Omoluabi Mortgage Bank Plc - Dec 2017 Audited Accounts€¦ · OMOLUABI MORTGAGE BANK PLC TABLE OF...

71

OSOGBO, NIGERIA YEAR ENDED 31 DECEMBER 2017 OMOLUABI MORTGAGE BANK PLC FINANCIAL STATEMENTS

Transcript of Omoluabi Mortgage Bank Plc - Dec 2017 Audited Accounts€¦ · OMOLUABI MORTGAGE BANK PLC TABLE OF...

OSOGBO, NIGERIA

YEAR ENDED 31 DECEMBER 2017

OMOLUABI MORTGAGE BANK PLC

FINANCIAL STATEMENTS

OMOLUABI MORTGAGE BANK PLC

TABLE OF CONTENTS

FOR THE YEAR ENDED 31 DEECMBER 2017

CONTENTS PAGE

Financial highlights

1

Independent auditors report 2

Statement of profit or loss and other comprehensive income 6

Statement of financial position 7

Statement of changes in equity 8

Statement of cash flows 9

Statement of prudential adjustments 10

Statement of significant accounting policies 11

Notes to the financial statements 29

Other national disclosures:

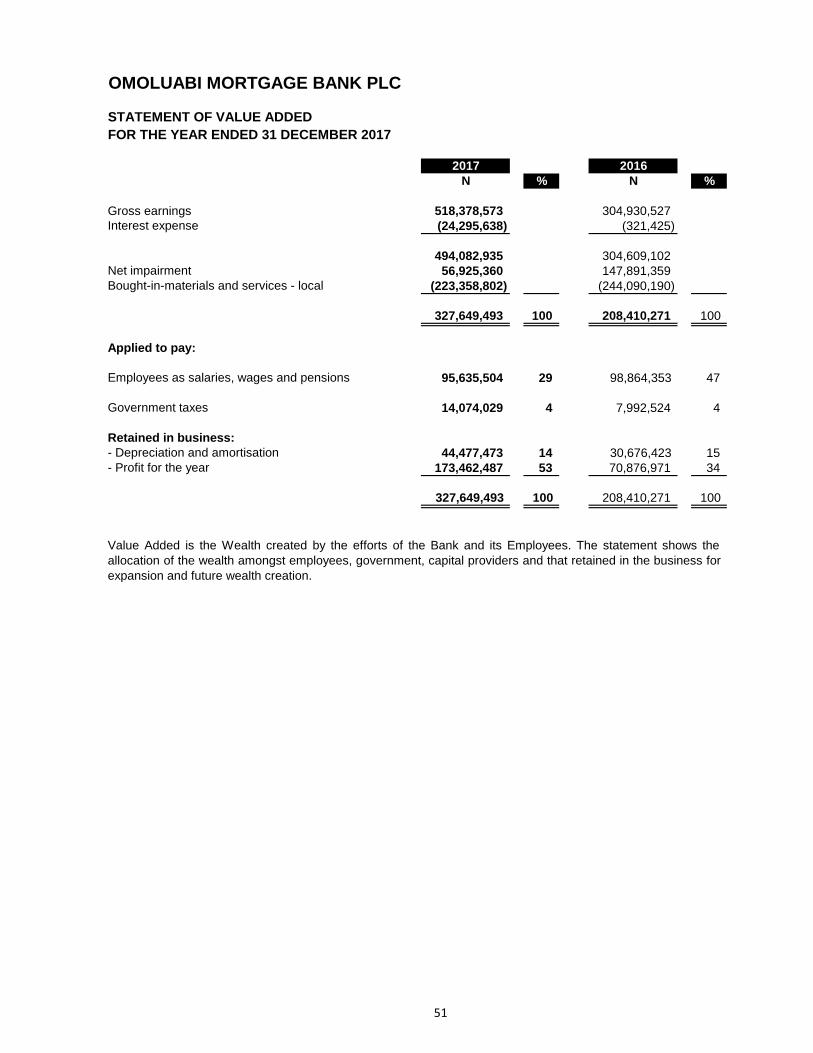

Statement of value added 51

Financial summary 52

Statement of directors' responsibilities in relation to the

preparation of the financial statements

OMOLUABI MORTGAGE BANK PLC

FINANCIAL HIGHLIGHTS

FOR THE YEAR ENDED 31 DECEMBER, 2017

2017 2016

N N

Major items in statement of financial position

Loans and advances 861,051,528 548,813,501

Property, plant & equipment 232,646,945 226,564,050

Assets held for sale 349,396,405 584,947,509

Due to customers 1,229,794,828 388,914,722

Borrowed funds 117,866,652 8,122,069

Share capital 2,500,000,000 2,500,000,000

Shareholders fund 2,608,320,211 2,433,239,503

Total assets 4,158,172,701 3,305,156,939

Major items in statement of comprehensive income

Gross earnings 518,378,573 304,930,527

Impairment charge 56,925,360 147,891,359

Profit before taxation 187,536,516 78,869,495

Taxation (14,074,029) (7,992,524)

Profit after taxation 173,462,487 70,876,971

Ratios % %

Cost to income 70.22 90.16

Return on assets 4.17 2.14

Return on shareholders fund 6.65 2.91

Capital adequacy 92.01 219.83

Liquidity 169.43 192.69

Earnings per share (kobo) 3.50 1.35

Others Number Number

Number of branches 3 3

Number of staff 61 57

Number of shares in issue 5,000,000,000 5,000,000,000

Dividend paid - -

Ratings BB+ N/A

1

1

To become an indisputably clear leader in the mortgage banking industry and make mortgage banking a worthwhile experience to our teeming clientele and lift the business to a world class standard.

Provide dedicated professionally oriented mortgage banking and financial services with a commitment towards ensuring all time

security of customers’ deposits.

25

OMOLUABI MORTGAGE BANK PLC is a specialized Mortgage Financial

Institution promoted initially by the Government of Osun State, Nigeria. The Bank was

initially incorporated as Osun Building Society Limited but later had several name changes

to LIVINGSPRING SAVINGS AND LOANS LIMITED, OMOLUABI SAVING AND LOANS

LIMITED, OMOLUABI SAVINGS AND LOANS Plc and very recently to OMOLUABI

MORTGAGE BANK Plc to reflect its transformation aims and the virtues of the people of

the State.

The Bank was licensed by the Federal Mortgage Bank of Nigeria (FMBN) in March 1999

and began operation on the 9th

of April, 1999. The Bank is regulated by the Central Bank of

Nigeria and supervised by the Other Financial Institution Supervision Department (OFISD)

Of the Central Bank of Nigeria.

The main objective of the Bank is to provide wholesome housing, Mortgage and property

debt solutions in particular and general banking services within Osun State and the

Nation. The Bank is totally committed to the provision of high quality banking and financial

services to her numerous customers. The Head- office of the organization is located at Old

Governor’s Office, Gbongan Road, Osogbo, Osun State, Nigeria.

26

Mr Adebayo Jimoh joined the services of John Holt PLC (A British Multinational Company) as a Management Trainee in 1983 from where he rose through the ranks in quick succession to become the Deputy General Manager in charge of Operations for the company in 1993.Mr Jimoh served as a General Manager for John Holt Ventures from 1994-1996 and thereafter moved to Yamaha Almarine Company as General Manager in 1997. He was later promoted as Chief Executive in Charge of Trade and Export for John Holt Group in Nigeria and West Africa before his appointment as Executive Director in charge of Group operations of John Holt PLC in 2003.

In May 2005,he was appointed Group Managing Director/CEO of Odua Investment Company Ltd, the Investment Basket of the Five South Western States in Nigeria. He served for a period of nine years and retired in October 2014.Adebayo Jimoh currently runs a Cotton Export Business under the name Synergy Cotton and Agro Allied Company in partnership with Plexus Cotton, UK. He is the Chairman of the Company. He is a Fellow of the Nigeria Institute of Management, Fellow of the National Institute of Marketing of Nigeria and a Member of the Institute of Directors.

Mr Adewumi Adesola is an efficient tax administrator and member of the pioneer tax consultants to Lagos State Government tax audit and administration since 1995 till date. A Managing Partner of Adesola Adewumi & Co. (Chartered Accountants) since 1995 and the Managing Director of Clear-Cut Solutions Ltd 1995 till date .He is also the Chairman of David Sons Paints & Chemical Industries Ltd since 2009.

He is a Fellow of the Institute of Chartered Accountants of Nigeria.

Mr Bola Oyebamiji is a fellow of Institute of Chartered Economists of Nigeria, A Chartered Banker and an Associate of Institute of Management and a Member, Nigerian Economic Submit Group (NESG).

He has over 28 years’ experience as a banker which includes Wema Bank Plc( Assistant Manager),Trans International Bank Plc ( Senior Manager) ,Trans International Bank Plc (Principal Manager), Spring Bank Plc Adeola Odeku (Corporate Branch) and Enterprise Bank Ltd (Regional Manager). He is the Managing Director of Osun State Investment Company Limited Osun-State since 2012 to date. He is also the current Commissioner for Finance of the state of Osun.

