Online travel report by Dealroom June 2016

30

Online Travel: a Deep Dive Europe and beyond June 2016

-

Upload

yoram-wijngaarde -

Category

Travel

-

view

1.393 -

download

2

Transcript of Online travel report by Dealroom June 2016

Online Travel: a Deep Dive

Europe and beyondJune 2016

1. Introduction

2. Macro view

3. Strategic landscape

4. Funding & valuation data

2

Table of contents

Who is Dealroom.co■ Dealroom is Europe’s leading online resource for rich

data and analytics on private tech companies

■ Natural language processing and algorithms are used to capture real-time insights on 500K companies

■ Data is verified and curated by an internal team of analyst and by our community of 10K+ founders, VCs, accelerators, journalists

■ Founded in 2013 by a team with backgrounds in investment banking, data science and IT

3

About this report

Curation & research by Dealroom’s team

10,000+ contributors (founders, VCs, …)

Big data analytics on 500,000+ companies

This report■ This report combines algorithmic and funding data

from Dealroom with industry research and insider interviews, to provide a 360° view on the online travel space

■ The scope is global, but with European emphasis

■ In addition to this presentation, the full report also consists of an online database with curated lists, which are references throughout this presentation

■ For more information, also check dealroom.co’s blog

Yoram WijngaardeFounder of Dealroom.coFormer tech, media and telecom M&A advisor at Lehman Brothers and NOAH Advisors

Authors and contributors

4

Julien PulsContent curatorWith Dealroom since 2014. Formerly at CMB CapitalUniversité Jean Moulin, Lyon

Contributors

John Erceg (private investor, hotelier, serial entrepreneur)Founder of Budgetplaces, sold in 2011 to private equity. MBA from IESE business school, Worldwide Market Development Manager for HP. From California, lived in Barcelona since 1994.

Avi Meir (Co-founder and CEO, TravelPerk) Founder of Hotel Ninjas, sold to Priceline in 2014. MBA from IESE Barcelona. Former Senior Product Owner at Booking.com and Product Vice President at budgetplaces.com

Joe Haslam (Chairman & Co-founder, Hot Hotels)HotHotels offers discount, mobile only rates up to 7 Days in advance of your stay. In 55 Countries & 333 cities in Europe, Africa, Middle East, Asia & the Americas (Techstars Boston, Summer 2015 class).

Patrick Martin (Partner - LD&A Jupiter Corp Finance) M&A advisor in media & tech since 1993. Former Head of Media at Alegro Capital, Co-CEO of 2k Media, and Managing Partner of Helkon Media.

Chris Moller (Campanda CEO & founder, Möller Ventures)Campanda is a booking platform for RVs which raised €5m series A last year. Chris is also the former CEO and founder of erento, a marketplace for renting goods and services, sold in 2011 to Russmedia.

Axel Schmiegelow (CEO, iTravel)Serial entrepreneur focused on the web, social media, and software. itravel is an experience-based online and mobile tour operator that offers leisure travelers a platform to fully customize trips.

Jaime Novoa (Data Analyst at Tech.eu) Also owner of Novobrief, an English language blog covering the Spanish startup ecosystem. Previously a writer for StartupXplore, Weblogs and We Are Social.

Jose Luis Martinez (CEO, HundredRooms)Former Head of Kayak in Spain, and Managing Director of Spain and Portugal. Former Director for Spain eDreams ODIGEO. Advisor to Board of Directors in Minube. In 2008 founded Viamedius.

Jan Wegenaar (CEO, Advalley.io) Direct marketing & travel entrepreneur. Launched voucher concept, sold to WTA in 2007. Founded Advalley.io in 2011, a B2B voucher marketplace for merchants and advertisers.

Robin Wauters (Founder at Tech.eu)Advisor / minor shareholder of several tech starups such as Checkthis (Frontback), Maily.com, Argus Labs (Jini.co), Showpad.com and Oxynade.com. Former Editor at The Next Web, Vitualization.com and TechCrunch.

Editors

RJ Friedlander (Founder & CEO, ReviewPro)Over 17 years experience in Internet and technology in Europe, the US and Asia. Led projects that have generated more than $300 million in revenue. Senior executive at Grupo Planeta for about 10 years.

Philipp Brinkmann, (Founder and CEO, Tripsta)Tripsta is a leading OTA in Greece and operates in 50+ markets. Philipp has also been on the board of several companies in the travel, e-commerce, and media industries.

Carlos Rodríguez-Maribona Andrés (COO, Minube)Minube is a leading UK based travel guide, a community of over 1.5 million like-minded travelers. Carlos was formerly an Associate at the investment division of Axon Partners Group.

Elliott Pritchard (CMO, Triptease)Former Chief Marketing Officer at Travel Republic, he has assumed leading positions at P&O Cruises, Kuoni, and MarketingNet.

Naveen Sharma (CMO, Lodgify)Lodgify enables vacation rental owners and managers to easily create a website for their properties and manage their reservations. Former Senior Consultant at Cloudbridge.

Friedrich von Scanzoni (CEO, Burda Asia)Broad management experience in digital media (13 years), in start-up, growth and restructuring environments. Former Managing Director International at HolidayCheck and VP of VP Corporate Development at Tomorrow Focus.

Nico van der Veen (Founder & CEO, MaxMind)MaxMind is an independent connector between hotels and OTA's, delivering real-timerate and availability data, reservation software suite and reservation API essentials.

