Oliver Tant, Chief Financial Officer

25

Discipline Oliver Tant, Chief Financial Officer

Transcript of Oliver Tant, Chief Financial Officer

Discipline

Oliver Tant, Chief Financial Officer

2 |

Disclaimer

Certain statements in this presentation

constitute or may constitute forward-looking

statements. Any statement in this

presentation that is not a statement of

historical fact including, without limitation,

those regarding the Company’s future

expectations, operations, financial

performance, financial condition and

business is or may be a forward-looking

statement. Such forward-looking statements

are subject to risks and uncertainties that

may cause actual results to differ materially

from those projected or implied in any

forward-looking statement. These risks and

uncertainties include, among other factors,

changing economic, financial, business or

other market conditions. These and other

factors could adversely affect the outcome

and financial effects of the plans and events

described in this presentation. As a result,

you are cautioned not to place any reliance

on such forward-looking statements. The

forward-looking statements reflect knowledge

and information available at the date of this

presentation and the Company undertakes no

obligation to update its view of such risks and

uncertainties or to update the forward-looking

statements contained herein. Nothing in this

presentation should be construed as a profit

forecast or profit estimate and no statement

in this presentation should be interpreted to

mean that the future earnings per share of

the Company for current or future financial

years will necessarily match or exceed the

historical or published earnings per share of

the Company. This presentation has been

prepared for, and only for the members of the

Company, as a body, and no other persons.

The Company, its directors, employees,

agents or advisers do not accept or assume

responsibility to any other person to whom

this presentation is shown or into whose

hands it may come and any such

responsibility or liability is expressly

disclaimed. The material in this presentation

is not provided for tobacco product

advertising or promotional purposes. This

material does not constitute and should not

be construed as constituting an offer to sell,

or a solicitation of an offer to buy, any

tobacco products. The Company’s products

are sold only in compliance with the laws of

the particular jurisdictions in which they are

sold.

