OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE, …

27

am:ramC,-I ctil c•144, arriztvr, 4wtrzir reirc en, OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE, AHMEDABAD1 *Fdtzr anra er waif, Laravicti * Mid CENTRAL EXCISE BUILDING, NEAR OM. POLYTECHNIC Antra, wenn - 380 018 AIMIAWADI, AHMEDABAD — 380 015. F.No: V.84/15-20/PPI Pumps/ADC/OA-I/2014 ailtaLteM: Date of Order : 28.111014 uZf *1 .4 altar: Date of Issue : 28.11.2014 zrt tre3A cad (41 . ) 1 - frt (facd4.) fAirirt 31t1 “113cid1H iwr dr Thv 44m tr orief) t This copy is granted free of charge for private use of the person(s) to whom it is sent. zEft ml &11 z 4a. Tfr 3lItYt #f 17fzi - *1 arFETTZ 39aTa mt r t, at. 31T 3f1t# fdad Y9-47 (3111-#), 4,a 14 actlIC 4)d-44 dcme 514#, 311nTaitt, 31- FIRTRR-15 3:14t# a.Z elchica t I sacs 3141# trar* -rt 4T arrayOA . yaw aruar 3i1 31W 441.0511171: ebio-f ( -Ad er t graT tf Mrgf I 411-ii azid 2.00/- dim{ wrnivileier fecric F;Tf wrfnr I Any person deeming himself aggrieved by this Order may appeal against this order in Form E.A.1 to Commissioner (Appeals), Central Excise, Central Excise Bhavan, Near Government Polytechnic, Ambawadi, Ahmedabad -15 within sixty days from date of its communication. The appeal should bear a court fee stamp of Rs.2.00f- only. anti Sal %Iraqi- at tiRict A. .TT.- (S) iWzigrar, 2001 Si.{ 3 aTAaCr I Tfr'th -F fA'a ardit The Appeal should be filed in form No. accordance with provisions of Rule 3 accompanied with the following: 5.rcr srr- Copy of the aforesaid appeal. fa S4 1 al cede trw 3u 3ITter S sr#rfat# sritrgfer rat art tcr itrk fd. t g.13. 34`4141 3Wa 311tRT t't 3W 1 511 11 , 19T S 2.00/- fit 0-4I4e1ef Yr tactic afaszr wirrOcrir vrItv Copies of the Decision (one of which at least shall be certified copy of the order appealed against) or copy of the said Order bearing a court fee stamp of Rs.2.00/-. 3Ti2,er i ed- F" ZiP:11 Yr, t ali CI CT4 aelicht 3:1flatzT ur Rt 7.5% att sitrar Kr* 3:PLI4T apHoil att St* aNt coo t atm,' 3. WaTa 31117 gl9,c?1 tl An appeal agaisnt this order shall lie before the Tribunal on payment of 7.5% of the duty demanded where duty or duty and penalty are in dispute, or penalty, where penalty alone is in dispute". /Reference :Mliuf AW3111. watt Thtlt. F.No: V.84/15-20/PPI Pumps/ADC/OA-I/2014 dated 06.052014 issued to M/s. PPI Pumps Pvt.Ltd., Plot No.14 & 16E, GIDC, Phase-I, Vatva, Ahmedabad. cg, r wita Passed by: DeManaj Kumar Rajak, ADDITIONAL COMMISSIONER ks*ksks *sksksneks*skmekks ,, s , ksk*sksk*skskk*kkkklmk*skkk** skkseksks,ksk 7ff .311r tOrder-In-Original No.: 47/CX-I Ahmd/ADC/MKR/20.14 ,,,,, kkkm kk*********kk**************************kks*skk********* kk ***** ks * ** **** araT t 5#4, (3 , 4 ) 1 Rt &TfttiaS au OIV 13H4t 4,0-414 ortio 39 - 4111 39 -4r1 3141 , c r47rrerr f*v HMaH fa,Lir 71cr : E.A.-I in duplicate. It should be filed by the appellants in of the Central Excise (Appeals) Rules, 2001. It shall be

Transcript of OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE, …

am:ramC,-I ctil c•144, arriztvr, 4wtrzir reirc en,

OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE, AHMEDABAD1

*Fdtzr anra er waif, Laravicti * Mid

CENTRAL EXCISE BUILDING, NEAR OM. POLYTECHNIC Antra, wenn - 380 018 AIMIAWADI, AHMEDABAD — 380 015.

F.No: V.84/15-20/PPI Pumps/ADC/OA-I/2014 ailtaLteM: Date of Order : 28.111014

uZf *1.4 altar: Date of Issue : 28.11.2014

zrt tre3A cad (41 .) 1 -frt (facd4.) fAirirt 31t1

“113cid1H iwr dr Thv 44m tr orief) t This copy is granted free of charge for private use of the person(s) to whom it is sent.

zEft ml &11z4a. Tfr 3lItYt #f 17fzi- *1 arFETTZ 39aTa mt r t, at. 31T 3f1t# fdad

Y9-47 (3111-#), 4,a 14 actlIC 4)d-44 dcme 514#, 311nTaitt, 31-FIRTRR-15

3:14t# a.Z elchica t I sacs 3141# trar*-rt 4T arrayOA . yaw aruar 3i1

31W 441.0511171: ebio-f (-Ad er t graT tf Mrgf I 411-ii azid 2.00/-

dim{ wrnivileier fecric F;Tf wrfnr I

Any person deeming himself aggrieved by this Order may appeal against this order in Form E.A.1 to

Commissioner (Appeals), Central Excise, Central Excise Bhavan, Near Government Polytechnic,

Ambawadi, Ahmedabad -15 within sixty days from date of its communication. The appeal should bear a

court fee stamp of Rs.2.00f- only.

anti Sal %Iraqi- at tiRict A. .TT.-

(S) iWzigrar, 2001 Si.{ 3

aTAaCr I Tfr'th-F fA'a ardit The Appeal should be filed in form No.

accordance with provisions of Rule 3

accompanied with the following:

5.rcr srr-

Copy of the aforesaid appeal.

fa S4 1 al cede trw 3u 3ITter S sr#rfat# sritrgfer rat art tcr itrk fd.t

g.13. 34`4141 3Wa 311tRT t't 3W 1 511 11,19T S 2.00/- fit 0-4I4e1ef Yr tactic

afaszr wirrOcrir vrItv Copies of the Decision (one of which at least shall be certified copy of the order appealed against) or copy of the said Order bearing a court fee stamp of Rs.2.00/-.

3Ti2,er i ed-F" ZiP:11 Yr, tali CI CT4 aelicht 3:1flatzT ur Rt

7.5% att sitrar Kr* 3:PLI4T apHoil att St* aNt

coo t atm,' 3.WaTa 31117 gl9,c?1 tl An appeal agaisnt this order shall lie before the Tribunal on payment of 7.5% of the duty

demanded where duty or duty and penalty are in dispute, or penalty, where penalty alone is in dispute".

/Reference :Mliuf AW3111. watt Thtlt. F.No: V.84/15-20/PPI Pumps/ADC/OA-I/2014 dated

06.052014 issued to M/s. PPI Pumps Pvt.Ltd., Plot No.14 & 16E, GIDC, Phase-I, Vatva,

Ahmedabad.

cg, r wita Passed by: DeManaj Kumar Rajak, ADDITIONAL COMMISSIONER

ks*ksks *sksksneks*skmekks ,, s ,ksk*sksk*skskk*kkkklmk*skkk** skkseksks,ksk

7ff .311r tOrder-In-Original No.: 47/CX-I Ahmd/ADC/MKR/20.14

,,,,, kkkm kk*********kk**************************kks*skk********* kk ***** ks *** ****

araT t 5#4, (3 ,4 )

1 Rt &TfttiaS au OIV 13H4t 4,0-414 ortio

39 -4111 39-4r1 3141 , c r47rrerr f*v

HMaH fa,Lir 71cr : E.A.-I in duplicate. It should be filed by the appellants in

of the Central Excise (Appeals) Rules, 2001. It shall be

Page 1 of 26 47/CX-I Ahmd/ADC/MKR/2014

BRIEF FACTS OF THE CASE:

M/s PPI Pumps Pvt. Ltd., 14 & 16-E, Phase-I, GIDC, Phase-I, Vatva, Ahmedabad

(herein after referred to as the assessee) was engaged in the manufacture of various

products falling under Chapter 84 of the First Schedule to the Central Excise Tariff Act,

1985 and having Central Excise Registration No. AABCP5949DEM001. The said

assessee was also availing the benefit of Cenvat Credit Scheme as envisaged in the

Cenvat Credit Rules, 2004. During the course of Audit in the month of June' 2013 by the

Audit wing of C.Ex., Ahmedabad-I for the period from March, 2011 to February 2013, it

was noticed that the said assessee had availed the Cenvat Credit of Service Tax on

Commission paid to foreign/loal Agent.