Mr Kolawole Obtained a Bachelors of Science degree in Accountancy from University of

27

Maiduguri. He started his career in the Civil Service as Accountant Grade 11 in 1987 and rose through the ranks and bcame a Deputy Director in 2005 and Director, Treasury and Pension Services from 2007 – 2012.

He has participated in several seminars and workshops both locally and internationally some of which include Financial Management Training Course at Obafemi Awolowo University, Ile- Ife, A workshop on financial Management & Disbursement for Project Financial Management Units ( PFMUs) organized by the World Bank(2005). Training Course on Public Finance Management, Issues and Solutions Organised by Crown Agents, London in 2006.

Mr Kolawole is the current Accountant – General, State of Osun from 2012 till date.

Ayo is a Chartered Accountant and started his career with KPMG Lagos in 2003 where he worked for 3 years and rose to the position of Audit Semi-Senior in the Assurance & Business Advisory Division. Afterwards, he worked as an Analyst in the Project Finance & Real Estate Unit of ARM. He joined PRI Project LLC in 2009 as the Vice President in the Lagos Office. He also worked as an Investment Analyst with Grofin Nigeria, a multi-national specialist SME Development Finance company offering risk capital to viable enterprises through its $250m Aspire funds and its 10 offices in 9 countries. He is Currently the Managing Director of Omoluabi Mortgage Bank since 2015.

Dr. D. O. Yinusa graduated with First Class Honours in Economics from Obafemi Awolowo University, Ile-Ife, Nigeria and obtained his PhD in Economics in 2005. He has won many academic distinctions and awards including the prestigious Fulbright Visiting Scholar, Graduate School of Arts and Science, Fordham University, NY, USA, South Africa-Norway Tertiary Education Development (SANTED) Programme, (2009).

Dr. Yinusa has served as consultant to a number of national and international organisations including UNDP (Botswana and Nigeria), Botswana National Productivity Centre, Botswana, African Development Bank (AfDB), Abidjan, C’ote d’Ivoire, African Capacity Building Foundation (ACBF), Harare, Zimbabwe, European Union (EU) – African University Network, Germany, West African Monetary Institute (WAMI), Ghana, National Bureau of Statistics (NBS), Nigeria and Centre for Gender and Social Policy Studies, Nigeria. He was the Special Adviser to Osun State Governor (Ogbeni Rauf Adesoji Aregbesola) on Commerce, Cooperatives and Empowerment, Osogbo between August 2011 – Nov 2014. Dr. Yinusa is currently an associate professor in Obafemi Awolowo University and the Commissioner for Economic Planning & Budget in the State of Osun

.

A former Legislator, State of Osun House of Assembly from 2012 - 2015 Hon Sijuwade was the Managing Consultant / Executive Director (Finance),Lagos State Passenger Personal Accident Insurance Programme from 2006- 2010 , Chief Executive Officer ,Monarch Ventures Limited, and also Chief Executive Officer ,Pathfinder Investment Network Limited- 2006 to 2010

28

He became the General Manager, Capital Market Operations in Abacus Securities Limited /Abacus Merchant Bank Ltd from1986 – 1999 and Manager in Charge of Operations of Arco Petroleum Limited (1984–1986). He was a member of the Presidential Trade Mission to France on the invitation extended to Abacus Merchant Bank to offer financial Advisory Services in 1989. Award winner of the Most Distinguished Legislator in Tourism decorated by the Government of Imo State in collaboration with Nigeria Media Links at the National Conference / Awards on Culture, Hospitality and Tourism Development in Nigeria.

He retired as General Manager, First Bank of Nig. Plc in 2003 after over 2 decades in the Banking Industry. In the course of his excellent career, he had attended professional courses both locally and internationally some of which are Advanced International Business Management: London – 1999, Strategic Management for Directors and Senior Managers, London – May 2003. Senior Bankers Course by Manchester Business School – 1990. He is a Member of the Nigeria Computer Society , a Member of the Chartered Institute of Bankers of Nigeria and also a Member of the Computer Professional Registration Council of Nigeria .

He is the Managing Consultant of GBADEBO Adekunle OLORI & Co from 2010 till date. A company that runs consultancy on project management, quality control, financial reporting and formulation of strategic policies on mortgages and other financial products.

He was formerly Chief Executive Officer, Eaziway Financial (UK), from Feb 2005-Dec 2009 and Managing Director, Budget Line Travels (UK), between 2001 and 2005. He was the Financial Controller, Zomax Incorporation (Ireland) from 2000 to 2001 with activities spanning from preparation of final accounts responsible for bills payables and receivables, trainings of subordinates all over Europe. Senior Consultant ,Petroleum Special Trust Fund (PTF) , 1996-1998, Senior Lecturer on Audit Practice, Taxation, Cost Accounting with student pye, (1996-2000).) Lecturer on mortgage practice with London Tower College, Hackney London between, 2004-2007.

29

Corporate Governance The Central Bank of Nigeria in its Circular BSD/04/2006 of March 2, 2006 released a new Corporate Governance Code which includes the protection of equity ownership, enhancement of sound organizational structure and promotion of industry transparency. The Code requires Banks to include in their annual report and accounts, compliance report to the Code of Corporate Governance. In compliance

therefore, we state below our Compliance Report as at December 31st 2017:

Compliance Status

In line with the provisions of the new Code, the Bank has put in place a robust internal control and risk management framework that will ensure optimal compliance with internationally acceptable corporate governance indices in all its operations. In the opinion of the Board of Directors, the Bank has substantially complied with the new Code of Corporate Governance during the 2017 financial year.

Statutory Bodies

Apart from the CBN Code of Corporate Governance, which the Bank has strived to comply with since inception, it further relies on other regulatory bodies to direct its policy thrust on Corporate Governance.

Shareholders’ meeting

The shareholders remain the highest decision making body of Omoluabi Mortgage Bank Plc., subject however to the provisions of the Memorandum and Articles of Association of the Bank, and other applicable legislation. At the Annual General Meetings (AGM), decisions affecting the Management and strategic objectives of the Bank are taken through a fair and transparent process. Such AGMs are attended by the shareholders or their proxies and proceedings at such meetings are monitored by members of the press and representatives of the Nigerian Stock Exchange, Central Bank of Nigeria, Nigeria Deposit Insurance Commission, Corporate Affairs Commission, Securities and Exchange Commission and the Bank’s statutory auditors.

Ownership Structure

Osun State Government and Osun State Local Government Councils represent public sector participation in the ownership of the Bank however they are not majority shareholders in the bank. The Bank is owned by shareholders in the private sector. The lists of shareholders consist of individuals, Public Sector and institutional investors.

Board of Directors

The Board of Directors consists of the Chairman, Managing Director/Chief Executive Officer (MD/CEO) and Non-Executive Directors (Non-EDs). The Directors have diverse background covering Economics, Management, Accounting, Psychology, Information Technology, Public Administration, Law, Engineering, and Business Administration. These competences have impacted on the Bank’s stability and growth. The office of the Chairman of the Board is distinct and separate from that of the Managing Director/Chief Executive Officer and the Chairman does not participate in running the daily activities of the Bank. There are no family

30

ties within the Board members. We confirm that the Chairman of the Board is not a member of any Board Committee and appointment to the Board is made by the shareholders at the Annual General Meeting upon the recommendation of the Board of Directors.

Membership of the Board of Directors

Memberships of the Board of Directors during the year ended 31 December, 2017 were as follows:

S/N NAME POSITION HELD

1. Adebayo Jimoh Chairman

2. Ayodele Olowookere Managing Director/CEO

3. Bola Oyebamiji Director (Non-Executive)

4. Dr. Olalekan Yinusa Director (Non-Executive)

5. Hon. (Prince) Adetilewa Sijuwade Director (Non-Executive)

6. Gbadebo Adekunle Director (Non-Executive)

7. Akintayo Kolawole Director (Non-Executive)

8. Micheal Omolaja Director (Non-Executive)

9. Adesola Adewunmi Director (Non-Executive)

Tenure of Office

The tenure of office of an Executive and a Non-Executive Director is a renewable term of 4 (Four) years each.

Delegation of Powers

The Board of Directors delegates any of their powers to Committees consisting of such members of their body as they think fit and have oversight functions on the Committees.

The Board also delegates authority to the Management in line with best practices, for the day-to-day Management of the Bank through the MD/CEO, who is supported in this task by the Four (4) Management Staff.

Standing Board Committees

The Board carries out its oversight responsibilities through Six (6) standing Committees whose terms of reference it reviews regularly. All the Committees have clearly defined terms of references, which set out their roles, responsibilities and functions, scope of authority and procedures for reporting to the Board.

