study the seller’s optimal pricingstrategy when the valuation distributions F 4�05 andG4�1 � �05 are exogenously given. We first formulatethe seller’s problem in terms of threshold consumertypes and then streamline the model around two keyparameters—information intensity at preorder, �, andnormalized margin of the product, 4�− c5/�. Afterthat, we discuss properties of the seller’s profit func-tion and show that it is optimal for the seller to exer-cise both preorder and retail. Finally, we characterizethe optimal solution through numerical analysis. In§5, we will allow the seller to control the amount ofinformation at the preorder stage, i.e., altering distri-butions F and G, and study the seller’s information-release strategy.

4.1. Seller’s Pricing Problem, Consumer ValuationThresholds, and Normalized Margin

The seller tries to maximize her profit, whereas con-sumers try to maximize their expected utility giventhe preorder price p0 and retail price p1. If the distribu-tions F and G are given, the seller solves the followingoptimal pricing problem:

maxp01p11x4·51y4·5

4p0 −c5∫

�0

x4�05dF 4�05

+4p1 −c5∫

�0

[

∫

�1

y4�15dG4�1 ��05

]

41−x4�055dF 4�05 (1)

s.t. y4�15=

{

1 �1 ≥p11

0 �1<p13(2)

x4�05=

1 �0 −p0 ≥

∫

�1

y4�154�1 −p15dG4�1 ��051

0 �0 −p0<∫

�1

y4�154�1 −p15dG4�1 ��050(3)

Constraint (2) describes the purchase behavior ofa type �1 consumer at stage 1, and constraint (3)describes that of a type �0 consumer at stage 0. To

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information ControlManagement Science 57(6), pp. 1055–1077, © 2011 INFORMS 1061

focus on the joint effect of pricing and informationrelease instead of capacity or inventory planning, weassume that the seller has ample capacity and canperfectly match supply with demand. In addition, weassume without loss of generality that a consumerwill purchase the product if he is indifferent betweenbuying and not buying.

Constraint (2) states that consumers’ purchase deci-sion at the retail stage follows a simple thresholdpolicy. The theorem below shows that their purchasedecision at the preorder stage also follows a thresholdpolicy, which implies that preorder enables the sellerto capture high valuation consumers at an early stage.

Theorem 1. Given the preorder price p0 and retail pricep1, a consumer with initial type �0 would preorder if andonly if �0 ≥ �0, and he would purchase at the retail stage(given that he has not preordered) if and only if his finaltype �1 ≥ �1, where �0 and �1 are determined by

�1 = p11 (4)

p0 =

∫ p1

−�

�1 dG4�1 � �05+ p1°G4p1 � �05

= p1 −

∫ p1

−�

G4�1 � �05 d�10 (5)

A sketch of the proof is presented here forcompleteness, and more details are provided inAppendix A. Because a consumer purchases the prod-uct at stage 1 if and only if �1 − p1 ≥ 0, it can beshown that he should preorder at stage 0 if and onlyif p1 −p0 ≥

∫ p1−�

4p1 −�15 dG4�1 � �05. That is, he preordersif and only if the preorder discount p1 − p0 exceedshis potential regret,

∫ p1−�

4p1 − �15 dG4�1 � �05, or equiv-alently,

∫ p1−�

G4�1 � �05 d�1.5 Because G4�1 � �05 decreaseswith �0 for any �1,

∫ p1−�

G4�1 � �05 d�1 decreases with �0

and hence a consumer’s optimal preorder strategy isa threshold policy.

Because∫ p1

−�G4�1 � �05 d�1 is monotone in �0, �0 is

uniquely determined by p0 and p1 from expression (5).Thus, the price pair 4p01 p15 and threshold-type pair4�01 �15 have a one-to-one correspondence, and theseller’s pricing problem (1)–(3) can be reformulatedbased on the threshold types:

max�01 �1

ç4�01 �15 = 4p04�01 �15− c5 °F 4�05

+ 4�1 − c5 °G4�1 � �0 < �05F 4�051 (6)

5 We assume that a consumer derives negative utility from the prod-uct if his final type �1 is negative. If the consumer can dispose of theproduct costlessly, his potential regret would be

∫ p10 G4�1 � �05 d�1.

In our model, due to the normal distributions of the types, when�> 3�, the probability of a negative final valuation and the differ-ence between the two regret expressions are negligible. We thankGuillermo Gallego for this comment.

where

p04�01 �15 = �1 −

∫ �1

−�

G4�1 � �05 d�1

= �1°G4�1 � �05+

∫ �1

−�

�1 dG4�1 � �050 (7)

In the objective function, °G4�1 � �0 < �05F 4�05 is a short-hand notation for

∫ �0−�

∫ +�

�1dG4�1 � �05 dF 4�05. Notice

that setting �0 = +� (or p0 ≥ p1) is equivalent to apure-retail strategy.

