Onion & Garlic - Home - OLAM SVIolamsvi.com/downloads/market-report-onion-garlic-feb-2016.pdf ·...

7

market report FEBRUARY 2016 Onion & Garlic Dehydrated Onion Market Summary 2016 US onion crop planting progressing well; ‘El Nino’ having benefic impact on CA snowpack and precipitation; Chopped/ minced and ELB powder fraction availability to remain tight through mid-2016; Indian Kharif (winter) crop acreage reportedly down ~25%, but up ~10-15% in Gujarat, Maharashtra and M.P. – main areas for the dehydration crop; dehydrated onion prices attractive for the moment; if monsoons are normal, weakness could extend to Q3; Egypt winter crop output down ~20%; however, fresh and dehydrated onion prices range bound momentarily, due to weak fresh market demand; EU seeing tight fresh onion availability and accompanied pricing volatility in Q1 2016 driven by reduced end of season inventories and lower planted acreage in 2016. Impact likely to follow through on dehydrated onion pricing as well. USA Onion planting for the 2016 crop is currently in progress. Planted acreage is estimated to be up marginally over last year as a direct result of the shortened 2015 harvest. Planting is complete in the desert (S. California), Kern and early Westside regions. Oregon and Northern California will see planting commence in March and April. Meanwhile, the onset of “El Nino” this season has been quite benefic for California’s agriculture as of date. December and January have seen high pressure weather systems over California’s Central Valley regularly breached by moisture-heavy low pressure systems from the Pacific. Precipitation levels have been decent for this time of the year and the snow pack formation has improved. (See chart below). Reservoir levels however, are still well below normal. The forward weather outlook is cautiously optimistic. Federal water allocations for the past two years (2014, 2015) have been at an unprecedented zero percent; however, allocations for 2016 are speculated to be slightly better than last year’s level. It should be noted however, that while rain will help alleviate drought conditions, several consecutive years of significant precipitation and snowpack will be needed to replenish California’s aquifers and reservoirs. Buyer contracting for the 2014-15 season is largely complete. New contracting will start only by mid-2015.

Transcript of Onion & Garlic - Home - OLAM SVIolamsvi.com/downloads/market-report-onion-garlic-feb-2016.pdf ·...

marketreport FEBRUARY 2016

Onion & Garlic

Dehydrated Onion

Market Summary2016 US onion crop planting progressing well; ‘El Nino’ having benefi c impact on CA snowpack and precipitation; Chopped/ minced and ELB powder fraction availability to remain tight through mid-2016; Indian Kharif (winter) crop acreage reportedly down ~25%, but up ~10-15% in Gujarat, Maharashtra and M.P. – main areas for the dehydration crop; dehydrated onion prices attractive for the moment; if monsoons are normal, weakness could extend to Q3; Egypt winter crop output down ~20%; however, fresh and dehydrated onion prices range bound momentarily, due to weak fresh market demand; EU seeing tight fresh onion availability and accompanied pricing volatility in Q1 2016 driven by reduced end of season inventories and lower planted acreage in 2016. Impact likely to follow through on dehydrated onion pricing as well.

USAOnion planting for the 2016 crop is currently in progress. Planted acreage is estimated to be up marginally over last year as a direct result of the shortened 2015 harvest. Planting is complete in the desert (S. California), Kern and early Westside regions. Oregon and Northern California will see planting commence in March and April.