In Compliance with Code No. 6 on industry transparency, due process, data integrity and disclosure requirement, the Board has in place the following Committees and reporting structures through which its oversight functions are performed:

Statutory Audit Committee;

Board Investment, Risk and Credit Committee;

Board Establishment, Finance and General Purpose Committee;

Statutory Audit Committee

This is a joint shareholders/Board Committee that comprise of an equal number of 3 (Three) shareholders and 3 (Three) Directors. The Committee has oversight function on Internal Control system and financial reporting. The Committee’s terms of reference are:

General

31

The Committee shall:

- Ensure that there is an open avenue of communication between the External Auditors and the Board and confirm the Auditors’ respective authority and responsibilities.

- Oversee and appraise the scope and quality of the audits conducted by the Internal and External Auditors.

- Review annually, and if necessary propose for formal Board adoption, amendments to the Committee’s terms of reference.

Whistle Blowing

- Review arrangements by which staff of the Bank may, in confidence, raise concerns about possible improprieties in matters of financial reporting or other matters.

- As global best practice however that a direct channel of communication is established

between the whistle blower and the authority to take action, investigate or cause to be investigated the matter being blown, the Committee shall ensure that arrangements are in place for the proportionate and independent investigation and follow-up of such matters.

Regulatory Reports

The Committee shall also:

- Examine CBN/NDIC examination Reports and make recommendations thereof.

- Monitor and review the standards of risk management and internal control, including the processes and procedures for ensuring that material business risks, including risks relating to IT security, fraud and related matters, are properly identified and managed, the effectiveness of internal control, financial reporting, accounting policies and procedures, and the Bank’s statements on internal controls before they are agreed by the Board for each year’s Annual Report.

- Consider and review the process for risk management annually to ensure adequate oversight of risk faced by the Bank and the system of internal controls and reporting of those risks within the Bank.

- Receive regular Reports on significant litigation and financial commitments and potential liability (including tax) issues involving the Bank.

Membership

The Committee comprises of a total number of six (6) members made up of three (3) Non-Executive Directors and three (3) Shareholders as follows:

Non - Executive Directors: 1. Prince Sola Adewumi - Chairman

2. Tayo Kolawole - Member

3. Dr. Olalekan Yinusa - Member

Shareholders:

4. Mr. Odewale Odeyinka - Member

5. Mr. Olugbosun Ariyo - Member 6. Mr. Yaya Ajagbe Suraj - Member

32

Quorum : Four (4) members, 2 (Two) Non-executive directors and 2 (Two) shareholders. Board Investment, Risk and Credit Committee The Board Investment, Risk and Credit Committee is charged with the responsibility of evaluating and or approving all credits beyond the powers of Management from N25 Million to 150 Million for fund based facilities. The following are its terms of reference.

Roles The Roles of the Committee are:

i. Oversee Management’s establishment of policies and guidelines, to be adopted by the Board

ii. Articulating the Bank’s tolerances with respect to credit risk, and overseeing Management’s administration of, and compliance with, these policies and guidelines.

iii. Oversee Management’s establishment of appropriate systems (including policies, procedures, management and credit risk stress testing) that support measurement and control of credit risk.

iv. Periodic review of Management’s strategies, policies and procedures for managing credit risk, including credit quality administration, underwriting standards and the establishment and testing of provisioning for credit losses.

v. Overseeing the administration of the Bank’s credit portfolio, including Management’s responses to trends in credit risk, credit concentration and asset quality.

vi. Coordinate as appropriate its oversight of credit risk with the Board Risk Management Committee in order to assist the Committee in its task of overseeing the Bank’s overall management and handling of risk.

vii. Evaluate and or approve all credits beyond the powers of the Executive Management. viii. Ensure that a qualitative and profitable Credit Portfolio exist for the Bank.

ix. Evaluate and recommend to the Board all credits beyond the Committee’s powers.

x. Review of credit portfolio within its limit in line with set objectives. xi. Review of classification of credit advances of the Bank based on prudential guidelines

on quarterly basis. xii. Approving the restructuring and rescheduling of credit facilities within its powers;

xiii. Write-off and grant of waivers within powers delegated by the Board;

xiv. Review and monitor the recovery of non-performing insider related loans. xv. Overseeing the overall Risk Management of the Bank;

xvi. Reviewing periodically, Risk Management objectives and other specific Risk Policies for consideration of the full Board;

xvii. Evaluating the Risk Rating Agencies, Credit Bureau and other related Service Providers to be engaged by the Bank;

xviii. Approving the internal Risk Rating Mechanism.

xix. Reviewing the Risk Compliance reports for Regulatory Authorities; xx. Reviewing and approving exceptions to The Bank’s Risk Policies;

xxi. Review of policy violations on Risk issues at Senior Management Level;

xxii. Certifying Risk Reports for Credits, Operations, Market/Liquidity subject to limits set by the Board;

xxiii. Evaluating the risk profile and risk management plans for major projects and new ventures to determine the impact on the Bank’s risk profile.

xxiv. Ensuring compliance with global best practice standards as required by the Regulators. xxv. Monitoring the market, Operational, Reputational, Liquidity, Compliance, Strategic,

Legal and other Risks as determined by the Board. xxvi. Any other oversight functions as may, from time to time, be expressly requested by the

33

Board.

Membership

The Committee has 5 (Five) members comprising of 4 (Four) Non-Executive Directors, the Managing Director/CEO. The committee members are as follows:

1. Michael Omolaja - Chairman

2. Gbadebo Adekunle - Member

3. Dr. Olalekan Yinusa - Member

4. Prince Adetilewa Sijuwade - Member

5. Ayo Olowookere - Member

Quorum

3 (Three) members.

Board Establishment, Finance and General Purpose Committee: Roles

i) The committee is responsible for the overall governance and personnel function of the Board.

ii) To consider and make recommendations to the Board on acquisition of Fixed Assets, Review and recommend nomination of directors to the Board based on a proper selection process.

iii) To ensure adequate succession planning for Board of Directors and Chief Executive Officer.

iv) To ensure the orientation and continuous education of Directors.

v) To monitor the procedures established for compliance with regulatory requirements for related party transactions.

vi) To monitor staff compliance with the Code of Ethics and Business Conduct of the Bank. vii) To ensure compliance with regulatory standards of Corporate Governance and

regularly identify international best practices of corporate governance and close any identified gaps.

viii) Recruitment/ promotion of staff to Assistant General Manager level and above and to approval of the remuneration.

ix) To decide on the benefits and other terms and conditions of the service contracts of such officers recommend to the Board.

x) To determine the terms and conditions of the service contract including remuneration of the bank’s policies committed by staff of Assistant General Manager level and above and apply appropriate sanctions where necessary.

xi) To review and approve of policies on staff welfare and fringe benefits; annual review of the Board Charter.

xii) To ensure the annual review of the Board and board committees’ performance.

Membership

1. Bola Oyebamiji - Chairman

2. Gbadebo Adekunle - Member

3. Tayo Kolawole - Member

4. Michael Omolaja - Member

5. Ayo Olowookere - Member

34

Quorum

3 (Three) Members Remuneration of Directors The Shareholders, at the Bank’s Annual General Meeting, set and approved the annual remuneration of members of the Board of Directors. The annual emoluments of the Directors are stated in the Annual Report.

Internal Control The Bank has separate staff within the internal audit function from operational and management Internal control Charter for its internal audit exercise. The Charter isolates and insulates the Internal Audit Division from the control and influence of the Executive Management so as to independently review the Bank’s operations. Under the Charter, the Internal Auditors’ report is submitted directly to the Board Audit Committee.

Compliance The Bank has in place a compliance department in line with regulatory provisions. The compliance department is responsible for monitoring the Bank compliance to legislative and regulatory provisions, circulars and pronouncements. It is also responsible for monitoring compliance of the Bank’s operations, processes and procedures to internal policies. The compliance department is independent of the internal control function and reports directly to the Managing Director.

Executive Management Committee

The Executive Management Committee (EXCO) reviews and approves credit facilities up to its limit and an amount above its limit goes to the Board Credit Committee for review and approval. The Committee meets once a month or as the need arises.

Membership of the Executive Management Committee (EXCO) is made up of the Managing Director/Chief Executive Officer as Chairman with all Executive Management Staff

Risk Management

The Board of Directors and Management of Omoluabi Mortgage Bank Plc. are committed to establishing and sustaining best practices in Risk Management in line with international practice. For this purpose, the Bank operates a centralized Risk Management and Control Division, with responsibility to ensure that the Risk Management processes are implemented in compliance with Policies approved by the Board of Directors.

The Board of Directors determines the Bank’s goals, in terms of risk, by issuing a Risk Policy. The Policy both defines acceptable levels of risk for day-to-day operations as well as the Bank’s willingness to incur risk, weighed against the expected rewards. The Risk Policy is detailed in the Enterprise Risk Management (ERM) Framework, which is a structured approach to identifying opportunities, assessing

the risk inherent in these opportunities and managing these risks proactively in a cost effective manner. It is a top-level integrated approach to events identification, analysis, assessment, monitoring and identification of business opportunities. Specific policies are also in place for managing risks in the different risk area of Credit, Market and Operational Risks.