2. A letter dated 02.08.2013 was issued by the Jurisdictional Range

Superintendent, Range-IV, Division-II, ("the JRS") to the assessee regarding non

admissibility of the input credit of commission paid to the Foreign/Local agent and to

reverse the same, if it was taken. The assessee was also requested to submit the

details of such Service Tax credit taken on commission paid to foreign/Local agent, but

they had not submitted the same. On being summoned on 30.09.2013, Shri Rajnikant

R. Bhaysar appeared before the JRS on 01.10.2013 and his statement was recorded,

wherein he promised to produce details of Cenvat credit availed by them on commission

paid to local & foreign Agent. However, he did not produce relevant documents even

after lapse of long period, and several reminders were issued to them. Thereafter, the

details/documents were submitted by the assessee on 10.03.2014. It was noticed that

the said assessee had wrongly availed CENVAT Credit of service tax amounting to

Rs.10,32,149/- (for the period from April 2009 to September-2013) paid on the sales

commission paid to the foreign/local agents for clearance of the finished goods.

Whereas it appeared in light of legal provisions that the assessee had failed to comply

with the statutory provisions & procedure laid down for availing the CENVAT Credit in

as much as they had availed cenvat credit of service tax paid on sales commission paid

to the foreign/local agents. The service provided by sales commission agents was not

included /defined as input service in rule 20) of Cenvat Credit Rules, 2004.

3.1 It was noticed that the said assessee had availed Cenvat Credit of service tax

paid on commission to local/foreign sales agent for the period from April, 2009 to

September, 2013. Further inquiry in the matter was caused and a statement of Shri

Rajnikant R. Bhaysar, authorized signatory of M/s PPI Pumps Pvt. Ltd., 14 & 16-E,

Phase-I, GIDC, Phase-I, Vatva, Ahmedabad was recorded on 01.10.2013 under Section

14 of the Central Excise Act, 1944; wherein he interalia stated that M/s PPI Pumps Pvt.

Ltd. availed and utilized CENVAT credit on sales commission paid to the Foreign/local

sales agents, regarding the delay of the submission of details of cenvat credit taken on

commission paid to foreign/local agent, he stated that there was delay on their part; that

they had taken cenvat credit on Deibt note but they had not taken any cenvat credit on

credit note; that they had not taken any cenvat credit after September 2013 on the

Page 2 of 26 47/CX-1 Ahmd/ADC/MKR/2014

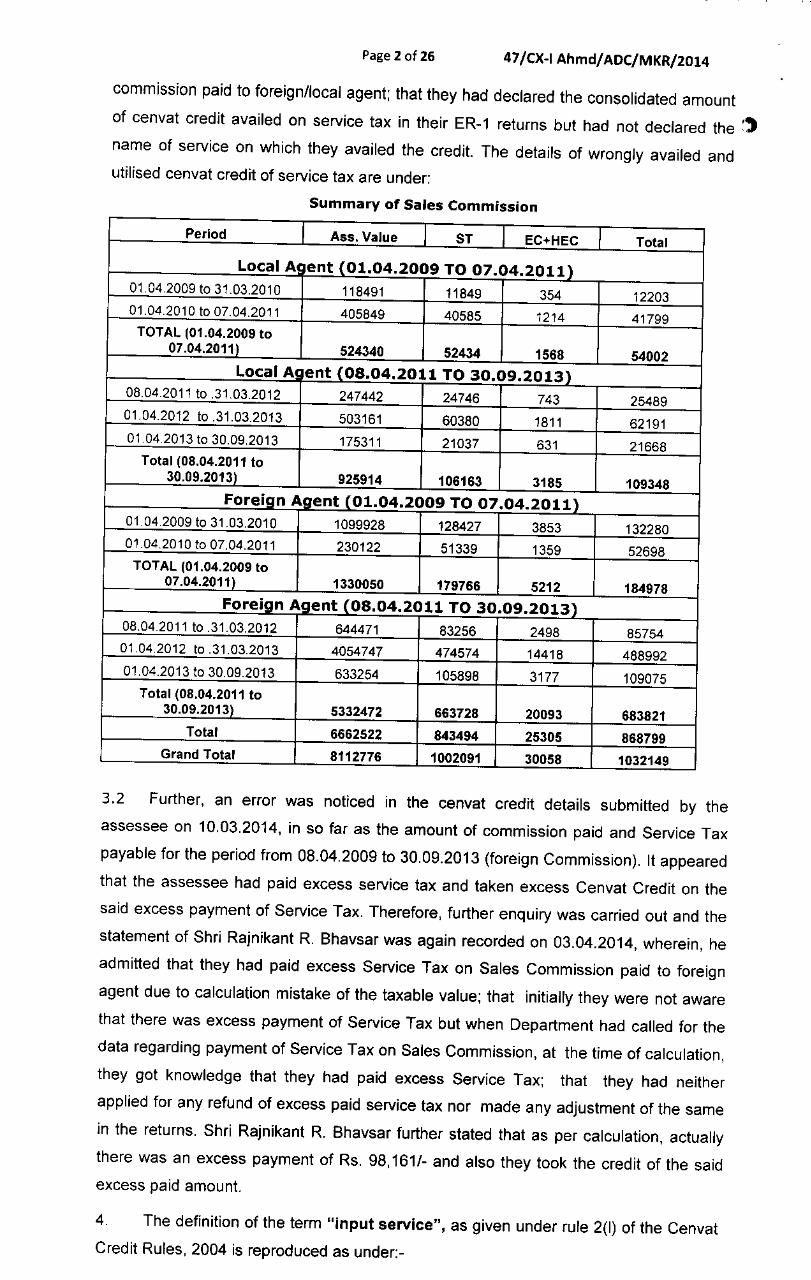

commission paid to foreign/local agent; that they had declared the consolidated amount

of cenvat credit availed on service tax in their ER-1 returns but had not declared the 1

name of service on which they availed the credit. The details of wrongly availed and

utilised cenvat credit of service tax are under:

Summary of Sales Commission

Period I Ass. Value I ST I EC+HEC I Total

Local A ent (01.04.2009 TO 07.04.2011) 01.04.2009 to 31.032010 118491 11849 354 12203 01.04.2010 to 07.04.2011 405849 40585 1214 41799

TOTAL (01.04.2009 to 07.04.2011) 524340 52434 1568 54002

Local As ent (08.04.2011 TO 30.09.2013) 08.04.2011 to .31.03.2012 247442 24746 743 25489 01.04.2012 to .31.03.2013 503161 60380 1811 62191 01.04.2013 to 30.09.2013 175311 21037 631 21668

Total (08.04.2011 to 30.09.2013) 925914 106163 3185 109348

Foreign Agent (01.04.2009 TO 07.04.2011) 01.04.2009 to 31.032010 1099928 128427 3853 132280 01.04.2010 to 07.04.2011 230122 51339 1359 52698

TOTAL (01.04.2009 to 07.04.2011) 1330050 179766 5212 184978

Foreign Agent (08.04.2011 TO 30.09.2013) 08.04.2011 to .31.03.2012 644471 83256 2498 85754 01.04.2012 to .31.03.2013 4054747 474574 14418 488992 01.04.2013 to 30.09.2013 633254 105898 3177 109075

Total (08.04.2011 to 30.09.2013) 5332472 663728 20093 683821

Total 6662522 843494 25305 868799 Grand Total 8112776 1002091 30058 1032149

3.2 Further, an error was noticed in the cenvat credit details submitted by the

assessee on 10.03.2014, in so far as the amount of commission paid and Service Tax

payable for the period from 08.04.2009 to 30.09.2013 (foreign Commission). It appeared

that the assessee had paid excess service tax and taken excess Cenvat Credit on the

said excess payment of Service Tax. Therefore, further enquiry was carried out and the

statement of Shri Rajnikant Ft Bhaysar was again recorded on 03.04.2014, wherein, he

admitted that they had paid excess Service Tax on Sales Commission paid to foreign

agent due to calculation mistake of the taxable value; that initially they were not aware

that there was excess payment of Service Tax but when Department had called for the

data regarding payment of Service Tax on Sales Commission, at the time of calculation,

they got knowledge that they had paid excess Service Tax; that they had neither

applied for any refund of excess paid service tax nor made any adjustment of the same

in the returns. Shri Rajnikant R. Bhaysar further stated that as per calculation, actually

there was an excess payment of Rs. 98,161/- and also they took the credit of the said

excess paid amount.

