On Local Government Indiana’s Property Tax, 2008 Larry DeBoer Purdue University February 1, 2008.

30

On Local Government Indiana’s Property Tax, 2008 Larry DeBoer Purdue University February 1, 2008

-

date post

21-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of On Local Government Indiana’s Property Tax, 2008 Larry DeBoer Purdue University February 1, 2008.

On Local Government

Indiana’s Property Tax, 2008

Larry DeBoerPurdue UniversityFebruary 1, 2008

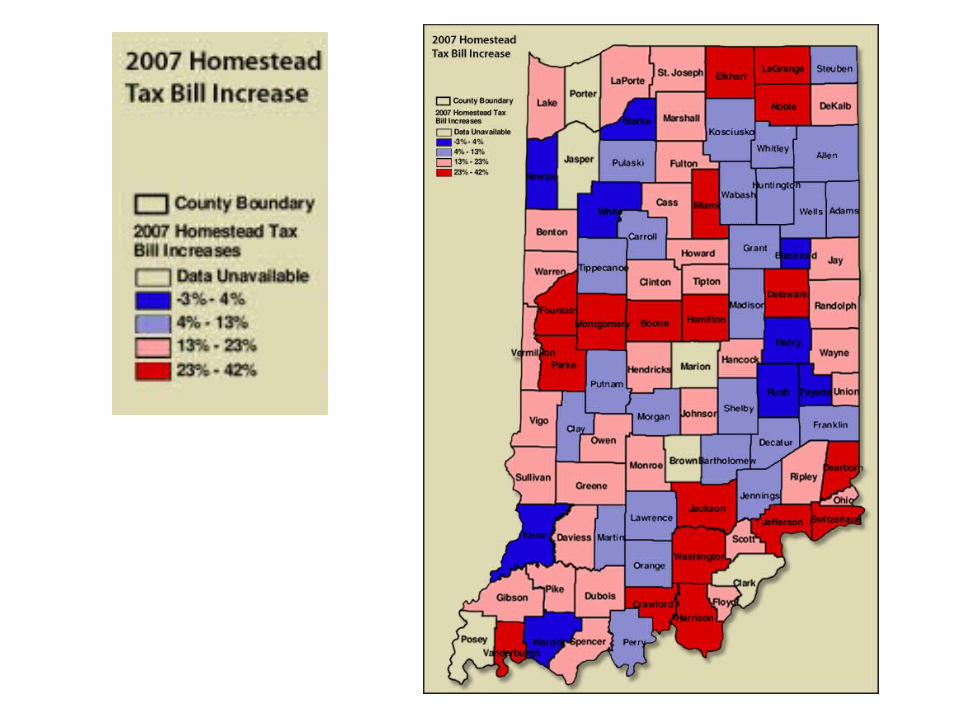

Homeowner Property Taxes, 2008

Total estimated average increase in homeowner taxes, statewide 8%Trending from 2005 to 2006 prices

1%Cap on state tax relief 1%$50 million homestead credit reduction to $250 million 4%Increases in local government tax collections 3%Farmland base rate increase from $880 to $1,140 -1%

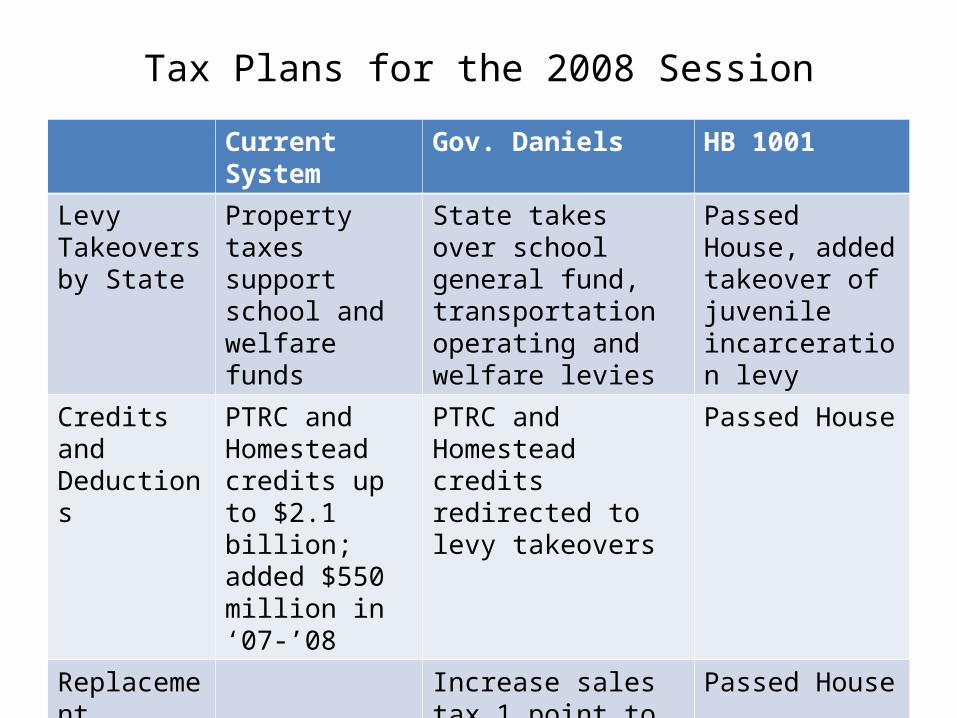

Tax Plans for the 2008 Session

Current System Gov. Daniels HB 1001

Levy Takeovers by State

Property taxes support school and welfare funds

State takes over school general fund, transportation operating and welfare levies