By the assumption of the valuation control modelthat �0 ∼ N4�1��25 and �1 � �0 ∼ N4�01 41 − �5�25,we have F 4�05 = ê44�0 −�5/

√��5 and G4�1 � �05 =

ê44�1 − �05/√

1 −��5, where ê4 · 5 and later �4 · 5denote the cumulative distribution function (c.d.f.)and probability density function (p.d.f.) of the stan-dard normal distribution. Clearly, the seller’s problem(1)–(3) or (6)–(7) is fully determined by four parame-ters 4�1 c1�1�5. The next result shows that the prob-lem is essentially determined by only two measures:the normalized margin, defined as z= 4�− c5/�, andthe preorder information intensity, � ∈ 40115. Themeasure z captures the intrinsic profitability of theproduct, whereas � captures the amount of informa-tion available at the preorder stage.

Theorem 2. Given the normalized margin z =

4�− c5/� and preorder information intensity �, the sellersolves the following normalized model without loss ofgenerality:

max�01 �1

p0°ê

(

�0 − z

�0

)

+�1

∫ �0

−�

°ê

(

�1 − �0

�1

)

d

(

ê

(

�0 − z

�0

))

1

(8)where

p0 = �0 −�1�

(

�1 − �0

�1

)

+ 4�1 − �05 °ê

(

�1 − �0

�1

)

1

�0 =√�1 and �1 =

√1 −�0

If the solution to the normalized model is 4�∗0 1 �

∗1 5, the solu-

tion to the original model (6)–(7) is 4��∗0 + c1��∗

1 + c5 andthe optimal profit under the original model is � times thenormalized one.

The normalized model can be viewed as a spe-cial instance of the original model with marginal costc = 0, standard deviation � = 1, and mean valuation�= z. Because of the simple relationship between thenormalized model and the original one, we will focuson the normalized model in the rest of this paper.

4.2. Seller’s Profit Function andOptimality of Preorder

The seller’s total profit ç4�01 �15 consists of the pre-order profit ç04�01 �15 from stage 0 and the retail profit

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information Control1062 Management Science 57(6), pp. 1055–1077, © 2011 INFORMS

Figure 2 Profit Functions ç04�01 �15, ç14�01 �15, and ç4�01 �15, from Left to Right, for 4z1 �5= 4110025

Preorder profit Retail profit Total profit

ç14�01 �15 from stage 1. By the normalized model (8),we have

ç04�01�15 = p0°ê

(

�0 −z

�0

)

=

(

�0 −�1�

(

�1 −�0

�1

)

+4�1 −�05 °ê

(

�1 −�0

�1

))

· °ê

(

�0 −z

�0

)

1 (9)

ç14�01�15 = �1

∫ �0

−�

°ê

(

�1 −�0

�1

)

d

(

ê

(

�0 −z

�0

))

=�1

�0

∫ �0

−�

°ê

(

�1 −�0

�1

)

�

(

�0 −z

�0

)

d�00 (10)

The three profit functions, ç04�01 �15, ç14�01 �15, andç4�01 �15, are illustrated in Figure 2, from left to right,for the instance 4z1�5 = 4110025.6 As shown in thefigure, the graphs of ç04�01 �15 and ç14�01 �15 resem-ble two mountain ridges, roughly parallel to the twoaxes, and the sum of the two, ç4�01 �15, resembles anL-shaped ridge. This non-concavity is an importantfeature of the seller’s total profit function. One impli-cation of this fact, as will soon be seen, is the possi-ble existence of multiple optimal solutions, which israrely mentioned in the existing preorder (advance-selling) literature.

To facilitate subsequent analysis, we examine thefirst-order conditions next.

Proposition 1. The first-order condition

¡ç4�01 �15

¡�0= 0

is equivalent to

�0 −�0

°ê44�0 − z5/�05

�44�0 − z5/�05=

�1�4ã�/�15

ê4ã�/�151 (11)

6 The attentive reader may have noticed that the preorder and totalprofits are negative at 4�01 �15 = 40105. This is because �0 = �1 = 0corresponds to p0 < p1 = 0.

where ã� = �1 − �0. For any ã� ∈ 4−�1+�5, Equa-tion (11) is satisfied by a unique �0. The first-order condi-tion ¡ç4�01 �15/¡�1 = 0 is equivalent to

°ê

(

ã�

�1

)

°ê

(

�0 −z

�0

)

+

∫ �0

−�

ê

(

�0 −�0 −ã�

�1

)

d

(

ê

(

�0 −z

�0

))

= �1�4�1 − z5ê

(

�21 �0 −�2

0ã� −�21 z

�0�1

)

0 (12)

Equation (11) enables us to express �0 as a func-tion of ã� and the total profit function ç4�01 �15as ç4�04ã�51ã� + �04ã�55, which reduces the two-variable optimization problem to a one-variableproblem that can be reliably solved by standardcomputing software such as MATLAB. This lays thefoundation for the numerical analysis in the remain-der of this paper.

Next, we show that it is always optimal for theseller to sell at both stages.

Theorem 3. Assume � ∈ 40115 or neither F nor G isa one-point distribution. Then the optimal solution to theseller’s problem (6)–(7) or (8) must satisfy �0 < +� and�1 <+�. That is, it is optimal for the seller to adopt bothpreorder and retail.

