ogram in Banking Finance -...

66

o gram in Banking & Financ e Option: Banking and Risk Management Topic: FOREIGN EXCHANGE EXPOSURE IN GAMBIA'S BANKING INDUSTRY- GUARANTY TRUST BANK (G) LTD AS A CASESTUDY Paper Submitted in Partial Fulfdlment of the Requirement for tbe Degree of Masters ofBusiness Administration: Banking & Finanoe (2007-2008) · Submitted by CAMARA Lamin M0170MBF09 2 11111111111 11111 11111111111 Under the supervision of Mr. JAMMEH Bakary Principal Economist, Economie Research Department Central Bank of The Gambia (CBG)

Transcript of ogram in Banking Finance -...

~ ogram in Banking & Finance

Option: Banking and Risk Management

Topic:

FOREIGN EXCHANGE EXPOSURE IN

GAMBIA'S BANKING INDUSTRY

GUARANTY TRUST BANK (G) LTD AS A

CASESTUDY

Paper Submitted in Partial Fulfdlment of the Requirement for tbe Degree of Masters ofBusiness Administration: Banking & Finanœ (2007-2008) ·

Submitted by

CAMARA Lamin

M0170MBF09 2

11111111111 11111 11111111111

Under the supervision of

Mr. JAMMEH Bakary Principal Economist, Economie

Research Department Central Bank of The Gambia (CBG)

DEDICATION

This piece ofwork is dedicated to my beloved wife, Yama SONKO, my Dad, Mum and the rest

of the family whose morale support kept me on my toes through the rough roads of my study

and research period. lt is also dedicated to ali friends and loved ones especially the Staff of

Guaranty Trust Bank (G) Ltd (GTB) for being there for me when i most needed them.

ACKNOWLEDGEMENT

The accomplishment of this feat was not an easy task. lt is against this background that i must

acknowledge the contribution of the following people, who in one way or the other, are

paramount in the assembling of this piece of work.

1 am quite indebted to Mr. Alkali BAH, my Unit Head, who read my first Draft and gave me

valuable advice on research finding strategies, to the staff of Credit Administration unit, for

their understanding during my intermittent absence on research trips to the Central Bank of The

Gambia(CBG), to the Unit Heads of Financial Control (FIN CON), Asset Liability Management

(ALM) and TREASURY for their cooperation in the provision of data, to Olalekan SANUSI

(Managing Director) and the entire Management of Guaranty Trust Bank (G) Limited (GTB)

for their relentless support during and after the study period, to lsatou NY ASSI and Elizabeth

JATTA Customer information service (GTB) for the typing of part of the scripts.

1 will not do justice to this piece of work without acknowledging the morale contributions of

Professer Boubacarr BAIDARI (MBF Project Coordinator, CESAG), Mr. Aboudou

OUATTARA (Lecturer), Madame BALIMA (Lecturer) and Madame Chantal OUEDRAOGO

(Project Secretary). 1 must also acknowledge the support of Kainding SAMBOU Finance

Department for his valuable discussions and Yahya CHAM, Economist at the Research

Department of the Central Bank of The Gambia (CBG) for furnishing me with information on

CBG which is essential for this research paper.

Last but not the least; 1 must with ali my heart, sincerely, recognise the unt1inching support of

my superviser Mr. Bakary JAMMEH (Principal Economist, Economie Research Department,

Central Bank of The Gambia) who has, to a great extent, rekindled my love for figures and

guided me through the dynamics oftesting the hypothesis of the research paper.

11

SUMMARY

Foreign Exchange Exposure refers to the sensitivity of a firm's cash flow to changes in

exchange rates. Assessing the sensitivity of a firm's value to exchange rate changes has been

one of the most challenging issues in the international financial management over the last three

decades. Moreover, this field of studies could be regarded as Greenfield in the developing

countries especially in the Gambia where extensive research in this area is at its infant stage.

This paper developed a simple model based on Richard Levich's (2001, 2nd Edition) Regression

approach to the economie measure of exchange rate exposure. The study made an analysis of

Guaranty Trust Bank (G) Ltd and briefly looked at the Banking lndustry as a whole. The study

finds that the long-run elasticity of the Euro and the Pounds Sterling despite been positive, both

were insignificant in deterrnining changes in Profit Before Tax (PBT) of Guaranty Trust Bank

(G) Ltd. However, the coefficient of the Dollar was significant and negative, indicating long-run

liability exposure. The Banking Industry on the other hand shows asset exposure relating to

changes in both the US dollar and Euro, which has positive coefficients.

Résumé

Risque d'échange fait allusion à l'effet de la sensibilité des flux de trésorerie au changement

des taux de change. L'évaluation de la sensibilité de la valeur d'une entreprise au changement

des taux de changes a été 1 'une des questions pertinentes dans le monde de la gestion financière

depuis une trentaine d'années. De plus, ce domaine d'étude est nouveau dans les économies du

tiers monde surtout en Gambie où des recherches dans ce domaine sont peu évoluées.

Ce mémoire a développé un model simple fondé sur l'approche par la Régression, comme une

mesure de risque d'échange, de Richard Levich (2001, 2éme Edition). L'étude s'est focalisé sur

la Guaranty Trust Bank (G) Ltd et a jeté un clin d'œil Sur l'industrie Bancaire en Gambie. La

recherche montre que l'élasticité du long terme d'Euro et La Livre Sterling ont des chiffres

positifs, mais ses chiffres ne sont pas significatifs pour déterminer le changement du profit

sans taxe de Guaranty Trust Bank (G) Ltd. A l'opposé, le coefficient du Dollar est significatifs

et négatif, Preuve que le passive de la banque supporte un risque de change. L'industrie

bancaire, pour sa part, supporte un risque de taux de change au niveau de son actif: lié au Dollar

américain (USD) et l'Euro qui ont des coefficients positifs.

iii

TABLE OF ABBREVIATIONS

ADF: The Augmented Dickey- Fuller Test ALM: Asset and Liability Management CBA: Central Bank Act CBG: Central Bank of The Gambia CESAG: Centre Africaine D'Etude Supérieure en Gestion EUR (€): Euro FCY: Foreign Currency FDI: Foreign Direct Investment FI: Financial Institutions FIA: Financial Institutions Act GBP (f): Great British Pounds GCCI: Gambia Chamber of Commerce and Industry GDP: Gross Domestic Product GMD: Gambia Dalasi (The name given to the Gambian Currency) GTB: Guaranty Trust Bank (Gambia) Limited GTBANK: Guaranty Trust Bank (Gambia) Limited IMF: International Monetary Fund LCY: Local Currency LIBOR: London Interbank Operating Rate LIFFE: London International financial futures and options Exchange MPC: Monetary Policy Committee OMEs: Owner Managed Enterprises PBT: Profit Before Tax PRGF: Poverty Reduction and Growth Facility program SAP: Structural Adjustment Program SMEs: Small Medium Scale Enterprises T-BILLS: Treasury Bills US: United States of America USD ($): United States Dollar V AR: Vector Autoregressive

lV

LIST OF TABLES AND CHARTS

Tables

Table 1: Banks' Sources Of Incarne 3rd Quarter 2007 & 2008 in Millions ..................... 13 Table 2: Results of Augmented Dickey- Fuller Test.. ......................................................... 2 Table 3 : Unrestricted Co-integration Rank Test (Trace) ..................................................... 3 Table 4 : Long-run model .......................................................................................................... 4 Table 5 : Results of Long- Run Regression ......................................................................... 0 Table 6: Results of Breusch-Godfrey Seriai Correlation LM Test ..................................... 2 Table 7: Heteroskedasticity Test: ARCH TEST ................................................................... 3 Table 8 : Result of Short- Run Dynamic Model ................................................................... 5 Table 9: Result of Breusch-Godfrey Seriai Correlation LM Test.. ..................................... 8 Table 1 0 : Heteroskedasticity Test: Breusch-Pagan-Godfrey ............................................. 8

Ch arts

Chart 1 : Histogram of the Jacque-Sera Test ....................................................................... l Ch art 2 : Result of the CUMSUM's test ................................................................................. .4 Chart 3: Result of the CUMSUM's test ................................................................................. .4 Ch art 4 : Jacque-Be ra Test (Banking lndustry) ..................................................................... 7 Ch art 5 : Exchange Rates Movement from 2004 .................................................................. 0 Chart 6: Exchange Rates Movement from 2005 .................................................................. 0 Chart 7 : Exchange Rates Movement from 2006 .................................................................. 1 Chart 8 : Exchange Rates Movement from 2007 .................................................................. ! Ch art 9 : Exchange Rates Movement from 2008 .................................................................. 2

Figures

Figure 1 : GTB Exchange Earning 2007 .................................................................................. 0 Figure 2 : GBT PBT analysis 2007 ........................................................................................... 0 Figure 3 : GTB SPOT POSITION 2007 ................................................................................... 1 Figure 4: GTB MID RATES 2007 ............................................................................................. 1 Figure 5 : GTB Total LCY & FCY Deposits 2007 ................................................................... 2 Figure 6 : PBT- Banking lndustry vs GTBANK ...................................................................... l Figure 7 : Exchange Earning (000) 2008 ............................................................................... 3 Figure 8 : GTB SPOT POSISTION 2008 ............................................................................... 3

v

O. INTRODUCTION

The Gambia, a small open economy with a population of 1.4 million (2003 census), has enjoyed

rdative macroeconomie stability during the early years after independence in 1965. Annual

inflation rate plurnmeted to -2.0 percent while the economy grew by 6.2 percent (World Bank

1970).

Prior to the liberalisation in 1986, The Gambia has a fixed exchange rate regime with a priee

control system. There was credit rationing, mainly, to the agricultural sector and government

interventions in the form of subsidies to boost production in the sector. However, the country

experienced severe macroeconomie instability in early 1980s, fuelled by overvalued exchange

rate, large budget deficits financed mainly by domestic borrowing, huge external debt and

unfavourable terms of trade for agricultural products. Consequently, inflation rate rose from

10.6 percent in 1983 to 22.1 percent in 1984 and 56 percent in 1986, while GDP growth

declined from 3.5 percent to -0.8 percent. This was coupled with severe lost of reserves (about

less than a month's import cover for the Country).