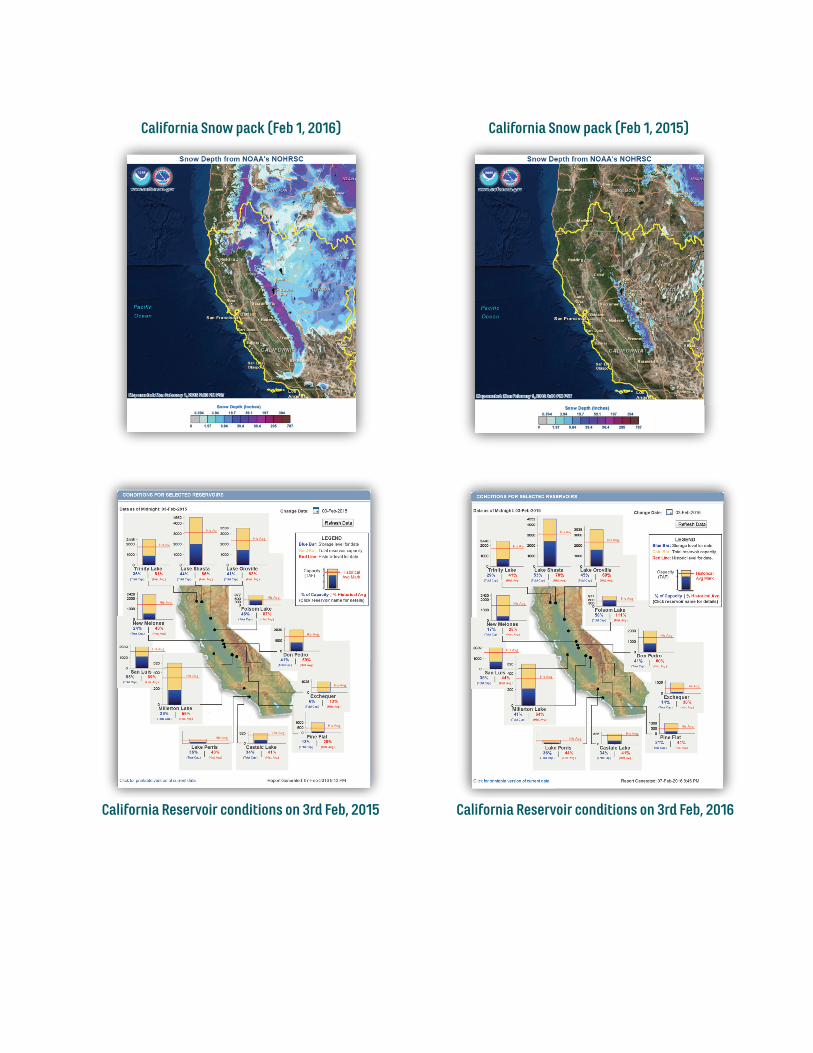

Meanwhile, the onset of “El Nino” this season has been quite benefi c for California’s agriculture as of date. December and January have seen high pressure weather systems over California’s Central Valley regularly breached by moisture-heavy low pressure systems from the Pacifi c. Precipitation levels have been decent for this time of the year and the snow pack formation has improved. (See chart below). Reservoir levels however, are still well below normal. The forward weather outlook is cautiously optimistic. Federal water allocations for the past two years (2014, 2015) have been at an unprecedented zero percent; however, allocations for 2016 are speculated to be slightly better than last year’s level. It should be noted however, that while rain will help alleviate drought conditions, several consecutive years of signifi cant precipitation and snowpack will be needed to replenish California’s aquifers and reservoirs.

Buyer contracting for the 2014-15 season is largely complete. New contracting will start only by mid-2015.

California Snow pack (Feb 1, 2016) California Snow pack (Feb 1, 2015)

California Reservoir conditions on 3rd Feb, 2015 California Reservoir conditions on 3rd Feb, 2016

