of Financial audit and compliance audit

75

AUDIT REPORT AUDIT OF THE PROPOSED LAW ON THE FINAL STATEMENT OF ACCOUNTS OF THE STATE BUDGET OF MONTENEGRO FOR 2013 Type of audit: Financial audit and compliance audit Audited entity: Government of Montenegro ‐ Ministry of Finance Subject of audit: Proposal Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013 Audit duration: 140 audit days Auditing Board members: Mr Milan Dabović, PhD, President of Senate ‐ Head of Auditing Board Mr Dragiša Pešić, Member of Senate – Member of Auditing Board

Transcript of of Financial audit and compliance audit

AUDIT REPORT

AUDIT OF THE PROPOSED LAW ON THE FINAL STATEMENT OF ACCOUNTS OF THE STATE BUDGET OF MONTENEGRO FOR 2013

Type of audit: Financial audit and compliance audit Audited entity: Government of Montenegro ‐ Ministry of Finance Subject of audit: Proposal Law on the Final Statement of Accounts of the State Budget of

Montenegro for 2013 Audit duration: 140 audit days

Auditing Board members:

Mr Milan Dabović, PhD, President of Senate ‐ Head of Auditing Board Mr Dragiša Pešić, Member of Senate – Member of Auditing Board

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

3

On the basis of Article 9 of the Law on State Audit Institution and the Decision of the Auditing Board responsible for the audit and composed of Mr Milan Dabović PhD, Head of the Auditing Board and Mr Dragiša Pešić, member of the Auditing Board, the State Audit Institution conducted the financial audit of the Proposal Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013. The audit covered the legal part and the explanation, Report on Consolidated Public Spending for 2013, Report on Cash Flow for 2013 prepared according to the economic classification, Report on Cash Flow for 2013 prepared according to the functional classification, Report on Arrears as of 31 December 2013, a summary overview of the key accountancy policies and other explanatory information, as well as the audit of compliance of the activities and financial transactions with the laws and secondary legislation. Responsibility of the Management for the Financial Reports According to Article 39 of the Law on the Budget and Fiscal Responsibility1, Minister of Finance is responsible for the execution of the state budget, as well as for the preparation and presentation of financial statements in line with the Rulebook on the Manner of Drafting, Compiling and Filing Financial Statements of the Budget, State Funds and Local Self‐Government Units2. According to Article 40 paragraph 4 of the Law on the Budget and Fiscal Responsibility, it is the budget executor in the spending unit that is responsible for legality in the use of the funds allocated to that spending unit. This responsibility includes designing, implementing and ensuring internal controls relevant for the preparation and presentation of the financial statements without materially wrong presentations caused by fraud or by error. The Government of Montenegro and the responsible persons in the spending units are responsible for ensuring compliance of all activities, financial transactions and information entered into the financial statements with the relevant legislation. Responsibility of the State Audit Institution The responsibility of the State Audit Institution is to express its opinion about the Proposal Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013 on the basis of the audit it performs and to express its opinion on whether, in their material aspects, the activities, financial transactions and information given in the financial statements are in compliance with the current applicable legislation. The audit was performed according to Articles 4 and 9 of the Law on State Audit Institution3, relevant International Standards of Supreme Audit Institutions (ISSAI) and the Annual Audit Plan of the State Audit Institution for 2014 No. 4011‐06‐1540 of 27 December 2013. Adhering to the International Standards of Supreme Audit Institutions (ISSAI) the State Audit Institution complied with the requirements of ethics. It planned and performed the audits in the way that provided reasonable assurances that in the report there are no materially wrong presentations of data. The audit included the procedures for obtaining audit evidence about the amounts disclosed in the financial statements, including the assessment of the risk of materially wrong presentation caused by frauds or errors. The risk assessment dealt with internal controls relevant for the development and fair presentation of the financial statements, with a view to designing the audit procedures that are appropriate in given circumstances, but not with a view to expressing opinion about the effectiveness of the internal controls. The audit included the assessment of the applied accountancy procedures and the assessment of the general presentation of financial statements. We are of the opinion that the audit evidence secured in the audit process on the selected sample of 60.10% i.e. on the amount of 963,652,728.45€, are sufficient and appropriate to provide a basis for the expressed audit opinion.

1 OGM 20/14 as of 25 April 2014

2 OGM 23/14

3 OGM 28/04, 27/06, 78/06, 17/7, 73/10 and 40/11

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

4

Financial audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013, the end of which is on 31 December 2013, established that the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013 was in all material aspects prepared in compliance with the Law on Budget and the Rulebook on the Rulebook on the Manner of Drafting, Compiling and Filing Financial Statements of the Budget, State Funds and Local Self‐Government Units and that it does not contain materially significant errors in the presentation of the results (deficit). Accordingly, the Auditing Board expresses its unqualified opinion with emphasis on the matter. The following matter is hereby emphasized:

1. The funds in the amount of 7,198,449.13 were allocated to the Radio and Television of Montenegro through a direct payment from the Central Account of the State Treasury and there were no records of this amount on the side of the revenues and expenditures in the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013.

We recommend that the Government of Montenegro and the Ministry of Finance consider the option of planning the funds for the Radio and Television of Montenegro through the annual law on budget as a transfer to institutions, individuals, non‐governmental and public sector; that they realize the planned funds through the General Ledger of the State Treasury and that they report about this spending within the Law on the Final Statement of Accounts of the State Budget of Montenegro.

2. The Ministry of Finance did not ensure full records of the balance and turnover of financial

assets through the system of the General Ledger of the State Treasury (class 1). Therefore, we particularly indicate to the fact that it is necessary to record the balance and the turnover of the monetary transactions that are done through the accounts in the system of the Consolidated Account of the State Treasury according to Article 6 of the Regulation on Uniform Classification of Accounts for the Budget, Extra‐budgetary Funds and Budgets of Municipalities.

It is recommended that the Ministry of Finance ensures the records of the balance and turnover of the monetary transactions that are done through the accounts in the system of the Consolidated Account of the State Treasury according to Article 6 of the Regulation on Uniform Classification of Accounts for the Budget, Extra‐budgetary Funds and Budgets of Municipalities.

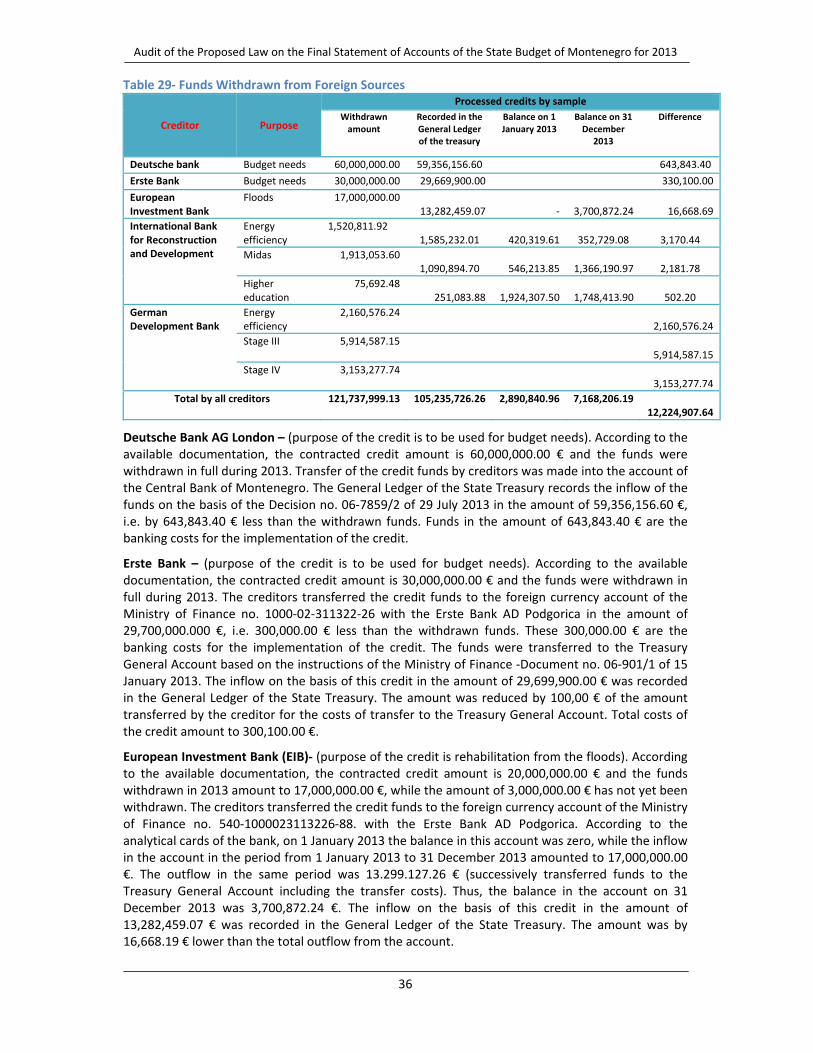

3. General Ledger of the State Treasury records the inflow of the funds on the basis of loans and credits from national sources in the amount of 115,000,000.00 €, while the emissions of Treasury bills amount to 29,850,142.00 €. The funds in the amount of 159,858,658.00 €, that are related to the inflow and payment of the Treasury bills were not recorded in the General Ledger of the State Treasury and neither were the costs of the banking services for the transactions of finances based on borrowings abroad in the amount of 996,466.51 €.

We recommend to the Ministry of Finance to record in the General Ledger of the State Treasury the expenditures based on the banking services, as well as the emission and repayment of the securities in gross amount. This should be done using the Ministry's decisions since in such a way additional costs can be avoided. The Compliance Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013 established that the spending units, users of the budget funds have not put their business activities in all their aspects in compliance with the legislation that governs budget operations in Montenegro. Therefore, the relevant auditing board expresses its qualified opinion. Basis for expressing the opinion lies in the following:

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

5

1. Total financing sources were confirmed by the inflow to the foreign currency accounts in the commercial banks and in the liquidity account intended for the inflow of funds from the emission of securities, in the amount of 333,867,350.25 € and by the repayment of the principal of the debt in the amount of 158,591,727.18 €. Thus, the net borrowings on the basis of credits and issued securities amount to 175,525,623.07 €. According to Article 11 paragraph 4 of the Law on the Budget of Montenegro for 2013 (Official Gazette of Montenegro, no. 66/12) the borrowing is not clearly defined, i.e. it is not emphasized whether it is a net borrowing or a gross amount out of which the net borrowing is derived after the principal is paid.

In the annual budget laws the Government of Montenegro and the Ministry of Finance have to define the limit for borrowings of the state more precisely by adding the indication "gross or net borrowing".

2. The audit established that in 2013 the budget spending was overrun by the amount of

261,155,210.71 €. Out of the total expressed overrun of the budget spending, the amount of 238,602,065.82 € was the allowed overrun for payment of interest, repayment of the principal and expenditures expressed for the arrears on the basis of payments related to judicial rulings, expenditures financed from donations and expenditures incurred in the implementation of international contracts. Non‐allowed overrun amounts to 22,553,144.89 € and it is based on expenditures for the purchase of securities and payment of the expenditures from the group of accounts for arrears based on judicial rulings that are above allowed according to Article 12 of the Law on the Budget of Montenegro for 2013 (Official Gazette of Montenegro, no. 66/12).

It is recommended that the fiscal discipline is strengthened further and that the compliance with Article 40 paragraph 1 of the Law on the Budget and Fiscal Responsibility (Official Gazette of Montenegro, no. 20/14) is ensured. This paragraph stipulates that the spending units are obliged to use the funds within the limits defined in the Law on the State Budget.

3. Consolidated data of the spending units show that the revenues made through own

activities the units undertake on the basis of the law, were used for financing expenditures of the spending unit that made such revenues. However, we are hereby indicating to the fact that such funds were used in the spending units up to the amounts made and not in line with the budget constraints defined in the annual budget plan.

We therefore recommend that in the process of planning the budget through the annual budget laws the Government of Montenegro plans the amount of the revenues made through own activities of the spending units and that the revenues thus made are used in compliance with the constraints defined in the annual budget law.

4. Accounting records of the Tax Administration do not ensure the records that would be

harmonized with the Rulebook on Tax Accountancy in terms of the expressed balance in the accounts of the class "1" ‐ accounts of monetary funds, class "3" ‐ accounts of public revenue payers (including the deposit accounts) and class "7" ‐ accounts of public revenues. Tax Administration has not ensured the implementation of the provisions of the Order on the Manner of Payment of Public Revenues, chapter General Provisions, Article 5, which defines the obligation that, after being identified, the payments are transferred from the clearing account to the Central Account of the State Treasury at least once a day, with the obligation to have the zero balance on the clearance accounts at the end of the day.

Tax Administration is recommended to ensure consistent compliance with the legislation in the development of the Tax Final Statements of Accounts, and to harmonize regularly the balance with the General Ledger of the State Treasury and with the Central Bank of Montenegro.

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

6

5. Audit of expenditures recorded in the group of accounts 463 ‐ Repayment of Arrears from

Previous Years ‐ established that the payment of expenditures is not in compliance with the Regulation on Uniform Classification of Accounts for the Budget, Extra‐budgetary Funds and Budgets of Municipalities and that the paid expenditures do not present arrears but extraordinary expenditures that were not planned in the annual budget law.

It is recommended that in the group of accounts 463 ‐ Repayment of Arrears from Previous Years ‐the expenditures for the payment of arrears not planned in the budget are also recorded, because in that case there is no possibility to pay the arrears from the budget lines approved for the expenditures.

6. According to the Statement of Cash Flows III, Pension and Disability Insurance Fund

presented the earmarked revenues in the amount of 243,521,066.72 € and general revenues in the amount of 144,033,315.10 €. Pension and Disability Insurance Fund recorded the earmarked revenues based on the data from the clearing accounts and the data from the "Recipient’s statements". The Proposed Law on the Final Statement of Accounts of the Budget for 2013 stipulates that the earmarked revenues amount to 316,094,340.63 €, while the general revenues amount to 71,460,041.19 €. This is not in line with the data presented by the Pension and Disability Insurance Fund. Article 178 of the Pension and Disability Insurance Act stipulates that the expenditures of the Pension and Disability Insurance Fund are costs based on the contributions for health insurance of the pension users. Law on Budget for 2013 did not plan any expenditure in the group of accounts 423‐7 ‐ Contributions for health insurance of pension users.

