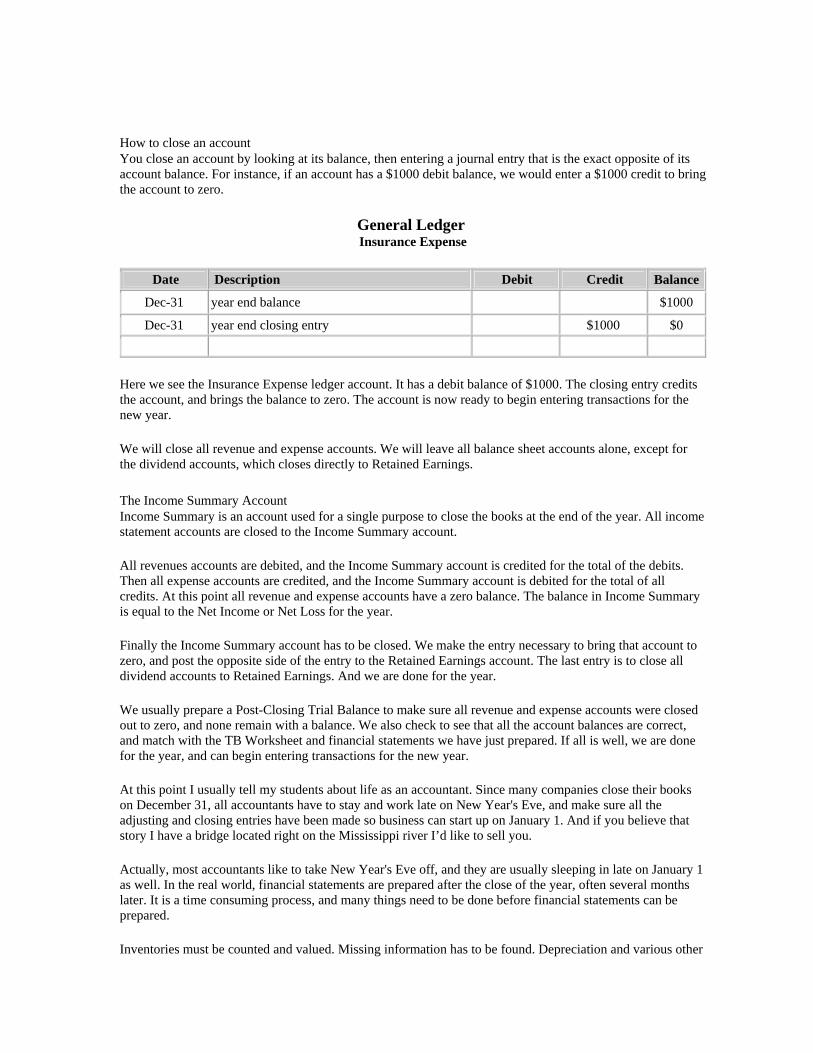

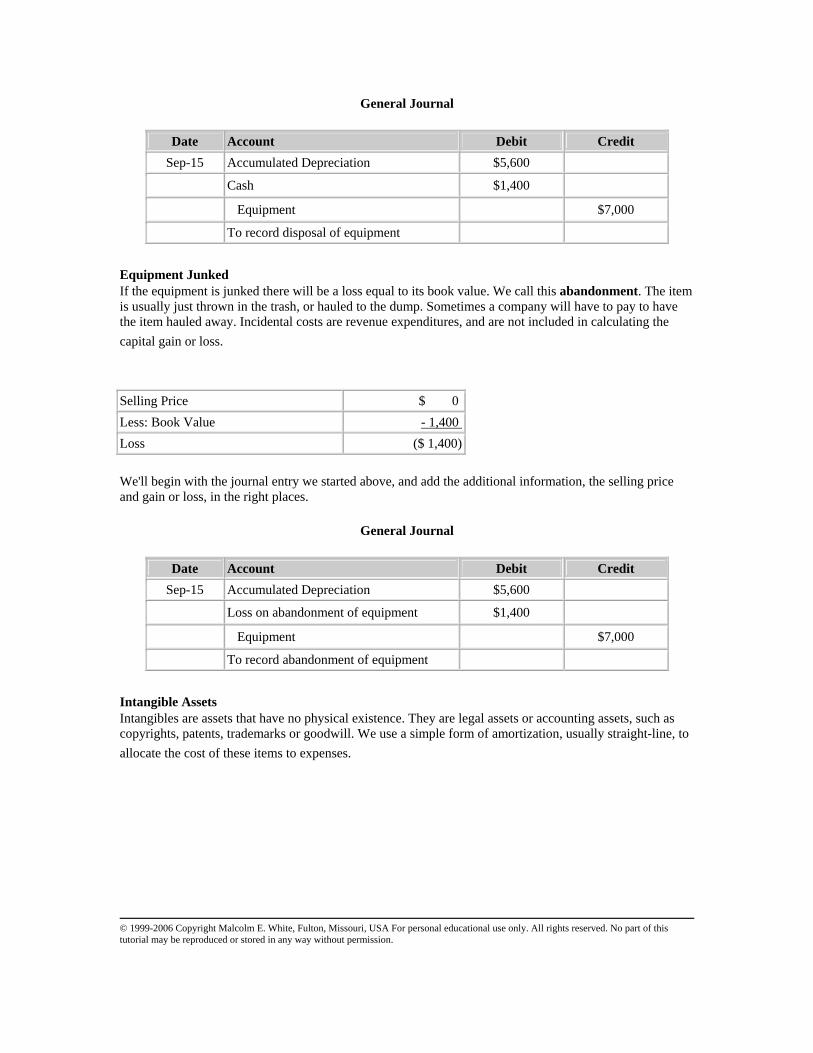

Online Accounting Tutorial

140

Online Accounting Tutorial Contents 1. Accounting – an introduction 2. Basic financial statements 3. Capturing economic events 4. Accruals and deferrals 5. Reporting financial results 6. Merchandising activities 7. Financial assets 8. Inventories and cost of goods sold 9. Plant assets and depreciation 10. Liabilities 11. Stockholders’ equity 12. Income and changes in retained earnings 13. Statement of cash flows 14. Financial statement analysis 16. Management accounting 17. Job order costing 18. Process costing 20. Cost volume profit analysis 21. Incremental analysis 23. Operational budgeting 24. Standard cost systems © 1999-2006 Copyright Malcolm E. White, Fulton, Missouri, USA For personal educational use only. All rights reserved. No part of this tutorial may be reproduced or stored in any way without permission.

description

Online Accounting Tutorial

Transcript of Online Accounting Tutorial

Online Accounting Tutorial

Contents

1. Accounting – an introduction 2. Basic financial statements 3. Capturing economic events 4. Accruals and deferrals 5. Reporting financial results 6. Merchandising activities 7. Financial assets 8. Inventories and cost of goods sold 9. Plant assets and depreciation 10. Liabilities 11. Stockholders’ equity 12. Income and changes in retained earnings 13. Statement of cash flows 14. Financial statement analysis 16. Management accounting 17. Job order costing 18. Process costing 20. Cost volume profit analysis 21. Incremental analysis 23. Operational budgeting 24. Standard cost systems

© 1999-2006 Copyright Malcolm E. White, Fulton, Missouri, USA For personal educational use only. All rights reserved. No part of this tutorial may be reproduced or stored in any way without permission.

Chapter 1 Accounting - An Introduction

A short history of accounting Luca Pacioli: The Father of Accounting Forms of Business Organizations

This tutorial is prepared for my students enrolled in Accounting Principles classes I teach for Columbia College, in the Extended Studies and Online Education divisions. It is free for anyone to use for their own personal education, but please see copyright at the bottom of the page. This tutorial is a work in progress. Caveat emptor.

Textbook used in this course: Financial and Managerial Accounting: The Basis for Business Decisions, Edition 14, Williams, et al. Irwin/McGraw-Hill, Publishers. I don't cover every topic in this tutorial. I try to hit major topics, and provide information that I would normally present in a classroom lecture. This tutorial can be used along side any accounting principles textbook. The chapter numbers may not co-incide with other textbooks but the information should be approximately the same. I do not cover FASB pronouncements in this tutorial as that information is generally covered in Intermediate Accounting, in preparation for the CPA exam and a career in accounting.

Chapter 1 introduces you to accounting as a profession, and as it is used to make financial and business decisions. Billions of dollars exchange hands every day, in millions of separate business transactions. These are recorded and reported on using a comprehensive set of guidelines, referred to as Generally Accepted Accounting Principles (GAAP).

Accounting - n. The bookkeeping methods involved in making a financial record of business transactions and in the preparation of statements concerning the assets, liabilities, and operating results of a business.1

System - n. A group of interacting, interrelated, or interdependent elements forming a complex whole.1

Accounting System - the people, procedures, and resources used to gather, record, classify, summarize and report the financial information of a business, government or other financial entity.

Double-entry bookkeeping - the practice of recording a business transaction in two equal parts, called debit and credit entries. Debit refers to the left column and credit refers to the right column, in an accounting journal.

Each transaction describes both: (1) the object of the transaction - such as rent, telephone, or payroll expense; sales, fee or interest revenue. (2) the source of payment - cash or credit.