The proof of this result builds on the monotonehazard-ratio properties of the normal distribution:(1) °ê4�5/�4�5 decreases with � and lim�→+�

°ê4�5/�4�5= 0, and (2) ê4�5/�4�5 increases with � andlim�→−� ê4�5/�4�5 = 0. In other words, the resultholds for any distributions with such properties. Fora fixed �1 (or p1), choosing �0 < +� has two effects.On one hand, it leaves a positive surplus to con-sumers with high initial valuations. On the otherhand, it increases market participation, because a con-sumer with an initially high but finally low valuationwould purchase the product through preorder but notthrough retail. The proof of the theorem suggests thatthe second effect dominates the first. Therefore, for

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information ControlManagement Science 57(6), pp. 1055–1077, © 2011 INFORMS 1063

a fixed p1, both the seller and the consumers benefitfrom the preorder option: the seller gets the chanceto segment the market twice and meet different con-sumers in different stages, and consumers receive anoffer of price discount. As a result, the seller’s profit,aggregate consumer surplus, and social welfare allimprove. This differs from the result of Shugan andXie (2004) that in a discrete-valuation model the opti-mality of preorder depends on model parameters ingeneral.

4.3. Optimal Solution ThroughNumerical Analysis

In this subsection, we investigate the seller’s opti-mal pricing strategy through representative examples,with the same normalized margin z = 005 but differ-ent preorder information intensity �. The discussionalso prepares us for the detailed analysis of the impactof � in the next section.

Benchmark Case: Pure Retail 4� = 15. We start withthe case in which the seller uses retail exclusively,which is equivalent to choosing � = 1 so that con-sumers are fully informed at the preorder stage. Inthis situation, the seller should charge the optimalpure-retail price 009220. At this price, 33065% of theconsumers purchase the product, and the seller’sprofit, aggregate consumer surplus, and social welfareare 003103, 002229, and 005332, respectively.

Case I: � = 005. The seller’s profit function ç4�01 �15in this scenario is illustrated in Figure 3 through acontour map, with contour interval 000025 (the profitdifference between consecutive contour lines). For thesake of clarity, the profit function is truncated after20 contour levels.

The map demonstrates a unique local (and global)maximizer 4�01 �15= 410141211000475, with seller profit003147. This solution corresponds to preorder andretail prices 4p01 p15 = 400785611000475. The seller cap-tures high valuation consumers early by settingthe preorder (retail) price lower (higher) than thepure-retail price 009220. Compared with the bench-mark case without preorder, the change in consumersurplus given the preorder option depends on the ini-tial valuation �0: consumers with low initial valua-tions will see their surplus decline due to the higherretail price, whereas those with high initial valuationswill enjoy higher surplus due to the preorder discountand relatively low risk of regret. We depict consumersurplus for various initial types in Figure 4(a). Thesolid and dotted lines represent consumer surpluswith and without the preorder option, respectively.Figure 4(b) illustrates the (normal) probability densityfunction of the initial type �0 in the given range.

The proportion of consumers who preorder is givenby °ê44�0 − z5/

√�5, as shown in expression (8). In this

example, the proportion is 1802%. That is, the seller

Figure 3 Contour Map of the Seller’s Total Profit ç4�01 �15, for4z1 �5= 400510055

�0� 1

1.0 1.5 2.0 2.5 3.0

1.0

1.5

2.0

2.5

3.0

0.31470.3122

0.30970.3072

0.3047

focuses on the high end of the market at the preorderstage, and we say that the seller adopts a niche preorderpricing strategy. Because consumers are reasonablywell informed about the product when �= 005, thetotal market participation with the preorder optionis similar to that without it (the benchmark case).The seller’s profit increases by 104% (to 003147), theaggregate consumer surplus decreases by 303% (to002156), and the social welfare declines by less than1% (to 0.5303).

Case II: � = 000193. The contour map of the seller’stotal profit in this case is displayed in Figure 5, withcontour interval 0000075. For clarity, the profit func-tion is truncated after 10 levels. The map revealstwo optimal solutions 4�01 �15 = 400703010096705 and400424211090595, with the same seller profit 003112 (themap also reveals a saddle point at 400527611028765).The two optimal solutions represent two distinctivepricing strategies.

(1) The valuation thresholds 4�01 �15 = 400703010096705 correspond to prices 4p01 p15= 400426010096705.At this optimal solution, the total market partici-pation, the seller’s profit, aggregate consumer sur-plus, and social welfare are all similar to those inCase I. Even though the seller offers a larger pre-order discount than in Case I, the preorder propor-tion is actually lower (at 702%), because consumers areless certain about their valuations now, as � is muchsmaller. The seller again adopts a niche preorder pric-ing strategy at this solution.