Imperial Brands Investor Day | June 2016

3 |

Quality, Agility, Discipline

Sustainability

Driving revenue, margins, cash and dividend growth

Quality Agility Discipline

Brand, product and

market choices

Simplification and

continuous

improvement

Resource, cost

and cash

optimisation

Imperial Brands Investor Day | June 2016

Consistent themes

4 |

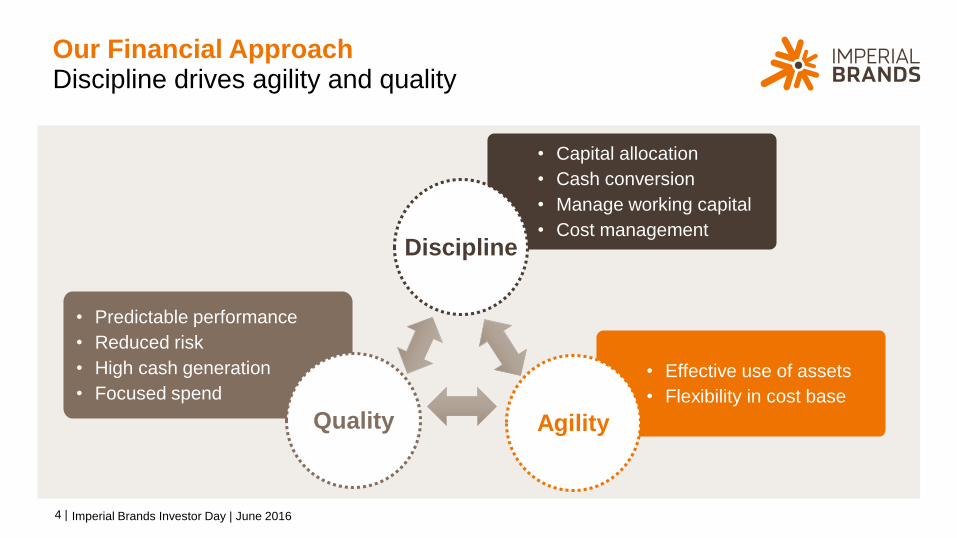

Our Financial Approach

Imperial Brands Investor Day | June 2016

Discipline drives agility and quality

• Capital allocation

• Cash conversion

• Manage working capital

• Cost management

• Effective use of assets

• Flexibility in cost base

• Predictable performance

• Reduced risk

• High cash generation

• Focused spend

Discipline

Quality Agility

5 |

Cash flow from

operations

Dividend growth of

at least 10% pa

Reduction of net debt

Investment in strongest

brands and key markets

Uses of CashSources of Cash

Clearly

defined

prioritiesWorking capital

efficiency

Effective asset

management

Capital Allocation

Imperial Brands Investor Day | June 2016

Focused use of cash

6 |

Average2011-13

2013 2014 2015 HY16 Target

82%

86%

91%

97%

105%

95%

Cash Conversion

• Key KPI

• ‘Incremental’ £850m cash

FY13–FY15 versus

previous average

Imperial Brands Investor Day | June 2016

Consistent improvement

7 |

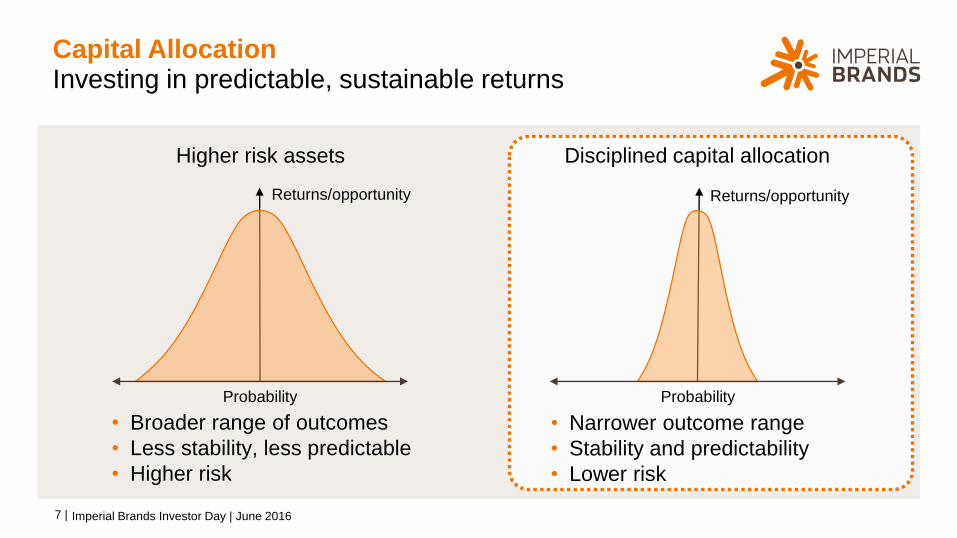

Capital Allocation

Higher risk assets

Imperial Brands Investor Day | June 2016

Investing in predictable, sustainable returns

Disciplined capital allocation

Returns/opportunity

Probability Probability

Returns/opportunity

• Narrower outcome range

• Stability and predictability

• Lower risk

• Broader range of outcomes

• Less stability, less predictable

• Higher risk

8 |

Net Debt

Imperial Brands Investor Day | June 2016

Capital discipline supports de-leverage

£2.1bn reduction

in like-for-like

debt since FY13

Closing adj.net debt

FY13

Like-for-likereduction

Closing adj.net debt

FY14

Like-for-likereduction

Adj. net debtpre-acquisition

cost

USAacquisition

cost

Closing adj.net debt

FY15

£9.1bn £8.1bn £7.0bn £11.6bn

£1.0bn£1.1bn

£4.6bn

9 |

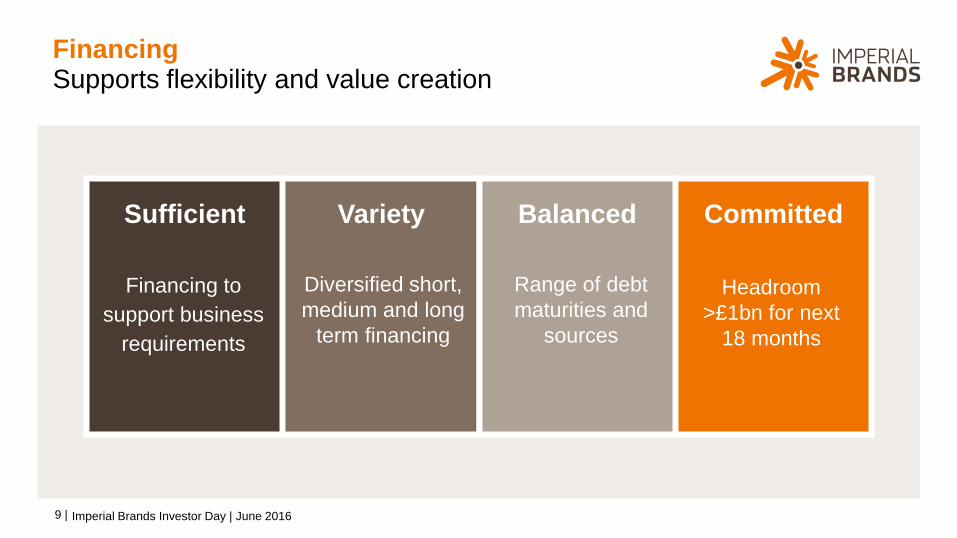

Financing

Imperial Brands Investor Day | June 2016

Supports flexibility and value creation

Sufficient Variety Balanced Committed

Financing to

support business

requirements

Diversified short,

medium and long

term financing

Range of debt

maturities and

sources

Headroom

>£1bn for next

18 months

10 |

Financing Structure

• Maturity spread to manage refinancing risk and cash profile

• No financing requirement over the next 18 months

• ECP has diversified short term financing reducing reliance on bank debt

Imperial Brands Investor Day | June 2016

Matched to the needs of the business

68%

32%

0

500

1,000

1,500

2,000

2,500

3,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032

£m

Bond issues Bank debt

Interest split

Fixed

≈

2032

c.£2.0bn

ECP

Bank c.£4.5bn

c.£11.1bnBond

Diversified funding sources

Bank debt £1bn term loan & £3.5bn RCF (undrawn) Floating

11 |

Credit Ratings

• Committed to investment grade

status

• ‘Efficient’ rating with stable outlooks

• A- (S&P, Fitch) and A3 (Moody’s)