State Treasury and the Pension and Disability Insurance Fund should harmonise their data on the amount of the earmarked and general revenues expressed in the Proposed Law on the Final Statement of Accounts of the Budget for 2013. Expenditures based on the contribution for the health care of the pension users should be planned in the annual budget law according to Article 178 of the Pension and Disability Insurance Act and the Budget Law.

7. Item 134 of the Chapter X (ten) of the Directions on State Treasury Operations is not in

compliance with Article 43 of the Budget Law, which is now Article 60 of the Law on the Budget and Fiscal Responsibility.

It is necessary for the Ministry of Finance to harmonize its Directions on State Treasury Operations with the Law on Budget and Fiscal Responsibility.

8. Using the funds of the current budget reserve is not in full compliance with the provisions of

the Budget Law and the Rulebook on Detailed Criteria for the Use of Resources of the Current and Permanent Budget Reserve. The audit identified irregularities in the implementation of Article 3 of the Rulebook on Detailed Criteria for the Use of Resources of the Current and Permanent Budget Reserve. Decisions of the Government and the decisions of the Ministry of Finance were used for reallocation of the funds in such a way that the planned funds were increased by 12,440,685.98 € and reduced by 5,565,879.78 €. The reduction of the reserve funds led to the overrun over the allowed limit of up to 10% of the total planned expenditures the amount of which is reduced and this is not in line with Article 35 of the Budget Law.

Use of the funds of the current budget reserve should be harmonized with the provisions of the Budget Law and the Rulebook on Detailed Criteria for the Use of Resources of the Current and Permanent Budget Reserve.

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

7

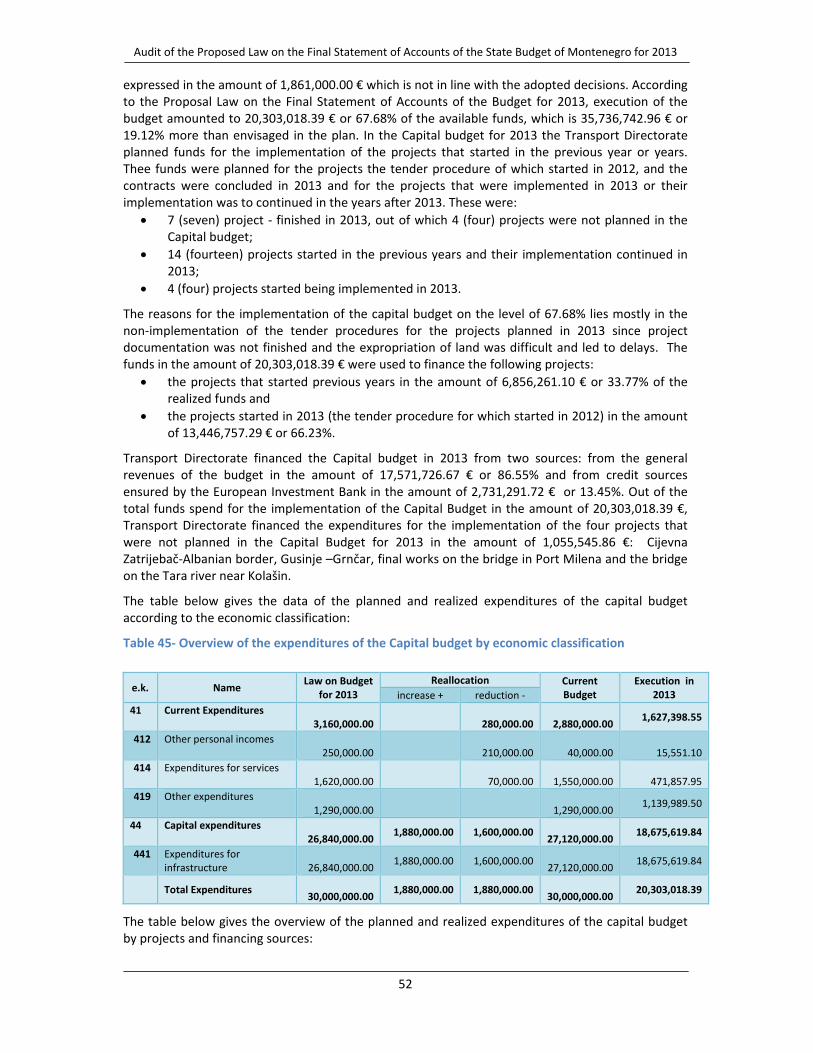

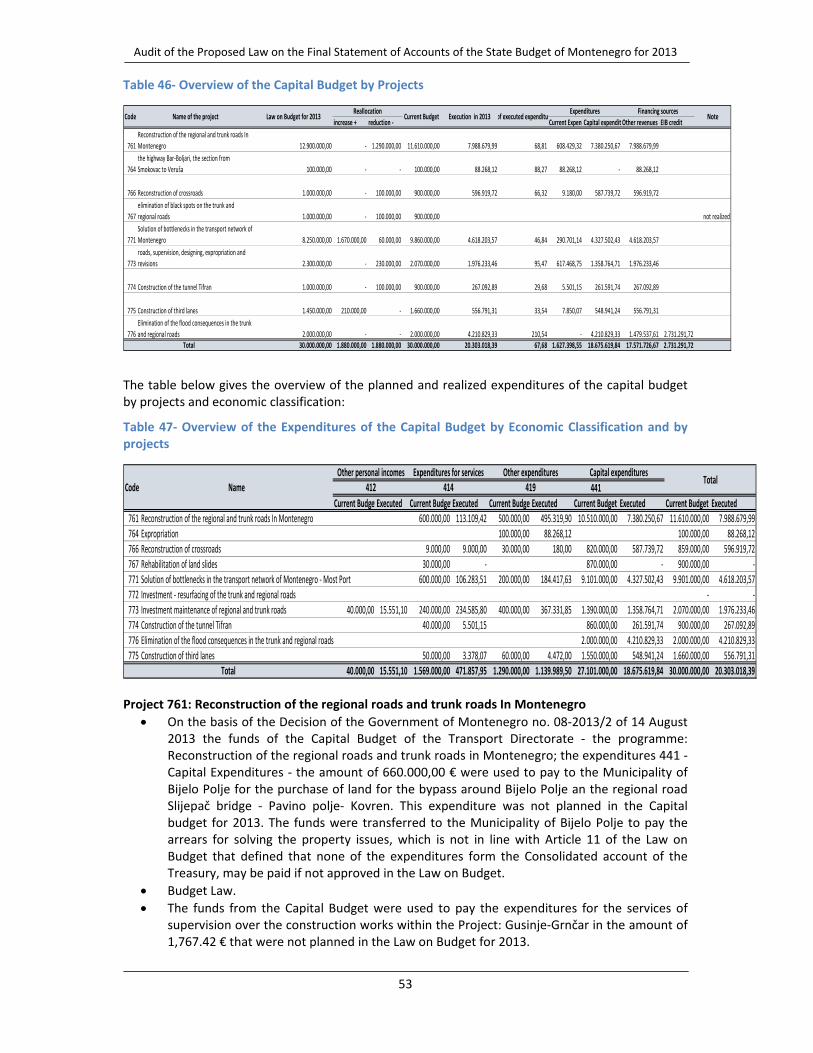

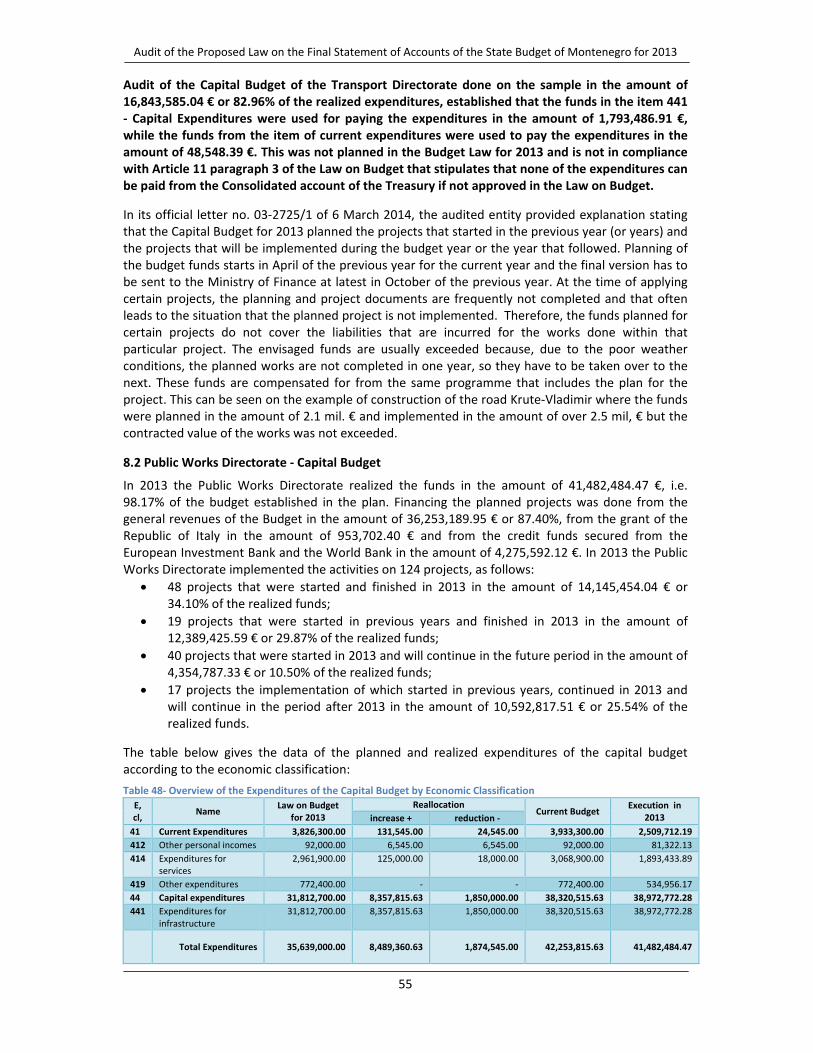

9. Audit of the capital budget of the Transport Directorate established that the funds in the budget item 441 ‐ Capital Expenditures were used for paying the expenditures in the amount of 1,793,486.91 €, while the funds from the item of current expenditures were used to pay the expenditures in the amount of 48,548.39 €. This was not planned in the Budget Law for 2013. Audit of the capital budget of the Public Works Directorate established that the funds in the budget item 441 ‐ Capital Expenditures were used for paying the expenditures in the amount of 5,911,815.63 €, which was not planned in the Budget Law for 2013. This is not in compliance with Article 11 paragraph 3 of the Budget Law. Audit of expenditures recorded in the group of accounts 463 ‐ Repayment of Arrears from Previous Years established that the payment of expenditures is not in compliance with the Regulation on Uniform Classification of Accounts for the Budget, Extra‐Budgetary Funds and Budgets of Municipalities and that the paid expenditures do not present arrears but extraordinary expenditures that were not planned in the annual budget law.

It is recommended for the Capital Budget to be executed according to Article 11 paragraph 3 of the Budget Law, which stipulates that no expenditure from the consolidated account of the State Treasury may be paid if it is not approved in the Budget Law.

10. Audit of the management of the state property identified certain deficiencies, some of which

were described in the Report on the Audit of the Proposed Law on the Final Statement of Accounts of the Budget for 2012.

All spending units are recommended to ensure records of the state property in line with the Property Law and secondary legislation.

11. Audit of the public procurement systems identified recurrent deficiencies which are related

to the inadequate planning of procurement, non‐execution of the procedures in line with the legislation and imprecise compilation of the tender documents.

As for the public procurement, the State Audit Institution wishes to draw attention of the spending units to the necessity of making the public procurement system transparent and of complying consistently with the Public Procurement Law.

12. A number of recommendations given in the Report on the Audit of the Proposed Law on the

Final Statement of Accounts of the Budget for 2012 and individual audit reports have not been implemented.

It is recommended that in the forthcoming period the Government of Montenegro and the Ministry of Finance intensify their activities on the implementation of the recommendations given in the Annual Report on the conducted audits of the State Audit Institution for the period October 2012 ‐ October 2013.

13. Audit of the internal financial control systems of the spending units that were subject to the audit revealed that the internal financial control system is not established on the satisfactory level, while the internal audit units started audits of certain processes.

Activities on the establishment of the financial control function and the internal audit function in the spending units have to be intensified in line with the Law on Public Internal Financial Control and internal audit standards.

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

8

REPORT ON THE AUDIT OF THE PROPOSED LAW ON FINAL STATEMENT OF ACCOUNTS OF THE BUDGET OF MONTENEGRO FOR 2013

1. INTRODUCTION State Audit Institution conducted the financial audit and the compliance audit of the Proposed Law on Final Statement of Accounts of the Budget of Montenegro for 2013. Financial audit implies control of reliability and accuracy of financial statements. Compliance audit implies control of the compliance of operations with the legislation regulating the public spending system in Montenegro.

Goal of the financial audit of the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 is to express the opinion about the level to which the financial report is true and fair.

Goal of the compliance audit of the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 is to express the opinion about compliance with the legislation governing budget operations in Montenegro.

Subject of the audit is the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 drafted in line with Article 51 of the Budget Law4, Rulebook on the Unique Classification of Municipal Budgets5 and Rulebook on the Manner of Drafting, Compiling and Filing Financial Statements of the Budget, State Funds and Local Self‐Government Units6. The audit controlled the following: initial and final statement of the Consolidated Account of the Treasury; overview of the deviations from the planned amounts; report on the borrowings that were taken; report on the expenditures from the budget reserves; report on the guarantees given throughout the fiscal year; report on the capital projects; report on the implementation of the programme budget; report on the state debt and issued guarantees; report on the written‐off tax and non‐tax claims and the report on receipts and expenditures of public institutions that are not included in the Consolidated Account of the State Treasury. Audit of the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 included the system of planning, recording and reporting in the field of budget spending. Alongside the documentation and reports that were controlled in the Ministry of Finance ‐ State Treasury, the audit included individual financial statements, records and documentation by spending units. Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013 included the control of the following budget spending units: Ministry of Finance ‐ State Treasury (budget management, expenditures for interest, expenditures for debt repayment, given loans and credits), reserves, Ministry of Interior, Police Directorate, Office for Fight against Trafficking in Human Beings, Customs Administration, Tax Administration, Real‐Estate Administration, Misdemeanour bodies, Administration for Prevention of Money Laundering and Terrorism Financing, Statistical Office, Protector of Property Interests of Montenegro, Ministry of Science, State Archives, Public Institution National Museum of Montenegro, Metrology Office, Agency for Protection of Competition, Ministry for Information Society and Telecommunications, Pension and Disability Insurance Fund, Transport Directorate and Public Works Directorate.