(2) The valuation thresholds 4�01 �15 = 400424211090595 correspond to prices 4p01 p15= 400394911090595.Instead of capturing only high valuation consumersat preorder, the seller offers a deep discount to induce

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information Control1064 Management Science 57(6), pp. 1055–1077, © 2011 INFORMS

Figure 4 Consumer Surplus (a) and p.d.f. (b) of the Initial Type �0,for 4z1 �5= 400510055

0

0.1

0.2

0.3

0.4

0.5

0.6

–0.

5

–0.

3

–0.

0

0.2

0.5

0.7

1.0

1.2

1.5

1.7

2.0

2.2

2.5

2.7

3.0

0

0.5

1.0

1.5

2.0

2.5(a)

(b)

–0.

5

–0.

2

0.1

0.4

0.7

1.0

1.3

1.6

1.9

2.2

2.5

2.8

Con

sum

er s

urpl

usPr

obab

ility

den

sity

�0

�0

With preorder

Without preorder

the majority (7007%) of consumers to preorder, whichcan be called a mass preorder pricing strategy. Com-pared with the benchmark case, although the partic-ipation rate increases dramatically, the social welfarein fact decreases by 20% due to the inefficiency in allo-cating the good to ill-informed consumers who willlikely regret later (the relatively low normalized mar-gin z= 005 makes this situation particularly relevant).The difference in consumer surplus with and with-out the preorder option also becomes larger, as can beseen from Figure 6(a). The aggregate consumer sur-plus declines by more than 40% because consumersare almost homogeneous at the preorder stage andthe seller can extract their surplus (or information rent)relatively easily. The combination of consumer sur-plus reduction and social welfare loss improves theseller’s profit by less than half a percent. This exam-ple contrasts with the result of Xie and Shugan (2001)that advance selling benefits the seller through theincrease of market participation, not the reduction ofbuyer surplus.

Comparing Case II with Case I, we observe thatthe seller can improve her profit by increasing � from000193 to 005, i.e., releasing more information at the

Figure 5 Contour Map of the Seller’s Total Profit ç4�01 �15, for4z1 �5= 400510001935

�0

� 1

0.4 0.6 0.8 1.0 1.20.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

0.30970.3104

0.3089

0.3104

0.3097

0.3089

0.3082

0.3112

0.3112

preorder stage. Although the social welfare is lowerwith the preorder option in both cases, we remarkthat one can easily find examples in which marketparticipation, social welfare, and seller’s profit allincrease significantly with the preorder option, espe-cially when z is relatively large. The scenario z = 005is chosen in this subsection for its connection with alater discussion in §5.3.

General Results. Extensive numerical analysis showsthat the seller’s pricing problem (8) given z and � mayhave a unique local optimum, as in Case I above, ortwo local optima, as in Case II. The two optima situa-tion occurs only for z ∈ 400226710058625, the “mediummargin” scenario in §5.3. When it happens, one ofthe local optima corresponds to a niche preorder pric-ing strategy and the other a mass preorder one; thelatter dominates the former when � is small but isovertaken by the former as � increases. When the nor-malized mean z is smaller, the niche preorder optimumis the unique local optimum; when z is large enough,the mass preorder optimum is the only one.

Another general result is that for any given z, theoptimal preorder discount p1 − p0 decreases with �and approaches 0 as � approaches 1, as illustrated inFigure 7. This is consistent with the video game exam-ple in the introduction, in which smaller discounts arecoupled with more information. Notice that the curvefor z = 005 is discontinuous at � = 000193 because theoptimal preorder and retail prices are discontinuousat this �, as evident from the gap between the twooptimal solutions in Figure 5.

A thorough investigation of the impact of the pre-order information intensity � is the subject of the nextsection. If the seller releases more information, social

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information ControlManagement Science 57(6), pp. 1055–1077, © 2011 INFORMS 1065

Figure 6 Consumer Surplus (a) and p.d.f. (b) of the Initial Type �0,for 4z1 �5= 400510001935 and 4�01 �15= 400424211090595

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0

0.08

0.16

0.24

0.32

0.40

0.48

0.56

0.64

0.72

0.80

0.88

0.96

0

0.1

0.2

0.3

0.4

0.5

0.6

0.70

0.08

0.16

0.24

0.32

0.40

0.48

0.56

0.64

0.72

0.80

0.88

0.96

(a)

(b)

Con

sum

er s

urpl

usPr

obab

ility

den

sity

�0

�0

With preorder

Without preorder

welfare can be improved through more efficient allo-cations, but consumers can obtain higher informationrent as well. How should the seller strike a balancebetween information rent extraction and social wel-fare improvement? This will be a key question as westudy the seller’s information-release strategy.

Figure 7 Optimal Preorder Discount for z ∈ 80100511059 and � ∈ 40115

0.2 0.30.1 0.4 0.5 0.6 0.7 0.8 0.90

1

2

3

4

5

6

�

z = 0.0z = 0.5z = 1.5

Preo

rder

dis

coun

t5. Seller’s Optimal Information

StrategyIn the above analysis of the seller’s pricing strategy,the preorder information intensity � was exogenouslygiven. In the real world, however, the seller can oftencontrol the amount of product information at the pre-order stage. The more information the seller releases(the larger the �), the better a consumer understandsthe characteristics of the product and his own prefer-ences at the preorder stage.