The evolving nature of Risk Management practices and the dynamic character of the

35

banking industry necessitate regular review of the effectiveness of each Enterprise Risk Management component. In the light of this, the Bank’s Enterprise Risk Management Framework is subject to continuous review to ensure effective Risk Management. The review is done in either or both of the following ways:

- Continuous self-evaluation and monitoring by the Risk Management Division in

conjunction with Internal Control; and - Independent evaluation by external Auditors and Examiners.

Implementation of Code of Corporate Governance

In compliance with Code No. 6.1.11, the Bank has a Compliance Department with responsibilities of implementing Code of Corporate Governance in addition to monitoring compliance of the Money Laundering requirements.

The Chairman of the Board does not serve as Chairman/Member of any of the Board Committees;

The Bank’s organizational chart approved by CBN reflects clearly defined lines of responsibility and hierarchy;

The Bank also has in place, a system of internal control, designed to achieve efficiency, effectiveness of operations, reliability of and regulations at all levels of financial reporting and compliance with applicable laws.

Breaches of the Code

The Bank is not aware of any violation to the Code of Corporate Governance.

Olabisi Fayombo FRC/2013/ICAN/00000002883 For: Adekunle Fagbile Company Secretary

CERTIFICATION PURSUANT

To Section 60(2) of the Investments and Securities Act No. 29 of 2007 FOR THE YEAR ENDED 31st

DECEMBER, 2017

We the undersigned hereby certify the following with regard to Audited Accounts for the year ended

31st December, 2017 that:

1. We have reviewed the report and to the best of our knowledge, the report does not contain: a. Any untrue statement of a material fact, or

b. Any omission of material fact, which would make the statements, misleading in the light of the circumstances under which such statements were made.

2. To the best of our knowledge, the financial statement and other financial information included in the report fairly present in all material respects the financial state and results of operations of the company as at and for the periods presented in the report.

3. We are responsible for: a. Establishing and maintaining internal controls

b. The design of such internal controls and to ensure that material information relating to the company is made known to the officers within the company particularly during the period in which the periodic reports are being prepared.

c. Evaluating the effectiveness of the company’s internal controls within 90 days prior to the report;

d. Presenting in the report our conclusions about the effectiveness of the company’s internal control based on our evaluation as of that date.

4. We have disclosed to the auditors of the company and Audit Committee:

a. All significant deficiencies in the design or operation of internal controls which would adversely affect the company’s ability to record process, summarize and report financial data and have identified for the Company’s Auditor any material weakness in internal controls, and

b. Any fraud, whether or not material, that involves management or other employees who have significant role in the company’s internal controls.

5. We have identified in the report whether or not there were significant changes in the internal controls or other factors that could significantly affect internal control subsequent to the date of our evaluation, including any corrective actions with regard to significant deficiencies and material weaknesses.

DATED THIS 25th DAY OF APRIL, 2018

OLUSOLA AFOLABI AYODELE OLOWOOKERE CHIEF FINANCIAL OFFICER MANAGING DIRECTOR/CEO

REPORT OF THE AUDIT COMMITTEE

In compliance with the provisions of Section 359(6) of the Companies and Allied matters Act, Cap C20 LFN 2004, we confirm that the accounting and reporting policies of the Bank were in accordance with statutory requirements and agreed ethical practices.

In our opinion, the scope and planning of both the internal and external audits for the year

ended 31st December 2017 were adequate. We have also received, reviewed and discussed the audit report on Management matters and were satisfied with the

departmental responses thereon.

The Members of the Audit Committee reviewed the Audited Report on related party transactions and are satisfied with their status as required by the Central Bank of Nigeria (CBN). The Committee also reviewed the IFRS disclosure requirements and is satisfied with the disclosures thereon.

The internal control system of the bank was also being constantly and effectively monitored.

Dated 25th April, 2018

Prince Sola Adewumi FCA, CFE (Chairman, Audit Committee) FRC/2016/ICAN/00000015608

Members of the Audit Committee

Mr. Tayo Kolawole (Director) Dr. Olalekan Yinusa (Director) Mr. Odewale Odeyinka (Member) Mr. Olugbosun Ariyo (Member) Mr.Yaya Ajagbe Suraj (Member)

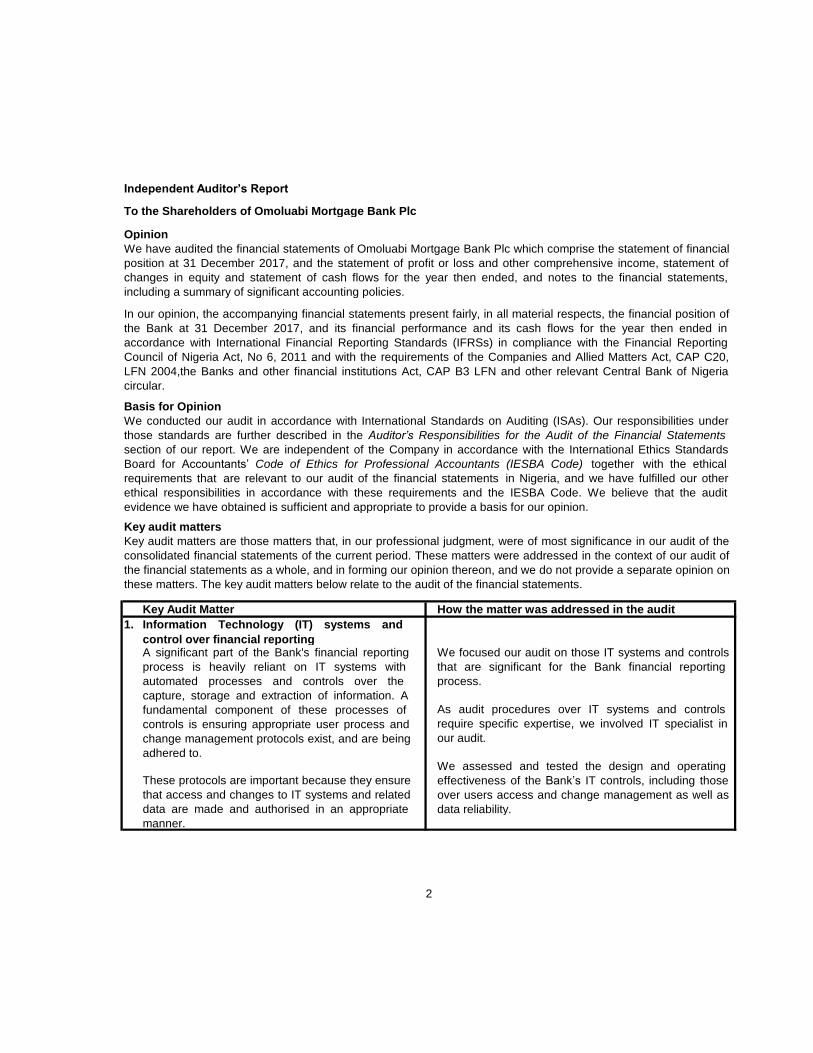

Independent Auditor’s Report

To the Shareholders of Omoluabi Mortgage Bank Plc

Opinion

Basis for Opinion

Key audit matters

Key Audit Matter How the matter was addressed in the audit

1.

A significant part of the Bank's financial reporting

process is heavily reliant on IT systems with

automated processes and controls over the

capture, storage and extraction of information. A

fundamental component of these processes of

controls is ensuring appropriate user process and

change management protocols exist, and are being

adhered to.

We focused our audit on those IT systems and controls

that are significant for the Bank financial reporting

process.

As audit procedures over IT systems and controls

require specific expertise, we involved IT specialist in

our audit.

We have audited the financial statements of Omoluabi Mortgage Bank Plc which comprise the statement of financial

position at 31 December 2017, and the statement of profit or loss and other comprehensive income, statement of

changes in equity and statement of cash flows for the year then ended, and notes to the financial statements,

including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of

the Bank at 31 December 2017, and its financial performance and its cash flows for the year then ended in

accordance with International Financial Reporting Standards (IFRSs) in compliance with the Financial Reporting

Council of Nigeria Act, No 6, 2011 and with the requirements of the Companies and Allied Matters Act, CAP C20,

LFN 2004,the Banks and other financial institutions Act, CAP B3 LFN and other relevant Central Bank of Nigeria

circular.

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under

those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements

section of our report. We are independent of the Company in accordance with the International Ethics Standards

Board for Accountants’ Code of Ethics for Professional Accountants (IESBA Code) together with the ethical

requirements that are relevant to our audit of the financial statements in Nigeria, and we have fulfilled our other

ethical responsibilities in accordance with these requirements and the IESBA Code. We believe that the audit

evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the

consolidated financial statements of the current period. These matters were addressed in the context of our audit of

the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on

these matters. The key audit matters below relate to the audit of the financial statements.