Money eventually changes hands in (almost**) all transactions, either at the time of the transaction, or perhaps at a future date in the case of items purchased on credit. Sometimes a transaction involves cash directly, at the time of the event, such as a cash sale at a grocery store. It is more common, and safer, to use a checking account for routine purchases. These are all considered part of the Cash account.

Many, and perhaps most, transactions in a business take place on a credit basis. Businesses usually purchase their supplies and merchandise on a 30-day account, known as a trade account, or Accounts Payable. Sales are typically made in a similar fashion, called Accounts Receivable.

**Adjusting and closing entries are not typical, and represent special entries made by accountants to prepare financial statements, and reset certain accounts at the end of a fiscal year.

An Accounting history page at TAMU

Marble tablet: Account

of Disbursements of the Athenian State

c. 418-415 BC

A short history of accounting Accounting was born before writing or numbers existed, some 10,000 years ago, in the area known as Mesopotamia, later Persia, and today the countries of Iran and Iraq. This area contains the Tigris Euphrates river valley, a large fertile area 10,000 years ago with a large thriving population and active trading between towns and cities up and down the two rivers.

Writing and numbers would be not be invented for about another 5,000 years. And what happens next will directly lead to the invention of both writing and number systems.

At that time, merchants faced many of the same problems businesses face today. They had to ship their merchandise up and down the rivers, and that meant trusting a boatman with their goods. Unfortunately, not all boatmen were honest, and disagreements often arose about how much was shipped versus what was received at the other end.

It is hard for us today to imagine a world without writing and numbers. Try to imagine yourself in their position.... what would you do?

To deal with the problem, merchants came up with an ingenious plan. They made small clay tokens, in various shapes and with various markings, to indicate different products. One would mean a basket of grain, another would mean a pot of oil, etc. They had over 200 such tokens to indicate a large variety of common goods, including food, leather, clothing, utensils, tools, jewelry, etc.

Bollae and tokens circa 3300 BC

Before shipping their goods, a merchant would take one token for each item in the shipment, and encase the tokens in a ball of clay, called a "bollae" (pronounced "bowl-eye") - meaning ball. The ball would be dried in the sun, given to the boatman, and then broken by the buyer on the other end of the transaction. The buyer would match the tokens with the items in the shipment, to verify that everything sent was accounted for.

This is the function of protection of assets, and is a major function of all modern accounting systems. It was important 10,000 years ago and is just as important now. Today we see merchants doing the same thing as their counterparts 10 millennia ago - today they get a bill of lading - a listing of the merchandise entrusted to a shipper.

The system of using bollae continued for almost 5,000 years, all before the invention of writing or numbers. One day, probably by accident, a wet clay bollae was rolled over a loose token, laying on the

ground. The impression of the token was left in the wet clay. Merchants began pressing the tokens on the outside of the bollae, in addition to putting the tokens inside the ball.

Eventually they would press tokens into a flat piece of clay, leaving an impression for each item. Remember, they didn't have numbers yet, so they would press a token into the clay for each individual item. Probably by accident one day the right token couldn't be found, and someone used a stick or other object to make the right marks in the soft clay tablet. And writing was born...

New symbols were soon created representing multiple items, and suddenly both writing and number systems were invented. The last phase of this remarkable process took about 500 years, but once writing was invented, it caught on like wildfire, and was the most popular thing anyone had ever seen.

People were so much in love with writing they did it every chance they could. We have a huge amount of archaeological evidence to support this notion. Thousands of small clay tablets still survive today.

A common example: a worker sent his boss a note saying he would be late for work that day because he had chores to do. He would hire a scribe to write the tablet (only a few people could read or write), and hire a child to carry the note to his boss. They sent notes like we use the phone today, and they loved it. They wrote for the sheer joy of it - the ability to communicate at a distance.

Written accounting records are some of the oldest writings that have survived until today, and they date back to circa 3300-3200 BC. These early records were simple single-entry listings of wages paid, temple assets, taxes and tributes to the king or Pharaoh. This simple system was used until the mid-1400s, and a period known as the Renaissance.

Picture in the Tomb of Chnemhotep, pharaoh of Egypt circa 1950 BC. The ancient Egyptian scribe (seated on the left) prepared his accounts on papyrus with a calamus. The accompanying text reads "Minute care is not only taken in the case of large amounts, but even the smallest quantities of corn or dates are conscientiously entered." In ancient Egypt, the accountants were literally bean-counters. They also counted rice, beer, and everything else. Ancient Egyptians were paid in "kind" - they had not invented money yet so workers were paid with food, beer, clothing, etc. (Everyone drank beer back then, because it was more sanitary than the water. The alcohol content was very low, because they used a short brewing process. )

It is interesting to note that the Mediterranean and European nations had no concept of the number zero until the middle ages. They learned the concept of zero from Middle Eastern mathematicians, who also knew about the movements of the stars and planets, and had figured out the earth was round, and revolved around the sun in an orbit, etc. It took the Europeans another 500 years to figure that out, largely because those concepts were contrary to views held by the Roman Catholic church at the time. It's also hard to do math using Roman numerals, so their math skills were limited until they started using Arabic numbers.

c. 8500 BC c. 3500 BC c. 3000 BC c. Late 1400s merchants begin to use bollae and tokens to protect shipments

scribing marks onto wet clay replaces use of bollae & tokens

writing & number systems fully developed & in use

Luca Pacioli documents double entry accounting

Luca Pacioli links long bio short bio polyhedra

By the time Christopher Columbus was trying to sail west, a new form of accounting was in use by merchants in Venice . Luca Pacioli (pot-chee-O-lee) set down in writing for the first time a description of the double-entry system of accounting, which we still use today in much the same form. Although he didn't actually invent the system he is called "the father of accounting" for his contributions and for documenting the system in his fifth book on mathematics Summa de Arithmetica, Geometria, Proportioni et Proportionalita (Everything About Arithmetic, Geometry and Proportion).

More on Pacioli and accounting history Nice page on Luca Pacioli by TAMU

Written as a digest and guide to existing mathematical knowledge, bookkeeping was only one of five topics covered. The Summa's 36 short chapters on bookkeeping, entitled De Computis et Scripturis (Of Reckonings and Writings) were added "in order that the subjects of the most gracious Duke of Urbino may have complete instructions in the conduct of business," and to "give the trader without delay information as to his assets and liabilities" (All quotes from the translation by J.B. Geijsbeek, Ancient Double Entry Bookkeeping: Lucas Pacioli's Treatise, 1914)..

Luca Pacioli was a remarkable man. He was one of the best mathematicians of his time, and was a close friend of Leonardo DaVinci. They collaborated on many projects. Pacioli helped DaVinci lay out his painting, The Last Supper, with mathematical precision. And Leonardo illustrated Luca's books on mathematics and accounting. History is full of instances of collaboration between these two great thinkers and Renaissance men.

Modern accounting follows the same principles set down by Luca Pacioli over 500 years ago. However, today it is a highly organized profession, with a complex set of

rules for the fair disclosure and presentation of information in financial statements. Every day trillions of dollars in transactions are recorded by business, government and financial institutions world-wide. They all follow the same general set of rules.

In the United States, we follow Generally Accepted Accounting Principles (GAAP) as specified by the Financial Accounting Standards Board (FASB). We use the US Dollar for all financial statements and transactions. Other countries use similar accounting rules as the US, but there are differences from country to country. If you had a business in France, you would use the French equivalent to our GAAP.

GAAP developed over 500 years from the basic concepts Luca Pacioli set forth in the 1400s. There is a great deal of similarity in accounting practices around the world because they all have a common origin.

What accountants do.... Many people incorrectly believe that accountants' work primarily consists of bookkeeping. Most professional accountants do little or no bookkeeping. Accountants are involved in the preparation of financial statements, and the interpretation of financial information, rather than day-to-day recording of routine transactions. This work includes making sure the financial statements comply with GAAP, provide adequate disclosure of essential financial information, and are free from material errors and misstatements.

Forms of Business Organizations Sole Proprietor - One owner Partnership - 2 or more owners LLC - 1 or more owners (as allowed by state law) Corporation - unlimited number of owners (stockholders)

Legal and Business Info nolo.com

The business entity is the legal form the owners have chosen, depending on their particular needs. The legal form will determine how the company will file tax returns and the owner's individual exposure to legal liability for lawsuits brought against the company.

Corporations and LLCs both provide a layer of legal protection for the owners. Sole Proprietors and General Partners are exposed to unlimited legal liability. This is why most business are organized as corporations. The LLC form has been available in the US for about a decade, but has become a very popular business form. The number of LLCs is growing rapidly, but the predominant business form is still the corporation.

The Balance Sheet presentation and accounts used will vary depending on the way the company is organized. Sole Proprietorships use the Owner's Equity account. Corporations have accounts for stock and retained earnings. Partnerships have accounts for Partner's Capital, contributions and distributions. LLCs may be organized like a corporation or partnership, and will use the appropriate set of accounts depending on how the company is set up.

Quick Quiz State the four most common forms of business enterprises and briefly describe them.

1The American Heritage® Dictionary of the English Language, Fourth Edition, Copyright © 2000 by Houghton Mifflin Company.