This prompted the authorities to embark on a Structural Adjustment Programme (SAP) aimed at

streamlining domestic credit through the liberalisation of the financial system, maintenance of

low inflation and stable exchange rate while at the same time, attaining a certain desired level of

growth.

A floating exchange rate regime was introduced in 1986. The liberalisation of the financial

system brought in sorne benefits. Inflation rate plummeted to 9.6 percent from 56.6 percent in

1986. Underpinned by sound economie management, the country was able to maintain single

digit inflation with a stable exchange rate for nearly a decade.

Consequently, economie growth remained vibrant in late 1990s through 2000 with real GDP

growth averaging 3 percent per annum. However, a large fiscal and monetary expansion in 2001

led to the destabilization of the Gambian economy.

To reverse this economie trend, the country embarked on structural reforms, implementation of

prudent macroeconomie policies and these coupled with a good harvest in 2003/2004 helped to

stabilize the Dalasi and reined inflationary pressures in the fourth quarter of2003.

Overall budget deficit as a percentage ofGDP was 4.5 percent in 2004 compared to 4.7 percent

in 2003. Annual (end period) inflation feil sharply to 8 percent in December 2004 from 18

percent a year earlier, leading to a substantial fall in interest rates. Economie growth reached 7.7

percent at the end of2006.

To consolidate these economie gains and broadcn povcrty reduction through high and non

volatile economie growth, the Government of The Gambia entercd into agreement with the

International Monetary Fund (IMF) in January 2007 culminating into the Poverty Reduction and

Growth Facility (PRGF) program.

In 2008, GDP growth decline to 6.1 percent from 6.3 percent in 2007, due largely to contraction

in the service sector which reflects the unsettled conditions in the global financial markets

resulting in tighter credit conditions, exacerbated by high fuel and food priees. These

unfavourable global developments led to reduced exports, tourism receipts, remittances and

foreign direct investment (FDI) flows ali of which restrain growth over the near future.

Consequently, Real GDP in 2009 is forecast to slowdown further to 3.9 percent.

The Gambia, as noted earlier, is small open economy in which monetary and Exchange rate

policies cannot be easily separated. The Central Bank ofthe Gambia (CBG) adopted an indirect

monetary po licy framework in the context of the economie and financial reforms undertaken in

1986. A treasury bills market (moncy market) was introduced in 1987 to facilitate migration to

indirect instruments in the conduct of monetary policy from the use of direct instruments i.e.

selective credit contrais. Currently, the CBG uses weekly auctioning of treasury and Central

Bank bills through primary dealers to meet public sector financing and control of moncy supply.

CBG uses a monetary targeting framework to pursue its priee stability objective, and uses its

rediscounts rates to signal changes in its po licy stance. The commercial banks choose the ir own

deposit and lending rates without strings attached. CBG sets an intermediate target for growth in

broad moncy (the nominal anchor of the system) and uses reserve moncy as its operational 2

target. The Monetary Policy Committee (MPC) set up in 2004, oversees monetary policy

implementation and ensures that priee stability objectives are given prominence in monetary

and exchange rate management of the Bank.

It is worth noting that the MPC, since its establishment, though stiJl defining its priee objective

in terms of headline inflation, has been reporting on core inflation as weil as other indicators as

barometers of underlining priee developments. The main instrument used by CBG to influence

the path of reserve moncy is the issuance of T-bills. A 7-day deposit instrument was recently

introduced for the purpose of a better separation between Fiscal operations and monetary po licy

operations. The independence ofthe Bank in the conduct ofmonetary po licy has been enhanced

under the revised Statute of the Central Bank Act (2005), which also stipulates priee stability as

the overrid ing mandate of the Bank as weil as the creation of a sound financial system for

sustained economie growth and poverty reduction.

0.1. PROBLEM STATEMENT

The move by the CBG to operate an inter-bank floating exchange regime to provide a more

efficient, non-interventionist mechanism for determining the official rate resulted in the dalasi's

movement being dependent on the market forces of supply and demand in the Foreign exchange

market. Data from CBG, since 1997, showed graduai appreciation of the foreign major

currencies (i.e. Dollar & Pounds sterling) against the Dalasi. When the Euro was introduced in

January 2002, it followed the same trend as the dollar & Pounds Sterling. However, in 2005, the

dalasi showed marked appreciation against the currencies under discussion only to stabilize in

2006. (See Appendix-III Chart 5-9 for graphical analysis ofthe Exchange rate movement)

Drama unfolded in 2007, when the dalasi recorded an unprecedented gain against ali the three

currencies (i.e. Pound Sterling, Dollar & Euro). On October, 301h, 2007, the Dalasi appreciated

to a four-year record high against the Dollar, the Pound Sterling, and the Euro by "30.6%,

23.0% and 22.9% respectively"-(Budget Speech 2008 p321 ).This drastic appreciation of the

Dalasi raised a lot of eyebrows both within the public and private scctor domains-thus the nced

to investigate this phenomenal Exchange rate movement and its impact on Guaranty Trust Bank

(G) Limited and the Banking Industry in general.

3

In probing briefly into the volatility ofthe Dalasi and policy, this study seeks to find out the

Exchange Rate Exposure on Guaranty Trust Bank (G) Limited and the Banking lndustry.

Commercial banks in the Gambia deal in foreign Currency. They have Nostro (foreign

accounts) accounts in foreign currency, avait foreign currency loans, do foreign transfers on

behalf of customers; carry out cash shipment to fund their accounts abroad, settle Letter of

Credits (LCs) on behalf of customers and above ali, do foreign exchange trading. This paper

seeks to find out:

./ The Foreign Exchange Exposure of Guaranty Trust Bank (G) Ltd and the Gambia's

Banking Industry

./ The impact of Exchange Rate changes on Profit Before Tax

./ Hedging Proposais if any to mitigate the foreign exchange exposure

0.2 Intcrcst of the Subjcct

This piece of work will enable me understand to a great extent changes in the exchange rates,

their impact on the Banking Industry at large and most specifically their impact on Bank

Performance-Guaranty Trust Bank (G) Ltd.

ForCESAG

This study will increase its opportunity to increase its documentation in various topics of

interest which wou Id be at the disposai of research students to serve as a source of

supplementary information in foreign exchange rate changes most specifically its impact on a

commercial bank's performance.

For Profession al Rcsearchers

The study should rather be a window of opportunity to investigate the dynamics of foreign

currency exposure in developing countries- Africa, especially the Gambia were techniques such

as currency forward contracts, currency futures, currency options, currency swaps, etc. Used as

tools to hedge against foreign exchange risk is in its infant stage. 4

0.3 HYPOTHESES

Hypotheses are expected to guide any study and provide a framework for organising the

resulting conclusions. lt is a way ofpredicting the possible outcomes of an investigation. Trying

to work out the impact of foreign exchange exposure in Guaranty Trust Bank (G) Ltd and

Banking Industry in The Gambia can lead to two sets of conclusions. As a consequence, the

hypothesis associated with this objective is as follows:

lh o (Nul/ hypothesis): "Guaranty Trust Bank (G) Ltd and the Gambia 's ban king industry are

exposed to fluctuations in the Exchange rates"

H1, A (Alternative hypothesis): "Guaranty Trust Bank (G) Ltd and the Gambia 's banking

industry are not exposed to fluctuations in the Exchange rates"

ln our methodology, we would elaborate on the above objectives and methods adopted to test

this hypothesis

0.4. Organization of Study

The dissertation is divided into Two Parts. The first part includes theoretical issues, literature

review and methodology. Part two deals with the empirical analysis, research findings and

hedging proposais against exchange rate exposure.

5

PART l(ONE): Exchange Rate Policy, Movement, Financial System, the

Banking lndustry, Guaranty Trust Bank & Theoretical Issues

SECTION 1: Exchange Rate policy, Movement, Financial System & the Ban king lndustry

1. Dcvclopment of Exchangc Rate Policy Regimes in the Gambia

The floating Exchange rate regime was introduced in the Gambia in 1986 as part of the

Economie Recovery Package. It abolished the fixed parity between the Dalasi and the Pound

Sterling and left the Exchange rate to be determined by the free interaction of the market forces

of demand and supply in the context of the inter-bank market.

With the introduction of the exchange rate regime, ali restrictions on current and capital

transactions were lifted.

At the outset, the inter-bank market consisted of commercial banks, which were the only ones

with the authority to deal in foreign currency on daily basis at market-determined rates of

exchange. At the end of every week, representatives from the commercial bank would meet at

the Central bank for their fixing sessions. During these sessions, they review development in the

currency market (both domestic and international) and the Central Bank announces the

Exchange rate for custom evaluation purposes for the following week. The rate is based purely

on the outcome of the buying and selling activities of the participants in the inter-bank market

reported to the bank on daily basis. For each currency, a mid rate is determined based to the

weighted average buying and selling rates during the week. Consistent with the trade

liberalisation policy, the commercial bank are not required, under the floating exchange rate

regime, to obtain approval from the Central Bank to sell foreign exchange to their customers for

ali current transactions.

ln bid to increase competition in foreign exchange and to improve the allocation efficiency, the

Central Bank allowed the licensing of foreign exchange Bureaux in 1990 that also participated

in the inter-bank market.

The floating exchange rate regime has the following objectives:

./ Ta promote voluntary surrender of foreign exchange ta the banking system by

eliminating the financial disincentive ta do sa and by providing greater liberalised access

ta foreign exchange;

./ Ta promote a better balance between the demand for the supply of foreign exchange by

way of an orderly and non-discriminatory allocation system;

./ Ta smoothen the seasonal fluctuation in the country's foreign exchange earnings; and

./ Ta provide a clean measure of the priee scarcity value of foreign exchange ta the

economy sa as ta guide economie agents in their pricing and investment decisions.

The exchange rate regime was not implemented in isolation. In arder to achieve their objective,

other support ive liberal measures were adopted either prior ta the floating or after it.