Passed House, added takeover of juvenile incarceration levy

Credits and Deductions

PTRC and Homestead credits up to $2.1 billion; added $550 million in ‘07-’08

PTRC and Homestead credits redirected to levy takeovers

Passed House

Replacement Revenue

Increase sales tax 1 point to 7%

Passed House

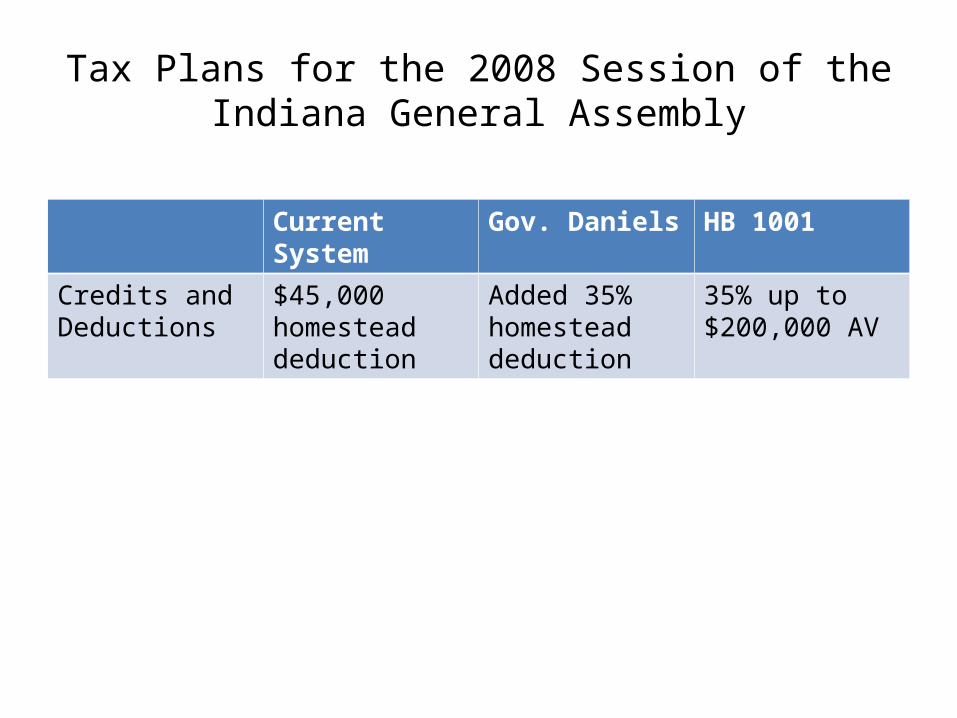

Tax Plans for the 2008 Session of the Indiana General Assembly

Current System Gov. Daniels HB 1001

Credits and Deductions

$45,000 homestead deduction

Added 35% homestead deduction

35% up to $200,000 AV

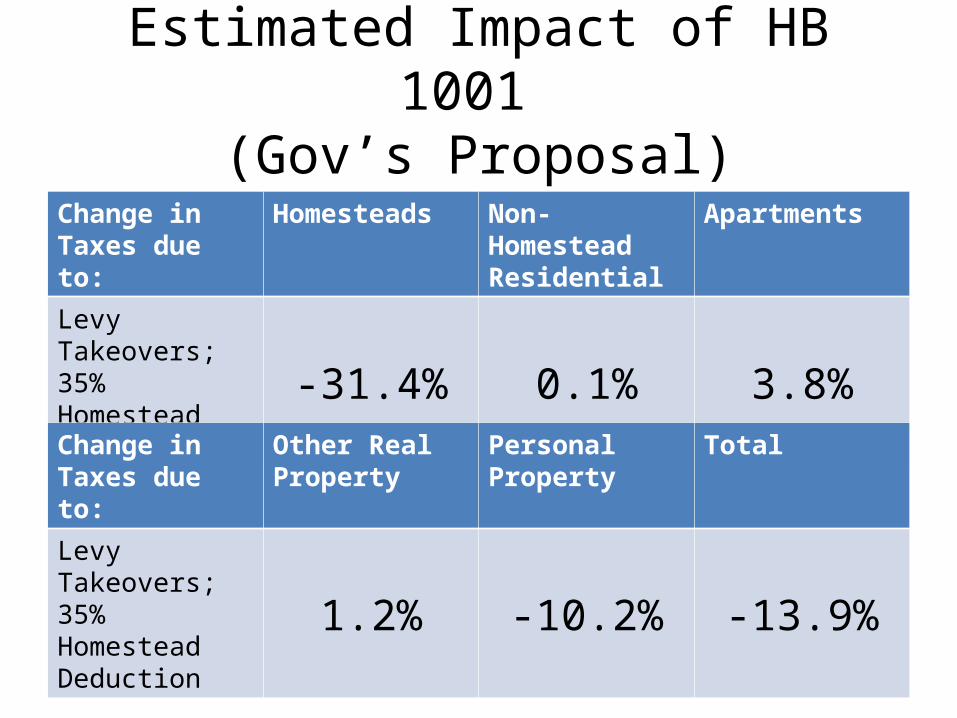

Change in Taxes due to:

Homesteads Non-Homestead Residential

Apartments

Levy Takeovers; 35% Homestead Deduction

-31.4% 0.1% 3.8%

Change in Taxes due to:

Other Real Property

Personal Property

Total

Levy Takeovers; 35% Homestead Deduction

1.2% -10.2% -13.9%

Estimated Impact of HB 1001 (Gov’s Proposal)

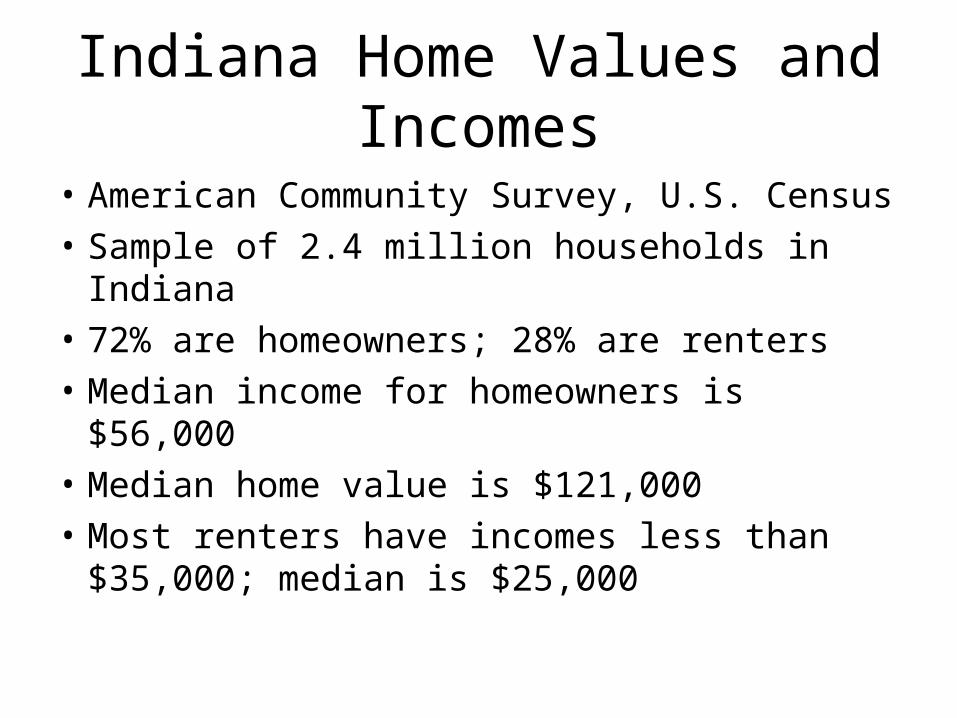

Indiana Home Values and Incomes

• American Community Survey, U.S. Census• Sample of 2.4 million households in Indiana• 72% are homeowners; 28% are renters• Median income for homeowners is $56,000• Median home value is $121,000• Most renters have incomes less than $35,000;

median is $25,000

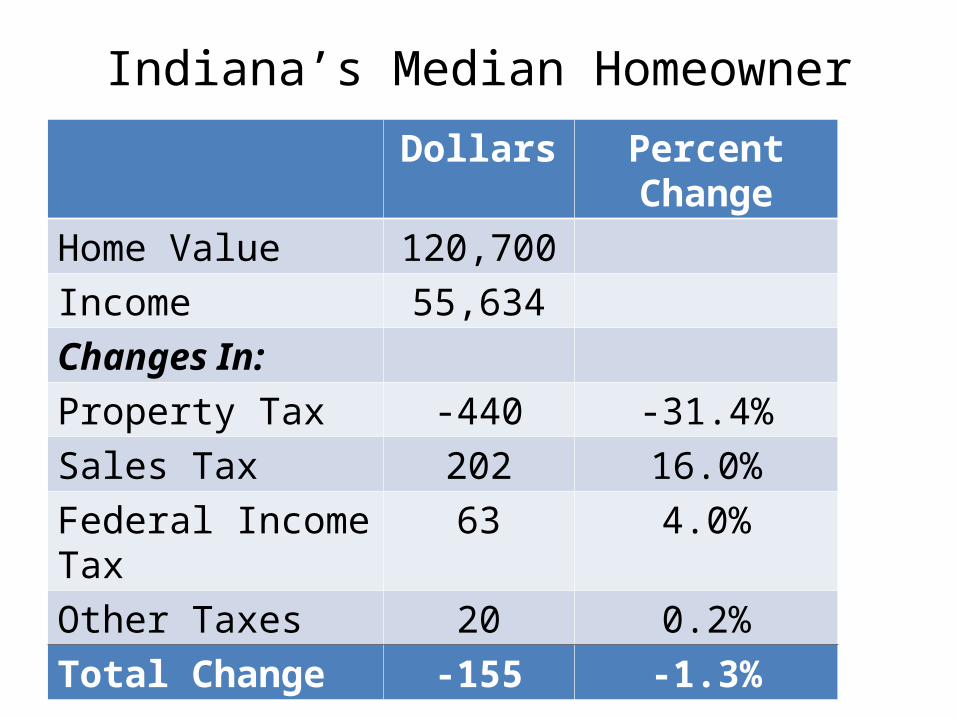

Indiana’s Median Homeowner

Dollars Percent ChangeHome Value 120,700Income 55,634Changes In:Property Tax -440 -31.4%Sales Tax 202 16.0%Federal Income Tax 63 4.0%Other Taxes 20 0.2%Total Change -155 -1.3%

