OPPORTUNITIES FOR INTEREST GENERATING INVESTMENTS …

56

Legend Financial Advisors, Inc. ® 5700 Corporate Drive, Suite 350, Pittsburgh, PA 15237-5829 Phone: (412) 635-9210 E-mail: [email protected] www.legend-financial.com OPPORTUNITIES FOR INTEREST GENERATING INVESTMENTS OVER THE NEXT THREE YEARS Presented By Louis P. Stanasolovich, CFP ® , CEO and President Legend Financial Advisors, Inc. ®

Transcript of OPPORTUNITIES FOR INTEREST GENERATING INVESTMENTS …

Legend Financial Advisors, Inc.® 5700 Corporate Drive, Suite 350, Pittsburgh, PA 15237-5829

Phone: (412) 635-9210 E-mail: [email protected] www.legend-financial.com

OPPORTUNITIES FOR INTEREST

GENERATING INVESTMENTS OVER THE

NEXT THREE YEARS

Presented By

Louis P. Stanasolovich, CFP®, CEO and President

Legend Financial Advisors, Inc.®

LOU STANASOLOVICH, CFP®,

CEO & PRESIDENT

Lou is founder, CCO, CEO and President of Legend Financial Advisors, Inc.®

and EmergingWealth Investment Management, Inc. ®

Legend’s founder, Lou was selected by Financial Planning magazine as part of

their inaugural Influencer Awards for the Wealth Creator Award recognizing the

advisor who has made the most significant contributions to best practices for

portfolio management.

He is one of only four advisors nationwide to be selected 12 consecutive

times by Worth magazine as one of “The Top 100 Wealth Advisors”

in the country.

Lou has also been selected 13 times by Medical Economics magazine as one of

“The 150 Best Financial Advisors for Doctors in America”

Lou has been selected five times by Dental Products Report as one of “The Best Financial Advisors for Dentists in

America.”

He has twice been named one of “The 100 Great Financial Planners in America” by Mutual Funds magazine.

Lou has been named three times to Investment Advisor magazine’s “IA 25” list, ranking the 25 most influential people in

and around the financial advisory profession.

Lou was profiled in Financial Planning magazine as one of the country’s “Movers & Shakers” recognizing the top

individuals who have done the most to advance the financial advisory profession.

Lou has also been selected three times by Pittsburgh Magazine as one of the Pittsburgh area’s FIVE STAR Wealth

Managers, a list that represents the most elite financial advisors in Pittsburgh.

With over 30 years advising clients, he has shared his financial planning and investment management expertise through

dozens of speeches, radio and television broadcasts, webcasts, and hundreds of times as an interviewee, writer and

publisher.

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

COMMON

CHARACTERISTICS OF

INTEREST GENERATING

INVESTMENTS (DEBT)

DEBT INVESTMENT RISK CHARACTERISTICS

Source: Legend Financial Advisors, Inc.®, Copyright 2016

Legend Financial Advisors, Inc.®, Reprinted with Permission

TOTAL RETURN LOSSES OF 5.0% OR MORE IN

U.S. 10-YEAR TREASURY BONDS, 1950 TO-DATE

Source: The Leuthold Group, LLC, Perception Express, August 7, 2018, http://leuth.us/stock-market

REPRINTED WITH PERMISSION FROM THE LEUTHOLD GROUP, LLC

As of: August 7, 2018

COPYRIGHT 2019 THE LEUTHOLD GROUP, LLC

Source: The Leuthold Group, LLC, www.leutholdgroup.com

COPYRIGHT 2019 THE LEUTHOLD GROUP, LLC

REPRINTED WITH PERMISSION FROM THE LEUTHOLD GROUP, LLC

As of: September 30, 2018

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC..

YIELD CURVE: ALL U.S. ISSUERS

As Of: March 5, 2019

As of: March 5, 2019

Source: Barclays Capital, JP Morgan, BofA Merrill Lynch and Standard & Poor’s via

Eaton Vance Monthly Market Monitor, February 2019 www.eatonvance.com

FIXED INCOME CHARACTERISTICS AND PERFORMANCE ANALYSIS

As of: January 31, 2019

Averages

REPRINTED WITH PERMISSION OF EATON VANCE DISTRIBUTORS, INC.