Prior to the floatation, such measures included the adoption of a liberalised trade po licy and

restrictive tiscal and monetary policies. Liquidity and reserve requirement as weil as credit

ceilings were imposed on commercial banks. (Credit ceilings were however, abolished in

1991 as the central bank switched ta indirect monetary contrais).

Measures were also taken ta streamline revenue collection and keep a lid over expenditure

wh ile the Central Bank adopted a system of foreign exchange budgeting to predetermine limits

on the govcrnment's foreign exchange requirement whilst consolidating its reserve

accumulation. The governmcnt also removed ali restrictions on trade.

Following the floating, supportive policies included the adoption of prudent external debt

management po licy and a flexible interest rate policy. These were complemented by an array of

structural rcforms and sectoral strategies.

The most visible impact of the floatation has been on the foreign exchange market. The inter

bank market has been functioning smoothly since its inception there has been a steady reduction

of the margins between the inter-bank markets and the parallel market rates of foreign

7

exchange. In sorne instances, the two rates were almost completely harmonised. The parallel

market has been virtually absorbed into the formai banking system.

The floatation has also helped in the rechanneling into the official market a substantial portion

ofthe foreign exchange which is used to be supplied to the parallel market and therefore went

unrecorded.

Another positive effect of the floating exchange rate regime has been the consolidation of

reserve accumulation reflecting robust improvement in the overall balance ofpayment position.

In terms of output, the realignment of the exchange rates has boosted the competitive edge of

the Gambia.

The succcss achieve in the exchange rate front culminated in the Gambia's acceptance of the

conditions under Article 8 ofiMF's Articles of Agreement in 1993. This made the Gambia one

of the very few low-income countries to guarantee the international convertibility of their

currencies.

Jt could be concluded that the floating exchange rate regime has achieved most of its stated

objectives. It has provided the Gambia with a market-based system whieh is flexible enough to

adjust to changing economie situations and that affect the equilibrium exchange rate for the

Dalasi.

2. Exchange Rates Movcmcnts

The Gambian economy, underpinned by solid macroeconomie policies and complete liberalized

capital account has experienced a massive inflow of foreign capital in recent years. Since 1986,

The Gambia maintained a proven record of protracted capital and financial account

liberalization, which has been fully adhered to even in times of economie crisis and exchange

rate volatility. It should be noted that free movement of capital actually enhances more inflows.

The main sources of foreign exchange inflows are tourism, re-exports, foreign direct investment

(FDI), privatization receipts and private remittances. The latter alone is estimated at D 1.8 billion

in 2006 compared to 01.5 billion in 2003 and this was sustained in 2007. It is generally 8

assumed that the officially documented private remittances are usually a fraction of total

inflows. Tourism receipt is estimated at 01.8 billion in 2006 compared to 01.3 billion, 00.7

billion and 00.9 billion in 2003, 2002, and 200 l respectively. It was within the thresholds of

02.3 billion in 2007. For its part, FOI rose from 00.5 billion in 2003 to 02.3 billion in 2006

and was generally maintained at this leve) in 2007. FOI was estimated at 00.2 billion for both

2001 and 2002.

Transaction volumes in the inter-bank market for foreign exchange grcw by 180.8 per cent to

034.07 billion in 2006 from 012.13 billion in 2003. Transactions volumes stood at 011.30

billion in 2002. In the nine months to end-September 2007 transaction volumes grew by 28.5

per cent to 030.71 billion compared to 023.90 billion in the corresponding period of the

preceding year. rn US dollar terms, transactions volumes increased to US2.1 billion or 394.4 per

cent from 2003. Between January and September 2007, transaction volumes amounted to

US$1.2 billion compared to US$0.8 billion in the same period in 2006 (MPC press release

December 2007).

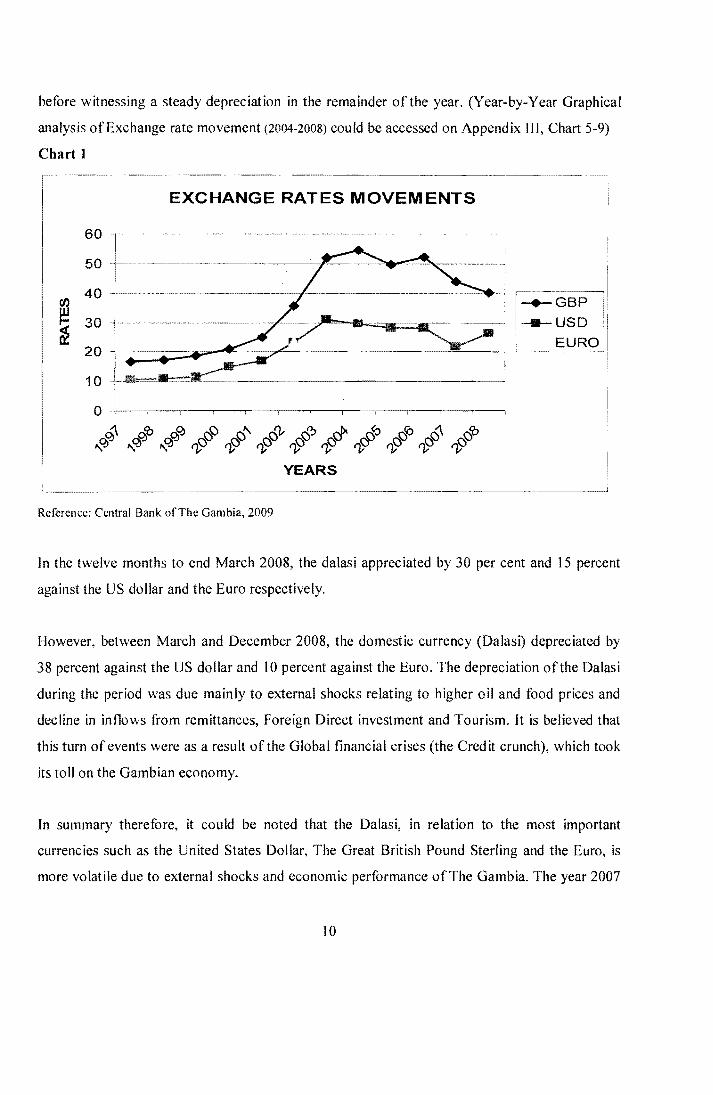

As could be seen on Chart 1 below, the Dalasi gradually lost strength against the Pound and the

Dollar from 1997 to 2002. However, it could be noted that a steep depreciation of the Dalasi

was experienced between 2002 and 2003 against ali major currencies (i.e. Pounds Sterling,

Dollar & Euro). This period was marred with economie difficulties due to low productivity and

increase in imports. This resulted in heavy demand on foreign exchange and consequently the

steep depreciation ofthe Dalasi.

The dalasi remained relatively stable in 2004. It should be noted that the strengthening of the

Dalasi Vis-à-vis major currencies started in 2005, following the implementation ofthe prudent

monetary and fiscal policies, coupled with increase foreign inflows and rebounding economie

growth. During 2006, the Dalais !ost ground against ali currencies, except the US dollar, which

was weakening against most international currencies.

Fluctuation in the value of the dalasi became more pronounced a fier the sharp appreciation of

the currency in the third quarter of 2007. A partial reversai occurred in the fourth quarter of

2007, representing market correction. Responding to supply and demand conditions in the inter

bank market for foreign exchange, the dalasi strengthened once again in the first quarter of2008 9

be fore witnessing a steady depreciation in the remainder of the year. (Year-by-Year Graphical

analysis ofExchange rate movement (2004-2008) cou Id be accessed on Appendix III, Chart 5-9)

Chart 1

EXCHANGE RATES MOVEMENTS

0

~ PJ'O PJC!> !:)() d' !:)']., !:)~ d" _C'\~ ~ ~ !:)'0 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~~ ~

YEARS

Reference: Central Bank of The Gambia, 2009

In the twelve months to end March 2008, the dalasi appreciated by 30 per cent and 15 percent

against the US dollar and the Euro respectively.

However, between March and Decembcr 2008, the domestic currency (Dalasi) depreciated by

38 percent against the US dollar and 10 percent against the Euro. The depreciation ofthe Dalasi

during the period was due mainly to externat shocks relating to higher oil and food priees and

decline in inflows from remittances, Foreign Direct investment and Tourism. It is believed that

this turn of events were as a result ofthe Global financial crises (the Credit crunch), which took

its toll on the Gambian economy.

In summary therefore, it could be noted that the Dalasi, in relation to the most important

currencies such as the United States Dollar, The Great British Pound Sterling and the Euro, is

more volatile due to external shocks and economie performance of The Gambia. The year 2007

10

is characterised by an appreciation ofthe Oalasi, which unfortunately has been checked by oil

shocks and international financial crises.

3. The Gambia Financial System

The Gambia Financial System has evolved rapidly over the last severa! years, and is markedly

liberalised now. Most interest rates are freely determined, direct contrais have been eliminated,

exchange contrais abolished and the country has moved to indirect system ofmonetary contrais

using open market operations. These measures increased competition in the domestic financial

system.

As a result of developments and policy practices changes in the legislation have also taken

place. The Financial Institutions Act (FIA), Central Bank Act (CBG Act) has been revised. The

FIA Act 2003 has been enacted while the CBG Act 1992 is almost in its final stage of revision.

The Insurance Act 2003 and the Money Laundering Act 2003 have also been enacted.

The Central Bank ofThe Gambia is mandated under the provisions of the Financial Institutions

Act (FIA) 2003 and the Central Bank Act (CBA) 2006 to license and regulate ali financial

institutions in The Gambia. The Bank has an open policy towards Greenfield investment in the

financial sector that would promote and enhance the country's sound financial system.

Against this background, developments in the financial sector continued to be vibrant and

deepen as new banks and foreign exchange bureau were licensed to operate. The net foreign

assets of deposit money banks, which stood at negative 047.8 million (net liability) in 2001,

increased from 01.01 billion at end-Oecember 2003 to 01.46 billion at end-Oecember 2006 or

by 44.5 per cent. Between Oecember 2006 and July 2007, the Net Foreign Assets of

Commercial Banks grew by 39.0 percent to 02.03 billion. Similarly the net foreign assets of

the Central Bank at 01.2 billion in 2001 rose to 04.3 billion in 2006. The net externat position

ofthe Bank increased to 04.6 billion or 5.3 percent from the beginning of the year. (MPC Press

Release Oecember, 2007)

The Gambia's financial sector has been growing in numbers. It consists of commercial banks,

insurance companies, foreign exchange bureaus, microfinance institutions and other non-bank

finance companies. However, commercial banks dominate this industry controlling over 90%.