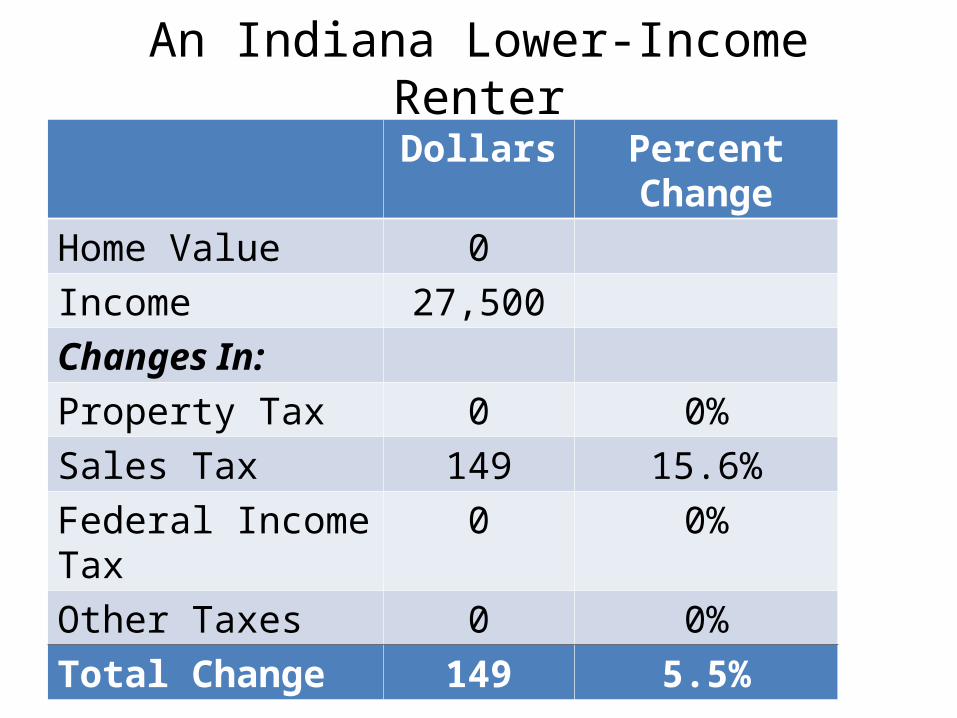

An Indiana Lower-Income Renter

Dollars Percent ChangeHome Value 0Income 27,500Changes In:Property Tax 0 0%Sales Tax 149 15.6%Federal Income Tax 0 0%Other Taxes 0 0%Total Change 149 5.5%

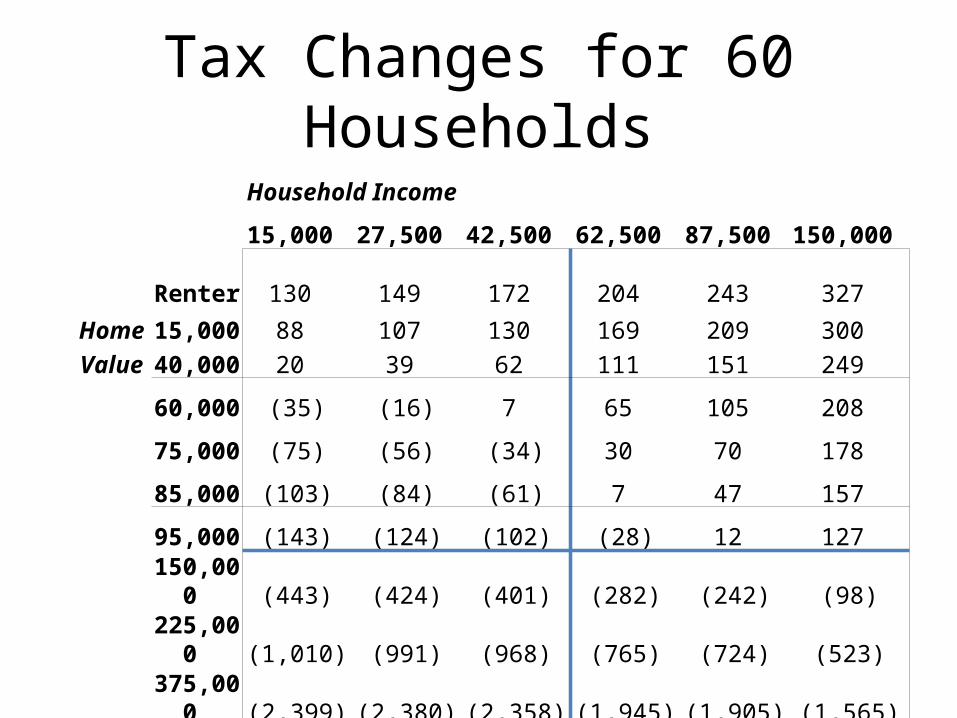

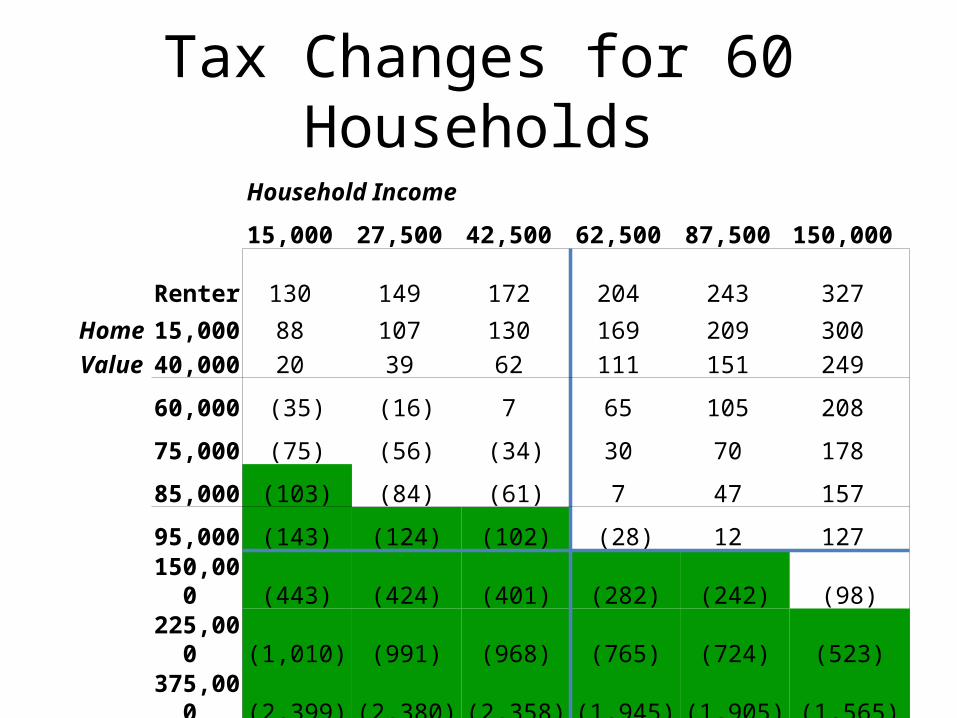

Tax Changes for 60 HouseholdsHousehold Income

15,000 27,500 42,500 62,500 87,500 150,000

Renter 130 149 172 204 243 327

Home 15,000 88 107 130 169 209 300

Value 40,000 20 39 62 111 151 249

60,000 (35) (16) 7 65 105 208

75,000 (75) (56) (34) 30 70 178

85,000 (103) (84) (61) 7 47 157

95,000 (143) (124) (102) (28) 12 127

150,000 (443) (424) (401) (282) (242) (98)

225,000 (1,010) (991) (968) (765) (724) (523)

375,000 (2,399) (2,380) (2,358) (1,945) (1,905) (1,565)

Tax Changes for 60 HouseholdsHousehold Income

15,000 27,500 42,500 62,500 87,500 150,000

Renter 130 149 172 204 243 327

Home 15,000 88 107 130 169 209 300

Value 40,000 20 39 62 111 151 249

60,000 (35) (16) 7 65 105 208

75,000 (75) (56) (34) 30 70 178

85,000 (103) (84) (61) 7 47 157

95,000 (143) (124) (102) (28) 12 127

150,000 (443) (424) (401) (282) (242) (98)

225,000 (1,010) (991) (968) (765) (724) (523)

375,000 (2,399) (2,380) (2,358) (1,945) (1,905) (1,565)

Tax Changes for 60 HouseholdsHousehold Income

15,000 27,500 42,500 62,500 87,500 150,000

Renter 130 149 172 204 243 327

Home 15,000 88 107 130 169 209 300

Value 40,000 20 39 62 111 151 249

60,000 (35) (16) 7 65 105 208

75,000 (75) (56) (34) 30 70 178

85,000 (103) (84) (61) 7 47 157

95,000 (143) (124) (102) (28) 12 127

150,000 (443) (424) (401) (282) (242) (98)

225,000 (1,010) (991) (968) (765) (724) (523)