5

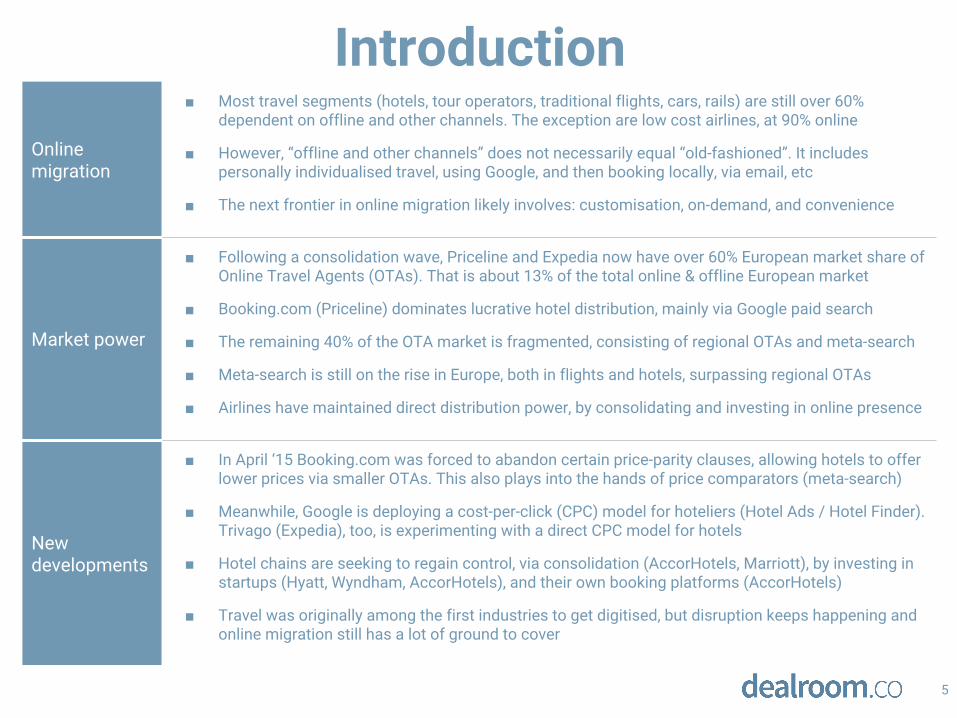

Introduction

Online migration

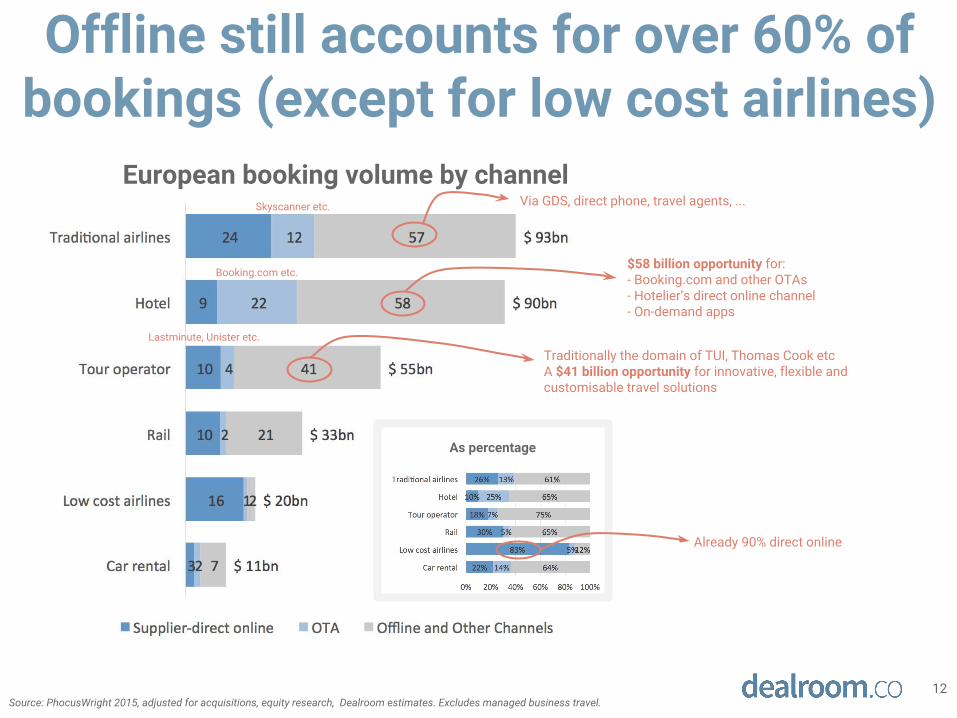

■ Most travel segments (hotels, tour operators, traditional flights, cars, rails) are still over 60% dependent on offline and other channels. The exception are low cost airlines, at 90% online

■ However, “offline and other channels” does not necessarily equal “old-fashioned”. It includes personally individualised travel, using Google, and then booking locally, via email, etc

■ The next frontier in online migration likely involves: customisation, on-demand, and convenience

Market power

■ Following a consolidation wave, Priceline and Expedia now have over 60% European market share of Online Travel Agents (OTAs). That is about 13% of the total online & offline European market

■ Booking.com (Priceline) dominates lucrative hotel distribution, mainly via Google paid search

■ The remaining 40% of the OTA market is fragmented, consisting of regional OTAs and meta-search

■ Meta-search is still on the rise in Europe, both in flights and hotels, surpassing regional OTAs

■ Airlines have maintained direct distribution power, by consolidating and investing in online presence

New developments

■ In April ‘15 Booking.com was forced to abandon certain price-parity clauses, allowing hotels to offer lower prices via smaller OTAs. This also plays into the hands of price comparators (meta-search)

■ Meanwhile, Google is deploying a cost-per-click (CPC) model for hoteliers (Hotel Ads / Hotel Finder). Trivago (Expedia), too, is experimenting with a direct CPC model for hotels

■ Hotel chains are seeking to regain control, via consolidation (AccorHotels, Marriott), by investing in startups (Hyatt, Wyndham, AccorHotels), and their own booking platforms (AccorHotels)

■ Travel was originally among the first industries to get digitised, but disruption keeps happening and online migration still has a lot of ground to cover

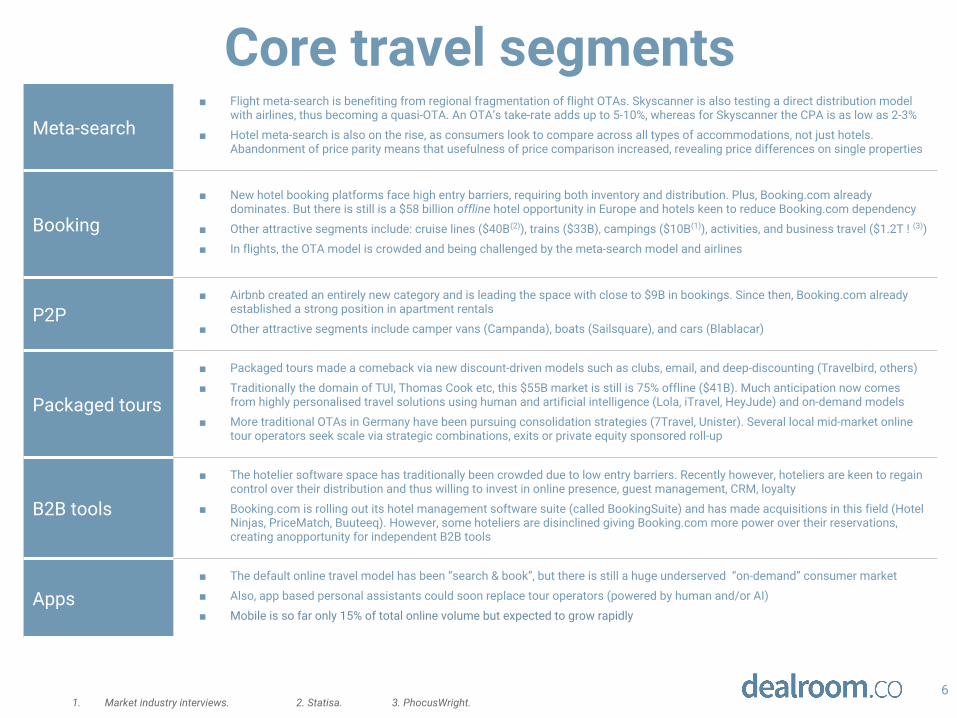

Meta-search■ Flight meta-search is benefiting from regional fragmentation of flight OTAs. Skyscanner is also testing a direct distribution model

with airlines, thus becoming a quasi-OTA. An OTA’s take-rate adds up to 5-10%, whereas for Skyscanner the CPA is as low as 2-3%

■ Hotel meta-search is also on the rise, as consumers look to compare across all types of accommodations, not just hotels. Abandonment of price parity means that usefulness of price comparison increased, revealing price differences on single properties

Booking

■ New hotel booking platforms face high entry barriers, requiring both inventory and distribution. Plus, Booking.com already dominates. But there is still is a $58 billion offline hotel opportunity in Europe and hotels keen to reduce Booking.com dependency

■ Other attractive segments include: cruise lines ($40B(2)), trains ($33B), campings ($10B(1)), activities, and business travel ($1.2T ! (3))

■ In flights, the OTA model is crowded and being challenged by the meta-search model and airlines

P2P■ Airbnb created an entirely new category and is leading the space with close to $9B in bookings. Since then, Booking.com already

established a strong position in apartment rentals

■ Other attractive segments include camper vans (Campanda), boats (Sailsquare), and cars (Blablacar)

Packaged tours

■ Packaged tours made a comeback via new discount-driven models such as clubs, email, and deep-discounting (Travelbird, others)

■ Traditionally the domain of TUI, Thomas Cook etc, this $55B market is still is 75% offline ($41B). Much anticipation now comes from highly personalised travel solutions using human and artificial intelligence (Lola, iTravel, HeyJude) and on-demand models

■ More traditional OTAs in Germany have been pursuing consolidation strategies (7Travel, Unister). Several local mid-market online tour operators seek scale via strategic combinations, exits or private equity sponsored roll-up

B2B tools

■ The hotelier software space has traditionally been crowded due to low entry barriers. Recently however, hoteliers are keen to regain control over their distribution and thus willing to invest in online presence, guest management, CRM, loyalty

■ Booking.com is rolling out its hotel management software suite (called BookingSuite) and has made acquisitions in this field (Hotel Ninjas, PriceMatch, Buuteeq). However, some hoteliers are disinclined giving Booking.com more power over their reservations, creating anopportunity for independent B2B tools

Apps■ The default online travel model has been “search & book”, but there is still a huge underserved “on-demand” consumer market

■ Also, app based personal assistants could soon replace tour operators (powered by human and/or AI)