4 OGM 40/01, 44/01, 28/04, 71/05, 12/07, 73/08, 53/09, 46/10 and 49/10 5 OGM 35/05, 37/05, 81/05 and 02/13

6 OGM 32/10, 14/11 and 16/13

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

9

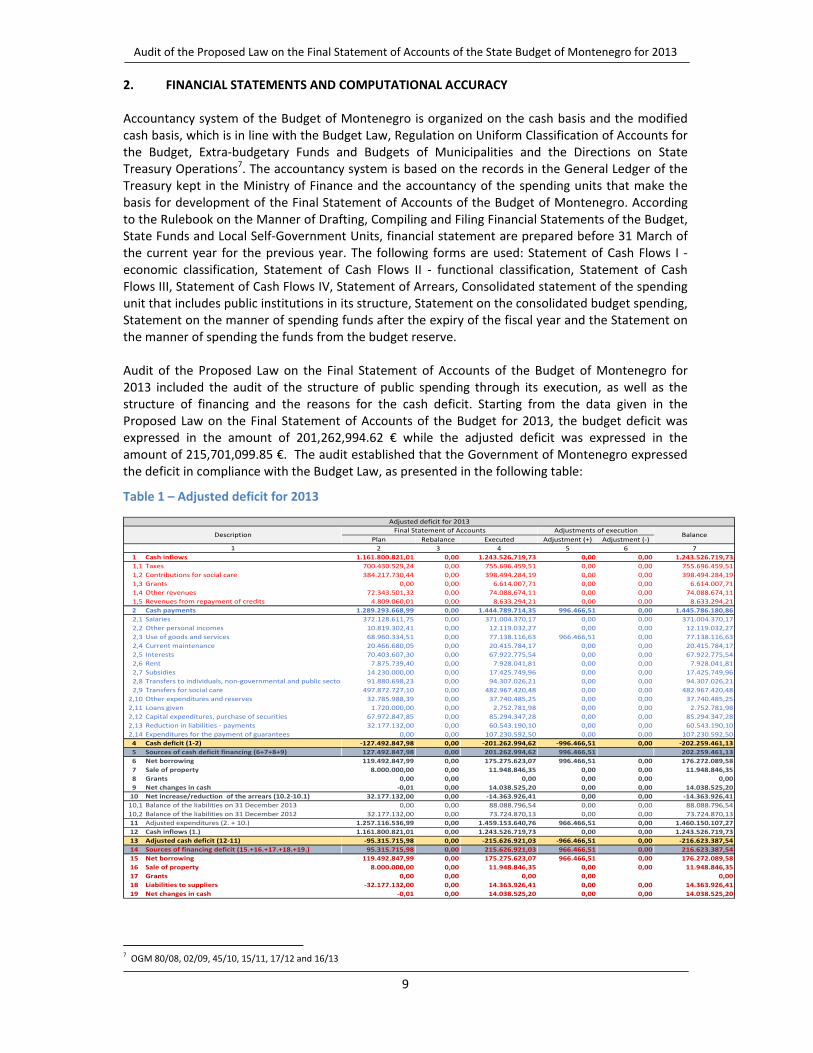

2. FINANCIAL STATEMENTS AND COMPUTATIONAL ACCURACY Accountancy system of the Budget of Montenegro is organized on the cash basis and the modified cash basis, which is in line with the Budget Law, Regulation on Uniform Classification of Accounts for the Budget, Extra‐budgetary Funds and Budgets of Municipalities and the Directions on State Treasury Operations7. The accountancy system is based on the records in the General Ledger of the Treasury kept in the Ministry of Finance and the accountancy of the spending units that make the basis for development of the Final Statement of Accounts of the Budget of Montenegro. According to the Rulebook on the Manner of Drafting, Compiling and Filing Financial Statements of the Budget, State Funds and Local Self‐Government Units, financial statement are prepared before 31 March of the current year for the previous year. The following forms are used: Statement of Cash Flows I ‐ economic classification, Statement of Cash Flows II ‐ functional classification, Statement of Cash Flows III, Statement of Cash Flows IV, Statement of Arrears, Consolidated statement of the spending unit that includes public institutions in its structure, Statement on the consolidated budget spending, Statement on the manner of spending funds after the expiry of the fiscal year and the Statement on the manner of spending the funds from the budget reserve. Audit of the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 included the audit of the structure of public spending through its execution, as well as the structure of financing and the reasons for the cash deficit. Starting from the data given in the Proposed Law on the Final Statement of Accounts of the Budget for 2013, the budget deficit was expressed in the amount of 201,262,994.62 € while the adjusted deficit was expressed in the amount of 215,701,099.85 €. The audit established that the Government of Montenegro expressed the deficit in compliance with the Budget Law, as presented in the following table: Table 1 – Adjusted deficit for 2013

Plan Rebalance Executed Adjustment (+) Adjustment (‐)

2 3 4 5 6 7

1 Cash inflows 1.161.800.821,01 0,00 1.243.526.719,73 0,00 0,00 1.243.526.719,73

1,1 Taxes 700.430.529,24 0,00 755.696.459,51 0,00 0,00 755.696.459,51

1,2 Contributions for social care 384.217.730,44 0,00 398.494.284,19 0,00 0,00 398.494.284,19

1,3 Grants 0,00 0,00 6.614.007,71 0,00 0,00 6.614.007,71

1,4 Other revenues 72.343.501,32 0,00 74.088.674,11 0,00 0,00 74.088.674,11

1,5 Revenues from repayment of credits 4.809.060,01 0,00 8.633.294,21 0,00 0,00 8.633.294,21

2 Cash payments 1.289.293.668,99 0,00 1.444.789.714,35 996.466,51 0,00 1.445.786.180,86

2,1 Salaries 372.128.611,75 0,00 371.004.370,17 0,00 0,00 371.004.370,17

2,2 Other personal incomes 10.819.302,41 0,00 12.119.032,27 0,00 0,00 12.119.032,27

2,3 Use of goods and services 68.960.334,51 0,00 77.138.116,63 966.466,51 0,00 77.138.116,63

2,4 Current maintenance 20.466.680,05 0,00 20.415.784,17 0,00 0,00 20.415.784,17

2,5 Interests 70.403.607,30 0,00 67.922.775,54 0,00 0,00 67.922.775,54

2,6 Rent 7.875.739,40 0,00 7.928.041,81 0,00 0,00 7.928.041,81

2,7 Subsidies 14.230.000,00 0,00 17.425.749,96 0,00 0,00 17.425.749,96

2,8 Transfers to individuals, non‐governmental and public sector 91.880.698,23 0,00 94.307.026,21 0,00 0,00 94.307.026,21

2,9 Transfers for social care 497.872.727,10 0,00 482.967.420,48 0,00 0,00 482.967.420,48

2,10 Other expenditures and reserves 32.785.988,39 0,00 37.740.485,25 0,00 0,00 37.740.485,25

2,11 Loans given 1.720.000,00 0,00 2.752.781,98 0,00 0,00 2.752.781,98

2,12 Capital expenditures, purchase of securities 67.972.847,85 0,00 85.294.347,28 0,00 0,00 85.294.347,28

2,13 Reduction in liabilities ‐ payments 32.177.132,00 0,00 60.543.190,10 0,00 0,00 60.543.190,10

2,14 Expenditures for the payment of guarantees 0,00 0,00 107.230.592,50 0,00 0,00 107.230.592,50

4 Cash deficit (1‐2) ‐127.492.847,98 0,00 ‐201.262.994,62 ‐996.466,51 0,00 ‐202.259.461,13

5 Sources of cash deficit financing (6+7+8+9) 127.492.847,98 0,00 201.262.994,62 996.466,51 202.259.461,13

6 Net borrowing 119.492.847,99 0,00 175.275.623,07 996.466,51 0,00 176.272.089,58

7 Sale of property 8.000.000,00 0,00 11.948.846,35 0,00 0,00 11.948.846,35

8 Grants 0,00 0,00 0,00 0,00 0,00 0,00

9 Net changes in cash ‐0,01 0,00 14.038.525,20 0,00 0,00 14.038.525,20

10 Net increase/reduction of the arrears (10.2‐10.1) 32.177.132,00 0,00 ‐14.363.926,41 0,00 0,00 ‐14.363.926,41

10,1 Balance of the liabilities on 31 December 2013 0,00 0,00 88.088.796,54 0,00 0,00 88.088.796,54

10,2 Balance of the liabilities on 31 December 2012 32.177.132,00 0,00 73.724.870,13 0,00 0,00 73.724.870,13

11 Adjusted expenditures (2. + 10.) 1.257.116.536,99 0,00 1.459.153.640,76 966.466,51 0,00 1.460.150.107,27

12 Cash inflows (1.) 1.161.800.821,01 0,00 1.243.526.719,73 0,00 0,00 1.243.526.719,73

13 Adjusted cash deficit (12‐11) ‐95.315.715,98 0,00 ‐215.626.921,03 ‐966.466,51 0,00 ‐216.623.387,54

14 Sources of financing deficit (15.+16.+17.+18.+19.) 95.315.715,98 0,00 215.626.921,03 966.466,51 0,00 216.623.387,54

15 Net borrowing 119.492.847,99 0,00 175.275.623,07 966.466,51 0,00 176.272.089,58

16 Sale of property 8.000.000,00 0,00 11.948.846,35 0,00 0,00 11.948.846,35

17 Grants 0,00 0,00 0,00 0,00 0,00

18 Liabilities to suppliers ‐32.177.132,00 0,00 14.363.926,41 0,00 0,00 14.363.926,41

19 Net changes in cash ‐0,01 0,00 14.038.525,20 0,00 0,00 14.038.525,20

Adjusted deficit for 2013

1

Final Statement of Accounts Adjustments of executionBalanceDescription

7 OGM 80/08, 02/09, 45/10, 15/11, 17/12 and 16/13

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

10

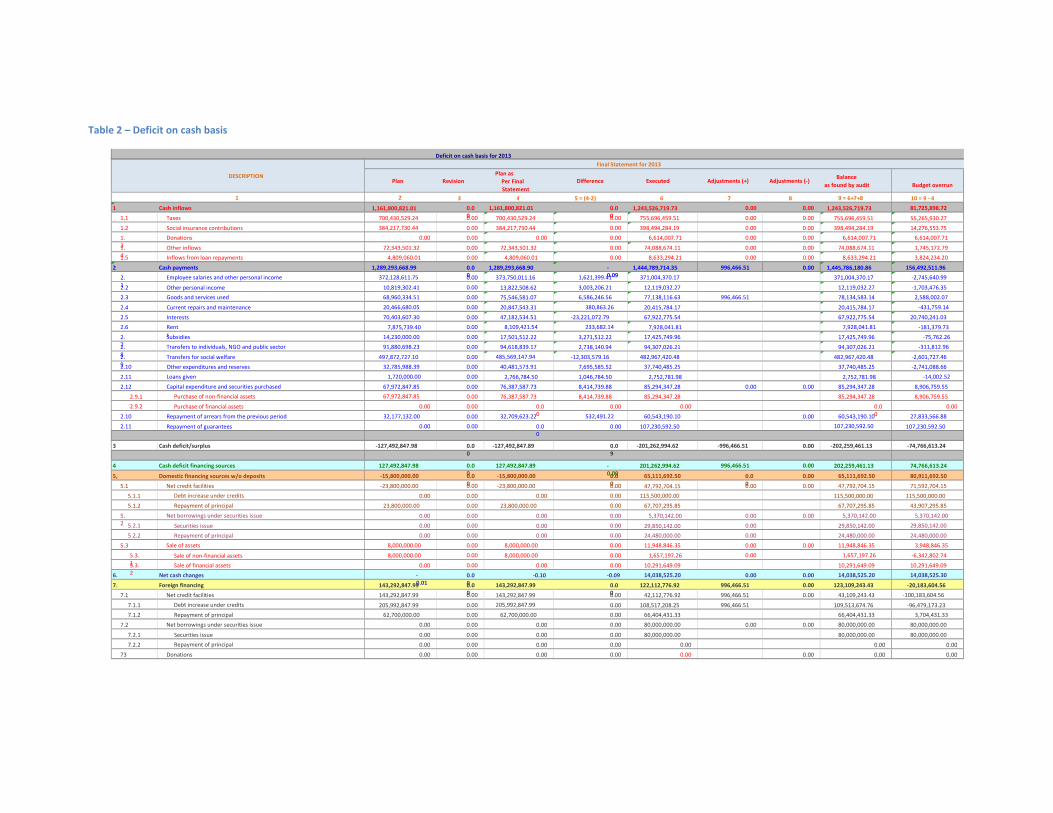

Budget deficit was expressed in line with Article 14 of the Law on the Budget and Fiscal Responsibility (OGM, 20/14) and the State Audit Institution did not establish any materially significant mistakes that would require changes in the expressed results. We would like to note that the General Ledger of the State Treasury did not record the costs of banking services in the amount of 996,466.51 € because they were directly deducted from the funds withdrawn by the banks. The expenditures for the banking services and the negative exchange differences, deficit are adjusted for these funds and the inflow from the foreign borrowings is increased by the same amount as presented in the table above. In the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 the amount of the capital expenditures is increased. These expenditures used to be presented as the repayments of debts in the past. Thus, the way they are presented now is a result of the implementation of the State Audit Institution's recommendation about the methodology for presenting the deficit from the previous year. The audit established that the Government of Montenegro financed the cash deficit of 201,262,994.62 € from the following sources:

Net borrowing ........................................ 175,275,623.07 €,

Sale of property ..................................... 11,948,846.35 € and

Reducing its deposit ............................... 14,038,525.20 €. The deficit on the modified cash basis in the amount of 215,626,921.03 € was financed from the following sources:

Net borrowing ........................................ 175,275,623.07 €,

Sale of property ..................................... 11,948,846.35 €

Reducing its deposit ............................... 14,038,525.20 € and

Net increase of arrears ....................... 14,363,926.41 €.