The existing literature on information release isrestricted to the static environment in which the sellerand consumers interact only once (e.g., Lewis andSappington 1991, Johnson and Myatt 2006), and hencethe finding that it is optimal to release all or noth-ing may not apply in the dynamic preorder setting.When the seller releases all information, a consumer’sinitial valuation �0 fully reveals his final valuation �1and the maximum profit attainable by the seller is thesame as that under pure retail, which is suboptimalby Theorem 3. Therefore, full information release isnever optimal in our model, as summarized below.

Corollary 1. If the seller can choose the preorderinformation intensity � in problem (8), the optimal � mustbe strictly less than 1. That is, full information release issuboptimal.

The departure from the existing literature indi-cates that the trade-off between consumer surplusand social welfare is more complex in a dynamicenvironment such as ours. To find the seller’s opti-mal information strategy, we start with the followingbenchmark case.

5.1. Benchmark Case: No Information atPreorder 4�= 05

In the extreme case in which consumers have noinitial information about the product and the sellerdoes not release any information at all, the preorderinformation intensity is given by � = 0, and con-sumers’ initial valuations reduce to a single point,�0 = z. Then the seller should choose either preorderor retail instead of both because either all consumersor none will preorder. Notice that this situation differsfrom the one in the previous section, in which it isassumed that �> 0, or �0 is normally distributed, andhence Theorem 3 applies (nevertheless, it is shown inAppendix B that the seller’s profit function and opti-mal pricing strategy are continuous at �= 0). We con-sider the seller’s two extreme strategies, pure retailand pure preorder, next.

Pure Retail and Pure Preorder. When the sellerchooses pure retail, consumers can only learn their(true) valuations at stage 1 and would purchase if andonly if �1 ≥ p1. (This situation is equivalent to setting� = 1, where consumers learn their true valuations

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information Control1066 Management Science 57(6), pp. 1055–1077, © 2011 INFORMS

at stage 0 and the preorder and retail stages essen-tially collapse into one.) Because the distribution of �1

is ê4�1 − z5, the seller’s pricing problem reduces to astatic problem, çR4z5 = maxp pê4z − p5, and the opti-mal price satisfies the first-order condition ê4z− pR5−pR�4z−pR5= 0, or pR =ê4z− pR5/�4z− pR5 (the super-script “R” stands for pure “r”etail). It is straightfor-ward to show that both pR4z5 and çR4z5 increase withz and 4çR5′4z5=ê4z−pR5 ∈ 40115, which approaches 1as z goes to infinity.

If the seller wants all consumers to preorder, shecan set the preorder price p0 = z and retail pricep1 = +�, generating profit çP 4z5 = z (“P” stands forpure “p”re-order). Because 4çP 5′4z5 = 1 > 4çR5′4z5,there exists a single threshold z† such that çP 4z5 ≥

çR4z5 if and only if z ≥ z†, which can be foundthrough straightforward computation. We obtain thefollowing result immediately:

Proposition 2. Given � = 0, the seller should chooseeither preorder or retail, and the former is better than thelatter if and only if z > z† = 002267.

In other words, the seller prefers completely homo-geneous consumers to extremely heterogeneous onesif and only if z > z† = 002267.

Rotation of the Demand Curve. Proposition 2 impliesthat if the seller only sells at a single stage, the rightchoice between pure preorder (homogeneous con-sumers) and pure retail (heterogeneous ones) dependson the normalized margin z. This can be explainedthrough the rotation of the demand curve, introducedby Johnson and Myatt (2006).

If all consumers have the same valuation z, thedemand curve is flat; when consumers become moreand more heterogeneous, the demand curve rotatesclockwise.7 When z is large enough, the optimal staticprice p should be smaller than z to capture themajority of consumers—i.e., the seller would adopta mass-market pricing strategy; a clockwise rotationof the demand curve would result in fewer sales atthe price p, and hence the seller would prefer morehomogeneous consumers and withholding informa-tion. This scenario is illustrated in Figure 8(a) forp′ < z. On the contrary, when z is small or even neg-ative, the optimal static price p ought to be largerthan z to capture high valuation consumers only—i.e., the seller would opt for a niche-market pricingstrategy; a clockwise rotation of the demand curve(by releasing more information) would bring in moresales and benefit the seller, as illustrated in Figure 8(a)for p′′ > z.

7 With a unit of consumers, the demand curve can be obtained fromthe c.d.f. of the valuation � through a 90� counterclockwise rotationand proper relabeling of the axes, as can be seen in Figure 8.

Figure 8 Demand Curve Rotation in the (a) One-Period Setting and(b) First Period of a Two-Period Setting

Quantity0.5

z

p ′′

p′

Pric

ePr

ice

Quantity0.5

z

(b)

(a)

�0

p0

�0

p0

′′

′

′

′′

When the seller adopts both preorder and retail, theinitial valuation threshold �0 is brought into the pic-ture, and Figure 8(b) demonstrates the rotation effectof the preorder demand curve. We will see that theabove effect remains a driving factor, but the result ismore intricate, especially for intermediate z’s.