■ Mobile is so far only 15% of total online volume but expected to grow rapidly

61. Market industry interviews. 2. Statisa. 3. PhocusWright.

Core travel segments

7

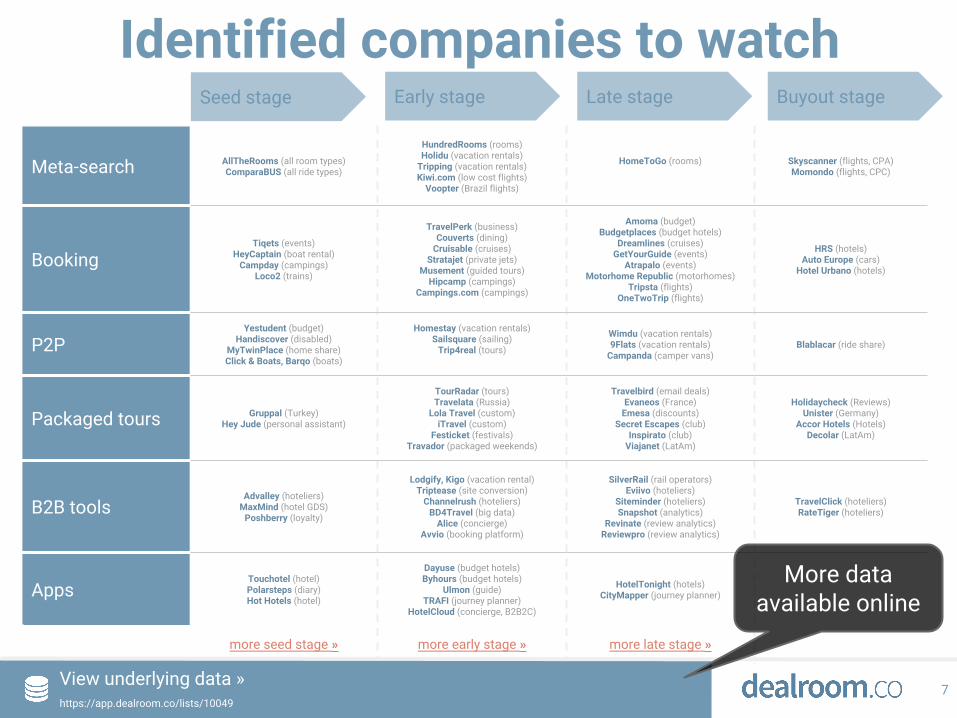

Identified companies to watch

Meta-search AllTheRooms (all room types)ComparaBUS (all ride types)

HundredRooms (rooms)Holidu (vacation rentals)

Tripping (vacation rentals)Kiwi.com (low cost flights)

Voopter (Brazil flights)

HomeToGo (rooms) Skyscanner (flights, CPA)Momondo (flights, CPC)

BookingTiqets (events)

HeyCaptain (boat rental)Campday (campings)

Loco2 (trains)

TravelPerk (business)Couverts (dining)

Cruisable (cruises)Stratajet (private jets)

Musement (guided tours)Hipcamp (campings)

Campings.com (campings)

Amoma (budget)Budgetplaces (budget hotels)

Dreamlines (cruises)GetYourGuide (events)

Atrapalo (events)Motorhome Republic (motorhomes)

Tripsta (flights)OneTwoTrip (flights)

HRS (hotels)Auto Europe (cars)

Hotel Urbano (hotels)

P2PYestudent (budget)

Handiscover (disabled)MyTwinPlace (home share)Click & Boats, Barqo (boats)

Homestay (vacation rentals)Sailsquare (sailing)

Trip4real (tours)

Wimdu (vacation rentals)9Flats (vacation rentals)

Campanda (camper vans)Blablacar (ride share)

Packaged tours Gruppal (Turkey)Hey Jude (personal assistant)

TourRadar (tours)Travelata (Russia)

Lola Travel (custom)iTravel (custom)

Festicket (festivals)Travador (packaged weekends)

Travelbird (email deals)Evaneos (France)

Emesa (discounts)Secret Escapes (club)

Inspirato (club)Viajanet (LatAm)

Holidaycheck (Reviews)Unister (Germany)

Accor Hotels (Hotels)Decolar (LatAm)

B2B toolsAdvalley (hoteliers)

MaxMind (hotel GDS)Poshberry (loyalty)

Lodgify, Kigo (vacation rental)Triptease (site conversion)

Channelrush (hoteliers)BD4Travel (big data)

Alice (concierge)Avvio (booking platform)

SilverRail (rail operators)Eviivo (hoteliers)

Siteminder (hoteliers)Snapshot (analytics)

Revinate (review analytics)Reviewpro (review analytics)

TravelClick (hoteliers)RateTiger (hoteliers)

AppsTouchotel (hotel)Polarsteps (diary)Hot Hotels (hotel)

Dayuse (budget hotels)Byhours (budget hotels)

Ulmon (guide)TRAFI (journey planner)

HotelCloud (concierge, B2B2C)

HotelTonight (hotels)CityMapper (journey planner)

more seed stage » more early stage » more late stage »

Seed stage Early stage Late stage Buyout stage

View underlying data » https://app.dealroom.co/lists/10049

More data available online

1. Introduction

2. Macro view

3. Strategic landscape

4. Funding & valuation data

8

Table of contents

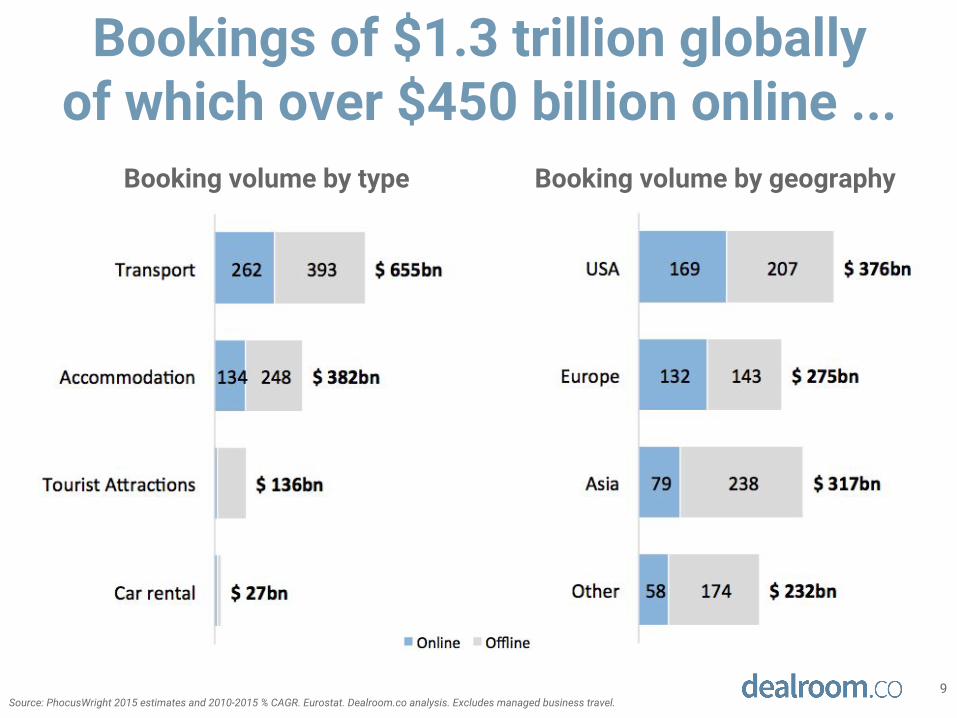

Bookings of $1.3 trillion globally of which over $450 billion online ...

9Source: PhocusWright 2015 estimates and 2010-2015 % CAGR. Eurostat. Dealroom.co analysis. Excludes managed business travel.

Booking volume by type Booking volume by geography

Booking, Kayak, OpenTable, Agoda, ...

$ 60B firm value = 13 x $ 4.6B EBITDA

Expedia, Trivago, HomeAway, Orbitz, Travelocity, Wotif, ...