4. The definition of the term "input service", as given under rule 2(1) of the Cenvat

Credit Rules, 2004 is reproduced as under:-

Page 3 of 26 47/CX-I Ahmd/ADC/MKR/2014

"U) "input service" means any service, —

(i) used by a provider of taxable service for providing an output service; or

00 used by a manufacturer, whether directly or indirectly, in or in relation to the manufacture

of final products and clearance of final products upto the place of removal,

and includes services used in relation to setting up, modernization, renovation or repairs of a

factory, premises of provider of output service or an office relating to such factory or premises,

advertisement or sales promotion, market research, storage up to the place of removal,

procurement of inputs, activities relating to business such as accounting, auditing, financing,

recruitment and quality control, coaching and training, computer networking, credit rating, share

registry and security, inward transportation of inputs or capital goods and outward transportation

up to the place of removal; a

5. The definition of input service fixes the meaning of that expression and the

services, used by the manufacturer, were required to have a nexus with the

manufacture of the final product and clearance of the final product upto the place of

removal. Place of removal is well defined in Section 4(3)(c)of the Central Excise

Act,1944 and the services which were enumerated in the inclusive clause, which applies

both, in the context of the provider of output services as well as the manufacture, cannot

be read de hors the meaning of input service under Rule 20) of Cenvat Credit Rules,

2004. Therefore, all the activities relating to business, which were input services used

by the manufacturer in relation to the manufacture of final product and clearance of the

final product upto the place of removal alone appeared to be eligible. After the final

products are cleared beyond the place of removal, there will be no scope for

subsequent use of service to be treated as input services. Therefore, services utilized

beyond the stage of manufacturing and clearance of the goods from the factory could

not be treated as input services. Thus, it appeared that for the purpose of ascertaining

the admissibility of cenvat credit on services, the nature of service availed should be in

consonance with the above parameters. Hence, the said assessee appeared to have

wrongly availed Cenvat Credit of Service tax paid on commission paid to local/foreign

sale agent for sale of finished goods cleared to their customers contrary to the

provisions of Rule 3 of Cenvat Credit Rules, 2004 read with Rule 20) ( H) of the Cenvat

Credit Rules, 2004 which needed to be recovered from them along with interest.

6. Further, the provisions of Rule 3(1) of Cenvat Credit Rules, 2004, allowing a

manufacturer or producer of final product or a provider of taxable service to take Cenvat

Credit of various duties/taxes leviable under different provisions of law read as under;-

"RULE 3. CENVAT Credit. - (1) A manufacturer or producer of final products or a provider of

taxable service shall be allowed to take credit (hereinafter referred to as the CENVAT credit) of -

(ii) (Hi) .......

(iv) .

(v) ...

(vi) .

Page 4 of 26 47/a-I Ahmd/ADC/MKR/2014

(via) ... (vii) (viia) . (viii) (ix) the service tax leviable under section 66 of the Finance Act; and (x) (xa) (xi) paid on-

(i) any input or capital goods received in the factory of manufacture of final product or premises of the provider of output service on or after the 10th day of September, 2004; and

(ii) any input service received by the manufacturer of final product or by the provider of output services on or after the 10th day of September, 2004,

including the said duties, or tax, or cess paid on any input or input service, as the case may be, used in the manufacture of intermediate products, by a job-worker availing the benefit of exemption specified in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 214/86- Central Excise, dated the 25th September, 1986. published in the Gazette of India vide number G.S.R. 547 (E), dated the 25th September, 1986, and received by the manufacturer for use in, or in relation to, the manufacture of final product, on or after the 10th day of September, 2004."

7. It appeared that services of local/foreign sales commission agent used by the

manufacturer were neither used, directly nor indirectly, in or in relation to the

manufacture of final products. Therefore, the said assessee appeared to have wrongly

availed cenvat credit of service tax paid on commission paid to local/foreign agent which

did not fall within the purview of definition of input service. The said service appeared to

be availed by the said assessee after the clearance of finished goods from the factory

gate i.e. beyond the place of removal. Since, the services of local/foreign sales

commission agent did not have any relation with the manufacturing activity and also did

not appear to fall within the ambit of definition of input services as defined under Rule

2(I) of Cenvat Credit Rules, 2004, the manufacturer should not be allowed to take credit

on such ineligible service as per Rule 3 of Cenvat Credit Rules, 2004.

8. Further, services of the sales commission agent also did not appear to fall under

the category of sales promotion. As per the definition of commission agent defined

under clause (a) to the Explanation under section 65(19) of the Finance Act 1994, a

commission agent is a person who acts on behalf of another person and causes

sale or purchase of goods. In other words, the commission agent appeared to be

directly responsible for selling or purchasing on behalf of another person and that such

activity cannot be considered as sales promotion. There appeared to be a clear

distinction between sales promotion and sale. A commission agent was directly

concerned with sales rather than sales promotion. Therefore, the services provided by

commission agent did not fall within the purview of the main or inclusive part of the

definition of 'input service' as laid down in rule 2(I) of the Cenvat Credit Rules, 2004 and

it appeared that the said assessee did not appear to be eligible for CENVAT credit in

Page 5 of 26 47/CX-I Ahmd/ADC/MKR/2014

respect of the service tax paid on commission paid to local/foreign sale agents for sales

of final product.

9. Further, the excess payment made by the assessee to the tune of Rs. 98,161/-

could not be considered as payment of Service Tax and was merely a deposit as such.

The said assessee was not entitled to take Cenvat Credit of such excess deposit made

by them and the same did not fall under any of the category of duties envisaged under

rule 3 of Cenvat Credit Rules, 2004. As such, they were not entitled to the suo mob

Cenvat credit of such excess deposit amount.

10. It was pertinent to note that the Hon'ble High Court of Gujarat in the case of

Commissioner of Central Excise, Ahmedabad-II Vs. Cadila Health Care Ltd, 2013-TIOL-

12-HC-AHM-ST, had held that "Commission agent is directly concerned with the sales

rather than sales promotion and as such the service provided by such commission

agent would not fall within the purview of the main or inclusive part of the definition of

input service as laid down in rule 2(1) of the Cenvat Credit Rules, 2004. Consequently,

Cenvat credit would not be admissible in respect of the commission paid to foreign

agents". Further, the Hon'ble CESTAT Ahmedbad's Order in the case of Commissioner

of Customs & Central excise, Surat-II V/s. Astik Dyestuff P. Ltd. vide order No.

A/10339/WZB/AHD/2013 dated 01.03.2013 had held that "the law laid down by Hon'ble

High Court of Gujarat in the case of Cadila Healthcare (Supra) is squarely applicable to

the facts of the present case. No distinction can be made between the commission paid

to foreign agent and the agent operating within the territory of India because nature of

services provided by both the categories of agents are same. Consequently, Cenvat

Credit would not be admissible in respect of service tax paid on the commission paid to

the local agents". It appeared that the ratio of the decision of the Hon'ble High Court of

Gujarat as well as Hon'ble CESTAT, Ahmedabad was squarely applicable for services

of sales commission for local/foreign agents.

11. It was noticed that the said assessee had wrongly availed CENVAT Credit of

service tax amounting to Rs.10,32,149/- (for the period from April 2009 to September-

2013) paid on the sales commission paid to the local/foreign agents for the sales of their

finished goods (as detailed in Annexure 'At to the SCN). The said wrongly availed

Cenvat credit was inclusive of suo-moto Cenvat credit taken by them of excess payment

made by them as detailed in Annexure-A2 to the SCN. It appeared in light of legal

provisions that the said assessee had failed to comply with the statutory provisions &

procedure laid down for availing the CENVAT Credit in as much as they had availed

cenvat credit of service tax paid on sales commission paid to the local/foreign agents

and also they had availed Cenvat credit of excess payment made by them. The service

provided by sales commission agents was not included/defined as input service in rule

2(1) of Cenvat Credit Rules, 2004.

Page 6 of 26 47/CX-I Ahmd/ADC/MKR/2014

12. Further, Rule 9(6) of the Cenvat Credit Rules, 2004 stipulates that the burden of

proof regarding admissibility of Cenvat Credit shall lie upon the manufacturer or provider

of output service taking such credit. In era of self-assessment, the onus of taking

legitimate cenvat credit had been passed on to the assessee in terms of the said rules.

In other words, it was the responsibility of the assessee to take cenvat credit only if the

same was admissible. In the instant case the credit taken in respect of services availed

beyond the factory gate appeared to be inadmissible in as much as the same did not fall

within the ambit of the definition of 'input services' as specified under Rule 2(1) of the

Cenvat Credit Rules, 2004. Thus it appeared that the said assessee knew that the

services in respect of which they had taken cenvat credit were the services availed

beyond the factory gate and related to sales which in turn did not have any relation

whatsoever in or in relation to manufacture of goods. Further, the services provided by

commission agent had been held to be concerned with sales and not for sales

promotion by the Hon'ble High Court of Gujarat in the case of Commissioner of Central

Excise, Ahmedabad-II vs. M/s. Cadila Healthcare Limited, supra. Also, Rule 2(1) of

Cenvat Credit Rules, 2004 defining what constitutes an input service, did not include

services related with sales in the definition of 'input services'.