5.2. Information Release: Impact of �on Seller’s Profit

In this subsection, we examine how the seller’s profitis affected by a small change of �. Previously, theseller’s profit function was expressed as ç4�01 �15,in terms of the valuation thresholds 4�01 �15. It canbe written in terms of the prices 4p01 p15 as well,which turns out to be more convenient in explain-ing the impact of �. By the envelope theorem, ifp04�5 and p14�5 are the optimal prices given �, thederivative of the seller’s profit with respect to �,dç4�1p04�51 p14�55/d�, equals ¡ç4�1p04�51 p14�55/¡�,and it suffices to investigate the impact of � given p0and p1, at their optimal values.

When the seller sells at both stages, the purchas-ing threshold at stage 0 is given by �0 and the pre-order profit is given by ç04�1p01 p15 = p0

°ê4u5, where

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information ControlManagement Science 57(6), pp. 1055–1077, © 2011 INFORMS 1067

u= 4�0 − z5/�0 and °ê4u5 gives the proportion of con-sumers who preorder. Because

¡

¡�°ê4u5= −�4u5

¡u

¡�=

1�2

0

�4u5

(

4�0 − z5d�0

d�−�0

¡�0

¡�

)

1

the change in the proportion of preorder consumers isdriven by two effects simultaneously: (1) a demand-rotation effect on marginal (preorder) consumers,measured by 4�0 − z5d�0/d�, that may increase ordecrease the preorder demand depending on thesign of �0 − z; and (2) a regret effect on marginalconsumers, measured by −�0¡�0/¡�, that alwaysincreases the preorder demand, as shown below:

Lemma 1. The partial derivative of the preorder thresh-old �0 with respect to the preorder information intensity �is given by

¡�04�1p01 p15

¡�= −

12�1

�44p1 − �05/�15

ê44p1 − �05/�15< 0. (13)

When the prices p0 and p1 are fixed, as � increases,consumers become more heterogeneous at the pre-order stage, and hence the preorder demand curverotates clockwise as in Figure 8(b). In the meantime,consumers become more assertive about their truevaluations at the preorder stage and as a result aremore willing to purchase early to secure the preorderdiscount, which pushes �0 downward and drives thedemand up.

When z < 0 (which implies z < 0 < p0 < �0), as moreinformation is available at preorder, both the demand-rotation effect (the scenario z < p′′

0 < � ′′0 in Figure 8(b))

and the regret effect propel the preorder demand, sothe aggregate preorder proportion increases.

Proposition 3. When z < 0, given p0 and p1, theproportion of consumers who preorder, °ê4u4�1p01 p155,increases with �, or equivalently, ¡u4�1p01 p15/¡� < 0.

In the other direction, we can show that as zapproaches infinity, the proportion of preorder con-sumers approaches 1 and the demand rotation effectsuppresses the preorder demand:

Proposition 4. For any � < 1, there exists a z0 suchthat for all z > z0, °ê4u5 > � under the optimal pricingpolicy.

Because °ê4u5 > 005 is equivalent to z > �0, theproposition implies that the demand-rotation effectreduces the preorder demand when z is large enough(the scenario z > � ′

0 > p′0 in Figure 8(b)), in oppo-

site to the regret effect. Further numerical analysisverifies that when z is large enough the demand-rotation effect dominates the regret effect and °ê4u5decreases with � (or ¡u/¡� > 0) under the optimalpricing policy.

The change of � also impacts the seller’s retailprofit,

ç14�1p01 p15= p1

∫ �0

−�

°ê

(

p1 − �0

�1

)

d

(

ê

(

�0 − z

�0

))

0

Because

¡

¡�

∫ �0

−�

°ê

(

p1 − �0

�1

)

d

(

ê

(

�0 − z

�0

))

=ê

(

−ã�

�1

)

�4u5¡u

¡�−

12�0�1

�4u5�

(

ã�

�1

)

(derived in the proof of Theorem 4), for fixed p0and p1, the change in retail demand also dependson two effects: (1) a demand-substitution effect onmarginal consumers, captured by the first term above,that influences consumer participation at the retailstage depending on the sign of ¡u/¡�, the oppo-site of 4¡/¡�5 °ê4u5; and (2) a regret effect on lowvaluation consumers, captured by the second term,which always dampens the retail demand becausewith more accurate initial valuations, the lower ê4u5quantile of consumers is less likely to buy at the retailstage.

The next theorem aggregates the profit changesat both stages. The functions u4�1p04�51 p14�55 andã�4�1p04�51 p14�55 are simply denoted by u and ã� inthe theorem.

Theorem 4. The derivative of the seller’s total profitwith respect to � is given by

dç4�1p04�51 p14�55

d�

= −�0°ê4u5

¡u

¡�−

p14�5

2�0�1�4u5�

(

ã�

�1

)

1 (14)

where �0 =√�, and �1 =

√1 −�.