Information Technology (IT) systems and

control over financial reporting

We assessed and tested the design and operating

effectiveness of the Bank’s IT controls, including those

over users access and change management as well as

data reliability.

These protocols are important because they ensure

that access and changes to IT systems and related

data are made and authorised in an appropriate

manner.

2

Key Audit Matter How the matter was addressed in the audit

1.

2. Loans and other receivables-impairment

Our audit procedures included:

Other Information

3

The Bank uses a vendor customized Enterprise

Resource Planning application (EasyBank AX).

In a limited number of cases we adjusted our planned

audit approach as follows:

The Bank has an IT division to manage the IT

function, and/or to assist with operational

requirements (includes service providers for major

functions).

We extended our testing to identify whether there

had been unauthorised or inappropriate access or

changes made to critical IT systems and related data;

Information Technology (IT) systems and

control over financial reporting (Cont'd)

Loans and other receivables are stated at their

amortised cost less appropriate allowance for

impairment. As disclosed in note 10 and note 18

the Bank assesses at each reporting date whether

there is objective evidence that financial asset is

impaired. In carrying out this assessment,

management relies on entity-developed internal

models. For instance in assessing collective

impairment ,the company uses historical trend of

the probability of default, timing of recoveries and

the amount of loss incurred, adjusted for

management determined risk rating.

We focused our testing of the impairment of trade and

other receivables on the key assumptions made by the

management.

Understand, evaluate and validate controls over

recognition and measurement.

Understand, evaluate and validate contracts over

recognition and measurement.

Review, evaluate and validate agreement over credit

process including age analysis of loan customers.

Critically evaluating the determination of the

expected cash flows used in assessing and

estimating impairments and the reasonableness of

any assumptions.

Evaluate whether the model used to calculate the

recoverable amount complies with the requirement of

IAS 39.

The directors are responsible for the other information. The other information comprises the Chairman’s statement,

Directors’ Report; Audit Committee’s Report, Corporate Governance Report and Bank Secretary’s report but does

not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of

assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in

doing so, consider whether the other information is materially inconsistent with the financial statements or our

knowledge obtained in the audit, or otherwise appeared to be materially misstated.

If based on the work we have performed on the other information that we obtained prior to the date of this auditors

report, we conclude that there is a material misstatement of this other information, we are required to report that fact.

We have nothing to report in this regard.

There is significant measurement uncertainty

involved in this assessment, which makes it a key

audit matter.

In the event that the IT system failed, Business

operations will be disrupted/hampered until systems

are online.

Where automated procedures were supported by

systems with identified deficiencies, we extended our

procedures to identify and test alternative controls;

and

As our audit sought to place a high level of reliance

on IT systems and application controls related to

financial reporting, a high proportion of the overall

audit effort was in this area.

Where required, we performed a greater level of

testing to validate the integrity and reliability of

associated data reporting.

Responsibilities of the Directors and Those Charged with Governance for the Financial Statements

Those charged with governance are responsible for overseeing the Bank’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

•

•

•

•

•

•

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from

material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion.

Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance

with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and

are considered material if, individually or in the aggregate, they could reasonably be expected to influence the

economic decisions of users taken on the basis of these financial statements.

The directors are responsible for the preparation and fair presentation of the financial statements in accordance with

International Financial Reporting Standards in compliance with the Financial Reporting Council of Nigeria Act, No 6,

2011 and the requirements of the Companies and Allied Matters Act, CAP C20, LFN 2004, and for such internal

control as the directors determine is necessary to enable the preparation of financial statements that are free from

material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the Bank’s ability to continue as a

going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of

accounting unless the directors either intend to liquidate the Bank or to cease operations, or have no realistic

alternative but to do so.

4

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism

throughout the audit. We also:

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error,

design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and

appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from

fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions,

misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the

Bank’s internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and

related disclosures made by the directors.

Conclude on the appropriateness of the director’s use of the going concern basis of accounting and based on the

audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast

significant doubt on the Bank’s ability to continue as a going concern. If we conclude that a material uncertainty

exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated

financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on

the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may

cause the Bank to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and

whether the financial statements represent the underlying transactions and events in a manner that achieves fair

presentation.

Obtain sufficient appropriate audit evidence regarding the financial information of the Bank to express an opinion

on the consolidated financial statements. We are responsible for the direction, supervision and performance of

the Bank audit. We remain solely responsible for our audit opinion.

We communicate with the Audit Committee regarding, among other matters, the planned scope and timing of the

audit and significant audit findings, including any significant deficiencies in internal control that we identify during our

audit.

OMOLUABI MORTGAGE BANK PLC

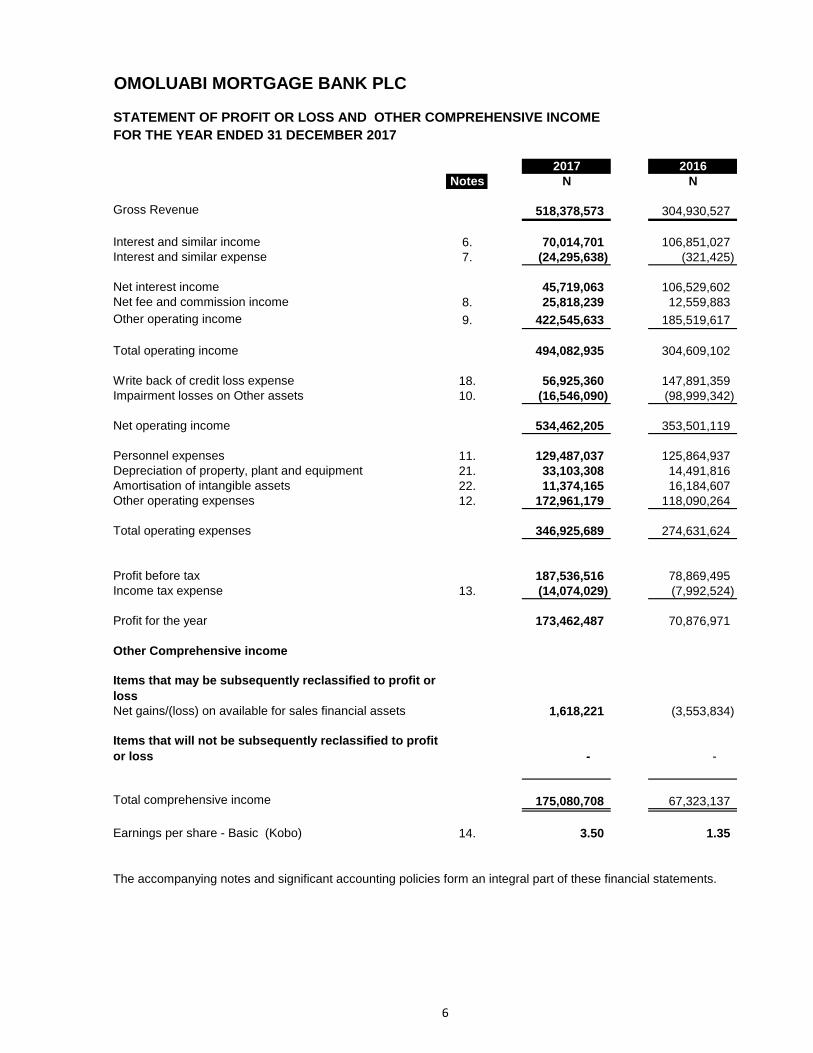

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 DECEMBER 2017

2017 2016

Notes N N

Gross Revenue 518,378,573 304,930,527

Interest and similar income 6. 70,014,701 106,851,027

Interest and similar expense 7. (24,295,638) (321,425)

Net interest income 45,719,063 106,529,602

Net fee and commission income 8. 25,818,239 12,559,883

Other operating income 9. 422,545,633 185,519,617

Total operating income 494,082,935 304,609,102

Write back of credit loss expense 18. 56,925,360 147,891,359

Impairment losses on Other assets 10. (16,546,090) (98,999,342)

Net operating income 534,462,205 353,501,119

Personnel expenses 11. 129,487,037 125,864,937

Depreciation of property, plant and equipment 21. 33,103,308 14,491,816

Amortisation of intangible assets 22. 11,374,165 16,184,607

Other operating expenses 12. 172,961,179 118,090,264

Total operating expenses 346,925,689 274,631,624

Profit before tax 187,536,516 78,869,495

Income tax expense 13. (14,074,029) (7,992,524)

Profit for the year 173,462,487 70,876,971

Other Comprehensive income

Items that may be subsequently reclassified to profit or

loss

Net gains/(loss) on available for sales financial assets 1,618,221 (3,553,834)

Items that will not be subsequently reclassified to profit

or loss - -

Total comprehensive income 175,080,708 67,323,137

Earnings per share - Basic (Kobo) 14. 3.50 1.35

The accompanying notes and significant accounting policies form an integral part of these financial statements.