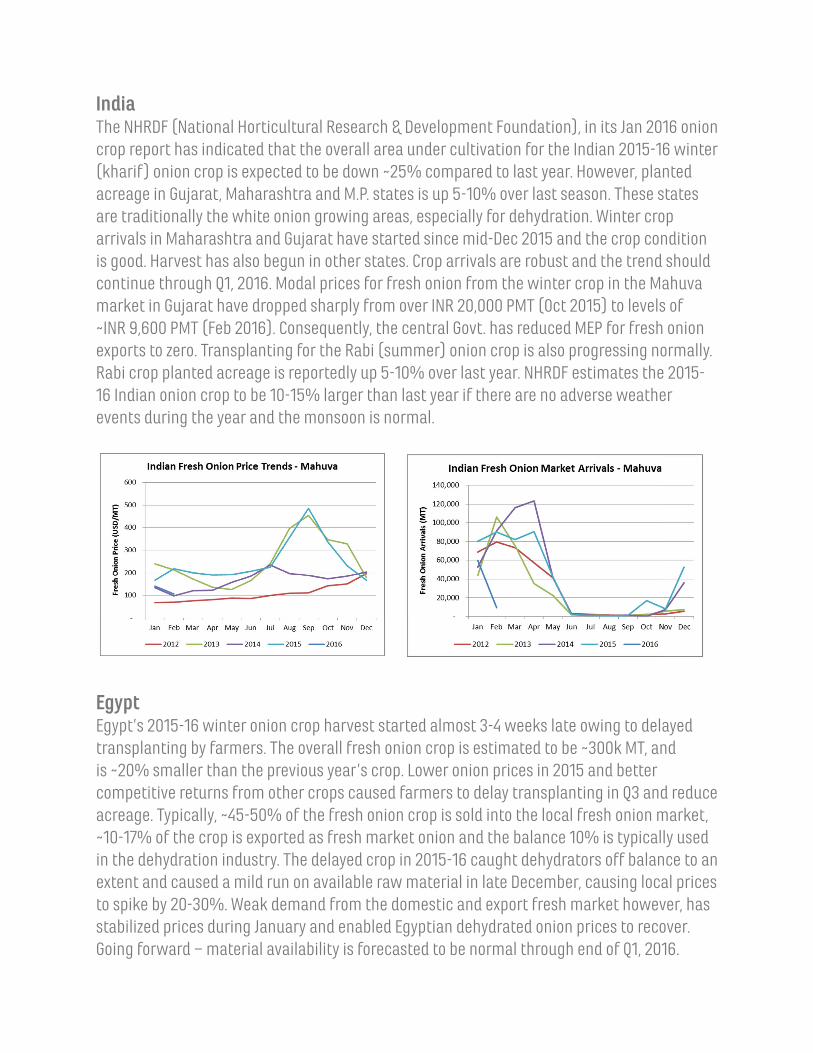

IndiaThe NHRDF (National Horticultural Research & Development Foundation), in its Jan 2016 onion crop report has indicated that the overall area under cultivation for the Indian 2015-16 winter (kharif) onion crop is expected to be down ~25% compared to last year. However, planted acreage in Gujarat, Maharashtra and M.P. states is up 5-10% over last season. These states are traditionally the white onion growing areas, especially for dehydration. Winter crop arrivals in Maharashtra and Gujarat have started since mid-Dec 2015 and the crop condition is good. Harvest has also begun in other states. Crop arrivals are robust and the trend should continue through Q1, 2016. Modal prices for fresh onion from the winter crop in the Mahuva market in Gujarat have dropped sharply from over INR 20,000 PMT (Oct 2015) to levels of ~INR 9,600 PMT (Feb 2016). Consequently, the central Govt. has reduced MEP for fresh onion exports to zero. Transplanting for the Rabi (summer) onion crop is also progressing normally. Rabi crop planted acreage is reportedly up 5-10% over last year. NHRDF estimates the 2015-16 Indian onion crop to be 10-15% larger than last year if there are no adverse weather events during the year and the monsoon is normal.

EgyptEgypt’s 2015-16 winter onion crop harvest started almost 3-4 weeks late owing to delayed transplanting by farmers. The overall fresh onion crop is estimated to be ~300k MT, and is ~20% smaller than the previous year’s crop. Lower onion prices in 2015 and better competitive returns from other crops caused farmers to delay transplanting in Q3 and reduce acreage. Typically, ~45-50% of the fresh onion crop is sold into the local fresh onion market, ~10-17% of the crop is exported as fresh market onion and the balance 10% is typically used in the dehydration industry. The delayed crop in 2015-16 caught dehydrators off balance to an extent and caused a mild run on available raw material in late December, causing local prices to spike by 20-30%. Weak demand from the domestic and export fresh market however, has stabilized prices during January and enabled Egyptian dehydrated onion prices to recover. Going forward – material availability is forecasted to be normal through end of Q1, 2016.

FUTURE OUTLOOK

USA• Supply shortfalls possible in chopped, minced and ELB fractions in H1 2016 • Buyers urged to work with suppliers and manage forecasts regularly to prevent stock-outs• 3-5% increase in re-contract pricing likely for 2016-17• Early re-contracting recommended

Europe• Tight availability in H1 2016 with corresponding pricing volatility• Supply gaps to be filled from India, China and Egypt

Egypt• CY2015-16 short winter crop could put upward pressure on pricing by the end Q1• Crop quality however is excellent, especially on color and low micro levels• Short/medium term coverage should be considered, especially for low micro/premium grades

India• 2015-16 winter crop pricing and availability to be favorable to last year• If monsoons are normal, lower prices could extend into H2, 2016• Medium to long term coverage should be strongly considered

China• Carry in Inventories are adequate• Chinese RMB weakness could throw up cost saving opportunities

EuropeEuropean fresh onion carry in inventories into 2016 are expected to be lower than levels seen in a traditional year. The second half of 2015 saw a sharp increase in exports of onion driven by a favorable exchange rate. Consequently, end of season inventories are low and prices have moved up as a result. The continued export ban to Russia has forced EU growers to reduce planted acreage for 2016.