The first term on the right-hand side of Equa-tion (14) aggregates the profit changes from marginalconsumers whose initial valuations are near �0. Thesecond term captures the change from the lower ê4u5quantile of consumers who do not preorder. The the-orem implies that if more information results in lowerpreorder demand (¡u/¡�> 0), which occurs when thenormalized margin z is large enough as mentionedabove, the seller should withhold information at thepreorder stage. This theorem facilitates the investi-gation of the seller’s information-release strategy atpreorder.

5.3. Optimal Information StrategyTo reflect the fact that the seller may be forcedto disclose certain product information at the pre-order stage and consumers may have certain initialknowledge about the product beyond the seller’s con-trol, we extend the basic model so that consumers

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information Control1068 Management Science 57(6), pp. 1055–1077, © 2011 INFORMS

Figure 9 Seller’s Optimal Information-Release Strategy Map

Release informationup to upper threshold

Withhold information

0.2267 0.58620–0.5–1.00

0.2

0.4

0.6

�0

0.8

1.0

0.5 1.0 1.5

z

Upper threshold �*(z)

Lower threshold �*(z)

can possess some initial information at stage 0, rep-resented by the initial information intensity �0 ∈

60115. The total amount of information that can bereleased by the seller at preorder is therefore limitedto � ∈ 6�0117. The seller’s optimal information strategyclearly depends on �0 and the normalized margin z.In Figure 9, we draw a strategy map for the seller onhow much additional information to release for anygiven z and �0. The map can be best explained inthree sections, according to the value of z.

High-Margin Section. When z is relatively large (z >005862), the seller’s optimal profit ç4z1�5 decreaseswith � in the entire interval 60117. In this region of thestrategy map, the seller should not disclose any infor-mation in addition to the initial information alreadygained by consumers. Because the expected marginis large enough, the seller should adopt a mass pre-order strategy and use preorder effectively to captureaverage consumers. Consequently, she should with-hold information.

As an example, the optimal profit function ç4z1�5for z= 1 is illustrated in Figure 10(a). The two extremescenarios are ç4z105=çP 4z5= 1 (via pure preorder, atprice 1) and ç4z115 = çR4z5 = 005066 (via pure retail,at price pR4z5 = 101317). The profit function is strictlydecreasing in � ∈ 60117. Thus, the seller should notrelease any additional information regardless of �0.

Low-Margin Section. When z is small (z < z† =

002267), the seller’s optimal profit function ç4z1�5is quasi-concave in � and has a unique maximizer�∗4z5 ∈ 40115. In this region of the strategy map,the seller should release information up to �∗4z5 ifconsumers have less information to begin with—i.e.,�0 <�∗4z5—and should withhold information other-wise. Because the expected margin is low, consumersare skeptical at stage 0. The seller should adopt aniche preorder strategy and release a great deal ofinformation to stimulate demand from high valuation

consumers; on the other hand, she should also with-hold some information so as to benefit from both pre-order and retail (Corollary 1).

The case z = 0 is illustrated in Figure 10(c), withextreme scenarios ç4z105 = ç4z115 = çR4z5 = 001700(via pure retail, at price 007518). The case z = −002is illustrated in Figure 10(d), with ç4z105 = ç4z115 =

çR4z5 = 001288 (via pure retail, at price 006940). Weobserve that both profit functions have a single peakand that the optimal �∗4z5 increases as z decreasesbecause more information is needed to stir up the pre-order demand when z is smaller.

Medium-Margin Section. When z is in the middle(002267 < z< 005862), the seller’s optimal informationstrategy is more intriguing because the profit functionç4z1�5, for � ∈ 60117, has two local maxima, corre-sponding to two preorder strategies: a mass preorderstrategy and a niche preorder one. By choosing a tiny� (≥�0), the seller may effectively capture the majorityof consumers at the preorder stage when consumersare almost homogeneous; by choosing a larger � andinjecting more heterogeneity into the consumer valu-ation, the seller may attract high valuation consumersat the preorder stage, which can be particularly usefulwhen z is relatively small. Which strategy is better forthe seller is affected by how much information con-sumers initially possess.

We find that when z < 002288 the seller shouldcontinue to adopt the niche preorder strategy as shedoes in the low-margin situation, by releasing a largeamount of information up to the threshold �∗4z5.When z > 002288 and �0 is smaller than a certainthreshold �∗4z5, the seller should adopt the masspreorder strategy and withhold information as shedoes in the high-margin situation. However, whenz > 002288 but �0 ∈ 4�∗4z51�

∗4z55, the seller shouldadopt the niche preorder strategy and release infor-mation up to �∗4z5. Intuitively, when the informationabout a somewhat niche product is leaked to the extent

INFORMS

holds

copyrightto

this

article

and

distrib

uted

this

copy

asa

courtesy

tothe

author(s).

Add

ition

alinform

ation,

includ

ingrig

htsan

dpe

rmission

policies,

isav

ailableat

http://journa

ls.in

form

s.org/.