$ 17B firm value= 10 x $ 1.7B EBITDA

eDreams, OpodoGovoyages

$ 25B firm value

$ 1B firm value

$ 625M firm value= 6.4 x $ 94M EBITDA

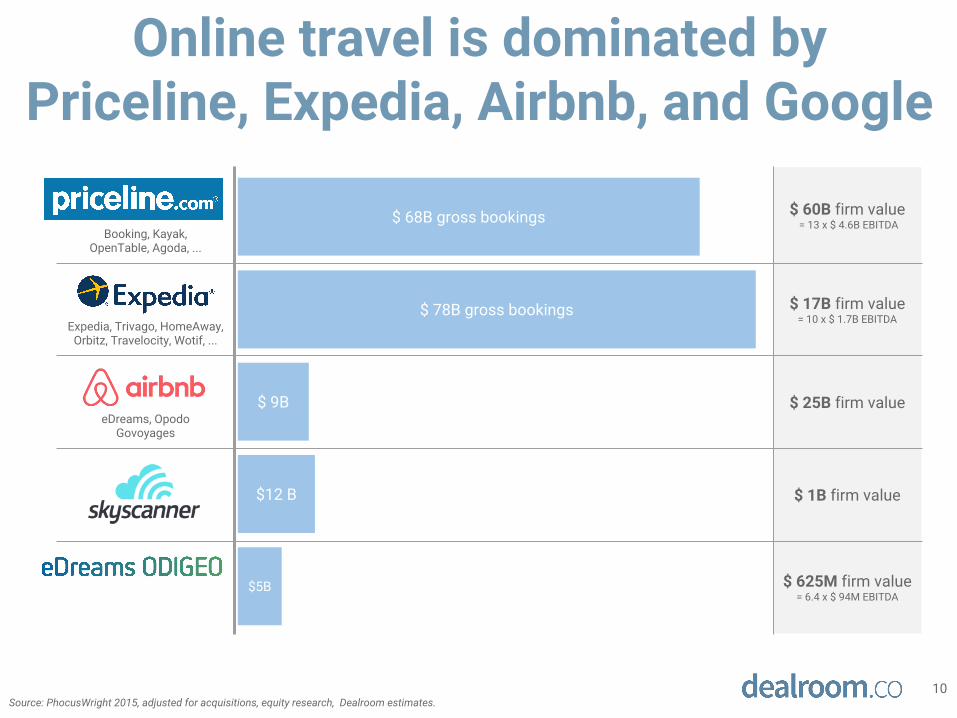

Online travel is dominated by Priceline, Expedia, Airbnb, and Google

10Source: PhocusWright 2015, adjusted for acquisitions, equity research, Dealroom estimates.

$ 68B gross bookings

$ 78B gross bookings

$5B

$12 B

$ 9B

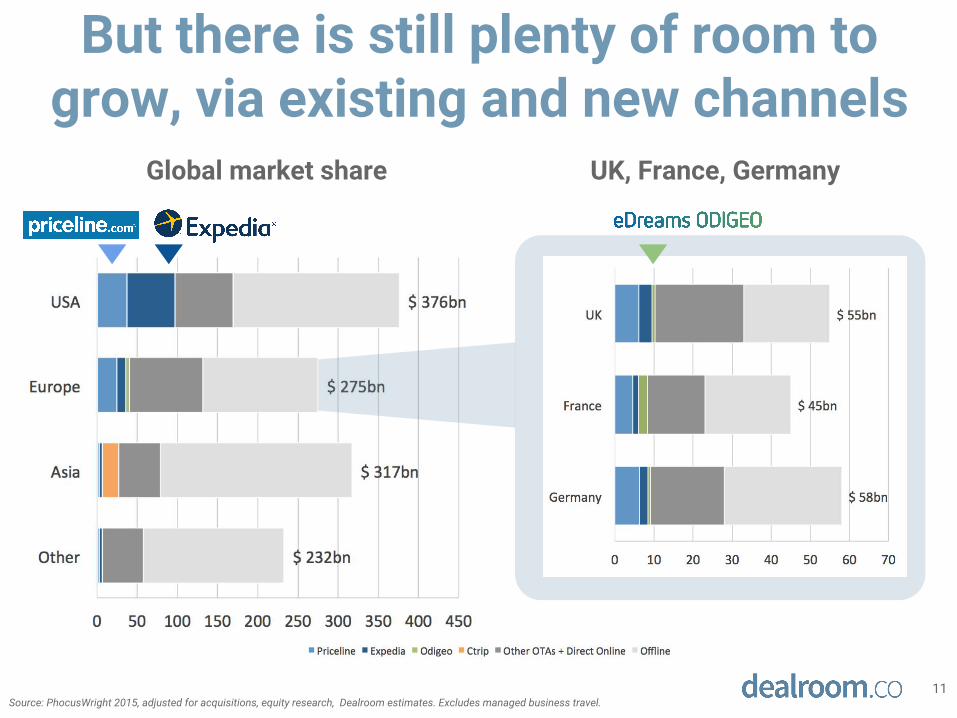

But there is still plenty of room to grow, via existing and new channels

11Source: PhocusWright 2015, adjusted for acquisitions, equity research, Dealroom estimates. Excludes managed business travel.

Global market share UK, France, Germany

Offline still accounts for over 60% of bookings (except for low cost airlines)

12Source: PhocusWright 2015, adjusted for acquisitions, equity research, Dealroom estimates. Excludes managed business travel.

As percentage

European booking volume by channel

Already 90% direct online

Via GDS, direct phone, travel agents, ...

Booking.com etc.$58 billion opportunity for: - Booking.com and other OTAs- Hotelier’s direct online channel- On-demand apps

Traditionally the domain of TUI, Thomas Cook etcA $41 billion opportunity for innovative, flexible and customisable travel solutions

Skyscanner etc.

Lastminute, Unister etc.

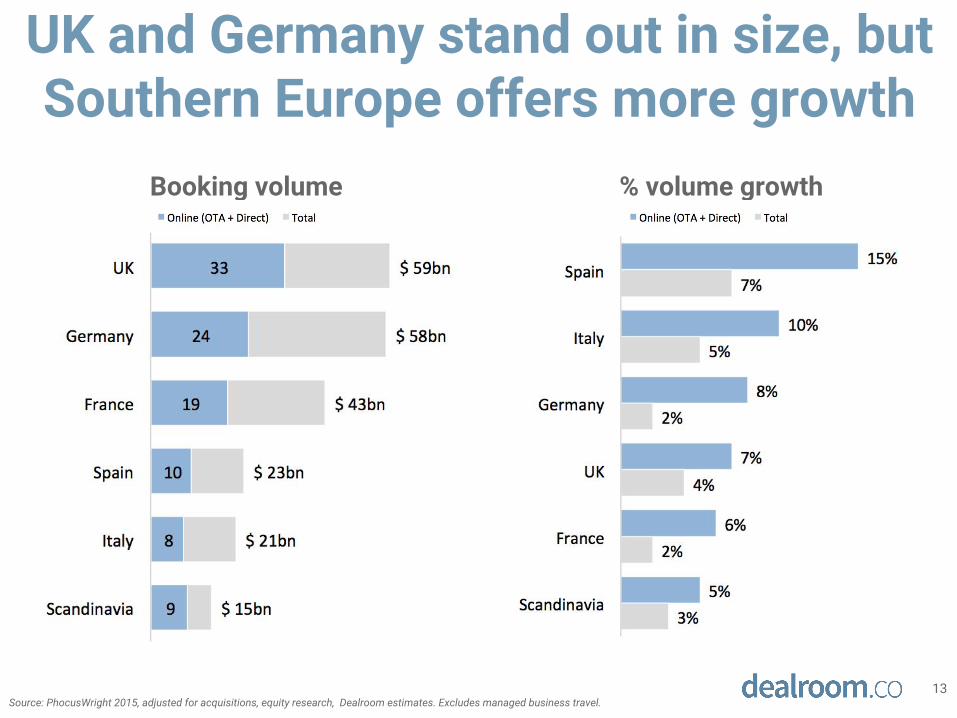

13Source: PhocusWright 2015, adjusted for acquisitions, equity research, Dealroom estimates. Excludes managed business travel.