13. Further, the said assessee, in era of self assessment when onus of taking

legitimate Cenvat credit had been passed on to the assessee, took Cenvat credit in

violation of Cenvat Credit Rules. It appeared that the said assessee had taken the

cenvat credit on the services which did not qualify as 'input services' despite knowing

that the same had been availed beyond the factory gate and had not been used in or in

relation to the manufacture of final product and as such would not fall within the ambit of

the definition of 'input service'. The said assessee, though, it had been expressly

provided in Rule 9(6) of Cenvat Credit Rules, 2004 that "... burden of proof regarding

the admissibility of the Cenvat credit shall lie upon the manufacturer..." took credit of

service tax paid on commission paid to local/foreign sale commission agent which did

not qualify to be included as "input service" defined under Rule 2(1) of Cenvat Credit

Rules, 2004. Further, the assessee deliberately delayed to furnish the details and

required documents in respect of credit taken of Service tax on commission paid to

foreign/local agent, which caused substantial delay in issuance of show cause notice in

the matter. The said act on the part of assessee was deliberate to avoid giving complete

details as called for by the department, which can be clearly construed as suppression

of facts on their part. Therefore, it appeared that there was wilful mistatement and

supression of facts on the part of the assessee, as they failed to furnished the details in

time inspite of various reminders and summons. They have furnished the

details/documents only on 10.03.2014. Thus, it appears that the said assessee have

contravened the provisions of the Cenvat Credit Rules, 2004 by suppressing the facts

with intent to evade payment of duty in as much as (i) the assessee had taken the

Cenvat Credit on the service despite knowing that the same did not qualify as 'input

services' (ii) the service had not been used in or in relation to the manufacture of final

Page 7 of 26 47/CX-I Ahmd/ADC/MKR/2014

products and services were related to sales and not sales promotion and as such would

not fall within the ambit of the definition of 'input service' (iii) by failing to discharge the

obligation cast on them under Rule 9(6) of the Cenvat Credit Rules, 2004 and (iv) by not

informing the department about the availment of credit of services tax paid on

commission paid to local/foreign sale agent. Therefore, the said Cenvat Credit

amounting to Rs.10,32,149/- appeared to have been wrongly taken and utilized for the

payment of duties of excise (v) The assessee also availed excess cenvat credit on

excess payment of Service Tax which they were not entitled for the suo moto cenvat

credit of such excess payment which resulted in revenue loss to the Government during

the period from April 2009 to September 2013. Thus, the said wrongly availed Cenvat

credit was required to be recovered from them by invoking provisions of extended

period of five years contained in section 11A(5) of the Central Excise Act,1944

(erstwhile Section 11A(1) of the Central Excise Act,1944 for the period covered upto

07.04.2011 )

14. Rule 14 of the Cenvat Credit Rules, 2004 provides that where the CENVAT credit

has been taken or utilized wrongly or has been erroneously refunded, the same along

with interest shall be recovered from the manufacturer. In the instant case, the said

assessee appeared to have taken and utilised cenvat credit of service tax paid on

commission paid to local/foreign sales agents during the period from April, 2009 to

September-2013. It also appeared that the said assessee had contravened the

provisions of Rule 2 of Cenvat Credit Rules, 2004 read with Rule 3 of Cenvat Credit

Rules, 2004 for credit taken of service tax paid on commission paid to local/foreign

sales agents. The said assessee had taken and utilised an amount of Rs.10,32,149/-

during the said period. Out of the total amount of Rs.10,32,149/-, the assessee was

required to pay the amount of Rs.8,68,7991- ( inclusive of Cenvat credit of excess

payment of Rs. 47,983/-) under Rule 14 of Cenvat Credit Rules, 2004 read with

provisions of erstwhile Sections 11A(1) of the Central Excise Act,1944 being the

relevant provision of the law for the period upto 07.04.2011. The remaining amount of

Rs.1,63,350/- (inclusive of Cenvat credit of excess payment of Rs. 50,178/-) was

required to be recovered under Rule 14 of Cenvat Credit Rules,2004 read with

Section11A(5) of the Central Excise Act,1944 being the relevant provision of the law for

the period from 08.04.2011. Rule 14 of the Cenvat Credit Rules, 2004 read with

provision under Section 11M of the Central Excise Act,1944 (erstwhile Section11AB of

the Central Excise Act,1944 for the relevant period) shall apply mutatis mutandis for

effecting recovery of interest.

15. In view of the above, it appeared that the said assessee had contravened the

provisions of Rule 2(I) read with Rule 3 of the Cenvat Credit Rules, 2004 in as much as

they had taken credit of Service Tax paid on services which did not qualify as 'input

services'; Rule 9(6) of the Cenvat Credit Rules, 2004 in as much as they had failed to

discharge the burden of proof regarding admissibility of Cenvat Credit. They had also

Page 8 of 26 47/CX-I Ahmd/ADC/MKR/2014

taken suo-moto Cenvat credit of excess payment made by them instead of claiming

refund of the same. Further, it appeared that the said assessee had suppressed the

material facts regarding taking of Cenvat Credit of duty paid on services not covered

under the definition of input services, by way of not indicating the same in their

monthly/quarterly returns or in any other manner and also by deliberately delaying to

furnish the requisite details/documents to the department. Therefore, the said assessee

had rendered themselves liable for penalty in terms of Rule 15(3) of the Cenvat Credit

Rules, 2004 [Applicable during the relevant period i.e. upto 26.02.2010)] and Rule 15(2)

of the Cenvat Credit Rules, 2004 [Applicable during the relevant period .i.e. 27.02.2010

to 07.04.2011] read with Section 11AC of Central Excise Act, 1944 and & Rule 15(2) of

the Cenvat Credit Rules, 2004 [Applicable during the relevant period from 08.04.2011

read with Section 11AC(1)(b) of Central Excise Act, 1944 for the above said

contraventions. They are also liable to penalty under Rule 15A of CCR, 2004, for their

act of suo moto Cenvat credit of excess payment made by them as discussed above.

16. A Show Cause Notice dated 06.05.2014 was, therefore, issued by the Additional

Commissioner of Central Excise, Ahmedabad-I, from F.No.V.84/15-20/PPI Pumps/ADC/

O&A/ 2014 to M/s PPI Pumps Pvt. Ltd., Ahmedabad, calling them to show cause as to why:-

(i) Cenvat credit of Rs.8,68,799/- (inclusive of Cenvat credit of excess payment of

Rs. 47,983/-) for the period from April 2009 to 07.04.2011 (inclusive of Education Cess

and Higher Education Cess) wrongly availed by them as Cenvat Credit of Service Tax

paid on commission paid to foreign/local agent should not be disallowed and recovered

from them under Rule 14 of Cenvat Credit Rules,2004 read with Section 11A(1) of

Central Excise Act,1944.

(ii) Cenvat credit of Rs.1,63,350/- ( inclusive of Cenvat credit of excess payment of

Rs. 50,178/-) for the period from 08.04.2011 to September-2013 (inclusive of Education Cess and Higher Education Cess) wrongly availed by them as Cenvat Credit of

Service Tax paid on commission paid to foreign/local agent should not be disallowed

and recovered from them under Rule 14 of Cenvat Credit Rules,2004 read with

Section 11A(5) of Central Excise Act,1944.

(iii) Interest should not be charged & recovered from them for wrong availment of

Cenvat Credit under Rule 14 of Cenvat Credit Rules, 2004 read with erstwhile Section

11AB for the relevant period and now Section 11AA of Central Excise Act, 1944 as

applicable during the relevant period.

(iv) Penalty should not be imposed upon them under Rule 15(3) of the Cenvat Credit

Rules, 2004 [Applicable during the relevant period i.e. upto 26.02.2010] & Rule 15(2) of

the Cenvat Credit Rules, 2004 [Applicable during the relevant period .i.e. 27.02.2010 to

07.04.2011] read with Section 11AC of Central Excise Act, 1944 & Rule 15(2) of the

Page 9 of 26 47/CX-I Ahmd/ADC/MKR/2014

Cenvat Credit Rules, 2004 [Applicable during the relevant period from 08.04.2011 read

with Section 11AC (1)(b) of Central Excise Act, 1944.

(v) Why penalty should not be upon them imposed under Rule 15A of Cenvat Credit

Rules, 2004 for availing suo moto Cenvat Credit of Rs.98,161/- on the excess payment

made by them .

DEFENCE SUBMISSION:-

17.1. The assessee, in their defence reply dated Nil, maintained that the CENVAT

credit taken on service tax paid on commission paid to foreign agent/local agent under

Business Auxiliary Service, was input service. They reproduced Rule 2(1) of the

CENVAT Credit Rules, 2004 for "input service" and submitted that for the purpose of

selling their goods in foreign market, they were availing services of foreign sales agent;

that before manufacturing final product, order was placed by local/foreign agents and

then goods were being manufactured and exported and thus the services were availed

prior to removal of goods.

17.2 They submitted that the adjudicating authority erred in distinguishing the

judgment of Ho'ble High Court of Gujarat in case of CCE, Ahmedabad-II Vs. M/s.Cadila

Health Care Ltd. (2013-TIOL-12-HC-AHM-ST) and wrongly concluded that sales

commission agent does not appear to fall under category of sales promotion; that the

foreign agent becomes link between purchaser and seller and the service of the

local/foreign agent is used for promotion or marketing of export of goods produced by

the manufacturer; that such activity is related to the business of the assessee and is

taxable under business auxiliary services as per provision of Section 65(19) of the

Finance Act, 1994.