2.57

2.70

3.28

2.94

3.31

3.91

6.94

6.92

6.24

5.65

6.25

2.58

IndexCoupon

(%)

Spread

(bps)

Price

($)

Yield to

Worst (%)Maturity

(yrs.)

Duration

(yrs.)

Source: Bloomberg Barclays, LCD, and Morningstar

Eaton Vance Monthly Market Monitor, February 2019, www.eatonvance.com

CORPORATE DEBT MARKET ANALYSIS

REPRINTED WITH PERMISSION OF EATON VANCE DISTRIBUTORS, INC.

As of: January 31, 2019

PRICE IMPACT OF A 1% RISE IN INTEREST RATES

Source: U.S. Treasury, Barclays Capital, FactSet, J.P. Morgan Asset Management

COPYRIGHT 2019 J.P. MORGAN ASSET MANAGEMENT

REPRINTED WITH PERMISSION OF J.P. MORGAN ASSET MANAGEMENT

As of: December 31, 2018

Sectors shown are provided by Barclays

and are represented by Broad Market; MBS:

U.S. Aggregate Securitized – MBS;

Corporate: U.S. Corporates; Municipals:

Muni Bond 10-year; High Yield: Corporate

High Yield; TIPS: Treasury Inflation

Protection Securities (TIPS). Floating Rate:

FRN (BBB); Convertibles: U.S. Convertibles

Composite; ABS: ABS + CMBS. Yield and

return information based on bellwethers for

Treasury securities. Sector yields reflect

yield to worst, while Treasury yields are

yield to maturity. Correlations are based on

10-years of monthly returns for all sectors.

Change in Interest Rates))+(0.5 *Price*

Convexity * (Change in Interest Rates) ^2).

SOURCE: BLOOMBERG INVESTMENT SERVICE

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®As Of: January 31, 2019

SOURCE: BLOOMBERG INVESTMENT SERVICE

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®As Of: January 31, 2019

DURATION OF THE BARCLAYS U.S. AGGREGATE

Source: FactSet, J.P. Morgan Asset Management

COPYRIGHT 2019 J.P. MORGAN ASSET MANAGEMENT

REPRINTED WITH PERMISSION OF J.P. MORGAN ASSET MANAGEMENT

As of: December 31, 2018

THE CASE FOR

FLOATING-RATE

LOANS

FLOATING-RATE LOAN PRIMER

1. Corporate Debt Issued By Below-Investment-Grade Borrowers

2. Most Issuers Are Significant In Size And Scale – And Many Are Familiar

Household Names

3. Companies Undertake Loans For Recapitalizations, Acquisitions And

Refinancings

4. Coupon Income From Floating-rate Loans Resets Regularly (About Every 40-60

Days On Average) To Maintain A Fixed Spread Over A Variable Base Rate,

Usually Libor

5. Loans Are Often Referred To As “Senior And Secured”: They Typically Have

The Highest Priority Of Claims In An Issuer’s Capital Structure And Are

Secured By Specific Collateral

6. Other Common Monikers: Bank Loans, Leveraged Loans, Senior Loans (All Are

Synonymous)

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

LOANS VS. BONDS: HYPOTHETICAL RETURNS IN VARIOUS

RATE SCENARIOS

Source: Eaton Vance

Floating-Rate Loan Chart Book Q4 2018, www.eatonvance.com

As of: December 31, 2018

REPRINTED WITH PERMISSION FROM EATON VANCE

Source: Eaton Vance

Eaton Vance, Floating-Rate Loan Chart Book Q4 2018, www.eatonvance.com

10-YEAR CORRELATION WITH U.S. TREASURIES

As of: December 31, 2018

REPRINTED WITH PERMISSION OF EATON VANCE DISTRIBUTORS, INC.

DESPITE A HISTORIC “BULL RUN” IN BONDS…… Loans Outperformed Bonds In Majority Of Intra One-Year Periods

Source: Eaton Vance, Floating-Rate Loan Chart Book Q1 2015, www.eatonvance.com

Note: Loans are represented by Credit Suisse Leveraged Loan Index and bonds are represented by the Barclays Capital U.S. Aggregate Index.