© 1999-2006 Copyright Malcolm E. White, Fulton, Missouri, USA For personal educational use only. All rights reserved. No part of this tutorial may be reproduced or stored in any way without permission.

Chapter 2 Basic Financial Statements

The accounting process Financial Statements The Accounting Equation Chart of Accounts

Chapter 2 introduces you to the basic financial statements used to communicate a company's financial information to outsiders - parties other than the company's directors and managers, who are the "insiders."

What is a financial statement? What does it tell us? Why should we care? T hese are good questions and they deserve an answer.

A business is a financial entity separate from its owners. Each business must keep financial records. A number of federal and state laws require this. But even if there were no laws, it would still be a good idea anyway. Businesses provide vital goods and services to those living in the community. They provide jobs for people, and tax dollars that improve our roads, parks and schools. It is in everyone's best interest that our community's businesses be successful.

B usiness owners take a risk. What if no one wants to buy their goods or services? The owner has spent time and money to start a business, purchased land, buildings and equipment, hired people to work in the business.... all this done with the hope that the business will be successful. And if the business is NOT a success, the owner may have lost his or her life's savings, workers must find jobs, and creditors may go unpaid.

F inancial information may not make a business successful, but it helps the owner make sound business decisions. It can also help a bank or creditor evaluate the company for a loan or charge account. And the IRS will be interested in collecting the appropriate amount of income tax. So financial information will serve many purposes.

F inancial information comes in many forms, but the most important are the Financial Statements. They summarize relevant financial information in a format that is useful in making important business decisions. If this were not possible, the whole process would be a waste of time. Too much information may be equally useless. Financial statements summarize a large number of Transactions into a small number of significant categories. To be useful, information must be organized.

Quick Quiz The financial statements of a business entity: A) Include the balance sheet, income statement, and income tax return. B) Provide information about the profitability and financial position of the company. C) Are the first step in the accounting process.

D) Are prepared for a fee by the Financial Accounting Standards Board. Click for answers

Financial statements have generally agreed-upon formats and follow the same rules of disclosure. This puts everyone on the same level playing field, and makes it possible to compare different companies with each other, or to evaluate different year's performance within the same company. There are three main financial statements:

1. Income Statement 2. Balance Sheet 3. Statement of Cash Flows

Each financial statement tells it's own story. Together they form a comprehensive financial picture of the company, the results of its operations, its financial condition, and the sources and uses of its money. Evaluating past performance helps managers identify successful strategies, eliminate wasteful spending and budget appropriately for the future. Armed with this information they will be able to make necessary business decisions in a timely manner.

The accounting process in a nutshell: 1) Capture and Record a business transaction, 2) Classify the transaction into appropriate Accounts, 3) Post transactions to their individual Ledger Accounts, 4) Summarize and Report the balances of Ledger Accounts in financial statements.

There are 5 types of Accounts. 1) Assets 2) Liabilities 3) Owners' Equity (Stockholders' Equity for a corporation) 4) Revenues 5) Expenses

All the accounts in an accounting system are listed in a Chart of Accounts. They are listed in the order shown above. This helps us prepare financial statements, by conveniently organizing accounts in the same order they will be used in the financial statements.

Financial Statements The Balance Sheet lists the balances in all Asset, Liability and Owners' Equity accounts.

The Income Statement lists the balances in all Revenue and Expense accounts.

The Balance Sheet and Income Statement must accompany each other in order to comply with GAAP. Financial statements presented separately do not comply with GAAP. This is necessary so financial statement users get a true and complete financial picture of the company.

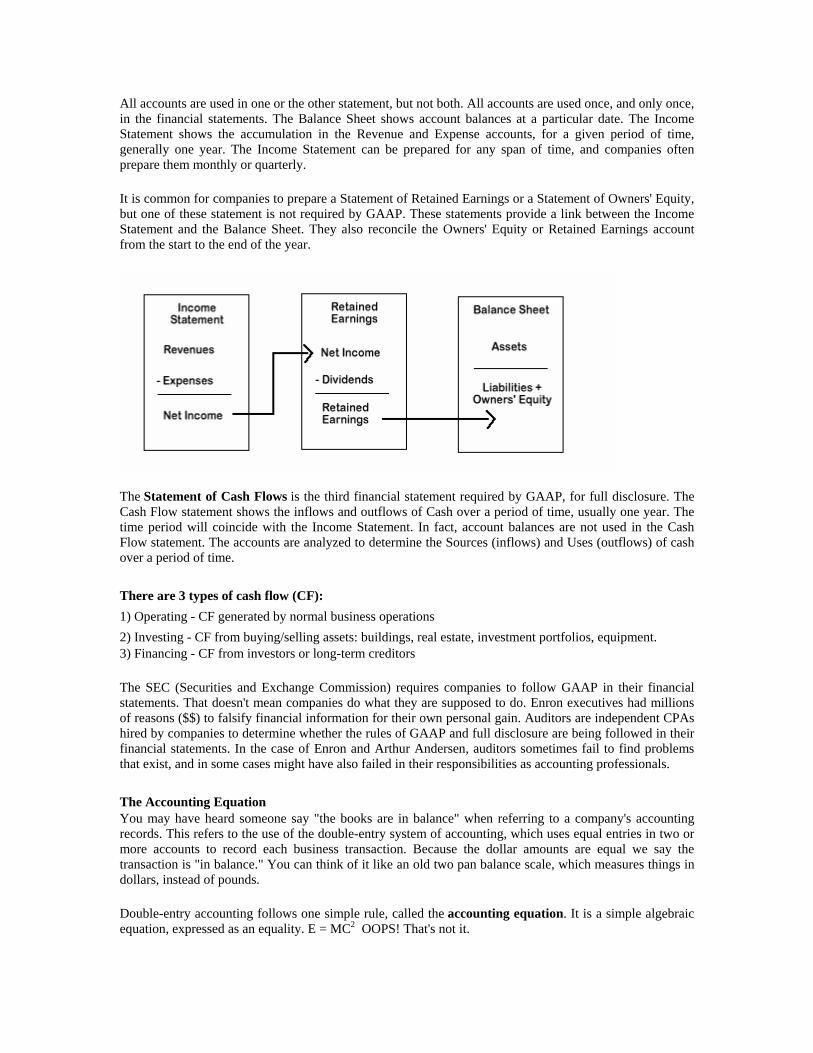

All accounts are used in one or the other statement, but not both. All accounts are used once, and only once, in the financial statements. The Balance Sheet shows account balances at a particular date. The Income Statement shows the accumulation in the Revenue and Expense accounts, for a given period of time, generally one year. The Income Statement can be prepared for any span of time, and companies often prepare them monthly or quarterly.

It is common for companies to prepare a Statement of Retained Earnings or a Statement of Owners' Equity, but one of these statement is not required by GAAP. These statements provide a link between the Income Statement and the Balance Sheet. They also reconcile the Owners' Equity or Retained Earnings account from the start to the end of the year.

The Statement of Cash Flows is the third financial statement required by GAAP, for full disclosure. The Cash Flow statement shows the inflows and outflows of Cash over a period of time, usually one year. The time period will coincide with the Income Statement. In fact, account balances are not used in the Cash Flow statement. The accounts are analyzed to determine the Sources (inflows) and Uses (outflows) of cash over a period of time.

There are 3 types of cash flow (CF): 1) Operating - CF generated by normal business operations 2) Investing - CF from buying/selling assets: buildings, real estate, investment portfolios, equipment. 3) Financing - CF from investors or long-term creditors

The SEC (Securities and Exchange Commission) requires companies to follow GAAP in their financial statements. That doesn't mean companies do what they are supposed to do. Enron executives had millions of reasons ($$) to falsify financial information for their own personal gain. Auditors are independent CPAs hired by companies to determine whether the rules of GAAP and full disclosure are being followed in their financial statements. In the case of Enron and Arthur Andersen, auditors sometimes fail to find problems that exist, and in some cases might have also failed in their responsibilities as accounting professionals.

The Accounting Equation You may have heard someone say "the books are in balance" when referring to a company's accounting records. This refers to the use of the double-entry system of accounting, which uses equal entries in two or more accounts to record each business transaction. Because the dollar amounts are equal we say the transaction is "in balance." You can think of it like an old two pan balance scale, which measures things in dollars, instead of pounds.

Double-entry accounting follows one simple rule, called the accounting equation. It is a simple algebraic equation, expressed as an equality. E = MC2 OOPS! That's not it.

The Accounting Equation really is:

Assets = Liabilities +

Owners' Equity

another way to think about it everything we own = who provided the financing

Remember in Chapter 1, I told you that each transaction describes both an object and form offinancing. In the accounting equation, Assets are the objects, and are on the Left side of the equation. Financing activities are on the Right side of the equation. Liabilities represent borrowings and credit arrangements. Owners' Equity represents investments by owners, residual net worth and retained earnings from ongoing business operations.

The accounting equation uses "simple math" and involves only addition and subtraction. In fact, almost all the math you will do in this course is simple math. We will occasionally use multiplication and division, but all changes to accounts will be addition or subtraction.

Think for a moment about a new company. It's accounting system consists of a new, "fresh" set of books, no entries have ever been made, all accounts have a zero balance.

