Omega Pharma Consumer Health O T C - midcapforums.com · In 2011, Omega Pharma will have an...

22

p. 1 January-February 2008 Omega Pharma Consumer Health A pure OTC company with a strong balance sheet O T C O T C

Transcript of Omega Pharma Consumer Health O T C - midcapforums.com · In 2011, Omega Pharma will have an...

p. 1

January-February 2008

Omega Pharma

Consumer Health

A pure OTC company

with a strong balance sheet

O T CO T C

p. 2

January-February 2008

The OTC market

Definition Omega Pharma: all products available at the

pharmacy that can be bought without doctor’s prescription

OTC

Dermo-cosmetics

Food supplements

Non-prescription pharma-ceuticals

Medical devices

p. 3

January-February 2008

Brief history: 20 years of growth

� 1987: foundation by 2 pharmacists, including Marc Coucke

� “By pharmacists, for pharmacists”

� 1994: MBO by Marc Coucke

� 1998: IPO � acquisitions � critical mass + diversification

� 1998 ���� development B2B/Arseus

� 2000 ���� international development of OTC

� 2000 – Pharmygiène � France

� 2000 - Chefaro � Spain, UK, Germany, the Netherlands

� 2004 – Wartner + 60 ex-Pfizer brands � brand portfolio

� 2004 – Medestea, Aco Hud � Italy and Scandinavia

� 2007 – Bittner Pharma � rest of Europe, Russia, Ukraine,…

� 5 Oct. 2007: IPO Arseus

� � Omega = pure OTC player

� � Strong balance sheet

Marc Coucke, co-founder and current Chairman of

the Board

p. 4

January-February 2008

Omega Pharma today

� Pure OTC company

� Carve-out Arseus (24% participation through equity method)

� In Belgium (and only in Belgium) also long-term partnership with

EG/Stada for distribution of generics

� 5 reporting segments

� Belgium: historical home market

� France: first market abroad since 2000 – integrated in 2005-2006

� North-Europe: Scandinavia, Germany

� South-Europe: Portugal-Spain-Italy-Greece

� Rest of Word: CEE and key account markets (UK, Ireland,

Netherlands)