375,000 (2,399) (2,380) (2,358) (1,945) (1,905) (1,565)

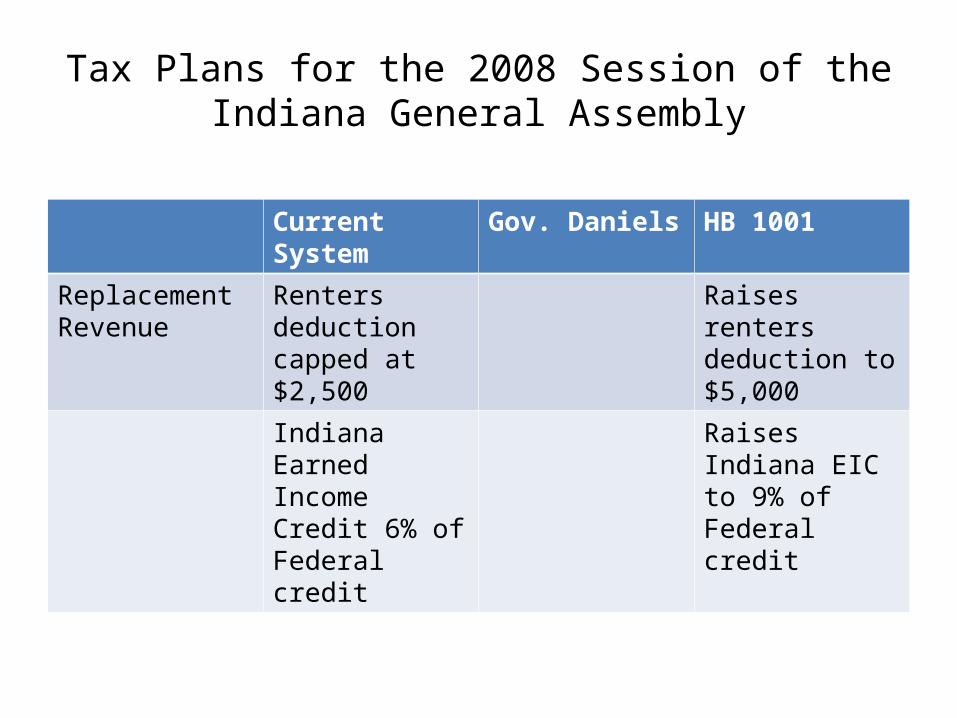

Tax Plans for the 2008 Session of the Indiana General Assembly

Current System Gov. Daniels HB 1001

Replacement Revenue

Renters deduction capped at $2,500

Raises renters deduction to $5,000

Indiana Earned Income Credit 6% of Federal credit

Raises Indiana EIC to 9% of Federal credit

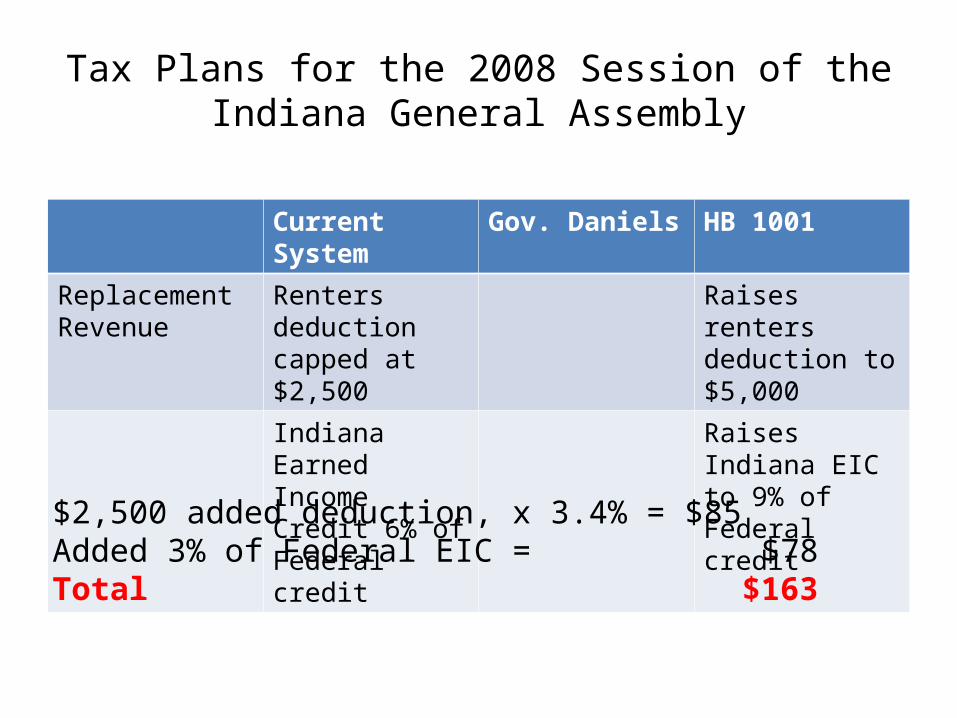

Tax Plans for the 2008 Session of the Indiana General Assembly

Current System Gov. Daniels HB 1001

Replacement Revenue

Renters deduction capped at $2,500

Raises renters deduction to $5,000

Indiana Earned Income Credit 6% of Federal credit

Raises Indiana EIC to 9% of Federal credit

$2,500 added deduction, x 3.4% = $85Added 3% of Federal EIC = $78Total $163

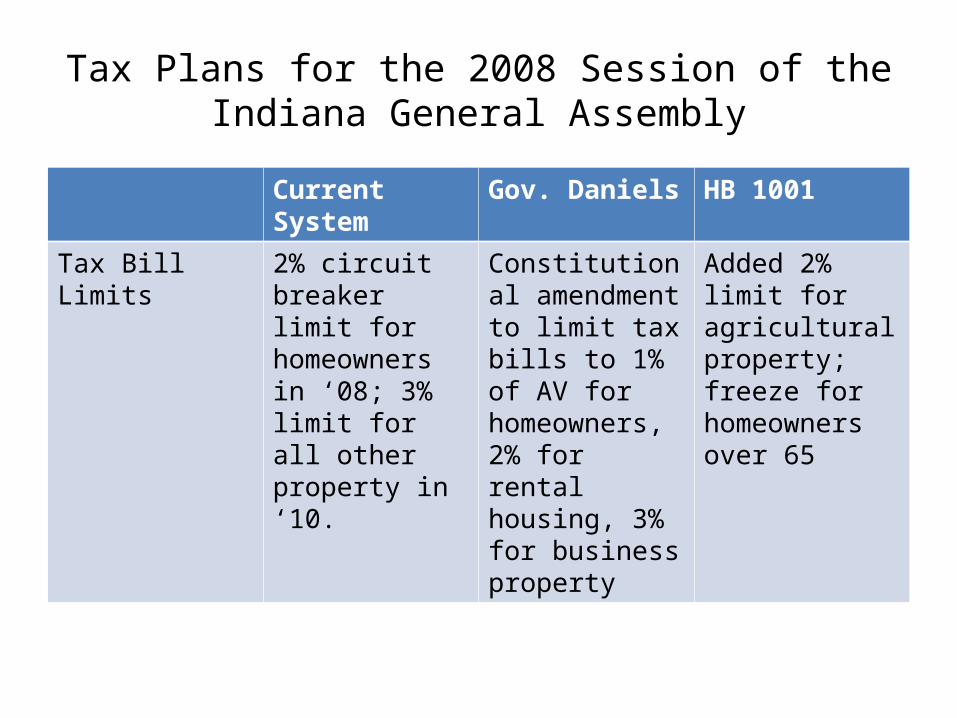

Tax Plans for the 2008 Session of the Indiana General Assembly

Current System Gov. Daniels HB 1001

Tax Bill Limits 2% circuit breaker limit for homeowners in ‘08; 3% limit for all other property in ‘10.