Analysis includes all rolling one-year periods since inception of Credit Suisse Leveraged Loan Index in February 1992.

As of: March 31, 2015

REPRINTED WITH PERMISSION FROM EATON VANCE

Source: Eaton Vance

Eaton Vance, Floating-Rate Loan Chart Book Q4 2018, www.eatonvance.com

DISTRIBUTION OF ALL QUARTERLY TOTAL RETURNS:

Q1 1992 TO Q3 2018

As of: December 31, 2018

REPRINTED WITH PERMISSION OF EATON VANCE DISTRIBUTORS, INC.

Source: The Leuthold Group, LLC, Perception Express, December 7, 2018, http://leuth.us/bond-market

REPRINTED WITH PERMISSION FROM THE LEUTHOLD GROUP, LLC

As of: December 7, 2018

COPYRIGHT 2018 THE LEUTHOLD GROUP, LLC

MUNICIPAL TAX EQUIVALENT YIELD / BARCLAYS U.S. CORPORATE BOND YIELD

1.8

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

1.6

1.4

1.2

1.0

0.8

Yield Ratio

Median: 1.15

Nov-18:

1.09

FROM NOW UNTIL

THE RECESSION

CHARACTERISTICS OF

A PRE-RECESSION ECONOMY

1. More Volatility In The Stock Market

2. Slowing Economic Conditions

3. Slowing Profit Growth Of Companies

4. A Declining Stock Market Over At Least Six Months

5. Generally Rising Interest Rates

6. An Inversion Of The Yield Curve Occurs (Two-Year U.S.

Treasury Yield Curves Become Higher Than The Ten-Year

Yield Curve)

7. Commodity Prices Rise

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

Source: Bloomberg Investment Services, L.P.

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®As Of February 28, 2019

Source: Bloomberg Investment Services, L.P.

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®As Of March 5, 2019

Source: Bloomberg Investment Services, L.P.

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®As Of February 28, 2019

Source: Bloomberg Investment Services, L.P.

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

As Of: February 28, 2019

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

As Of March 5, 2019

SOURCE: BLOOMBERG INVESTMENT SERVICE

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

As of: March 1, 2019

SOURCE: BLOOMBERG INVESTMENT SERVICE

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®As of: March 2019

FLOATING-RATE LOANS VS. SELECT ASSET CLASSES

SOURCE: BLOOMBERG INVESTMENT SERVICE

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®As of: March 1, 2019

As of: March 1, 2019 SOURCE: BLOOMBERG INVESTMENT SERVICE

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

2007-2009 RECESSION

3 MONTH T-BILLS VS. 90 DAY COMMERCIAL PAPER

July 1, 2007 To January 15, 2008

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

As Of March 1. 2019

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

SPX INDEX PAST 6 MONTHSJuly 15, 2007 To January 18, 2008

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

As Of February 28, 2019

2019 RECESSION EVALUATION

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

3 MONTH T-BILLS VS. 90 DAY COMMERCIAL PAPER

January 1, 2018 To March 5, 2019

As Of March 5, 2019

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

As Of February 20. 2019

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

As Of February 20, 2019

Source: Bloomberg Investment Services

COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

REPRINTED WITH PERMISSION OF LEGEND FINANCIAL ADVISORS, INC.®

As Of March 1. 2019

WHAT INTEREST GENERATING

INVESTMENTS TO USE AS A U.S.

RECESSION APPROACHES

1. Variable Rate Debt Investments:

a. Bank Loans

b. Highly Discounted Jumbo Adjustable Interest Rate Mortgages

2. Investments To Avoid:

a. Foreign And Emerging Market Bonds

b. Most Intermediate And Long-Term Bonds Of All Types

c. Probably Utilities

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

DURING THE

FIRST HALF OF

THE RECESSION

CHARACTERISTICS OF THE

FIRST HALF OF A RECESSION

1. Volatility (VIX) Increases Substantially In the Stock Market

2. The Stock Market Decline Accelerates

3. Economic Conditions Decrease – High Yield Prices Fall Precipitously

4. Possible Deflation

5. Profit Growth Goes Negative

6. Energy Prices Decline

7. Interest Rates Begin To Decline

8. The U.S. Dollar Rises

9. Gold Bullion Prices Decline

10. Food Prices Rise

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

BARCLAYS U.S. HIGH YIELD BOND MINUS TREASURY BOND YIELD

20

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

15

10

5

Source: The Leuthold Group, LLC, Perception Express, December 7, 2018, http://leuth.us/bond-market