• Entered CEE in January 2007

• First step beyond Western Europe

S-Europe

18%

N-Europe

13%

ROW

21%

France

23%

Belgium

25%

Emerging

Markets

9%

Western

Europe

91%

p. 5

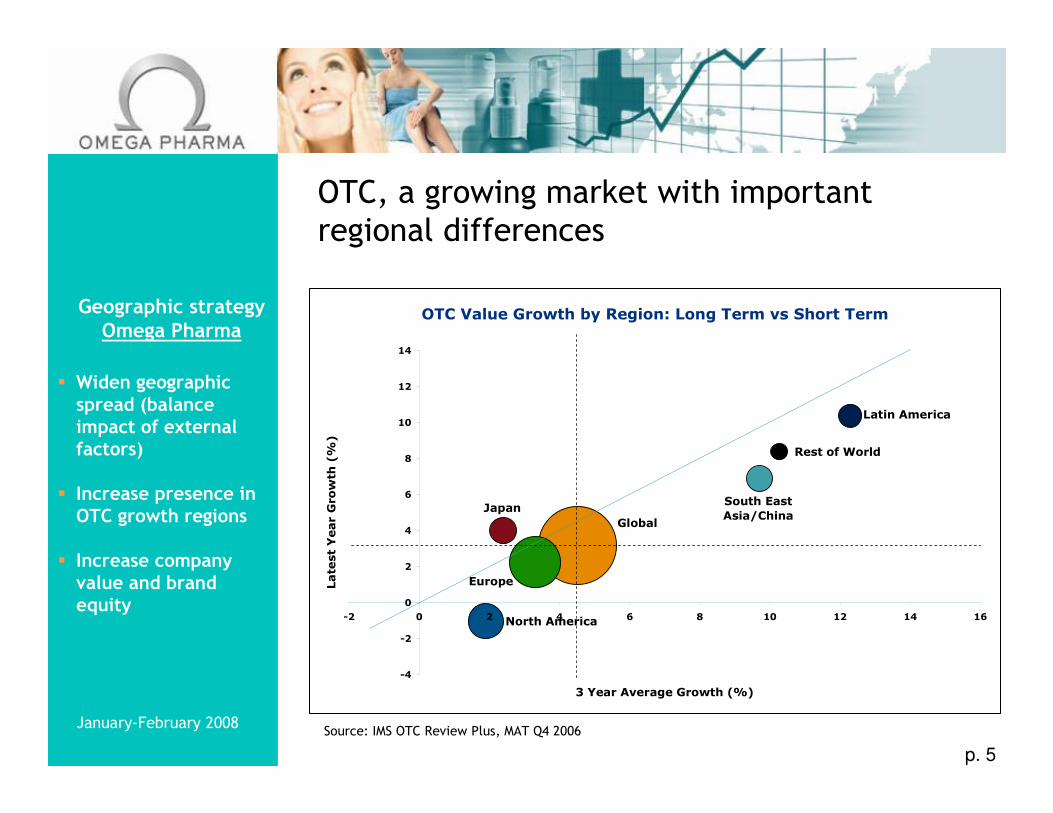

January-February 2008

OTC, a growing market with important

regional differences

OTC Value Growth by Region: Long Term vs Short Term

Rest of World

Global

Europe

North America

JapanSouth East

Asia/China

Latin America

-4

-2

0

2

4

6

8

10

12

14

-2 0 2 4 6 8 10 12 14 16

3 Year Average Growth (%)

Latest Year Growth (%)

Source: IMS OTC Review Plus, MAT Q4 2006

Geographic strategy Omega Pharma

� Widen geographic spread (balance impact of external factors)

� Increase presence in OTC growth regions

� Increase company value and brand equity

p. 6

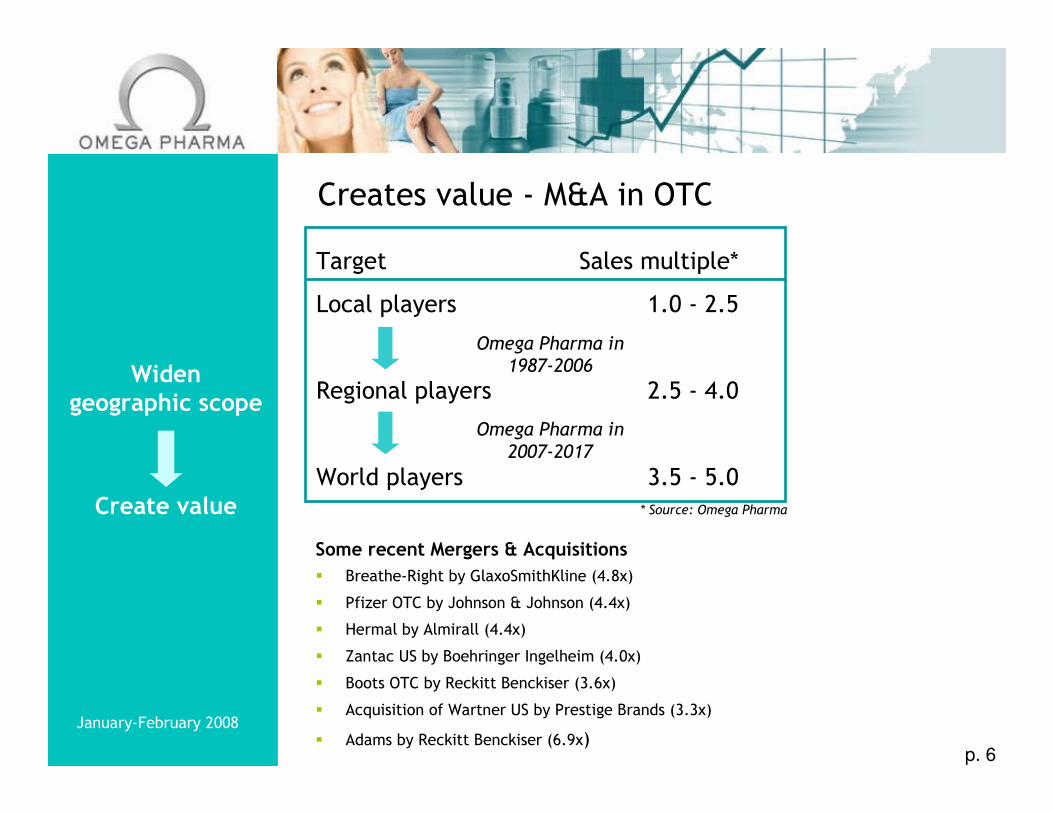

January-February 2008

Creates value - M&A in OTC

Target Sales multiple*

Local players 1.0 - 2.5

Regional players 2.5 - 4.0

World players 3.5 - 5.0

Some recent Mergers & Acquisitions

� Breathe-Right by GlaxoSmithKline (4.8x)