Constitutional amendment to limit tax bills to 1% of AV for homeowners, 2% for rental housing, 3% for business property

Added 2% limit for agricultural property; freeze for homeowners over 65

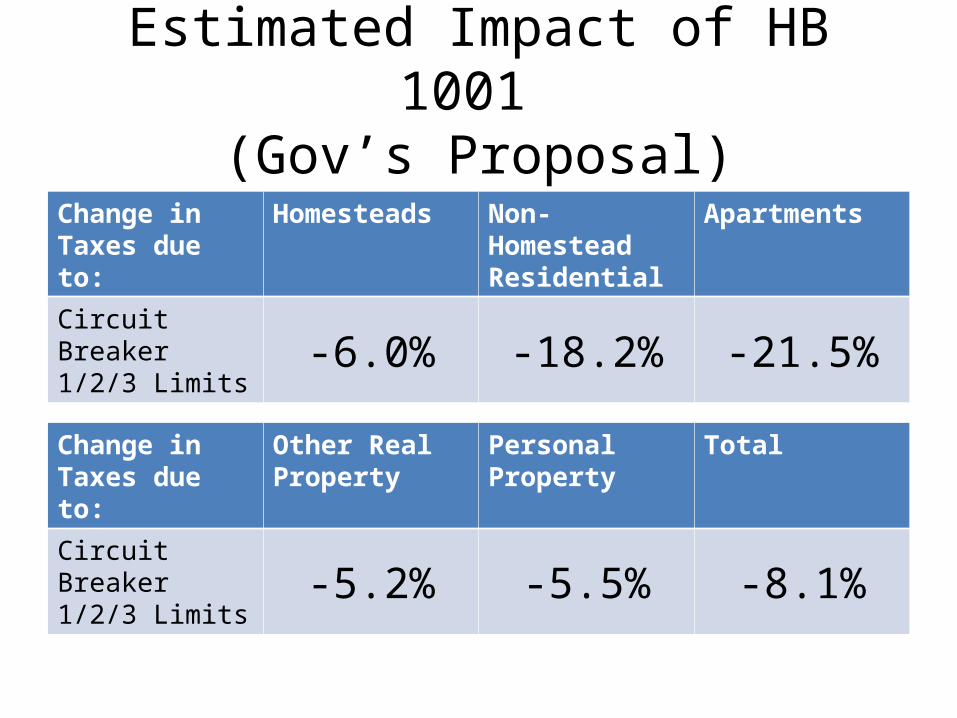

Change in Taxes due to:

Homesteads Non-Homestead Residential

Apartments

Circuit Breaker 1/2/3 Limits -6.0% -18.2% -21.5%

Change in Taxes due to:

Other Real Property

Personal Property

Total

Circuit Breaker 1/2/3 Limits -5.2% -5.5% -8.1%

Estimated Impact of HB 1001 (Gov’s Proposal)

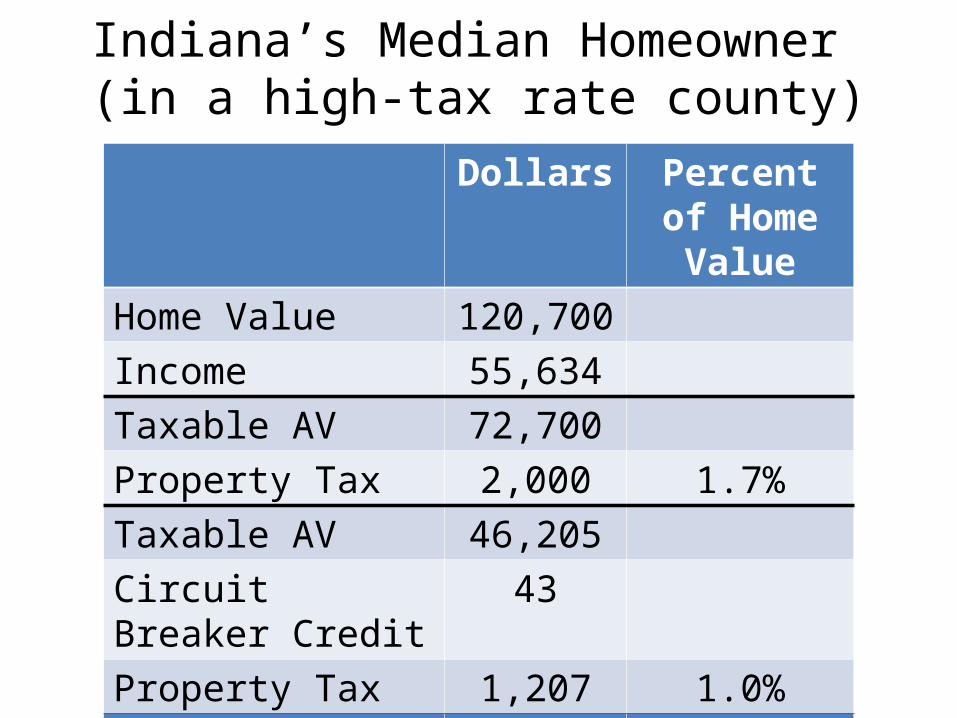

Indiana’s Median Homeowner (in a high-tax rate county)

Dollars Percent of Home Value

Home Value 120,700Income 55,634Taxable AV 72,700Property Tax 2,000 1.7%Taxable AV 46,205Circuit Breaker Credit

43

Property Tax 1,207 1.0%Percent Change -39.7%

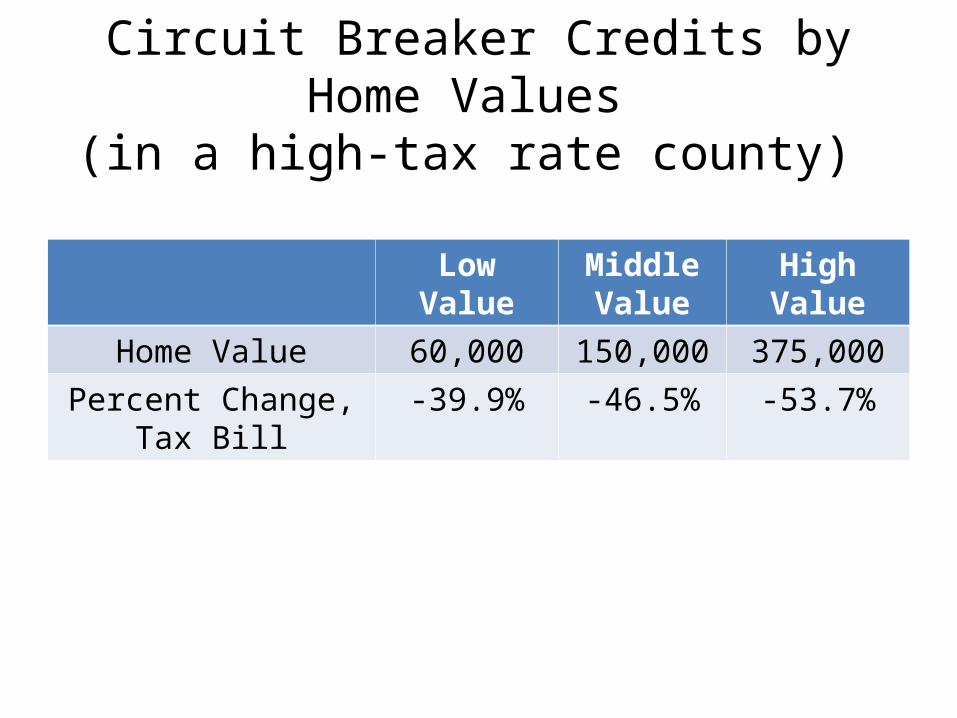

Circuit Breaker Credits by Home Values (in a high-tax rate county)