Il

Currcntly, thcrc arc at !east twelve banks with an average foreign cquity of ovcr 60%. Elevcn of

the banks arc involved in convcntional banking and one in Islamic banking. In terms ofscope of

activitics the banks opcrate mainly within the Greatcr Banjul area with sorne branches and

agcncies located in other parts of the country. The micro-finance institutions mainly cater for

the remaining parts of the country.

To concludc therefore, it should be noted thcre is marked improvcmcnt in the Gambia's

financial system, evidcnced in the growth of the net foreign assets (39%) from 2006. This

financial analysts be lieve, is as resu lt of an influx of Nigerian Owned banks, now numbcring

eight (8). This new devclopment will surely strain the Central of Bank's Supervisory

Dcpartment's human resources capacity in terms of effective supervision. It is high time that a

mechanism is put in place to arrest the situation.

4. The Banking lndustry

The banking industry remains sound. Total industry assets rose by 19.5 percent to 012.5 billion

year-on-years as at cnd-December 2008. The risk-weighted capital adequacy ratio stood at 35.9

percent in Deccmber 2008, weil above the statutory requircment of 8 percent. Non-performing

loans rose from 7.3 percent in Septembcr 2008 to 9.5 percent in Dccember 2008(CBG Bank

Supervisory Department). However, nonperforming loans werc adequately provisioned in

compliance with the statutory requirement.

It should also be noted that the Open Policy towards Greenfield Investment in the financial

sector by the Central Bank of the Gambia led to an intlux of Nigerian owned Banks into the

country. This, to sorne extent, had an impact in the banking industry. One major effect is the

reduction in Interest Margin and consequently, the interest income of the Industry. From the

table on the next page, it could be deduced that the interest income on Loans to Private Sector

declined from D55Million (Fifty -Five Million Dalasi), in the third quarter of2007, compared

to D52Million (Fifty-Two Million Dalasi) in the third quarter of 2008. It is interesting to also

note that Total Interest Income has plummeted to 37% oflndustry's Turnover compared to 60%

oflndustry's Turnover in the previous year.

12

Table 1: Banks' Sources Oflncome 3rd Quarter 2007 & 2008 in Millions

Q3. 07 Q3. 08 Growth 1

Banking Industry Value Percent Value Percent Percent

Treasury Bills 73 33% 78 21% 7% i

Other Government Securities - - - - - i

Intcrcst Income From Securitics 73 33% 78 21% 7%

Loans to Private Sector 55 25% 52 14% -5%!

Overdrafts to Private Sector 46 21% 60 16% 30%

Other Loans/ Overdrafts 2 1% 3 1% 50%

Intercst on Loans & Advanccs 103 47% 115 31% 12%

lnterest From Deposits With Banks 30 14% 24 6% -20%

Interest from Bills Purch. & Dise. 0.3 0% 1 0% 233%

Total Intcrcst Incomc 133.3 60% 140 37% 5%

Services Charged on Deposits 16 7% 16 4% 0%

Acceptance, Guarantees & LC Fees 7 3% 7 2% 0%

Fees/Other Charges On FX Transa. 66 30% 69 18% 5%

Unrealized FX Transactions -134 1

-61% 10 3% 107%

Other Non-Interest Income 60 27% 56 15% -7%

Total Non-Intcrcst Incomc 15 7% 158 42% 953%

TURNOVER 221 100% 376 100% ! 70%

Source: Banking Supervision Department, Central Bank ofThe Gambia

This triggered a shift by commercial banks to non-interest income ventures such as services,

charges on deposits, Bankers Acceptances, Guarantees, Fees on Letters of Credit (LCs) and

Foreign Exchange transactions. As such, it accounted for 42% of Jndustry's Turnover in the

third quarter of 2008, compared to meagre 7% in the corresponding period of 2007.

Nonctheless, there is marked improvement in the industry's Turnover of about 70% growth

from the corresponding year (i.e. Q3. 2007)

In conclusion, the Banking Industry remains profitable despite the influx of new banks. It

should also be noted that competition has impacted on the interest income as evident in a

meagre growth of 5% in 2008 and constituting 37% of the total turnover in 2008 compared to

60% of total turnover in 2007. As the interest margin continues to thin down, Commercial

banks arc likely to be forccd to improve on their services to ensure growth in turnover.

13

5 Guaranty Trust Bank (G) LTD- Overview

Guaranty Trust Bank (G) Limitcd emerged as a force to be reckoned in the Gambia's Banking

Industry after just seven years in existence. A subsidiary of Guaranty Trust Bank (PLC),

Guaranty Trust Bank (Gambia) Ltd obtained banking license to commence full commercial

banking business in The Gambia on 51h March 2002. Guided by its strategy ofproviding quality

service to ali its customers everywhere in the country, it embarked on branch expansion, which

increased its branch network to eight. lt is hoped that by the end of2009, GTB will be boasting

of 12 branches (2 new branches within the Greater Banjul area & 2 in the provincial towns of

Farafenni and Basse).

Apart from being a commercial bank with first class products and services, the bank is driven

by its strong culture of ethics, integrity and high sense of corporate Culture. Presently, Guaranty

Trust bank (Gambia) is the fastest growing bank in The Gambia as shown by the Databank

securities Gambia Ltd report on the Gambian banking industry 2005. To cap it ali, Guaranty

Trust bank (Gambia) L TD has been crowned as the "Bank of the Year 2008" by the Gambia

Chamber of Commerce and Industry (GCCI).

a) Market segmentation

Over the years, GTB has remained committed to providing professional banking services for

various facets of The Gambian eco no my. Its Corporate Bank Group, Commercial Bank Group,

Public Sector Group, Retail Bank Group and Treasury ali offer personalized services to meet its

customer's every need.

i) Corporate Bank Group

This group serves Multi-nationals and large corporate organizations in Manufacturing, Energy,

Aviation, Telecommunications, Import and Export sectors among others. To effectively and

efficiently market these corporate bodies, the group is supervised by a Group Head, three

Relationship Managers and Account Officers to man the following sub-segments:

a) Manufacturing and Trading

b) Energy and Telecommunications

c) Hospitality

14

ii) Commercial Bank Group

The commercial Bank Group is structured ta suit the banking needs of the middle market

players such as Government contractors, traders and medium scale corporate organizations.

Recently, FI (Financial Institutions) have been moved from Corporate ta Commercial. This

includes, Banks, Foreign exchange Bureaus and Micro- finance Institutions. A Group Head also

heads this unit and three Relationship Managers coupled with account officers as backups.

iii) Public Sector Group

The Public sector Group deals directly with Government Institutions at the national and local

levels, Non-governmental organizations and Embassies, providing financial advisory services

and other tailor made products and services.

iv) Retail Bank Group

This segment is structured to develop and serve individuals and owner managed enterprises

/Small & medium scale enterprises (OMEs/SMEs) account holders, as weil as respond ta the

personal needs ofthe Bank's most valued Customers.

ln addition, a parti cu lar unit was carved ta specifically hand le the needs of H igh Net worth

individuals (Senior Banking Officers, Managing Directors of Companies, Senior Government

Officiais, Lawyers and other highly placed people within the society).This enabled account

officers ta map out specialized products and services befitting such a cohort of people in the

community.

v) Treasury Unit

This unit operates as a profit center, divided into four main desks, namely:

a) Local Currency Trading

b) Foreign Currency Trading

c) Assets and Liability Management (ALM)

d) Administrative management

With each ofthese groups, the bank operates on a participatory and professional front. On one

hand, it strives ta actively acquire the knowledge needed to service its customers and on the

15

other hand it imparts informed knowledge on how the customers can improve their businesses.

This way, the bank provides total solutions that meet every customer's needs.

5.1 FOREIGN EXCHANGE EXPOSURE (RISK) AT GUARANTY TRUST BANK

Guaranty Trust Bank Gambia deals in different foreign currencies. The exchange rates ofthese

currencies do fluctuate from time ta time against the Dalasi (the local currency). Theses

exchange rate volatilities do have an impact, either positively or negatively on the profitability

ofthe Bank.

5.2 DEFINITIONS OF RISKS

Risk is the variability of actual returns from expected returns. Risk is uncertainty that has an

impact on the health of the Bank or institution, Guaranty Trust Bank (G) not an exception.

5.3 TYPES OF RISKS THAT GURANTY TRUST BANK (G) LTD FACES

Guaranty Trust Bank (G) Ltd like any other financial institutions faces different types ofrisks in

the cause of its operations.

Risk can be grouped into two headings- Business risk and financial risk

Business-Risk: - This covers those risks arising rrom manufacturing and marketing products

and services.

Financial Risks: - Those risks arising rrom unexpected movements in currencies, interest rates,

commodities, and equities. Financial risk can be subdivided into:

a) Market Risk - Uncertainty related to changes in value or liquidity of financial

instruments.

b) Credit Risk- The risk that a borrower might default on a promised payment.

c) Operational Risk - Uncertainty regarding the possibilities that a contract cannat be

enforced.

d) Exchanged Rate Risk - This is the uncertainty created in expected cash flows in

domestic currency, as a result ofunanticipated changes in currency rates.

Our concern in this subsection, howcver, will be based on exchange rate risk 16

5.3 EXCHANGE RATE EXPOSURE/RISK IN GUARANTY TRUST BANK

Guaranty Trust Bank deals in different foreign currencies. These are the US dollar (USD),

pound sterling (GBP), Euro (EUR), FCF A & Swiss Franc (CHF)

The main transactions that GTB effects which involve foreign exchange are trade finance,

foreign transfers and foreign exchange trading. The principal departments which initiate the

above mentioned transactions are:

(i) Corporate Banking Department

This department ho ids the accounts of large Institutional clients, sorne of which do have

forex and foreign exchange accounts. These clients do instruct the bank to effect transfers on

their behalf, sell foreign currencies to or buy foreign currencies from the Bank.