� Pfizer OTC by Johnson & Johnson (4.4x)

� Hermal by Almirall (4.4x)

� Zantac US by Boehringer Ingelheim (4.0x)

� Boots OTC by Reckitt Benckiser (3.6x)

� Acquisition of Wartner US by Prestige Brands (3.3x)

� Adams by Reckitt Benckiser (6.9x)

Create value * Source: Omega Pharma

Omega Pharma in

1987-2006

Omega Pharma in

2007-2017

Widen geographic scope

p. 7

January-February 2008

Worldwide OTC ranking

Source: OTC Bulletin, 31 May 2007 (based on the figures reported by the companies concerned)

(*) The acquisition of the OTC activities from Pfizer is not yet fully included in the 2006 figures of

Johnson&Johnson.

(**) = 100 % since IPO Arseus

OTC Market

� Highly fragmented

market (top 10

companies = 33% of

world market)

� Market

consolidation

expected in 2008-

2010.

� Most companies

still have dual focus

(Rx – OTC).

� Omega Pharma is

the only pure OTC

player worldwide.

� Omega Pharma has

a unique business

model.

No separate reporting for OTCNovartis

No separate reporting for OTCSanofi-Aventis

No separate reporting for OTCProcter & Gamble

6.4%EUR 398 millionConsumer Health CareMerck KGaA

5.3%EUR 415 millionOTCSchering Plough

72%**EUR 729 millionConsumer HealthOmega Pharma **

61.8%EUR 916 millionSelf MedicationTaisho

10.1%EUR 1 064 millionConsumer Health CareBoehringer Ing.