Booking volume % volume growth

UK and Germany stand out in size, but Southern Europe offers more growth

14

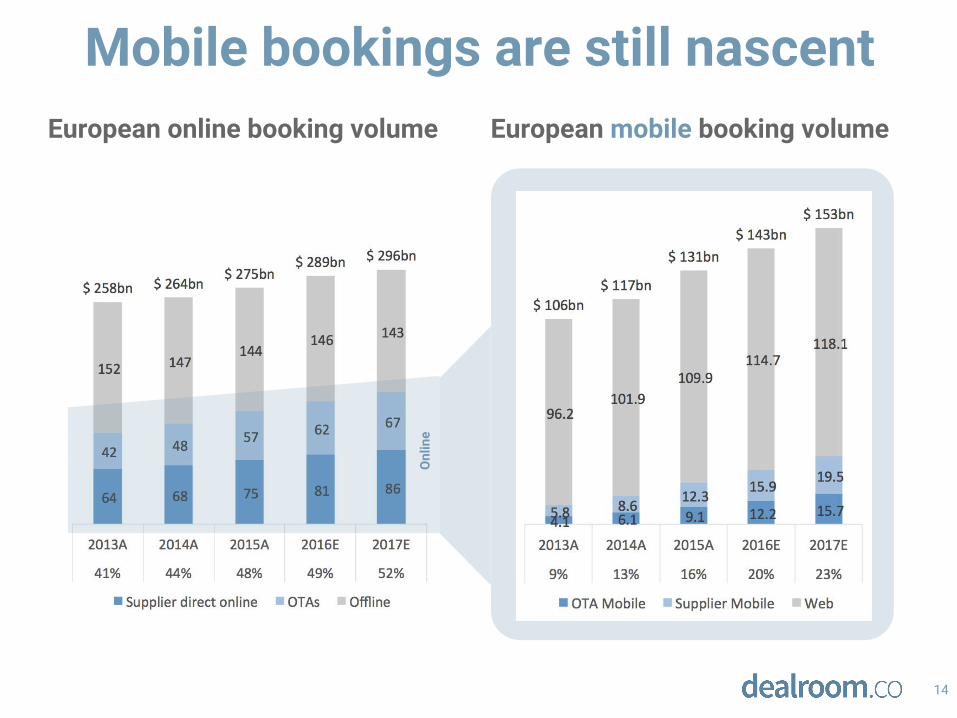

Mobile bookings are still nascent European online booking volume European mobile booking volume

Onl

ine

1. Introduction

2. Macro view

3. Strategic landscape

4. Funding & valuation data

15

Table of contents

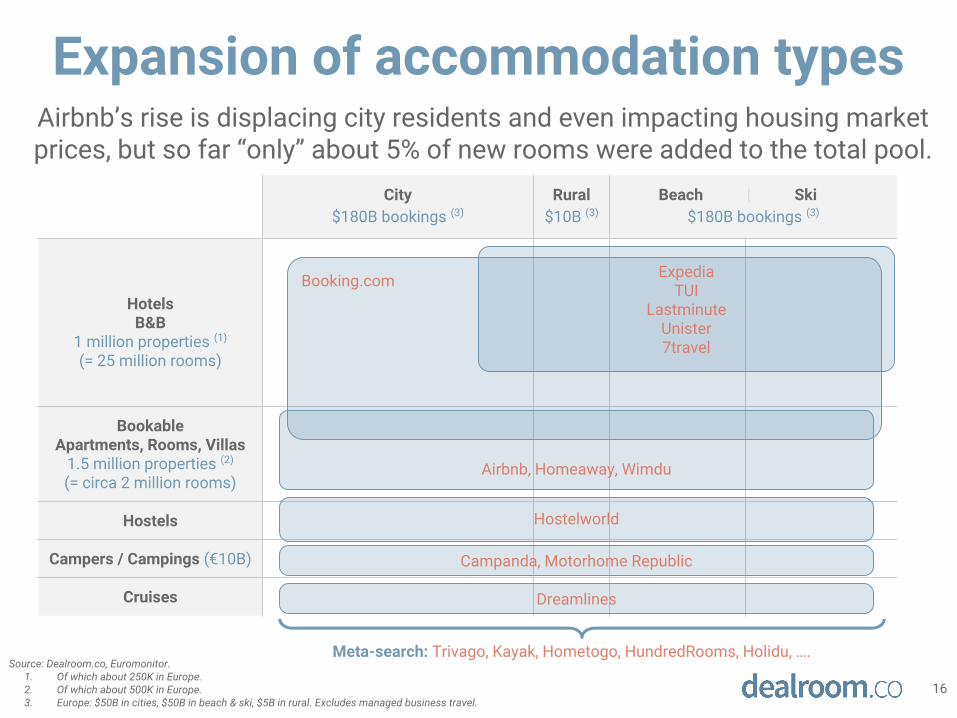

Expansion of accommodation types

16

City$180B bookings (3)

Rural$10B (3)

Beach | Ski $180B bookings (3)

HotelsB&B

1 million properties (1)

(= 25 million rooms)

Bookable Apartments, Rooms, Villas

1.5 million properties (2)

(= circa 2 million rooms)

Hostels

Campers / Campings (€10B)

Cruises

Booking.com

Hostelworld

Airbnb, Homeaway, Wimdu

ExpediaTUI

LastminuteUnister 7travel

Campanda, Motorhome Republic

Dreamlines

Source: Dealroom.co, Euromonitor. 1. Of which about 250K in Europe.2. Of which about 500K in Europe.3. Europe: $50B in cities, $50B in beach & ski, $5B in rural. Excludes managed business travel.

Meta-search: Trivago, Kayak, Hometogo, HundredRooms, Holidu, ….

Airbnb’s rise is displacing city residents and even impacting housing market prices, but so far “only” about 5% of new rooms were added to the total pool.

GuestsHotels

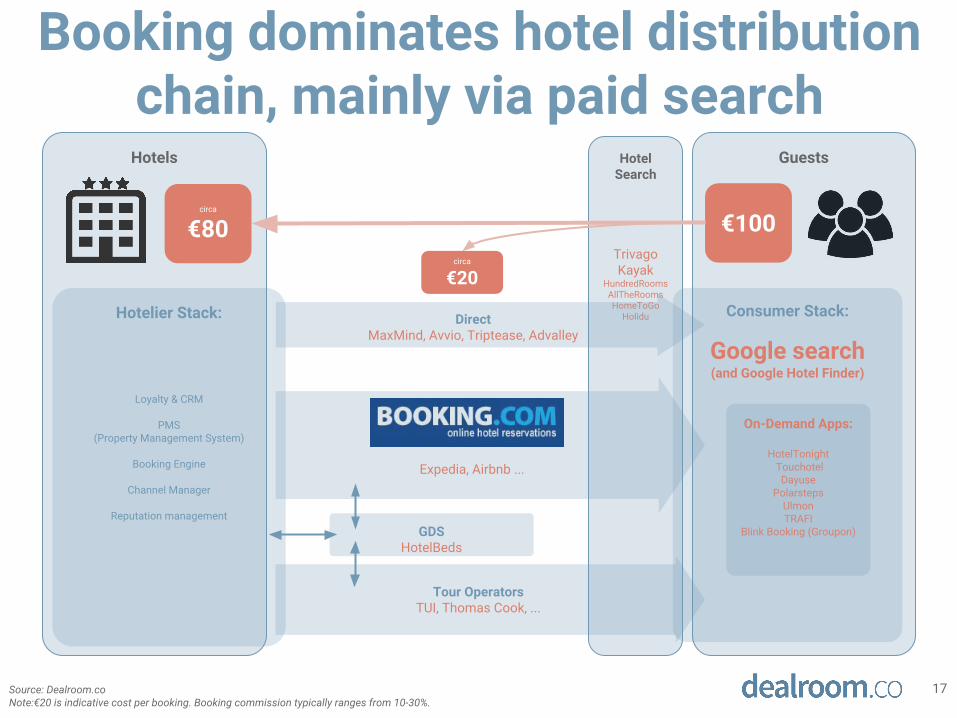

Booking dominates hotel distribution chain, mainly via paid search

17

circa

€80 €100

HotelSearch

TrivagoKayak

HundredRoomsAllTheRoomsHomeToGo

HoliduHotelier Stack:

Loyalty & CRM

PMS (Property Management System)

Booking Engine

Channel Manager

Reputation management

Direct MaxMind, Avvio, Triptease, Advalley

Expedia, Airbnb ...