(ii) Commercial Banking

ft handles the accounts of small and medium scale enterprises involved in manufacturing,

trading etc. These customers sometimes import and also export their products. In their

dealings with the bank, these clients do cali on the bank to buy or sell foreign currencies and

effect foreign transfers on their behalf.

(iii) Retail Banking Department

1t holds accounts for individual clients, alternatively called persona! account holders. Sorne

of these individuals have foreign accounts through which they effect different transactions.

Others also authorize the Bank to debit their Dalasi current account to buy foreign

currencies to pay for their bills (e.g wards school fees, medical and other travel expenses

among others).

(iv) Trade Support Dcpartment

lt is one of the most important departments whose activities have a tremendous impact on

the foreign exchange transactions of the bank. It establishes Letters of Credit for customers

makes and receives foreign exchange payments on behalf of its clients in respect of import

and exports. It also effects different types of foreign exchange transfers on behalf of its

customers. 17

(v) Branches

Ali the eight (8) branches of the bank do hold foreign exchange accounts for their clients

through which they receive and make payments in foreign exchange payments. They also

sell or buy foreign currencies from the public. These transactions impact significantly on the

Bank's foreign exchange position.

(vi) Trcasury Dcpartment

This is the hub of the foreign exchange operations. It is the department that manages the

Bank's foreign exchange position.

Any department that initiates a transaction, which involves the payment of foreign currency,

first contacts the treasury department for approval. This is so because it is the Treasury

Department that keeps and manages the foreign currency reserves of the Bank. The

Departmcnt on its own also trades on the foreign exchange market. It also maves funds from

one foreign account to another as part of its foreign exchange risk management functions.

To conclude therefore, it would be noted that Guaranty Trust Bank (G) Ltd like ali other

commercial banks that deal with foreign currency, especially in floating exchange rate

system, is at the mercy of foreign exchange exposure(risk). As such, it is pertinent therefore,

to know the bank's sensitivity to foreign exchange volatility.

18

SECTION 2 {TWO): literature Review and Research Methodology

2.1 Theoretical issues and Literature Review

a) The Currency Risk Concept

The current system of floating exchange rates that replaced the Brettons Woods fixed rate

system has made the currency risk an important business risk. No wonder the business world

has little doubt about the existence of it. Alfred KENYON (1981) has given an illustration of

this common awareness about currency risks in international business, as follows:

"lt is widely known that J. LYONS ofteashop firm had to sell their teashops and lost

their independence because they borrowed non-sterling currencies to finance assets in the

United Kingdom, and that Royce recorded a very large Joss in 1979 because they had taken

major contracts in US dollars"

Y et, to the question "What is currency risk?" there is no template-like answer. There seems to

be rather less agreement on just what is currency risk. Books on the topics use a number of

expressions like economie, transaction, accounting, translation, and balance sheet exposures,

but they do not ali define them in the same way. Very few authors have tried to set out rigorous

or formai definitions.

One author who does define exposures formally is David P. WALKER (1978). According to

him, "an asset, liability or income-stream is exposed to exchange rate risk when a currency

movement will change, for better or worse, its parent currency value".

E. CLARK and B. MAROIS (1996), defined currency risk as "volatility of the exchange rate",

whereas Professor S. ROSS (1998) of Yale University fou nd in this ki nd of risk, "the natural

consequence of international operations in a world where relative currcncy values move up and

down".

According to these authors, currency exposure is intimately linked with the fluctuating nature of

exchange rates in international financial markets. Despite their relevancy, sorne caution is in

19

arder usmg them, because they don't wholly capture the issue of currency exposure to

international firms with sales and production operations in foreign currencies.

To provide a more accurate definition, Richard LEVI CH (1998) laid on the concept of currency

risk (exposure) a purely mathematical sight. Currency exposure, he explained, is "the sensitivity

of the market value of the firm to a change in the (local to foreign currency) exchange rate "This

definition has the advantage of extending exchange rate exposure to a wide range of firms,

including those with domestic operations and with assets and liabilities denominated in

domestic currency only.

Throughout our study, currency exposure, which could be as a result of either an appreciation or

depreciation, will be used in either of the previous meanings, depending on the focus. However,

it is important to recall that in finance, we can distinguish many types of currency exposure:

accounting currency exposure, economie exposure, balance sheet or translation exposures, etc.

Let's have a look at the ir individual meanings.

i) Accounting versus Economie Currency Exposures

David P. WALKER defines an accounting exposure as the "possibility that those foreign

denominated items which are consolidated into a company's published financial statements will

show a translation Joss (or gain) as a result of currency movements since the previous balance

sheet date." In economie exposure, he sees "the possibility that the parent currency-dominated

net present value ofthe foreign subsidiary's cash-flows will be adversely affected by exchange

rate movements".

On the same wavelength with WALKER is Andreas PRINDL (1976) who sees in accounting

risk, the possibility" that the publicly stated value ofthe company's assets, equity and incarne

may be adversely affected by the movement of currencies in which it has dealings".

Unlikely, his view of economie exposure takes in "the whole range of the future effects of

parity changes which have occurred or may possibly occur in the future". It includes the case

"where an actual conversion may be made or where the cash-flow effect of an exchange Joss is

an impediment to the operations of one subsidiary, but also "the impact on future sales of a 20

company situated in a country whose currency has appreciated, or future profits where the local

currency has depreciated".

ii) Translation versus Transaction Currency Exposure

A fier defining accounting and economie exposures, Andreas PRINDL goes on to say that "the

impact of actual conversions is called 'transaction exposure', adding that, this is not all

encompassing as the term 'economie exposure'." This point makes translation and transaction

exposures worth looking at.

John HEYWOOD (1978) defines translation or balance sheet exposure muchas David Walker

defines accounting exposure. But to explain economie or transaction exposures, he quotes the

simplest case where a company has "one export order to sell goods in a currency. If the

currency in which the goods are invoiced appreciates, the company will make a gain; if it

depreciates, the company will suffer a Joss. He adds "the exposure arises as soon as the order is

taken, but it will not show in the financial accounts ... until it becomes a 'receivable' ."

J. A. DONALDSON (1980) distinguishes between transaction and translation exposures.

Transaction exposures "are revenue in nature and exist for relatively short periods". He said that

a sale from a seller to buyer in another country must be in the currency of, at best, one of them,

and the other one has an exposure, but only "when there is a period of delay in payment for the

goods" and " most transaction exposures arise from the granting of credit ". Translation

exposures on the other hand "relate to the balance sheet and are in existence for periods in

excess of a year."

These examples show "that the terminology is not yet agreed. There is sorne similarity ofviews

about balance sheet, translation and accounting risk, which most authors treat as almost

interchangeable tenns." For the economie exposure, things are stiJl foggy. For example, what

Donaldson calls transaction currency risk, PRINDL considers it an economie exposure.

To gain a clear understanding of the above classifications, a look at the different currency risk

measures may be worthwhile. In other words,

How can currency exposure be assessed? 21

b) Currency Risk Measurement

Foreign exchange position means for an individual foreign currency, assets denominated in that

currency minus liabilities denominated in that currency. A foreign exchange position of zero is

referred to as a closed foreign exchange position. A positive or negative foreign exchange

position is referred to as an open foreign exchange position. "Long position" means an open

foreign exchange position for an individual foreign currency where assets denominated in that

currency exceed liabilities denominated in that currency, plus the impact of off-balance sheet

items.

On the other hand, "short position" means an open foreign exchange position for an individual

foreign currency where liabilities denominated in that currency exceed assets denominated in

that currency, plus the impact of off-balance sheet items. Therefore, it should be noted that a

company with an open foreign exchange position (short or long) incurs a currency risk, i.e. a

potential gain or loss depending on the currency's future rate. This exposure can be measured in

severa! ways.

E. CLARK and B. MAROIS (1996) distinguish two methods: the first method limits the

analysis to commercial transactions and financial flows whereas the second looks at the averai!

balance sheet, including foreign investment and liabilities.

Using another approach, Richard LEVICH (1998), distinguishes what he calls "accounting

measures of foreign exchange exposure" and "economie measures of foreign exchange

exposure", the former being split into translation exposure and transaction exposure.

i) The Accounting Measure Method

Basically, the departure point for the accounting method is the information in the company's

accounts. Accounts receivable and short-term financial claims grouped by currency indicate the

firm's long position whereas accounts payables and short-term financial liabilities grouped by

currency indicate the firm's short position. For accounting purposes, the definition net exposure

is exposed assets minus exposed liabilities, provided that the accounting information is

complemented by the expected cash flows resulting from decisions that have been made or

likely to be made. But, as stressed by E. ClARK and B. MAROIS (1996) cash flows from non-22

commercial transactions (dividend payments and debt amortization) must also be considered.

The assessment ofthe company's currency exposure rcquires mastery of ali the firm's decision

making circuits. In fact, more than a mere accounting issue, currency exposure reflects the

company' s economie position in foreign exchange. Hence, the necessity of economie measures.

ii) The Economie Measure Approach

As underlined by Richard LEVICH1998), an economie measure of foreign exchange exposure

captures more than the combination of effects on balance sheet items (translation exposure) and

on plan transactions (transaction exposure)". It captures the entire range of effects on the future

cash flows of the firm, including the effects of exchange rate changes on customers, su pp liers

and competitors.

At the present point, it might be helpful to stress that economie measures can be designed in two

ways: l) the regression approach which Richard LEVICH qualified as "the most appealing

method ofmeasuring economie exposure" and 2) the scenario approach.

1) The Regression Approach

The regression approach d irectly measures the ex po sure of a firm to exchange rate changes by

estimating the relationship between the firm's market value at time t (Mv;) and the spot rate (St)

using the equation:

With:

-The coefficient b measures the sensitivity ofthe market value to the local & foreign

currency exchange rate. Dimensions ofb should be in a foreign currency, whieh coïncides with

the definition in the Michael ADLER and Bernard DUMAS (1984) that exposure is an amount

of foreign currency that represents the sensitivity of the real value of the firm to random

variations in the exchange rate.