Assets = Liabilities + Owners' Equity $0 = $0 + $0

The books are in balance!!

If each, and every, transaction is a entered as a "balanced" entry, the books will stay in balance.

There are three general types of transactions and entries. 1) Routine, daily operating events - represents over 99% of all transactions. 2) Occasional events involving major assets, liabilities and owners' equity transactions. 3) Adjusting and Closing entries - made to prepare statements and close the books at the end of the year.

Here are some examples of common type 2 transactions. Before and after each one, the books must be in balance. In Chapter 3 we will see how these are actually entered into the books, in the form of journal entries.

Owner deposits $100 in the company checking account.

Assets = Liabilities + Owners' Equity

$100 = $0 + $100 Cash is an Asset, on the Left side. Owners' Equity is on the Right side.

The amounts are equal

A $1000 computer is purchased on credit.

Assets = Liabilities + Owners' Equity $1000 = $1000 + $0

Computer is an Asset, on the Left side. A Charge account is a Liability and is on the Right side.

The owner transfers a parcel of land to the company, and signs a contract for a building to be constructed. The land is worth $10,000 and the building will cost $90,000. The building will be paid for with a bank loan.

Assets = Liabilities + Owners' Equity $100,000 = $90,000 + $10,000

Land and Building are Assets, on the Left side. Bank loan is a Liability and is on the Right side. This is a compound entry, and involves more than two accounts.

Balance Sheet accounts can increase or decrease, so you will be adding to or subtracting from their balance after each transaction.

The accounting equation can be expressed in 3 ways:

1. Assets = Liabilities + Owners' Equity 2. Liabilities = Assets - Owners' Equity 3. Owners' Equity = Assets - Liabilities

It is common to abbreviate the accounting equation as A=L+OE. Using the numbers from the balance sheet above we get the following equations:

1. 33,000 = 14,000 + 19,000 [A=L+OE] 2. 14,000 = 33,000 - 19,000 [L=A-OE] 3. 19,00 = 33,000 - 14,000 [OE=A-L]

If you know any two of the amounts you can calculate the third.

Quick Quiz Try solving these equations for practice.

Assets = Liabilities + Owners' Equity 1 ? = 27,000 + 36,000 2 426,600 = ? + 168,400

3 1,537,618 = 692,327 + ? Click for answers

Try making up several examples on your own for practice.

We can see the Accounting Equation reflected in the layout of the Balance Sheet, as shown below. Notice that Total Assets equals the sum of Total Liabilities and Total Owners' Equity, shown in boldbelow.

ABC Company Balance Sheet

December 31, 2002 Assets

Cash $ 10,000 Accounts Receivable 6,000 Inventory 17,000 Total Assets $ 33,000 <- |

Liabilities & Owners' Equity | Accounts Payable $ 6,000 E Notes Payable 8,000 Q Total Liabilities 14,000 U A Common Stock, $1 par 10,000 L Retained Earnings 9,000 | Total Owners' Equity 19,000 | Total Liabilities & Owners' Equity $ 33,000 <-

Accounts and the Chart of Accounts An Account is a record used to summarize increases and decreases in a particular asset or liability, revenue or expense, or in owner's equity. Accounts usually have very simple and generic titles such as Cash, Accounts Payable, Sales, and Inventory. These are simple and descriptive terms under which many different transactions can be recorded.

Accounts are organized in a Chart of Accounts . This is a simple list of account titles presented in the following order: Assets, Liabilities, Owners' Equity, Revenue, Expenses. Organizing accounts in the correct order makes it much easier to prepare financial statements and enter transactions.

When doing homework problems students should read carefully and look for a Chart of Accounts, or for references to specific accounts, that should be used in that problem. If you don't find these, you should review the examples in the textbook chapter material for the correct accounts to use.

Here is a sample Chart of Accounts, showing accounts in the correct order. Account group dividers are usually omitted in actual practice. They are shown here for illustrative purposes, so the student can see how the Chart of Accounts is organized, and how it relates to the financial statements.

ABC Company, Inc. Chart of Accounts

Balance Sheet Accounts ---- Asset Accounts ---- Cash Accounts Receivable Prepaid Expenses Supplies Inventory Land Buildings Vehicles & Equipment Accumulated Depreciation Other Assets ---- Liability Accounts ---- Accounts Payable Notes Payable - Current Notes Payable - Long Term ---- Stockholders' Equity Accounts ---- Common Stock Retained Earnings

Income Statement Accounts ---- Revenue Accounts ---- Sales Revenue Sales Returns & Allowances Sales Discounts Interest Income ---- Expense Accounts ---- Advertising Expense Bank Fees Depreciation Expense Payroll Expense Payroll Tax Expense Rent Expense Income Tax Expense Telephone Expense Utilities Expense

© 1999-2006 Copyright Malcolm E. White, Fulton, Missouri, USA For personal educational use only. All rights reserved. No part of this tutorial may be reproduced or stored in any way without permission.

Chapter 3 Capturing Economic Events

General Ledger Debits and Credits Normal Account Balances Journal Entries The Income Statement

Chapter 3 introduces the concepts of debit and credit, and demonstrates bookkeeping activities. After studying Chapter 3 you should be able to:

• Prepare common journal entries • Post to the Ledger accounts • Prepare a basic Income Statement

Accounting Cycle - sequence of procedures used to record, classify and summarize accounting information in financial reports, on a regular basis.

Steps in the Accounting Cycle 1) Record (journalize) transactions. 2) Post journal entries to Ledger accounts. 3) Prepare a Trial Balance. 4) Make adjusting entries. 5) Prepare an Adjusted Trial Balance. 6) Prepare financial statements. 7) Journalize and post closing entries. 8) Prepare After-Closing Trial Balance.

General Journal and Journal Entries Every business transaction is recorded in the General Journal. The General Journal is called the book of original entry. A journal is a chronological record of transactions - they are in date order. Each entry is called a journal entry, and represents a different business transaction. Each transaction is recorded once, and only once. All journal entries follow the rules of debit and credit.

Journal entries should be made contemporaneously with the event they are recording, or reasonably soon after the event. Keep in mind that a journal is a chronological record of events. A contemporaneous writing is one that takes place at the same time as the event. This is the best time to record an event, because the facts and details are still fresh in our minds. Necessary documents, conversations, calculations, etc., are readily available to create a correct record of the event. If we wait too long, the event will be much more difficult to reconstruct.

In a legal sense, a contemporaneous writing carries much more weight than a writing made at a later date. And a writing carries much more weight than a mere recollection of events, months or years after the event has taken place. The courts recognize that people's memories about events are much clearer right after the event has taken place. As to the sale of real estate, state laws require a contemporaneous writing, to establish the exact terms and conditions of the sale. In contract law, this is called a “meeting of the minds,” and must be present for a valid contract to exist.

We will use verifiable, tangible evidence whenever it exists. Tangible evidence has physical existence – we can touch it, fold, staple, copy and file the document. We will look for a check, invoice, purchase order, contract or other business document that is a record of the event, a confirmation of payment received and goods delivered, etc. These documents become the back-up documentation for our journal entry.

General Ledger Transactions are classified into accounts appropriate to the business. Accounts represent major classifications, or categories, organized according to the 5 account types covered in Chapter 2. The accounts are listed in a Chart of Accounts.

Posting - journal entries are copied to the accounts in the Ledger. After posting, the balance in each account is updated. Accounts always carry the most current balance.

Balances in Ledger accounts ==become==> Financial Statements

Books & Bookkeeping Journals and Ledgers were historically written in by hand. They were actual books, which is where many of the terms we use come from. Terms like bookkeeping, journal, balanced books, etc. all came from the days of manually recording entries in books.

Today we use computers to do the same job, but the terminology is usually the same. The concepts we follow are identical whether we use a manual or computer based accounting system. We will use the rules of debit and credit, enter transactions into the Journal, and post to the Ledger.

Debits and Credits Journals and Ledgers can be viewed as pages of a book. Each page has lines and columns. A journal page has columns for the date, account name, and two columns for dollar amounts, referred to as the Debit and Credit columns.

Sample General Journal page

Date Account Debit Credit

Debit = Left column Credit = Right column

We enter dollar amounts in the Debit and Credit columns.

The totals in the Debit and Credit columns must be equal.

Caution!! Do not confuse the concepts of debit and credit we use here, with what you read in your bank statement. Banks copy their records, and send them to you. It reflects your bank account, from the bank's perspective - which is opposite of your perspective, in an accounting sense.

Sample Ledger page Account Title

Date Description Debit Credit Balance

The Ledger page has an additional column to calculate the balance in the account. The balance is updated after each entry.

A Credit balance is usually indicated by enclosing the number in parentheses: $ (500) would indicate a $500 Credit balance.

Accounts Payable

Date Description Debit Credit BalanceJan-1 Balance forward from Dec-31 (500)

The Dollar Sign $ is usually omitted in actual practice. We will always assume that we are using the US Dollar in all transactions, journals, ledgers and financial statements.

Entries are transferred (Posted) from the journal to the ledger pages on a regular basis.

When do we use Debit or Credit? When to use a debit or credit to record a journal entry is one of the biggest problems for beginning accounting students. It doesn't have to be difficult, if you remember a few simple rules.