6

OMOLUABI MORTGAGE BANK PLC

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 DECEMBER 2017

Available Regulatory

Issued Share Statutory Retained for Sale Risk

Capital Premium Reserves Earnings Reserves Reserves Total equity

N N N N N N N

At 1 January 2016 2,500,000,000 - 14,382,887 (148,466,521) - - 2,365,916,366

Profit for the year - - 70,876,972 - - 70,876,972

Other comprehensive Income - - - - (3,553,834) - (3,553,834)

Transfer (statutory) - - 14,175,394 (14,175,394) - - -

At 31 December, 2016 2,500,000,000 - 28,558,281 (91,764,943) (3,553,834) - 2,433,239,504

At 1 January 2017 2,500,000,000 - 28,558,281 (91,764,943) (3,553,834) - 2,433,239,504

-

Profit for the year - - 173,462,487 - - 173,462,487

Other comprehensive Income - - - - 1,618,221 1,618,221

Transfer (statutory) - - 34,692,497 (34,692,497) - - -

Proposed dividend - - - - - - -

At 31 December, 2017 2,500,000,000 - 63,250,779 47,005,046 (1,935,613) - 2,608,320,212

Statutory reserve

Regulatory risk reserve

Available for sale reserve

The revised guidelines for Primary Mortgage Banks in Nigeria require mortgage banks to make an annual appropriation to a statutory reserve. As

stipulated by section 5.4 of the of the revised guidelines, an appropriation of 20% of profit after tax is made if the statutory reserve is less than the paid

up share capital and 10% of profit after tax if the statutory reserve is equal to or in excess of the paid up capital.

The Central Bank of Nigeria stipulates that provisions for loans recognized in the profit or loss account be determined based on the requirements of

IFRS. The IFRS provision should then be compared with provision determined using the Prudential Guidelines and the expected impact/changes

treated in the retained earnings (See Statement of Prudential Adjustments).

Available For Sale (AFS) assets are measured at fair value in the balance sheet. Fair value changes on AFS assets are recognised directly in equity,

through the statement of changes in equity, except for interest on AFS assets (which is recognised in income on an effective yield basis), impairment

losses and (for interest-bearing AFS debt instruments) foreign exchange gains or losses. The cumulative gain or loss that was recognised in equity is

recognised in profit or loss when an available-for-sale financial asset is derecognised.

Attributable to equity holders

8

OMOLUABI MORTGAGE BANK PLC

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 31 DECEMBER 2017

2017 2016

Notes N N

Profit before tax 187,536,516 78,869,495

Adjustment for non-cash itemsWrite back of credit loss expense 10. (56,925,360) (147,891,359)

Impairments on other assets 20.1 15,278,132 109,592,666

Gain on disposal of assets 9. (231,300) -

Provisions for dimunition on quoted investment - 3,553,834

Profit on sales of quoted investment - (80,387)

Profit on disposal of Investment Held for sale (80,371,761) (2,560,000)

Loss on sales of mortgageable assets - 3,371,731

Depreciation of property, plant & equipment 21. 33,103,308 14,491,816

Amortisation of intangibles 22. 11,374,165 16,184,607

Cashflow before changes in working capital 109,763,700 75,532,403

Changes in working capital

Increase in loans and advances (312,238,027) (184,268,961)

Increase in other assets (436,372,137) (87,273,964)

Decrease/(increase) in non current assets 235,551,104 (383,571,384)

Increase in deposits 840,880,106 242,227,968

(Decrease)/increase other liabilities (263,604,443) 352,934,461

64,216,603 (59,951,880)

Tax paid 26. (9,085,193) (4,586,842)

Cash generated from operations 164,895,110 (64,538,722)

Cashflow from investing activities

Purchase of property, plant and equipment 21. (44,147,573) (177,650,566)

Purchase of intangible assets 22. (6,063,631) (34,615,458)

Disposal of asset held for sale - 29,371,731

Proceeds from disposal of property, plant and equipment 5,189,535 -

Proceeds from sale of held for sale assets 107,948,096 28,000,000

62,926,427 (154,894,293)

Cashflow from financing activities

Additional/(repayment of) borrowed funds 25. 109,744,583 (2,114,372)

109,744,583 (2,114,372)

Increase in cash and cash equivalent 337,566,120 (146,014,984)

Cash and cash equivalent as at beginning of period 1,696,067,590 1,842,082,574

Cash and cash equivalent as at end of period 2,033,633,710 1,696,067,590

Additional cash flow information

Cash and cash equivalent

Cash on hand (note 16) 16. 37,235,120 14,437,902

Balances with banks within nigeria 17. 341,692,030 415,382,967

Placements with banks 17. 1,654,706,560 1,266,246,721

2,033,633,710 1,696,067,590

The accompanying notes to the financial statement are an integral part of these financial statements.

Cash and cash equivalents comprise balances with less than three months' maturity from the date of acquisition,

including cash in hand, deposits held at call with other banks and other short-term highly liquid investments with original

maturities of less than three months.

9

OMOLUABI MORTGAGE BANK PLC

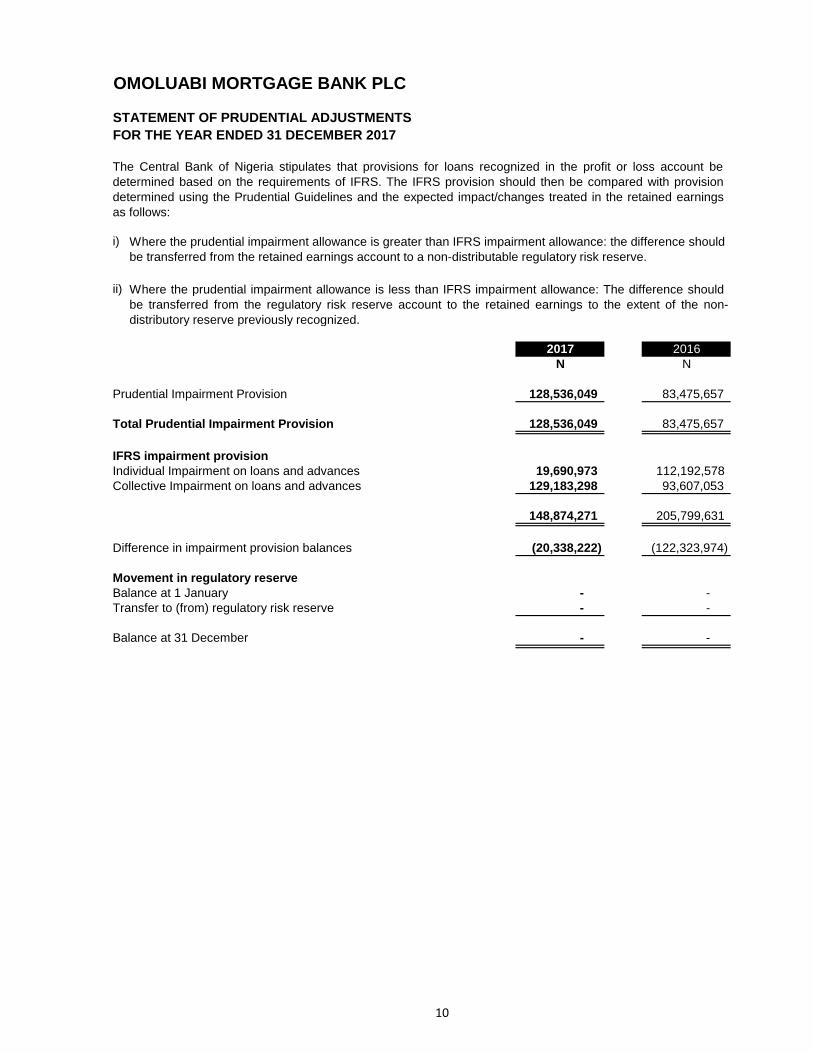

STATEMENT OF PRUDENTIAL ADJUSTMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

i)

ii)

2017 2016

N N

Prudential Impairment Provision 128,536,049 83,475,657

Total Prudential Impairment Provision 128,536,049 83,475,657

IFRS impairment provision

Individual Impairment on loans and advances 19,690,973 112,192,578

Collective Impairment on loans and advances 129,183,298 93,607,053

148,874,271 205,799,631

Difference in impairment provision balances (20,338,222) (122,323,974)

Movement in regulatory reserve

Balance at 1 January - -

Transfer to (from) regulatory risk reserve - -

Balance at 31 December - -

The Central Bank of Nigeria stipulates that provisions for loans recognized in the profit or loss account be

determined based on the requirements of IFRS. The IFRS provision should then be compared with provision

determined using the Prudential Guidelines and the expected impact/changes treated in the retained earnings

as follows:

Where the prudential impairment allowance is greater than IFRS impairment allowance: the difference should

be transferred from the retained earnings account to a non-distributable regulatory risk reserve.