generate only c.30bps benefit in

finance costs

• Recent Moody’s outlook stabilised

Imperial Brands Investor Day | June 2016

Stable grading with all agencies

Non investment

grade

Non investment

grade

Non investment

grade

Stable Outlook

A+

A

A-

BBB+

BBB

BBB-

Stable Outlook

S&P Fitch Moody’s

A1

A2

A3

Baa1

Baa2

Baa3 Stable Outlook

12 |

Managing Working Capital

Imperial Brands Investor Day | June 2016

Supports better cash generation

Stock CreditorsDebtors

FY14 FY15

• Supplier days on renegotiated

‘indirects’ improved by c.50%

• 10% reduction in debtor days

over past 2 years

FY13 FY15FY13 FY15

• 22% reduction in leaf stock

versus 10% volume decline

13 |

Managing Costs

Imperial Brands Investor Day | June 2016

Significant annual savings

• Changes ensure more efficient cost base

• Delivering £300m annual savings

FY13: £30m

£300m

FY14: £60m

FY15: £85m

£55m

£70m

To date FY16 To go By FY18

Manufacturing & supply chain

Sales & Marketing

Global procurement

Back office

Other

• Savings across all parts of business

• Reduced product cost, operating cost &

overheads

14 |

Shared Services

Imperial Brands Investor Day | June 2016

Simplify process, increase focus, better performance

• Leverage scale to harmonise process

• Increased cost base flexibility

• More effective service culture & customer focus

• Performance focus and continuous improvement

• Rolling out shared services for finance, HR and IS

• Centres in Poland, Philippines, Hungary & Czech Republic

15 |

Increasing Cost Base Flexibility

Imperial Brands Investor Day | June 2016

Agile cost base, effective assets – still more to go for

• Footprint optimisation

• Better fixed cost absorption

• Machine effectiveness & scalability

249

200

125

FY13 FY15 Target

• Simplification of portfolio

• Remove SKU complexity

• Effective investment in Growth Brands

16 |

Global Procurement

• Launched 2½ years ago for ‘indirect’ spend

• Leverages economies of scale via multi-

country sourcing

• Rightsizing supplier base

• Introduced e-procurement tools

Imperial Brands Investor Day | June 2016

Lower risk, lower cost, better performance

Contract

Management

Strategic

Sourcing

Procurement

Process

Optimisation

Value

17 |

FY11 FY12 FY13 FY14 FY15 FY16

24.3%

21.6%

20.5%

Taxation

• Strong track record

• Enhances earnings

• Creates value for shareholders