First, you will always use both a debit and credit. That's the idea of the double-entry system. You have two columns, so every journal entry will have an equal dollar amount in each column.

Remember the Accounting Equation?

Assets = Liabilities+Owners' Equity

Left side Right Side

Debit side Credit Side

Debit = Increase Credit = Decrease Credit = Increase

Debit = Decrease

Accounts on the Left side will INCREASE with a Debit (Left column) entry. Accounts on the Right side will INCREASE with a Credit (Right column) entry. They will each DECREASE with the OPPOSITE entry.

Refer to the Chart of Accounts to determine whether an account falls on the Left or Right side of the Accounting Equation. You will learn more about how this works as the course progresses. The textbook has many good examples.

Normal Account Balances Accounts have a normal balance - the balance they would have if increases to the account are more than decreases to the account. If the account has a balance opposite its normal balance, we say the balance is negative, in relation to what it should be. Negative in this sense does not refer to debits or credits, but to a normal or negative balance, regardless of whether that is a debit or credit balance.

You will save a lot of time making journal entries if you remember the normal balance for the accounts.

account type normal balance example

Revenue accounts credit sales revenue

Expense accounts debit rent expense

Asset accounts debit cash, accounts receivable

Liability accounts credit accounts payable

Owners' equity accounts credit capital stock

If you are recording a sale, or other income transaction, you would credit the revenue account, and debit some other account (cash or accounts receivable). If you are recording an expense, you would debit the expense account, and credit some other account.

Many transactions are so common it's easier to remember them, rather than try and think them through each time you have to record them. If you remember how to record one side of the journal entry it is fairly easy to figure out the other side from the information given, e.g.. cash sale v. credit sale.

Type of entry Do this

Record a sale credit a revenue account

Record an expense debit an expense account

Record a credit sale debit Accounts Receivable

Record a cash sale debit Cash

Buy supplies on credit credit Accounts Payable

If you refer to these charts in the beginning it will writing journal entries much easier. Soon you won't have to refer to your charts any more.

A funny accounting story (yes, there are accountant jokes) A young accountant often asked his boss for advice in writing journal entries. The boss would always open his desk drawer, look at something for a moment and then tell the young accountant how the make the correct journal entry. This went on for many years.

Finally the old accountant was ready to retire. The younger accountant asked the old man, "I don't know what I'm going to do without you. Whenever I've had a question you always knew the answer. What will I do when you're gone? And what's in your desk drawer? Every time I ask for advice you look in there?"

The old accountant took the younger one into his office and opened his desk drawer. There was a 3" x 5" index card. It said: "Debits on the Left, Credits on the Right" -----------

When you are just learning how to make journal entries, a little reminder or hint can make the task much easier. Don't try and reason out every journal entry. If you are going to replace the oil in your car, you don't have to know everything about how the engine works. You only have to find the one bolt to turn to let the oil out. Don't make the job any more difficult than it is.

As an accounting student I kept these little reminders around all the time. As a professional I've done the same thing, except with more complex issues. This is just good practice. Many of the tasks we do are very mechanical in nature. Follow a few simple rules, refer to the hints and tips.

About my student, Al (a true story) I taught at the Columbia College Jefferson City, MO Campus for several years. We had an administrative assistant there who enrolled in my accounting course. His name was Al (I didn't change the name, you know who you are ;-)

Al struggled for 7 weeks trying to understand debits & credits, and how it all fit together. Along about week 8 he was sweating bullets, and not at all comfortable about taking the comprehensive final. All sat in the front row. About the middle of the next to last class he sat up and loudly proclaimed, "I get it! I get it! I understand how it all works." He aced the final, and the course.

And then there was Mary (another true story) Mary was another student (I did change her name). She was a last semester senior, and needed accounting for her business major. This was her third attempt, and we were all hoping 3 would be a charm. At the end of the first week she told me her story, and said she had trouble with the terminology.

Mary worked in the real estate field, and had associated the term "equity" with "real property." In her mind, this was a correct association, and perhaps common slang in her office. If you look up the word equity in the dictionary, there is no association with real property. Mary was working under an incorrect definition.

In accounting real property falls under the Asset category, and equity specifically refers to Owners' Equity - the owners' claim to the business assets. This is also a dictionary definition. But Mary never could get past her own personal (incorrect) definition of equity. She dropped the course, and changed her major. She was looking at a minimum of 2 more years in school, because she got hung up on one definition.

I'm telling these stories for two reasons. First you might be another Al. The concepts we use may seem a little strange at first. But most students catch on, and usually long before the 8th week. And second, to make you aware that each discipline you study in college has its own vocabulary, terms and concepts. Some of them may be very unique to that particular field of study, and the terms may not apply anywhere else.

In the field of accounting, our terminology IS widely used. Millions of people use the same terms and concepts daily to mean the same thing. This is part of the concept of "generally accepted" - the part of GAAP that refers to common practices. Take a little time to understand the terminology you learn in this course, and it will help you for many years to come.

Accounting is nothing more than a way to organize information, so it is useful to people who have to make financial and business decisions. A large number of people use the same concepts, methods, etc. on a daily basis. You can too.

Easy Method to journal entries. Follow these simple steps. Ask yourself these questions:

1) Is Cash used in this transaction? Cash is your first Asset account, it falls on the Left side of the equation, and will be used very often. It is easy to remember the rules for the Cash account: Debit = Increase; Credit = Decrease.

2) Was Cash received or paid?

Cash Received = Increase = Debit Column = Left Column

Cash Paid = Decrease = Credit Column = Right Column

Decide whether Cash belongs in the Debit or Credit column, write the word "Cash" in the Account column, and the dollar amount in the Debit or Credit column. You are now half way done with the journal entry.

3) Enter the balancing dollar amount in the opposite column as Cash. You don't need to worry about the other account title yet. Remember that a double-entry journal entry needs equal dollar amounts in the Debit and Credit column for each journal entry. Make that dollar entry now, and you're 75% done.

4) Refer to the information given, check the Chart of Accounts, tighten your thinking bolts and select the correct account for the second part of the journal entry. Use account titles exactly as they appear in the Chart of Accounts. Don't get creative and make up account titles. If you want to be creative take an art class. (hee, hee... just kidding ;-)

5) If Cash was not used you can substitute "Cash" temporarily where it would go IF it had been used in the transaction. For instance, suppose you are at a restaurant. You could pay in cash, or charge the meal on a credit card. Either way you have paid for a meal, and the journal entry will be very similar. So you can pencil in the word "cash" lightly where it would go. After you finish the journal entry, refer to the Chart of Accounts and replace "cash" with the appropriate account, which will usually end with "Payable" or "Receivable" such as Accounts Payable, Interest Receivable, etc.

.............. The Cash account is equivalent to the company's checking account. The balance goes up when money is deposited in the account, and the balance goes down when checks are written. It works just like your checking account!

So now you know that Cash is an Asset account, is on the Left side of the accounting equation, and the balance can go up or down. The rules you use for the Cash account will be the same for all asset accounts. Now you know how to make journal entries for all asset accounts. Wasn't that easy?

Liability and Owners' Equity accounts are on the Right side of the Accounting Equation, and they follow the OPPOSITE rules as the Cash account. Now you know how to make journal entries for all those accounts! Wasn't that easy, too?

So if you can remember one thing, how the Cash account works, you can easily figure out each and every other account. Since there are only 2 sides to the Accounting Equation, there are only 2 possibilities. Pretty simple.

.............. Let's try an easy example using my simple system. Some transactions are routine and happen very frequently. It helps to know these, because they represent 99% of the total journal entries a company will make. All companies earn some sort of revenue, so let's look at a sale transaction: March 20, the company made a cash sale for $100.

1) Is Cash used in this transaction? Yes. 2) Was Cash received or paid? Received. [Increase = Debit Column] --- enter the Cash portion of the journal entry

Date Account Debit Credit Mar-20 Cash $100

The date always starts a journal entry. Enter the month once on a page, and put the day in front of each journal entry on the page, even if they are all on the same date. The day indicates the beginning of a new journal entry. You should also leave one or two blank lines between journal entries on a page.

3) Enter the balancing dollar amount in the opposite column from Cash.

Date Account Debit Credit Mar-20 Cash $100 $100

Almost done.......

4) Refer to the information given, check the Chart of Accounts, tighten your thinking bolts and select the correct account for the second part. This is a sale, so we will use Sales Revenue for the Credit side of the journal entry.

Date Account Debit Credit Mar-20 Cash $100 Sales Revenue $100

The journal entry is in balance, and is complete. The textbook will show that a memorandum can be entered on the line below the journal entry. This should be additional information that is not contained in the journal entry itself; information that will be useful when trying to reconstruct events at a later date.

.............. Another example. April 1, the company paid rent $500. 1) Is Cash used in this transaction? Yes. 2) Was Cash received or paid? Paid. [Decrease = Credit Column] --- enter the Cash portion of the journal entry 3) Enter the balancing dollar amount in the opposite column as Cash.