Where the prudential impairment allowance is less than IFRS impairment allowance: The difference should

be transferred from the regulatory risk reserve account to the retained earnings to the extent of the non-

distributory reserve previously recognized.

10

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

1. Statement of significant accounting policies

1.1 Reporting entity

1.2 Basis of preparation

a) Statement of compliance

b) Basis of measurement

- Assets and liabilities held for trading are measured at fair;

-

-

-

- Liabilities for cash-settled share-based payment arrangements are measured at fair value;

- Available-for-sale financial assets are measured at fair value.

c) Functional and presentation currency

These financial statements are presented in Naira, which is the Bank’s functional currency.

2. Significant accounting judgments, estimates and assumptions

Going concern

Omoluabi Mortgage Bank Plc (the Bank) is a public limited liability company domiciled in Nigeria. The

address of the Bank’s registered office is Old Governor’s Office, Gbongon Road, Osogbo, Osun State.

The Bank obtained its licence to operate as a Mortgage Bank on the 24th of February, 1999 and

commenced operations in March 1999. The Bank became a public limited liability company on 13th

January, 2014.

The Bank is primarily involved in business of Residential and Commercial Mortgage financing as well as

construction finance among other financial services.

The financial statements have been prepared in accordance with International Financial Reporting

Standards (IFRSs) as issued by the International Accounting Standards Board (IASB) in the manner

required by the Companies and Allied Matters Act, Cap C20, Laws of the Federation of Nigeria 2004,

the Financial Reporting Council of Nigeria Act, 2011, the Bank’s and Other Financial Institutions Act of

Nigeria, and Relevant Central Bank of Nigeria circulars. The IFRS accounting policies have been

consistently applied to all periods presented.

The financial statements have been prepared on the historical cost basis except for the following

material items in the statement of financial position:

Financial instruments designated at fair value through profit or loss are measured at fair value;

investments in equity instruments are measured at fair value;

Other financial assets not held in a business model whose objective is to hold assets to collect

contractual cash flows or whose contractual terms do not give rise solely to payments of principal

and interest are measured at fair value;

Recognized financial assets and financial liabilities designated as hedged items in qualifying fair

value hedge relationships are adjusted for changes in fair value attributable to the risk being

hedged;

The preparation of the financial statements in conformity with IFRSs requires management to make

judgments, estimates and assumptions that affect the application of accounting policies and the reported

amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting

estimates are recognized in the period in which the estimate is revised and in any future periods affected.

The Bank’s Management has made an assessment of the Bank’s ability to continue as a going concern

and is satisfied that the Bank has the resources to continue in business for the foreseeable future.

Furthermore, Management is not aware of any material uncertainties that may cast significant doubt upon

the Bank’s ability to continue as a going concern. Therefore, Management will continue to prepare the

financial statements on the going concern basis.

11

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

Fair value of financial instruments

Impairment losses on loans and advances

Impairment of available-for-sale investments

Deferred tax assets

Determination of collateral value

The bank also records impairment charges on available–for–sale equity investments when there has been

a significant or prolonged decline in the fair value below their cost. The determination of what is

‘significant’ or ‘prolonged’ requires judgment. In making this judgment, the bank evaluates, among other

factors, historical share price movements and duration and extent to which the fair value of an investment

is less than its cost.

Deferred tax assets are recognized in respect of tax losses to the extent that it is probable that taxable

profit will be available against which the losses can be utilized. Judgment is required to determine the

amount of deferred tax assets that can be recognized, based upon the likely timing and level of future

taxable profits, together with future tax planning strategies.

The monitoring of market value of collateral is done on a regular basis. Fair value is adjusted to reflect

current market conditions. The amount of collateral required depends on the assessment of the

counterparty credit risk.

The Bank reviews its individually significant loans and advances at each statement of financial position

date to assess whether an impairment loss should be recorded in the income statement. In particular,

Management judgment is required in the estimation of the amount and timing of future cash flows when

determining the impairment loss. These estimates are based on assumptions about a number of factors

and actual results may differ, resulting in future changes to the allowance. The Present Value of such

cash flows as well as the present value of the fair value of the collateral is then compared to the Exposure

at Default.

Loans and advances that have been assessed individually and found not to be impaired and all

individually insignificant loans and advances are then assessed collectively in buckets of assets with

similar risk characteristics, to determine whether provision should be made due to incurred loss events for

which there is objective evidence but whose effects are not yet evident. The collective assessment of

impaired insignificant loans is done with a PD of 100% and the historical LGD while the collective

assessment of unimpaired insignificant loans and significant loans is done with the historical PD and LGD.

The bank reviews its debt securities classified as available–for–sale investments at each statement of

financial position date to assess whether they are impaired. This requires similar judgment as applied to

the individual assessment of loans and advances.

Where the fair values of financial assets and financial liabilities recorded on the statement of financial

position cannot be derived from active markets, they are determined using a variety of valuation

techniques that include the use of mathematical models. The inputs to these models are derived from

observable market data where possible, but where observable market data are not available, judgment is

required to establish fair values.

The Bank divides its loan portfolio into significant and insignificant loans based on Management approved

materiality threshold. The Bank also groups its risk assets into buckets with similar risk characteristics for

the purpose of collective impairment of insignificant loans and unimpaired significant loans.

The Probability of Default (PD) and the Loss Given default (LGD) are then computed using historical data

from the loan buckets.

12

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

3. Accounting development and impact

3.1 Summary of Standards and Interpretations effective for the first time

a Amendments to IFRS 12 Disclosure of Interests in Other Entities

b Amendments to IFRS for SMEs

Three amendments are however of larger impact:

-

-

-

c Amendments to IAS 7 Statement of Cash Flows

d Amendments to IAS 12 Income Taxes

-

- The carrying amount of an asset does not limit the estimation of probable future taxable profits.

-

-

3.2

3.2.1 Amendments effective from annual periods beginning on or after 1 January 2018

This amendment clarifies the scope of the standard by specifying that the disclosure requirements in

the standard, except for those in paragraphs B10–B16, apply to an entity’s interests listed in paragraph 5

that are classified as held for sale, as held for distribution or as discontinued operations in accordance

with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations

The standard now allows an option to use the revaluation model for property, plant and equipment as

not allowing this option has been identified as the single biggest impediment to adoption of the IFRS

for SMEs in some jurisdictions in which SMEs commonly revalue their property, plant and equipment

and/or are required by law to revalue property, plant and equipment;

The main recognition and measurement requirements for deferred income tax have been aligned with

current requirements in IAS 12 Income Taxes (in developing the IFRS for SMEs, the IASB had

already anticipated finalization of its proposed changes to IAS 12, however, these changes were

never finalized); and

The main recognition and measurement requirements for exploration and evaluation assets have

been aligned with IFRS 6 Exploration for and Evaluation of Mineral Resources to ensure that the IFRS

for SMEs provides the same relief as full IFRSs for these activities.

Unrealized losses on debt instruments measured at fair value and measured at cost for tax purposes

give rise to a deductible temporary difference regardless of whether the debt instrument's holder

expects to recover the carrying amount of the debt instrument by sale or by use.

This amendment to IAS7 clarify that entities shall provide disclosures that enable users of financial

statements to evaluate changes in liabilities arising from financing activities

Standards and interpretations issued/amended but not yet effective.

Estimates for future taxable profits exclude tax deductions resulting from the reversal of deductible

temporary differences.

Amends to recognition of deferred tax assets for unrealized losses, IAS 12 Income Taxes clarify the

following aspects:

An entity assesses a deferred tax asset in combination with other deferred tax assets. Where tax law

restricts the utilization of tax losses, an entity would assess a deferred tax asset in combination with

other deferred tax assets of the same type.

At the date of authorisation of these financial statements the following standards, amendments to existing

standards and interpretations were in issue, but not yet effective: This includes:

13

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

a Amendments to IFRS 2 Share-based Payment

b Amendments to IFRS 4 Insurance Contracts

-

Amends IFRS 4 Insurance Contracts provide two options for entities that issue insurance contracts within

the scope of IFRS 4:

An option that permits entities to reclassify, from profit or loss to other comprehensive income, some

of the income or expenses arising from designated financial assets; this is the so called overlay

Amends IFRS 2 Share-based Payment to clarify the standard in relation to the accounting for cash settled

share-based payment transactions that include a performance condition, the classification of share-based

payment transactions with net settlement features, and the accounting for modifications of share-based

payment transactions from cash-settled to equity-settled

14

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

-

c Amendments to IFRS 15 'Revenue from Contracts with Customers

- Identify the contract with the customer

- Identify the performance obligations in the contract

- Determine the transaction price

- Allocate the transaction price to the performance obligations in the contracts

- Recognize revenue when (or as) the entity satisfies a performance obligation.

d Amendments to IFRS 9 Financial Instruments

-

-

-

-

e Amendments to IAS 40 Investment Property

f Amendments to IFRS 1 First-time Adoption of International Financial Reporting Standards

Amends paragraph 57 to state that an entity shall transfer a property to, or from, investment property

when, and only when, there is evidence of a change in use. A change of use occurs if property meets, or

ceases to meet, the definition of investment property. A change in management’s intentions for the use of

a property by itself does not constitute evidence of a change in use. The list of examples of evidence in

Derecognition. The requirements for derecognition of financial assets and liabilities are carried

forward from IAS 39.