Imperial Brands Investor Day | June 2016

Efficient management creates value

23.0%

21.1%

20.0%

*

* As per HY16 results guidance

Adjusted Group tax rate

18 |

What this means for

investors

Imperial brands investor day | june 2016

19 |

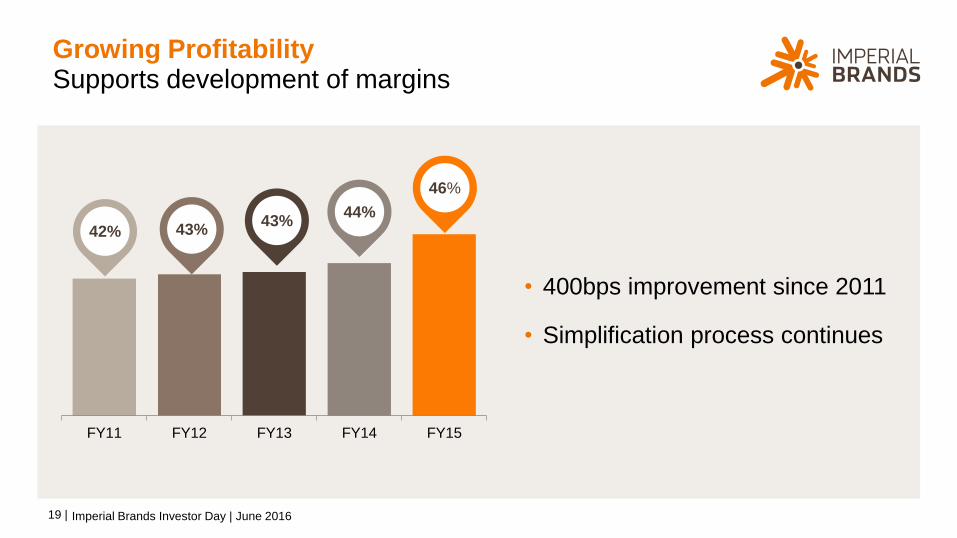

FY11 FY12 FY13 FY14 FY15

42%43%

46%

Growing Profitability

• 400bps improvement since 2011

• Simplification process continues

Imperial Brands Investor Day | June 2016

Supports development of margins

43%44%

20 |

Growing Cash Conversion

Imperial Brands Investor Day | June 2016

Strong cash performance

100% 100%97% 97%

94% 93% 92%89%

Imp

eria

l

PM

I

AB

I InB

ev

Re

ckitt

SA

B

Dia

ge

o

Un

ilever

BA

T

He

ineke

n

107%Cash conversion FY15*

* Based on FY15 disclosures for all companies. Percentage calculated on consistent basis across peers - equals net cash from operations pre tax and finance costs post capex, divided by

adjusted operating profit. Imperial percentage 107% adjusted for consistency (excludes restructuring cash costs & pension funding shortfall). FY15 disclosed cash conversion 97%

21 |

63

73

84

95

105

116

128

141

2008 2009 2010 2011 2012 2013 2014 2015

Dividend pence per share

Growing Dividend

• 8th year of >10% growth

• 12% CAGR since 2008

• £8bn in declared dividends

Consistent growth over time – up more than 120%

Imperial Brands Investor Day | June 2016

22 |

Growing DividendGrowing ahead of peers and FTSE

10%9%

8% 7% 7%

6%

5%4%

1%

4%

ImperialBrands

Diageo PMI SAB Altria RAI BAT Unilever Reckitt FTSE

Dividend growth over past 4 years

% growth is CAGR over last 4 years of dividends up to FY15. FTSE

total dividend payments 2015 £62.7bn versus £55.2bn in 2012.Imperial Brands Investor Day | June 2016

23 |

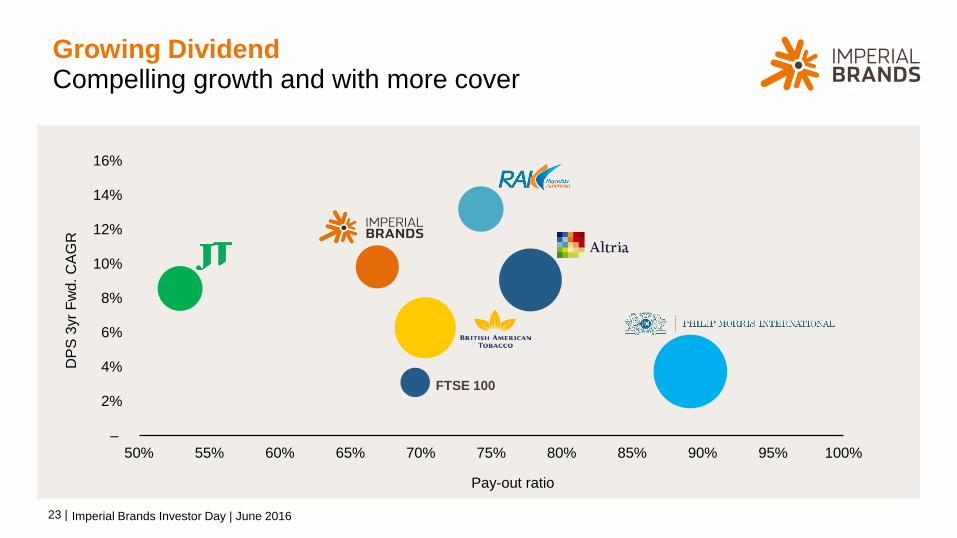

Growing DividendCompelling growth and with more cover

–

2%

4%

6%

8%

10%

12%

14%

16%

50% 55% 60% 65% 70% 75% 80% 85% 90% 95% 100%

FTSE 100

Pay-out ratio

DP

S 3

yr

Fw

d.

CA

GR

Imperial Brands Investor Day | June 2016

24 |

Our Financial ApproachQuality growth, sustainable returns

Efficiencies drive effectiveness and support

investment

Capital discipline supports consistent cash

generation

Investment improves quality of growth

Stronger balance sheet supports deleveraging

and dividend

Imperial Brands Investor Day | June 2016