17.3. They stated that according to Rule 3, Rule 3(ix) & (ixa) of CENVAT Credit Rules,

2004 a manufacturer or producer of final products or a provider of taxable service shall

be allowed to take credit paid on any input service received by the manufacturer of final

product or by the provider of output services on or after 10th day of September, 2004;

that CBEC Circular No. 943/04/2011-CX dated 19.04.2011, clarified that "The definition

of input services allows all credit on services used for clearance of final products up to

the place of removal. Moreover activity of sale promotion is specifically allowed and on

many occasions the remuneration for same is linked to actual sale. Reading the

provisions harmoniously it is clarified that credit is admissible on the services of sales of

the dutiable goods on commission basis."

17.4. They relied upon the following judgments, whereby, it was judicially held that

service tax paid on commission paid to foreign/local agents falls under definition of input

service and CENVAT credit thereof is admissible:

• Honorable CESTAT, New Delhi in case of CCE, Ludhiana Vs Forgings &

Chemicals Industries 2014(34) S.T.R 238 (Tri.-Del.).

Page 10 of 26 47/CX-I Ahmd/ADC/MKR/2014

• Honorable CESTAT, Bangalore in case of Lanco Industries Ltd Vs CCE,

Tirupathi 2009-TIOL-1209-CESTAT-BANG.

• Honorable High court of Punjab and Haryana in case of CCE, Ludhiana vs

Ambika Overseas, 2011-TIOL-951-HC-P&H-ST.

17.5. They submitted that they had availed of services of commission agents for sale

of final products; that the commission agents found buyers for the goods of assessee

and thereby, promoted the sale of goods of the assessee; that service of commission

agents was covered by the definition of input service; that the service tax paid to

commission agent for sale of final goods should fall within the ambit of Business

Auxiliary Service and therefore, fall within the purview of input service.

18.1. As regard the provision of extended period of five years they submitted that the

provision of Section 11A is not applicable in absence of permissible ground of willful

suppression or mis-statement of facts. In support of their view, they relied upon the

judgment of the Honourable Supreme Court of India in case of Continental Foundation

Jt. Venture Vs CCE, Chandigarh-I 2007 (216) E.L.T. 177 (S.C.), wherein it was held

that;

• "Suppression" used in the proviso to section 11A of the Central Excise Act, 1944

accompanied by very strong words as "fraud" or "collusion" and, therefore, has to

be constructed strictly.

• Mere omission to give correct information is not suppression of facts unless it

was deliberate to stop the payment of duty.

• Suppression means failure to disclose full information with intent to evade

payment of duty when the facts are known to both the parties, omission by one

party to do what he might have been done would not rendered it suppression.

When the Revenue invokes the extended period of limitation under section 11A

the burden is cast upon it to prove suppression of facts.

• As far as mis-statement or suppression of facts are concerned, they are clearly

qualified by the word "willful", preceding the words "mis-statement or suppression

of the facts" which means with intent to evade duty. The next set of words

"contravention of any of the provisions of this Act or Rules" are again qualified by

the immediately following words with intent to evade payment of duty".

18.2. They further submitted that the adjudicating authority had invoked Rule 2(I), Rule

3(1) and rule 9(6) of CCR, 2004 for wrongly taken Cenvat credit; that the adjudicating

authority had not justified the suppression or misstatement for invoking provisions of

extended period of 5 years for recovery thereof; that CENVAT credit had not been taken

by the reasons of fraud, collusion, any willful mis statement, and suppression of facts or

contravention of any of the provisions of this Act or of the rules made there under with

intent to evade payment of duty; that the adjudicating authority invoked provision of

Page 11 of 26 47/CX-I Ahmd/ADC/MKR/2014

extended period of five years and issued SCN on 06.05.2014 regarding wrongly availing

and utilizing CENVAT credit of Rs.10,32,149/- for the period from April, 2009 to

September, 2013; that the issue of SCN covering this period was not correct and not

legal as per provisions of Central Excise Act, 1944.

19.1. They quoted the provisions of Rule 14 of CENVAT Credit Rules, 2004 and

provisions of Sub section (1) to (5) of Section 11A of Central Excise Act, 1944 and

further submitted that the Show cause notice was not legal according to provisions of

the Central Excise Act, 1944.

19.2. They submitted that in show cause notice, adjudicating authority disallowed

CENVAT credit of Rs.10,32,149/- in terms of provisions of Rule 14 CENVAT Credit

Rules, 2004 read with Section 11A (1) and 11A(5) of Central Excise Act, 1944.

19.3. They submitted that Section 11A provides that where any duty of excise has not

been levied or paid or has been short-levied or short-paid for any reason recovery

action is to be taken; the Central Excise Officer shall issue notice within period of

one/five years depending on circumstances mentioned in this section; that there is no

provision in Section 11A to issue notice where credit of any duty of excise is taken

wrongly; that the adjudicating authority had issued notice under provision of Section

11A for recovery of CENVAT credit taken by the noticee, levy of interest and penalty

which is not legal according to the provisions of the Central Excise Act, 1944.

20.1. They further submitted that it was judicially held that departmental circulars are

binding on the Departmental officers and that Department cannot say that it is not

binding on them. They relied upon the following judgments :

• CCE and CE Vs Swati Chemicals Industries Ltd (2013) 294 ELT 208 (Gujarat)

• Madura Coats Ltd. Vs Assistant CCE Madurai-I, (2013)291 ELT 172 (Madras)

• Smartchem Technologies Ltd. Vs Union of India (2011) 272 ELT 522 (Gujarat)

• CCE, Nagpur Vs Ultratech Cement Ltd. (2010) 20 STR 577 (Bombay)

In above various judgments it was held as under:

a) Circular issued by the CBEC is binding on the Revenue.

b) It is not opened for the Revenue to agitate the issue before Court in contradiction of

the circular issued by the Department.

c) Revenue officers cannot take a stand contrarily to CBEC circular despite decision of

Tribunal being contrarily viewed.

d) Revenue cannot argue against stand taken by CBEC in departmental circular.

20.2. The adjudicating authority issued SCN for reversal of CENVAT credit taken on

service tax paid on commission paid to foreign agent under business auxiliary service

under provision of section 66(A) of Finance Act, 1994 and notification 30/2012-ST dated

Page 12 of 26 47/CX-I Ahmd/ADC/MKR/2014

20.06.2012; that the CBEC circular dated 29.04.2011 clearly mentions that credit is

admissible on the services of sales of the dutiable goods on commission basis. The 7

adjudicating authority was bound to follow Departmental circular and therefore,

issuance of SCN was in contravention of provision of circular and was not correct.

21.1. They quoted provisions of Rule 15 of CCR, 2004 and submitted that penalty

under Rule 15(2) and (3) of CENVAT Credit Rules, 2004 is not imposable:

21.2. They submitted that the assessee is not liable to pay penalty under Section

15(2) and (3) of CENVAT Credit Rules, 2004 in view of the following facts.

• CENVAT credit has not been taken by the reasons of fraud, collusion, any willful

misstatement, and suppression of facts or contravention of any of the provisions

of this Act or of the rules made there under with intent to evade payment of duty.

• The assessee is a manufacturer and filing monthly ER-I returns to the range

office and indicating there in availment and utilization of CENVAT credit.

• Government of India, Ministry of Finance, Department of Revenue, Tax Research

Unit Circular no. 943/04/2011/CX dated 29.04.2011 clarified that credit is

admissible on the services of sales of the dutiable goods on commission basis

and therefore his bonafide intention of CENVAT credit taken and utilized.

• During relevant period there were decisions of various CESTAT and Honorable

High Court of Punjab and Haryana that service tax paid on commission to the

commission agent is eligible for availment of CENVAT credit.

• Taking of CENVAT credit of service tax paid to the commission agent was out of

bonafide belief as to eligibility to CENVAT credit as it is in relation to business of

manufacturing and selling.

21.3. They further stated that as per the facts mentioned above, it proved that the

assessee had not taken credit with malafide intention and suppressing facts. Therefore,

levy of penalty under Rule 15(2) and (3) of CENVAT Credit Rules, 2004 was not legal

and required to be dropped.

21.4. They, quoting provisions of Rule 14 ibid, further submitted that there should be

no levy of interest. They submitted that they had not taken CENVAT credit wrongly but

taken according to prevailing provisions of CENVAT Credit Rules, 2004 and various

judicial pronouncements of CESTAT and High Court with bonafide intention. Therefore,

interest under Rule 14 could not be levied and recovered.

21.5 They quoted Rule 15A of Cenvat Credit Rules, 2004 and submitted that they

had paid excess service tax of Rs.98,161/- in respect of commission paid to foreign

agent under business auxiliary service under reverse charge mechanism and therefore,

they took Cenvat credit of Rs.98,161/-; that penalty under Rule 15A of Cenvat credit

Rules, 2004 is not leviable.

Page 13 of 26 47/CX-1 Ahmd/ADC/MKR/2014

PERSONAL HEARING:-

22 The personal hearing in the matter was held on 28/8/2014 and Shri Bishan Shah,

CA appeared for the same and requested for adjournment for one month for detail study

and collection of supportive documents and his request was considered Accordingly,

another personal hearing was held on 11/11/2014 and Shri Bishan Shah, CA appeared

for the same and reiterated their defense reply.