ChinaChina’s 2015-16 white onion crop has come in slight better than plan as the growing regions were not affected by adverse weather events. Production is estimated at ~16k MT. Summer crop planting is expected to be unchanged from last year.

Dehydrated Garlic

Market SummaryChinese dehydrated garlic prices rose sharply in mid-Dec 2015 despite planted acreage increase of 8-10% in 2016 garlic crop; low 2016 carry-in fl ake inventory and reduced crop expectations due to excessive cold weather in Dec/Jan are the main causes; unconfi rmed reports of potential peanut allergen contamination in Chinese garlic both in Europe as well as USA; issue causing some retail customers to shift over to US garlic, thereby putting pressure on limited garlic supplies. Spot US garlic prices spike 30-35% in Jan 2016 due to demand surge and tight inventory; availability across all fractions to remain tight through mid-2016 due to shortened 2015 crop; 2016 US garlic crop planting progressing normally.

ChinaContrary to market sentiment, local dehydrated garlic prices rose sharply in Dec 2015 to levels not seen since 2012. On Jan 4, 2016, fl ake prices crossed the RMB 19,000 PMT mark from levels of RMB 14.500 PMT prevailing in mid Dec 2015. This increase of ~30% is unprecedented augurs a tough period ahead. A combination of events has caused this market development and can be explained as follows:• Chinese fresh garlic production for CY 2015 was ~4.4-4.6 Mill. MT – lower than the

traditional 5 M MT benchmark• Estimated carry in inventory of fl ake at the beginning of the CY 2015 was ~90k MT • Total fl ake production in CY 2015 was ~95k MT, lower than the typical 100-150k MT

benchmark • Total fl ake availability for 2015-16 exports is therefore ~185k MT • Jan-Dec 2015 dehydrated garlic exports from China were ~178k MT. From this - ~78k MT

was exported during July –Dec 2015 and expected exports during Jan –June 2016 should be at least 80-85k MT (basis the export fi gures for 2014). Total exports for 2015-16 would therefore be ~158-163k MT

• This leaves the eff ective carry out inventory as of July 1 , 2016 at very low levels of ~22-27k MT. Total inventory of dehydrated garlic as of date is therefore only adequate to service export volumes through mid-2016

• New fl aking in 2016 can really be carried out only post Sept 2016 due to weather constraints. There is therefore a likelihood of a severe shortage in Q3, 2016

FUTURE OUTLOOK

Chinese Garlic• Chinese fl ake and dehydrated garlic prices should remain fi rm through Q3, 2016 • Current demand for fl ake is fi rm and driven more from intermediate exporters/ traders who short-

ed the market in 2015 in anticipation of lower fl ake prices post Chinese New year. Unfortunately – the lower carry in stocks into 2016 are now causing concerns and leading to tightening of prices

• Allergen related rejections and CBP/ FDA enforcement could cause supply disruptions • Higher exchange rate volatility • Shipment delays and defaults maybe a possibility• 2016 planted acreage expected to be 7-8% higher than last year • If 2016 crop is normal, prices could correct downwards by end of Q3 CY• Immediate coverage through Q3, 2016 is recommended, through reliable counter-parties

US Garlic• Supply shortfalls possible in H1 2016• If the supply squeeze from China prolongs beyond Q1, the current price increase in US garlic will

intensify further• Immediate coverage through new crop is recommended

USAThe US 2016 garlic crop planting is in progress. Despite a shortened crop in 2015, planted acreage for the 2016 crop has not increased and remains roughly the same as last year. Uncertainty over California’s water situation and anticipation of a larger Chinese 2016 harvest had forced a more cautious approach from US dehydrators and prevented them from raising production levels. However, with support from “El Nino”, a normal garlic crop can be expected.

January 2016 saw an abnormal increase in spot demand for US dehydrated garlic and caused prices to spike by ~30-40% over levels prevailing in December. This was driven by unconfi rmed reports of potential peanut allergen contamination in Chinese garlic both in Europe as well as USA. The issue has resulted in a serious concern over supply, causing a prudent shift to US garlic, thereby increasing pressure on current US garlic supplies

February 9, 2016For clarifications, doubts, comments – please contact your SVI Account manager for details.