25.0%EUR 1 814 millionHealth & Personal CareReckitt Benckiser

12.4%EUR 1 882 millionConsumer HealthcareWyeth

5.1%EUR 2 040 millionMcNeil OTC & NutritionalsJohnson & Johnson *

6.4%EUR 2 207 millionOTC MedicinesGlaxoSmithKline

21.6%EUR 2 531 millionConsumer CareBayer HealthCare

OTC as % oftotal group turnover

Turnover of theOTC divisionin 2006

OTC divisionGroup

The new ambition

p. 8

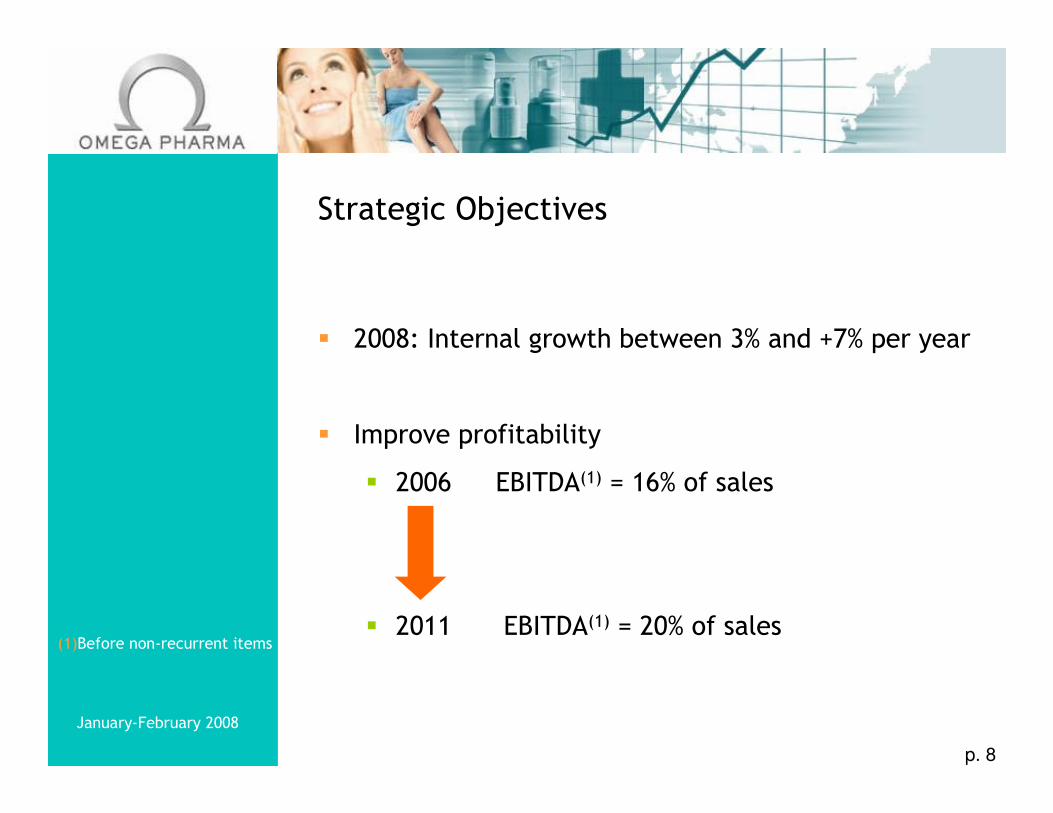

January-February 2008

Strategic Objectives

� 2008: Internal growth between 3% and +7% per year

� Improve profitability

� 2006 EBITDA(1) = 16% of sales

� 2011 EBITDA(1) = 20% of sales(1)Before non-recurrent items

p. 9

January-February 2008

3. Operational Excellence

2. Strengthen Star Brand &

Core Category approach

1. More focus on growth markets

�

� � �

� � �

Internal

sales

growth

� � �

� � �

� �

EBITDA

≥ 20%

Clear action programs

p. 10

January-February 2008

Source: OTCims and MIDAS – Data to Quarter 4 in both years

14

54

22

105

15

-40 0 40 80 120

TotalChange

LineExtn.

NewProds

PriceChange

BaseVolumeChange

CEE

9

3

13

4

-11

-40 -20 0 20 40

TotalChange

LineExtn.

NewProds

PriceChange

BaseVolumeChange

Western Europe

1. More focus on growth areas

/CIS

OTC market growth 2001-2006

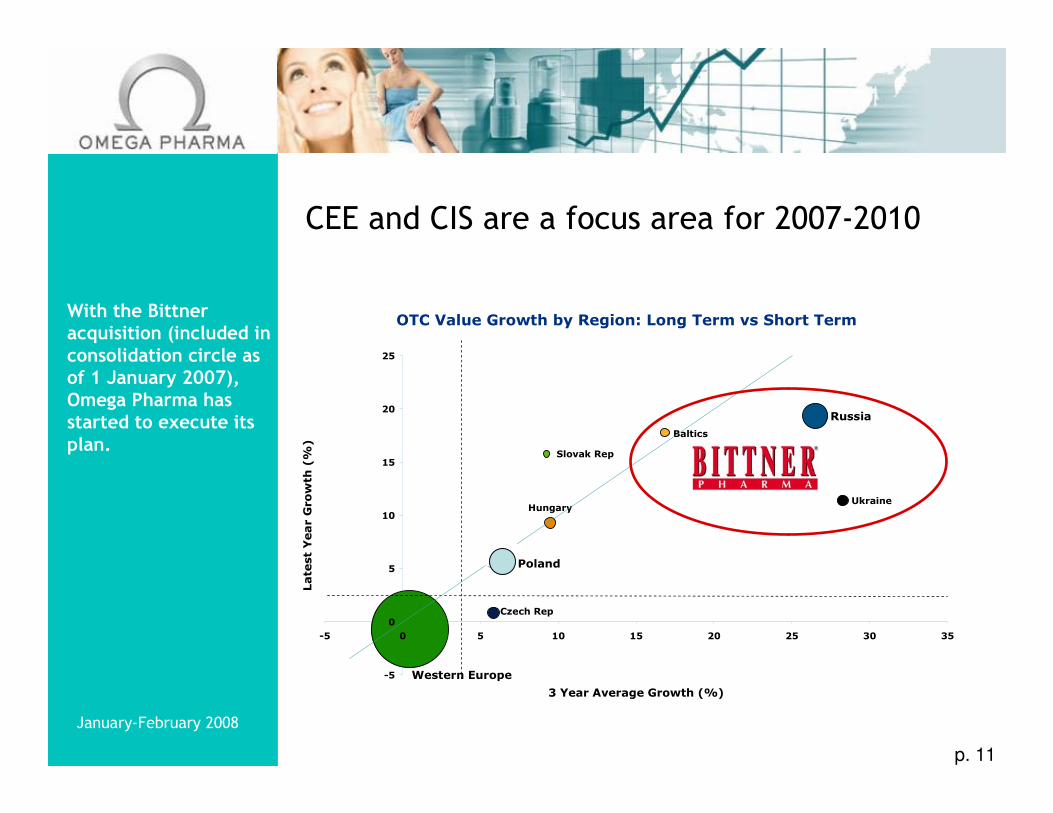

p. 11

January-February 2008

OTC Value Growth by Region: Long Term vs Short Term

Slovak Rep

Western Europe

UK

Russia

Poland

Czech Rep

HungaryUkraine

Baltics

-5

0

5

10

15

20

25

-5 0 5 10 15 20 25 30 35

3 Year Average Growth (%)

Latest Year Growth (%)

With the Bittner acquisition (included in consolidation circle as of 1 January 2007), Omega Pharma has started to execute its plan.