Figure 1 – Financing modified deficit

2.1. Compliance audit of the cash flow State Audit Institution checked the compliance of the budget revenues and expenditures and financing transactions with the data expressed in the Central Bank of Montenegro. It was done by checking the cash inflows and outflows through the accounts intended for the fiscal operations of the state. The check included the following accounts:

Treasury General Account and

Central account of the State Treasury

Treasury General Account ‐ According to the Directions on State Treasury Operations, item 45‐ the Ministry of Finance opened the main bank account, number 9070000000083001‐19. Out of the funds planned in the annual budget money is paid to and withdrawn from this account.

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

11

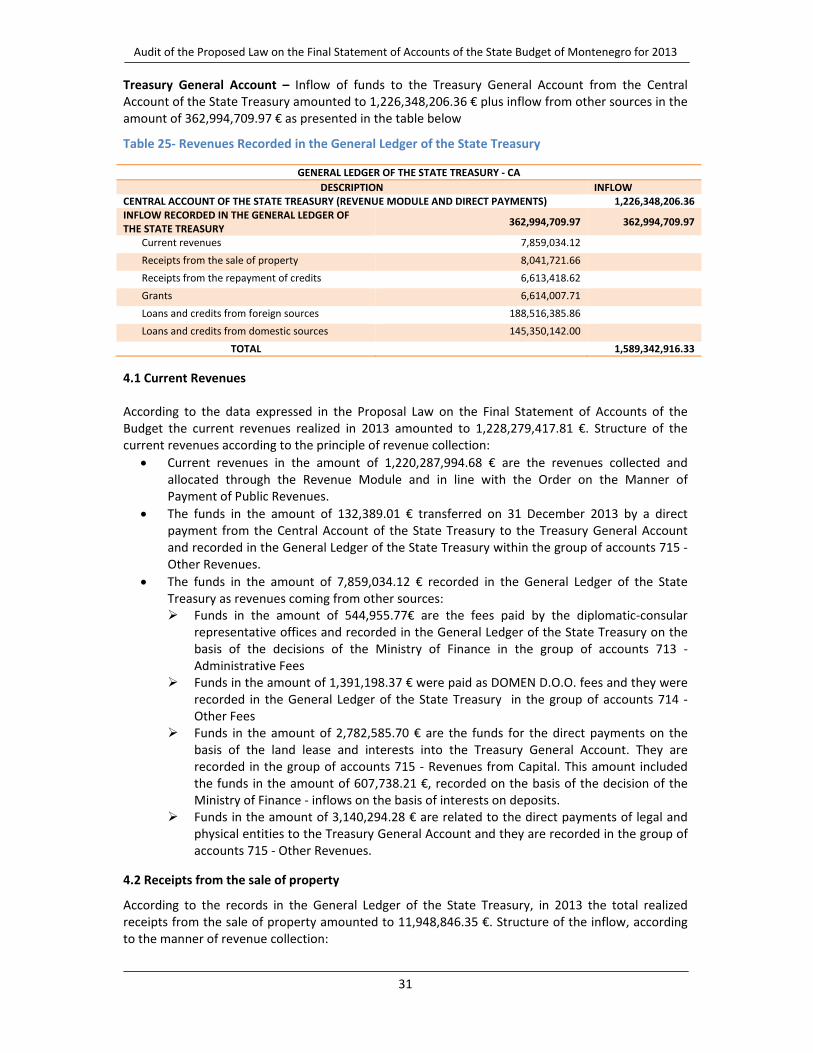

Central account of the State Treasury is the account of the State Treasury number 907000000008320198, used for collection and distribution of public revenues in line with the Order on the Manner of Payment of Public Revenues. The accounts used for collection of public revenues (416 accounts according to the Order and the four clearing accounts, through which the funds are transferred to the Central account of the State Treasury by the spending units that collect public revenues ‐ Customs Administration, Tax Administration, Ministry of Interior and Police Directorate. The audit established that the inflow and outflow of the funds expressed in the Central Account of the State Treasury amounted to 1,345,882,236.74 €. The table below shows the structure of inflow and outflow of funds:

Table 2 –Central Account of the State Treasury

CENTRAL ACCOUNT OF THE STATE TREASURY

Unrecorded cash 3,260,552.62 1,226,348,206.36 Treasury General Account

Tax Administration 919,005,317.80 3,260,552.62 Municipality of Herceg Novi

Customs Administration 368,994,673.62 7,198,449.13 Radio and Television of Montenegro

Ministry of Interior 8,599,251.13 25,342,823.37 Equalization Fund

Police Directorate 4,157,175.30 40,562,155.30 Local self‐government ‐

corresponding taxes Accounts of the ministries, other bodies and judiciary 41,865,266.27 43,134,448.00 Other

TOTAL INFLOW 1,345,882,236.74 35,601.99 Errors

BALANCE ‐0.03 1,345,882,236.77 TOTAL OUTFLOW

Funds collected by the units that collect revenues amount to 1,342,621.84 €, out of which the Tax Administration collected 919,005,317.80 €, Customs Administration collected 368,994,673.62 €, Ministry of Interior collected 8,599,251.13 €, Police Directorate collected 4,157,175.30 €, while other units collected 41,865,266.27 €. The amount of 3,260,552.62 € is the cash that was not recorded as a cash deposit of the Government of Montenegro from the previous period and it was used for financing public spending in 2013. The total inflow of funds to the Central Account of the State Treasury in the amount of 1,345,882,236.74 € was distributed as follows: the amount of 1,226,348,206.36 € to the Treasury General Account; 3,260,552.62 € to the Municipality of Herceg Novi as a financial support of the Government of Montenegro; 7,198,449.13 € to the Radio and Television of Montenegro; 25,342,823.37 € to the Equalization Fund; 40,562,155.30 € to the local self‐government since this was the amount of their corresponding taxes; 43,134,448.00 € to other users; while errors in the records amounted to 35,601.00 €. The funds in the amount of 7,198,449.13 were allocated to the Radio and Television of Montenegro through a direct payment from the Central account of the State Treasury and there was no records of this amount on the side of the revenues and expenditures in the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013. In such a way the level of expressed public spending was reduced. It is worthwhile mentioning that by including this transaction into the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 does not increase the level of deficit, but only the level of public spending and therefore of the comprehensiveness of the budget. We recommend that the Government of Montenegro and the Ministry of Finance consider the option of planning the funds of the Radio and Television of Montenegro through the annual law on budget, as a transfer to institutions, individuals, non‐governmental and public sector. We recommend that they realize the planned funds through the General Ledger of the State Treasury and that they report about this spending within the Law on the Final Statement of Accounts of the State Budget of Montenegro. The funds allocated to the Municipality of Herceg Novi as financial support, were directly paid from the Central Account of the State Treasury and therefore they were not recorded in the Treasury

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

12

General Account and the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013. However, the same amount from previous years was ensured through accumulation of cash from the revenues generated from land lease, a part of which belonged to the Municipality of Herceg Novi. This puts into doubt the consistency of the documentation authorizing the Central Bank of Montenegro to make the payment to the Municipality of Herceg Novi, and not its records nor the rights of the end user. Therefore the State Audit Institution did not make any adjustment of the expressed deficit by the amount of 3,260,552.62 €. Turnover of the funds presented on the debit side of the General Ledger of the State Treasury ‐ CTA (Consolidated Treasury Account) amounted to 1,610,225,705.13 €, out of which 20,882,788.91 € are the deposits from the previous year; 1,255,476,388.36 € are unpaid revenues; 188,516,385.86 € are loans and credits from the country and 145,350,142.00 € are loans and credits from abroad. Payments recorded in the General Ledger of the State Treasury amount to 1,603,381,441.53 €, while the cash in the end of the period amounts to 6,844,263.60 €. This amount of cash was confirmed by checking all accounts that were opened with the Central Bank of Montenegro and by random sample check in the Erste Bank where there are 12 accounts/sub‐accounts under the registry number of the Ministry of Finance. The table below shows the inflows and outflows of funds recorded in the General Ledger of the State Treasury ‐ CTA:

Table 3 –General Ledger of the State Treasury

+

Transferred balance 20,882,788.91 371,004,370.17 Gross salaries and contributions paid by the employer

Transfer ‐ Central account of the State Treasury 1,226,348,206.36 67,922,775.54 Interests Other recorded as inflow 29,128,182.00 12,119,032.27 Other personal incomes Loans and credits from abroad 188,516,385.86 23,613,640.46 Other expenditures Loans and credits from the country 145,350,142.00 27,269,260.95 Expenditures for material and servicesTOTAL INFLOW + opening balance 1,610,225,705.13 20,415,784.17 Expenditures for current maintenance

49,868,855.68 Expenditures for services 7,928,041.81 Rent

17,425,749.96 Subsidies14,79,096.09 Other health care rights 7,862,525.36 Other health insurance rights

383,189,899.52 Pension and disability insurance rights64,036,543.99 Social care rights 13,086,355.52 Funds for redundancies 1,485,645.23 Other transfers

92,821,380.98 Transfers to institutions, individuals, NGOs

69,860,622.71 Capital expenditures 2,752,781.98 Loans and credits

174,025,451.75 Repayment of debt 107,230,592.50 Repayment of guarantees

60,543,190.10 Repayment of liabilities from previous years

406,000.00 Permanent budget reserve 13,720,844.79 Current budget reserve

BALANCE 6,844,263.60 1,603,381,441.53 TOTAL OUTFLOW Total expressed inflows and outflows of funds in the General Ledger of the State Treasury ‐ CTA correspond to the revenues and expenditures expressed in the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013, except for the adjustment in the capital expenditures and repayment of debts for the amount of 15,433,724.57 €, which was used to adjust the deficit in the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013. Unpaid revenues in the amount of 1,589,342,916.33 € (1,610,225,705.13 € ‐ 20,882,788.91 €) show that the structure of collection by revenue units corresponds to the funds recorded in the Treasury General Account, which is presented in the table below:

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

13

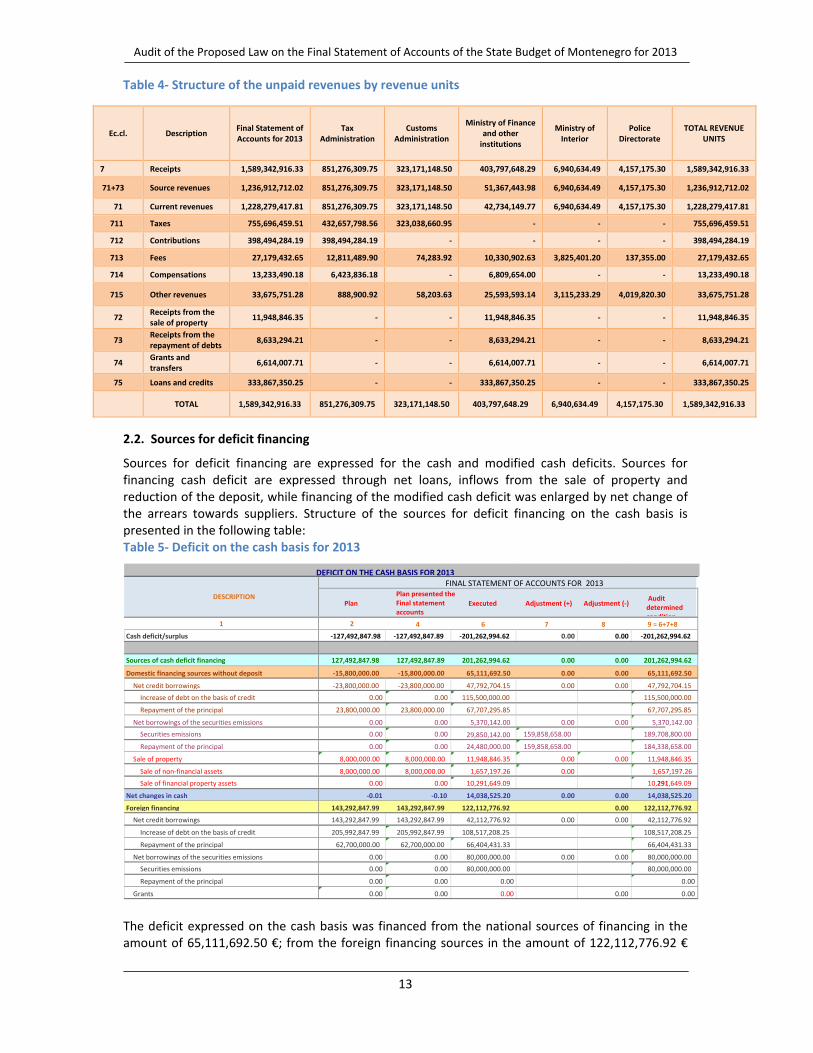

Table 4‐ Structure of the unpaid revenues by revenue units

Ec.cl. Description Final Statement of Accounts for 2013

Tax Administration

Customs Administration

Ministry of Finance and other institutions

Ministry of Interior

Police Directorate

TOTAL REVENUE UNITS

7 Receipts 1,589,342,916.33 851,276,309.75 323,171,148.50 403,797,648.29 6,940,634.49 4,157,175.30 1,589,342,916.33

71+73 Source revenues 1,236,912,712.02 851,276,309.75 323,171,148.50 51,367,443.98 6,940,634.49 4,157,175.30 1,236,912,712.02

71 Current revenues 1,228,279,417.81 851,276,309.75 323,171,148.50 42,734,149.77 6,940,634.49 4,157,175.30 1,228,279,417.81