Tour OperatorsTUI, Thomas Cook, ...

GDSHotelBeds

Consumer Stack:

Google search(and Google Hotel Finder)

circa

€20

Source: Dealroom.coNote:€20 is indicative cost per booking. Booking commission typically ranges from 10-30%.

On-Demand Apps:

HotelTonight Touchotel

DayusePolarsteps

UlmonTRAFI

Blink Booking (Groupon)

Buying traffic (cost per click)- Google Hotel Ads (Hotel Finder)- Trivago Direct Connect (Expedia)

- Still in somewhat experimental phase- In theory, hotel could outbid OTAs, if it can

get conversion rates on par

Online presence- Online suite & booking engine

(Avvio, BookingSuite)- Conversion optimisation (TripTease)

Walk in (= on-demand)

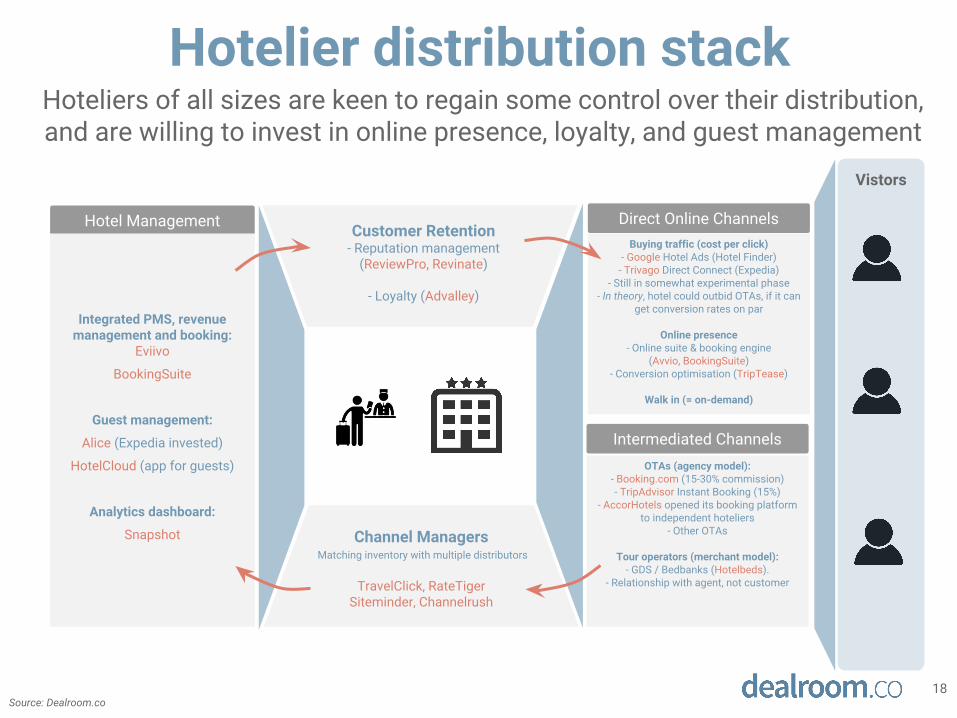

Hotelier distribution stack

18Source: Dealroom.co

OTAs (agency model):- Booking.com (15-30% commission)- TripAdvisor Instant Booking (15%)

- AccorHotels opened its booking platform to independent hoteliers

- Other OTAs

Tour operators (merchant model):- GDS / Bedbanks (Hotelbeds).

- Relationship with agent, not customer

Direct Online Channels

Intermediated Channels

Hoteliers of all sizes are keen to regain some control over their distribution, and are willing to invest in online presence, loyalty, and guest management

Vistors

Hotel Management

Channel Managers Matching inventory with multiple distributors

TravelClick, RateTigerSiteminder, Channelrush

Customer Retention- Reputation management

(ReviewPro, Revinate)

- Loyalty (Advalley)

Integrated PMS, revenue management and booking:

Eviivo

BookingSuite

Guest management:

Alice (Expedia invested)

HotelCloud (app for guests)

Analytics dashboard:

Snapshot

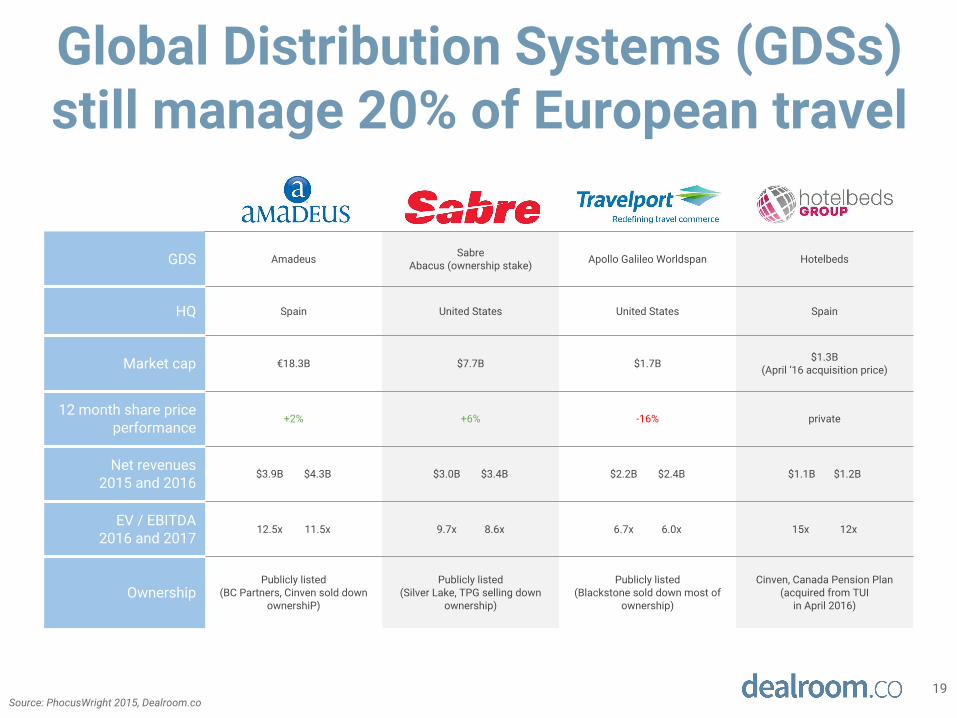

Global Distribution Systems (GDSs) still manage 20% of European travel

19

Amadeus Sabre Travelport Hotelbeds

GDS Amadeus Sabre Abacus (ownership stake) Apollo Galileo Worldspan Hotelbeds

HQ Spain United States United States Spain

Market cap €18.3B $7.7B $1.7B $1.3B(April ‘16 acquisition price)

12 month share price performance

+2% +6% -16% private

Net revenues2015 and 2016

$3.9B $4.3B $3.0B $3.4B $2.2B $2.4B $1.1B $1.2B

EV / EBITDA 2016 and 2017

12.5x 11.5x 9.7x 8.6x 6.7x 6.0x 15x 12x

OwnershipPublicly listed

(BC Partners, Cinven sold down ownershiP)

Publicly listed(Silver Lake, TPG selling down

ownership)

Publicly listed(Blackstone sold down most of

ownership)

Cinven, Canada Pension Plan (acquired from TUI

in April 2016)