CEE and CIS are a focus area for 2007-2010

p. 12

January-February 2008

5060 67

5040 33

0%

50%

100%

2006 9m2007 2011e

Star Brand & Core Categories Other brands

In 2011, Omega Pharma will have an integrated portfolio, fully competitive with peers ���� 2/3 = international activities

Contribution to Omega Pharma’s branded OTC sales (in %)

2. Star Brand & Core Category approach

p. 13

January-February 2008

Non-Core &

Generics

Anti-InsectNatural Remedies

Home Diagnostics

Dermo Category

2. Star Brand & Core Category approachCore Categories

� 62% of 2007 Sales

� Higher Gross Margin

� Top 3 position in (niche) segments

� High potential for further group synergies

2007 turnover per

product category

38%

Synergy Potential

� Product Development

� Marketing Concepts

� Marketing Communication

� Production & Procurement

p. 14

January-February 2008

Anti-Insect Products

Home diagnostics

Natural Remedies

DermoProducts

Anti-Headlice

Products

Anti-Mosquito

Products

Dermo-

therapeutics

Dermo-

cosmetics

Sun Care

Products

Slimming

Products

Herbal Products

VMS

Sleeping Aids

Core Categories

Organized in a way to maximize group synergies – both in the fields of Production & Procurement and Product Development & Marketing

p. 15

January-February 2008

Strong in innovation

� Product development and marketing innovation

� Center of Excellence for each Core Category

p. 16

January-February 2008

Further development CEE/CIS

Roll out

Star Brands

in CEE/CIS

(3 in 2008)

p. 17

January-February 2008

Transversal

Efficiency

Marketing &

New Product

Development

Flow of

Information

Procurement

& Production

Flow of Goods

Profitable and Sustainable Growth

3. Operational Excellence

p. 18

January-February 2008

Omega Pharma - 1st Half 2007

(1) Before non-recurrent items

and corporate costs 18.6%+28%78.7+14%422.0Consumer Health (OTC)

29.6%+65%21.1+53%71.4Omega Europe ‘Rest Of World’

20.7%+38%17.4+12%84.1Omega Pharma Southern Europe

26.4%+7%14.3+5%54.1Omega Pharma Northern Europe

25.2%+36%52.8+21%209.6Omega Pharma Europe

11.0%+35%10.8+12%98.4Omega Pharma France

13.3%+3%15.1+4%113.9Omega Pharma Belgium

1H07 margin

Growth2007Growth2007Consolidated results

in EUR million (in %)

EBITDA (1)TurnoverNon-audited management figures

p. 19

January-February 2008

Omega Pharma – 2nd Half 2007

+8%729.4789.1+2%367.2Consumer Health (OTC)

+42%110.5157.2+34%85.8Omega Europe ‘Rest Of World’

+10%129.6143.1+9%59.0Omega Pharma Southern Europe

+3%96.399.6+1%45.5Omega Pharma Northern Europe

+19%336.4400.0+17%190.4Omega Pharma Europe

+10%172.8190.4+8%92.0Omega Pharma France

-10%220.2198.7-23%84.8Omega Pharma Belgium

Growth20062007Growth2007Consolidated results

in EUR million (in %)

Full Year Turnover2nd Half -Turnover

Non-audited management figures

+ 50 million euro below initial

expectations because of:

• Poor summer in Europe -19m (e)

• Substantial drop in dynamics of

Generics in Belgium -31m (e)

• Good performance in South-

Europe, Nordics, France, CEE

• Business fundamentals intact

• Strategic ambitions remain valid

Generics Belgium

� Significant part of turnover in Belgium

� Partnerships with Eurogenerics/Stada

� Generic penetration from 3% to 8%. Still below EU average.