Amendments’ resulting from Annual Improvements 2014–2016 Cycle, the amendment deletes the short-

term exemptions in paragraphs E3–E7 of IFRS 1, because they have now served their intended purpose.

An optional temporary exemption from applying IFRS 9 for entities whose predominant activity is

issuing contracts within the scope of IFRS 4; this is the so-called deferral approach.

The application of both approaches is optional and an entity is permitted to stop applying them before the

new insurance contracts standard is applied.

IFRS 15 provides a single, principles based five step model to be applied to all contracts with customers.

The five steps in the model are as follows:

Guidance is provided on topics such as the point in which revenue is recognized, accounting for variable

consideration, costs of fulfilling and obtaining a contract and various related matters. New disclosures

about revenue are also introduced.

Amends IFRS 15 Revenue from Contracts with Customers also clarify three aspects of the standard

(identifying performance obligations, principal versus agent considerations, and licensing) and to provide

some transition relief for modified contracts and completed contracts

A finalized version of IFRS 9 which contains accounting requirements for financial instruments, replacing

IAS 39 Financial Instruments: Recognition and Measurement. The standard contains requirements in the

following areas:

Classification and measurement. Financial assets are classified by reference to the business model

within which they are held and their contractual cash flow characteristics. The 2014 version of IFRS 9

introduces a 'fair value through other comprehensive income' category for certain debt instruments.

Financial liabilities are classified in a similar manner to under IAS 39; however there are differences in

the requirements applying to the measurement of an entity's own credit risk.

Impairment. The 2014 version of IFRS 9 introduces an 'expected credit loss' model for the

measurement of the impairment of financial assets, so it is no longer necessary for a credit event to

have occurred before a credit loss is recognized

Hedge accounting. Introduces a new hedge accounting model that is designed to be more closely

aligned with how entities undertake risk management activities when hedging financial and non-

financial risk exposures

15

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

g Amendments to IAS 28 Investments in Associates and Joint Ventures

3.2.2 Amendments effective from annual periods beginning on or after 1 January 2019

a

Effective for an annual periods beginning on or after 1 January 2019

- IFRS 16 substantially carries forward the lessor accounting requirements in IAS 17. Accordingly, a lessor

continues to classify its leases as operating leases or finance leases, and to account for those two types

of leases differently;

- IFRS 16 contains expanded disclosure requirements for lessees. Lessees will need to apply judgement

in deciding upon the information to disclose to meet the objective of providing a basis for users of financial

statements to assess the effect that lease;

- New standard that introduces a single lessee accounting model and requires a lessee to recognise

assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of

low value. A lessee is required to recognise a right-of-use asset representing its right to use the underlying

leased asset and a lease liability representing its obligation to make lease payments. A lessee measures

right-of-use assets similarly to other non-financial assets (such as property, plant and equipment) and

lease liabilities similarly to other financial liabilities. As a consequence, a lessee recognises depreciation of

the right-of-use asset and interest on the lease liability, and also classifies cash repayments of the lease

liability into a principal portion and an interest portion and presents them in the statement of cash flows

applying IAS 7 Statement of Cash Flows;

- IFRS 16 also requires enhanced disclosures to be provided by lessors that will improve information

disclosed about a lessor’s risk exposure, particularly to residual value risk;

- New standard that introduces a single lessee accounting model and requires a lessee to recognise

assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of

low value. A lessee is required to recognise a right-of-use asset representing its right to use the underlying

leased asset and a lease liability representing its obligation to make lease payments. A lessee measures

right-of-use assets similarly to other non-financial assets (such as property, plant and equipment) and

lease liabilities similarly to other financial liabilities. As a consequence, a lessee recognises depreciation of

the right-of-use asset and interest on the lease liability, and also classifies cash repayments of the lease

liability into a principal portion and an interest portion and presents them in the statement of cash flows

applying IAS 7 Statement of Cash Flows.

- IFRS 16 contains expanded disclosure requirements for lessees. Lessees will need to

apply judgement in deciding upon the information to disclose to meet the objective of providing a basis for

users of financial statements to assess the effect that leases have on the financial position, financial

performance and cash flows of the lessee.

- IFRS 16 substantially

carries forward the lessor accounting requirements in IAS 17. Accordingly, a lessor continues to classify

its leases as operating leases or finance leases, and to account for those two types of leases differently.

- IFRS 16 also requires enhanced disclosures to be provided by lessors

that will improve information disclosed about a lessor’s risk exposure, particularly to residual value risk.

- IFRS 16 supersedes the following Standards and

Interpretations:

a) IAS 17 Leases;

b) IFRIC 4 Determining whether an Arrangement contains a Lease;

c) SIC-15 Operating Leases—Incentives; and

d) SIC-27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease.

This amendment Clarifies that the election to measure at fair value through profit or loss an investment in

an associate or a joint venture that is held by an entity that is a venture capital organization, or other

qualifying entity, is available for each investment in an associate or joint venture on an investment by

investment basis, upon initial recognition.

IFRS 16 'Leases'

16

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

3.2.3 New standards, amendments and interpretations issued but without an effective date

a Amendments to IFRS 9 Financial Instruments

IFRS 9 introduces new requirements for classifying and measuring financial assets, as follows:

-

-

-

-

All other instruments (including all derivatives) are measured at fair value with changes recognized in

the profit or loss

Investments in equity instruments can be designated as 'fair value through other comprehensive

income' with only dividends being recognized in profit or loss

Debt instruments meeting both a 'business model' test and a 'cash flow characteristics' test are

measured at amortised cost (the use of fair value is optional in some limited circumstances)

At the date of authorisation of these financial statements the following standards, amendments to existing

standards and interpretations were in issue, but without an effective: This includes:

Also a revised version of IFRS 9 incorporating requirements for the classification and measurement of

financial liabilities, and carrying over the existing derecognition requirements from IAS 39 Financial

Instruments: Recognition and Measurement.

The concept of 'embedded derivatives' does not apply to financial assets within the scope of the

Standard and the entire instrument must be classified and measured in accordance with the above

guidelines.

17

OMOLUABI MORTGAGE BANK PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2017

b

-

-

4. Significant accounting policies

4.1 Revenue recognition

These requirements apply regardless of the legal form of the transaction, e.g. whether the sale or

contribution of assets occurs by an investor transferring shares in a subsidiary that holds the assets

(resulting in loss of control of the subsidiary), or by the direct sale of the assets themselves.

Require the partial recognition of gains and losses where the assets do not constitute a business, i.e.

a gain or loss is recognized only to the extent of the unrelated investors’ interests in that associate or

Amends IFRS 10 Consolidated Financial Statements and IAS 28 Investments in Associates and Joint

Ventures (2011) to clarify the treatment of the sale or contribution of assets from an investor to its

associate or joint venture, as follows:

The revised financial liability provisions maintain the existing amortised cost measurement basis for most

liabilities. New requirements apply where an entity chooses to measure a liability at fair value through

profit or loss in these cases, the portion of the change in fair value related to changes in the entity's own

credit risk is presented in other comprehensive income rather than within profit or loss.

Amendments to IFRS 10 and IAS 28 Consolidated Financial Statements and Investments in

Associates and Joint Ventures

Require full recognition in the investor's financial statements of gains and losses arising on the sale or

contribution of assets that constitute a business (as defined in IFRS 3 Business Combinations)

The accounting policies set out below have been applied consistently to all periods presented in these

financial statements.

Interest income is recognized in profit or loss using the effective interest method. The effective interest

rate is the rate that exactly discounts the estimated future cash payments and receipts through the

expected life of the financial asset or liability (or, where appropriate, a shorter period) to the carrying

amount of the financial asset or liability. When calculating the effective interest rate, the bank estimates

future cash flows considering all contractual terms of the financial instrument, but not future credit losses.

The calculation of the effective interest rate includes all transaction costs and fees and points paid or

received that are an integral part of the effective interest rate. Transaction costs include incremental costs

that are directly attributable to the acquisition or issue of a financial asset or liability.

Interest income and expense presented in the statement of comprehensive income include interest on

financial assets and financial liabilities measured at amortized cost calculated on an effective interest

basis. Interest income and expense on all trading assets and liabilities are considered to be incidental to