711 Taxes 755,696,459.51 432,657,798.56 323,038,660.95 ‐ ‐ ‐ 755,696,459.51

712 Contributions 398,494,284.19 398,494,284.19 ‐ ‐ ‐ ‐ 398,494,284.19

713 Fees 27,179,432.65 12,811,489.90 74,283.92 10,330,902.63 3,825,401.20 137,355.00 27,179,432.65

714 Compensations 13,233,490.18 6,423,836.18 ‐ 6,809,654.00 ‐ ‐ 13,233,490.18

715 Other revenues 33,675,751.28 888,900.92 58,203.63 25,593,593.14 3,115,233.29 4,019,820.30 33,675,751.28

72 Receipts from the sale of property

11,948,846.35 ‐ ‐ 11,948,846.35 ‐ ‐ 11,948,846.35

73 Receipts from the repayment of debts

8,633,294.21 ‐ ‐ 8,633,294.21 ‐ ‐ 8,633,294.21

74 Grants and transfers

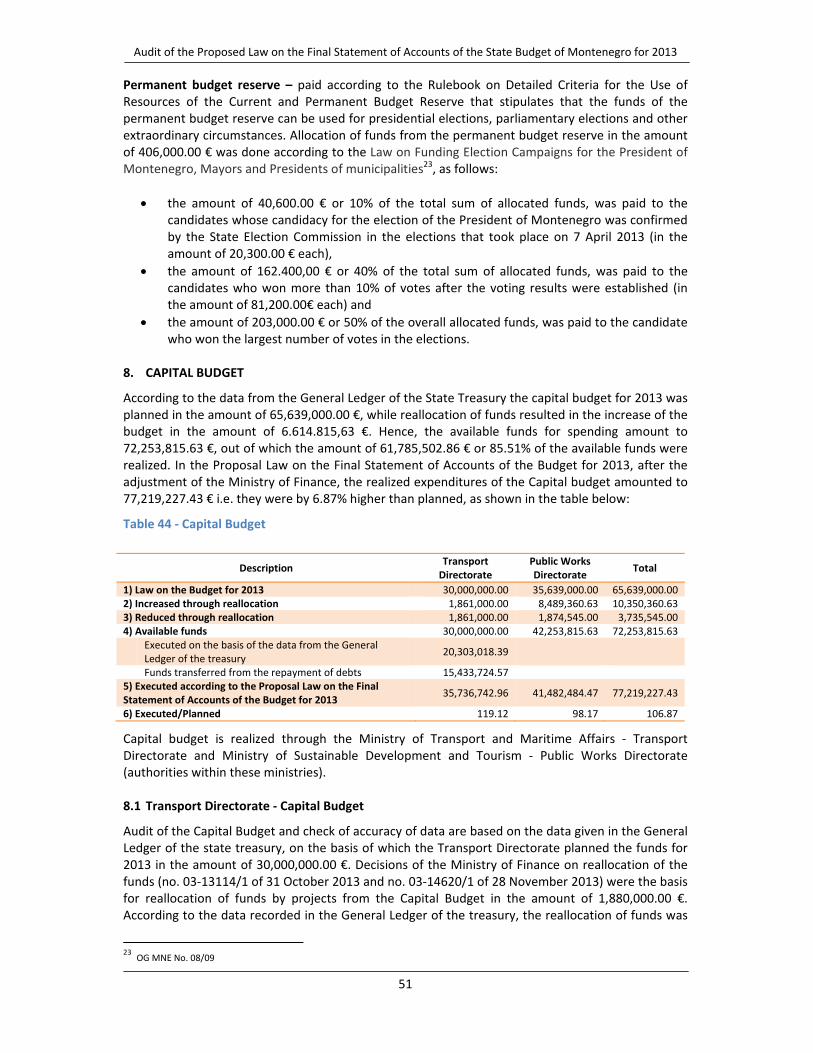

6,614,007.71 ‐ ‐ 6,614,007.71 ‐ ‐ 6,614,007.71

75 Loans and credits 333,867,350.25 ‐ ‐ 333,867,350.25 ‐ ‐ 333,867,350.25

TOTAL 1,589,342,916.33 851,276,309.75 323,171,148.50 403,797,648.29 6,940,634.49 4,157,175.30 1,589,342,916.33

2.2. Sources for deficit financing

Sources for deficit financing are expressed for the cash and modified cash deficits. Sources for financing cash deficit are expressed through net loans, inflows from the sale of property and reduction of the deposit, while financing of the modified cash deficit was enlarged by net change of the arrears towards suppliers. Structure of the sources for deficit financing on the cash basis is presented in the following table: Table 5‐ Deficit on the cash basis for 2013

The deficit expressed on the cash basis was financed from the national sources of financing in the amount of 65,111,692.50 €; from the foreign financing sources in the amount of 122,112,776.92 €

Plan

Plan presented the Final statement accounts

Executed Adjustment (+) Adjustment (‐) Audit determined condition

2 4 6 7 8 9 = 6+7+8

Cash deficit/surplus ‐127,492,847.98 ‐127,492,847.89 ‐201,262,994.62 0.00 0.00 ‐201,262,994.62

Sources of cash deficit financing 127,492,847.98 127,492,847.89 201,262,994.62 0.00 0.00 201,262,994.62

Domestic financing sources without deposit ‐15,800,000.00 ‐15,800,000.00 65,111,692.50 0.00 0.00 65,111,692.50

Net credit borrowings ‐23,800,000.00 ‐23,800,000.00 47,792,704.15 0.00 0.00 47,792,704.15

Increase of debt on the basis of credit 0.00 0.00 115,500,000.00 115,500,000.00

Repayment of the principal 23,800,000.00 23,800,000.00 67,707,295.85 67,707,295.85

Net borrowings of the securities emissions 0.00 0.00 5,370,142.00 0.00 0.00 5,370,142.00

Securities emissions 0.00 0.00 29,850,142.00 159,858,658.00 189,708,800.00

Repayment of the principal 0.00 0.00 24,480,000.00 159,858,658.00 184,338,658.00

Sale of property 8,000,000.00 8,000,000.00 11,948,846.35 0.00 0.00 11,948,846.35

Sale of non‐financial assets 8,000,000.00 8,000,000.00 1,657,197.26 0.00 1,657,197.26

Sale of financial property assets 0.00 0.00 10,291,649.09 10,291,649.09

Net changes in cash ‐0.01 ‐0.10 14,038,525.20 0.00 0.00 14,038,525.20

Foreign financing 143,292,847.99 143,292,847.99 122,112,776.92 0.00 122,112,776.92

Net credit borrowings 143,292,847.99 143,292,847.99 42,112,776.92 0.00 0.00 42,112,776.92

Increase of debt on the basis of credit 205,992,847.99 205,992,847.99 108,517,208.25 108,517,208.25

Repayment of the principal 62,700,000.00 62,700,000.00 66,404,431.33 66,404,431.33

Net borrowings of the securities emissions 0.00 0.00 80,000,000.00 0.00 0.00 80,000,000.00

Securities emissions 0.00 0.00 80,000,000.00 80,000,000.00

Repayment of the principal 0.00 0.00 0.00 0.00

Grants 0.00 0.00 0.00 0.00 0.00

DESCRIPTION

1

DEFICIT ON THE CASH BASIS FOR 2013 FINAL STATEMENT OF ACCOUNTS FOR 2013

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

14

and from the cash deposits in the amount of 14,038,525.20 €. National financing sources were ensured from the credits in the amount of 67,707,295.85 €; from securities emissions in the amount of 5,370,142.00 € and from the sale of property in the amount of 11,948,846.35 €. Foreign financing sources were ensured in the total amount of 122,112,776.92 €, out of which 42,112,776.92 € from the credits and 80,000,000.00 € from securities emissions. It has to be taken into account that the securities emissions in the country were not recorded as gross but as set‐off amount, and therefore there are no records of the overall turnover. This is why the State Audit Institution adjusted the turnover of securities in the country by the amount of 159,858,658.00 €. This adjustment did not have any impact on the net borrowings or the change in the amount of the expressed deficit. According to Article 11 paragraph 4 of the Law on the Budget of Montenegro for 2013 (Official Gazette of Montenegro, no. 66/12) the borrowing is not clearly defined, i.e. it is not emphasized whether it is a net borrowing or a gross amount out of which the net borrowing is derived after the principal is paid. In the annual budget laws the Government of Montenegro and the Ministry of Finance have to define more precisely the boundary for the borrowings of the state by adding the indication "gross or net borrowing".

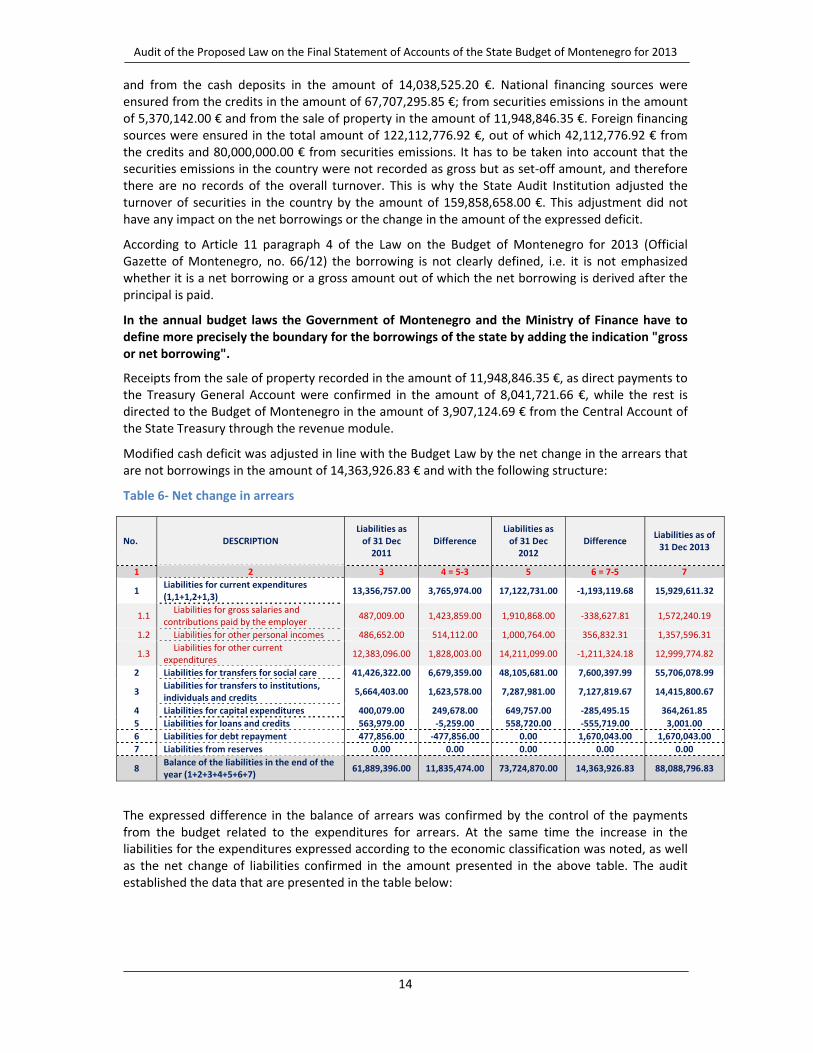

Receipts from the sale of property recorded in the amount of 11,948,846.35 €, as direct payments to the Treasury General Account were confirmed in the amount of 8,041,721.66 €, while the rest is directed to the Budget of Montenegro in the amount of 3,907,124.69 € from the Central Account of the State Treasury through the revenue module. Modified cash deficit was adjusted in line with the Budget Law by the net change in the arrears that are not borrowings in the amount of 14,363,926.83 € and with the following structure: Table 6‐ Net change in arrears

No. DESCRIPTION Liabilities as of 31 Dec 2011

Difference Liabilities as of 31 Dec 2012

Difference Liabilities as of 31 Dec 2013

1 2 3 4 = 5‐3 5 6 = 7‐5 7

1 Liabilities for current expenditures (1,1+1,2+1,3)

13,356,757.00 3,765,974.00 17,122,731.00 ‐1,193,119.68 15,929,611.32

1.1 Liabilities for gross salaries and

contributions paid by the employer 487,009.00 1,423,859.00 1,910,868.00 ‐338,627.81 1,572,240.19

1.2 Liabilities for other personal incomes 486,652.00 514,112.00 1,000,764.00 356,832.31 1,357,596.31

1.3 Liabilities for other current

expenditures 12,383,096.00 1,828,003.00 14,211,099.00 ‐1,211,324.18 12,999,774.82

2 Liabilities for transfers for social care 41,426,322.00 6,679,359.00 48,105,681.00 7,600,397.99 55,706,078.99

3 Liabilities for transfers to institutions, individuals and credits

5,664,403.00 1,623,578.00 7,287,981.00 7,127,819.67 14,415,800.67

4 Liabilities for capital expenditures 400,079.00 249,678.00 649,757.00 ‐285,495.15 364,261.85

5 Liabilities for loans and credits 563,979.00 ‐5,259.00 558,720.00 ‐555,719.00 3,001.00

6 Liabilities for debt repayment 477,856.00 ‐477,856.00 0.00 1,670,043.00 1,670,043.00

7 Liabilities from reserves 0.00 0.00 0.00 0.00 0.00

8 Balance of the liabilities in the end of the year (1+2+3+4+5+6+7)

61,889,396.00 11,835,474.00 73,724,870.00 14,363,926.83 88,088,796.83

The expressed difference in the balance of arrears was confirmed by the control of the payments from the budget related to the expenditures for arrears. At the same time the increase in the liabilities for the expenditures expressed according to the economic classification was noted, as well as the net change of liabilities confirmed in the amount presented in the above table. The audit established the data that are presented in the table below:

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

15

Table 7‐ Records of arrears RECORDS OF ARREARS

DESCRIPTION amount amount

Balance on 31 December 2012 73,724,870.15

Repayment of arrears (reduction) 66,814,689.64

Increase in arrears 81,178,616.03

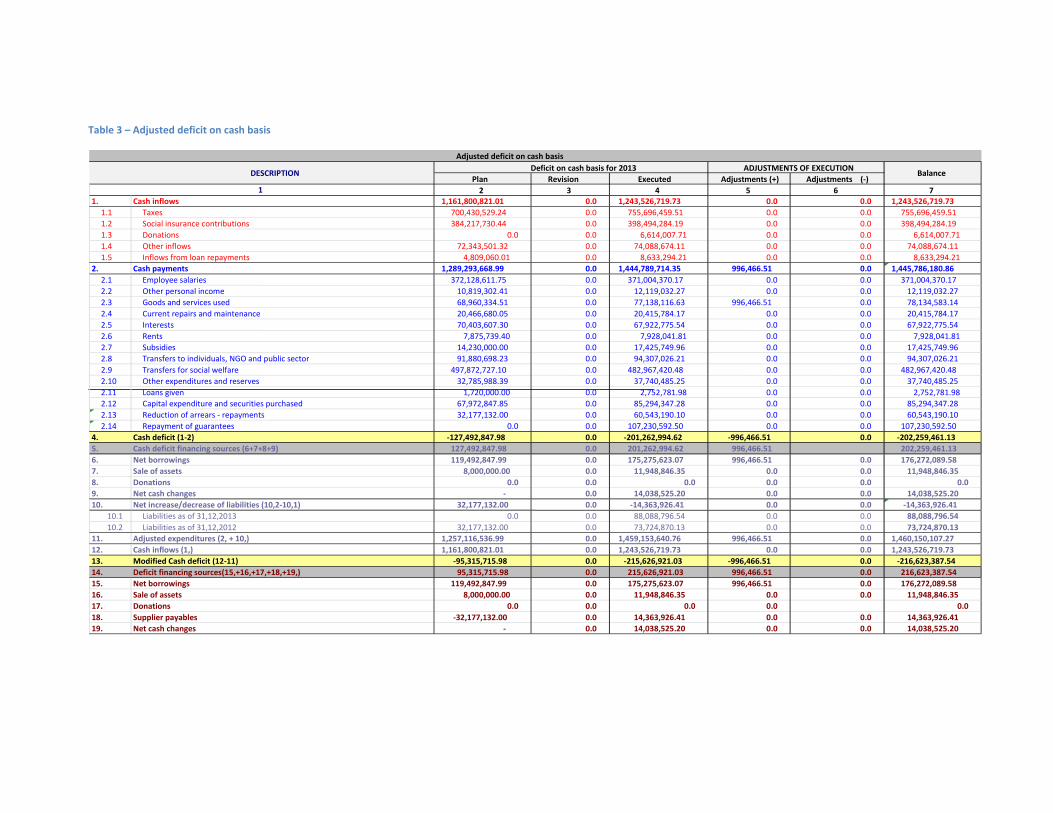

Balance on 31 December 2013 88,088,796.54 Opening balance of arrears reduced by repayment of arrears and increased by increase arrears results in the amount of 88,088,796.54 €. If the expenditures expressed on the cash basis are adjusted by the same amount, the result is the amount of the adjusted deficit as presented in the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013. Table 8‐ Adjusted Cash Deficit

ADJUSTED CASH DEFICIT

Budget incomes 1,243,526,719.73

Adjusted budget expenditures 1,459,153,640.74

Cash deficit ‐215,626,921.01 We would like to emphasise that the State Audit Institution cannot support the statements expressed in the statement of reasons enclosed to the Proposed Law on the Final Statement of Accounts of the Budget of Montenegro for 2013 on the page 136 related to the amendments to the provisions governing the calculations of the surplus/deficit. We would like to note that the adjustment of expenditures is reduced by repayment of liabilities and increased by arrears and therefore the result is adjusted by the net effect. If liabilities are repaid next year they will reduce the expenditures, which will be contrary to the statement that the deficit will be increased two times. This opinion of the State Audit Institution is supported through the processing of the data that were analysed using the flows expressed as the changes in the balance sheet on the basis of the available data that are mostly based on the cash transactions and partly expressed accountancy categories related to the changes in the records of arrears that are not borrowings. Data on the changes in the balance sheet are presented in the table below: Table 9‐ Balance sheet Non‐financial assets 73,345,500.93 73,060,006.19 73,060,006.19

Purchase of the fixed assets and inventories 85,294,347.28 85,008,852.54 85,008,852.54 for cash 85,294,347.28 85,008,852.54 85,008,852.54Grants 0.00 0.00 0.00

Reduction of the fixed assets and inventories 11,948,846.35 11,948,846.35 11,948,846.35 Sale for cash 11,948,846.35 11,948,846.35 11,948,846.35 Depreciation 0.00 0.00 0.00

Financial assets ‐11,285,743.22 ‐11,841,462.18 ‐11,841,462.18

Cash ‐14,038,525.20 ‐14,038,525.20 ‐14,038,525.20 Increase 1,749,201,574.33 1,749,201,574.33 1,749,201,574.33 Reduction 1,763,240,099.53 1,763,240,099.53 1,763,240,099.53

Liabilities 2,752,781.98 2,197,063.02 2,197,063.02 Loans given 2,752,781.98 2,197,063.02 2,197,063.02Other loans 0.00 0.00 0.00

Liabilities 189,639,549.46 189,639,549.46 189,639,549.46

Loans and credits 175,275,623.07 175,275,623.07 175,275,623.07 Credits taken and the emissions of securities 493,726,008.25 493,726,008.25 493,726,008.25Repayment of credits and the emissions of

securities due 318,450,385.18 318,450,385.18 318,450,385.18 Arrears 14,363,926.39 14,363,926.39 14,363,926.39 Net increase in liabilities 81,178,616.03 81,178,616.03 81,178,616.03 Net reduction in liabilities 66,814,689.64 66,814,689.64 66,814,689.64

Cash deficit ‐201,262,994.62 ‐14,363,926.39

Adjusted cash deficit ‐215,626,921.01 87,205,915.56

Net value ‐128,421,005.45

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

16

Repayment of Arrears from Previous Years in the group of accounts 463 is used for extraordinary expenditures and not for the real repayment of the liabilities. This increases the discretionary spending beyond the legally defined limit. Expenditures in the group of accounts 463 should include the repayment of the arrears for the expenditures that were not planned in the budget, because there is no possibility to pay the arrears from the budget lines approved for the expenditures.

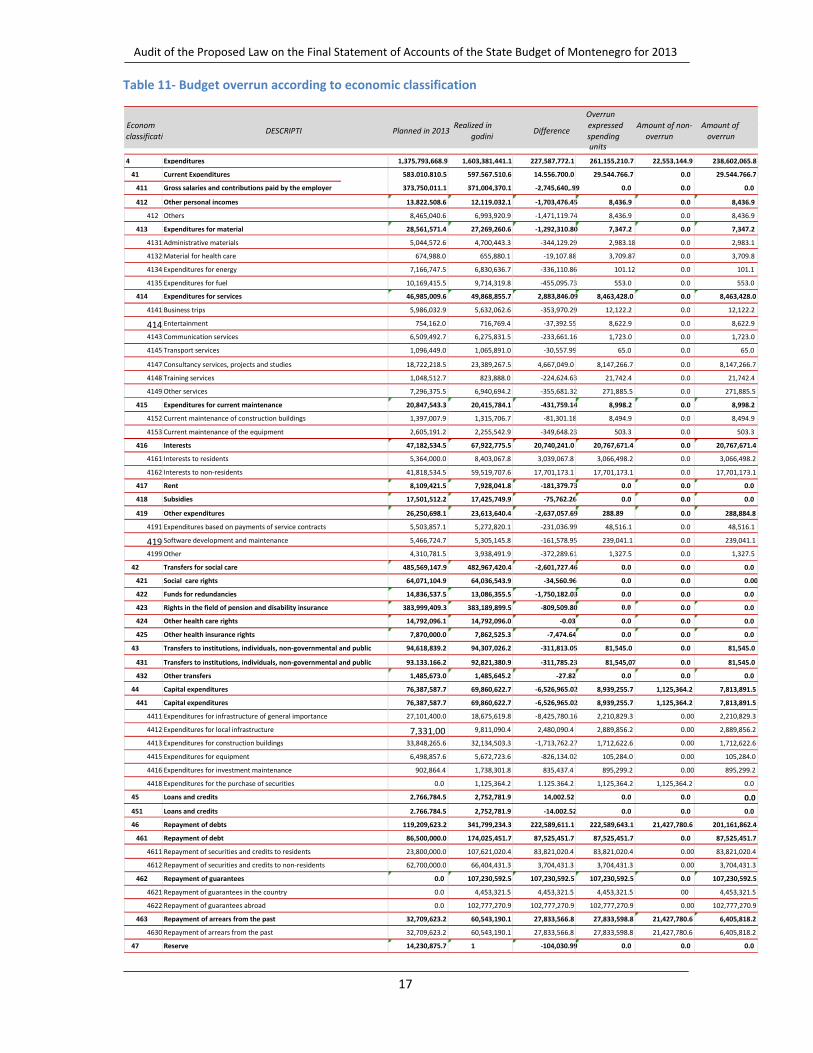

2.3 Budgetary Overrun 66/12). Table 10‐ Budgetary Overrun

DESCRIPTION Amount

TOTAL OVERRUN 261,155,210.73

Non‐allowed overrun 22,553,144.91

Non‐allowed overrun ‐ repayment of arrears from previous years (463) 21,427,780.67

Expenditures for the purchase of securities 1,125,364.24

Allowed overrun 238,602,065.82

Allowed overrun ‐ interests 20,767,671.43

Allowed overrun ‐ repayment of the debt principal and liabilities from the previous period 201,161,862.46

Allowed overrun ‐ grants 4,223,126.62

Allowed overrun ‐ international agreements 12,449,405.31

The table below shows budget overrun by expenditure lines expressed in the economic classification:

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

17

Table 11‐ Budget overrun according to economic classification

4 Expenditures 1,375,793,668.9 1,603,381,441.1 227,587,772.1 261,155,210.7 22,553,144.9 238,602,065.8

41 Current Expenditures 583,010,810.5 597,567,510.6 14,556,700.0 29,544,766.7 0.0 29,544,766.7

411 Gross salaries and contributions paid by the employer 373,750,011.1 371,004,370.1 ‐2,745,640,.99 0.0 0.0 0.0

412 Other personal incomes 13,822,508.6 12,119,032.1 ‐1,703,476.45 8,436.9 0.0 8,436.9

412 Others 8,465,040.6 6,993,920.9 ‐1,471,119.74 8,436.9 0.0 8,436.9

413 Expenditures for material 28,561,571.4 27,269,260.6 ‐1,292,310.80 7,347.2 0.0 7,347.2

4131 Administrative materials 5,044,572.6 4,700,443.3 ‐344,129.29 2,983.18 0.0 2,983.1

4132 Material for health care 674,988.0 655,880.1 ‐19,107.88 3,709.87 0.0 3,709.8

4134 Expenditures for energy 7,166,747.5 6,830,636.7 ‐336,110.86 101.12 0.0 101.1

4135 Expenditures for fuel 10,169,415.5 9,714,319.8 ‐455,095.73 553.0 0.0 553.0

414 Expenditures for services 46,985,009.6 49,868,855.7 2,883,846.09 8,463,428.0 0.0 8,463,428.0

4141 Business trips 5,986,032.9 5,632,062.6 ‐353,970.29 12,122.2 0.0 12,122.2

414 Entertainment 754,162.0 716,769.4 ‐37,392.55 8,622.9 0.0 8,622.9

4143 Communication services 6,509,492.7 6,275,831.5 ‐233,661.16 1,723.0 0.0 1,723.0

4145 Transport services 1,096,449.0 1,065,891.0 ‐30,557.99 65.0 0.0 65.0

4147 Consultancy services, projects and studies 18,722,218.5 23,389,267.5 4,667,049.0 8,147,266.7 0.0 8,147,266.7

4148 Training services 1,048,512.7 823,888.0 ‐224,624.63 21,742.4 0.0 21,742.4

4149 Other services 7,296,375.5 6,940,694.2 ‐355,681.32 271,885.5 0.0 271,885.5

415 Expenditures for current maintenance 20,847,543.3 20,415,784.1 ‐431,759.14 8,998.2 0.0 8,998.2

4152 Current maintenance of construction buildings 1,397,007.9 1,315,706.7 ‐81,301.18 8,494.9 0.0 8,494.9

4153 Current maintenance of the equipment 2,605,191.2 2,255,542.9 ‐349,648.23 503.3 0.0 503.3

416 Interests 47,182,534.5 67,922,775.5 20,740,241.0 20,767,671.4 0.0 20,767,671.4

4161 Interests to residents 5,364,000.0 8,403,067.8 3,039,067.8 3,066,498.2 0.0 3,066,498.2

4162 Interests to non‐residents 41,818,534.5 59,519,707.6 17,701,173.1 17,701,173.1 0.0 17,701,173.1

417 Rent 8,109,421.5 7,928,041.8 ‐181,379.73 0.0 0.0 0.0

418 Subsidies 17,501,512.2 17,425,749.9 ‐75,762.26 0.0 0.0 0.0

419 Other expenditures 26,250,698.1 23,613,640.4 ‐2,637,057.69 288.89 0.0 288,884.8

4191 Expenditures based on payments of service contracts 5,503,857.1 5,272,820.1 ‐231,036.99 48,516.1 0.0 48,516.1

419 Software development and maintenance 5,466,724.7 5,305,145.8 ‐161,578.95 239,041.1 0.0 239,041.1

4199 Other 4,310,781.5 3,938,491.9 ‐372,289.61 1,327.5 0.0 1,327.5

42 Transfers for social care 485,569,147.9 482,967,420.4 ‐2,601,727.46 0.0 0.0 0.0

421 Social care rights 64,071,104.9 64,036,543.9 ‐34,560.96 0.0 0.0 0.00

422 Funds for redundancies 14,836,537.5 13,086,355.5 ‐1,750,182.03 0.0 0.0 0.0

423 Rights in the field of pension and disability insurance 383,999,409.3 383,189,899.5 ‐809,509.80 0.0 0.0 0.0

424 Other health care rights 14,792,096.1 14,792,096.0 ‐0.03 0.0 0.0 0.0

425 Other health insurance rights 7,870,000.0 7,862,525.3 ‐7,474.64 0.0 0.0 0.0

43 Transfers to institutions, individuals, non‐governmental and public 94,618,839.2 94,307,026.2 ‐311,813.05 81,545.0 0.0 81,545.0

431 Transfers to institutions, individuals, non‐governmental and public 93,133,166.2 92,821,380.9 ‐311,785.23 81,545,07 0.0 81,545.0

432 Other transfers 1,485,673.0 1,485,645.2 ‐27.82 0.0 0.0 0.0

44 Capital expenditures 76,387,587.7 69,860,622.7 ‐6,526,965.02 8,939,255.7 1,125,364.2 7,813,891.5

441 Capital expenditures 76,387,587.7 69,860,622.7 ‐6,526,965.02 8,939,255.7 1,125,364.2 7,813,891.5

4411 Expenditures for infrastructure of general importance 27,101,400.0 18,675,619.8 ‐8,425,780.16 2,210,829.3 0.00 2,210,829.3