Chu and Zhang: Optimal Preorder Strategy with Endogenous Information ControlManagement Science 57(6), pp. 1055–1077, © 2011 INFORMS 1069

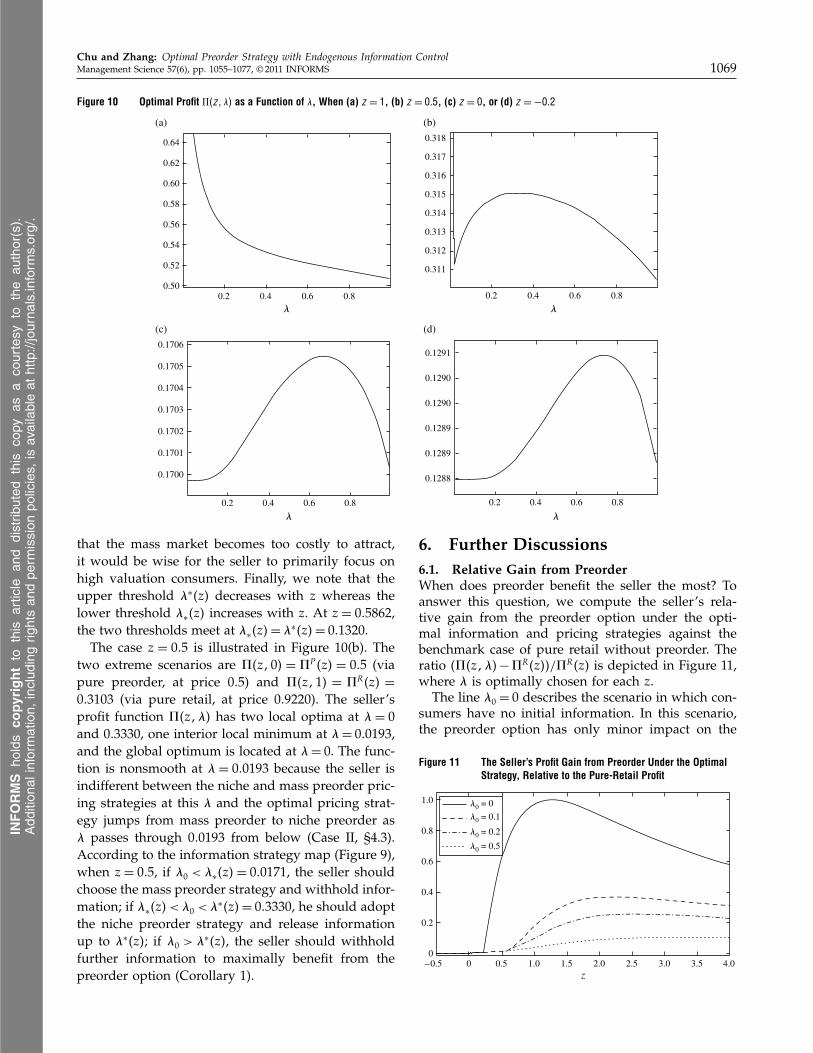

Figure 10 Optimal Profit ç4z1 �5 as a Function of �, When (a) z = 1, (b) z = 005, (c) z = 0, or (d) z = −002

0.80.60.40.2

0.1700

0.1701

0.1702

0.1703

0.1704

0.1705

0.1706

(c) (d)

(b)(a)

0.80.60.40.2

0.1291

0.1290

0.1290

0.1289

0.1289

0.1288

0.50

0.52

0.54

0.56

0.58

0.60

0.62

0.64

0.80.60.40.2 0.80.60.40.2

0.311

0.312

0.313

0.314

0.315

0.316

0.317

0.318

� �

� �

that the mass market becomes too costly to attract,it would be wise for the seller to primarily focus onhigh valuation consumers. Finally, we note that theupper threshold �∗4z5 decreases with z whereas thelower threshold �∗4z5 increases with z. At z = 005862,the two thresholds meet at �∗4z5= �∗4z5= 001320.

The case z = 005 is illustrated in Figure 10(b). Thetwo extreme scenarios are ç4z105 = çP 4z5 = 005 (viapure preorder, at price 005) and ç4z115 = çR4z5 =

003103 (via pure retail, at price 009220). The seller’sprofit function ç4z1�5 has two local optima at � = 0and 003330, one interior local minimum at �= 000193,and the global optimum is located at �= 0. The func-tion is nonsmooth at � = 000193 because the seller isindifferent between the niche and mass preorder pric-ing strategies at this � and the optimal pricing strat-egy jumps from mass preorder to niche preorder as� passes through 000193 from below (Case II, §4.3).According to the information strategy map (Figure 9),when z = 005, if �0 < �∗4z5 = 000171, the seller shouldchoose the mass preorder strategy and withhold infor-mation; if �∗4z5 < �0 <�∗4z5= 003330, he should adoptthe niche preorder strategy and release informationup to �∗4z5; if �0 > �∗4z5, the seller should withholdfurther information to maximally benefit from thepreorder option (Corollary 1).