-"a" is a constant variable, a provision for the part of the market value variation, the

explanation ofwhich lies in other factors.

"e" is the error term, E (e) =0 and is independent, identically distributed (iid) 23

2) The Scenario Approach

Given a scenario, one can estimate the firm's cash flows (and its market value) conditional on

an exchange rate path. The scenario approach is weil suited to a spreadsheet analysis where one

is encouraged to ask a variety of"what-if' questions.

e) Currency Risk Management

As previously d iscussed throughout the literature review of the currency risk definition and

assessment, exchange rate changes may have complex and subtle effects on the company's

performance-thus the necessity for hedging. Along with the financial markets development,

many tools, techniques and strategies have been developed to cover currency risks.

In developed countries, hedging strategies are many. They help firms of any size to mitigate

currency risks. Richard LEVICH (1998) examined sorne ofthose techniques such as currency

forward contracts, currency futures, currency options, currency swaps, etc. According to him,

"an important step in the process of determining financial hedging instruments for a firm is to

firstly analyze its currency cash tlows, the number of currencies, and the degree of certainty

about the cash tlows." Moreover, not ail these techniques can be used in ali cases especially

when such techniques are also in their infant stage in the Gambia's banking sector.

To a large extent this paper will basically adopt currency exposure as defined by Richard M.

LEVICII (1998) who as noted earlier on defined Foreign Currency Exposure as "the sensitivity

of the market value of the firm to a change in the (local to foreign currency) exchange rate"

Thus the reader would later realise that this definition suits us best because it has the advantage

of extending exchange rate exposure to a wide range of firms, including those with domestic

operations and with assets and liabilities denominated in domestic currency only. The reader

would note that Guaranty Trust Bank (G) Ltd reports its financial performance in Dalasi

denomination, which is the Gambian local currency.

In addition, this paper will adopt the regression method as explained by Richard M Levich to

test our hypothesis.

24

2.2 Research Mcthodology

To develop a measure of foreign exchange exposure, we need to start with an operational

definition of a firm's value. The value of a firm can be expressed in terms of a stream ofpresent

and future cash flows as follows:

(1)

The market value of a firm at time t (MJ!;) is the summation ofthe firm's cash flows (CF) over

time discounted back to their present value by an appropriate discount factor or discount rate (i)

It should be noted (CF) in this case is equal to after-tax profit Iess net investment.

Moreover, Cash flows in each currency are discounted at its own appropriate interest rate and

multiplied by a spot exchange rate.

In order to keep the mode! tractable so that the effects of the market structure could be

examined, wc assumed that the net investment of the firm is equal to zero and that cash flows

are expccted to be constant from year to year. In that the present value can be written:

MVt=CF = (1-T) "

. . 1 1

Where T is the tax rate and n is profit before taxes.

The basic measure of foreign exchange exposure is:

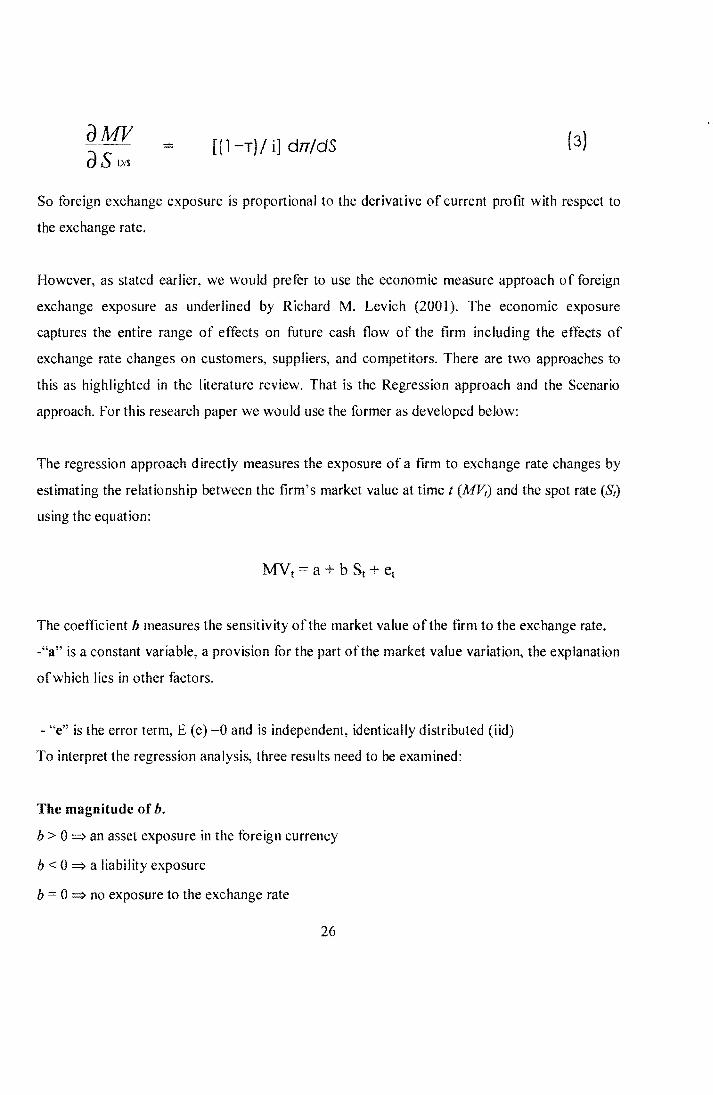

iJMJI as Dl$

(2)

Where S is exchange rate expressed as home currency/foreign currency. This measures the

nominal value (in home currency) that is exposed to the exchange rate. However, with taxes and

the discount rate constant, foreign exchange exposure becomes:

25

= as Dl$

[(1-T)/ i] drr/dS (3)

So foreign exchange exposure is proportional to the derivative of current profit with respect to

the exchange rate.

However, as stated earlier, we would prefer to use the economie measure approach of foreign

exchange exposure as underlined by Richard M. Levich (200 1 ). The economie exposure

captures the entire range of effects on future cash flow of the firm including the effects of

exchange rate changes on customers, suppliers, and competitors. There are two approaches to

this as highlighted in the literature review. That is the Regression approach and the Scenario

approach. For this research paper we would use the former as developed below:

The regression approach d irectly measures the exposure of a firm to exchange rate changes by

estimating the relationship between the firm's market value at time t (MVr) and the spot rate (St)

using the equation:

The coefficient b measures the sensitivity of the market value ofthe firm to the exchange rate.

-"a" is a constant variable, a provision for the part of the market value variation, the explanation

ofwhich lies in other factors.

- "e" is the error term, E (e) =0 and is independent, identically distributed (iid)

To interpret the regression analysis, three results need to be examined:

The magnitude of b.

b > 0 =::} an asset exposure in the foreign currency

b < 0 =::} a liability exposure

b = 0 =::} no exposure to the exchange rate

26

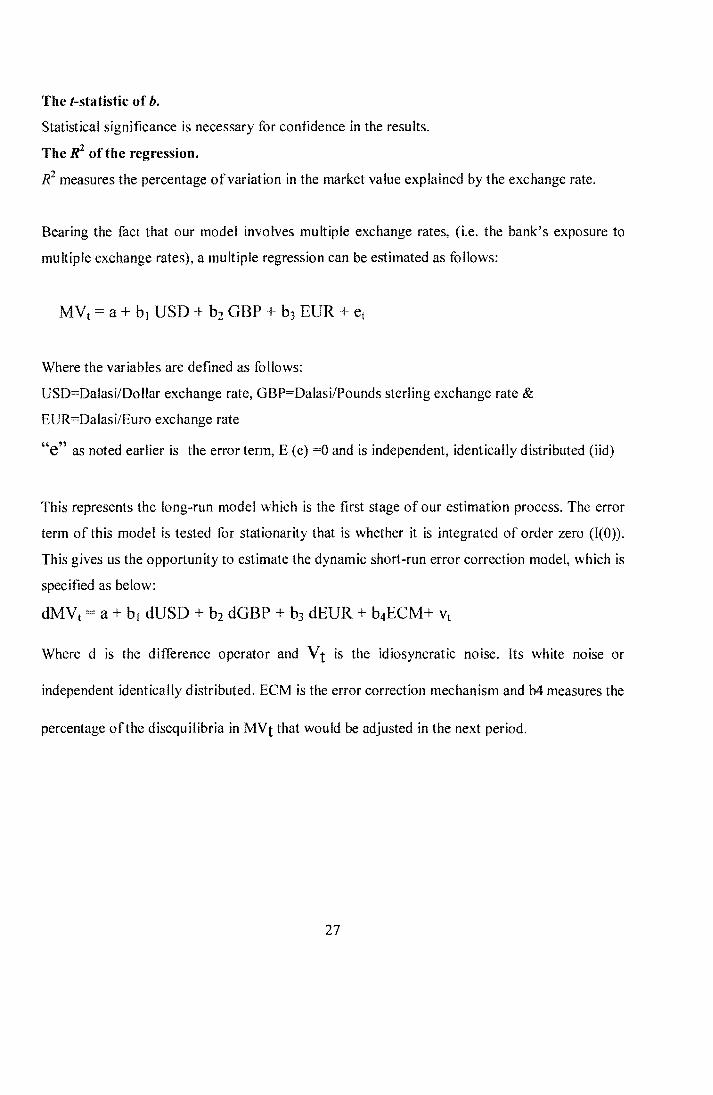

The t-statistic of b.

Statistical significance is necessary for confidence in the results.

The R2 of the regression.

R2 measures the percentage of variation in the market value explained by the exchange rate.

Bearing the fact that our mode! involves multiple exchange rates, (i.e. the bank's exposure to

multiple exchange rates), a multiple regression can be estimated as follows:

MVt =a+ b1 USD+ bz GBP + b3 EUR +et

Where the variables are defined as follows:

USD=Dalasi/Dollar exchange rate, GBP=Dalasi/Pounds sterling exchange rate &

EUR=Dalasi/Euro exchange rate

"e" as noted earlier is the error term, E (e) =0 and is independent, identically distributed (iid)

This represents the long-run mode! which is the first stage of our estimation process. The error

term of this mode! is tested for stationarity that is whether it is integrated of order zero (I(O)).