DISCUSSION AND FINDINGS :-

23. I have carefully gone through the case records as well as the written and oral

submissions made by the assessee in their defence. From the case records, I find that

the issue on hand is, to decide the admissibility of Cenvat credit availed by the said

assessee (i) on service tax paid on commission paid to their local/foreign agents for sale

of their finished goods and (ii) on excess Service tax paid by them in respect of

Commission paid to foreign agent under business auxiliary service

24. With regard to the first issue, I find that as per the details called for from the said

assessee, it was observed that the said assessee had availed Cenvat credit of service

tax paid on commission paid to their sales commission agent to the tune of

Rs.10,32,149/- during the period from April, 2009 to September, 2013. The said Cenvat

credit is denied mainly on the ground that the service provided by their commission

agent does not fall within the ambit of definition of "input service" as provided under

Rule 2(1) of the Cenvat Credit Rules, 2004 ( here-in-after referred to as CCR, 2004). As

such the said assessee is not entitled to the Cenvat credit of service tax paid on such

service provided by the commission agent for sale of their finished goods.

25. At the outset, I would like to examine the definition of "input service" as defined

under Rule 2(I) of CCR, 2004, which reads as under:

"input service" means any service,-

used by a provider of taxable service for providing an output service; or

(ii) used by the manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products upto the place of removal,

and includes services used in relation to setting up, modernization, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion market research, storage up to the place of removal, procurement of inputs, activities relating to business, such as accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, and security, inward transportation of inputs or capital goods and outward transportation up to the place of removal;

26.1 In the instant case, I find that the assessee had taken Cenvat Credit of Service

Tax paid by them on commission paid to Sales Agents. I find that services of Sales

Commission Agent used by the assessee are used neither directly nor indirectly, in or in

relation to the manufacture of their final products. Therefore, the said assessee has

wrongly availed Cenvat credit of Service Tax paid on commission paid to such

Page 14 of 26 47/CX-I Ahmd/ADC/MKR/2014

commission agent and this service does not fall within the purview of definition of input

service. The said service had been availed by the said assessee after the clearance of

finished goods from their factory gate i.e. beyond the place of removal. Since, the

services of Sales Commission agent have no relation with the manufacturing activity

and also do not appear to fall within the ambit of definition of input services as defined

under Rule 2(1) of Cenvat Credit Rules, 2004, the manufacturer shall not be allowed to

take credit on such ineligible services as per Rule 3 of Cenvat Credit Rules, 2004.

26.2. Further, services of the sales commission agent also do not fall under the

category of sales promotion. As per the definition of commission agent defined under

clause (a) to the Explanation under section 65(19) of the Finance Act 1994, a

commission agent is a person who acts on behalf of another person and causes sale or

purchase of goods. In other words, the commission agent appears to be directly

responsible for selling or purchasing on behalf of another person and that such activity

cannot be considered as sales promotion. There has to be a clear distinction between

sales promotion and sale. A commission agent is directly concerned with sales rather

than sales promotion. Therefore, the services provided by commission agent does not

fall within the purview of the main or inclusive part of the definition of 'input service' as

laid down in rule 2(I) of the Cenvat Credit Rules, 2004 and the said assessee is not

eligible for CENVAT credit in respect of the service tax paid on commission given to

Commission Agents.

26.3. I also find that Hon'ble High Court of Gujarat in case of Commissioner of Central

Excise, Ahmedabad-II V/s. M/s. Cadila Health Care Ltd., 2013 —TIOL-12-HC-AHM-ST,

while dealing with the issue of admissibility of service tax paid on commission paid to

overseas agents as Cenvat credit has observed as under:

(vi) As noted hereinabove, according to the assessee the services of a commission

agent would fall within the ambit of sales promotion as envisaged in clause (i) of

section 65(19) of the Finance Act, 1994, whereas according to the appellant a

commission agent is a person who is directly concerned with the sale or purchase of

goods and is not connected with the sales promotion thereof. Under the circumstances,

the question that arises for consideration is as to whether services rendered by a

commission agent can be said fall within the ambit of expression 'sales promotion'. It

would, therefore, be necessary to understand the meaning of the expression sales

promotion.

(vii) The expression 'sales promotion' has been defined in the Oxford Dictionary of

Business to mean an activity designed to boost the sales of a product or service. It may

include an advertising campaign, increased PR activity, a free-sample campaign,

offering free gifts or trading stamps, arranging demonstrations or exhibitions, setting up

competitions with attractive prizes, temporary price reductions, door-to-door calling,

telephone selling, personal letters etc. In the Oxford Dictionary of Business English,

sales promotion has been defined as a group of activities that are intended to improve

sales, sometimes including advertising, organizing competitions, providing free gifts

Page 15 of 26 47/CX-I Ahmd/ADC/MKR/2014

and samples. These promotions may form part of a wider sales campaign. Sales

promotion has also been defined as stimulation of sales achieved through contests,

demonstrations, discounts, exhibitions or tradeshows, games, giveaways, point-of-sale

displays and merchandising, special offers, and similar activities. The Advanced Law

Lexicon by P. Ramanatha Aiyar, third edition, describes the term sales promotion as

use of incentives to get people to buy a product or a sales drive. In the case of

Commissioner of Income-tax v. Mohd. Ishaque Gulam, 232 ITR 869, a Division

Bench of the Madhya Pradesh High Court drew a distinction between the expenditure

made for sales promotion and commission paid to agents. It was held that commission

paid to the agents cannot be termed as expenditure on sales promotion.

(viii) From the definition of sales promotion, it is apparent that in case of sales

promotion a large population of consumers is targeted. Such activities relate to

promotion of sales in general to the consumers at large and are more in the nature of

the activities referred to in the preceding paragraph. Commission agent has been

defined under the explanation to business auxiliary service and insofar as the same is

relevant for the present purpose means any person who acts on behalf of another

person and causes sale or purchase of goods, or provision or receipt of services, for a

consideration. Thus, the commission agent merely acts as an agent of the principal for

sale of goods and such sales are directly made by the commission agent to the

consumer. In the present case it is the case of the assessee that service tax had been

paid on commission paid to the commission agent for sale of final product. However,

there is nothing to indicate that such commission agents were actually involved in any

sales promotion activities as envisaged under the said expression. The term input

service as defined in the rules means any service used by a provider of taxable service

for providing an output service or used by the manufacturer whether directly or

indirectly, in or in relation to the manufacture of final products and clearance of final

products from the place of removal and includes services used in relation to various

activities of the description provided therein including advertisement or sales

promotion. Thus, the portion of the definition of input service insofar as the same is

relevant for the present purpose refers to any service used by the manufacturer directly

or indirectly in relation to the manufacture of final products and clearance of final

products from the place of removal. Obviously, commission paid to the various agents

would not be covered in this expression since it cannot be stated to be a service used

directly or indirectly in or in relation to the manufacture of final products or clearance of

final products from the place of removal. The includes portion of the definition refers to

advertisement or sales promotion. It was in this background that this court has

examined whether the services of foreign agent availed by the assessee can be stated

to services used as sales promotion. In the absence of any material on record as

noted above to indicate that such commission agents were involved in the activity of

sales promotion as explained in the earlier portion of the judgement, in the opinion of

this court, the claim of the assessee was rightly rejected by the Tribunal. Under the

circumstances, the adjudicating authority was justified in holding that the commission

agent is directly concerned with the sales rather than sales promotion and as such the

services provided by such commission agent would not fall within the purview of the

Page 16 of 26 47/CX4 Ahmd/ADC/MKR/2014

main or inclusive part of the definition of input service as laid down in rule 20) of the

Rules.

(ix) As regards the contention that in any event the service rendered by a commission

agent is a service received in relation to the assessees activity relating to business, it

may be noted that the includes part of the definition of input service includes activities

relating to the business, such as accounting, auditing, financing, recruitment and

quality control, coaching and training, computer networking, credit rating, share

registry, and security. The words activities relating to business are followed by the

words such as. Therefore, the words such as must be given some meaning. In Royal

Hatcheries (P) Ltd. v. State of A.P., 1994 Supp (1) SCC 429, the Supreme Court held

that the words such as indicate that what are mentioned thereafter are only illustrative

and not exhaustive. Thus, the activities that follow the words such as are illustrative of

the activities relating to business which are included in the definition of input service

and are not exhaustive. Therefore, activities relating to business could also be other

than the activities mentioned in the sub-rule. However, that does not mean that every

activity related to the business of the assessee would fall within the inclusive part of the

definition. For an activity related to the business, it has to be an activity which is

analogous to the activities mentioned after the words such as. What follows the words

such as is accounting, auditing, financing, recruitment and quality control, coaching and

training, computer networking, credit rating, share registry, and security. Thus, what is

required to be examined is as to whether the service rendered by commission agents

can be said to be an activity which is analogous to any of the said activities. The

activity of commission agent, therefore, should bear some similarity to the illustrative

activities. In the opinion of this court, none of the illustrative activities, viz., accounting,

auditing, financing, recruitment and quality control, coaching and training, computer

networking, credit rating, share registry, and security is in any manner similar to the

services rendered by commission agents nor are the same in any manner related to

such services. Under the circumstances, though the business activities mentioned in

the definition are not exhaustive, the service rendered by the commission agents not

being analogous to the activities mentioned in the definition, would not fall within the

ambit of the expression activities relating to business. Consequently, CENVAT credit

would not be admissible in respect of the commission paid to foreign agents.