Source: PhocusWright 2015, Dealroom.co

View underlying data » https://app.dealroom.co/lists/10048

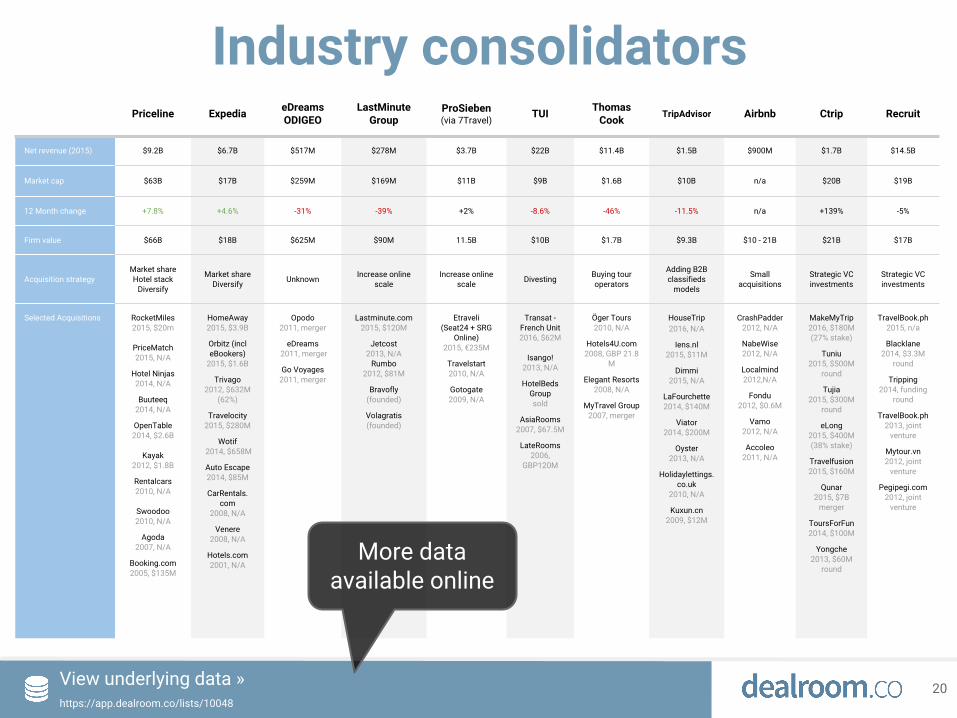

Industry consolidators

20

Priceline Expedia eDreams ODIGEO

LastMinute Group

ProSieben (via 7Travel)

TUI Thomas Cook TripAdvisor Airbnb Ctrip Recruit

Net revenue (2015) $9.2B $6.7B $517M $278M $3.7B $22B $11.4B $1.5B $900M $1.7B $14.5B

Market cap $63B $17B $259M $169M $11B $9B $1.6B $10B n/a $20B $19B

12 Month change +7.8% +4.6% -31% -39% +2% -8.6% -46% -11.5% n/a +139% -5%

Firm value $66B $18B $625M $90M 11.5B $10B $1.7B $9.3B $10 - 21B $21B $17B

Acquisition strategyMarket shareHotel stack

Diversify

Market shareDiversify Unknown Increase online

scaleIncrease online

scale Divesting Buying tour operators

Adding B2B classifieds

models

Small acquisitions

Strategic VC investments

Strategic VC investments

Selected Acquisitions RocketMiles2015, $20m

PriceMatch 2015, N/A

Hotel Ninjas 2014, N/A

Buuteeq 2014, N/A

OpenTable 2014, $2.6B

Kayak 2012, $1.8B

Rentalcars 2010, N/A

Swoodoo 2010, N/A

Agoda 2007, N/A

Booking.com 2005, $135M

HomeAway 2015, $3.9B

Orbitz (incl eBookers)

2015, $1.6B

Trivago 2012, $632M

(62%)

Travelocity 2015, $280M

Wotif 2014, $658M

Auto Escape 2014, $85M

CarRentals.com

2008, N/A

Venere 2008, N/A

Hotels.com 2001, N/A

Opodo 2011, merger

eDreams 2011, merger

Go Voyages 2011, merger

Lastminute.com 2015, $120M

Jetcost 2013, N/A

Rumbo 2012, $81M

Bravofly (founded)

Volagratis (founded)

Etraveli (Seat24 + SRG

Online) 2015, €235M

Travelstart2010, N/A

Gotogate2009, N/A

Transat - French Unit 2016, $62M

Isango!2013, N/A

HotelBeds Group sold

AsiaRooms 2007, $67.5M

LateRooms2006,

GBP120M

Öger Tours 2010, N/A

Hotels4U.com 2008, GBP 21.8

M

Elegant Resorts 2008, N/A

MyTravel Group 2007, merger

HouseTrip2016, N/A

Iens.nl2015, $11M

Dimmi2015, N/A

LaFourchette2014, $140M

Viator 2014, $200M

Oyster2013, N/A

Holidaylettings.co.uk

2010, N/A

Kuxun.cn 2009, $12M

CrashPadder 2012, N/A

NabeWise 2012, N/A

Localmind 2012,N/A

Fondu 2012, $0.6M

Vamo 2012, N/A

Accoleo 2011, N/A

MakeMyTrip2016, $180M (27% stake)

Tuniu2015, $500M

round

Tujia2015, $300M

round

eLong2015, $400M (38% stake)

Travelfusion2015, $160M

Qunar2015, $7B

merger

ToursForFun2014, $100M

Yongche2013, $60M

round

TravelBook.ph2015, n/a

Blacklane2014, $3.3M

round

Tripping2014, funding

round

TravelBook.ph2013, joint

venture

Mytour.vn2012, joint

venture

Pegipegi.com2012, joint

venture

More data available online

Fragmented European OTA landscape

21 View underlying data » https://app.dealroom.co/lists/10053

Mid-sized online tour operators will likely seek scale via strategic combinations, exits or private equity sponsored roll-up

More data available online

1. Introduction

2. Macro view

3. Strategic landscape

4. Funding & valuation data

22

Table of contents

View underlying data » https://app.dealroom.co/funding-rounds?industries=travel.must&locations=Europe.must

23

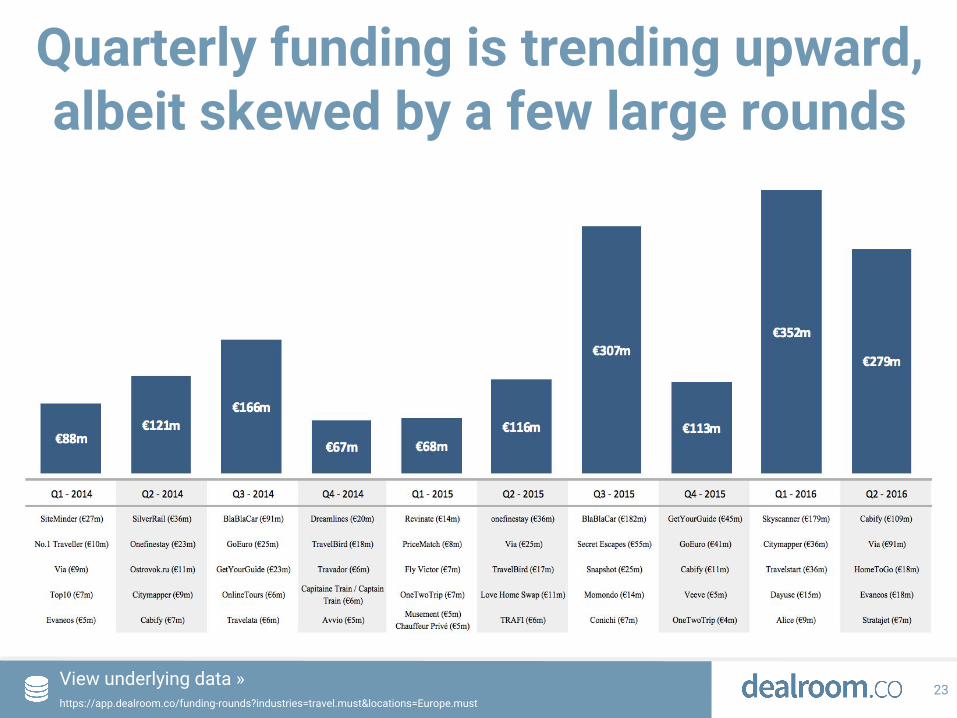

Quarterly funding is trending upward, albeit skewed by a few large rounds

View underlying data » https://app.dealroom.co/exits?industries=travel.must&locations=Europe.must

Selected recent exits

24

Date Target Acquiror Transaction Value Selling Investors Previously Invested Capital

May-16 Splendia Voyage Prive n/a Omnes Capital, Alten Capital €4.3M

May-16 Hotelbeds Group Cinven (consortium) €1.2B TUI n/a

Apr-16 HouseTrip TripAdvisor n/a Index Ventures, Balderton Capital, Accel Partners €54.3M

Apr-16 onefinestay Accor Hotels €148MPROfounders Capital, Index Ventures, Canaan Partners , Intel Capital, Accor Hotels, David Magliano