This gives us the opportunity to estimate the dynamic short-run error correction mode!, which is

specified as below:

dMVt a+ b1 dUSD + bz dGBP + b3 dEUR + b4ECM+ Vt

Where d is the difference operator and Vt is the idiosyncratic noise. Its white noise or

independent identically distributed. ECM is the error correction mechanism and b4 measures the

percentage of the disequilibria in MVt that would be adjusted in the next period.

27

Empirical Analysis

PARTTWO

Section 1 Empirical Analysis and Rescarch Findings

1.1 Empirical Analysis-Guaranty Trust Bank (G) Ltd

The Gambia does not have a stock market and as a result, data on stock returns is not readily

available. Following 2003 to 2008 data the market value proxied by profit before taxis used.

The monthly data on profit before tax of Guaranty Trust Bank and the exchange rate of Euro,

Great British Pound and the US Dollar (bath quarterly and monthly) were sourced from

Guaranty Trust bank and the Central Bank of The Gambia data base respectively. Additionally,

data on profit before tax (PBT) for the banking industry was sourced from the Central Bank of

the Gambia.

a) Unit Root Test

The Augmented Dickey-Fuller (ADF) (1979) test was used to determine the arder of integration

of the variables. We first tested whether the variables are I (1), that is integrated of arder one,

including an intercept or bath intercept and trend in the ADF regression. If I (1) is rejected in

favour of I (0), no differencing of the variables wou id be required. The Nu li Hypothesis is as

follows:

A: H0 : I (1) vs. H,: I(O)

B: Ho: I (2) vs. H,: 1(1)

Unit root test (first difference) with intercept

Table 1 : Results of first Difference ADF Test

ADF test Critical values

! 1 5 10

Variables with intercept percent percent percent

EUR -8.367 -3.526 -2.905 -2.589

GBP -4.597 -3.53 -2.905 -2.590

PBT -8.79 -3.53 -2.905 -2.590

USD -4.493 -3.53 -2.905 -2.590 i

By including only the intercept in the ADF regression, ali the variables were l(l) at 1 percent

leve) ofsignificance. We could not reject the null hypothesis in A abovc. This indicates that the

variables should be differcnccd once in order to be stationary.

b) Co integration Test

Johanscn (1988, 1991) co-integration method/proccdure was used to determine the number of

co-integrating relations among the variables. The number of co-integrating relations is

examined in a system containing four variables. The following Vcctor Autorcgressive (VAR)

mode! was estimated using two lags ofexchange rates and profit beforc tax.

Where (PBT, EUR, USD, GBP)

ln testing for co-integration, we allowcd for linear deterministic trend in the data but no trend in

the co-integrating equation. If the variables arc co-integrated, there exists a long-run

relationship between them.

2

Table 2 : Unrestricted Co-integration Rank Test (Trace)

No of observations is 65

! Hypothesized Trace 0.05

No. ofCE(s) Eigenvalue Statistic Critical Value Prob.**

None* 0.282389 48.89375 47.85613 0.0398

At most 1 0.193548 25.99762 29.79707 1 0.1288

At most 2 0.139400 11.15494 15.49471 0.2022 i

At most 3 0.011475 0.796321 3.841466 0.3722

Trace test indicates 1 co integrating eqn(s) at the 0.05 levet

* denotes rejection of the hypothesis at the 0.05 leve!

For a system including profit before tax and the cxchange rates (EUR, USD and GBP), Trace

test reveals one co-integrating relations at 5 percent leve! of significance. This implies that

there exists a stable long-run relationship between profit before tax (PBT) ofGuaranty Trust

Bank (GTB) and the exchange rates (EUR, USD and GBP).

Firstly, a long-run mode! was estimated. In this mode!, ali the variables were included at levels

and also no logarithm was used as demanded by the specification of the mode!. The long-run

mode! contains sorne errors which need to be corrected, thus leading to short-run dynamic

mode!. The long-run madel is as follows.

Table 3: Long-run mode1

EURO i USD 1 GBP

coefficients 3.2 -263.9 46.7

t- statistic -0.71 -2.45* 0.96

R-squared=0.74, DW=l.07, F-stat=O.OO

*denotes significance at 5 percent leve! ofsignificance.

3

!

The long-run elasticity of EURO and GBP despite been positive, both were insignificant in

determining changes in PBT ofGuaranty Trust Bank. The coefficient ofthe USD was

significant and negative, indicating long-run liability exposure. R-squared indicates that these

variables explains about 74 percent of changes in profit before tax in the long-run while F-stat

shows that at least one ofthese variables is significant in determining changes in PBT.

The error term of the long-run mode! was tested for stationarity that is integrated of order zero (1

(0)). By including only the intercept and also allowing for one lag in the ADF regression, the

error term of the long-run mode! was integrated of order zero that is I (0). This allows for the

error correction specification ofthe mode!.

c) Short-run Error Correction modcl

A short-run error correction mode! was used to determine the relationship between profit before

tax ofGTB and exchange rate ofthe Domestic currency (Dalasi) against the major international

currencies (USD, GBP and EURO). (See Appendix I Table 5) The research findings of the

short-run error correlation mode! used are detailed below in sub-section 1.1.

1.2 Rcscarch Findings

a) Guaranty Trust Bank (G) Ltd

A dynamic short-run error correction mode! was estimated to determine the relationship

between profit before tax (PBT) and the rates of exchange of the US dollar (USD), the Great

British Pound (GBP) and the Euro (EUR). The results show that current exchange rate ofthe

US dollar is significant in influencing changes in profit before tax (PBT) of Guaranty Trust

Bank at 10 percent leve! of significance(Table 5 Appendix 1). The sign of the coefficient is

negative, indicating liability exposure toUS dollar exchange rate. On the other hand, the current

exchange rate ofEuro (EUR) and Great British Pound (GBP) were insignificant.

The lagged value ofthe US dollar (4 lags) on profit before taxis signifieant at 10 percent leve!

of significance (Table 5 Append ix I). However, its coefficient is positive, indicating asset

exposure. Similarly, the coefficients of the second lag, fifth and sixth lags of Great British

Pound were significant at 1 percent, 5 percent and 10 percent levels of significanee. The sign of 4

their coefficients is positive, reflecting asset exposure. No significant lags were observed in case

of the Euro. A dummy variable, reflecting exchange rate appreciation from April, 2007 was

significant at 1 percent leve! of significance. Its coefficient has a negative sign, reflecting

liability exposure.

The coefficient of the error term from the long-run regression is negative and significant at l

percent leve] ofsignificance. The size ofthe coefficient indicates that the speed ofadjustment in

Guaranty trust bank is quite fast. It shows that about 69 percent of the disequilibria in the profit

before tax due to exchange rate exposure is corrected in the next period. R-squared shows that

these variables exp lain about 59 percent of the variations in profit before tax. The F-statistic

also shows that at !east one of these variables is significant in determining changes in profit

be fore tax (Table 5 Append ix 1).