(x) For the reasons stated hereinabove, this court is unable to concur with the contrary

view taken by the Punjab and Haryana High Court in Commissioner of Central Excise,

Ludhiana v. Ambika Overseas (supra). Insofar as this issue is concerned, the question

is answered in favour of the revenue and against the assessee.

26.4 The Hon'ble CESTAT, Ahmedabad, in the case of Commissioner of Customs &

Central Excise, Surat-II v/s Astik Dyestuff P. Ltd. vide order

No.A/10339/VVZB/AHD/2013 dated 01.03.2013 has held that "the law laid down by

Hon'ble High Court of Gujarat in the case of Cadila Healthcare (Supra) is squarely

applicable to the facts of the present case. No distinction can be made between the

commission paid to foreign agents and the agents operating within the territory of India

because natures of services provided by both the categories of the agents are same.

Page 17 of 26 47/CX-I Ahmd/ADC/MKR/2014

Consequently, Cenvat Credit would not be admissible in respect of commission paid to

local sales (Commission) Agents".

26.5. I find that the ratio of above decisions of Hon'ble High Court and Hon'ble

CESTAT are squarely applicable in the instant case and accordingly, I tend to hold that

the said assessee is not eligible for Cenvat credit of service tax paid on commission

paid to the sales agents.

26.6. I further find that Rule 2(1)00 of Cenvat Credit Rules, 2004, defines the eligible

category of Services for availing credit. The said definition of input service fixes the

meaning of that expression and the services, used by the manufacturer, are required to

have a nexus with the manufacture of the final product and clearance of the final

product up to the place of removal. Place of removal is well defined in Section 4(3)(c)of

the Central Excise Act,1944 and the services which are enumerated in the inclusive

clause, which applies both, in the context of the provider of output services as well as

the manufacturer, cannot be read de hors the meaning of input service under Rule 2(I)

of Cenvat Credit Rules, 2004. Therefore, all the activities relating to business, which are

input services used by the manufacturer in relation to the manufacture of final product

and clearance of the final product up to the place of removal alone would be eligible.

After the final products are cleared beyond the place of removal, there will be no scope

for subsequent use of service to be treated as input services. Therefore, services

utilized beyond the stage of manufacturing and clearance of the goods from the factory

cannot be treated as input services. Thus, for the purpose of ascertaining the

admissibility of Cenvat Credit on services, the nature of service availed should be in

consonance with the above parameters. It is evident that the above services does not

have any nexus with the manufacturing activities and as such does not fall within the

ambit of definition of input service".

26.7. Further, I would also like to rely upon the decision in case of Commissioner of

C.Ex., Chennai Vs Sundaram Brake Linings - 2010 (19) S.T.R. 172 (Tri. — Chennai)

which is applicable in the present case. In the said case of Commissioner of C. Ex.,

Chennai Vs Sundaram Brake Linings, Hon'ble CESTAT, Chennai, relying on a

decision of Hon'ble Supreme Court in case of Maruti Suzuki Ltd. v. CCE, Delhi - 2009

(240) E.L.T. 641 (S.C.), held that use of the input service must be integrally connected

with the manufacture of the final product. The input service must have nexus with the

process of manufacture. It has to be necessarily established that the input service is

used in or in relation to the manufacture of the final product. One of the relevant tests

would be that, can the final product emerge without the use of the input service in

question. In the case on hand, the services of sales agents were utilized beyond the

factory gate, hence the Nexus theory and Relevance test as broadly discussed by the

Hon'ble Supreme Court in case of Maruti Suzuki (Supra) is not established.

26.8. I further find that the said assessee could not establish nexus between the

service availed by them and the manufacture of the finished excisable goods as per the

Page 18 of 26 47/CX-I Ahmd/ADC/MKR/2014

ruling in the case of Vikram Ispat Vs CCE, Raigad - 2009 (16) S.T.R. 195. It was also

held in the said case that any service to be brought within the ambit of definition of 'input

service' should be one which should satisfy the essential requirement contained in the

main part of the definition. This requirement is equally applicable to the various items

mentioned in the inclusive part of the definition as well. The Tribunal also held that no

credit can be allowed unless the assessee provides evidence to establish the nexus

between the services and the manufacture of the final products. Based on the above

decision also, I find that the services in the question are not falling within the definition

of "input service".

26.9. The Hon'ble Tribunal in the case of CCE, Nagpur Vs Manikgarh Cement

Works - 2010 (18) S.T.R. 275 has also held that to fall within the scope of definition of

input service, a service must have been used in or in relation to the manufacture or

clearance of final product, directly or indirectly. It is further held by Tribunal that the

Hon'ble Supreme Court in the case of Maruti Suzuki Ltd. Vs CCE, Delhi - 2009 (240)

E.L.T. 641 (S.C.) has overruled the decision of the Bombay High Court in the case of

Coca Cola India Pvt. Ltd. Vs CCE, Pune - 2009 (15) S.T.R. 657 (Born.) = 2009 (242)

E.L.T. 168 (Born.). The Tribunal has also held in view of the main part of definition that

the decision of the Hon'ble Supreme Court in Maruti Suzuki (supra) though rendered in

a case relating to 'inputs' is also applicable to a case of 'input service'.

26.10. I also note that in the case of Maruti Suzuki Vs Commissioner [2009 (240)

E L T 641 (S.C.)], the Hon'ble Supreme Court has laid down that the nexus has to be

established between the inputs or input service on one hand and finished goods on

other hand.

26.11 Even the larger Bench of Tribunal in the case of Vandana Global Ltd. Vs CCE,

Raigad - 2010 (253) E.L.T. 440 (Tri. -LB), has applied the decision of the Hon'ble

Supreme Court in the case of Maruti Suzuki (supra) according to which credit in respect

of input or input service is admissible only if it is integrally connected to the manufacture

of the finished excisable goods.

26.12 Thus, in view of the above judicial pronouncements including the decision of

Hon'ble High Court of Gujarat in case of M/s. Cadila Healthcare Ltd. as discussed in

foregoing paras, I hold that the assessee is not entitled to Cenvat Credit on the services

in question and the same is required to be recovered from them along with interest.

26.13 With regard to the second issue pertaining to Cenvat credit on excess payment

of Service Tax, I find that an error was noticed in the cenvat credit details submitted by

the assessee on 10.03.2014, in so far as the amount of commission paid and Service

Tax payable for the period from 08.04.2009 to 30.09.2013 (foreign Commission). The

assessee had paid excess service tax and taken excess Cenvat Credit on the said

excess payment of Service Tax. Shri Rajnikant R. Bhaysar in his further statement

recorded on 03.04.2014, has categorically admitted that they had paid excess Service

Tax on Sales Commission paid to foreign agent and had availed Cenvat credit thereof.

Page 16 of 26 47/CX4Ahmd/ADC/MKR/2014

Thus, it is evident that the said assessee had wrongly availed CENVAT Credit of service

tax amounting to Rs.10,32,149/- (for the period from April 2009 to September-2013)

paid on the sales commission paid to the local/foreign agents for the sales of their

finished goods (as detailed in Annexure 'Al' to the SCN), which is also inclusive of suo-

moto Cenvat credit wrongly taken by them of excess payment made by them as

detailed in Annexure-A2 to the SCN. They were not eligible to take Cenvat credit of

such suo moto excess payment of service tax as such excess payment of S.Tax by no

stretch of imagination can be considered as 'input service' as defined in the statute as

mentioned above and also such excess payment of S.Tax does not fall under any of the

category of admissible duties and taxes under Rule 3 of CCR, 2004 for the purpose of

availing Cenvat credit thereof.

27. Now coming to the submissions made by the said assessee in support of their

defence, I find that the said assessee has mainly given their defence on two aspects i.e.

(1) they, relying on various decisions of Tribunals and High Courts and CBEC Circular

No. 943/04/2011-CX dated 29/4/2011, has argued that service of sales commission

agents in question is covered under the definition of "input service" and the Cenvat

credit of service tax paid on commission paid to such sales agents is admissible to

them; and (2) relying on various judicial pronouncements, they have argued that

extended period cannot be invoked in this case and they are not liable for any penalty

and interest.

28. As regards their arguments with regard to admissibility of Cenvat credit in

question, I find that in terms of my above findings supported by the judicial

pronouncements on the issue as discussed in the foregoing paras, it is very much clear

that the service of sales commission agent does not fall within the ambit of the definition

of "input service" as defined in the statute as mentioned above and as such the

assessee is not entitled to the Cenvat credit of service tax paid thereon.