Date Account Debit Credit Apr-1 $500 Cash $500

Note that it is customary to enter the debit part first, and the credit entry second. The credit entry account title is indented, to help set it off from the debit account titles. These practices are used to make the journal entry easier to read, and reduce errors in posting.

4) Refer to the information given, check the Chart of Accounts, tighten your thinking bolts and select the correct account for the second part. This is an example of paying an expense, in this case Rent Expense.

Date Account Debit Credit Apr-1 Rent Expense $500 Cash $500

An important tool for accountants...

Take care of your eraser and keep it close at all times..............

Another example .... without cash. April 20, the company opens a charge account at Office Emporium. They buy a $1000 computer, and say "charge it!"

1) Is Cash used in this transaction? No. [We will use the substitution method] 2) If Cash were used...Would it be received or paid? Paid. [Decrease = Credit Column] --- enter the "cash" portion of the journal entry. Pencil "cash" in lightly, you will replace it later with the correct account title. 3) Enter the balancing dollar amount in the opposite column.

Date Account Debit Credit Apr-20 $1000 cash $1000

Notice that I have roughed in the structure of the journal entry, but the actual accounts have not been entered yet.

4) Refer to the information given, check the Chart of Accounts, tighten your thinking bolts and select the correct account for the second part. This is an example of buying equipment, in this case we will use the account Office Equipment.

5) Refer to the Chart of Accounts and replace "cash" with the appropriate account, which will usually end with "Payable" or "Receivable" such as Accounts Payable, Interest Receivable, etc.

In this case we will use Accounts Payable, one of the most frequently used accounts. Accounts Payable is used to refer to most of the common, day-to-day debts and current liabilities that a company incurs. It is short-term debt, meant to be paid soon, like the phone bill, utility bill, etc.

Date Account Debit Credit Apr-20 Office Equipment $1000 Accounts Payable $1000

These are all examples of simple journal entries. There is one debit and one credit. Some transactions might involve more then two accounts, and we would use three or more lines to write those entries. These are called compound journal entries (or complex journal entries). There is no limit to the number of debit or credit accounts that can be included in a journal entry. All necessary accounts will be used. The journal entry will balance, regardless of the number of accounts used.

Let's try an example of a compound journal entry. June 5, the company buys building and land for $100,000. They make a down payment of $20,000 and sign a mortgage note with their bank for the balance. An appraisal shows the land alone has a value of $10,000.

1) Is Cash used in this transaction? Yes & No. [We will use the substitution method along with Cash] 2) If Cash were used...Would it be received or paid? Paid. [Decrease = Credit Column] --- enter the Cash portion of the journal entry. We will use Notes Payable to enter the $80,000 we borrowed from the bank, on its own line, but on the same side as Cash - the Credit side in this case.

Date Account Debit Credit June-5

Notes Payable $80,000 Cash $20,000

3) Enter the balancing dollar amount in the opposite column. 4) Refer to the information given, check the Chart of Accounts, tighten your thinking bolts and select the correct account for the second part. I left 2 blank lines above, because I knew we had both land and a building, which must be entered separately.

Date Account Debit Credit June-5 Land $10,000

Building $90,000 Notes Payable $80,000 Cash $20,000 -------- -------- Total $100,000 $100,000

In this example I have totaled the columns to show that the journal entry is in balance. In real accounting systems a total is only drawn at the bottom of the page, not after each journal entry.

Here's another example of a compound journal entry. This one also shows how to record the issue of common stock, a very important journal entry to know. On May 1, Bill, Bob and Quinn create a new corporation, BBQ, Inc. They raise capital in the company by selling 10,000 shares of Common Stock for $5 per share. The common stock has a Par value of $1 per share.

1) Is Cash used in this transaction? Yes. The organizers are raising initial capital to start a new company. If the stock were sold on a stock exchange this would be referred to as an IPO (Initial Public Offering). 2) If Cash were used...Would it be received or paid? Received. [Increase = Debit Column] --- enter the Cash portion of the journal entry. They sold 10,000 shares of stock at $5 per share, so they have raised 10,000 x $5 = $50,000.

Date Account Debit Credit May-1 Cash $50,000

3) Enter the balancing dollar amount in the opposite column. 4) Refer to the information given, check the Chart of Accounts, tighten your thinking bolts and select the correct account for the second part. Common stock is recorded as a credit to the Common Stock account. It is recorded at Par value, in this case $1 per share. So 10,000 x $1 = $10,000.

Date Account Debit Credit May-1 Cash $50,000

Common Stock $10,000

The journal entry is out of balance and we need to finish it up. Any excess raised by the sale of stock is credited to the Additional Paid-In Capital account.

Date Account Debit Credit May-1 Cash $50,000

Common Stock $10,000 Additional Paid-In Capital $40,000

This is a good example of an important journal entry every accountant and bookkeeper should know. We don't use it very often, but it's important to know how to make this type of journal entry.

A word about issuing stock. Each state has slightly different laws regarding corporations. Most states permit Par value stock, and some have a Legal Capital rule, forcing corporations to maintain tangible capital equal to the Legal Capital. This is in place to protect stockholders. Some states permit No-Par stock.

States also allow Preferred stock, which pays a fixed dividend, similar to an interest-bearing investment. Preferred stock usually has a Par value, and is recorded as in the example above, except the Preferred Stock

account is used. Some company's maintain a separate account Additional Paid-In Capital on Preferred Stock, but Additional Paid-In Capital usually reverts to the Common stockholders, regardless of it's source.

Posting to the Ledger Journal entries must be posted to the Ledger accounts on a regular basis. In many computer based systems this is done automatically, when journal entries are made. In a manual system, and some computer systems, the journal entries are posted on a daily, weekly or monthly basis, called "batch posting."

When you Post, you simply take each line from the journal entries, and transfer the amounts to the corresponding Ledger accounts. You have to be very careful to post all journal entries, get the dollar amounts right, and enter them in the correct column of the correct account. Needless to say, in a manual system errors do get made.

Posting is actually a routine and mechanical procedure.

Using T-Accounts You will see many examples of T-Accounts in your textbook. A T-Account is just a simple way to represent a Ledger account. It's handy for accounting students, because you can make quite a few T-Accounts on one page, and post journal entries quickly. This makes it easier to do homework assignments or analyze transactions.

Most of your homework assignments will only use a few accounts, and there will only be one or two entries to each account. You can make 3 T-Accounts across a page, and several rows down the page. The Cash account should be larger than the rest, since it will have quite a few entries in most assignments.

When you post to T-Accounts, make a large T and write the name of the account above it. Write the Debit entries on the left half of the T, and Credit entries on the right side of the T. I usually draw a line underneath the entries, net all the entries together, and put the balance on the correct side of the T below the line. The Income Statement Relates to a period of time. Revenue - the price of your goods and services Expenses - costs incurred in earning revenue

Net Income - the excess of Revenue over Expenses, on the Income Statement Net Loss - the excess of Expenses over Revenue, on the Income Statement

Net Income is synonymous with Net Profit.

Debit and Credit Rules Revenues = Credit Entry Expenses = Debit Entry

All revenue and expense entries follow these simple rules. The opposite side entry is usually made only to correct an error in an earlier journal entry. This is true of all income statement accounts.

Many balance sheet accounts tend to increase and decrease on a regular basis. Cash, Inventory, Accounts Receivable, Supplies, Accounts Payable all change on a frequent basis. Income statement accounts only increase, and do so according the the rules above. It is really easy to remember this simple rule.

..... Revenue ..... Example February 3, the company makes a credit sale of $250.

Date Account Debit Credit Feb-3 Accounts Receivable $250 Sales Revenue $250

Example February 5, the company makes a cash sale of $250.

Date Account Debit Credit Feb-5 Cash $250 Sales Revenue $250

These two entries are almost identical. Notice that Sales Revenue is on the Credit side in both entries. Remember this and it will make all your journal entries easier. When you record a revenue you will put it on the Credit side.

..... Expenses ..... Example February 1, the company pays rent, $500.

Date Account Debit Credit Feb-1 Rent Expense $500 Cash $500

Example February 5, the company has an service company clean their office every week. The fee is $100 each week, and the bill is paid at the end of the month. This is the first time the office has been cleaned this month.

Date Account Debit Credit Feb-5 Office Expense $100 Accounts Payable $100

These are both examples of an Expense entry. The expense part is always in the Debit column. You will list it first, and then either Cash or Accounts Payable. An entry to record Payroll Expense would credit Wages Payable. An entry to record Interest Expense would credit Interest Payable. These are special payable accounts. Most common business expenses will credit Accounts Payable or occasionally Cash.

When to record Revenue Realization Principle - at the time goods are sold or services are rendered.

When to record Expenses Matching Principle - offsetting expenses against revenues in the appropriate time period. For instance, the bill for June's long distance phone calls is paid in July. The long distance expense should show up on the June income statement.

© 1999-2006 Copyright Malcolm E. White, Fulton, Missouri, USA For personal educational use only. All rights reserved. No part of this tutorial may be reproduced or stored in any way without permission.

Chapter 4 Accruals and Deferrals

Revenue and Expense Accruals Deferrals Depreciation Adjusting Journal Entries Correcting entries Reclassifications Reversing entries

Chapter 4 demonstrates the adjusting entries made at the end of an accounting period to prepare financial statements.