� EG holds >50% MS

� Promising products become off-patent in near future:

� EPO (2008, hemo-dialysis, cancer)

� Recombinate (2008, hemophylia)

� Betaferon (2008, multiple sclerosis)

� Efexor (2008, depression, fobia)

� Xenical (2009, overweight)

� …

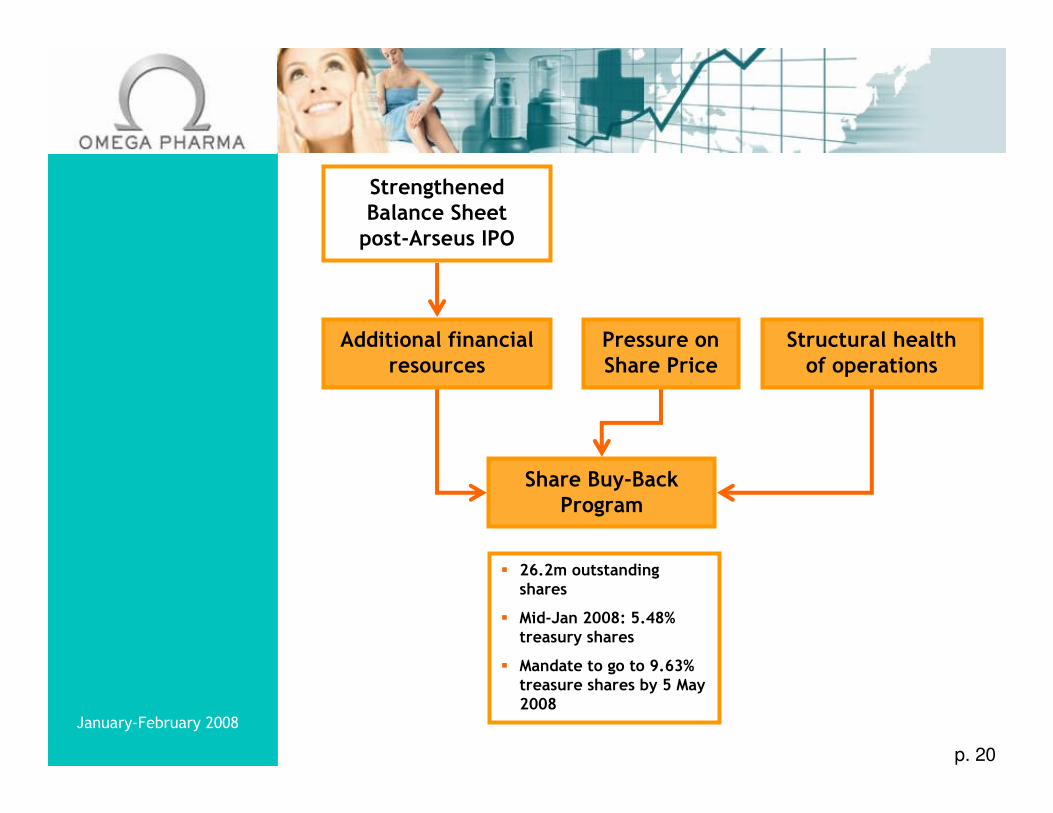

p. 20

January-February 2008

Strengthened Balance Sheet post-Arseus IPO

Share Buy-Back Program

Structural health of operations

Pressure on Share Price

Additional financial resources

� 26.2m outstanding shares

� Mid-Jan 2008: 5.48% treasury shares

� Mandate to go to 9.63% treasure shares by 5 May 2008

p. 21

January-February 2008

Omega OTC Conclusions

� Unique positioning in very attractive market

� Fundamentally strong business model with high

value creation

� High growth potential

� Further internationalisation

� Focus on growth areas

� Star Brands internationalisation

� Cross-selling of products

� Product innovation

� Corporate development / licensing-in

� Local initiatives

� High synergy potential

� Good organic/external growth opportunities

Strengths

� OTC focus

� Pharmacists’

network

� Brand strategy

� Segment selection

� Cross fertilization

Opportunities

� Attractiveness of

OTC worldwide

(CEE, SE-Asia, Latin

America)

� Active role in

consolidation of the

European OTC

market

� Competition not

focused on OTC (Rx

or mass market)

p. 22

January-February 2008

This presentation includes forward-looking statements (statements

that are not historical facts and relate to the future activities and

performance) that involve risks and uncertainties. These forward-

looking statements include statements about future strategies and the

anticipated benefits of these strategies, and they are subject to risks

and uncertainties. Actual results may differ materially from those

stated in any forward-looking statement based on a number of factors,

including the early stage of Omega Pharma group’s consideration of

these strategies, the possibility that Omega Pharma group may decide

not to implement these strategies, the ability of Omega Pharma group

to successfully implement them, and the possibility that the

anticipated benefits of these strategies are not achieved. Omega

Pharma group assumes no obligation to update the information

contained in this presentation.