REPRINTED WITH PERMISSION FROM THE LEUTHOLD GROUP, LLC

As of: December 7, 2018

COPYRIGHT 2018 THE LEUTHOLD GROUP, LLC

Nov-18:

4.29

Differential

Median: 4.99

HIGH YIELD BONDS

Source: J.P. Morgan Global Economic Research, J.P. Morgan Asset Management

COPYRIGHT 2019 J.P. MORGAN ASSET MANAGEMENT

REPRINTED WITH PERMISSION OF J.P. MORGAN ASSET MANAGEMENT

As of: December 31, 2018

Source: Bloomberg Barclays, LCD, and Morningstar

Eaton Vance Floating-Rate Loan Chart Book, Q4 2018, www.eatonvance.com

CORPORATE BOND MARKET UPDATE

REPRINTED WITH PERMISSION OF EATON VANCE DISTRIBUTORS, INC.

As of: December 31, 2018

Source: Eaton Vance

Eaton Vance, Floating-Rate Loan Chart Book Q4 2018, www.eatonvance.com

DISTRESS RATIO

Percent Of Bank Loans Below $80

As of: December 31, 2018

REPRINTED WITH PERMISSION OF EATON VANCE DISTRIBUTORS, INC.

WHAT INTEREST GENERATING

INVESTMENTS TO USE IN THE

FIRST HALF OF A U.S. RECESSIONAssumes A Rising U.S. Dollar

1. Money Markets, U.S. Treasury Bills, CDs, Stable Value Funds

(For Retirement Plans)

2. The U.S. Dollar

3. Intermediate and Long Dated U.S. Treasuries – GNMAs,

Short/Intermediate/Long-Zero Coupon U.S. Treasuries

4. Avoid: High-Yield Bonds, Bank Loans, Highly Discounted Jumbo

Adjustable Interest Rate Mortgages, Municipal Bonds, Foreign

And Emerging Market Bonds

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

DURING THE

SECOND HALF OF

THE RECESSION

CHARACTERISTICS OF THE

SECOND HALF OF A RECESSION

1. Interest Rates Continue To Fall

2. The Stock Market Begins To Decline Precipitously

3. Corporate Bond & Bank Loan Funds’ Default Rates Increase

4. Corporate Profits Continue To Bottom

5. Gold Bullion Begins To Rise

6. U.S. Dollar Begins To Fall

7. Commodities Tend To Fall

8. A Recession Is Officially Declared

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

Source: Palmer Square Capital Management, www.palmersquarecap.com

REPRINTED WITH PERMISSION FROM PALMER SQUARE CAPITAL MANAGEMENT, LLC

As of: March 31, 2018

COPYRIGHT 2019 Palmer Square Capital Management, LLC

HISTORICAL AVERAGE ANNUAL DEFAULT RATE

Sector Yield Historical Average Annual

Default Rate

CLO AAA 3.29% 0.00%

CLO AA 3.68% 0.00%

CLO A 4.48% 0.03%

CLO BBB 5.53% 0.13%

CLO BB 8.29% 0.47%

CLO B 10.17% 2.59%

Floating Rate Bank Loan BB/B 5.89% 3.20%

High Yield 6.33% 3.00%

Past performance is no guarantee of future returns.

Source: CLO yields from JP Morgan CLOIE Index, CLO average annual default rates from Moody’s 2000-2014; Floating

Rate Bank Loan BB/B (JLYMSBB) yields and default rates from JP Morgan 1998-2017, High Yield from BAML and default

rates from JPM 1982-2017, as of December 29, 2017.