In order for revenues and expenses to be reported in the time period in which they are earned or incurred, adjusting entries must be made at the end of the accounting period. Adjusting entries are made so the revenue recognition and matching principles are followed.

Chapter 4 completes the treatment of the accounting cycle for service type businesses. It focuses on the year-end activities culminating in the annual report. These include the preparation of adjusting entries, preparing the financial statements themselves, drafting the footnotes to the statements, closing the accounts, and preparing for the audit.

Four types of adjusting entries 1) converting assets to expenses 2) converting liabilities to revenue 3) accruing unpaid expenses 4) accruing uncollected revenues

Accounting systems are designed to handle a large number of routine transactions during the year very efficiently, usually with the aid of computers and devices like scanning cash registers, bar code inventory management systems and automatic credit card processing systems. The accounting system has the built-in capability to handle these items with little human intervention, creating appropriate journal entries, and posting thousands of transactions with little effort.

However, at the end of the year accountants must step in and prepare financial statements from all the information that has been collected throughout the year. An accounting system is designed to efficiently capture a large number of transactions. But this information is only partially in accordance to GAAP. The information needs a small amount of adjustment at the end of the year to bring the financial statements in alignment with the requirements of GAAP. And this is where adjusting entries come in.

GAAP also requires certain additional information, referred to as Notes to the Financial Statement. This is a combination of narrative and numerical information that must be prepared by a real live human. Computers can do many things, but the process of preparing financial statements requires professional judgment.

Revenue and Expense As with everything else in accounting, the terms revenue and expense have definitions. They are not difficult so define, but professional judgment is required to apply the definitions correctly, and in conformity with GAAP. You need to develop a working definition for both terms.

According to FASB in SFAC No. 3, "revenue is derived from delivering or producing goods, rendering services, or other major activities of the firm.” In his book Accounting Theory, (fourth edition, Irwin), Eldon S. Hendriksen comments,

"Revenue is best measured by the exchange value of the product or service of the enterprise....we still have the problem of deciding the point or points in time when we should measure and report the revenue....[I am] in general agreement with [the] view that revenue should be acknowledged and reported at the time of the accomplishment of the major economic activity if its measurement is verifiable and free from bias.

The term revenue realization is used in a technical sense by accountants to establish specific rules for the timing of reporting revenue under circumstances where no single solution is necessarily superior to others in the above context of revenue…..The general view is that realization represents the reporting of revenue when an exchange or severance has occurred. That is, goods or services must have been transferred to a customer or client, giving rise to either the receipt of cash or a claim to cash or other assets [accounts or notes receivable]….Thus, the term realization has come generally to mean the reporting of revenue when it has been validated by sale."

There might be other times revenue will be recorded and reported, not related to making a sale. For instance, long term construction projects are reported on the percentage of completion basis. But under most circumstances, revenue will be recorded and reported after a sale is complete, and the customer has received the goods or services.

According to Hendriksen, "...expenses are the using or consuming of goods and services in the process of obtaining revenues.... Frequently, expenses are defined in terms of cost expirations or cost allocations...be careful to distinguish between the measurement of an expense based on cost and the definition of an expense as an activity or process. Emphasis on the latter has the advantage of leaving the measurement of expense open for further discussion."

At the end of the year, or anytime before financial statements are prepared, accountants have to make certain adjustments to the books to make sure that all revenues and expenses are correctly recorded and reported. This is where adjusting entries, accruals and deferrals, come in. Some companies make adjusting entries monthly, in preparation of monthly financial statements.

Accruals - conditions are satisfied to record a revenue or expense, but money has not changed hands yet. Examples:

Accounts Receivable - work done or goods sold but the customer has not yet paid us

Accounts Payable - expenses incurred but we have not yet paid the supplier

These are recorded before financial statements are prepared, so the statements reflect all revenue earned, and expenses incurred.

Example - Accrued Revenue (accounts receivable) ComputerRx repairs computers. During March they fixed a computer, but the customer not picked it up or paid by the end of the month. The total value of the work done was $200, including parts, labor, etc.

The company should record both revenue and accounts receivable for $200 each. The work was done by the end of the month. Repair technicians were paid for their time and labor. Parts used in the repairs were also paid for. The company should record both the revenue and related expenses.

General Journal

Date Account Debit Credit Mar-31 Accounts Receivable $200 Computer Repair Revenue $200

To accrue revenue from repairs made during the month.

The following month when the customer picks up the computer and pays for it, the company will record the receipt of payment as follows.

Date Account Debit Credit Apr-15 Cash $200

Accounts Receivable $200 To record receipt of payments on account.

This is a generalized example of a journal entry. Many companies use an accounts receivable subsidiary ledger to keep track of each individual customer.

Example - Accrued Expense (accounts payable) ComputerRx installs computer networks. They often hire an independent contractor to run cables for the network. They are billed twice a month at a rate of $1.50 per foot of installed cable, including parts and labor. At the end of the month they estimate the contractor installed 500 feet of cable that they had not been billed for.

The company should record an accounts payable for $750 ($1.50 x 500 ft).

General Journal

Date Account Debit Credit Mar-31 Installation Expense $750

Accounts Payable $750

To accrue installation expense at end of month.

The following month when the company pays the installer, they will record the payment, as follows.

Date Account Debit Credit

Apr-10 Accounts Payable $750 Cash $750 To record payment on account.

Note, in both examples above, the revenue or expense is recorded only once, and in the correct month. The second journal entry reflects the receipt or payment of cash to clear the account receivable or payable.

Deferrals - money has changed hands, but conditions are not yet satisfied to record a revenue or expense.

Prepaid Expenses - insurance, rent, advertising paid in advance but the expense shows up on future income statements.

Unearned Revenue - subscriptions, maintenance contracts paid in advance but the revenue shows up on future income statements.

These are recorded before financial statements are prepared, so the statements reflect all revenue earned, and expenses incurred. Let's look at a time line and see how it works.

Deferrals are often referred to as allocations. Costs are spread over a number of months using a reasonable method of allocation. In the example below, we use the straight line method - an equal amount is allocated to each month. Other reasonable methods can be used as well.

Example - Deferred Expense The company has an option of paying its insurance policy once per year, twice a year (2 installments) or monthly (12 installments). They decide to pay it twice a year, in January and July. To get a proper matching of expense to the period we spread each 6-month payment equally over the period the insurance policy covers. The effect of this is to 1) match the appropriate expense with the month it relates to, and 2) eliminate

Month> Jan Feb Mar Apr May Jun total

$ spent> $600 $0 $0 $0 $0 $0 $600

Expense taken $100 $100 $100 $100 $100 $100 $600

Money is spent only once each 6 months, but the expense is allocated to each month by enter an adjusting journal entry in the books. Here's how the first journal entry would look.

General Journal Date Account Debit Credit

Jan-2 Prepaid Insurance $600 Cash $600

To record payment of 6 months insurance policy

And the entry to record January insurance expense at the end of the month.

Date Account Debit Credit Jan-31 Insurance Expense $100 Prepaid Insurance $100 To record one month insurance policy

And finally, the Ledger accounts.

General Ledger Prepaid Insurance

Date Description Debit Credit Balance

Jan-2 $600 $600 Jan-31 $100 $500

Prepaid Insurance declines each month as the expense is transferred from the Balance Sheet to the Income Statement.

Insurance Expense

Date Description Debit Credit Balance

Jan-31 $100 $100

Example - Deferred Revenue American Artist sells subscriptions to their magazine, published 12 times a year. A subscription costs $36 per year. People can subscribe at any time during the year. They record unearned subscription revenue when payment is received for a subscription.

General Journal Date Account Debit Credit

Apr-2 Cash $36 Unearned Subscription revenue $36 To record 1 year subscription received

Each month, as issues of the magazine are mailed, the company recognizes subscription revenue. How do they calculate their total subscription revenue? Each subscription earns them $3 per month ($36/12 issues). Last month they mailed out 3000 copies of the magazine. They will recognize $9,000 in subscription revenue ($3 x 3000 copies).

General Journal

Date Account Debit Credit Apr-30 Unearned Subscription revenue $9,000 Subscription revenue $9,000 To record 1 year subscription received

In both examples above, the company is transferring a deferred cost or revenue from the balance sheet to the income statement. We call this articulation.

Depreciation Depreciation is an exaple of a deferred expense. In this case the cost is deferred over a number of years, rather than a number of months, as in the insurance example above.

In 2000 the company buys a delivery truck for 12,000. They expect the truck to last 5 years. They decide to use the straight line method, with a salvage value (SV) of $2,000. The depreciable value is $10,000 ($12,000 cost - $2,000 SV). The annual depreciation expense is $2,000 ($10,000/ 5 years).

Year> 2001 2002 2003 2004 2005 total

$ spent> $12,000 $0 $0 $0 $0 $12,000

Expense taken $2,000 $2,000 $2,000 $2,000 $2,000 $10,000

Salvage Value $2,000

At the end of 5 years, the company has expensed $10,000 of the total cost. The $2,000 salvage value remains on the books.