4412 Expenditures for local infrastructure 7,331,00 9,811,090.4 2,480,090.4 2,889,856.2 0.00 2,889,856.2

4413 Expenditures for construction buildings 33,848,265.6 32,134,503.3 ‐1,713,762.27 1,712,622.6 0.00 1,712,622.6

4415 Expenditures for equipment 6,498,857.6 5,672,723.6 ‐826,134.02 105,284.0 0.00 105,284.0

4416 Expenditures for investment maintenance 902,864.4 1,738,301.8 835,437.4 895,299.2 0.00 895,299.2

4418 Expenditures for the purchase of securities 0.0 1,125,364.2 1,125,364.2 1,125,364.2 1,125,364.2 0.0

45 Loans and credits 2,766,784.5 2,752,781.9 14,002.52 0.0 0.0 0.0

451 Loans and credits 2,766,784.5 2,752,781.9 ‐14,002.52 0.0 0.0 0.0

46 Repayment of debts 119,209,623.2 341,799,234.3 222,589,611.1 222,589,643.1 21,427,780.6 201,161,862.4

461 Repayment of debt 86,500,000.0 174,025,451.7 87,525,451.7 87,525,451.7 0.0 87,525,451.7

4611 Repayment of securities and credits to residents 23,800,000.0 107,621,020.4 83,821,020.4 83,821,020.4 0.00 83,821,020.4

4612 Repayment of securities and credits to non‐residents 62,700,000.0 66,404,431.3 3,704,431.3 3,704,431.3 0.00 3,704,431.3

462 Repayment of guarantees 0.0 107,230,592.5 107,230,592.5 107,230,592.5 0.0 107,230,592.5

4621 Repayment of guarantees in the country 0.0 4,453,321.5 4,453,321.5 4,453,321.5 00 4,453,321.5

4622 Repayment of guarantees abroad 0.0 102,777,270.9 102,777,270.9 102,777,270.9 0.00 102,777,270.9

463 Repayment of arrears from the past 32,709,623.2 60,543,190.1 27,833,566.8 27,833,598.8 21,427,780.6 6,405,818.2

4630 Repayment of arrears from the past 32,709,623.2 60,543,190.1 27,833,566.8 27,833,598.8 21,427,780.6 6,405,818.2

47 Reserve 14,230,875.7 1 ‐104,030.99 0.0 0.0 0.0

Amount of non‐

overrun

Amount of

overrun

Econom

classificatiDESCRIPTI

Realized in

godiniDifference

Overrun expressed

spending units

Planned in 2013

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

18

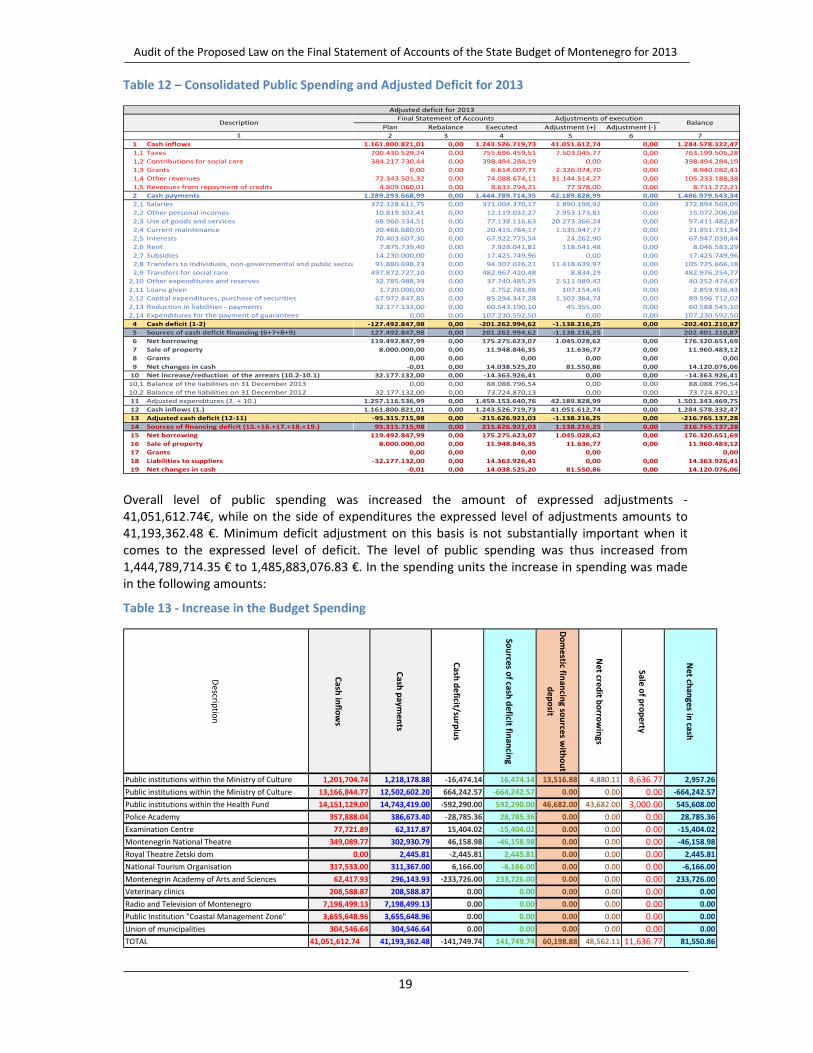

Overrun derived from the summary table complied according to the economic classification that presents the aggregate data for all budget users, shows that the overrun amounts to 227,587,772.15€. This was confirmed also by the individual expenditure lines and by spending units, which shows that the summary expenditure control, on the level of the budget, was not sufficient to stop certain overrun by spending units and expenditure lines. In 2013 the number of spending units that recorded the budget overrun was reduced, as well as the number of expenditure lines that recorded overrun. This shows that there are improvements in the fiscal discipline. The growth of payments based on court rulings are concerning since the payments on this basis increased in 2013 in comparison to 2012. It is recommended that the fiscal discipline is strengthened further and that Article 40 paragraph 1 of the Law on the Budget and Fiscal Responsibility (Official Gazette of Montenegro, no. 20/14) is complied with. This article stipulates that the spending units are obliged to use the funds within the boundaries defined in the Budget Law. 2.4. Scope of Public Spending Audit of the consolidated report established that a number of spending units ensures and uses their own funds according to Article 7 paragraph 1 of the Law on the Budget of Montenegro for 2013 (Official Gazette of Montenegro, no. 66/12), which reads: "The revenues generated by spending unit through its own activities on the basis of its legal authorities shall be used solely for financing expenditures of that particular spending unit up to the amount planned in the budget.” Consolidated data of the spending units show that the revenues generated through their own activities, based on the law, were used for financing expenditures of the spending units that generated them. However, we are hereby indicating to the fact that such funds were used in the spending units up to their full amount and not in line with the budget constraints defined in the annual budget plan. If direct financing from the Central Account of the State Treasury is added to that, the system of public spending is by 41,051,612.74 € higher. Spending units which generated their own revenues and received direct financing from the Central Account of the State Treasury are as follows: public institutions within the Ministry of Culture, public institutions within the Ministry of Education, public institutions within the Health Fund, Police Academy, Examination Centre, Montenegrin National Theatre, Royal Theatre "Zetski Dom", National Tourism Organisation, Montenegrin Academy of Arts and Sciences, veterinary clinics, Radio and Television of Montenegro, Public institution Coastal Management Zone, Union of Municipalities. Increase in the level of public spending by the expenditures financed from the revenues generated through the own activities of the spending units does not influence the level of the expressed deficit, but the expressed level of public spending is significantly adjusted. Therefore, the State Audit Institution consolidated the data with the adjustments on the side of receipts and on the expenditure side in order to ensure more accurate and more comprehensive picture of the level of public spending. That is presented in the table below:

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

19

Table 12 – Consolidated Public Spending and Adjusted Deficit for 2013

Plan Rebalance Executed Adjustment (+) Adjustment (‐)

2 3 4 5 6 7

1 Cash inflows 1.161.800.821,01 0,00 1.243.526.719,73 41.051.612,74 0,00 1.284.578.322,47

1,1 Taxes 700.430.529,24 0,00 755.696.459,51 7.503.045,77 0,00 763.199.505,28

1,2 Contributions for social care 384.217.730,44 0,00 398.494.284,19 0,00 0,00 398.494.284,19

1,3 Grants 0,00 0,00 6.614.007,71 2.326.074,70 0,00 8.940.082,41

1,4 Other revenues 72.343.501,32 0,00 74.088.674,11 31.144.514,27 0,00 105.233.188,38

1,5 Revenues from repayment of credits 4.809.060,01 0,00 8.633.294,21 77.978,00 0,00 8.711.272,21

2 Cash payments 1.289.293.668,99 0,00 1.444.789.714,35 42.189.828,99 0,00 1.486.979.543,34

2,1 Salaries 372.128.611,75 0,00 371.004.370,17 1.890.198,92 0,00 372.894.569,09

2,2 Other personal incomes 10.819.302,41 0,00 12.119.032,27 2.953.173,81 0,00 15.072.206,08

2,3 Use of goods and services 68.960.334,51 0,00 77.138.116,63 20.273.366,24 0,00 97.411.482,87

2,4 Current maintenance 20.466.680,05 0,00 20.415.784,17 1.535.947,77 0,00 21.951.731,94

2,5 Interests 70.403.607,30 0,00 67.922.775,54 24.262,90 0,00 67.947.038,44

2,6 Rent 7.875.739,40 0,00 7.928.041,81 118.541,48 0,00 8.046.583,29

2,7 Subsidies 14.230.000,00 0,00 17.425.749,96 0,00 0,00 17.425.749,96

2,8 Transfers to individuals, non‐governmental and public sector 91.880.698,23 0,00 94.307.026,21 11.418.639,97 0,00 105.725.666,18

2,9 Transfers for social care 497.872.727,10 0,00 482.967.420,48 8.834,29 0,00 482.976.254,77

2,10 Other expenditures and reserves 32.785.988,39 0,00 37.740.485,25 2.511.989,42 0,00 40.252.474,67

2,11 Loans given 1.720.000,00 0,00 2.752.781,98 107.154,45 0,00 2.859.936,43

2,12 Capital expenditures, purchase of securities 67.972.847,85 0,00 85.294.347,28 1.302.364,74 0,00 89.596.712,02

2,13 Reduction in liabilities ‐ payments 32.177.132,00 0,00 60.543.190,10 45.355,00 0,00 60.588.545,10

2,14 Expenditures for the payment of guarantees 0,00 0,00 107.230.592,50 0,00 0,00 107.230.592,50

4 Cash deficit (1‐2) ‐127.492.847,98 0,00 ‐201.262.994,62 ‐1.138.216,25 0,00 ‐202.401.210,87

5 Sources of cash deficit financing (6+7+8+9) 127.492.847,98 0,00 201.262.994,62 ‐1.138.216,25 202.401.210,87

6 Net borrowing 119.492.847,99 0,00 175.275.623,07 1.045.028,62 0,00 176.320.651,69

7 Sale of property 8.000.000,00 0,00 11.948.846,35 11.636,77 0,00 11.960.483,12

8 Grants 0,00 0,00 0,00 0,00 0,00 0,00

9 Net changes in cash ‐0,01 0,00 14.038.525,20 81.550,86 0,00 14.120.076,06

10 Net increase/reduction of the arrears (10.2‐10.1) 32.177.132,00 0,00 ‐14.363.926,41 0,00 0,00 ‐14.363.926,41

10,1 Balance of the liabilities on 31 December 2013 0,00 0,00 88.088.796,54 0,00 0,00 88.088.796,54

10,2 Balance of the liabilities on 31 December 2012 32.177.132,00 0,00 73.724.870,13 0,00 0,00 73.724.870,13

11 Adjusted expenditures (2. + 10.) 1.257.116.536,99 0,00 1.459.153.640,76 42.189.828,99 0,00 1.501.343.469,75

12 Cash inflows (1.) 1.161.800.821,01 0,00 1.243.526.719,73 41.051.612,74 0,00 1.284.578.332,47

13 Adjusted cash deficit (12‐11) ‐95.315.715,98 0,00 ‐215.626.921,03 ‐1.138.216,25 0,00 ‐216.765.137,28

14 Sources of financing deficit (15.+16.+17.+18.+19.) 95.315.715,98 0,00 215.626.921,03 1.138.216,25 0,00 216.765.137,28

15 Net borrowing 119.492.847,99 0,00 175.275.623,07 1.045.028,62 0,00 176.320.651,69

16 Sale of property 8.000.000,00 0,00 11.948.846,35 11.636,77 0,00 11.960.483,12

17 Grants 0,00 0,00 0,00 0,00 0,00

18 Liabilities to suppliers ‐32.177.132,00 0,00 14.363.926,41 0,00 0,00 14.363.926,41

19 Net changes in cash ‐0,01 0,00 14.038.525,20 81.550,86 0,00 14.120.076,06

1

Adjusted deficit for 2013

DescriptionFinal Statement of Accounts Adjustments of execution

Balance

Overall level of public spending was increased the amount of expressed adjustments ‐ 41,051,612.74€, while on the side of expenditures the expressed level of adjustments amounts to 41,193,362.48 €. Minimum deficit adjustment on this basis is not substantially important when it comes to the expressed level of deficit. The level of public spending was thus increased from 1,444,789,714.35 € to 1,485,883,076.83 €. In the spending units the increase in spending was made in the following amounts:

Table 13 ‐ Increase in the Budget Spending Descrip

tion

Cash

inflo

ws

Cash

paym

ents

Cash

deficit/su

rplus

Sources o

f cash deficit fin

ancin

g

Domestic fin

ancin

g sources w

ithout

dep

osit

Net cred

it borro

wings

Sale of p

roperty

Net ch

anges in

cash

Public institutions within the Ministry of Culture 1,201,704.74 1,218,178.88 ‐16,474.14 16,474.14 13,516.88 4,880.11 8,636.77 2,957.26

Public institutions within the Ministry of Culture 13,166,844.77 12,502,602.20 664,242.57 ‐664,242.57 0.00 0.00 0.00 ‐664,242.57

Public institutions within the Health Fund 14,151,129.00 14,743,419.00 ‐592,290.00 592,290.00 46,682.00 43,682.00 3,000.00 545,608.00