HIGH YIELD BONDS

Source: J.P. Morgan Global Economic Research, J.P. Morgan Asset Management

COPYRIGHT 2016 J.P. MORGAN ASSET MANAGEMENT

REPRINTED WITH PERMISSION OF J.P. MORGAN ASSET MANAGEMENT

As of: December 31, 2016

Average Latest

High Yield Spreads 5.9% 5.6%

High Yield Default Rates 3.9% 3.5%

Default rate is as of 11/30/2016 and Spread to Worst is as of 12/31/2016. Default rates are defined as the par value percentage of the total market trading at or

below 50% of par value and include any Chapter 11 filing, prepackaged filing or missed interest payments. Spreads indicated are benchmark yield to worst less

comparable maturity Treasury yields. Yield to worst is defined as the lowest potential yield that can be received on a bond without the issuer actually defaulting

and reflects the possibility of the bond being called at an unfavorable time for the holder. High yield is represented by the J.P. Morgan Domestic HY Index.

Investment grade is represented by the J.P. Morgan U.S. Liquid Index. Recovery rates are issuer-weighted and based on bond price 30 days after default date.

The 2009 adjusted recovery rate is based on year-end prices. *2016 recovery rate is for the last 12 months ending November 216, and is not included in the

average recovery rate calculated over the period.

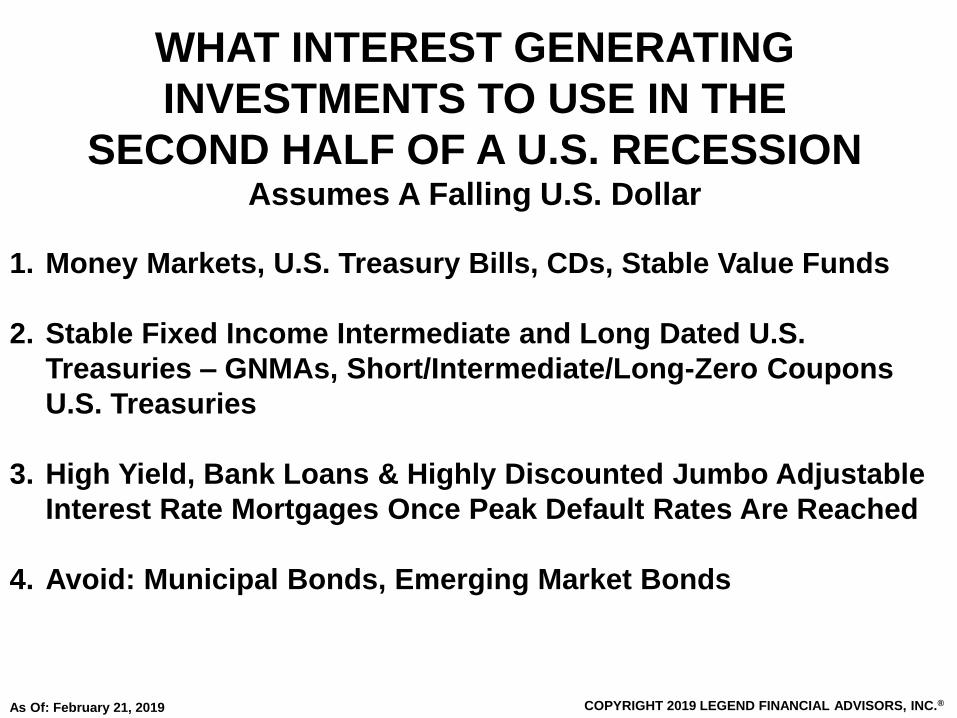

1. Money Markets, U.S. Treasury Bills, CDs, Stable Value Funds

2. Stable Fixed Income Intermediate and Long Dated U.S.

Treasuries – GNMAs, Short/Intermediate/Long-Zero Coupons

U.S. Treasuries

3. High Yield, Bank Loans & Highly Discounted Jumbo Adjustable

Interest Rate Mortgages Once Peak Default Rates Are Reached

4. Avoid: Municipal Bonds, Emerging Market Bonds

WHAT INTEREST GENERATING

INVESTMENTS TO USE IN THE

SECOND HALF OF A U.S. RECESSIONAssumes A Falling U.S. Dollar

As Of: February 21, 2019 COPYRIGHT 2019 LEGEND FINANCIAL ADVISORS, INC.®

QUESTIONS AND ANSWERS

Call Us With Any Questions

Or To

Schedule An Appointment

(412) 635-9210 Or (888) 236-5960

www.legend-financial.com