General Journal

Date Account Debit Credit Jan-2 Delivery Trucks $12,000 Cash $12,000 To record purchase of delivery truck

Dec-31 Depreciation Expense $2,000 Accumulated Depreciation $2,000

To record depreciation expense for the year

The straight line method is only one method used to calculate depreciation. The subject will be covered more in Chapter 9.

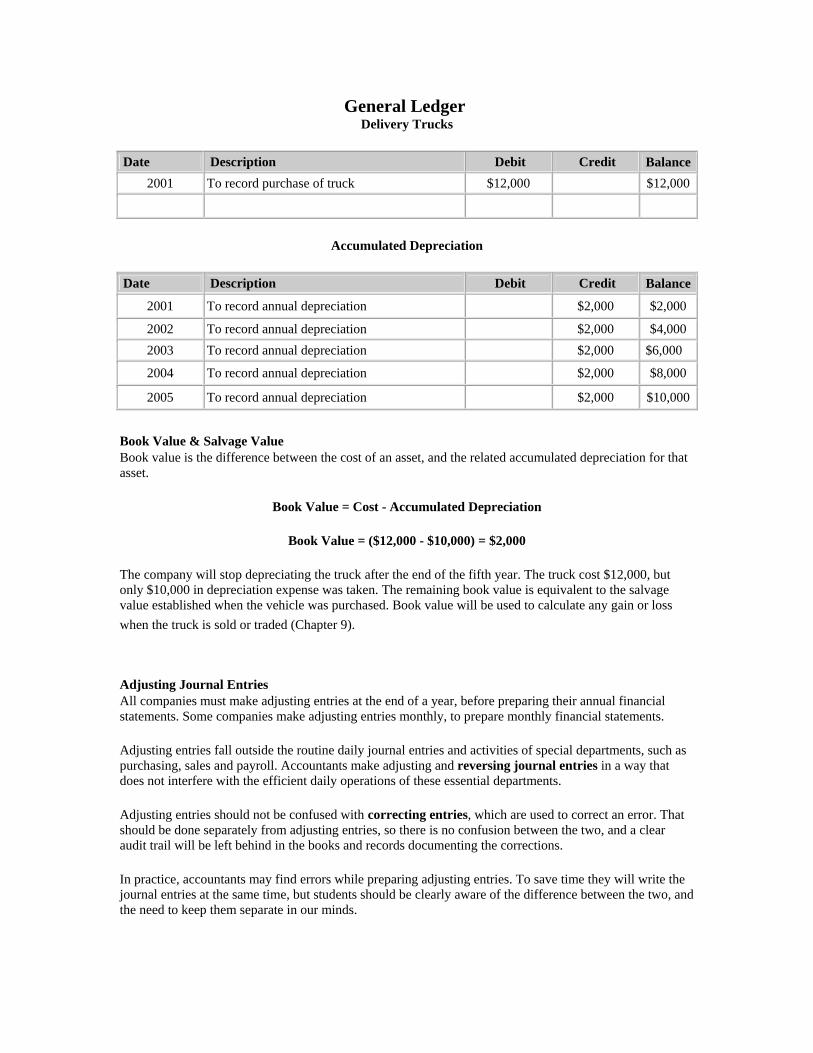

General Ledger Delivery Trucks

Date Description Debit Credit Balance2001 To record purchase of truck $12,000 $12,000

Accumulated Depreciation

Date Description Debit Credit Balance

2001 To record annual depreciation $2,000 $2,000 2002 To record annual depreciation $2,000 $4,000 2003 To record annual depreciation $2,000 $6,000 2004 To record annual depreciation $2,000 $8,000 2005 To record annual depreciation $2,000 $10,000

Book Value & Salvage Value Book value is the difference between the cost of an asset, and the related accumulated depreciation for that asset.

Book Value = Cost - Accumulated Depreciation

Book Value = ($12,000 - $10,000) = $2,000

The company will stop depreciating the truck after the end of the fifth year. The truck cost $12,000, but only $10,000 in depreciation expense was taken. The remaining book value is equivalent to the salvage value established when the vehicle was purchased. Book value will be used to calculate any gain or loss when the truck is sold or traded (Chapter 9).

Adjusting Journal Entries All companies must make adjusting entries at the end of a year, before preparing their annual financial statements. Some companies make adjusting entries monthly, to prepare monthly financial statements.

Adjusting entries fall outside the routine daily journal entries and activities of special departments, such as purchasing, sales and payroll. Accountants make adjusting and reversing journal entries in a way that does not interfere with the efficient daily operations of these essential departments.

Adjusting entries should not be confused with correcting entries, which are used to correct an error. That should be done separately from adjusting entries, so there is no confusion between the two, and a clear audit trail will be left behind in the books and records documenting the corrections.

In practice, accountants may find errors while preparing adjusting entries. To save time they will write the journal entries at the same time, but students should be clearly aware of the difference between the two, and the need to keep them separate in our minds.

Adjusting entries don't involve the Cash account. Any adjustments to Cash should be made in with the bank reconciliation (Chapter 7), or as a correcting entry.

Adjusting entries involve a balance sheet account and an income statement account. Here are some common pairs of accounts and when you would use them.

Income Statement Account Balance Sheet Account Adjustment to be made Sales Revenue (cr) Accounts Receivable (dr) Accrue unrecorded sales Earned Revenue (cr) Unearned Revenue (dr) Recognize earned revenue

Depreciation Expense (dr) Accumulated Depreciation (cr) Recognize depreciation expense

Insurance Expense (dr) Prepaid Insurance (cr) Apportion prepaid expense Interest Expense (dr) Interest Payable (cr) Accrue interest expense

Supplies Expense (dr or cr) Supplies (dr to increase, or cr to decrease account)

Recognize supplies used as an expense, and/or adjust Supplies account

Cost of Goods Sold (dr or (cr, as needed to offset Inventory adjustment)

Inventory (dr to increase, cr to decrease balance)

Adjust Inventory account to match year-end physical count

Legend: dr = debit; cr = credit; these are general rules of thumb. In all adjustments you should make the entry that is needed.

Notice most examples follow general rules: Revenues are credited, Expenses are debited, receivables are debited, payables are credited.

The Supplies or Inventory accounts need to be adjusted to reflect the physical amount of inventory or supplies at the end of the year. With Supplies we will count the physical items, for instance: 3 boxes of paper, 4 dozen pens, etc. and calculate a total value for supplies on hand, based on what we paid for the items originally. The Supplies account will be increased or decreased, as needed, to bring it to the correct balance.

Correcting entries A correcting entry should be entered whenever an error is found. If errors are found at the end of the year, while preparing financial statements, accountants usually go ahead and correct the error at that time. There are various reasons a correction might be needed. A wrong account or dollar amount might have been entered. The entry could have used a debit, when a credit should have been entered.

Errors will carry through to the financial statements, so it is important to detect and correct them. The type of error should be noted, and brought to management's attention, if the accountant feels the error might be intentional. Intentional errors are called "falsifications" and are an indication there might be fraud.

Reclassifications A reclassification is a correction entry used to correct a mis-classification or to change the classification of

an entry. This might be necessary if an entry is made without complete information. For instance, the company might purchase a building and land for a single price. The two assets need to be entered separately. The company may have to wait for an appraisal, and will make a journal entry to record the purchase, then reclassify a portion of the purchase price to allocate the correct values to the land and building.

Reversing entries A reversing entry is a very special type of adjusting entry. They can be extremely useful and should be used where necessary. A reversing entry comes in two parts: the original adjusting entry, and the reverse, or opposite entry. The second entry is written by simply reversing the position of all debits and credits. Ultimately, the end result on the books is zero, but the adjusting entry serves to correctly allocate an expense, so the financial statements are correct.

Let's look at an example. X Company has a payroll department, and cuts checks every two weeks after tabulating hours, and calculating net pay. A large number of allocations have to be made to various withholding accounts. The accountants don't want to interfere with the operations of the payroll department. And the employees also want the department to run efficiently so they can get their pay checks on time.

At the end of the year the accountants need to appropriately allocate payroll expenses, plus taxes due and payable. Rather than interfere with the payroll department the calculation is made on paper (or computer), and entered as an adjusting entry. It is marked to be reversed. After the closing entries are made, the first entries of the new year are the reversing entries. They undo the effects of the adjusting entry.

If the adjusting entry is not reversed, the books will not be correct. Both the accountants and payroll department will be making entries related to payroll. The reversing entry effectively allows the accountants to make adjusting entries without causing the books to be incorrect; the payroll department continues to make routine entries, and doesn't need to make any special entries or allocations.

Until you actually work with reversing entries they seem strange. Here's how the numbers play out. Let's look at a really simple example.

X Company's payroll expense is $1,500 per week; they pay salaries every two weeks. Assume that December 31 falls at the end of the week, and in the middle of the pay period. The payroll expense for the two week period needs to be split between two years, with $1,500 in year 1 and $1,500 in year 2.

Total for 2 week payroll = $3000

This is how the expense should be allocated: Dec 31

Last week of year 1 First week of year 2 $1500 $1500

This is the journal entry the payroll department will make Dec 31

Last week of year 1 First week of year 2 $0 $3000

At the end of the first week in January the payroll department will make its journal entry to record the two week payroll. But that journal entry will be for $3000, and not $1500 as it should be. Two things need to