Police Academy 357,888.04 386,673.40 ‐28,785.36 28,785.36 0.00 0.00 0.00 28,785.36

Examination Centre 77,721.89 62,317.87 15,404.02 ‐15,404.02 0.00 0.00 0.00 ‐15,404.02

Montenegrin National Theatre 349,089.77 302,930.79 46,158.98 ‐46,158.98 0.00 0.00 0.00 ‐46,158.98

Royal Theatre Zetski dom 0.00 2,445.81 ‐2,445.81 2,445.81 0.00 0.00 0.00 2,445.81

National Tourism Organisation 317,533.00 311,367.00 6,166.00 ‐6,166.00 0.00 0.00 0.00 ‐6,166.00

Montenegrin Academy of Arts and Sciences 62,417.93 296,143.93 ‐233,726.00 233,726.00 0.00 0.00 0.00 233,726.00

Veterinary clinics 208,588.87 208,588.87 0.00 0.00 0.00 0.00 0.00 0.00

Radio and Television of Montenegro 7,198,499.13 7,198,499.13 0.00 0.00 0.00 0.00 0.00 0.00

Public Institution "Coastal Management Zone" 3,655,648.96 3,655,648.96 0.00 0.00 0.00 0.00 0.00 0.00

Union of municipalities 304,546.64 304,546.64 0.00 0.00 0.00 0.00 0.00 0.00

TOTAL 41,051,612.74 41,193,362.48 ‐141,749.74 141,749.74 60,198.88 48,562.11 11,636.77 81,550.86

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

20

Article 42 of the Law on the Budget and Fiscal Responsibility (Official Gazette of Montenegro, no. 20/14) stipulates that all the public institutions that generate revenues by performing their own activities that are not included into the consolidated account of the treasury can use such revenues for financing current and capital expenditures, provided that they obtain the consent of the Ministry of Finance to their revenue and expenditure plan for the fiscal year and that they obtain in advance the notification of the state administration body in charge of supervision providing its consent. This Article stipulates the exemption from performing the financing transactions through the General Ledger of the State Treasury and including of these transactions into the annual budget law. The supervisory function that is to be implemented consistently in the next fiscal period is clearly and precisely defined. It is recommended that in the process of planning the budget through the annual budget laws the Government of Montenegro plans the amounts of the revenues generated through own activities of the spending units and that the revenues thus generated are used in compliance with the constraints defined in the annual budget law.

2.5. Statement on the manner of spending funds submitted after the expiry of a fiscal year Using the Statement on the manner of spending funds submitted upon the expiry of a fiscal year, on 31 December 2013, spending units reported the existence of funds in foreign currency accounts they had that were recorded in the General Ledger of the State Treasury as expenditure in 2013. The amount reported in this way was 1,102,617.08 €. On 31 January 2014 one spending unit reported the existence of funds in its accounts in the amount of 6,452.89 €. According to the submitted Statement on the manner of spending funds submitted upon the expiry of a fiscal year, the Ministry of Finance adopted the decision ordering the State Treasury to cancel the expenditures and to record the increase of the deposit of the Ministry of Finance.

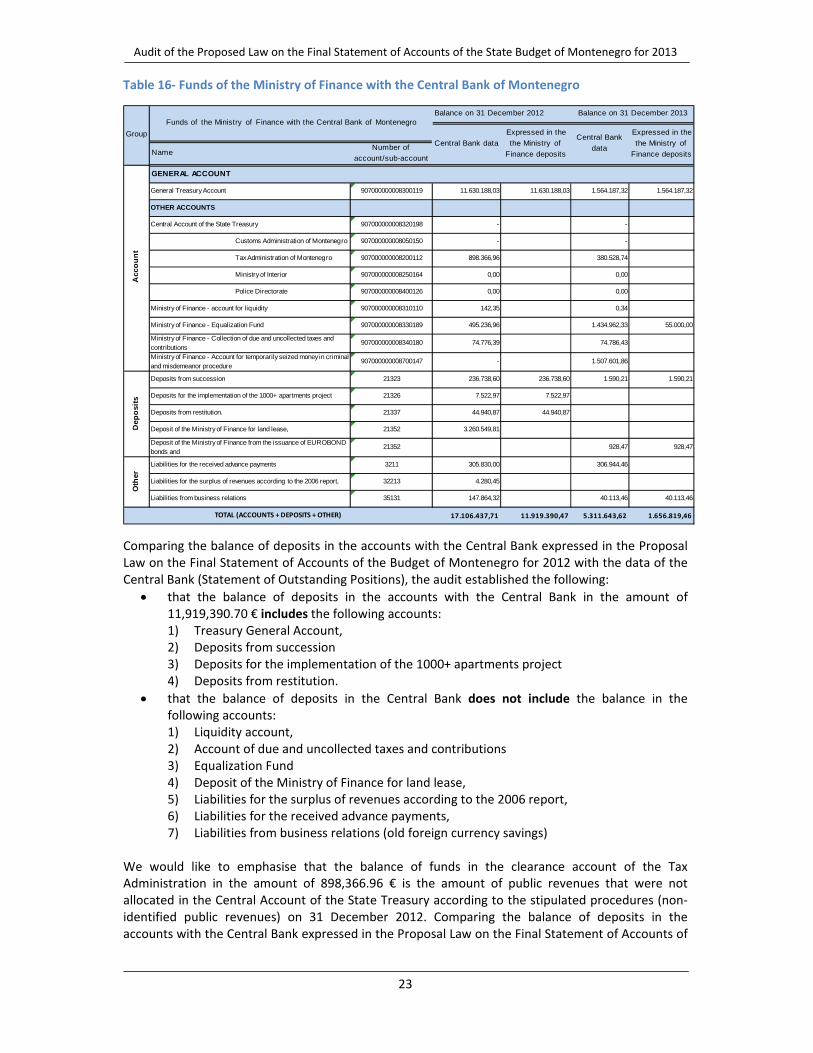

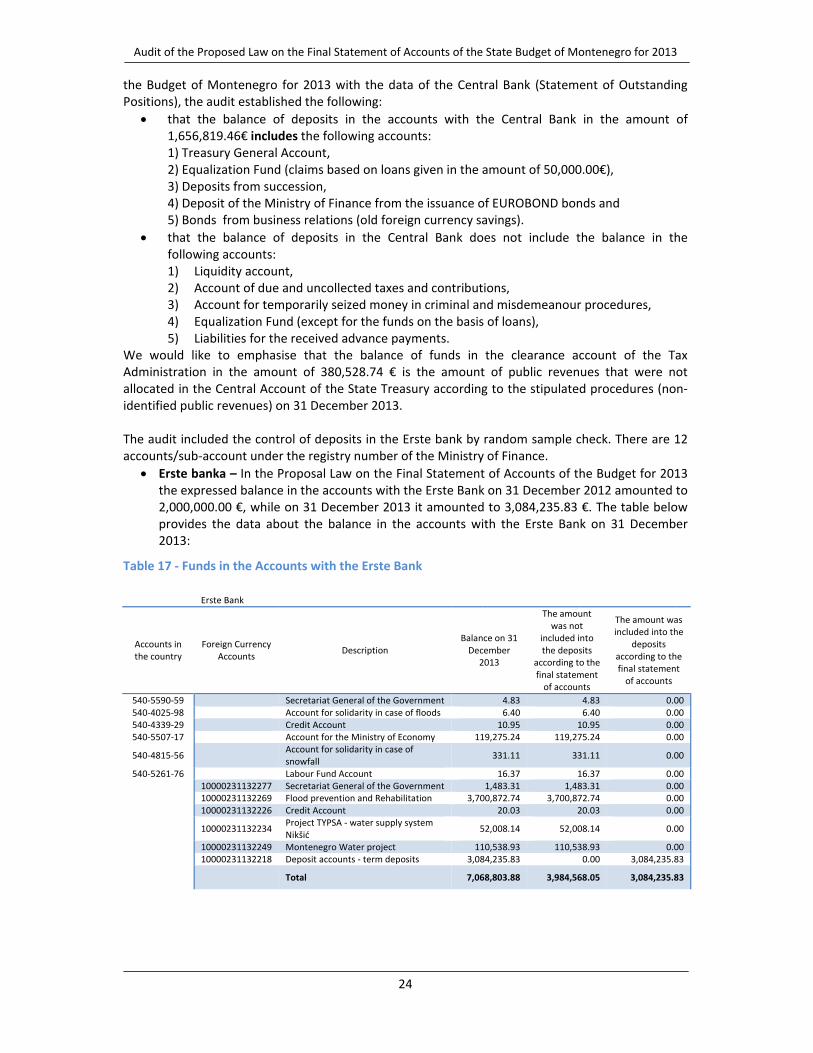

2.6. Report on the manner of spending funds from the current budgetary reserve According to the Rulebook on the Manner of Drafting, Compiling and Filing Financial Statements of the Budget, State Funds and Local Self‐Government Units, spending units are obliged to enclose to the annual financial statements the Report on the manner of spending funds from the current budgetary reserve ‐ Form 9. The available documentation shows that 79 spending units submitted the Report on the manner of spending funds from the current budgetary reserve, 10 of which submitted the Form 9 after the deadline expired. The submitted reports show that the funds from the current budget reserve were used by ten spending units in the total amount of 9,352,520.96 €, which matches the amounts recorded as the current budgetary reserve in the General Ledger of the State Treasury. 3. STATE CASH DEPOSITS Bank account is the account for receiving, paying and transferring state money. State money is the money that is under control or at disposal of the state or municipalities. Consolidated treasury account comprises all the accounts where state money is recorded and that are in the function of the state or municipal budgets. Accounts in the Central Bank of Montenegro ‐ According to the Agreement on banking operations and services related to the implementation of the decisions on the state debt No. 01‐2385/1 of 25 September 2001, the Central Bank of Montenegro undertook to perform banking operations with the state money and to act upon the order of the minister to open bank accounts for the purpose of banking operations. The table below gives an overview of the accounts opened with the Central Bank with the balance on 31 December 2012 and 31 December 2013:

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

21

Table 14‐Accounts open with the Central Bank of Montenegro

ACCOUNTS OPEN WITH THE CENTRAL BANK

DESCRIPTION Account number Balance on 31 December 2012

Balance on 31 December 2013

Treasury General Account 907000000008300119 11,630,188.03 1,564,187.32 OTHER ACCOUNTS Central Account of the State Treasury 907000000008320198 ‐ ‐ Customs Administration of Montenegro 907000000008050150 ‐ ‐ Tax Administration of Montenegro 907000000008200112 898,366.96 380,528.74 Ministry of Interior 907000000008250164 ‐ ‐ Police Directorate 907000000008400126 ‐ ‐ Ministry of Finance ‐ account for liquidity 907000000008310110 142.35 0.34 Ministry of Finance ‐ Equalization Fund 907000000008330189 495,236.96 1,434,962.33 Ministry of Finance ‐ Collection of due and uncollected taxes and contributions

907000000008340180 74,776.39 74,786.43

Ministry of Finance ‐ Account for temporarily seized money in criminal and misdemeanour procedures

907000000008700147 ‐ 1,507,601.86

Treasury General Account ‐ According to the Directions on State Treasury Operations, item

45‐ the Ministry of Finance issues an order for opening of the main bank account of the state. Out of the funds planned in the annual budget money is paid to and withdrawn from this account. According to the data of the Central Bank on the public revenues collected and allocated through the Treasury General Account, No 907‐83001‐19, for the period from 01 January 2013 to 31 December 2013, the total amount of the funds paid into the account amounted to 1,608,343,215.83 €, while the total amount of the funds paid from the account amounted to 1,618,409,216.54 €. On 31 December 2012 the funds in the account amounted to 11,630,188.03 €, while on 31 December 2013 they amounted to 1,564,187.32 €, as presented in the table above.

Central Account of the State Treasury – According to the Order on the Manner of Payment of Public Revenues, Section ‐ General Provisions (item 5 and item 7), the funds are collected through the Central Account of the State Treasury and they are distributed therefrom. The accounts used for collection of public revenues (416 accounts according to the Order) and the four clearing accounts, through which the funds are transferred to the Central Account of the State Treasury by the spending units that collect public revenues ‐ Customs Administration, Tax Administration, Ministry of Interior and Police Directorate. According to the Central Bank data, the public revenues collected to this account for the period from 1 January 2013 to 31 December 2013 amounted to 1,345,882,236.48 €. The same amount was allocated in the observed period.

Liquidity account – According to Article 7 of the Contract on performing banking operations and services related to the implementation of the decisions on the state debt No. 01‐2385 of 25 September 2001, it was established that the minister is obliged to open a special bank account in the Central Bank that will be used only for the payments of the funds from the sale of treasury bills issued by the Government with a view to improving budget liquidity. According to the data of the Central Bank for the period from 1 January 2013 to 31 December 2013, public revenues collected in this account amounted to 75,246,194.22 €, while the distributed public revenues amounted to 75,246,336.23 €. On 31 December 2012 the balance in this account was 142.35€ and on 31 December 2013 it was 0.34 €.

Account for collection of due and uncollected taxes and contributions – According to Article 9 of the Order on the collection of due and uncollected taxes and contributions and other pubic revenues8, the account was opened for the purpose of collecting the due and uncollected revenues from taxes, contributions for compulsory social insurance and other public revenues, except for the Value Added Tax, incurred before 31 December 2003.

8 OG MNE No. 24/04

Audit of the Proposed Law on the Final Statement of Accounts of the State Budget of Montenegro for 2013

22

According to the data of the Central Bank for the period from 1 January 2013 to 31 December 2013, public revenues collected in this account amounted to 10.04 € and there were no allocated public revenues. Hence, the balance on 31 December 2012 amounted to 74,776.39 € and it amounted to 74,786.43 € on 31 December 2013.

Account Equalization Fund – The account Equalization Fund is managed by the Ministry of Finance. According to Article 29 of the Law on Financing Local Self‐Government, this account is used for financial equalization in the financing of municipalities. According to the Central Bank data, in the period from 1 January 2013 to 31 December 2013 the amount of 26,462,823.37 € of public revenues were paid in the account Equalization Fund number 907‐83301‐89. In the same period the amount of allocated funds was 25,523,098.00 €. On 31 December 2012 the balance was 495,236.96 €, while it was 1,343,962.33 € on 31 December 2013.