€73.5M

Mar-16 Capitaine Train / Captain Train TheTrainline.com €165MOleg Tscheltzoff, Alven Capital, Index Ventures, CM-CIC Capital Prive, TheTrainline.com, Xavier Niel

€9.6M

Feb-16 Kuoni EQT Private Equity $1.4BVeraison Capital AG, Schroders, UBS Fund Management, Classic Fund Management, Go Investment Partners

public

Nov-15 Hostelworld.com IPO €245M Hellman & Friedman €202.5M (acquisition)

Oct-15 Etraveli ProSiebenSat1 Media AG €235M Segulah Advisor AB n/a

Jan-15 TheTrainline.com KKR €450M Exponent Private Equity n/a

Mar-14 CarTrawler BC Partners, Insight Venture Partners €440M ECI Partners, founders €50M

(50% stake)

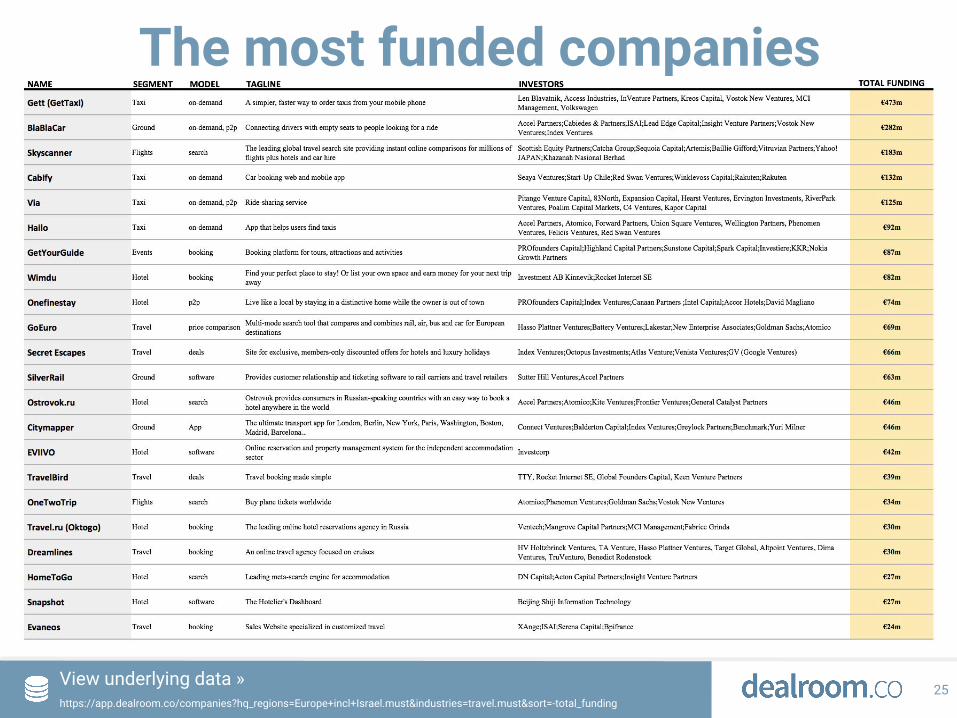

View underlying data » https://app.dealroom.co/companies?hq_regions=Europe+incl+Israel.must&industries=travel.must&sort=-total_funding

25

The most funded companies

View underlying data » https://app.dealroom.co/funding-rounds?industries=travel.must

26

The largest rounds

27

The most active funds

View underlying data » https://app.dealroom.co/markets/industries/travel/top-funds

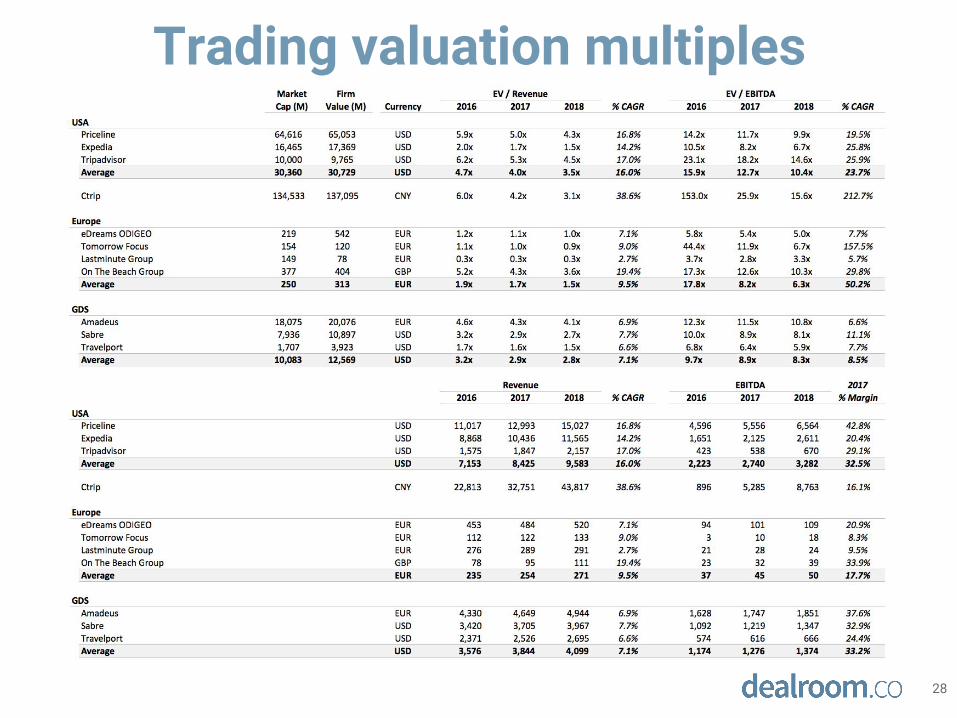

Trading valuation multiples

28

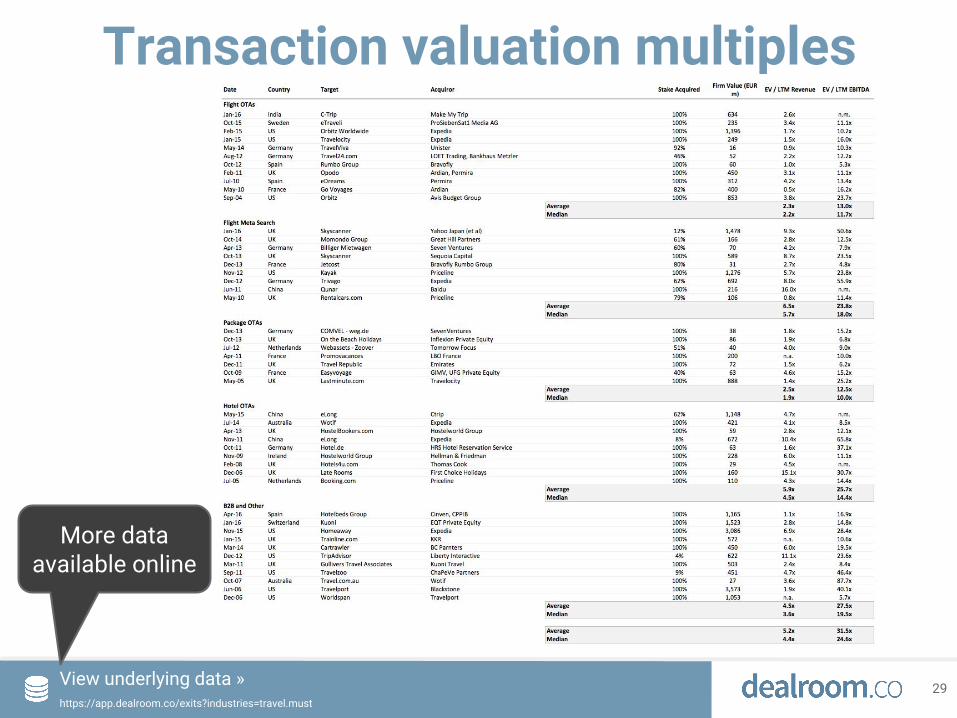

Transaction valuation multiples

29 View underlying data » https://app.dealroom.co/exits?industries=travel.must

More data available online

Rich data and analytics on private tech companies.

https://app.dealroom.co