Low Value Middle Value

High Value

Home Value 60,000 150,000 375,000Percent Change, Tax

Bill-39.9% -46.5% -53.7%

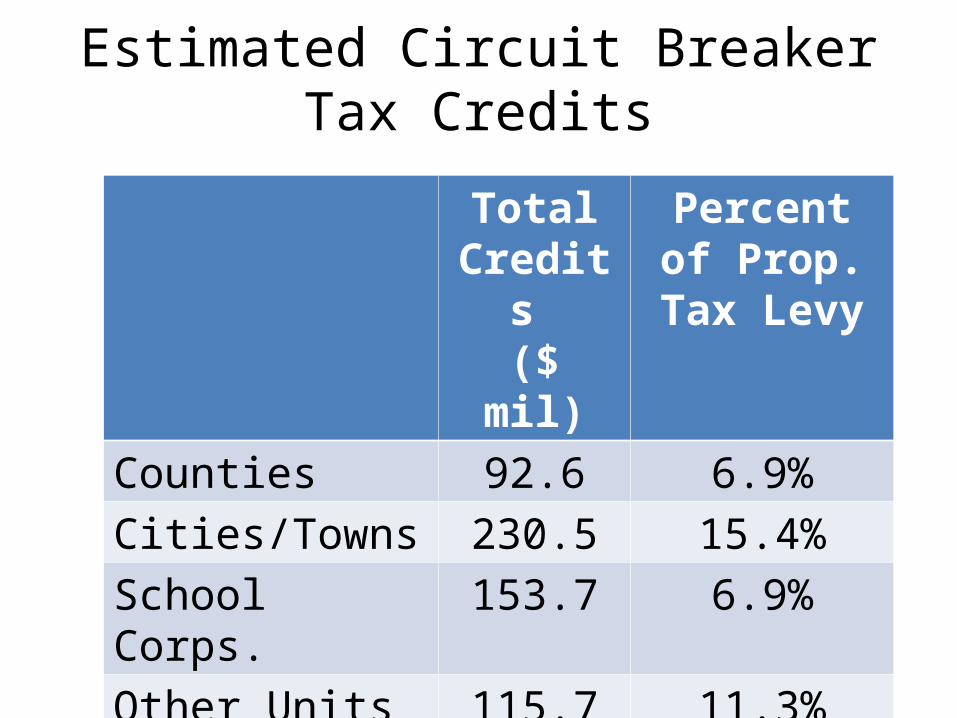

Estimated Circuit Breaker Tax Credits

Total Credits ($ mil)

Percent of Prop. Tax

LevyCounties 92.6 6.9%Cities/Towns 230.5 15.4%School Corps. 153.7 6.9%Other Units 115.7 11.3%Total 592.5 9.7%

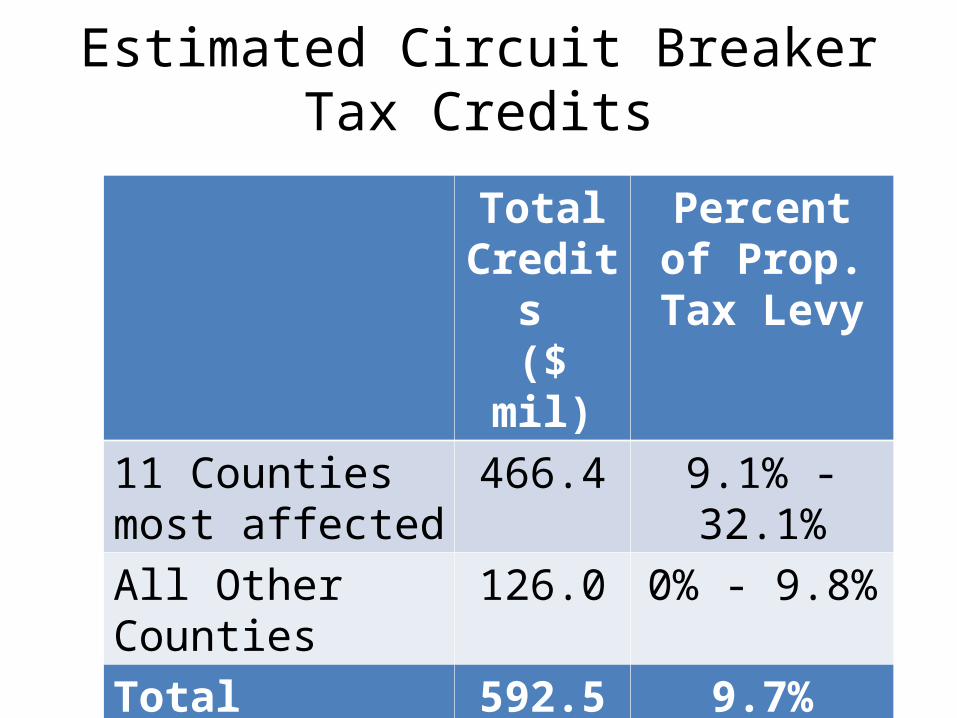

Estimated Circuit Breaker Tax Credits

Total Credits ($ mil)

Percent of Prop. Tax

Levy11 Counties most affected

466.4 9.1% - 32.1%

All Other Counties 126.0 0% - 9.8%Total 592.5 9.7%

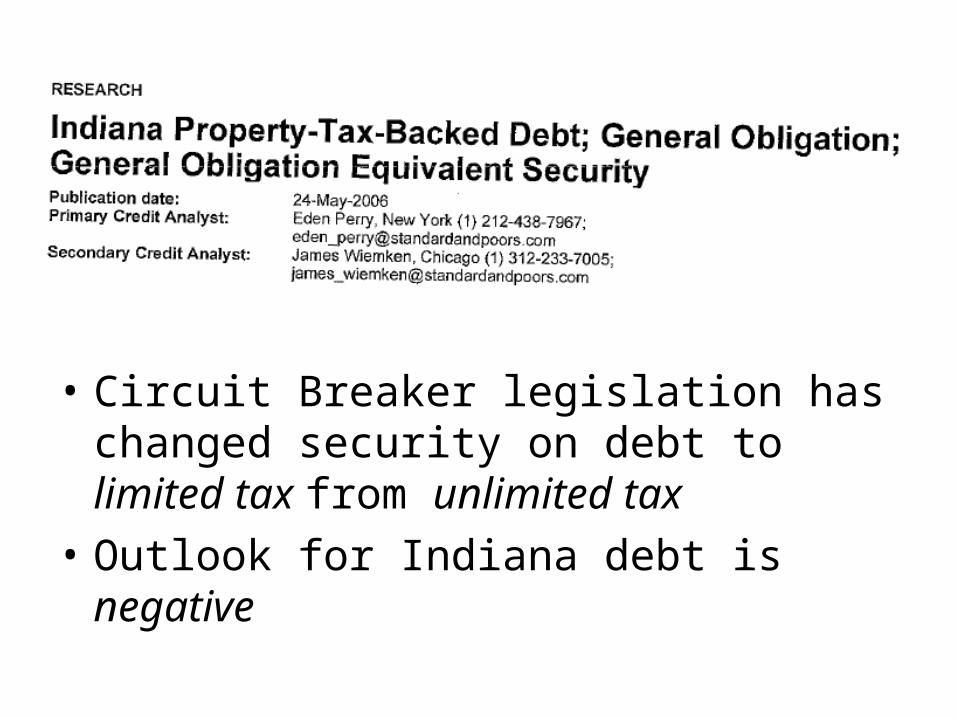

• Circuit Breaker legislation has changed security on debt to limited tax from unlimited tax

• Outlook for Indiana debt is negative

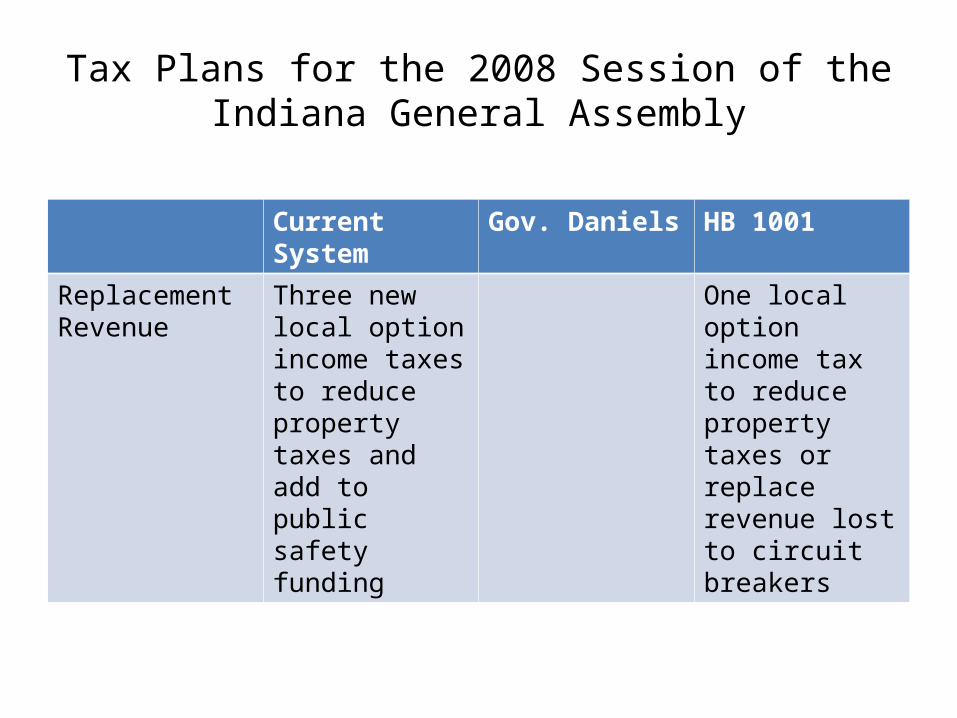

Tax Plans for the 2008 Session of the Indiana General Assembly

Current System Gov. Daniels HB 1001

Replacement Revenue

Three new local option income taxes to reduce property taxes and add to public safety funding