29.1. As regards their reliance in decisions of the (i) CESTAT, New Delhi in case of

CCE, Ludhiana Vs. Forgings & Chemicals Industries (ii) High Court of Punjab and

Haryana in CCE, Ludhiana Vs Ambika Overseas (iii) Lanco Industries Ltd. Vs.

CCE, Tirupathi etc. on the issue, I find that the Hon'ble H.C. of Gujarat in case of M/s.

Cadila Healthcare Ltd. (supra) has already ruled out that the services of sales

commission agents does not fall under the definition of 'input service" and as such

Cenvat credit is not admissible thereon. Further, I find that the Apex court in case of

U01 vs Kamlakshi Finance Corporations Ltd. (991(55) ELT 433 (SC)) has directed

department to pay utmost regard to the judicial discipline and give effect to orders of

higher appellate authorities which are binding on them. In the said judgment, the Apex

court has further directed that the order of Appellate Collector is binding on Assistant

Collectors working under his jurisdiction and the order of the Tribunal is binding upon

the Assistant Collectors and the Appellate Collectors who function under the jurisdiction

of the Tribunal. With due respect to the said decision of Hon'ble High Court of Punjab &

Haryana, I find that applying the ratio of decision of Apex court in case of Kamlakshi

Page 20 of 26 47/CX-I Ahmd/ADC/MKR/2014

Finance Corporations Ltd. (supra), the decision of Hon'ble H.C. of Gujarat in case of

M/s. Cadila Healthcare Ltd. (supra) is binding and I tend to follow the rulings of the"

Hon'ble H.C. of Gujarat in the case of M/s. Cadila Healthcare Ltd. (supra).

29.2. As regards their reliance on CBEC Circular dated 29/4/2011 pertaining to credit

of Business Auxiliary Service on account of sales commission, I find that the

admissibility of same has already been decided by Hon'ble H.C. as discussed above in

case of M/s. Cadila Healthcare Ltd. (supra). Further, Hon'ble Apex court in case of CCE,

Bolpur Vs Ratan Melting & Wire Industries (2008(231) ELT 22 (SC) has held that "when

the Supreme Court or the High Court declares the law on the question arising for

consideration, it would not be appropriate for the Court to direct that the circular should

be given effect to and not the view expressed in a decision of this Court or the High

Court".

29.3 The assessee with regard to the Cenvat credit of excess payment of service tax

by merely quoting Rule 15A of Cenvat Credit Rules, 2004, had submitted that they had

paid excess service tax of Rs.98,161/- in respect of commission paid to foreign agent

under business auxiliary service under reverse charge mechanism and therefore, they

took Cenvat credit of Rs.98,161/- and that penalty under Rule 15A of Cenvat credit

Rules, 2004 is not leviable. I am not impressed by the argument put forth by the

assessee on the issue and tend to hold that they were not eligible to Cenvat credit on

such suo moto excess payment as already discussed by me above.

29.3. In light of my exhaustive findings supported by judicial decisions as discussed in

foregoing paras, I am convinced to hold that the service of sales commission agent

does not fall within the ambit of definition of "input service" as defined under the statute

as discussed above and the said assessee was as such not entitled to Cenvat credit of

service tax paid on commission paid to such sales agents. They were also not eligible to

take Cenvat credit of suo moto excess payment of Service Tax. In view of the said facts,

I find that the assessee had contravened the provisions of Rule 2(1) read with Rule 3 of

the CENVAT Credit Rules, 2004 in as much as they had taken credit of service tax paid

on service which did not qualify as 'input service' and has also availed Cenvat credit of

suo moto excess payment of service tax. The wrongly availed Cenvat credit is thus

required to be recovered from them along with interest.

30.1 As regards invocation of extended period the assessee has argued that the

adjudicating authority has not justified how suppression or misstatement is involved with

intent to evade duty; that Cenvat credit has not been taken by the reasons of fraud,

collusion, any willful misstatement and suppression of facts and the issue of SCN

covering the extended period of five years is not correct and legal. In support of their

plea, they quote the Hon'ble Supreme Court of India in case of Continental Foundation

Jt. Venture Vs CCE, Chandigarh-I 2007 (216)ELT177(SC), wherein it was cited that

when the Revenue invokes the extended period of limitation under section 11A, the

burden is cast upon it to prove suppression of facts.

Page 21 of 26 47/CX-I Ahmd/ADC/MKR/2014

30.2 I concur with the above arguments put forth by the assessee with regard to

proposal of invoking the extended period in the impugned show cause notice so far as

first issue of wrong availment of Cenvat credit on regular service tax paid by them on

commission agents' service. It is evident that till the contradictory view was taken by

Gujarat High Court in case of M/s. Cadila Healthcare Ltd. (supra), the admissibility of

Cenvat credit on service tax paid on commission paid to such sales agents were ruled

in favour of the trade by various Tribunals and also Hon'ble Punjab and Haryana High

Court. It is also evident that CBEC in their aforesaid Circular has also clarified that the

Cenvat credit was admissible on services of commission agents. Thus, their action of

availing Cenvat credit in question at the relevant time was in accordance with such

circular and case laws. In this backdrop, I am not convinced to hold that there was any

suppression of facts or willful misstatement or ill-intention on part of the assessee and

as such none of the ingredients of section 11A of CEA'1944 enabling invocation of

extended period were present in this case. Accordingly, I hold that extended period

cannot be invoked in this case and the demand is to be limited to normal period only.

Considering the date of issue of present show cause notice on 06.05.2014 and

considering the date of filing of periodical return for the month of April'2013 on

06/05/2013 the demand can be restricted only for the period from April, 2013 till

September, 2013 instead of period from April, 2009 to September, 2013, as proposed in

the show cause notice.

30.3 However, with regard to the second issue of wrongly availing the cenvat credit of

suo moto excess payment of Service Tax, I find that the said fact was never declared by

the assessee in any manner to the department. In terms of the provisions of Rule 9(6) of

the CCR, 2004, the onus of availing legitimate Cenvat credit is on the assessee and in

this case, the assessee has failed to discharge the obligation cast upon them under

Rule 9(6) ibid. The said fact only came to the knowledge of the department while

verifying the details called for by the department and submitted by the assessee. Thus, I

find that there was suppression of facts and mis declaration on the part of the assessee

and as such the extended period can be invoked for recovery of such wrongly availed

cenvat credit on suo moto excess payment of service tax made by them. Accordingly, I

find that the said wrongly availed Cenvat credit to the tune of Rs. 98,161/- ( Rs. 47983 +

Rs. 50178) is required to be recovered from them in terms of provisions of Rule 14 of

CCR, 2004 read with erstwhile Section 110) and now Section 11A ( 5) as applicable

during the relevant period. They are also liable to pay interest in terms of provisions of

Rule 14 ibid read with erstwhile Section 11AB and now Section 11AA as applicable

during the relevant period.

31.1. As regards the assessee's contention that the Show Cause Notice is not legal

according to provision of the Central Excise Act, 1944 I find that there is a mis-

interpretation of Rule 14 of CCR, 2004 and the provisions of Section 11A of Central

Excise Act, 1944 on part of the assessee. The assessee submits that the adjudicating

authority mentioned in show cause notice that 'where the Cenvat credit has been taken

Page 22 of 26 47/CX-I Ahmd/ADC/MKR/2014

or utilized wrongly, the same along with interest shall be recovered from the

manufacturer and the provisions of sections 11A and 11AB of the Excise Act shall apply

mutatis mutandis for effecting such recoveries'. In this regard, I refer Rule 14 of Cenvat

Credit Rules, 2004 which reads as under:

Where the CENVAT credit has been taken or utilized wrongly or has been erroneously

refunded, the same along with interest shall be recovered from the manufacturer or the provider

of the output service and the provisions of sections 11A and 11AB of the Excise Act or sections

73 and 75 of the Finance Act, shall apply mutatis mutandis for effecting such recoveries.

31.2. I do not agree with the assessee's views, as a simple reading of the said rule

clearly provides that wrongly taken or utilized or erroneously refunded Cenvat credit

along with interest, shall be recovered from the manufacturer or the provider of output

service and the provisions of section 11A and 11AA (erstwhile Section 11AB) of the

CEA, 1944 shall apply mutatis mutandis for effecting such recoveries. Thus, the wrongly

availed Cenvat credit is required to be recovered from said assessee along with interest

in terms of provisions of Rule 14 of CCR read with Section 11A and Section 11AA ibid.

32. Regarding proposal of imposition of penalty under Rule 15(2) and (3) of Cenvat

Credit Rules, 2004 read with Section 11 AC of the Central Excise Act, I find that once

the charges of suppression of facts does not prove with regard to first issue on hand,

the penal provisions under said Rule 15(2) read with Section 11AC ibid cannot be

invoked in this case However, the said assessee has contravened the provisions of

CCR, 2004 as discussed above and thereby they are liable to penal action under Rule

15(1) of CCR, 2004. In this connection, I find that the case of Goodyear India Ltd. Vs

Commissioner Of Central Excise, New Delhi - 2002 (149) E.L.T. 618 (Tri. - Del.),