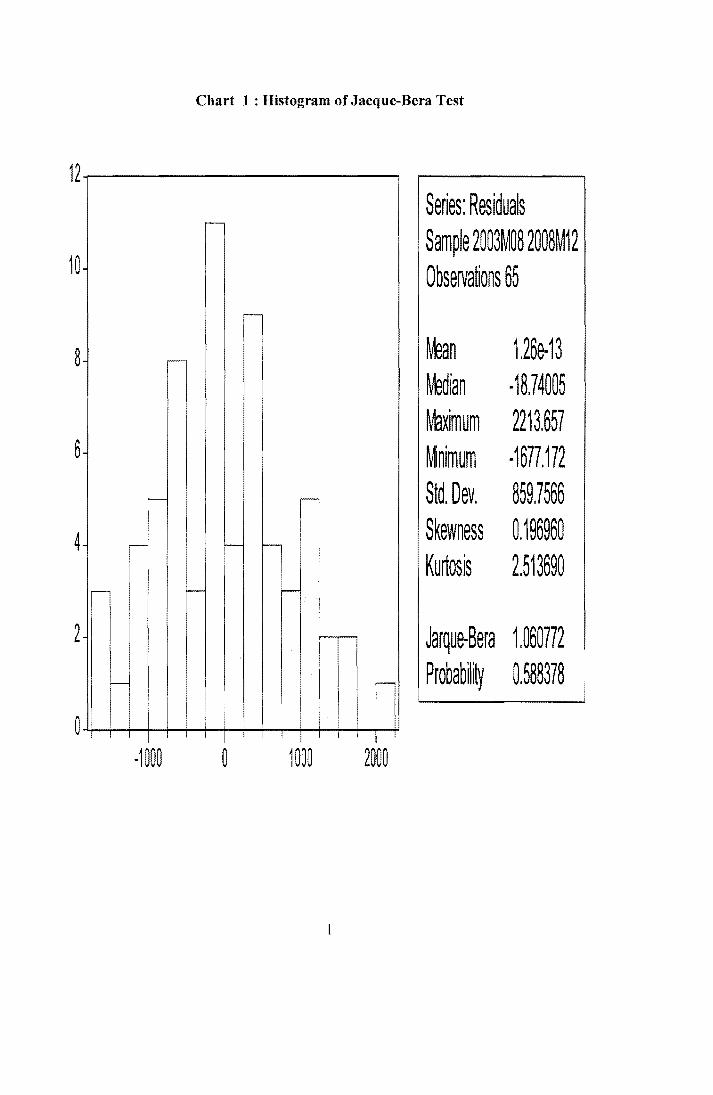

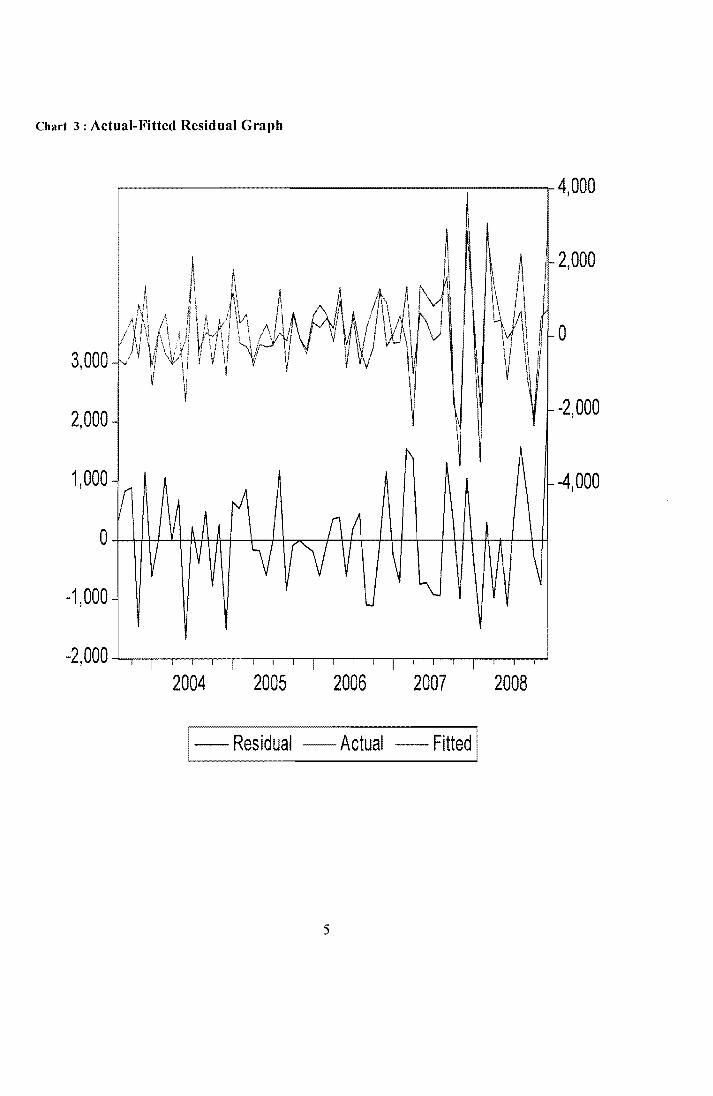

The mode! was tested for normality using Jarque-Bera test. The results indicate normality at 1

percent leve] of significance. This is also supported by the Kurtosis (2.5) and the residual series

has a skewness of0.19 (Chart 1 Appendix 1).

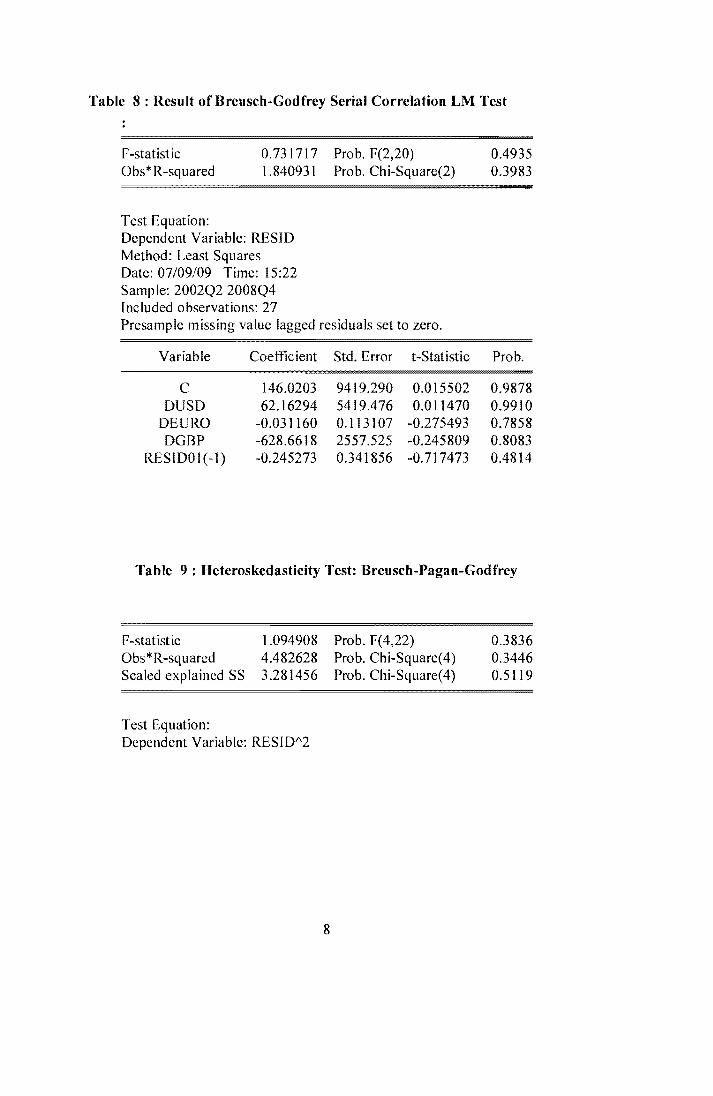

Seriai correlation test was also conducted using Breush-Godfrey seriai correlation test. The

results reveal no seriai correlation at 1 percent leve! of significance (Table 6 Appendix 1).

Additionally, Arch test indicates no heteroskedasticity at l percent significant levet (Table 7

Appendix 1). CUSUM of squares test reveals no specification error of the mode!.

These results prompted us to investigate what obtains at Guaranty Trust Bank (G) Ltd in

practice to ascertain whether it agrees with the findings as mentioned above. lt was realised that

foreign currency deposits(USD, GBP & EUR) constituted about 31% of of the Banks total

deposits as at end December, 2007. (Figure 5 Appendix III).

Moreover, it was also noted that Exchange Earnings had direct impact on the PBT.As could be

seen in Figure l & 2 Appendix III, Exchange Earnings and PBT seemed to follow the same

trend. One could not help but notice that in the month of September, 2007 Exchange Earnings

skyrocketed to &Million dalasi, mainly as a result of revaluation gains. Profit Before Tax, that

same month, was also &Million Dalasi. 5

Finally, our findings revealed that GTB positioned itself at oversold position in terms of foreign

exchange trading when the Dalasi showed sorne signs of appreciation in the early part of July

2007. This accounted for the revaluation gains as explained above. The Debit spot position ,

except for the British Pound, could not be reversed throughout the year (2008) exposing GTB

to fluctuations in foreign exchange rates.(Figure 8 Appendix III)

b) Rcscarch Findings-The Banking Industry

For the Banking Industry, only quarterly data from 2000-2008 on profit before tax was

available. As a result of data constrain, no lags were included in the regression analysis. The

long-run mode! was first estimated using ali the variables at levet and the error term of this

regression was tested for stationarity at leve! by including the intercept as weil as both the

intercept and trend in the ADF regression. Then the short-run error correction mode! was

estimated which showed significant improvements on the long-run model which has low R

squared (27 percent) and few significant variables( only the US dollar was significant at 10

percent leve! ofsignificance).

The results ofthe short-run dynamic mode! show asset exposure relating to changes in both the

US dollar and Euro which has positive coefficients and were significant at 5 percent and 10

percent levels of significance respectively (Table 8 Appendix I). The coefficient of the Great

British Pound was insignificant. The coefficient of the error term was negative and significant.

lt shows faster adjustment in the banking system as a whole with regards to changes in profit

before tax due to exchange rate changes.

The R-squared shows that these variables explain about 63 percent ofvariations in profit before

tax of the banking system. Additionally, the F-statistic was significant at 1 percent leve! of

significance, indicating that at !east one ofthese variables is significant in determining changes

in profit before tax( Table 8 Appendix II).

The mode! was also tested for normality using Jacque-Bera test. This test also shows normality

ofresidual series at ali conventional levels of significance (Chart 4 Appendix II). Additionally,

no seriai correlation was found in the mode! at ali levels of significance(Table 9 Appendix II) 6

wh ile heteroskedasticity was also rejected at 1 percent leve! of significance( Table 10 Appendix

II)

Consequently, hedging techniques as proposed in the next section could be adopted were

suitable to mitigate foreign exchange exposure in the Banking Industry especially Guaranty

Trust Bank (Gambia) Limited.

Section 2 HEDGING PROPOSALS FOR THE MANAGEMENT OF FOREIGN

EXCHANGE RISK

In the contest of this paper, hedging refers to those activities employed by firms to reduce or

eliminate their exposure to exchange rate changes arising from transactions or existing assets

and liabilities denominated in foreign currencies. Exchange rate fluctuations bring about

variability in the value of expected cash flows. So foreign exchange exposure or risk might

bring extra profits or !osses. But being exposed in a currency does involve a gambie, and most

businessmen wou Id pre fer not to let the ir company' s profit or !osses hinge on a gambie if they

can avoid it. Hence businesses look for ways ofminimizing or eliminating entirely their foreign

exchange exposure, so that they can plan their businesses and foresee their profits with greater

confidence. The Bank therefore, can do this by employing any of the under-listed tools and

techniques:

(a) Limits on foreign exchange position

(b) Shortening of tenor of foreign currency loans

(c) Foreign currency deposits (Accounts)

( d) Foreign currency swaps

(e) Forward contacts

(f) Currency options

2.1 Limits on Foreign Exchangc Position

Traders in treasury units would advice that banks should position themselves in debit spot

position throughout the period when the local currency strengthens against the foreign

currencies in ordcr to enjoy a great amount of revaluation gains and the reverse when it

weakens. Guaranty Trust Bank (G) Ltd made revaluation gains to the tune of GMD8Million in 7

September, 2007. (Appendix III -Figure 2). However this practice should be done with caution

because the exchange rates may fluctuate unfavourably at the shortest possible notice, especially

in the case ofpolitical instability.

1t is against this background that the Central Bank guide !ines stipulate a limit on foreign

exchange currency position as a percentage of the bank's shareholders funds. "Authorized

financial institutions must maintain a set of specifie internai limit on the risk exposure to

various currencies they are trading in. The overnight open limit of each currency should not

exceed 15% of the bank's adjusted capital." (Guideline 7 p.6) The use of other control measures