One local option income tax to reduce property taxes or replace revenue lost to circuit breakers

Tax Plans for the 2008 Session of the Indiana General Assembly

Current System Gov. Daniels HB 1001

Levy Limits Petition-remonstrance process for capital projects; referenda for added school levies

Referenda required for larger capital projects and excess levy increases

Referenda for large sports facilities only

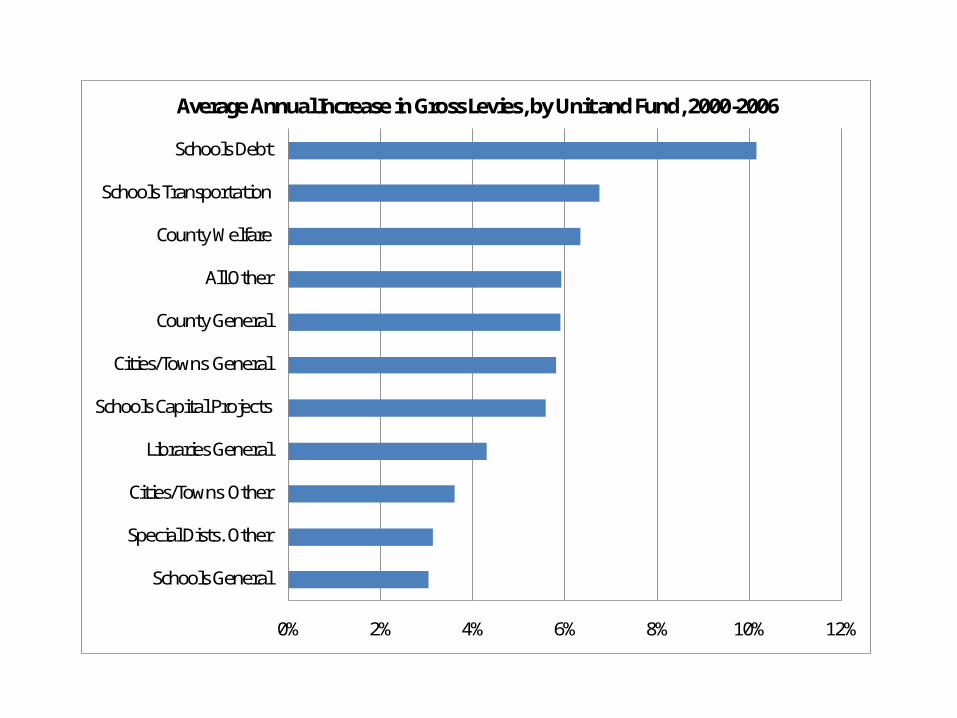

0% 2% 4% 6% 8% 10% 12%

Schools General

Special Dists. Other

Cities/Towns Other

Libraries General

Schools Capital Projects

Cities/Towns General

County General

All Other

County Welfare

Schools Transportation

Schools Debt

Average Annual Increase in Gross Levies, by Unit and Fund, 2000-2006

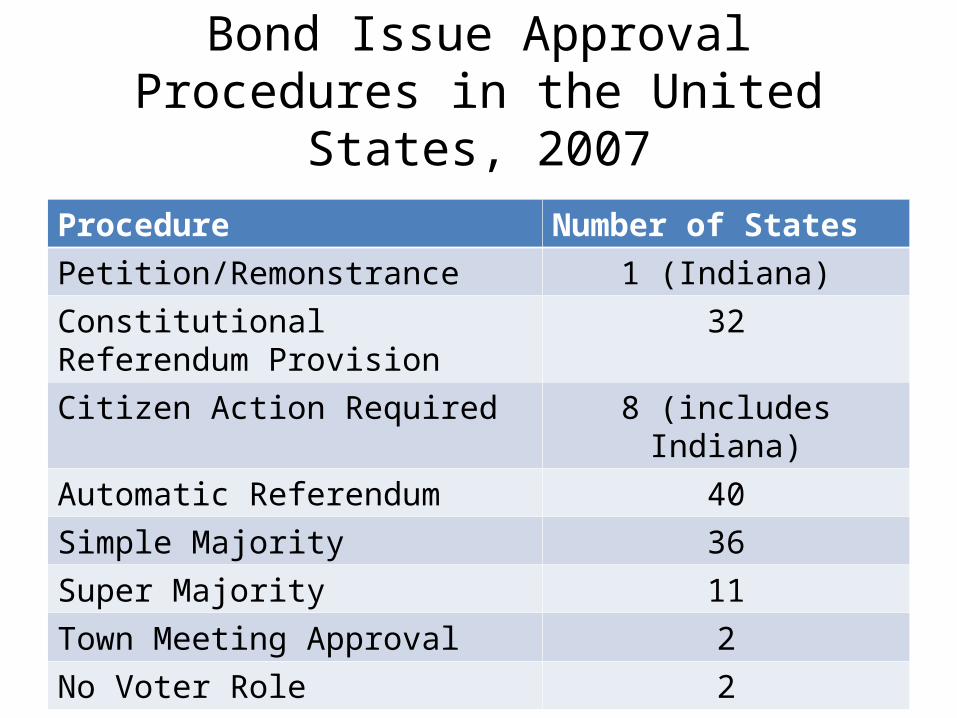

Bond Issue Approval Procedures in the United States, 2007

Procedure Number of StatesPetition/Remonstrance 1 (Indiana)Constitutional Referendum Provision

32

Citizen Action Required 8 (includes Indiana)Automatic Referendum 40Simple Majority 36Super Majority 11Town Meeting Approval 2No Voter Role 2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

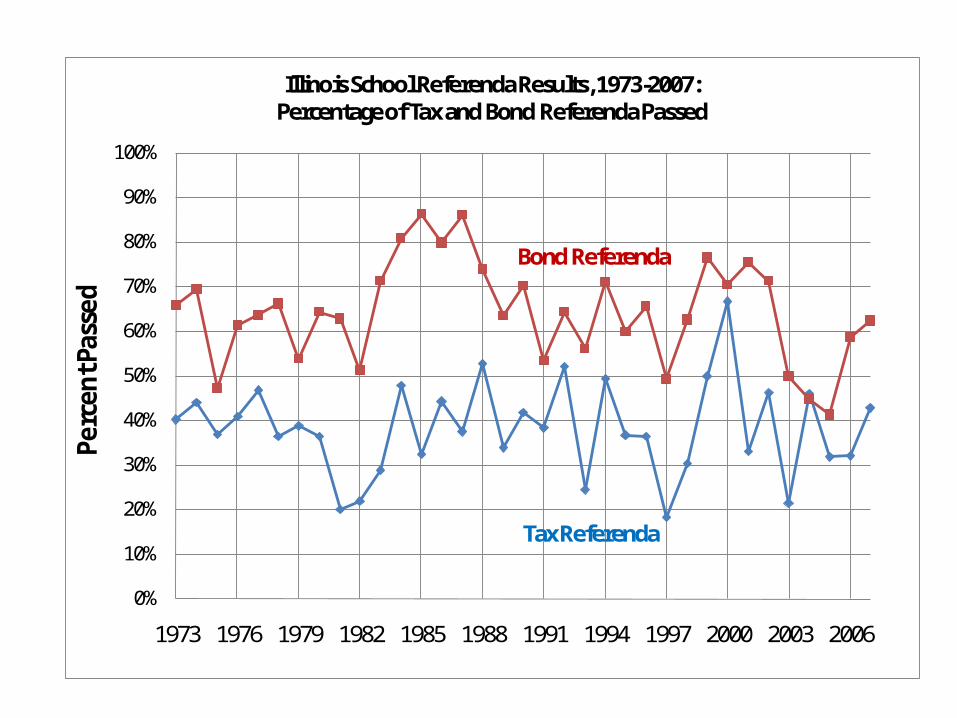

1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006

Perc

ent P

asse

dIllinois School Referenda Results, 1973-2007:

Percentage of Tax and Bond Referenda Passed

Bond Referenda

Tax Referenda

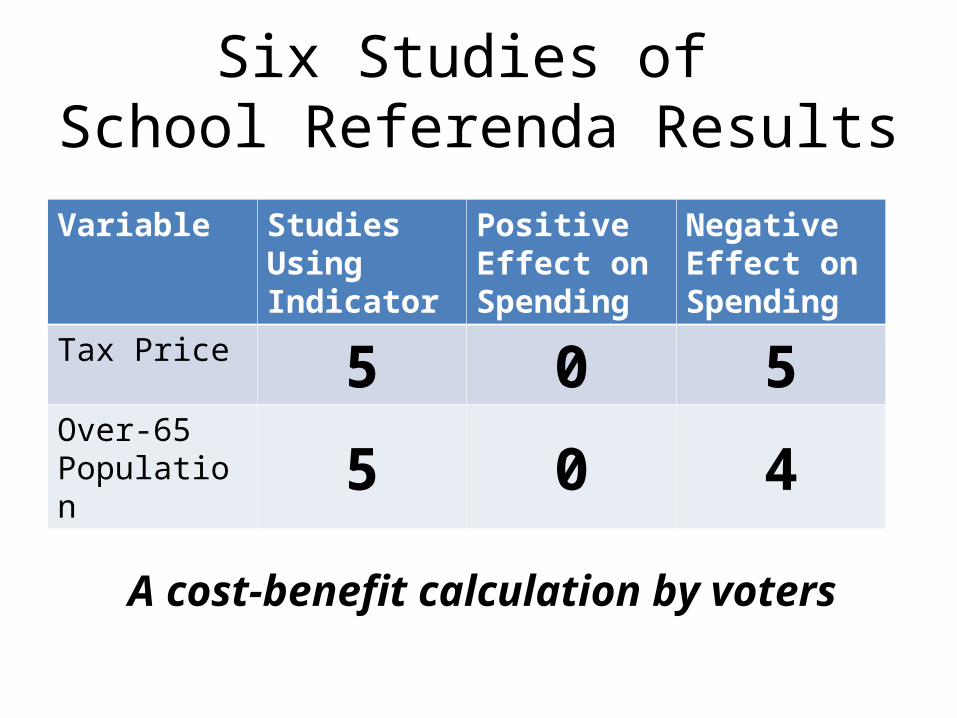

Six Studies of School Referenda Results

Variable Studies Using Indicator

Positive Effect on Spending

Negative Effect on Spending

Tax Price 5 0 5Over-65 Population 5 0 4

A cost-benefit calculation by voters

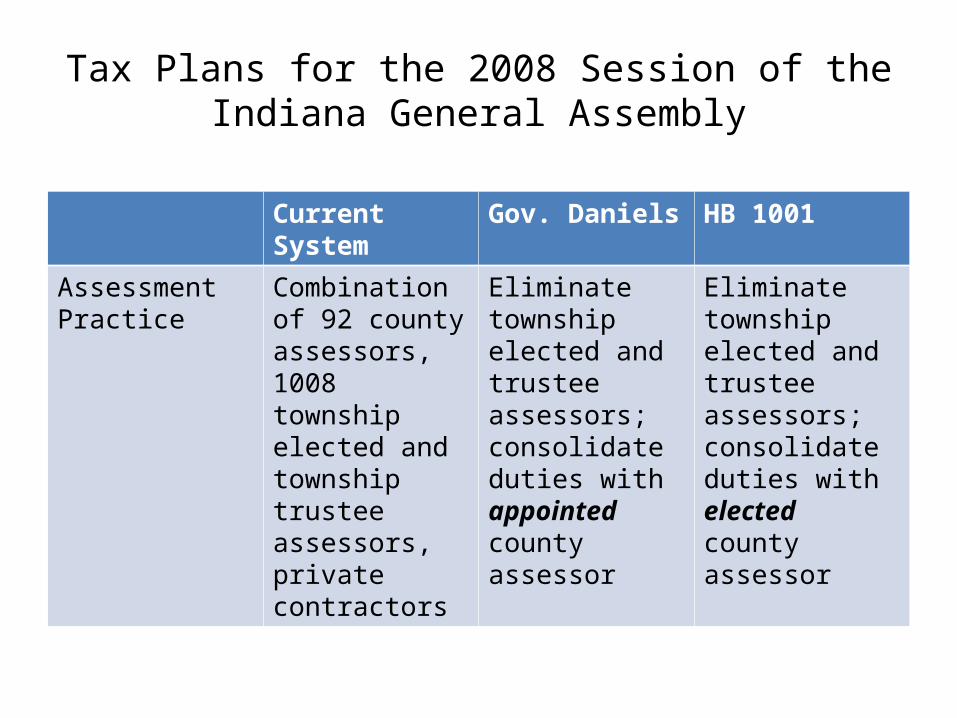

Tax Plans for the 2008 Session of the Indiana General Assembly

Current System Gov. Daniels HB 1001

Assessment Practice

Combination of 92 county assessors, 1008 township elected and township trustee assessors, private contractors

Eliminate township elected and trustee assessors; consolidate duties with appointed county assessor

Eliminate township elected and trustee assessors; consolidate duties with elected county assessor

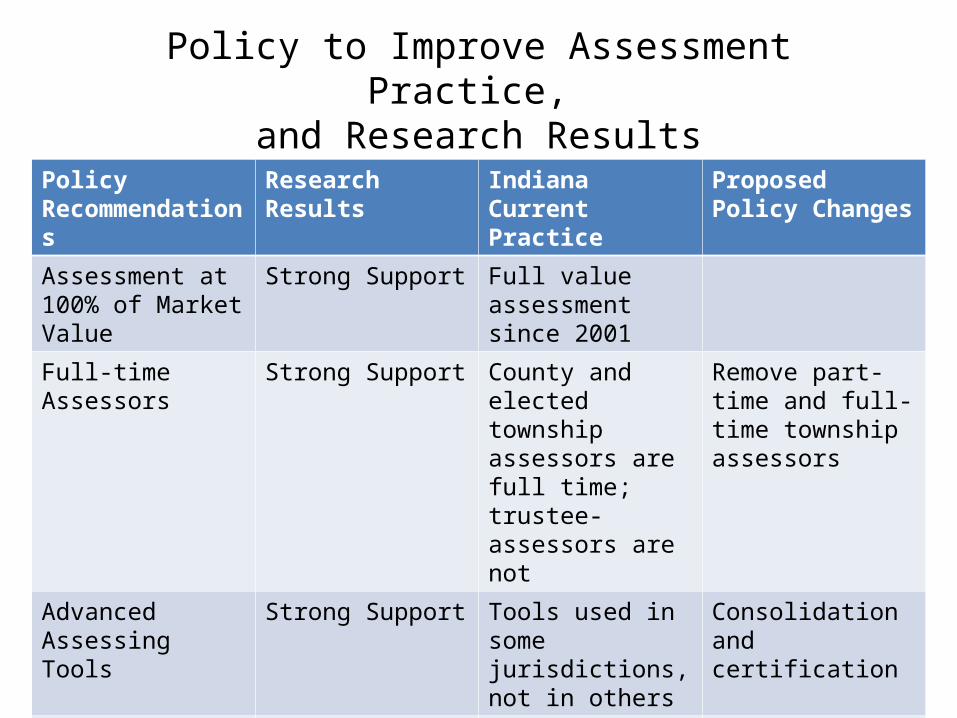

Policy to Improve Assessment Practice, and Research Results

Policy Recommendations

Research Results Indiana Current Practice

Proposed Policy Changes

Assessment at 100% of Market Value

Strong Support Full value assessment since 2001

Full-time Assessors Strong Support County and elected township assessors are full time; trustee-assessors are not

Remove part-time and full-time township assessors

Advanced Assessing Tools

Strong Support Tools used in some jurisdictions, not in others

Consolidation and certification

Consolidation to larger units

Larger units reduce costs; improved uniformity raises costs

Townships are basic assessing unit; counties assess in many counties

Consolidate assessment to counties